Airport Thermal Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

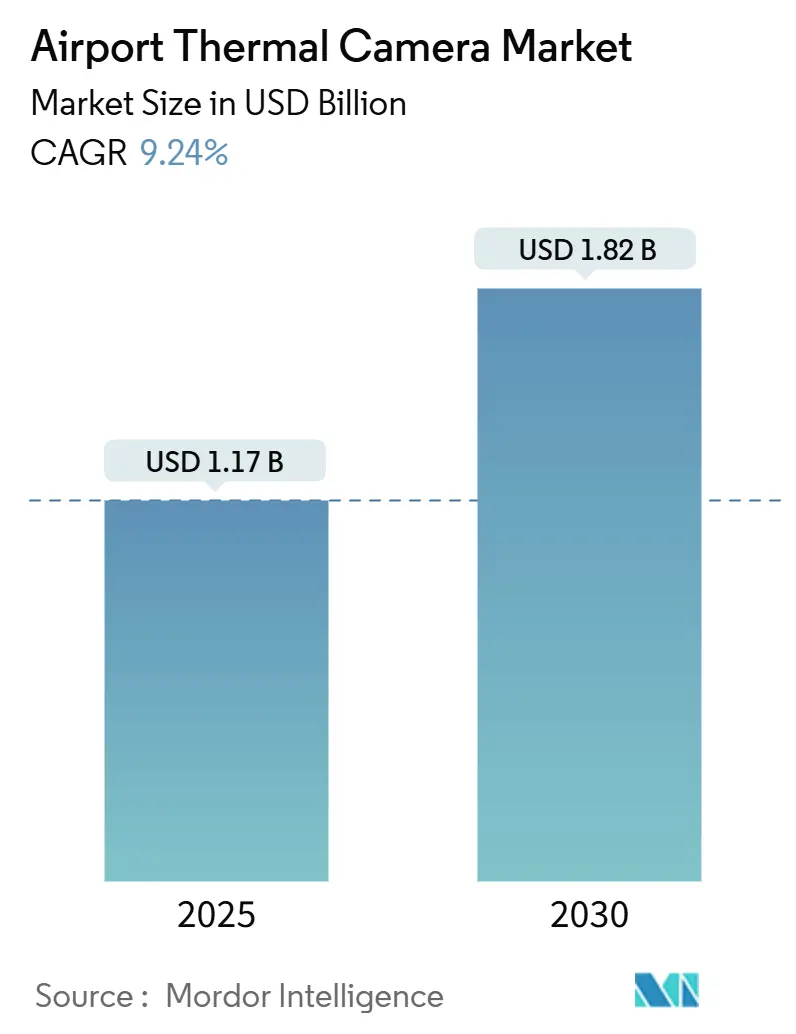

| Market Size (2025) | USD 1.17 Billion |

| Market Size (2030) | USD 1.82 Billion |

| Growth Rate (2025 - 2030) | 9.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Thermal Camera Market Analysis by Mordor Intelligence

The airport thermal camera market size reached USD 1.17 billion in 2025 and is projected to climb to USD 1.82 billion by 2030, translating to a 9.24% CAGR across the forecast period. Rapid modernization of checkpoint technology, rising perimeter-security obligations, and sustained infectious-disease preparedness combine to accelerate procurement across all airport classes. Early adopters now upgrade from single-purpose cameras to AI-ready, open-architecture platforms. At the same time, new-build terminals specify multi-sensor suites that treat thermal, radar, and visible video as one data stream. Vendors who embed edge analytics and support third-party algorithms are favored because their systems fit the Transportation Security Administration (TSA) and European Union (EU) open-architecture rules. Hardware resilience also matters as procurement teams weigh the impact of germanium export controls and look for optics made with alternative chalcogenide glass to avoid supply shocks.

Key Report Takeaways

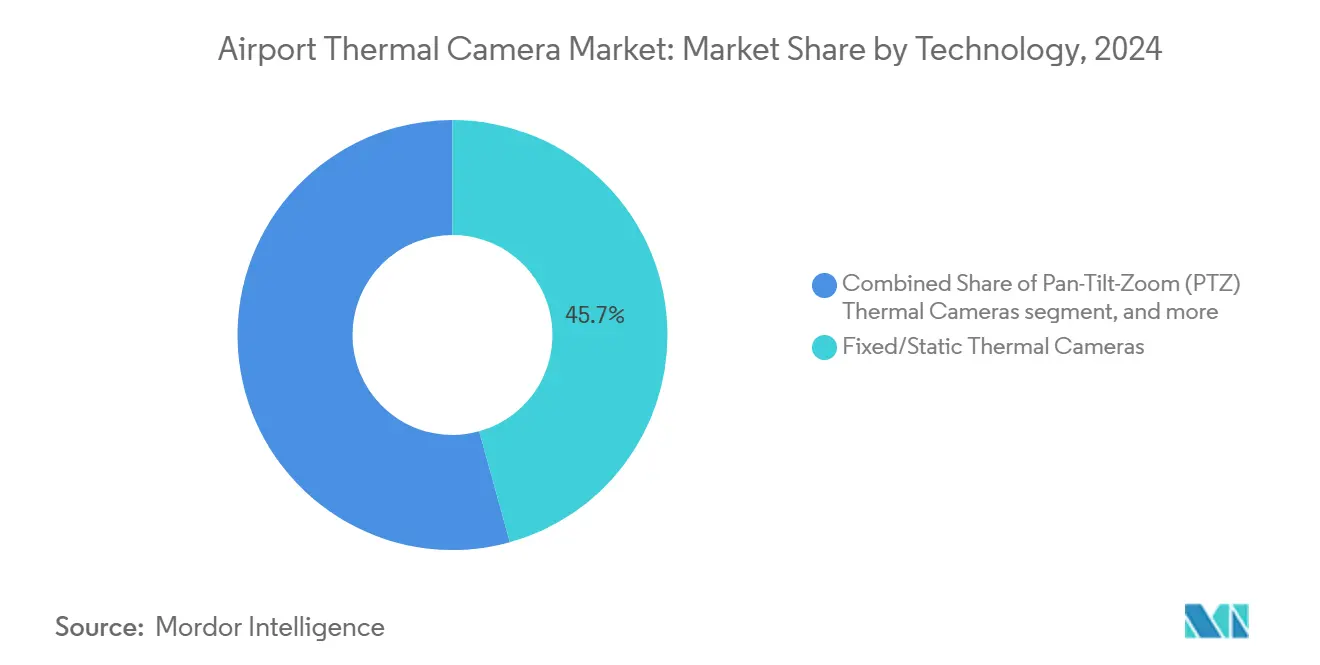

- By camera type, fixed/static systems led with 45.70% revenue share in 2024; dual-mode units are advancing at a 12.20% CAGR through 2030.

- By wavelength, long-wave infrared captured 60.70% of the airport thermal camera market share in 2024, whereas short-wave infrared is forecasted to grow 11.40% per year to 2030.

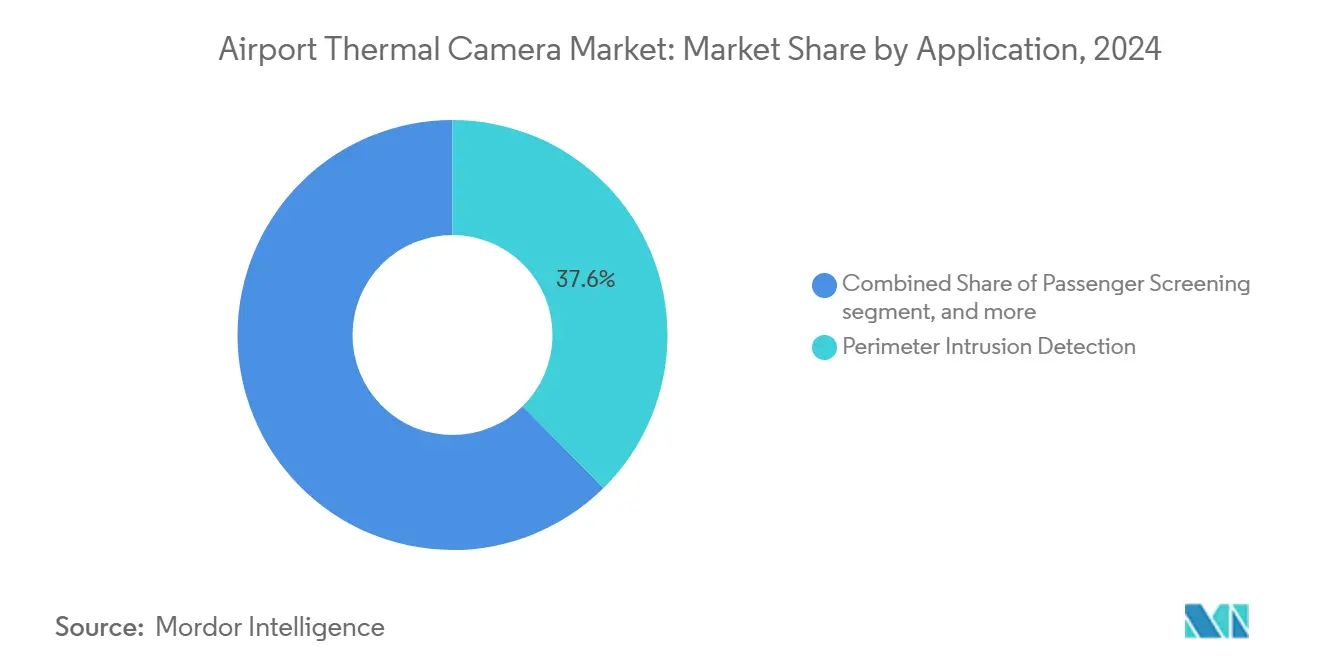

- By application, perimeter intrusion detection accounted for 37.60% of the airport thermal camera market size in 2024, while passenger screening is set to expand at a 12.45% CAGR through 2030.

- By installation location, perimeter fencing held a 38.90% share in 2024, yet terminal buildings are projected to rise at an 11.40% CAGR to 2030.

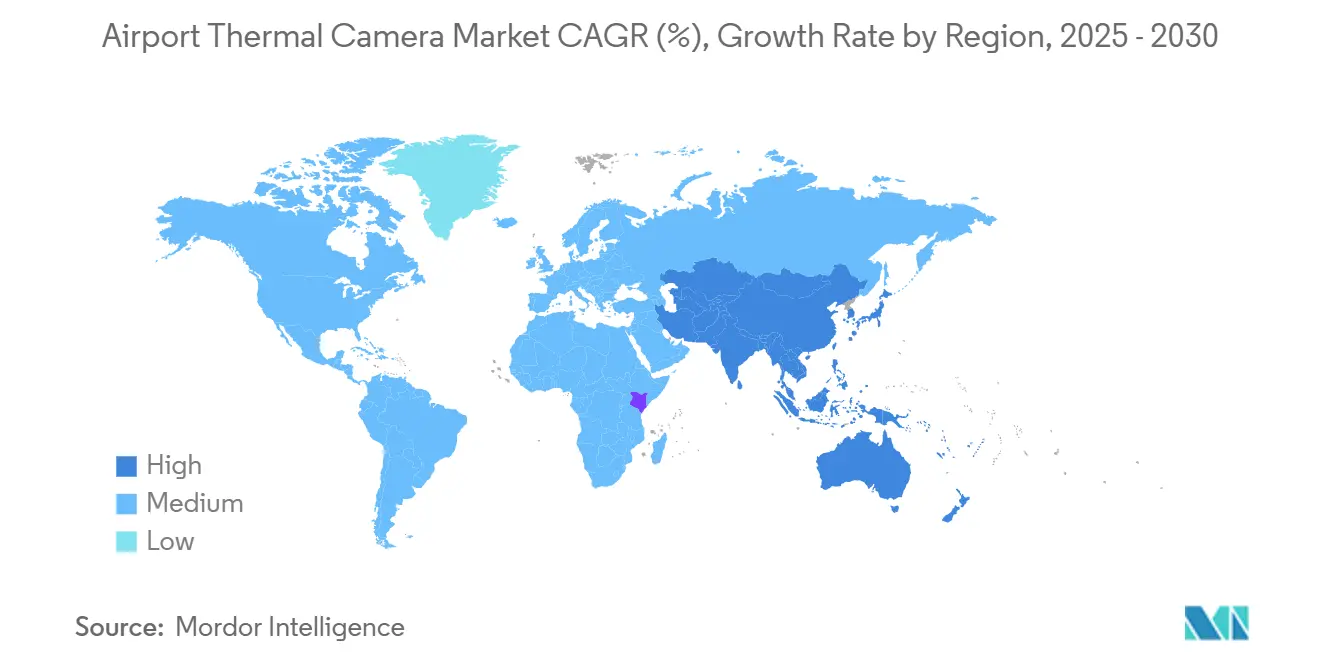

- By geography, North America dominated with a 36.78% share in 2024; Asia-Pacific is poised for the fastest 10.95% CAGR to 2030.

Global Airport Thermal Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened aviation security mandates | +2.1% | Global; early adoption in North America and Europe | Medium term (2-4 years) |

| Increasing adoption for infectious disease screening | +1.8% | Global; strongest growth in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Smart airport infrastructure investments | +1.6% | North America and Europe core; spillover to Asia-Pacific | Long term (≥ 4 years) |

| AI-enabled unmanned perimeter surveillance | +1.4% | Global; advanced rollouts in developed markets | Medium term (2-4 years) |

| All-weather operability requirements | +1.2% | Global; critical in harsh-climate airports | Long term (≥ 4 years) |

| Predictive maintenance sustainability push | +0.9% | North America and Europe lead; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Aviation Security Mandates

International regulators now stipulate layered detection that runs around the clock rather than at discrete checkpoints. TSA’s Checkpoint Requirements and Planning Guide specifies open-architecture imaging endpoints so that thermal feeds integrate with computed tomography scanners and millimeter-wave portals.[1]Source: Transportation Security Administration, “Checkpoint Requirements and Planning Guide,” tsa.gov The EU mirrors this approach by mandating advanced imaging at all commercial airports by 2025, which pushes operators to refresh legacy analog cameras. Airport consortia report smoother passenger throughput once visible and thermal streams merge into one threat-assessment dashboard, lowering secondary screening rates and operator workload. Vendors embedding standards-based interfaces win procurements because security teams can swap analytics modules without reinstalling hardware.

Increasing Adoption for Infectious Disease Screening

Thermal cameras, once reserved for cargo bays, now stand at terminal entrances as passive health checkpoints. Large hubs validated high-volume workflows during recent pilot programs that processed thousands of passengers each hour without reducing lane capacity. Integration with biometric gates allows temperature checks, identity confirmation, and ticket validation in one step, minimizing touchpoints and operator intervention. Health agencies value the contactless workflow because elevated readings trigger immediate secondary evaluation in an isolated room, avoiding broader disruption. Continuous firmware updates add mask-detection and crowd-density alerts, broadening the use case beyond fever screening into overall public-health surveillance.

Smart Airport Infrastructure Investments

Smart-airport budgets allocate escalating shares to sensor fusion, where thermal imaging is a core input alongside radar, LiDAR, and acoustics. Platforms built on common data structures funnel every sensor into a single operations center, reducing siloed decision-making and shortening incident response times. Heathrow’s centralized security center exemplifies how thermal feeds improve energy management by detecting overheated motors in baggage systems, prompting preventive action that limits downtime.[2]Source: Airports International, “Airport Security: The Latest Developments,” airportsint.com Edge processing enabled by 5G private networks keeps sensitive imagery on-site while delivering analytics within milliseconds, satisfying data-sovereignty rules and accelerating corrective actions.

AI-Enabled Unmanned Perimeter Surveillance

Edge-trained convolutional networks now classify humans, vehicles, and wildlife directly on the thermal sensor, eliminating constant human monitoring. When the algorithm detects an anomaly, it automatically cues a pan-tilt-zoom visible camera for forensic confirmation and dispatches alerts to mobile devices. Such closed-loop automation reduces false alarms because classification confidence reaches pre-programmed thresholds before escalation. Airports with wide perimeters benefit most, replacing extensive guard patrols with a handful of mobile responders who receive geolocated alerts and incident snapshots. Continuous learning models retrain on local weather and lighting conditions, further improving accuracy over time.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procurement and installation cost | -1.9% | Global; most restrictive in developing markets | Medium term (2-4 years) |

| Passenger privacy and data protection concerns | -1.2% | European Union and North America | Short term (≤ 2 years) |

| Thermal camouflage and spoofing risks | -0.8% | Global; critical in high-security hubs | Long term (≥ 4 years) |

| Infrared sensor supply chain disruptions | -1.4% | Global; advanced sensors most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procurement and Installation Cost

Premium radiometric thermal cameras retail between USD 5,000 and USD 25,000 per unit, and extensive facilities often require more than 300 units for full coverage. Network backbones, stainless-steel poles, and lightning protection kits add another 40% to upfront budgets. Annual support contracts covering firmware upgrades, cyber-hardening, and operator training reach 20–30% of capital value, straining finances at secondary airports operating on thin margins. Leasing and outcome-based models are emerging to lower the entry barrier, yet adoption remains limited outside North America.

Passenger Privacy and Data Protection Concerns

Regulators classify temperature data as sensitive health information. Under the European Union General Data Protection Regulation, airports must collect explicit consent or rely on public-health exemptions, which demand transparent signage and strict retention schedules. Facial-recognition modules exacerbate scrutiny because combined thermal and visible signatures enable biometric re-identification. Operators address the risk by anonymizing imagery at the edge, storing only metadata and threshold breaches, then automatically deleting all files after a defined window that rarely exceeds 30 days. These procedures add cost and complexity but are mandatory to avoid sanctions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Camera Type: Dual-Mode Integration Drives Innovation

Fixed/static cameras contributed 45.70% of 2024 revenue, underscoring operators’ reliance on continuous, maintenance-light perimeter monitoring. These units integrate thermal, visible, and radar triggers over Ethernet, easing tie-in with existing video management systems and reducing network bandwidth through on-edge video compression. Static devices watch for foreign object debris, human encroachment, and taxiway incursions around the clock in apron areas. Pan-tilt-zoom variants satisfy long-range surveillance in large-footprint airports, though their motorized drives require scheduled lubrication and increase mean-time-between-failure planning.

Dual-mode products, pairing a 640 × 512 thermal core with high-resolution color optics, register the highest 12.20% CAGR because they halve false alarms when both modalities concur. Several suppliers expose pixel-level data through an SDK, allowing airports to overlay thermal detection boxes onto visible streams within the same video window. Such fusion trims operator training because guards read one image, not two. The airport thermal camera market repeatedly rewards vendors able to supply these compact, drone-friendly modules that airport police now mount on quadcopters for incident verification flights.

By Wavelength: SWIR Technology Gains Momentum

Long-wave infrared continued to dominate, with a 60.70% 2024 share, due to cost-effective uncooled microbolometers aligning with human skin's 8–14 µm emission peak. The uncooled design eliminates cryogenic coolers, shrinks maintenance budgets, and simplifies installation in ceiling voids. Operators value long-wave reliability for runway surface-condition monitoring, where moisture quickly cuts visible contrast.

Short-wave infrared moves ahead at an 11.40% CAGR because its 0.9–1.7 µm band sees through smoke, mist, and exhaust plumes that scatter longer wavelengths. Short-wave sensors capture reflected solar photons during daylight, creating visible-like imagery even when conventional cameras succumb to backlighting. Airports adopting short-wave units in approach zones now meet all-weather visibility targets without doubling camera count. As pricing declines, procurement teams add short-wave arrays as a complementary layer, boosting the airport thermal camera market penetration in mixed-spectral deployments

By Application: Passenger Screening Transformation

Perimeter intrusion solutions secured 37.60% of 2024 revenue, underscoring security’s core mandate to deny unauthorized access. Fixed thermal chains line nearly every fence line in North American Category X airports, supplying real-time analytics that feed joint emergency operations centers staffed by police, fire, and TSA. When analytics detect movement, vector information is handed off to pan-tilt-zoom devices for classification and to ground radar for velocity confirmation, triggering dispatch within seconds.

Passenger screening shows 12.45% CAGR through 2030 as airports fuse temperature, biometric, and boarding data into single-step lanes. Gateways equipped with radiometric cameras isolate any passenger exhibiting a threshold breach, plus raise a secondary alert if facial-recognition tags them for additional screening. Therefore, the airport thermal camera market size for passenger-screening solutions rises faster than legacy fence installations, encouraging vendors to launch modular kiosks that airlines lease on a pay-per-screen basis.

By Installation Location: Terminal Integration Accelerates

Perimeter fencing installations held 38.90% of 2024 revenue as they formed the first line of defense. Layout designs place cameras at 200 m intervals with 30 % overlap to eliminate blind zones. Edge servers are positioned every 1 km of aggregate streams and run analytics locally before pushing relevant metadata to a data-center cluster behind the security operations center firewall. This zonal architecture meets cybersecurity best practices by containing the potential intrusion scope.

Terminal buildings are forecast to post an 11.40% CAGR because health and identity verification converge at landside entrances. Multi-sensor gantries now include radiometric arrays, ultraviolet document scanners, and millimeter-wave people-screeners in one arch. Operating staff need fewer physical interventions, cutting queue times and improving passenger satisfaction scores. As airports retrofit departure halls, the thermal camera market benefits from orders that specify radiometric accuracy better than ±0.3 °C to minimize nuisance alarms and comply with public-health guidance.

Geography Analysis

North America controlled 36.78% of 2024 sales, lifted by TSA grant programs funding advanced imaging at Category I and II airports. Open-architecture mandates stipulate that every new checkpoint endpoint accept third-party software, steering procurement toward hardware-agnostic thermal cameras. Canadian operators follow suit via the Verified Traveller initiative that pairs facial verification and fever detection at major hubs. Large install bases encourage continuous refresh cycles, supporting a robust aftermarket for firmware upgrades and analytics licenses.

Asia-Pacific records the fastest 10.95% CAGR, buoyed by parallel runway and terminal expansions across China and India. India’s Bureau of Civil Aviation Security requires body scanners at every airport that handles more than 2 million passengers annually, creating steady tenders for dual-mode thermal systems. Domestic Chinese suppliers leverage scale economies in uncooled microbolometers, undercutting foreign competition on price while still meeting global quality standards. Regional passenger growth means airports specify thermal imaging at the design phase, making retrofits unnecessary and reducing the total project cost of ownership.

Europe shows stable growth as the European Union harmonizes screening rules across member states and continues strict enforcement of passenger-privacy law. Operators, therefore, buy cameras offering real-time face-pixel blurring to satisfy GDPR requirements. Funds from the Connecting Europe Facility support upgrades at medium-sized airports in Eastern Europe, further broadening demand. Meanwhile, Middle East hubs invest in thermal analytics for perimeter-surveillance around ever-larger airfield footprints. South African facilities pilot radiometric cameras for solar farm maintenance on airport-owned land, diversifying use cases.

Competitive Landscape

The airport thermal camera market supports a moderately fragmented field where the top five vendors hold roughly one-third of global revenue. Teledyne Technologies leverages vertically integrated sensor fabrication to guarantee component availability despite export controls. Hikvision emphasizes AI acceleration chips that halve latency for perimeter analytics, while Bosch optimizes open-source codec support to simplify video-management integration. Smaller firms focus on edge-fusion software or specialized optics, often collaborating with larger camera makers under OEM agreements.

Strategic acquisitions intensify as incumbents target niche algorithm developers that speed adoption of multimodal screening. Teledyne’s purchase of several radiometric-software houses during 2024 accelerated its roll-out of precision temperature-analysis models, winning contracts from airports keen to merge maintenance and security functions. Supply-chain localization also gains traction; one North American newcomer fabricates chalcogenide lenses domestically, reducing exposure to germanium restrictions and appealing to TSA’s Buy-American preference. Competitive differentiation thus rests on AI breadth, optical-supply resilience, and standards-based interoperability—factors that collectively influence long-term customer lock-in.

Co-development programs with airport authorities further strengthen vendor relationships. Hanwha Vision’s 2025 launch of AI-radiometric cameras followed a year-long pilot at a major US hub that contributed training datasets and field feedback, shortening time-to-certification.[3]Source: Hanwha Vision, “News Center,” hanwhavision.com Bosch partners with European research institutes to validate privacy-preserving analytics, which improves regulatory acceptance and opens government subsidy channels. This technological depth and collaboration blend ensures a healthy but intensifying race for a share in the airport thermal imaging systems industry.

Airport Thermal Camera Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd.

Bosch Sicherheitssysteme GmbH (Robert Bosch GmbH)

Dahua Technology Co., Ltd.

Axis Communications AB

Teledyne FLIR LLC (Teledyne Technologies Incorporated)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SightLogix upgraded its SightSensor Infrared system, featuring improved detection, advanced Thermal AI for fewer false alarms, and user-friendly features. These enhancements ensure 24/7 security with consistent performance in all conditions, reaffirming SightLogix's commitment to cutting-edge outdoor thermal AI security solutions.

- January 2024: Hanwha Vision introduced advanced AI-powered radiometric thermal cameras, enhancing safety and precision in critical industries. With high-performance imaging, wide temperature detection (-40°C to 550°C), and AI-based object classification, these cameras ensure efficient monitoring, reduced downtime, and improved security. Flexible export options make them ideal for diverse industrial and commercial applications.

Global Airport Thermal Camera Market Report Scope

| Fixed/Static Thermal Cameras |

| Pan-Tilt-Zoom (PTZ) Thermal Cameras |

| Handheld/Portable Thermal Cameras |

| Dual-Mode Cameras |

| Long-Wave Infrared (LWIR 8–14 µm) |

| Mid-Wave Infrared (MWIR 3–5 µm) |

| Short-Wave Infrared (SWIR 0.9–1.7 µm) |

| Perimeter Intrusion Detection |

| Passenger Screening |

| Apron and Runway Monitoring |

| Fire Detection and Rescue |

| Equipment Preventive Maintenance |

| Terminal Buildings (Landside) |

| Airside and Apron |

| Perimeter Fencing |

| Control Towers and Critical Infrastructure |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Camera Type | Fixed/Static Thermal Cameras | ||

| Pan-Tilt-Zoom (PTZ) Thermal Cameras | |||

| Handheld/Portable Thermal Cameras | |||

| Dual-Mode Cameras | |||

| By Wavelength | Long-Wave Infrared (LWIR 8–14 µm) | ||

| Mid-Wave Infrared (MWIR 3–5 µm) | |||

| Short-Wave Infrared (SWIR 0.9–1.7 µm) | |||

| By Application | Perimeter Intrusion Detection | ||

| Passenger Screening | |||

| Apron and Runway Monitoring | |||

| Fire Detection and Rescue | |||

| Equipment Preventive Maintenance | |||

| By Installation Location | Terminal Buildings (Landside) | ||

| Airside and Apron | |||

| Perimeter Fencing | |||

| Control Towers and Critical Infrastructure | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is demand growing for airport thermal cameras?

Global revenue is projected to rise at a 9.24% CAGR from 2025 to 2030 as security and health-screening needs converge.

Which region offers the strongest expansion opportunities?

Asia-Pacific leads with a 10.95% CAGR driven by greenfield airport construction in China and India.

What segment shows the highest growth rate?

Dual-mode cameras that fuse thermal and visible imagery expand at a 12.20% CAGR through 2030.

Why are airports adding short-wave infrared sensors?

SWIR cameras maintain image quality in fog and smoke, yielding an 11.40% CAGR within the wavelength segment.

How do privacy regulations affect deployments?

European Union GDPR rules force anonymization and strict data-retention limits, raising implementation complexity and cost.

What is the key hurdle for smaller airports?

High capital and lifecycle costs remain the primary barrier, especially for facilities in developing markets.

Page last updated on: