Cattle Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 79.41 Billion |

| Market Size (2031) | USD 98.23 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

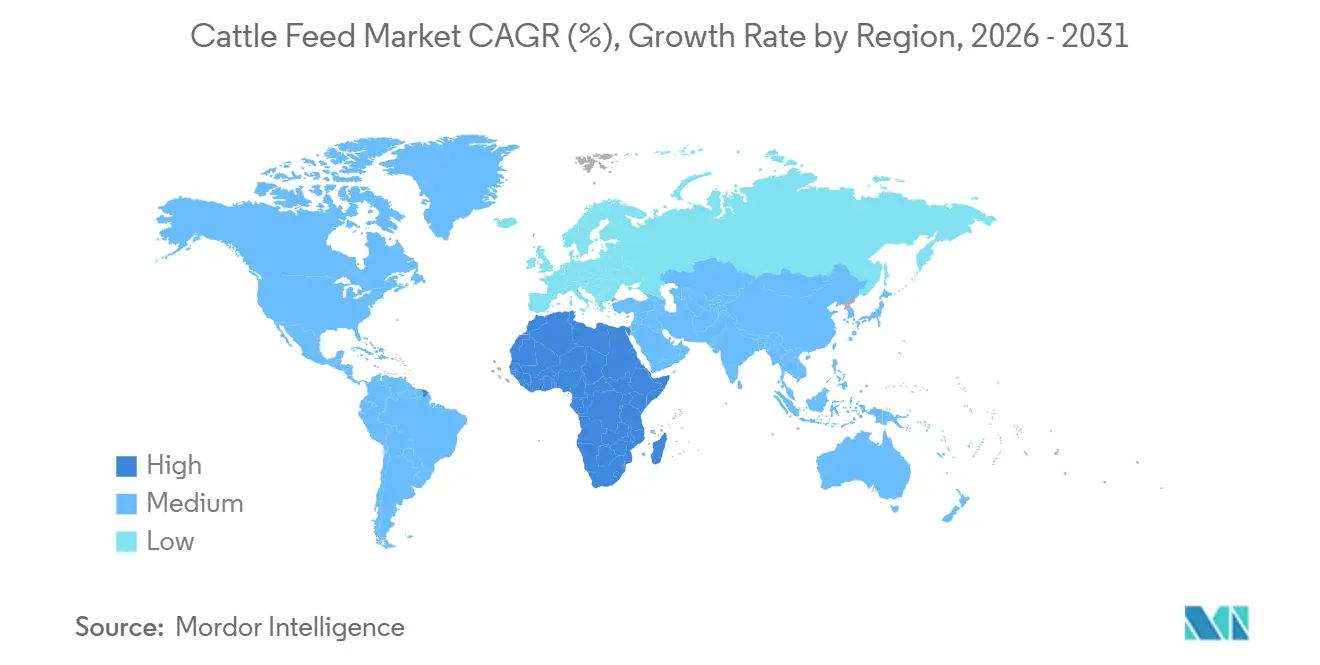

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

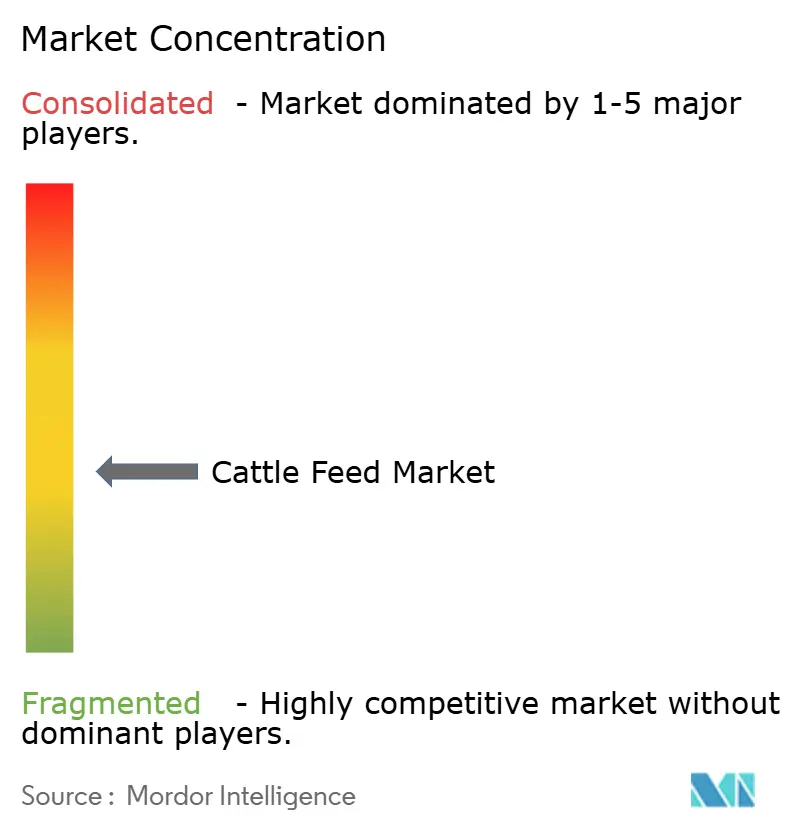

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cattle Feed Market Analysis by Mordor Intelligence

The cattle feed market size, estimated at USD 76.20 billion in 2025, is set to increase to USD 79.41 billion in 2026 and further climb to USD 98.23 billion by 2031, growing at a CAGR of 4.35% during the forecast period (2026–2031). Structural demand stems from sovereign protein-security mandates that are diverting grains toward domestic mills, paired with rapid feedlot intensification in South America, where high-energy rations now outcompete new-pasture conversion. Ingredient profiles are evolving as phytogenic additives replace antimicrobials under United States and European Union regulations, while liquid feeding systems are gaining traction in automated dairies due to their ability to reduce dust loss and enable real-time nutrient adjustments. Asia Pacific retains the largest regional base for industrializing herds in China and India. Africa is set to record the quickest absolute growth, driven by credit-backed dairy cooperative programs that bundle fortified rations with veterinary services. Competitive intensity remains moderate, leaving room for regional specialists who supply organic or climate-resilient blends, even as multinational grain integrators leverage their origination networks to protect margins during volatile crop cycles.

Key Report Takeaways

- By animal type, dairy cattle held 53.2% of the 2025 cattle feed market size, while beef cattle are projected to expand at a 5.2% CAGR through 2031.

- By ingredient, cereals accounted for 49.3% of the cattle feed market share in 2025, and feed additives are poised to register a 5.4% CAGR from 2026 to 2031.

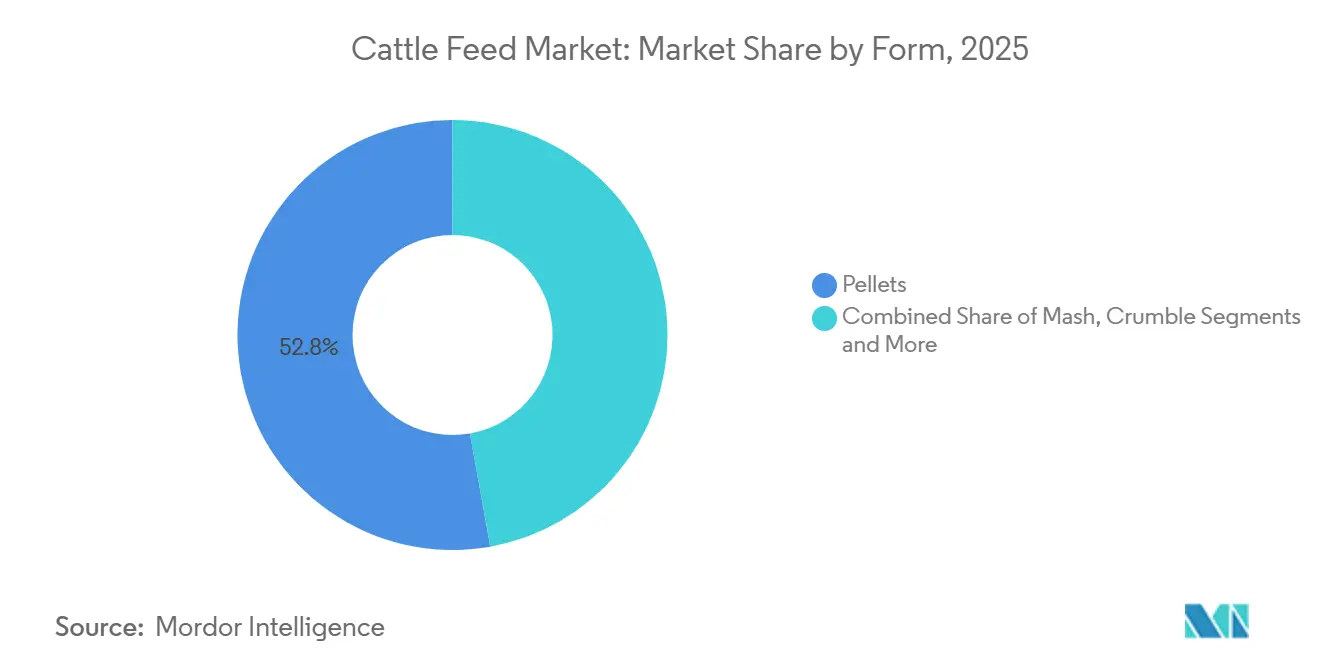

- By form, pellets led with 52.8% of 2025 revenue, whereas liquid feed is forecast to grow at 4.7% through 2031.

- By geography, the Asia Pacific captured 36.6% of the 2025 market value, yet Africa is projected to post a 5.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cattle Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives for feed fortification programs | +0.6% | Africa, South Asia, and Southeast Asia | Medium term (2 to 4 years) |

| Escalating demand for high-protein dairy and meat products | +0.9% | Global, with concentration in Asia Pacific and Middle East | Long term (≥ 4 years) |

| Rapid intensification of cattle farming in emerging economies | +0.8% | Africa, South America, and South Asia | Long term (≥ 4 years) |

| Commercialization of precision feeding technologies | +0.5% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Digital marketplaces simplifying feed procurement | +0.3% | Global, early adoption in North America, Europe, and China | Medium term (2 to 4 years) |

| Climate-resilient forage development boosting compound feed use | +0.4% | Sub-Saharan Africa, South Asia, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Feed Fortification Programs

Governments in Kenya, Ethiopia, and India have introduced mandates requiring minimum inclusion of trace minerals and vitamins in cattle feed. These policies reduce effective costs for farmers and accelerate the transition away from traditional on-farm mixes. Kenya’s subsidy program in 2024 covered 30% of the costs of fortified rations, which boosted compound feed demand by 120,000 metric tons in just nine months. India allocated INR 5 billion (USD 60.2 million) to build fortification infrastructure, with early adoption seen in Punjab and Haryana. The Food and Agriculture Organization's estimates suggest that compound feed penetration in Sub-Saharan Africa could reach 34% by 2028, creating strong opportunities for premix suppliers[1]Source: Food and Agriculture Organization “Livestock Systems Outlook 2024” fao.org.

Escalating Demand for High Protein Dairy and Meat Products

Rising incomes in countries such as China and Saudi Arabia are driving higher consumption of milk and beef. This trend is pushing farms to adopt rations with elevated protein levels to meet production targets. In 2024, China’s per-capita milk intake reached 42 kilograms, resulting in widespread adoption of diets with crude protein levels exceeding 18%. Saudi Arabia imported 1.2 million metric tons of compound feed to support its goal of achieving meat self-sufficiency[2]Source: Saudi Ministry of Environment Water and Agriculture “Vision 2030 Protein Targets” mewa.gov.sa. The demand has also fueled growth in liquid supplements containing rumen-protected fats, a segment now valued at USD 2.1 billion.

Rapid Intensification of Cattle Farming in Emerging Economies

Emerging economies are experiencing rapid consolidation of smallholder farms, which is increasing reliance on compound feed. Nigeria reported a 4.2% rise in cattle numbers in 2024, but compound feed usage grew by 11%, highlighting a shift toward confined feeding systems. Ethiopia projects that feedlots will account for 40% of beef output by 2030, requiring an additional 800,000 metric tons of feed annually. In Brazil, land prices have tripled since 2020, making feedlot finishing more attractive than expanding pastureland. These developments underscore the structural shift toward intensive cattle farming practices.

Commercialization of Precision Feeding Technologies

Advances in sensor technology are enabling farmers to tailor rations to individual animals. In 2024, 62% of robotic milking installations included automated feed modules, resulting in an 8% reduction in waste. Smart feeding platforms have demonstrated improvements in feed conversion efficiency, with early trials in the United States showing gains of 4.5%. The European Union’s Farm to Fork strategy now offers carbon credits to farms that adopt precision feeding systems. Together, these innovations are making precision feeding both economically and environmentally attractive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile grain prices impacting input costs | -0.7% | Global, acute in import-dependent Middle East and North Africa | Short term (≤ 2 years) |

| Shift toward plant-based diets in mature economies | -0.4% | North America and Western Europe | Long term (≥ 4 years) |

| Stringent antimicrobial regulations raising reformulation costs | -0.5% | European Union, United States, and Canada | Medium term (2 to 4 years) |

| Supply chain disruptions from extreme weather events | -0.6% | Global and concentrated in major grain exporting regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Grain Prices Impacting Input Costs

Grain price volatility continues to pose a challenge for feed manufacturers. Corn and soybean meal account for up to 75% of ration costs, leaving mills highly exposed to market swings. In 2024, Chicago corn prices fluctuated between USD 4.20 and USD 5.80 per bushel, compressing margins to below 3% in some quarters. Argentina’s drought reduced soybean exports by 22%, forcing buyers to pay premiums of USD 40 per metric ton from Brazil. Smaller mills without hedging tools face severe liquidity pressures during such periods.

Shift Toward Plant-Based Diets in Mature Economies

Consumer preferences in mature economies are shifting toward plant-based diets, reducing demand for cattle products. In 2024, beef intake in the United States decreased to 25.8 kilograms per capita from 26.4 kilograms per capita in 2023, while milk consumption in Germany declined by 1.8% during the same period[3]Source: United States Department of Agriculture Economic Research Service “Livestock and Meat Data 2024” ers.usda.gov. This trend reflects the rise of flexitarian lifestyles and growing interest in alternative proteins. Feed manufacturers are diversifying into the aquaculture and poultry segments to offset declining demand for cattle feed. However, the transition requires new formulations and client relationships, leaving some cattle-focused plants underutilized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Feedlot Economics Favor Beef Intensification

Dairy cattle continue to dominate the cattle feed market size, holding the largest share in 2025 at 53.2%. High-protein rations remain essential, but the rise of plant-based alternatives is putting pressure on processor margins. Large herds integrate bypass proteins and protected fats to sustain yields, while regulatory incentives under the Farm to Fork initiative encourage the adoption of low-emission feed technologies. Despite these advances, cost and palatability challenges still limit the widespread use of these technologies. Vertical integration by processors is also reshaping supply chains, diverting volumes from independent mills and consolidating control over feed formulations.

Beef cattle are positioned to expand more rapidly than dairy, advancing at a 5.2% CAGR through 2031. This reflects the cost competitiveness of feedlots compared to new pasture expansion in regions such as Brazil and Argentina, where land prices have increased significantly. Exporters are increasingly focused on marbling compliance to meet premium European Union quotas, further strengthening the outlook for beef finishing. Methane-reducing additives, though still at limited penetration, could become mainstream if carbon markets mature and incentives align with sustainability goals.

By Ingredient: Additives Outpace Commodities on Regulatory Tailwinds

Cereals retained the largest share in 2025 at 49.3%, serving as the primary energy source in the cattle feed market. Yield volatility and policy shocks are driving substitutable grains into rations, while precision micro-dosing of minerals and vitamins is becoming more common. South American crush capacity additions promise improved soybean meal availability, tempering price spikes. United States corn yield declines have led to a greater reliance on wheat and barley inclusion, despite lower metabolizable energy. These dynamics highlight the balance between commodity stability and innovation in functional feed ingredients.

Feed Additives are projected to be the fastest-growing ingredient category, rising at a 5.4% CAGR through 2031. Antimicrobial bans are prompting farms to shift toward phytogenics and enzymes, while investor confidence in functional ingredients remains strong. Cakes and meals remain principal protein carriers, but insect meal and single-cell proteins are gaining regulatory clearance, diversifying the protein base for ruminants. Specialty minerals and vitamins are benefiting from precision micro-dosing, a capability created by automated liquid systems that allow farms to fine-tune nutrient delivery, cow by cow.

By Form: Liquid Systems Gain Share in Automated Dairies

Pellets remain the dominant form, accounting for the largest cattle feed market share in 2025 at 52.8%. Their ease and widespread availability make them the preferred choice across commercial operations. Mash continues to serve rural smallholders but is slowly losing ground, while Crumble remains focused on calf starters. Texturized pellets are also gaining traction as a cost-effective alternative to traditional crumble formulations. The form segment illustrates how technology adoption and herd size influence feed choices, striking a balance between tradition and efficiency in modern cattle farming practices.

Liquid feed systems are anticipated to grow at a 4.7% CAGR during the forecast period (2026-2031), supported by robotic milking adoption and the need for precise nutrient delivery. These systems reduce labor and dust while enabling the supplementation of micro-nutrients that degrade during pelleting. Automated dairies have reported labor savings and improved component yields after switching to liquid feeding. Capital outlays for pumps and sensors show a favorable payback when herds exceed 150 cows, making liquid systems increasingly attractive for medium- and large-scale dairy operations.

Geography Analysis

Asia Pacific captured the largest 2025 share at 36.6%, driven by China’s industrialized dairies and India’s sizable herd. Large-scale Chinese farms housing over 1,000 head now produce the majority of the nation's milk, accelerating the adoption of compound feed. India’s cooperatives are investing in extension services and fortified rations, signaling significant upside potential in productivity. Regional demand is also supported by rising incomes and dietary shifts toward higher protein consumption, ensuring that the Asia Pacific region remains the anchor of global cattle feed demand in the years ahead.

Africa is forecast to grow at the fastest pace, advancing at a 5.5% CAGR through 2031. Subsidized credit programs and fortified ration mandates are driving the adoption of compound feed across dairy cooperatives. Food and Agriculture Organization estimates indicate that compound feed penetration could increase substantially by 2028, creating significant opportunities for premix suppliers. Nigeria’s herd expansion and donor-backed feed mills are reshaping supply chains, while South Africa’s advanced feedlots face infrastructure challenges. Africa’s growth trajectory reflects both structural demand and policy-driven modernization of livestock systems.

North America has faced herd contractions due to drought-driven cow liquidations, while Europe contends with flexitarian diets and herd caps. South America is split between Brazil’s expanding feedlot sector and Argentina’s slowdown under tax pressures. The Middle East remains heavily reliant on imports, with countries constrained by water scarcity. These regions exhibit mixed dynamics, with some experiencing intensification of scaling, while others face structural headwinds. Together, they highlight the uneven pace of cattle feed adoption globally, with Asia‑Pacific and Africa emerging as the clear growth leaders.

Competitive Landscape

The cattle feed market remains moderately fragmented, with regional taste differences and high capital requirements shaping competition. Global integrators leverage origination networks to secure inputs, while processor-run captive mills reduce reliance on third-party suppliers. White-space niches such as precision software and methane reduction additives are attracting venture funding, signaling innovation-driven opportunities. This balance between scale and specialization defines the competitive outlook, with both multinationals and regional players carving distinct positions in the evolving feed ecosystem.

Regional specialists defend market share through tailored formulations and certifications. Organic and non-GMO rations earn premiums but require segregated supply chains that multinationals cannot always justify. This dynamic creates space for smaller players to thrive in specialized segments. Their agility enables them to respond quickly to consumer preferences and sustainability demands, whereas larger firms tend to focus on efficiency and global sourcing. The coexistence of these strategies underscores the diversity of approaches shaping the cattle feed industry’s competitive landscape.

Moderate consolidation is projected as antimicrobial rules, volatile grain markets, and sustainability audits expand compliance costs. Better-capitalized firms are positioned to absorb these pressures, while startups continue to innovate in functional additives and digital solutions. The balance of global scale and regional specialization will define the competitive trajectory of the sector. Over time, consolidation may strengthen resilience, but innovation from smaller firms will remain critical to addressing emerging challenges in cattle feed production and sustainability.

Cattle Feed Industry Leaders

Cargill Incorporated

Archer Daniels Midland Company

Nutreco N.V. (SHV Holdings N.V.)

Charoen Pokphand Foods Group

Land O’Lakes Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Marks & Spencer has launched a novel feed supplement aimed at pasture-grazed dairy cows to reduce the carbon footprint of the retailer's fresh milk in the United Kingdom. This innovative feed additive, derived from corn fermentation and mineral salts, inhibits the formation of methane by digestive enzymes and is naturally metabolized in the cows' stomachs.

- January 2024: DSM, the leading innovator in nutrition, health, and beauty, received market authorization for Bovaer in Canada for use with dairy and beef cattle feed. This feed ingredient enables dairy and beef farmers to substantially lower their carbon footprint.

- June 2023: Godrej Agrovet launched a new campaign highlighting the importance of quality cattle feed for improving livestock health. The initiative emphasizes how better nutrition through scientifically formulated feed can enhance cattle productivity and support farmers’ livelihoods.

Global Cattle Feed Market Report Scope

Cattle feed consists of commercially produced formulations designed to supply proteins, energy, minerals, and vitamins essential for cattle's growth, maintenance, reproduction, and milk production. This report focuses exclusively on commercial cattle feed products, excluding on-farm fodder, forage, and crop residues.

The Cattle Feed Market is Segmented by Animal Type (Dairy Cattle, and Beef Cattle), Ingredient (Cereals, Cakes and Mixes, Food Wastages, Feed Additives, and Other Ingredients), By Form (Pellets, Mash, Crumble and Liquid), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The report offers market size and forecasts for cattle feed in terms of value (USD) and Volume (Metric Tons) for all the above segments.

| Dairy Cattle |

| Beef Cattle |

| Cereals |

| Cakes and Mixes |

| Food Wastages |

| Feed Additives |

| Other Ingredients |

| Pellets |

| Mash |

| Crumble |

| Liquid |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Animal Type | Dairy Cattle | |

| Beef Cattle | ||

| By Ingredient | Cereals | |

| Cakes and Mixes | ||

| Food Wastages | ||

| Feed Additives | ||

| Other Ingredients | ||

| By Form | Pellets | |

| Mash | ||

| Crumble | ||

| Liquid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the estimated value of the cattle feed market for 2026?

The cattle feed market size is estimated to reach USD 79.41 billion in 2026 and is projected to reach USD 98.23 billion by 2031.

Which region is projected to grow the fastest by 2031?

Africa is forecast to post the fastest growth with a 5.5% CAGR driven by policy-backed credit for fortified rations.

Which animal type segment is expanding the quickest?

Beef cattle feed demand is set to rise at a 5.2% CAGR during the forecast period 2026–2031, as feedlot finishing becomes more economical in South America.

How are precision technologies influencing feed efficiency?

Sensor-driven precision feeding platforms have cut waste by up to 8% and improved feed conversion by about 4.5% in early adopters.

Page last updated on: