Feed Acidulants Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

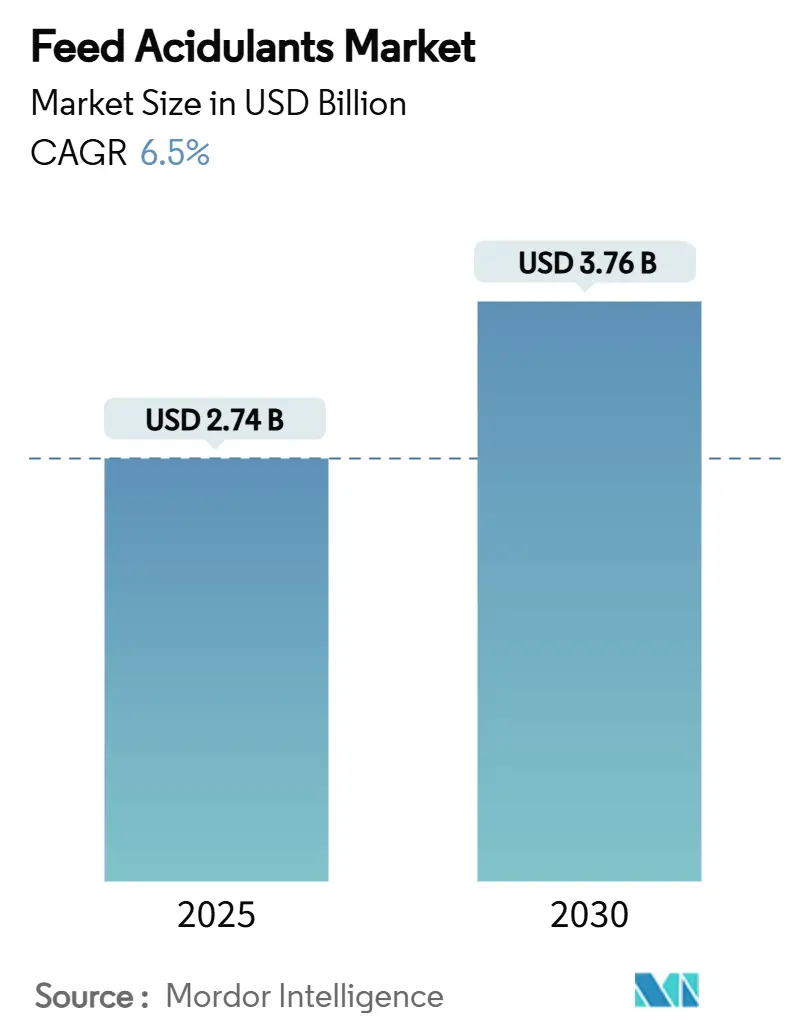

| Market Size (2025) | USD 2.74 Billion |

| Market Size (2030) | USD 3.76 Billion |

| Growth Rate (2025 - 2030) | 6.50% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Acidulants Market Analysis by Mordor Intelligence

The feed acidulants market size is estimated at USD 2.74 billion in 2025 and is projected to advance to USD 3.76 billion by 2030, reflecting a solid 6.5% CAGR over the forecast period. The demand for acidulants is increasing as livestock producers shift from antibiotic growth promoters to alternatives that provide similar gut-health benefits while meeting regulatory requirements. The European regulatory authorities' renewal of propionic acid approvals demonstrates confidence in these additives [1]Source: European Food Safety Authority, “Scientific Opinion on the Safety and Efficacy of Propionic Acid in Feed,” efsa.europa.eu. The expansion of industrial poultry production in the Asia-Pacific region increases the demand for pathogen control additives. The market growth is supported by advances in automated dosing technology, enabling liquid formulations to expand alongside established dry formats. The rising consumption of meat protein, pressure to improve feed efficiency, and focus on reducing livestock carbon emissions create opportunities for suppliers offering integrated acidulant and precision nutrition solutions.

Key Report Takeaways

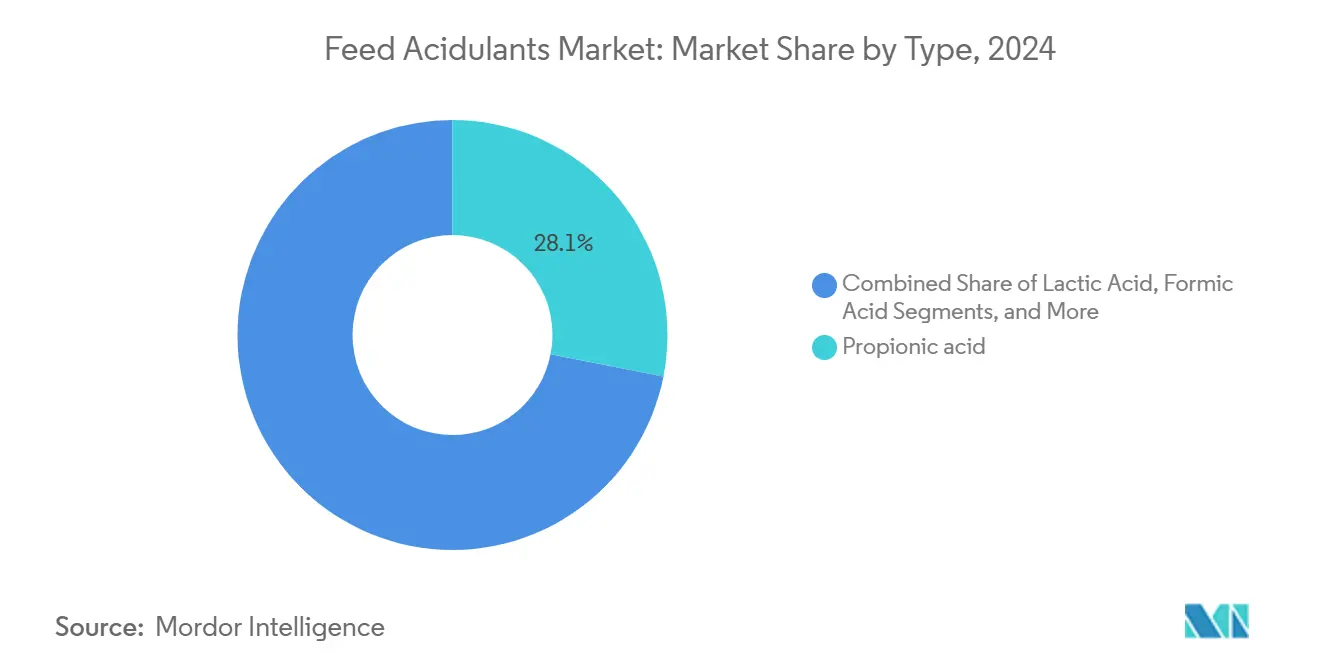

- By type, propionic acid captured 28.1% of the market share in 2024, and formic acid is forecast to expand at a 7.5% CAGR to 2030.

- By form, dry products captured 71.0% of the feed acidulants market share in 2024, while liquid products are set to grow at a 7.0% CAGR through 2030.

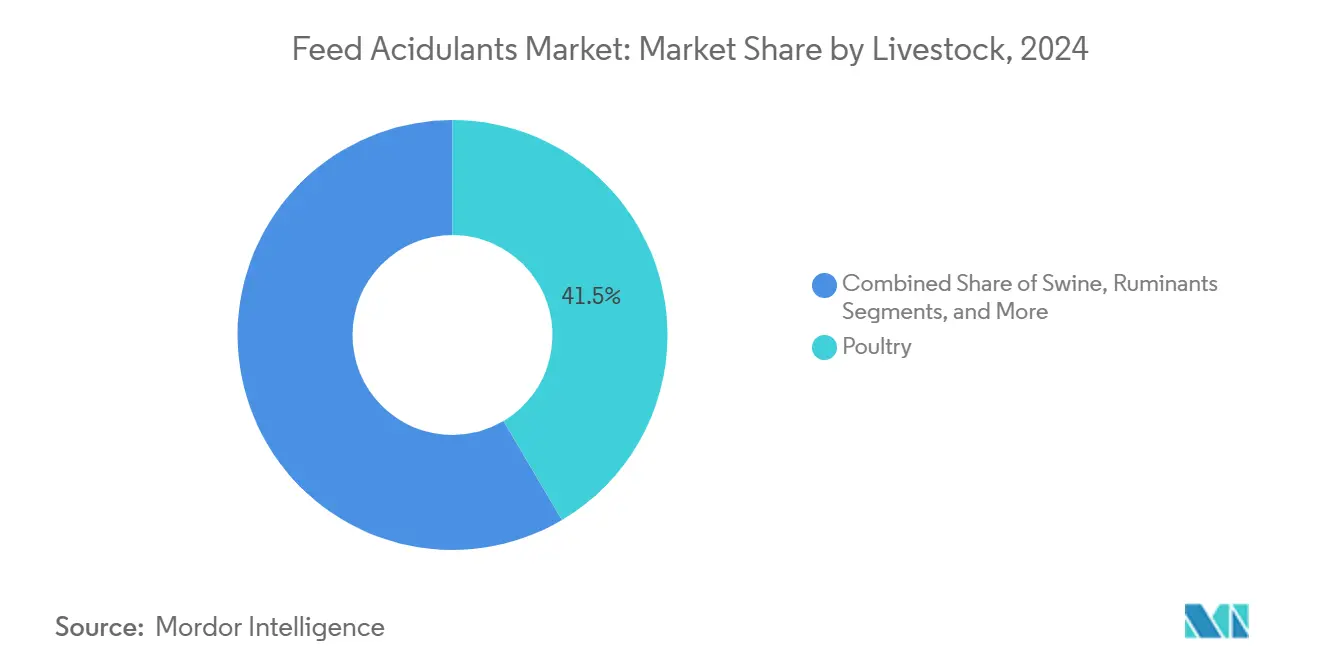

- By livestock, poultry accounted for a 41.5% share of the feed acidulants market size in 2024, and aquaculture is projected to advance at a 7.5% CAGR between 2025 and 2030.

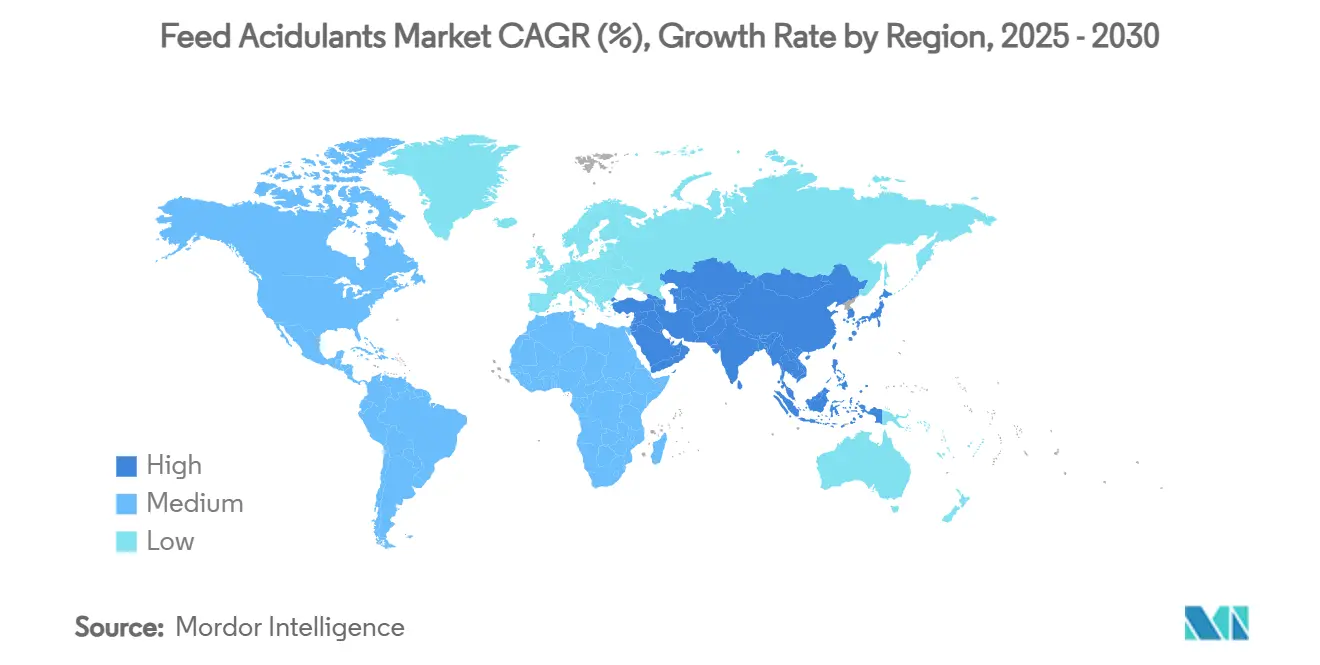

- By geography, Asia-Pacific commanded a 43.2% share of the feed acidulants market in 2024, and the Middle East region exhibits the fastest CAGR at 8.0% to 2030.

- BASF SE, Cargill Incorporated, ADM, Yara International ASA, and dsm-firmenich collectively held 41.3% of global revenue in 2024.

Global Feed Acidulants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising meat protein intake | +1.8% | Global, with highest impact in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Post-antibiotic feed regulations | +2.1% | North America and Europe primary, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Industrial-scale poultry farming | +1.6% | Asia-Pacific core, expanding to Africa and South America | Medium term (2-4 years) |

| Enhanced feed conversion focus | +1.2% | Global, with emphasis in cost-sensitive markets | Long term (≥ 4 years) |

| On-farm acidification tech adoption | +0.8% | North America and Europe early adopters, Asia-Pacific followers | Long term (≥ 4 years) |

| Carbon-footprint labeling of feed | +0.5% | Europe and North America primary, limited global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Meat Protein Intake

Global per-capita meat consumption increases steadily, driven by the growth of disposable income in emerging economies[2]Source: OECD and FAO, “Agricultural Outlook 2025-2034,” oecd.org . Additional feed demand presses producers to maximize nutrient utilization, positioning acidulants as cost-effective tools for extracting more usable energy from feed grains. Formic acid, especially in intensive broiler operations, benefits from pathogen suppression, which directly enhances carcass yield and quality.

Post-Antibiotic Feed Regulations

The withdrawal of antibiotic growth promoters across major markets has elevated acidulants to primary gut-health solutions[3]Source: European Food Safety Authority, “Scientific Opinion on the Safety and Efficacy of Propionic Acid in Feed,” efsa.europa.eu. Early EU adoption, followed by stricter rules in China and the United States, shifts purchasing criteria toward documented efficacy and safety data. Regulatory alignment boosts confidence in propionic and lactic acids, accelerating their incorporation into mainstream formulations.

Industrial-Scale Poultry Farming

Rapid poultry-farm consolidation in Asia-Pacific increases stocking densities, magnifying the threat of Salmonella and Campylobacter. Trials show that citric-acid supplementation in broiler diets improves body-weight gain and lowers feed conversion ratios, validating acidulants as indispensable performance enhancers. Liquid acid programs integrate seamlessly with automated feeders, ensuring uniform dosing across large flocks.

Enhanced Feed Conversion Focus

As corn and soybean markets continue to fluctuate unpredictably, producers are prioritizing even marginal improvements in feed efficiency to protect their profitability. Acidified aquaculture diets cut the energetic cost of digestion by 45% and improve feed conversion efficiency by 14%, demonstrating cross-species benefits. Suppliers leveraging encapsulation can deliver acids precisely to targeted gut segments, translating lab gains into commercial scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile organic-acid raw-material prices | -1.40% | Global with highest impact in import-dependent regions | Short term (≤ 2 years) |

| Stringent handling safety norms | -0.90% | Europe and North America primary, expanding globally | Medium term (2-4 years) |

| Fermentation-based feed probiotics cannibalizing acids | -0.60% | Global with early adoption in developed markets | Long term (≥ 4 years) |

| Container-shipping bottlenecks for formic acid | -0.40% | Asia-Europe trade corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Acidulants Raw-Material Prices

Acidulants raw material producers wrestle with fluctuating corn and petrochemical feedstock costs, compressing margins, and raising pricing volatility for downstream feed mills. Smaller suppliers with limited hedging capacity feel the greatest squeeze, prompting long-term contracts and risk-sharing clauses between mills and integrators.

Stringent Handling Safety Norms

The corrosive nature of formic and propionic acids requires specialized storage tanks, stainless-steel piping, and operator training, which adds capital expenses for smaller mills. International Maritime Organization codes also categorize these acids as hazardous cargo, lengthening documentation procedures and increasing freight premiums[4]Source: International Maritime Organization, “IBC Code Requirements for Formic Acid,” imo.org . Buffered or encapsulated formats ease compliance yet carry price premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Propionic Acid Dominance Faces Formic Acid Challenge

Propionic acid generated 28.1% of the feed acidulants market size in 2024, with dual mold control and performance benefits. Strong regulatory endorsements and existing production scale anchor its leadership. However, tightening food-safety targets intensify demand for formic acid, projected to register the fastest 7.5% CAGR. At this growth pace, formic acid’s share will close on propionic acid as producers value its superior efficacy against Salmonella and Campylobacter.

Formic-acid suppliers invest in buffered derivatives that mitigate equipment corrosion and worker-safety concerns, broadening adoption in high-volume mills. Citric, lactic, and sorbic acids retain niche roles in specialty programs where mild pH adjustment and consumer perception carry weight. The shifting portfolio encourages companies to position multi-acid blends that balance antimicrobial activity, palatability, and cost efficiency.

By Form: Dry Formulations Lead Despite Liquid Growth

Dry acidulants held a share of 71.0% of the feed acidulants market size in 2024, owing to their robustness during pelleting and lower freight cost per active unit. Pellet-stable powders allow feed mills to avoid separate dosing equipment, suiting regions with limited capital budgets. Encapsulation advances further expand powder utility by protecting acids until intestinal release.

Liquid products, though smaller, are growing 7.0% annually as integrators retrofit lines with automated pumps that guarantee batch-to-batch consistency. Liquids blend seamlessly into mash feeds and waterlines, providing rapid antimicrobial action. Suppliers differentiate via pH-stable emulsions that resist phase separation in humid tropical climates, gaining traction among Asia-Pacific poultry integrators.

By Livestock: Poultry Dominance Challenged by Aquaculture Growth

Poultry accounted for the feed acidulants market share of 41.5% in 2024. Demand stems from antibiotic-free broiler mandates that necessitate feed conversion improvements and pathogen load reduction. Continuous research shows that acidulants can lower Salmonella prevalence in processing plants, enabling integrators to meet retailer safety audits.

Aquaculture, while smaller, exhibits a 7.5% CAGR and is on track to outpace growth in terrestrial species. Encapsulated acids stabilize gut pH in carnivorous fish, cutting Feed Conversion Ratios (FCRs) and reducing nitrogenous waste. Swine and ruminant segments maintain steady adoption, leveraging acidulants for feed preservation during extended storage in humid regions.

Geography Analysis

Asia-Pacific controls 43.2% of global revenue, driven by rapid poultry intensification and a thriving aquaculture sector. Strong growth in India, Vietnam, and Indonesia pushes local compounders to integrate acids that suppress feed-borne pathogens while maintaining pellet hygiene. Government food-safety initiatives and private-label export ambitions further embed acid programs in standard rations. Competitive local supply combined with multinational joint ventures ensures price-competitive access across the region.

The Middle East registers the quickest 8.0% CAGR as governments invest in protein self-sufficiency. Saudi Arabia and Turkey deploy modern feed mills with automated liquid-acid dosing lines that support antibiotic-free production. Aquaculture in Egypt and Turkey benefits from citric and formic acids that enhance pellet water stability and digestion.

North America and Europe hold mature yet innovative markets. Regulatory clarity drives continuous reformulation, with carbon-footprint labeling encouraging lower-emission feed packs. North American integrators pursue precision-nutrition platforms pairing acids with real-time sensor feedback. Europe emphasizes buffered and encapsulated formats that mitigate worker safety concerns while dovetailing with methane-reduction initiatives in dairy and beef.

Competitive Landscape

The feed acidulants market shows moderate fragmentation, with the top five suppliers controlling 41.3% of revenue. BASF SE remains a key player, benefiting from its fully integrated chemical operations that help manage raw material volatility and support large-scale production across Asia-Pacific. Cargill Incorporated also holds a strong position by combining its acid offerings with broader protein-nutrition solutions, catering to integrators looking for comprehensive, one-stop services.

ADM’s new Paraná plant lifts South American output capacity 40%, aligning supply with expanding poultry and aquaculture demand. Evonik and Kemin differentiate through encapsulation and proprietary blends such as FORMYL Na that overcome corrosivity hurdles.

Yara International ASA is a key player in the global feed acidulants market, offering a range of acid-based solutions that enhance feed efficiency and animal health. Its strong focus on sustainable livestock nutrition supports its competitive position in this segment. dsm-firmenich asset reallocation toward methane-mitigation additives indicates a strategic exit from commodity acids but opens acquisition opportunities for regional specialists. Ongoing expansions by Brenntag and Galactic illustrate mid-tier players’ confidence in growth potential.

Feed Acidulants Industry Leaders

BASF SE

Cargill Incorporated

ADM

Yara International ASA

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kemin introduced PROSIDIUM, a peroxy acid-based feed pathogen control acidulants designed to reduce Salmonella and viral threats in raw feed, enhancing feed safety and animal health.

- October 2024: dsm-firmenich opened a new facility in Sete Lagoas, Brazil, with an annual production capacity of 100,000 metric tons of cattle supplements. This expansion enhances its feed additive portfolio in South America, addressing the demand for functional ingredients such as feed acidulants that improve ruminant health and productivity.

- June 2024: Kemin introduced FORMYL, a feed acidulant for swine in the United States market. The product, formulated with encapsulated calcium formate and citric acid, combines acidification and pathogen control benefits. FORMYL supports intestinal health, improves feed efficiency, and manages Enterobacteriaceae and E. coli challenges without antibiotic use.

- May 2024: Innovad Group has acquired Oligo Basics, a key player in Brazil's nutritional feed additives market. This acquisition strengthens Innovad's presence in the region and expands its product portfolio, including feed acidulants, to serve animal health and performance needs in the South American market.

Global Feed Acidulants Market Report Scope

Feed acidulants are organic or inorganic acids added to animal feed to lower pH, inhibit harmful bacteria, improve gut health, enhance nutrient absorption, and support better feed efficiency and animal performance.

The Feed Acidulants Market Report is segmented by Type (Lactic Acid, Formic Acid, Propionic Acid, Malic Acid, Citric Acid, Sorbic Acid, Acetic Acid, and Others), Form (Dry and Liquid), Livestock (Poultry, Swine, Ruminants, Aquaculture, and Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Lactic Acid |

| Formic Acid |

| Propionic Acid |

| Malic Acid |

| Citric Acid |

| Sorbic Acid |

| Acetic Acid |

| Others |

| Dry |

| Liquid |

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Type | Lactic Acid | |

| Formic Acid | ||

| Propionic Acid | ||

| Malic Acid | ||

| Citric Acid | ||

| Sorbic Acid | ||

| Acetic Acid | ||

| Others | ||

| By Form | Dry | |

| Liquid | ||

| By Livestock | Poultry | |

| Swine | ||

| Ruminants | ||

| Aquaculture | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the feed acidulants market?

The feed acidulants market is valued at USD 2.74 billion in 2025.

Which acid type holds the largest share?

Propionic acid leads with 28.1% revenue share in 2024.

Which region is growing fastest?

The Middle East shows the quickest growth with a 8.0% CAGR from 2025 to 2030.

What share do dry formulations command?

Dry products account for 71.0% of revenue and remain the dominant form of acidulants in 2024.

Page last updated on: