Airport Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 5.25 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

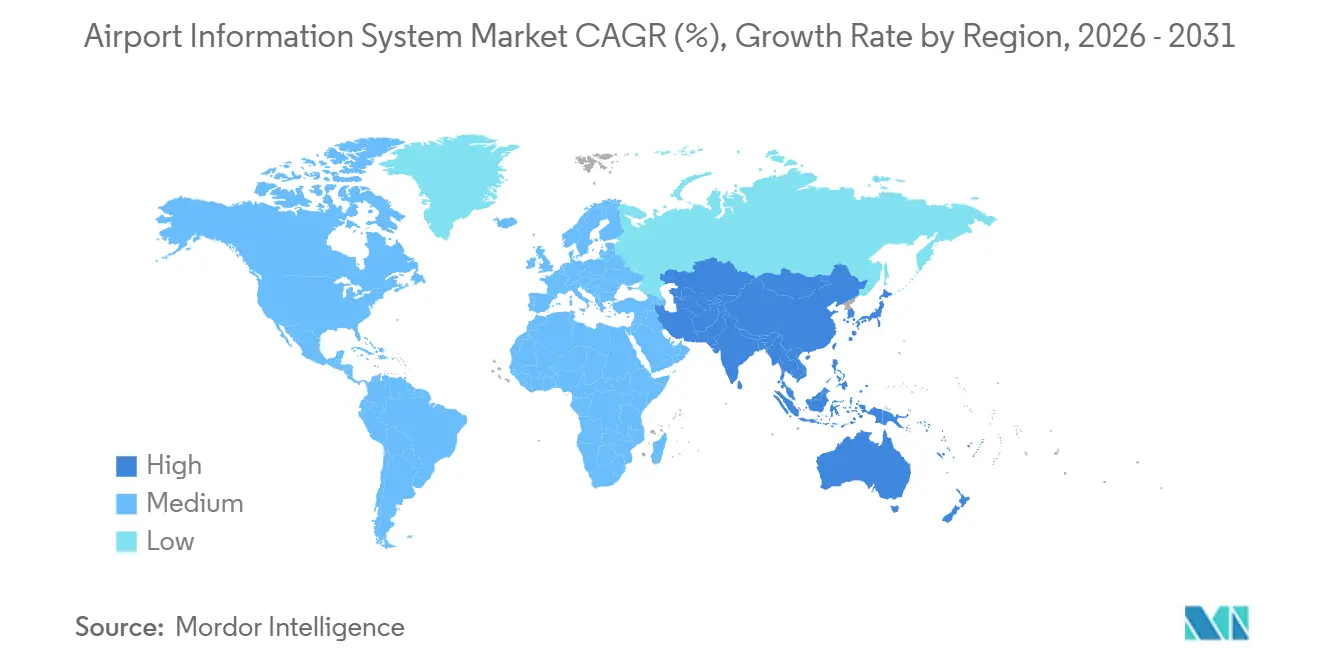

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

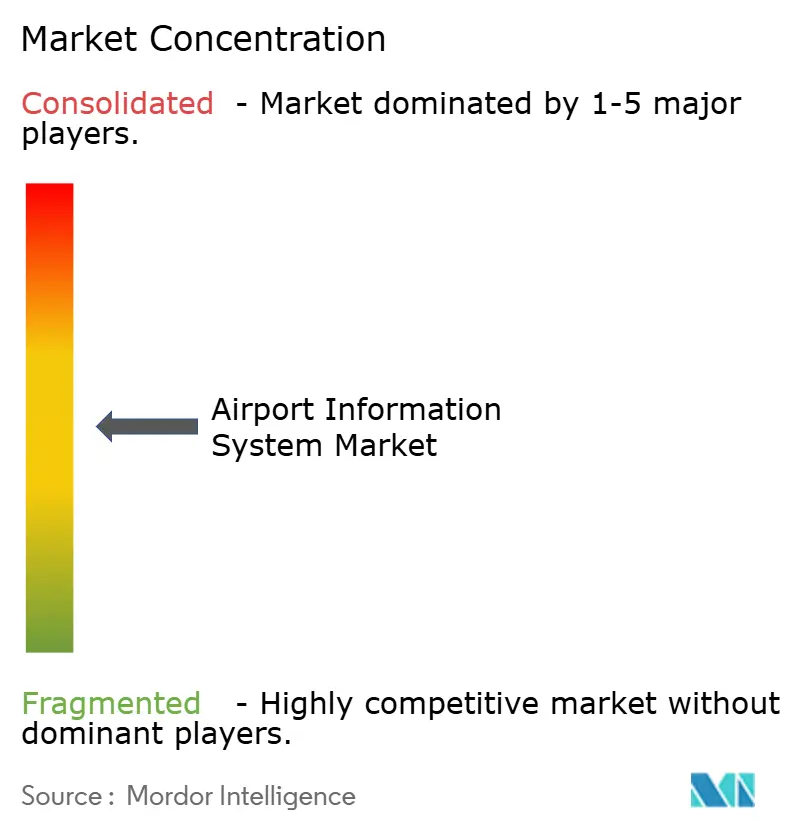

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Airport Information System Market Analysis by Mordor Intelligence

The airport information system market size is expected to grow from USD 4.15 billion in 2025 to USD 4.36 billion in 2026 and is forecasted to reach USD 5.25 billion by 2031 at a 3.82% CAGR over 2026-2031. Growth is supported by a steady recovery in global passenger volumes, continued investments in terminal modernization, and increasing adoption of biometric self-service technologies. However, overall growth remains moderate, as many Class A airports continue to rely on capital-intensive, on-premises architectures with 7-year refresh cycles.

Security applications account for the largest share of spending, driven by regulatory mandates for facial-recognition checks at exit gates. Terminal-side systems are also benefiting from airlines transitioning to common-use departure control systems (DCS), which distribute hardware costs across multiple carriers. Cloud-native deployments are the fastest-growing segment, with Class C airports opting for flexible subscription-based pricing models rather than making significant upfront investments.

Competitive dynamics are intensifying as established suite vendors unbundle their offerings into API-first microservices, creating opportunities for niche players specializing in areas such as resource optimization, predictive maintenance, and sustainability analytics.

Key Report Takeaways

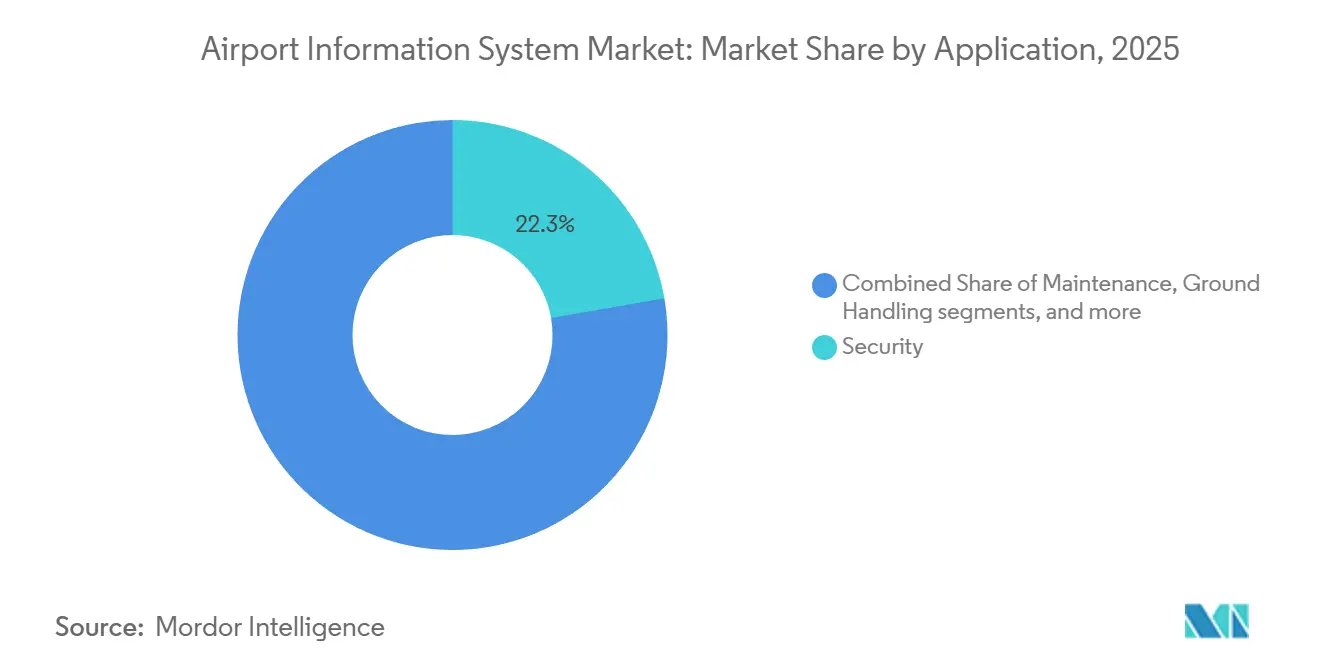

- By application, the security segment accounted for 22.27% of revenue in 2025 and is projected to grow at a CAGR of 5.83% through 2031.

- By system area, terminal-side platforms contributed 53.78% of revenue in 2025, while airside solutions are expected to achieve the highest CAGR of 6.22% during the forecast period.

- By deployment mode, on-premise solutions held 53.15% of the airport information system market share in 2025, whereas cloud/SaaS solutions are anticipated to grow at a CAGR of 7.98% through 2031.

- By airport size, Class C facilities represented 18% of spending in 2025 and are projected to record the highest CAGR of 5.13%, surpassing Class A hubs, which are expected to grow at a CAGR of 3.60%.

- By geography, North America led the market with 29.85% of revenue in 2025, while Asia-Pacific is forecasted to grow at the fastest CAGR of 5.31% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airport Information System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained recovery and growth in global air passenger traffic | +1.2% | Global; APAC spearheads recovery | Medium term (2–4 years) |

| Accelerated airport modernization and expansion programs | +0.9% | APAC and MEA | Long term (≥ 4 years) |

| Passenger-experience focus driving self-service and biometrics | +0.8% | North America and EU first adopters | Short term (≤ 2 years) |

| Deployment of 5G/private networks enabling real-time analytics | +0.6% | North America and APAC | Medium term (2–4 years) |

| Airport Collaborative Decision-Making (A-CDM) adoption surge | +0.5% | Europe leads; APAC and North America follow | Medium term (2–4 years) |

| Health-driven zero-touch processing mandates | +0.4% | Global regulatory push | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustained Recovery in Global Air Passenger Traffic

Passenger kilometers surpassed 2019 levels in Q1 2024, with IATA reporting October 2025 traffic as 6.6% higher than the previous year, indicating a sustained recovery in demand. The increasing traffic volumes have highlighted pre-pandemic capacity constraints at major hubs, driving IT investments toward platforms that enhance throughput without requiring additional physical gates. The Asia-Pacific region's 5.31% CAGR reflects the rapid growth of low-cost carriers, which favor common-use infrastructure to reduce turnaround times. Biometric single-token pilots have reduced processing times by 40%, increasing gate capacity and prompting airports to reconfigure retail spaces to accommodate higher-yield concessions. Airlines consolidating slots at mega-hubs are concentrating spending in these locations, while secondary cities in India, China, and the Gulf are bypassing traditional systems by adopting cloud-native Airport Operational Database (AODB) solutions from the outset.

Accelerated Airport Modernization and Expansion Programs

The US Bipartisan Infrastructure Law allocates USD 25 billion for airport upgrades, including USD 5 billion specifically for terminal IT, driving a surge in procurement activities at regional airports. In parallel, Saudi Arabia's King Salman International Airport aims to accommodate 185 million passengers by 2030, incorporating AI-driven slot optimization during its design phase.[1]BBC News. "Seattle-Tacoma Airport Ransomware Attack Recovery." bbc.com In Europe, grant funding is tied to carbon-reporting capabilities, compelling operators to integrate energy-monitoring systems into AODB workflows. These initiatives collectively extend the project pipeline and broaden demand beyond traditional Class A buyers. Vendors offering pre-configured ESG dashboards or digital twin simulators gain a competitive edge as authorities prioritize off-the-shelf compliance solutions to reduce consulting expenses.

Passenger-Experience Focus on Self-Service and Biometrics

The Transportation Security Administration (TSA) deployed 2,054 CAT-2 units across 231 US airports by mid-2024, reducing the average screening time by 30 seconds. This efficiency allowed airports handling 100,000 daily passengers to reallocate approximately 104 full-time officers. The freed-up space in airports has been repurposed into boutique stores, contributing to an 18% increase in non-aeronautical revenue in Europe during 2024. Additionally, the use of common-use kiosks has diminished airline brand touchpoints, shifting competitive efforts toward mobile applications that offer personalized services. Biometric exit checks, which have already processed 807 million travelers for US Customs and Border Protection (CBP), have reduced impostor incidents and enhanced border compliance. As biometric technology becomes more widely adopted, refusal queues have decreased, and operators have improved staff scheduling using real-time occupancy dashboards.

Airport Collaborative Decision-Making (A-CDM) Adoption Surge

In 2025, Australia aligned with Europe’s 34 compliant hubs, enabling shared turnaround milestones among airlines, ground handlers, and air traffic control (ATC). Early identification of delays allows carriers to re-route aircraft and adjust crew schedules, minimizing cascading disruptions. However, data governance remains a challenge, as airlines are reluctant to disclose proprietary operational metrics. Airports that appoint neutral data trustees experience higher participation rates and improved slot adherence, demonstrating that governance design can be as impactful as technology in delivering return on investment (ROI). Vendors offering modular interfaces that anonymize data feeds without compromising accuracy are gaining acceptance at privacy-focused European airports.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant capital investment and integration complexity | −0.7% | Global; heavier on smaller airports | Long term (≥ 4 years) |

| Rising concerns over cybersecurity vulnerabilities and data privacy | −0.5% | EU and North America with strict rules | Medium term (2–4 years) |

| Proprietary legacy systems limiting cross-platform interoperability | −0.4% | North America and Europe | Long term (≥ 4 years) |

| Shortage of advanced analytics and IT expertise among airport operators | −0.3% | Developing regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Significant Capital Investment and Integration Complexity

Large airport hubs typically allocate approximately USD 50 million to major IT overhauls, with migration timelines of 24 to 36 months to ensure systems remain operational during the transition. Additionally, hardware refresh cycles, which occur every 7 years, contribute to the financial burden by turning capital projects into ongoing operating expenses. Smaller airports face significantly higher per-passenger costs compared to Class A facilities, but they often lack equivalent revenue streams. As a result, they frequently adopt SaaS solutions that simplify complexity through per-transaction fees. Integration timelines further discourage some public-sector owners from approving modernization projects, even when return-on-investment (ROI) models are favorable.

Rising Concerns Over Cybersecurity Vulnerabilities and Data Privacy

In August 2024, a ransomware attack at Seattle-Tacoma International Airport disrupted baggage handling for three days, resulting in USD 12 million in recovery costs and lost revenue.[2]International Civil Aviation Organization (ICAO). "Global Air Traffic Recovery Update Q1 2024." icao.int Similarly, Delta Airlines experienced a CrowdStrike-related outage in July 2024, grounding 7,000 flights and highlighting how tightly integrated systems can exacerbate the impact of misconfigurations. European operators face additional challenges under the GDPR, which mandates anonymizing passenger data within 72 hours, in conflict with airlines' preference for 90-day data retention for revenue analytics. To mitigate risks, airports are increasingly implementing network segmentation and air-gapped operational systems, which raise project budgets by 10–15% but effectively reduce the potential impact of breaches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Security Commands Spend and Growth

Security applications accounted for 22.27% of revenue in 2025 and are projected to grow at 5.83% through 2031, surpassing all other application categories. The growth is driven by biometric exit verification, integrated into existing access-control systems and mandated by the US CBP for all international departures by 2026. By mid-2025, CBP systems processed 807 million travelers and detected 2,229 impostors, demonstrating operational maturity and reinforcing the business case for facial-recognition gates. Ground handling applications, which include baggage tracking and ramp management, account for 18% of spending but grow at a slower rate of 3.1%. This is due to the commoditization of RFID tag readers and airlines' reluctance to share real-time bag location data with competitors.

Finance and operations applications, such as revenue-management interfaces and slot accounting, account for 16% of the airport information system market. However, they face margin pressures from cloud-native ERP systems offered by Oracle and SAP, which are challenging aviation-specific vendors. Passenger information systems, including Flight Information Display Systems (FIDS) and mobile app backends, hold a 19% market share and are growing at 4.2%. This growth is supported by the transition from static displays to dynamic content delivery via Bluetooth beacons. Maintenance applications, the smallest segment at 15%, are undergoing disruption as predictive analytics shift from niche add-ons to core functionalities within AODB platforms. This evolution compresses standalone maintenance software revenue while embedding these capabilities into broader systems.

The US TSA operates 2,054 CAT-2 units across 231 airports, processing approximately 250 passengers per hour, which is double the throughput of manual checks. These systems identify discrepancies that human screeners miss in 8% of cases. Security checkpoints generate timestamped flow records that, when integrated with gate-assignment data, enable terminal operators to dynamically allocate retail staff and adjust concession hours. This capability increased non-aeronautical revenue per passenger by 12% at major European hubs in 2024. Additionally, the European Union's (EU's) Entry/Exit System, which requires biometric registration for non-EU nationals at all Schengen borders by the end of 2024, has prompted airports to upgrade their DCS platforms to support new data-exchange protocols. This compliance-driven refresh cycle is expected to sustain the growth of security applications through 2028.

By System Area: Terminal-Side Platforms Dominate Airside Stacks

Terminal-side systems accounted for 53.78% of revenue in 2025 and are projected to grow at 6.22% through 2031. This dominance reflects the concentration of passenger-facing touchpoints in departure and arrival halls. In contrast, airside systems, which include FIDS, AODB, Resource Management Systems (RMS), and Air Traffic Management (ATM) integration, held the remaining 46.22% of revenue and are expected to grow at a slower rate of 3.1%. This disparity is attributed to the maturity of flight information displays and the slower refresh cycles of operational databases.

Within terminal-side systems, DCS platforms are transitioning from airline-owned infrastructure to airport-provided common-use environments. This shift allows hardware costs to be distributed across multiple carriers and facilitates dynamic gate reassignment. For example, SITA's Flex platform, deployed at over 500 airports, illustrates this model. A single kiosk array serves 15 to 20 airlines, reducing per-carrier capital expenditures by 60% while increasing gate utilization by 18%. Additionally, Common Use Passenger Processing Systems (CUPPS) and Common Use Terminal Equipment (CUTE) interfaces are converging toward cloud-native APIs. This transition eliminates the need for on-site servers, leading to an annual reduction of 8–10% in terminal-side hardware revenue, even as software subscription revenues increase. Self-service kiosks and digital signage are the fastest-growing terminal-side subsegment, with a 7.40% CAGR. These technologies are driven by the dual objectives of reducing labor costs and enhancing the passenger experience.

Airports are increasingly replacing static flight information displays with 4K LED panels that can deliver personalized gate directions via QR code scanning. This innovation reduced misconnection rates by 14% at Amsterdam Schiphol in 2024. However, airside systems face different growth dynamics. FIDS technology has reached a plateau due to the long lifespan of LED panels (10 to 12 years) and the standardized nature of information architecture, which limits differentiation opportunities.

Meanwhile, AODB platforms, which serve as the operational backbone linking flight schedules to resource allocation, are incorporating machine-learning modules. These modules can predict turnaround delays 45 minutes earlier than traditional rule-based systems. However, the adoption of these advanced features remains concentrated at Class A airports, which typically have dedicated data science teams. RMS platforms that manage gate, stand, and ground service equipment allocation present a significant growth opportunity. Currently, fewer than 30% of airports utilize automated resource optimization, relying instead on manual dispatching. This results in 20–25% of assets remaining idle during peak hours, highlighting the potential for efficiency improvements through automation.

By Deployment Mode: Cloud Gains Yet On-Premise Persists

On-premises deployments accounted for 53.15% of spending in 2025, while the cloud/SaaS segment was the only segment to demonstrate near-double-digit growth at 7.98%. This divergence is influenced by airport size and data-sovereignty priorities. Class A airports, particularly in North America and Europe, prefer on-premise architectures to maintain control over passenger data and mitigate latency risks during network outages. Additionally, hosting software internally provides operators with leverage during vendor negotiations, enabling them to credibly threaten provider switches, which can result in a 15–20% reduction in maintenance fees.

Cloud deployments are more attractive to Class C and D airports, which often lack in-house IT staff and favor predictable per-transaction pricing over significant capital expenditures. For instance, Amadeus's Altéa Suite, offered as a SaaS subscription, charges USD 0.08 to USD 0.12 per passenger processed. This model aligns costs with revenue, eliminating the need for upfront hardware investments. Cloud adoption is accelerating in the Asia-Pacific region, where greenfield airports are integrating SaaS platforms from the outset. Navi Mumbai International Airport in India, set to open in 2025, has chosen cloud-native AODB and DCS systems that scale elastically with passenger growth, avoiding the over-provisioning issues that burden legacy hubs with underutilized server capacity.

Security concerns continue to pose challenges. GDPR's data-residency requirements mandate that EU airports use cloud providers with in-region data centers, which fragments vendor selection and increases costs by 10–15% compared to global hyperscale platforms. The Middle East offers a hybrid approach: the Dubai International Airport operates a private cloud that integrates data across its two terminals and the under-construction Al Maktoum International Airport. This approach combines the scalability of cloud architecture with the control of on-premise hosting. Such hybrid models are likely to gain popularity as airports aim to future-proof their infrastructure while retaining operational autonomy from hyperscale vendors.

By Airport Size: Class C Facilities Outpace Major Hubs

Class A airports, which handle over 25 million passengers annually, accounted for 39.87% of investments in 2025. However, Class C airports, serving 2.5 million to 10 million passengers, are projected to grow at a faster rate of 5.13%, surpassing the growth of larger hubs. This trend is attributed to the adoption of turnkey SaaS platforms in secondary cities, which eliminate the integration challenges associated with legacy infrastructure. Class B airports, handling 10 million to 25 million passengers, hold a 28% market share and are expected to grow at 4.1%. Meanwhile, Class D airports, serving fewer than 2.5 million passengers, represent 12% of the market and are projected to grow at 3.8%, constrained by limited budgets and the lack of economies of scale.

India's Noida International Airport, which aims to handle 12 million passengers upon opening, highlights the growth potential of Class C airports. By implementing Siemens' cloud-based baggage-handling system and NEC's biometric boarding platform, the airport avoids the middleware layers that typically extend integration timelines by 18 to 24 months at established hubs, underscoring the advantages of greenfield projects in secondary cities.

Class A airports face the "innovator's dilemma." Their existing on-premise systems generate sufficient revenue to justify incremental upgrades. Still, the cumulative cost of maintaining legacy interfaces often exceeds the total IT budget of a greenfield Class C facility. This creates a competitive divide in the market.

The competitive landscape is increasingly bifurcated. Vendors such as SITA and Amadeus maintain dominance at major hubs through long-term service contracts and high switching costs. In contrast, agile SaaS providers like Vision Box and Materna IPS are capturing a significant share at secondary airports, where deployment speed is prioritized over extensive customization.

Geography Analysis

North America accounted for 29.85% of revenue in 2025, supported by the FAA's USD 25 billion allocation under the Bipartisan Infrastructure Law and the presence of major Class A hubs such as Atlanta, Dallas, Chicago, and Los Angeles. These hubs drive per-airport IT expenditures exceeding USD 100 million. In contrast, Asia-Pacific is projected to lead growth at a rate of 5.31%, driven by significant projects such as China's Beijing Daxing expansion, India's Navi Mumbai and Noida airports, and the Middle East's King Salman International Airport in Riyadh, which is designed to accommodate 185 million passengers annually by 2030. Europe captures 26% of spending and grows at 3.90%, influenced by the EU's sustainability mandates and the maturity of A-CDM networks, which limit opportunities for transformative innovation.

Favorable demographic trends and robust policy support are bolstering growth in the Asia-Pacific region. China's Civil Aviation Administration has allocated USD 18 billion for airport digitalization between 2024 and 2026, with a focus on AODB and A-CDM deployments in tier-2 cities to alleviate congestion at major hubs, such as Beijing and Shanghai. Similarly, India's Airports Authority has announced USD 12 billion in infrastructure investments through 2028, with 40% dedicated to IT systems for new and expanded facilities. This shift in focus has strategic implications for vendors, as companies traditionally targeting North American and European markets are forming local partnerships in the Asia-Pacific region to align with procurement preferences that favor domestic suppliers. For instance, NEC's facial-recognition systems, implemented at Tokyo Narita and Osaka Kansai airports, leverage the company's local expertise to secure design-build contracts that are less accessible to foreign competitors.

Europe's growth trajectory is shaped by its regulatory framework. GDPR's data-residency and consent requirements extend biometric-system deployment timelines by 6 to 9 months as airports negotiate data-processing agreements with airlines and border authorities. Additionally, the EU's Entry/Exit System, which mandates biometric registration for non-EU nationals, has driven airports to upgrade DCS platforms to meet new compliance requirements. This compliance-driven refresh cycle sustained investments in 2024 and 2025 but is expected to taper by 2027 as the rollout concludes.

The Middle East's hub-and-spoke model focuses IT spending on a few large-scale airports. For example, Dubai's DXB, which handled 87 million passengers in 2024, operates a private cloud that integrates data across terminals and connects with Emirates' reservation system. This high level of customization justifies its USD 200 million IT budget, reflecting the region's emphasis on centralized, large-scale infrastructure investments.

Regulatory Landscape

The airport information system market is shaped by safety and operational standards set at the global level by the International Civil Aviation Organization (ICAO) through Standards and Recommended Practices (SARPs), alongside national and regional regulators such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA). ICAO Annex 14, Volume 1 updates under Amendment 18 introduce new and revised provisions spanning aerodrome design, visual aids, apron management, and ground handling with staged applicability, including 27 November 2025 and 26 November 2026 milestones that influence when airports prioritize upgrades to apron, turnaround, and ground handling information workflows.

In North America, FAA airport compliance and funding frameworks shape what airport sponsors can procure and how they document performance and compliance, with updated AIP eligibility guidance increasingly recognizing digital systems (for example, advanced digital construction management systems and cybersecurity controls) within airport capital programs. In Europe, EASA refreshed its Easy Access Rules for Aerodromes in March 2026, consolidating requirements and incorporating ground handling-related provisions aligned to Commission Delegated Regulation (EU) 2025/21, adding another compliance driver for airports to formalize data governance, operating procedures, and auditable system records across terminal-side and airside operations.

Value Chain Analysis

The airport information system value chain starts with standards, architecture, and core platform development for operational backbones such as AODB, A-CDM, and airport operations centers, then extends to specialist modules (biometrics, passenger processing, resource management, baggage and ramp systems, and analytics). Vendors and subsystem providers integrate with airport stakeholders including airlines, ground handlers, border agencies, and air navigation service providers, with interoperability requirements and data-sharing agreements often becoming decisive inputs alongside software functionality.

Procurement typically moves from airport planning and program management into solution design, systems integration, deployment, and long-term managed services, with the Master Systems Integrator role expanding on complex modernization programs that touch dozens of systems. Recent in-market examples show this integration-led model: DXC Technology was selected as master systems integrator for Perth Airport to coordinate design, integration, and testing across more than 70 IT and operational systems for a new terminal program, while large hub upgrades such as Chicago O'Hare have included replacement of legacy AODB and resource management capabilities through platform deployments. Downstream, operations and support are increasingly delivered via cloud-managed connectivity and platform operations, reflecting the shift from periodic hardware refresh projects toward continuous updates, cybersecurity hardening, and performance optimization across the airport ecosystem.

Competitive Landscape

The airport information system market is moderately fragmented, with the top five vendors, SITA, Amadeus, Honeywell, Thales, and Indra, collectively accounting for approximately 38% of the market share. This leaves significant opportunities for specialized players focusing on areas such as biometric gateways, resource optimization, and Airport Collaborative Decision Making (A-CDM) orchestration. The market has seen a strategic shift from monolithic suite sales to API-first microservices that integrate with existing systems, addressing concerns from procurement committees about the risks associated with complete system overhauls. For instance, SITA's Flex platform, implemented in over 500 airports, demonstrates this modular approach. Airlines can subscribe to individual modules, such as DCS, baggage tracking, and biometric solutions, reducing upfront capital expenditures while ensuring recurring revenue streams for the vendor.[3]SITA, “Heathrow extends network contract,” sita.aero

Amadeus's Altéa Suite, offered as a SaaS subscription, charges between USD 0.08 and USD 0.12 per passenger processed. This model aligns vendor revenue with airport throughput while eliminating the need for upfront hardware investments. The highest competitive intensity is observed in terminal-side systems, where the commoditization of self-service kiosks and digital signage has led to a 15–20% reduction in hardware margins since 2022. To maintain profitability, vendors are increasingly bundling software subscriptions and managed services with their hardware offerings. Additionally, untapped opportunities exist in predictive maintenance for airside assets, where data streams from AODB and RMS remain underutilized. Sustainability analytics is another growth area, driven by EU airports' compliance with Scope 3 emissions disclosure requirements under the Corporate Sustainability Reporting Directive.

Vision Box and NEC are integrating facial recognition modules into existing DCS platforms to create seamless travel corridors that connect curb-to-gate touchpoints and reduce passenger processing times by up to 40%. Similarly, ADB SAFEGATE's Advanced Visual Docking Guidance Systems, which utilize laser sensors to guide aircraft to precise gate positions, are being integrated with AODB platforms. This integration automates stand allocation and reduces aircraft turnaround times by 8-12 minutes. Emerging disruptors, such as INFORM's OptiFlight module, are leveraging reinforcement learning for gate assignment, achieving 12–15% improvements in resource utilization compared to traditional rule-based systems. These capabilities are particularly appealing to Class A airports looking to optimize resources and delay costly terminal expansions.

Airport Information System Industry Leaders

-

SITA N.V.

-

Amadeus IT Group, S.A.

-

THALES

-

Indra Sistemas, S.A.

-

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major near-term opportunity sits in compliance-driven refresh cycles for security, border processing, and ground handling coordination, where airports need systems that can produce auditable records, enforce role-based access, and integrate biometric and operational data without expanding physical footprints. Concrete program anchors include the US CBP push for biometric exit verification for international departures by 2026, the EU Entry/Exit System requirements at Schengen borders, and the staged ICAO Annex 14 applicability dates that elevate apron and ground handling process digitization ahead of the November 2026 milestone.

Modernization megaprojects and greenfield build-outs are expanding whitespace for cloud-native AODB, A-CDM, and resource optimization stacks, particularly where expansion planning embeds digital operations from the design phase. Examples include Dubai's Al Maktoum International Airport expansion program, which announced 55 billion AED of contracts to be awarded by end of 2026 for a first phase targeting 260 million passengers annually by 2032, and large-scale airport upgrades in Africa such as Kenya Airports Authority awarding a USD 1.2 billion modernization contract for Jomo Kenyatta International Airport in June 2026. In parallel, industry-driven technology transitions such as IATA's CUSS 2 migration (with CUSS 1.5 support ending 31 December 2025) create an actionable replacement cycle for kiosks and common-use passenger processing, accelerating demand for API-first, standards-aligned platforms that reduce integration time and vendor lock-in.

Recent Industry Developments

- July 2026: Western Sydney International Airport announced a partnership with Freightquip to operate Australia's first airport-wide ground support equipment (GSE) pooling program, starting in October 2026. The move centralizes allocation and utilization of shared assets, increasing the need for real-time resource tracking, dispatch, and operational data integration that ties into broader airport operations systems.

- April 2026: SITA launched the SITA Campus Network, a managed LAN/WLAN service for airport connectivity powered by HPE Aruba Networking. By productizing the airport network layer as a managed service, the launch supports always-on data exchange for AODB, A-CDM, and passenger processing applications while lowering the operational burden on airport IT teams.

- January 2025: Navi Mumbai International Airport awarded NEC Corporation a USD 45 million contract to implement an end-to-end biometric boarding system integrated with India's DigiYatra platform. The contract strengthens the business case for single-token passenger journeys and increases demand for interoperable interfaces between identity, departure control, and terminal operations systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the airport information system market is defined as revenues generated from airport-specific software and integrated hardware used to collect, process, and share real-time operational and passenger information across airside and terminal-side functions.

Scope exclusions: This sizing excludes stand-alone air-traffic-control radars, baggage conveyor hardware, and generic enterprise IT platforms that are not designed for airport operations.

Segmentation Overview

-

By Application

- Maintenance

- Ground Handling

- Finance and Operations

- Security

- Passenger Information

-

By System Area

-

Airside Systems

- Flight Information Display Systems (FIDS)

- Airport Operations Database (AODB)

- Resource Management Systems (RMS)

- Air Traffic Management (ATM) Integration

-

Terminal-Side Systems

- Departure Control Systems (DCS)

- Common-Use Passenger Processing (CUPPS/CUTE)

- Self-Service Kiosks and Digital Signage

-

Airside Systems

-

By Deployment Mode

- On-premise

- Cloud/SaaS

-

By Airport Size

- Class A

- Class B

- Class C

- Class D

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research began by mapping what airports typically classify as airport information systems, so adjacent airport technology categories do not get mixed into the same revenue pool. To anchor demand and operating context, we referenced public sources such as ICAO air transport statistics, IATA passenger and airline indicators, Airports Council International (ACI) airport operations publications, FAA aviation activity datasets, and Eurostat transport and mobility series.

We also reviewed airport authority procurement portals, public tender notices, and regulator or government infrastructure updates to understand rollout timing and upgrade triggers. Company annual reports, investor presentations, association websites, and reputable aviation and transportation press were used to cross-check module scope, deployment models, and typical contract structures. Then we used selective paid subscriptions for company financials and intelligence, and for general news and financials, to validate revenue exposure and the geographic mix. The desk research sources listed here are illustrative only, and many other public documents were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were held with airport IT leaders, operations teams, system integrators, and solution specialists to clarify what airports buy as integrated airport information system programs versus what is procured separately. These inputs helped validate adoption by airport class, common module bundles (such as FIDS and resource management), and realistic pricing and renewal behavior across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | APAC: 50% |

| Mid tier: 52% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 19% | Managers: 43% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach. Passenger and aircraft movement indicators were translated into expected system deployments by airport class and by core operational workflows. Once the demand pool was established, selective bottom-up approximations were used, including sampled supplier revenue checks, typical module attach rates, and ASP times volume estimates from procurement discussions. These checks were then used to adjust totals where gaps appeared.

Inputs used in the model (illustrative, not exhaustive) included passenger throughput by region, number of commercial airports by size category, terminal expansion and modernization timelines, the share of deployments shifting to cloud/SaaS, and common upgrade cycles for flight and passenger information platforms. For forecasting, scenario analysis was applied, using base, conservative, and aggressive paths tied to traffic growth, capex flexibility, and implementation lead times. The model was then tuned using consensus ranges shared in expert calls. Where a bottom-up check had missing company detail, peer benchmarks per airport class were applied, and the result was re-checked against tender volume signals and typical project durations.

Data Validation & Update Cycle

Outputs were triangulated against independent signals such as airport capex announcements, tender volumes, and installed-base replacement cycles, and then checked for currency timing and regional outliers. When a region showed a break from the expected linkage between traffic and spending, we reviewed the assumptions and re-contacted respondents to confirm whether it reflected a one-off event or a lasting change.

Before sign-off, the model goes through multi-step analyst reviews that include variance checks versus historical growth, pricing sanity checks, and consistency tests across airside and terminal-side application totals. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Airport Information System Market Size Measured Against Other Published Estimates

Published market sizes for airport information systems often do not align because different studies count different product bundles, start from different base years, and apply different pricing and currency timing assumptions. Differences also show up when one estimate is more sensitive to procurement cycles and implementation timing, while another leans more on broad traffic growth patterns.

Standalone air-traffic-control radars sit outside Mordor Intelligence's scope. That exclusion alone can widen the gap when other estimates bundle ATC equipment and wider airport technology into the same total. The spread also comes from whether baggage handling is counted as hardware-heavy systems or software-led platforms, how cloud subscriptions are annualized, and whether upgrade cycles are assumed to shorten across small and mid-sized airports without primary validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.36 B (2026) | |

| Trade Publisher A | USD 3.97 B (2024) | Uses an earlier base year and often reports factory-gate values across a wider list of airport systems, which can compress service-heavy revenue recognition versus deployment-based rollups. |

| Industry Research Outlet B | USD 4.24 B (2024) | Typically includes a broader bundle around airport information platforms and assumes faster monetization of cloud modules, which can lift totals when hardware and software are not separated consistently. |

Across the three figures, the differences mostly come from what is included in the system stack and how revenues are timed between one-time deployments and recurring contracts. By keeping inputs tied to airport traffic, upgrade cycles, deployment mix, and procurement signals, the sizing is easier to trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is driving the faster growth of cloud/SaaS deployments compared to on-premise systems?

Lower upfront cost, pay-per-passenger pricing, greenfield projects in Asia-Pacific, and vendor-managed cybersecurity push cloud/SaaS to a 7.98% CAGR.

Why do Class C airports exhibit faster growth than Class A hubs despite handling fewer passengers?

Turnkey SaaS lets Class C sites skip 18–24-month integrations and hefty middleware fees, lifting their CAGR to 5.13% versus 3.6% for Class A.

How are cybersecurity incidents reshaping procurement priorities?

High-profile ransomware and outage losses make air-gapped networks and built-in incident response mandatory, adding 10–15% to project budgets.

What explains the dominance of terminal-side systems over airside platforms in revenue share?

Passenger touchpoints refresh every 5–7 years, driving spend, while airside FIDS and AODB age 10-plus years and face commoditization.

How is the EU's Entry/Exit System mandate influencing biometric-system deployments?

Compliance forces DCS upgrades and large kiosk orders but raises costs 10–15% due to EU data-residency rules and longer procurement cycles.

What white-space opportunities exist for new entrants?

Predictive maintenance, Scope 3 emissions analytics, and ultra-low-cost SaaS for Class D airports remain largely untapped.

Page last updated on: