Aircraft Cameras Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 32.9 Million |

| Market Size (2031) | USD 53.51 Million |

| Growth Rate (2026 - 2031) | 10.22% CAGR |

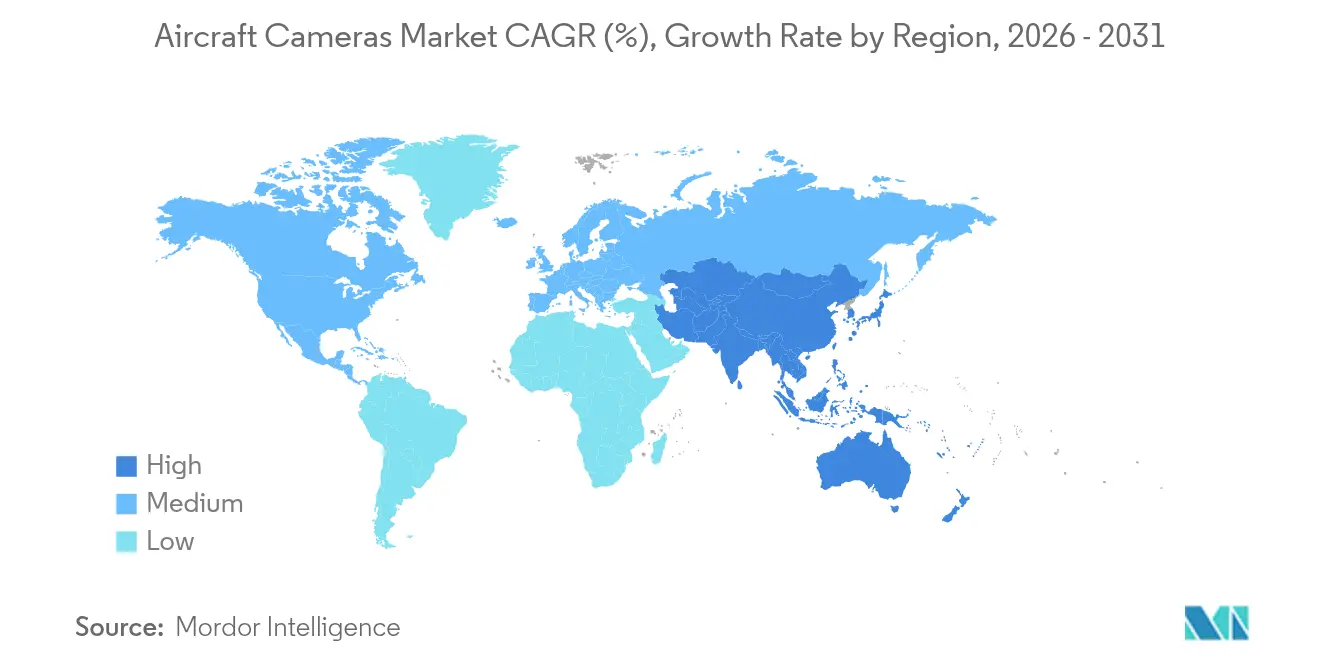

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

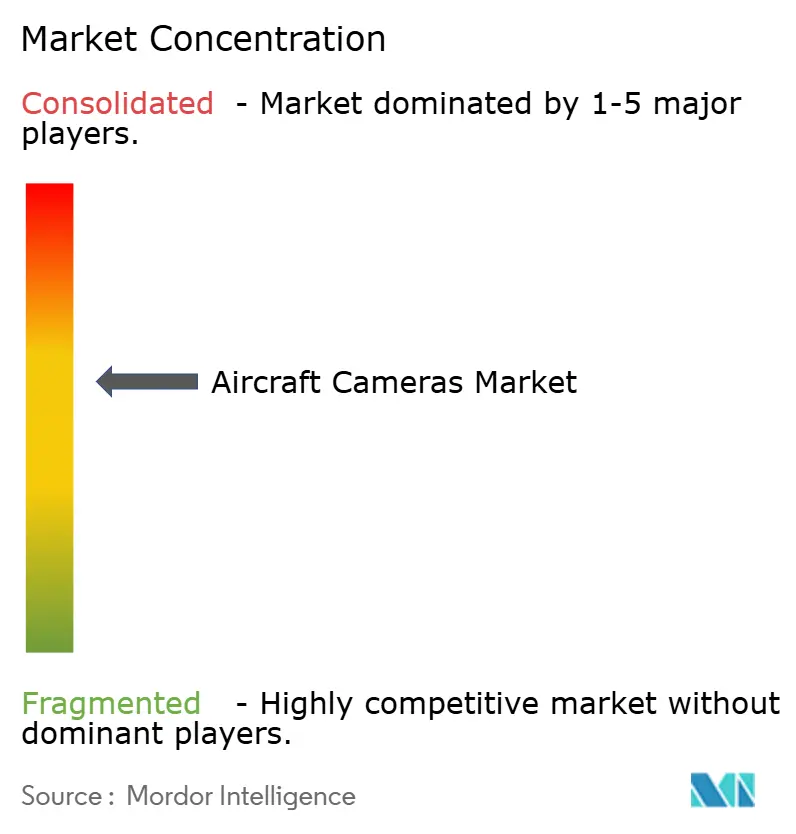

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Cameras Market Analysis by Mordor Intelligence

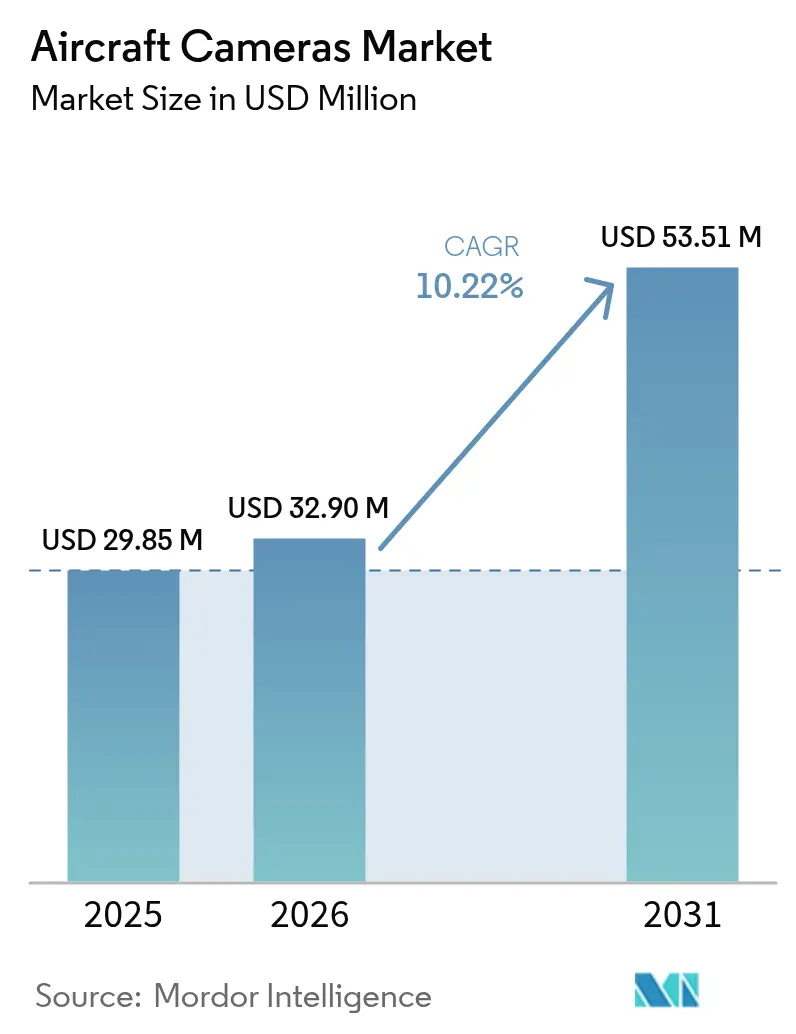

The aircraft cameras market size is expected to grow from USD 29.85 million in 2025 to USD 32.9 million in 2026 and is forecast to reach USD 53.51 million by 2031 at 10.22% CAGR over 2026-2031. Heightened regulatory pressure for cockpit-video recorders, escalating retrofit activity for 4K cabin-surveillance systems, and the rapid mainstreaming of unmanned and eVTOL platforms collectively underpin this trajectory. Demand also benefits from airlines’ preference for modular plug-and-play upgrades that avoid long ground times, while OEM linefit programs bake advanced imaging into next-generation airframes. In parallel, defense procurement, exemplified by the US Army’s HADES initiative, creates a robust pipeline for multisensor ISR solutions that rely on ruggedized, high-fidelity optics. Competitive intensity rises as traditional avionics majors compete with niche vision-tech firms that bring AI-enabled edge processing to predictive maintenance and autonomous flight applications.

Key Report Takeaways

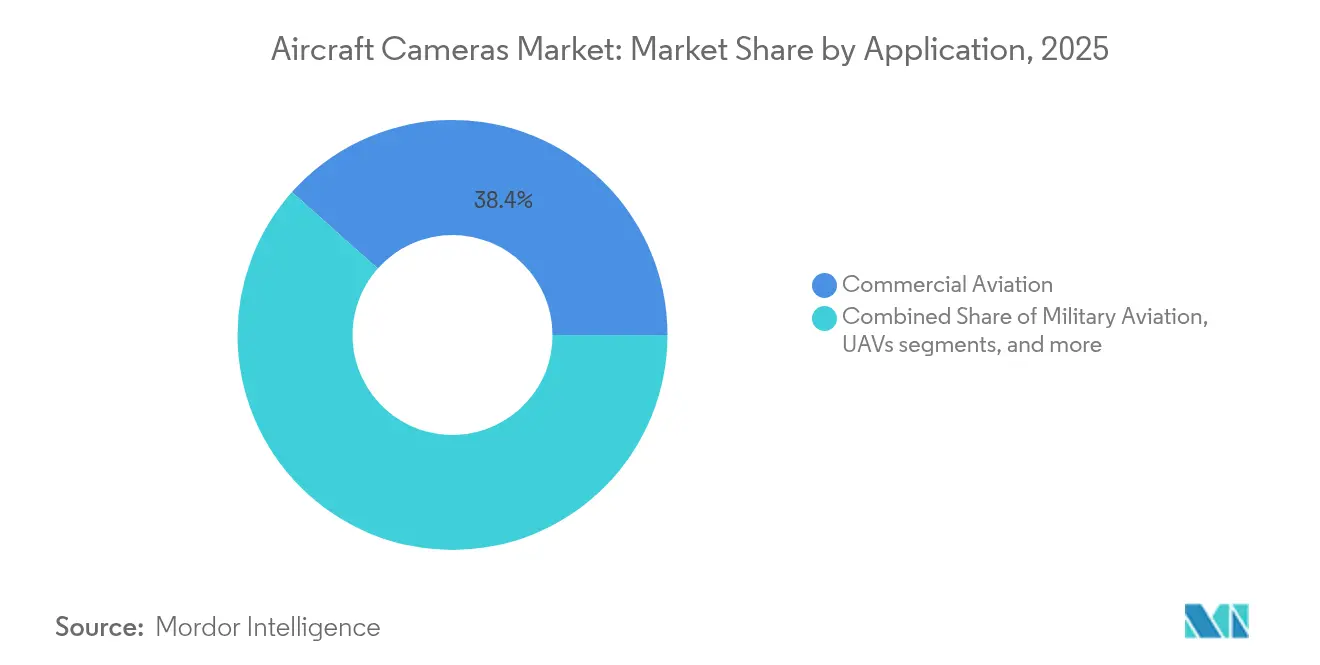

- By application, commercial aviation led with 38.42% revenue share in 2025, while unmanned aerial vehicles (UAVs) are projected to expand at a 12.08% CAGR to 2031.

- By camera installation, external systems commanded 56.75% of the aircraft cameras market share in 2025 and are advancing at an 11.03% CAGR through 2031.

- By camera type, multispectral/hyperspectral units accounted for 36.88% of the aircraft cameras market size in 2025; AI-enabled smart cameras represent the fastest-growing type with an 11.52% CAGR to 2031.

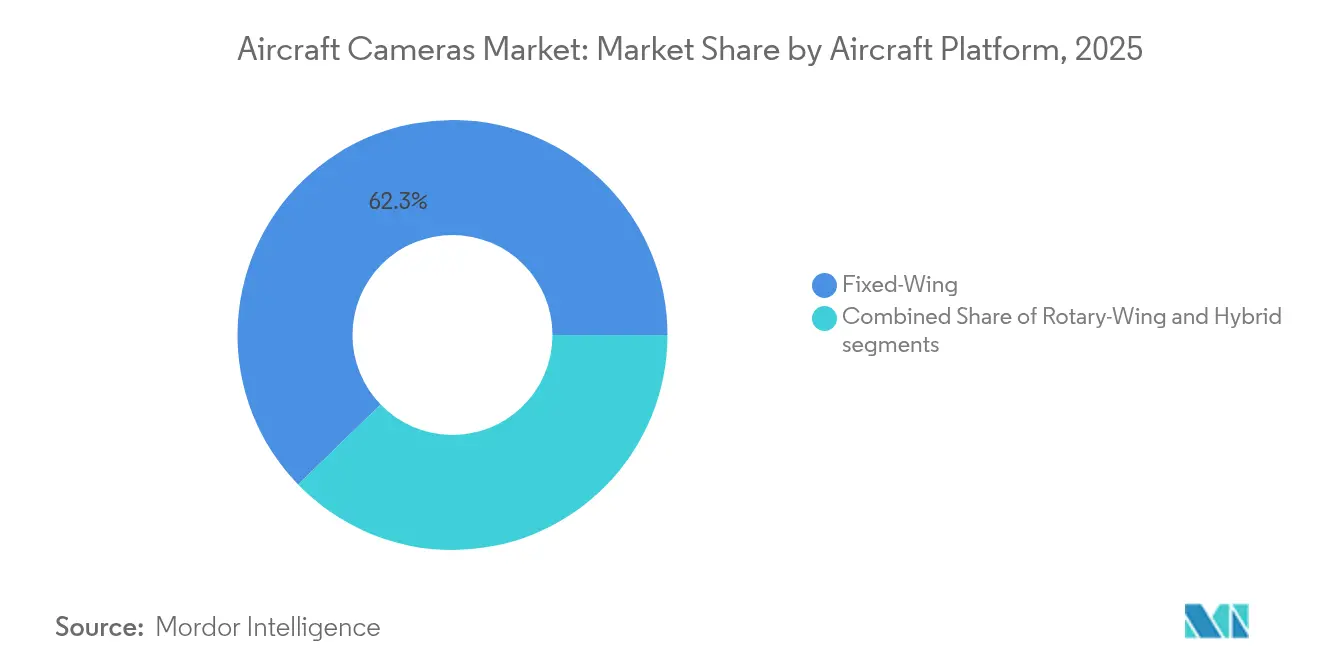

- By aircraft platform, fixed-wing aircraft held a 62.25% market share in 2025, whereas hybrid eVTOL concepts are poised to achieve the highest 10.34% CAGR during the forecast horizon.

- By region, North America led with a 37.95% market share in 2025, while the Asia-Pacific region is set to post the fastest growth, with a 10.31% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Cameras Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising retrofit demand for 4K cabin-surveillance upgrades | +2.10% | North America, Europe, Global fleets | Medium term (2-4 years) |

| AI-assisted predictive-maintenance cameras for digital-twin programs | +1.80% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Mandatory EASA/FAA cockpit-video recorders from 2028 | +1.60% | Global | Medium term (2-4 years) |

| Growth in unmanned and eVTOL platforms needing SWaP-optimized imaging | +1.40% | North America, Asia-Pacific | Short term (≤2 years) |

| Thermal/IR camera integration for wildfire monitoring operations | +0.90% | North America, Australia, Mediterranean Europe | Short term (≤2 years) |

| Demand for 360° taxi-aid systems on next-gen widebody aircraft | +0.70% | Global hub airports | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Retrofit Demand for 4K Cabin-Surveillance Upgrades

Airlines are accelerating the modernization of in-cabin video infrastructure as safety guidelines become stricter and insurers seek more granular incident evidence. Air Canada’s A320 and A321 upgrade program highlights the pivot toward high-resolution cameras that deliver facial-recognition-ready imagery and integrate seamlessly with existing cabin-management systems.[1]Air Canada, “Fleet modernization updates,” aircanada.com Short installation windows favor modular, plug-and-play designs, enabling carriers to refresh surveillance capability during overnight checks instead of extended heavy-maintenance visits. The 4K baseline has quickly become the de facto procurement specification, positioning vendors with scalable, open-architecture solutions to capture retrofit budgets. As regulators consider broader mandates for behavioral analytics functions, suppliers who validate AI algorithms under DO-178C will likely enjoy an early-mover advantage in the aircraft cameras market.

AI-Assisted Predictive-Maintenance Cameras for Digital-Twin Programs

To feed digital-twin ecosystems, OEMs and tier-one integrators increasingly embed vision sensors inside wings, engines, and airframes. Lockheed Martin’s AAIR platform uses computer vision to detect microcracks and paint degradation, trimming unscheduled maintenance by up to 15% while extending component life cycles.[2]Lockheed Martin, “AAIR autonomous inspection platform,” lockheedmartin.com Real-time video analytics processed at the edge eliminate latency, enabling operators to optimize maintenance schedules and maintain high fleet availability. Demand for ruggedized, low-latency cameras that support standardized data interfaces is growing faster than legacy inspection borescopes. Vendors who certify edge-AI modules under avionics safety standards gain a compelling foothold, particularly as airlines converge their digital engineering and MRO budgets.

Mandatory EASA/FAA Cockpit-Video Recorders from 2028

Regulatory momentum toward 25-hour cockpit video retention will trigger a sizable wave of compliance-driven procurement. The US National Transportation Safety Board’s post-accident recommendations have galvanized both FAA and EASA rulemaking, targeting entry into force in 2028.[3]National Transportation Safety Board, “Most wanted safety improvements,” ntsb.gov Approximately 6,000 active commercial jets fall under the scope of retrofit, creating a multi-year order backlog for certified suppliers. Incumbent avionics houses with DO-160-qualified hardware and cyber-secure data-management suites are best positioned. Nevertheless, privacy objections from pilot unions in North America and Europe remain a key variable that could stretch certification timelines or dilute technical specifications, moderating the upside for some aircraft cameras market participants.

Growth in Unmanned and eVTOL Platforms Needing SWaP-Optimized Imaging

The rapid expansion of drone logistics, defense ISR, and urban air mobility (UAM) ecosystems is generating new demand for size-, weight-, and power-constrained (SWaP-constrained) optics. The US government’s policy to prioritize domestic drone supply chains gives local camera manufacturers preferred-vendor status. Concurrently, breakthroughs in metalens technology produce optics thinner than a human hair without compromising optical quality, perfectly aligning with the payload envelopes of small air vehicles. As regulators expand beyond-visual-line-of-sight (BVLOS) corridors, detect-and-avoid camera assemblies become a mandatory kit, providing a lucrative niche for vendors that can merge optical fidelity with ultralow power draw.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High DO-178/DO-254 certification costs for new camera hardware | -1.20% | Global, hits smaller vendors hardest | Long term (≥4 years) |

| Pilot-union privacy push-back on cockpit video | -0.80% | North America, Europe | Medium term (2-4 years) |

| Export-control restrictions on dual-use EO/IR sensors | -0.60% | US-China trade lanes | Short term (≤2 years) |

| Persistent semiconductor supply-chain volatility | -0.50% | Global, Asia-Pacific fabs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High DO-178/DO-254 Certification Costs for New Camera Hardware

End-to-end certification at DO-178C Level A often exceeds USD 2 million per product line and can consume up to 24 months, effectively locking out many startups.[4]ConsuNova, “DO-178C cost drivers,” consunova.com The burden includes exhaustive documentation, software verification, and environmental qualification that only deep-capital incumbents can shoulder. As a result, breakthrough optical concepts take longer to reach commercial airframes, and competitive pricing pressure is muted. This dynamic reinforces the position of tier-one avionics suppliers, further concentrating the aircraft cameras market around a handful of players.

Pilot-Union Privacy Push-Back on Cockpit Video

European and North American pilot associations argue that audio and flight-data recorders provide adequate insight into incidents, warning that continuous video may be misused for disciplinary action. Negotiations have introduced carve-outs such as limited data retention or encryption keys controlled by third-party safety boards, potentially scaling back system complexity and unit pricing. Nonetheless, any protracted labor dispute could stall airline retrofit schedules, dampening near-term revenue cycles for cockpit-camera vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: UAVs Drive Next-Generation Imaging Demand

UAVs are forecasted to register a 12.08% CAGR as militaries and civil operators expand their missions, ranging from border surveillance to parcel delivery. The aircraft cameras market size allocated to UAV payloads is projected to reach USD 9.05 billion by 2031, underpinned by the US Army’s HADES deep-sensing program and similar initiatives in Asia. Despite maturing growth, commercial aviation remains the revenue anchor with a 38.42% share in 2025, thanks to mandatory safety retrofits and widebody linefit commitments. Military aviation continues to procure high-dynamic-range EO/IR turrets for manned ISR platforms. At the same time, business and general aviation operators adopt lightweight interior cameras that feed real-time engine health data into cloud analytics.

UAV adoption shifts the optical design roadmap toward ultralight, low-power assemblies that can survive harsh vibration profiles and high-altitude temperature swings. Suppliers incorporating FPGA-based onboard processing reduce datalink bandwidth, a critical constraint for beyond-line-of-sight (BLOS) missions. Airlines prioritize 4K cabin clarity in manned segments to support facial analytics and in-flight service optimization. Special-mission operators, notably search and rescue (SAR) and medical evacuation (Medevac), pursue dual-sensor packages that combine long-wave IR with visible zoom for all-hours operations, sustaining stable demand even during commercial down cycles.

By Camera Installation Type: External Systems Strengthen Market Leadership

External installations captured 56.75% of the aircraft cameras market share in 2025, buoyed by airline appetite for 360° taxi-aid suites and military demand for gimbal-mounted ISR turrets. Growth through 2031 is projected at 11.03% CAGR, raising external-camera revenues to an estimated USD 32.15 million. While smaller in number, internal cameras are increasingly integrated into predictive maintenance architectures, allowing for automatic visual inspections of landing gear bays and avionics racks during overnight turns.

External housings enable broader fields of view and simplify certification, as they avoid electromagnetic compatibility issues within pressurized cabins. Retrofit opportunities abound because camera pods can be attached to existing hard points without requiring primary structural reinforcement. Conversely, internal installations face cabin-layout constraints and stricter flammability standards. Market participants, therefore, bundle interior sensors with health-monitoring subscriptions, monetizing data rather than unit sales alone.

By Type: Multispectral Dominance, AI-Smart Cameras Accelerate

Multispectral and hyperspectral cameras accounted for 36.88% of the 2025 revenue pool, favored by defense and environmental-monitoring operators that require band-specific analytics. The aircraft cameras market size for this category is expected to surpass USD 19.43 million by 2031 as programs such as Germany’s PEGASUS SIGINT aircraft adopt wideband sensor suites. AI-enabled smart cameras, featuring embedded GPUs and neural accelerators, are growing at the fastest rate, with a 11.52% CAGR, and carving out a share from traditional electro-optical models.

The transition to software-defined architectures enables operators to upgrade capabilities via firmware, prolonging asset life cycles and reducing the total cost of ownership. Infrared sensors maintain a strong foothold in nighttime SAR and military targeting, while 360-degree panoramic units migrate from high-end biz jets to mainstream narrowbodies as pricing falls. Suppliers investing in open-standards middleware enjoy interoperability advantages that resonate with cost-conscious airlines.

By Aircraft Platform: Fixed-Wing Fleet Drives Volume, Hybrids Fuel Incremental Growth

Fixed-wing aircraft held a 62.25% share in 2025, reflecting the vast installed commercial fleet and ongoing surveillance conversions of business jets into ISR roles. Rotary-wing demand centers on airborne law enforcement and offshore energy, where stabilized turrets enable overwater search tasks. Hybrid platforms, encompassing tiltrotors and eVTOL craft, are projected to generate the steepest 10.34% CAGR as urban mobility projects finalize certification pathways.

Fixed-wing linefit packages are increasingly integrating nose-mounted volumetric sensors that support taxi-aid, runway-incursion alerts, and predictive maintenance imaging. eVTOL developers specify distributed camera arrays that serve as both detect-and-avoid systems and passenger-experience enhancers, such as panoramic cabin views. This multi-use philosophy boosts attachment rates beyond legacy crew-only installations, enriching the aircraft camera market opportunity per airframe.

By Sales Channel: Retrofit Momentum Outpaces Linefit Growth

OEM linefit retained 57.40% share in 2025 but is projected to cede relative ground as retrofit CAGRs hit 12.02% through 2031. Delivery delays for new aircraft push airlines to modernize existing jets, accelerating purchase orders for modular interior and exterior vision kits. MRO providers leverage camera maintenance as a new revenue stream, bundling periodic lens cleaning and software update services into hourly cost programs.

Incoming cockpit-video mandates and insurance-related cabin-surveillance requirements catalyze retrofit efforts. Vendors offering drop-in replacements compatible with legacy flight-data buses capture spend without necessitating costly rewiring of the avionics bay. Over time, predictive maintenance subscriptions may eclipse hardware margins, mirroring the software-as-a-service (SaaS) playbooks prevalent in ground-vehicle telematics.

Geography Analysis

North America accounted for 37.95% of 2025 revenue, anchored by US defense ISR budgets and a sizable commercial fleet undergoing safety retrofits. The US Army’s HADES contract pipeline alone could absorb nearly USD 1 billion in sensor purchases over the next decade. Canada’s investment in WESCAM MX-20 systems for P-8A maritime patrol aircraft underscores continued regional appetite for high-end EO/IR payloads. Mexico contributes a moderate but rising demand tied to cross-border security surveillance and low-cost carrier fleet expansions.

The Asia-Pacific region represents the fastest-growing geography, with a 10.31% CAGR outlook. China’s proliferation of indigenous drones spurs the development of local camera manufacturing clusters, despite export-control frictions. India, Japan, and South Korea channel defense offsets into sensor technology transfer, gradually building domestic competence. Commercial carriers from Indonesia to Australia accelerate in-cabin safety upgrades in response to tightening ICAO audit requirements.

Europe maintains steady momentum, leveraging programs such as Germany’s EUR 1.2 billion (USD 1.41 billion) PEGASUS SIGINT fleet and the UK runway-incursion prevention mandates. The French and Italian defense ministries tender multi-sensor turret purchases to modernize their rotary-wing fleets, while regional airlines prioritize 360° taxi-aid kits to reduce ground-damage costs at congested airports. Eastern European demand lags due to budget constraints, and sanctions limit Russian access to Western camera technology, prompting the substitution of lower-spectral-resolution domestic optics.

Competitive Landscape

Market concentration is moderate, with the top five suppliers accounting for a significant global revenue share. Collins Aerospace, Thales, and L3Harris leverage long-term supplier-furnished equipment contracts and deep certification pedigrees to secure repeat linefit awards. Teledyne's acquisition spree integrates sensor fabs with system-level integration, enabling end-to-end vertical control that appeals to defense primes. Honeywell and Curtiss-Wright emphasize edge-computing gateways that fuse multiple camera feeds, differentiating themselves on the depth of data analytics rather than relying solely on optics.

Specialized challengers, such as Trakka Systems and KID-Systeme, target high-growth niches, SAR and cabin Wi-Fi camera networks, offering lighter form factors and rapid product refresh cycles. Software-defined architectures lower airlines' switching costs, allowing smaller vendors to penetrate legacy fleets via retrofit channels.

Strategic collaboration defines recent activity: L3Harris combined imaging payloads with Air Tractor's rugged airframes to win the US Special Operations Armed Overwatch award. HENSOLDT partners with Lufthansa Technik to integrate PEGASUS sensor suites, minimizing certification risk through early alignment with civil MRO experts. These alliances illustrate how domain knowledge and integration bandwidth now rival pure optical performance as determinants of contract success.

Aircraft Cameras Industry Leaders

Collins Aerospace (RTX Corporation)

Teledyne Technologies Incorporated

Leonardo S.p.A.

HENSOLDT AG

LATECOERE S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: L3Harris won a Canadian contract to supply 16 WESCAM MX-20 EO/IR systems for the Royal Canadian Air Force's P-8A Poseidon aircraft, standardizing ISR sensors across both manned and unmanned fleets.

- March 2025: Teledyne FLIR OEM introduced radiometric versions of its Boson+ thermal and Hadron 640R+ dual thermal-visible camera modules. These new offerings deliver pixel-level temperature measurement capabilities, broadening their application across industries such as unmanned ground vehicles (UGVs), unmanned aircraft systems (UAS), security, handheld devices, and artificial intelligence (AI) solutions.

Global Aircraft Cameras Market Report Scope

Aircraft cameras enhance pilots' situational awareness by providing views of the aircraft's interior and surroundings. This study focuses on EO/IR cameras installed on military aircraft, excluding those used on UAVs.

The aircraft camera market is segmented by application, type, and geography. By application, the market is segmented into commercial aircraft and military aircraft. By type, the market is segmented into internal cameras and external cameras. The report also covers the market sizes and forecasts for the aircraft cameras market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Commercial Aviation |

| Military Aviation |

| Business and General Aviation |

| Unmanned Aerial Vehicles (UAVs) |

| Special Mission Aircraft (ISR, SAR, Medevac) |

| Internal Cameras |

| External Cameras |

| Electro-Optical (Visible) |

| Infrared (LWIR and MWIR) |

| Night-Vision/Low-Light |

| Multispectral/Hyperspectral |

| 360-Degree and Panoramic |

| AI-Enabled Smart Cameras |

| Fixed-Wing |

| Rotary-Wing |

| Hybrid |

| OEM Linefit |

| Retrofit/Aftermarket/MRO |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Commercial Aviation | ||

| Military Aviation | |||

| Business and General Aviation | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Special Mission Aircraft (ISR, SAR, Medevac) | |||

| By Camera Installation Type | Internal Cameras | ||

| External Cameras | |||

| By Type | Electro-Optical (Visible) | ||

| Infrared (LWIR and MWIR) | |||

| Night-Vision/Low-Light | |||

| Multispectral/Hyperspectral | |||

| 360-Degree and Panoramic | |||

| AI-Enabled Smart Cameras | |||

| By Aircraft Platform | Fixed-Wing | ||

| Rotary-Wing | |||

| Hybrid | |||

| By Sales Channel | OEM Linefit | ||

| Retrofit/Aftermarket/MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft cameras market in 2026?

The market is valued at USD 32.9 million in 2026 and is projected to grow to USD 53.51 million by 2031.

Which application segment is expanding the fastest?

Unmanned aerial vehicles (UAVs) lead growth with a forecasted 12.08% CAGR through 2031.

What region offers the strongest demand outlook?

Asia-Pacific shows the highest regional CAGR at 10.31% owing to drone expansion and fleet modernization.

Why are airlines retrofitting 4K cabin cameras?

Tighter safety protocols and insurance requirements are pushing carriers to adopt high-resolution systems that enable facial recognition and behavioral analytics.

How will new cockpit-video mandates affect suppliers?

The EASA/FAA mandate starting 2028 is expected to trigger a multi-year retrofit wave across about 6,000 aircraft, benefiting vendors with certified, privacy-compliant solutions.

Page last updated on: