Aquaponics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

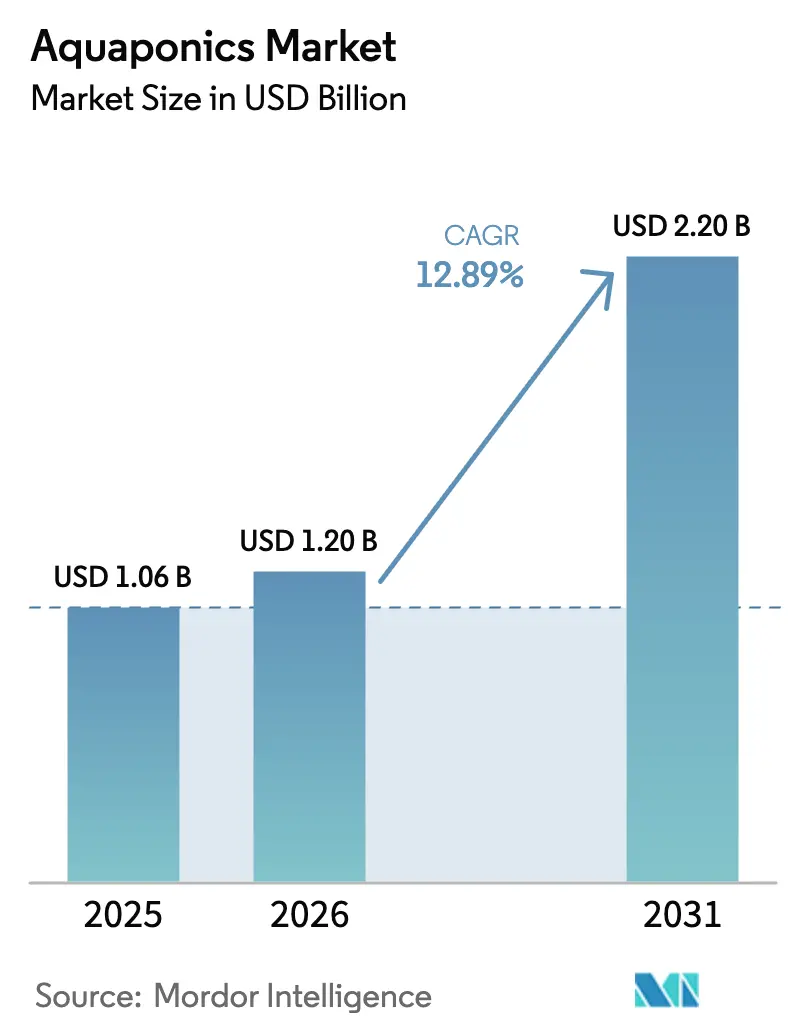

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 2.20 Billion |

| Growth Rate (2026 - 2031) | 12.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aquaponics Market Analysis by Mordor Intelligence

The aquaponics market size was valued at USD 1.06 billion in 2025 and estimated to grow from USD 1.20 billion in 2026 to reach USD 2.20 billion by 2031, at a CAGR of 12.89% during the forecast period (2026-2031). Scaling from experimental greenhouses to climate-controlled commercial hubs, the aquaponics market now supplies grocers, restaurants, and direct-to-consumer channels with synchronized harvests of fresh protein and produce. Demand is strongest in metropolitan regions that value pesticide-free greens, shorter supply chains, and year-round availability, while technology infusions, such as artificial intelligence-guided feeding, Internet of Things (IoT) sensors, and automated climate controls, continue to compress labor inputs and reduce mortality events. Rising water scarcity, circular-economy mandates, and government incentives are expanding the addressable market for aquaponic projects, prompting operators to shift their crop portfolios toward premium herbs and adopt modular designs that reduce upfront capital costs. Competitive intensity remains moderate because no single operator controls sufficient capacity to dictate pricing, yet first movers are consolidating regional footholds through vertical integration across hatchery genetics, proprietary feeds, and direct distribution.

Key Report Takeaways

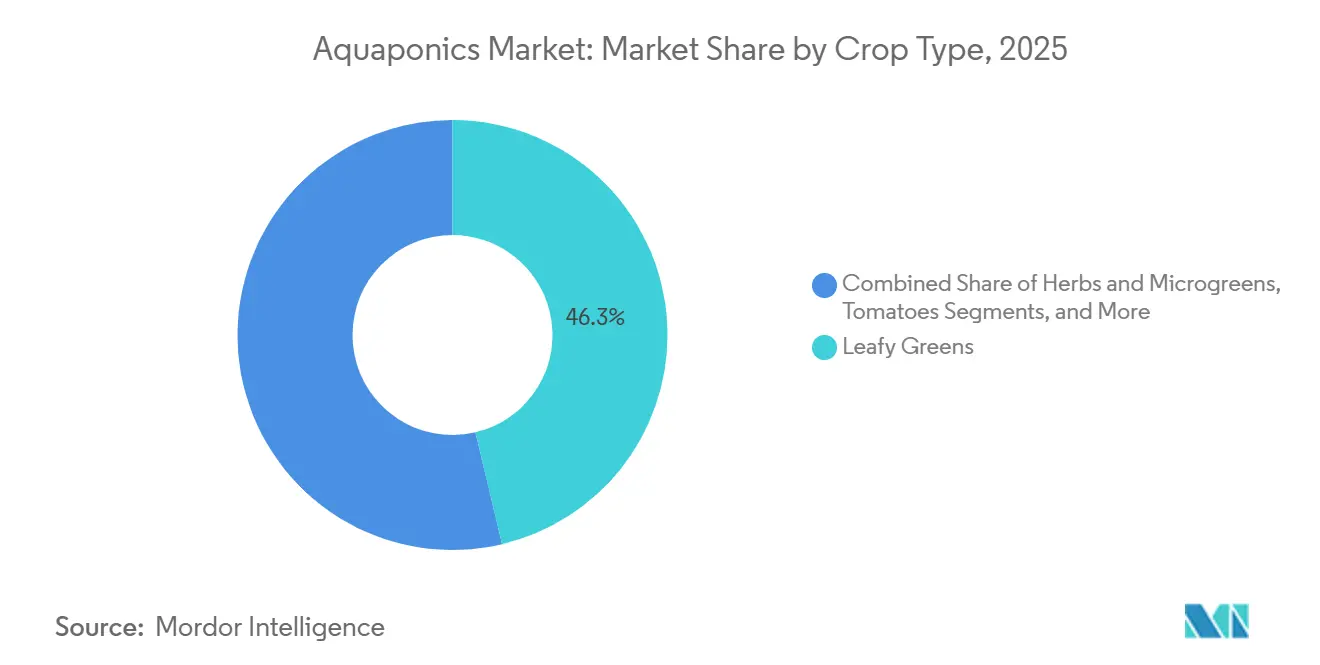

- By crop type, leafy greens accounted for 46.3% of the aquaponics market size in 2025, whereas herbs and microgreens are anticipated to expand at a 13.7% CAGR through 2031.

- By fish species, tilapia commanded 38.7% of revenue in 2025, while catfish is advancing at a 13.4% CAGR through 2031.

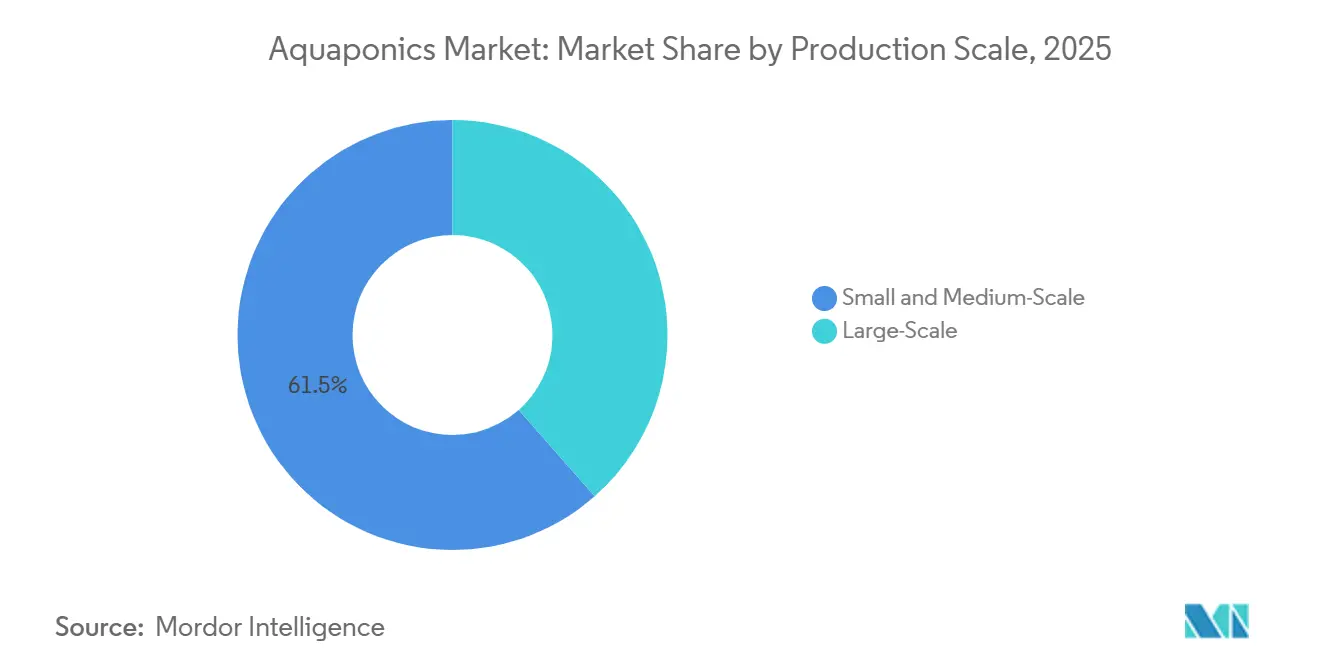

- By production scale, small and medium-scale systems accounted for 61.5% of revenue in 2025 and are projected to grow at 13.3% through 2031.

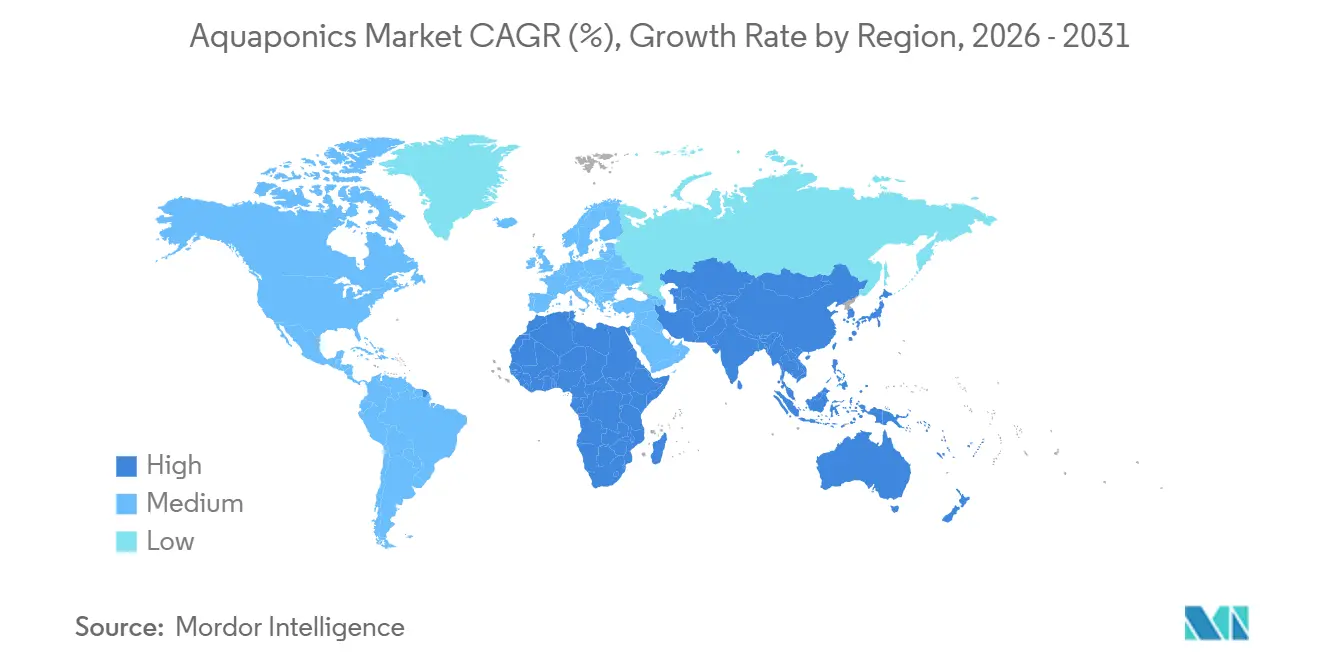

- By geography, North America led the aquaponics market with a 34.2% share in 2025, while the Asia-Pacific region is projected to be the fastest-growing at a 13.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aquaponics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for locally sourced pesticide-free produce | +2.8% | Global with strongest uptake in North America, Europe, and urban Asia-Pacific hubs | Medium term (2-4 years) |

| Adoption of circular-economy water-conservation practices | +2.3% | Middle East, North Africa, and water-stressed areas in Asia-Pacific | Long term (≥4 years) |

| Integration with vertical farming for urban food security | +2.1% | Singapore, China, Japan, and selected Middle Eastern and North American cities | Medium term (2-4 years) |

| Commercialization of high-value medicinal herbs | +1.6% | North America, Europe, and Asia-Pacific pharmaceutical and nutraceutical clusters | Long term (≥4 years) |

| Government incentives for sustainable agriculture | +2.0% | North America, Europe, Asia-Pacific, emerging Middle East and Africa | Short term (≤2 years) |

| Advances in controlled-environment monitoring | +2.4% | North America and Europe, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Locally Sourced Pesticide-Free Produce

Urban shoppers are increasingly demanding traceable vegetables harvested within 24 hours, and aquaponics eliminates the need for synthetic pesticides because fish cannot tolerate chemical residues in recirculating water. Superior Fresh LLC shuttered its hydroponic lettuce production in Indiana in 2024 to concentrate capital on its integrated Wisconsin complex, signaling that dual protein-and-produce models generate superior margins[1]Source: Jane Smith, “Superior Fresh Closes Indiana Facility,” Hatchery International, hatcheryinternational.com. Retail premiums of 20.0-30.0% encourage operators to bypass wholesale channels through farmers’ markets and subscription deliveries, stabilizing cash cycles during peak demand seasons.

Adoption of Circular-Economy Water-Conservation Practices

Aquaponics recycles approximately 90.0% of the system's water, aligning perfectly with European Union circular economy directives and drought mitigation strategies in the Middle East. Singapore’s Agri-Food and Veterinary Authority has earmarked SGD 309 million (USD 229.3 million) to support low-water agrifood research through 2025[2]Source: Singapore Food Agency, “Singapore Aquaculture Plan 2024,” sfa.gov.sg. The LIFE-LEMNERGY project in the European Union, currently running in the 2021-2027 phase, has achieved nitrogen removal above 85.0% by integrating duckweed nutrient recovery, cutting discharge, and generating biogas that offsets climate-control energy costs[3]Source: European Commission, “LIFE-LEMNERGY Project Results,” cordis.europa.eu.

Integration with Vertical Farming for Urban Food Security

Stacking aquaponic grow beds inside multistory buildings multiplies production per square meter, which is essential for land-constrained megacities. Singapore’s “30 by 30” blueprint seeks to meet 30.0% of nutritional demand locally by 2030, and the 2024 Singapore Aquaculture Plan reserved coastal and rooftop sites for dense fish-and-vegetable hubs. BIGH’s 4,000-square-meter rooftop farm in Brussels produces 35 metric tons of vegetables and 4 metric tons of fish annually, reaching retailers within two hours. Comparable pilots in Japan retrofit disused warehouses to improve access for aging rural populations that lack grocery options.

Commercialization of High-Value Medicinal Herbs

Herbs such as basil, mint, cilantro, and parsley already generate wholesale prices two to three times higher than lettuce, yet growers are pursuing ginseng, kratom, and cannabis for pharmaceutical and nutraceutical supply chains that demand contaminant-free inputs. These botanicals reach maturity in just three to six weeks, permitting rapid inventory turns and gross margins above 60.0%. Asia-Pacific’s traditional medicine sector is a critical off-take channel, while North American and European buyers emphasize traceability for regulated extracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital and operational complexity | -2.1% | Global, most acute in emerging markets with limited project finance | Short term (≤2 years) |

| Zoonotic pathogen management risks | -1.3% | North America and Europe, where food-safety scrutiny is highest | Medium term (2-4 years) |

| Limited availability of skilled labor | -1.5% | Global, especially in rural zones and developing economies | Medium term (2-4 years) |

| Fragmented regulatory standards across markets | -1.4% | North America, Europe, Asia-Pacific, and Middle East with divergent rules | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital and Operational Complexity

Commercial installations cost USD 500-1,000 per square meter, exceeding hydroponic equivalents by up to 50.0%, because integrated systems must harmonize fish tanks, biofilters, and climate management systems. Energy accounts for as much as 40.0% of operating budgets in temperate zones, and power outages can cause catastrophic fish mortality if backup generators fail. Payback often stretches beyond five years, a horizon that traditional agricultural lenders and venture capital find unattractive.

Zoonotic Pathogen Management Risks

Salmonella, Listeria, and Escherichia coli can migrate through shared water and contaminate produce if biosecurity measures are not followed. The United States Food and Drug Administration's Produce Safety Rule requirements, along with European Union microbial criteria, compel operators to adopt ultraviolet sterilization, ozone injection, and rigorous testing protocols, thereby inflating costs without generating additional revenue. Ambiguity in official guidance leaves smaller farms exposed to inconsistent audit interpretations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Herbs and Microgreens Expand Margins Faster Than Leafy Greens

Leafy greens captured 46.3% of revenue in 2025, while herbs and microgreens are advancing at a 13.7% CAGR through 2031. Herbs mature in three to six weeks, versus eight to ten weeks for head lettuce, enabling faster cash rotation. Wholesale prices for basil, mint, and cilantro are two to three times higher than those for lettuce, reflecting the higher energy costs associated with climate-controlled environments. Tomatoes, cucumbers, and berries remain niche because they require precise calcium-to-magnesium balancing and pollination services, which increase labor inputs. Medicinal botanicals, including ginseng and kratom, require licensing and third-party potency assays, yet their margins can exceed 60.0% when supply contracts with pharmaceutical buyers are secured.

Additional expansion into strawberries, peppers, and Asian specialty vegetables is unfolding in the Asia-Pacific region, where rising disposable income underpins the willingness to pay for novelty and safety certifications. The International Organization for Standardization 22000 framework is increasingly stipulated in export contracts to Europe and Japan. Operators with diversified crop portfolios hedge against market volatility, but they must manage species-specific nutrient uptakes to avert deficiencies that can ripple through the integrated system.

By Fish Species: Catfish Challenges Tilapia’s Lead

Tilapia held a 38.7% of the aquaponics market share in 2025, owing to robust tolerance for pH swings and variable temperatures.

Infinity Blue Barramundi LLC (MainStream Aquaculture Group) positions barramundi as a premium alternative, emphasizing its high omega-3 content and white, flaky flesh, which is ideal for upscale restaurants.

By Production Scale: Modular Systems Democratize Entry

Small and medium-scale systems account for 61.5% of the aquaponics market size in 2025 and are projected to expand at a 13.3% CAGR through 2031, underscoring how modular kits lower barriers for urban entrepreneurs.

Large-scale systems above 50,000 square feet can require more than USD 5 million in capital but capture volume contracts with supermarket chains and institutional buyers. Superior Fresh LLC aggregates Atlantic salmon and leafy greens on its Wisconsin site, while Springworks Farm Maine, Inc.'s 500,000-square-foot complex targets hospitals and universities.

Geography Analysis

North America led the aquaponics market in 2025, with a 34.2% revenue share, as consumers paid premiums for pesticide-free produce and state grants offset capital expenses for controlled-environment facilities. Activity concentrates in Wisconsin, California, and the Mid-Atlantic, where urban density keeps the distribution radius short. Canada’s Agricultural Clean Technology Program subsidizes retrofits in British Columbia and Ontario, regions that are particularly affected by high heating costs during the winter[4]Source: Government of Canada, “Agricultural Clean Technology Program,” canada.ca. Regulatory clarity is an advantage because the United States Department of Agriculture (USDA) allows organic labeling for aquaponic outputs, simplifying marketing and price positioning.

The Asia-Pacific region is the fastest-growing zone, with a 13.1% CAGR projected to 2031, as megacities face land scarcity and increasing food security mandates. China repurposes idle warehouses for integrated fish and plant hubs, while Japan funds community resilience pilots in rural prefectures. India’s clusters in Bangalore and Mumbai respond to food-safety concerns among middle-class consumers, and Australia promotes barramundi to differentiate from tilapia-heavy imports. South Korea is exploring rooftop systems in Seoul and Busan, although its urban agriculture policy is still in formation.

Europe’s investment trajectory aligns with the circular economy directives. Belgium’s BIGH rooftop farm proves that harvest-to-shelf times under two hours can be profitable. The United Kingdom’s Flo-Gro shrimp configuration widens species options, but inconsistent organic certification and elevated energy tariffs challenge Southern European operators. The Middle East and Africa utilize aquaponics to conserve scarce freshwater resources. The United Arab Emirates and Saudi Arabia blend desalination with solar power to reduce operating costs. South Africa pilots off-grid aquaponics in Cape Town and Johannesburg, while Brazil and Argentina nurture early-stage deployments in São Paulo and Buenos Aires, tempered by limited project finance and regulatory uncertainty.

Competitive Landscape

The aquaponics market remains highly fragmented in 2025, with key players including Superior Fresh LLC, ECF Farmsystems GmbH, Infinity Blue Barramundi LLC (MainStream Aquaculture Group), BIGH, and Springworks Farm Maine, Inc. This distribution renders the aquaponics market moderately concentrated because no single entity can dictate commodity pricing. Leaders pursue vertical integration that spans hatchery genetics, proprietary feeds, and direct distribution, thereby compressing supply-chain margins while securing volume commitments from grocery chains and institutional buyers.

Technology adoption differentiates players. Edge-connected sensor arrays and artificial intelligence analytics boost labor productivity by 20.0-30.0% and reduce fish mortality by flagging dissolved-oxygen drops in real-time. Springworks Farm Maine, Inc.'s predictive feeding software fine-tunes rations to ambient temperature fluctuations, resulting in lower feed conversion ratios and reduced waste. Intellectual property filings related to biofilter media and modular racking systems suggest an escalating competition to drive energy efficiency and simplify operating complexity.

Regions such as sub-Saharan Africa, Southeast Asia outside Singapore, and South America represent expansion corridors. However, scarce project finance and patchwork regulations limit rapid capacity additions. Smaller contenders chip away at incumbents by targeting hyperlocal delivery models and farmers’ markets that reward freshness and community branding. The absence of harmonized organic standards across jurisdictions fragments brand strategy and forces the development of tailored compliance roadmaps for each export market.

Aquaponics Industry Leaders

ECF Farmsystems GmbH

BIGH

Infinity Blue Barramundi LCC (MainStream Aquaculture Group)

Superior Fresh LLC

Springworks Farm Maine, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Aquaponics Association has partnered with Indoor Ag-Con to organize a specialized industry workshop, scheduled for February 2026, in Las Vegas, United States. The workshop aims to enhance commercial production practices, improve system scalability, and facilitate integration into controlled environment agriculture and supply chains.

- September 2025: Innovasea Systems Inc. partnered with the Andrew J. Young Foundation to jointly develop two fully recirculating aquaponics facilities in the United States (Colorado and Georgia) with integrated fish and vegetable production. Innovasea Systems Inc. supplies Recirculating Aquaculture System (RAS) technology, system design support, and operations scalability, targeting sustainable local food production and reduced freshwater use.

- July 2025: The state of Assam, India, inaugurated the "Aqua Tech Park" in Sonapur, a collaborative hub for water technology. This facility focuses on research and the practical application of advanced water-efficient systems, including aquaponics. The initiative seeks to develop integrated food production solutions and strengthen regional agri-aqua innovation capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aquaponics market as all revenue generated from purpose-built, closed-loop systems in which nutrient-rich finfish effluent is biologically converted and circulated to hydroponic grow beds, with produce and fish sold at ex-facility prices. We cover equipment, sensors, software, inputs, and the sale of vegetables, herbs, micro-greens, and fish across commercial, community, educational, and hobby scales.

Scope exclusion: Open ponds or soil farms that merely repurpose fish tank water without continuous recirculation are outside our numbers.

Segmentation Overview

- By Crop Type

- Leafy Greens

- Herbs and Microgreens

- Tomatoes

- Cucumbers

- Berries

- Other Crops

- By Fish Species

- Tilapia

- Catfish

- Trout

- Other Fish

- By Production Scale

- Large-Scale

- Small and Medium-Scale

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- Netherlands

- France

- United Kingdom

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next interviewed system integrators, commercial growers, extension officers, and equipment distributors spanning North America, Europe, Asia-Pacific, and the Gulf. These dialogues helped us validate capital cost curves, stocking densities, energy intensity, and the produce price premiums suggested by desk research.

Desk Research

We pulled foundational data from FAO Fisheries Statistics, USDA NASS Greenhouse Census, Eurostat aquaculture output, UN FAOSTAT crop yield series, and policy trackers from the European Commission and Japan MAFF. Peer-reviewed articles on nutrient conversion hosted on Springer and ScienceDirect gave biological ratios, while press releases captured new capacity announcements. Paid resources, including D&B Hoovers and Dow Jones Factiva, supplied company financials and project timelines. The sources highlighted are illustrative; many additional publications were reviewed for cross-checks and clarity.

Market-Sizing & Forecasting

A top-down build begins with regional fish harvest and protected-crop output, followed by a recirculation penetration factor and average system footprint. Selective bottom-up checks, supplier revenue roll-ups, and sample ASP × volume probes fine-tune totals. Key variables include water-use savings, feed conversion ratios, crop cycle times, average retail mark-ups, grant disbursement pipelines, and electricity tariffs, all updated annually. Multivariate regression, supported by expert consensus on variable trajectories, projects demand through 2030.

Data Validation & Update Cycle

Each model pass runs through anomaly screens, variance thresholds, and a two-level analyst review; any outlier triggers a recall to respondents for clarification. Reports refresh every twelve months, with interim updates when major regulatory or technological shifts occur, and a final sense check just before release.

Why Mordor's Aquaponics Baseline Commands Confidence

Published estimates often diverge because firms select different system scopes, price definitions, and refresh cadences. Our disciplined variable selection, annual revision schedule, and multi-region primary validation keep findings tightly aligned with on-ground reality.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.42 B | Mordor Intelligence | |

| USD 1.20 B | Global Consultancy A | Excludes SaaS monitoring fees; uses 2023 currency parity |

| USD 1.57 B | Industry Journal B | Assumes universal 12 % ASP uplift; limited primary checks |

The comparison shows that, by matching scope to fully closed-loop systems and triangulating prices with growers in multiple regions, Mordor delivers an equitable, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the 2026 valuation of the aquaponics market and its projected 2031 size?

The aquaponics market size stood at USD 1.2 billion in 2026 and is anticipated to reach USD 2.2 billion by 2031.

Which crop type is expanding fastest in commercial aquaponics facilities?

Herbs and microgreens are growing at a 13.7% CAGR to 2031 because their short cycles and premium prices boost margins.

Why is Asia-Pacific the fastest-growing region for aquaponics?

Land scarcity, food-security mandates, and sizable government grants drive Asia-Pacific’s 13.1% CAGR through 2031.

What limits rapid expansion of large-scale aquaponic farms?

Capital costs of USD 500-1,000 per square meter and the need for skilled labor delay payback periods beyond five years.

How do sensors and artificial intelligence improve aquaponic operations?

Real-time monitoring and predictive analytics cut labor needs by up to 30.0% and reduce fish mortality through early intervention.

Page last updated on: