Airport Scanners Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

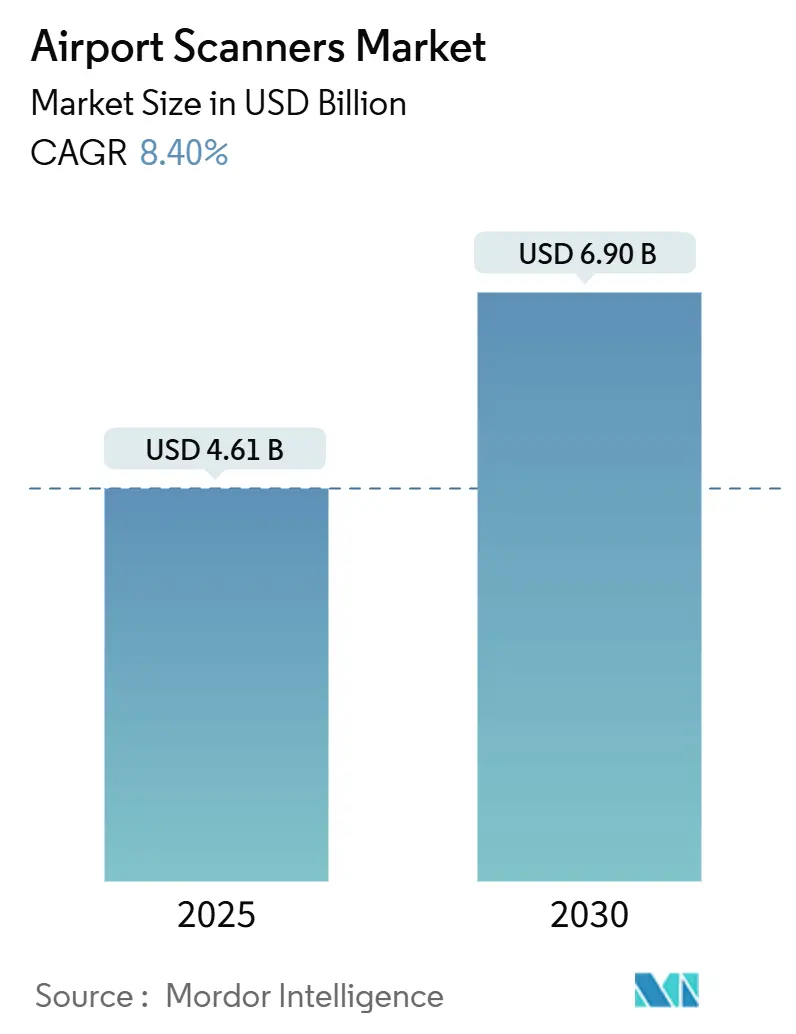

| Market Size (2025) | USD 4.61 Billion |

| Market Size (2030) | USD 6.90 Billion |

| Growth Rate (2025 - 2030) | 8.40% CAGR |

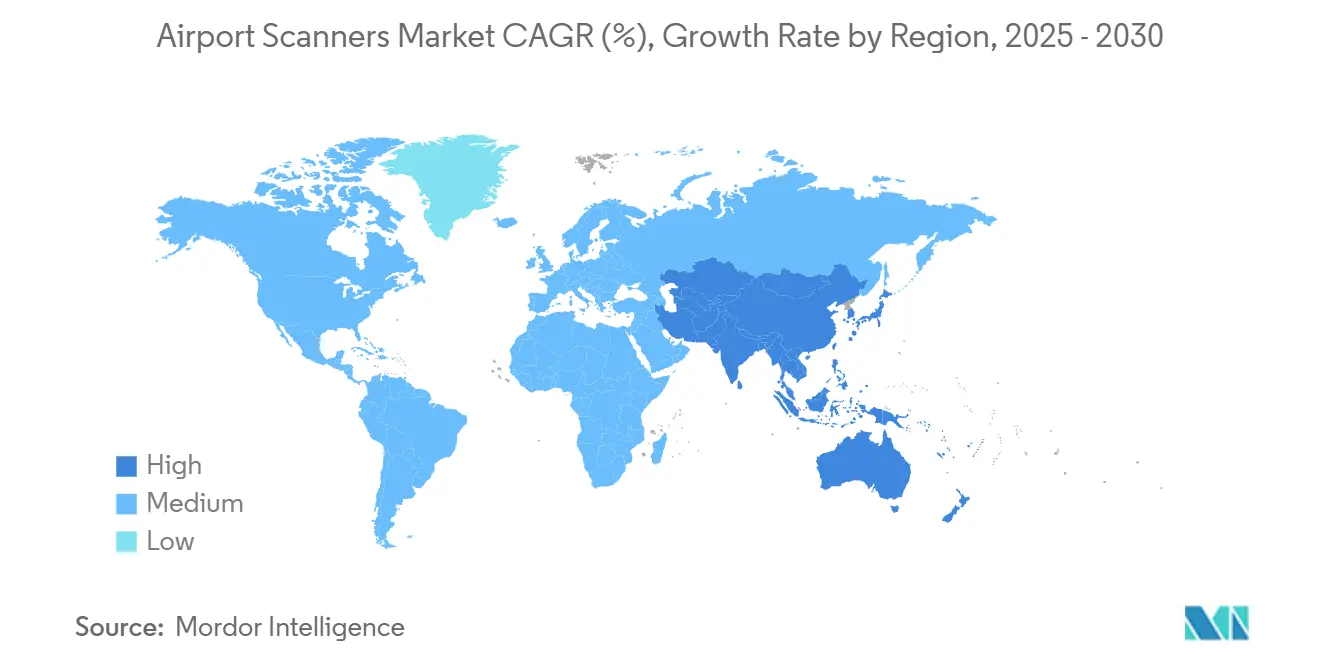

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Scanners Market Analysis by Mordor Intelligence

The airport scanner market size is valued at USD 4.61 billion in 2025 and is projected to reach USD 6.90 billion by 2030, registering an 8.40% CAGR over the forecast period. Mandatory deployment of computed-tomography (CT) systems, rapid airport capacity expansion in emerging regions, and government-funded checkpoint modernization programs jointly accelerate equipment demand. TSA’s 920-unit CT procurement underscores how regulatory mandates realign vendor roadmaps toward advanced imaging. Asia-Pacific mega-terminal projects and Africa’s greenfield hubs amplify volume requirements, while artificial intelligence (AI) driven automated threat recognition reshapes competitive positioning by emphasizing software over hardware differentiation. Service-centric contracting models gain traction as operators prioritize lifecycle support to guarantee uptime and regulatory compliance.

Key Report Takeaways

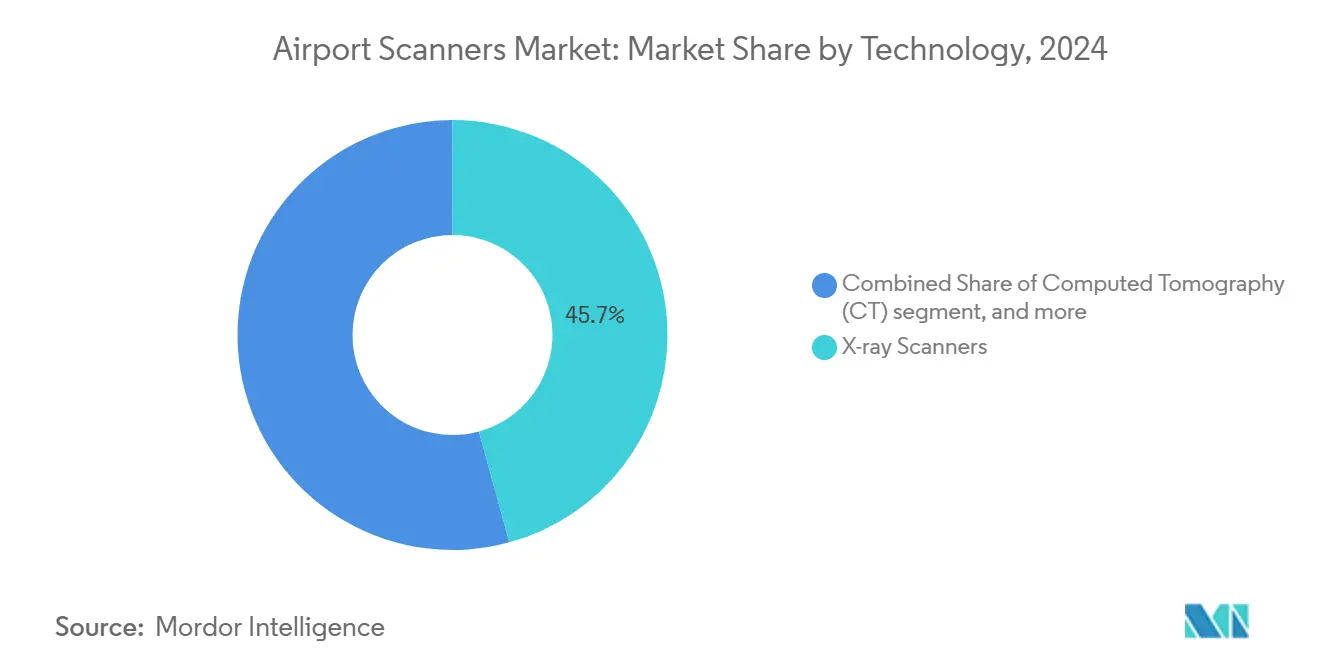

- By technology, X-ray scanners held a 45.74% share of the airport scanner market in 2024, whereas CT systems are forecasted to register a 10.56% CAGR through 2030.

- By product type, baggage scanners accounted for 49.70% of the airport scanner market size in 2024, while cargo and vehicle scanners are poised for an 11.70% CAGR during 2025-2030.

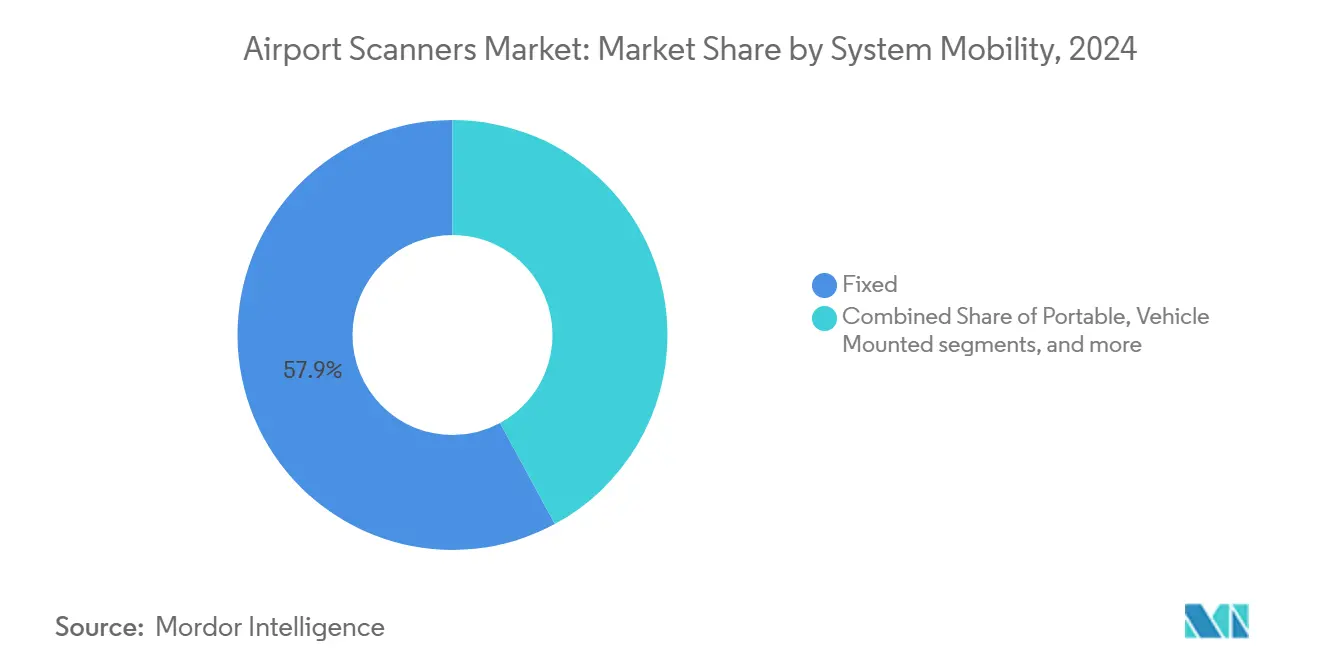

- By system mobility, fixed installations commanded 57.89% revenue in 2024; portable units are projected to rise at a 10.90% CAGR to 2030.

- By end user, commercial airports captured 85.30% revenue share in 2024; military airports are expected to expand at a 9.55% CAGR through 2030.

- North America dominated with 37.90% regional revenue in 2024, whereas Asia-Pacific is anticipated to post a 10.60% CAGR between 2025 and 2030.

Global Airport Scanners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory CT adoption in aviation security standards | +2.1% | Global, early in North America and EU | Medium term (2-4 years) |

| Global airport capacity expansion (Asia-Pacific and Africa) | +1.8% | Asia-Pacific core; spill-over to MEA and Africa | Long term (≥ 4 years) |

| Government funding boosts for checkpoint upgrades | +1.4% | North America and EU; selective APAC | Short term (≤ 2 years) |

| Replacement of legacy X-ray with dual-energy systems | +1.2% | Global, mature markets | Medium term (2-4 years) |

| AI-driven automated threat recognition rollout | +1.0% | North America, EU, advanced APAC | Medium term (2-4 years) |

| Self-service passenger scanning kiosks | +0.8% | North America, EU, select APAC hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory CT adoption in aviation security standards

TSA’s multiyear contract for 920 CT units compels airports to replace single-energy X-ray with volumetric imaging that allows electronics and liquids to remain in bags, shortening queue times.[1]Source: Transportation Security Administration, “Advanced Imaging Procurement,” tsa.gov The European Civil Aviation Conference validated CT-based explosives detection, giving operators regulatory certainty.[2]Source: European Civil Aviation Conference, “Common Evaluation Process,” ecac-ceac.org ICAO’s outcome-focused Aviation Security Manual encourages flexible technology choices that meet detection benchmarks. Vendors with CT-compliant portfolios gain scale economies, whereas smaller manufacturers struggle with certification costs. As adoption rises, airports justify premium pricing through throughput gains that offset staffing pressures.

Global airport capacity expansion (APAC and Africa)

Sydney Terminal 2, U-Tapao, and numerous African greenfield hubs require end-to-end screening ecosystems integrating baggage, cargo, and perimeter inspection. Brisbane Airport’s Rapiscan deployment reflects preference for proven platforms over experimental prototypes during time-critical expansion phases. Changi Terminal 5’s design-stage inclusion of biometric security sets a blueprint that other projects aim to emulate. Simultaneous build-outs challenge supplier production lines, lengthening lead times and raising component prices. Modular scanner architectures gain appeal where phased passenger growth demands incremental capacity additions.

Government funding boosts for checkpoint upgrades

US Airport Improvement Program grants and DHS preparedness funds subsidize capital-intensive equipment, enabling mid-tier airports to install advanced imaging once reserved for major hubs.[3]Source: Department of Homeland Security, “Preparedness Grants,” dhs.gov TSA’s Innovation Checkpoint at Las Vegas validates emerging solutions under real-world conditions, de-risking purchases for operators. Vendors with federal contracting expertise hold an edge because compliance paperwork and security clearances deter new entrants. Grant cycles create procurement clusters, producing short-run demand spikes that stress manufacturing throughput.

Replacement of legacy X-ray with dual-energy systems

Airports retire obsolete scanners ahead of regulatory deadlines, favoring dual-energy X-ray that provides better material discrimination without CT-level costs. Munich Airport’s deployment of RTT 110 lanes illustrates reduced manual inspections and smoother passenger flow. Long-term service contracts, such as Smiths Detection’s seven-year US maintenance deal, reveal operator preference for comprehensive lifecycle coverage. Backward-compatibility requirements raise technical barriers that protect incumbents.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy concerns over body-image capture | -1.2% | EU and North America; selective APAC | Long term (≥ 4 years) |

| High capital and lifecycle costs of scanners | -1.8% | Global, especially emerging markets | Medium term (2-4 years) |

| Cyber vulnerabilities in connected screening networks | -0.9% | Global, digitally advanced economies | Short term (≤ 2 years) |

| Tariff and component-supply disruptions | -0.7% | Global; acute in Asia-Pacific manufacturing clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Privacy concerns over body-image capture

GDPR obligations force EU airports to store only anonymized data, limiting AI training depth and sometimes downgrading detection fidelity. Opt-in programs such as Milan Linate’s FaceBoarding report lower-than-expected participation due to biometric skepticism. Vendors respond with privacy-preserving algorithms that blur anatomy while highlighting threats, yet these solutions can raise false-alarm rates, increasing secondary inspections and staff workload.

High capital and lifecycle costs of scanners

TSA’s cybersecurity directives promote encryption, network segmentation, and continuous patching protocols, which heighten deployment complexity. Legacy devices without embedded security must be isolated, undermining integrated analytics. Contractual negotiations increasingly hinge on breach liability clauses, extending sales cycles and escalating insurance costs for both vendors and operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: CT upgrade momentum accelerates

X-ray scanners continue to anchor checkpoints with a 45.74% revenue base due to entrenched fleets and lower capital hurdles. CT installations are projected to advance at a 10.56% CAGR to 2030. Yet, dual-energy retrofits are hastening the migration path toward volumetric imaging as regulatory deadlines tighten. mmWave and terahertz platforms remain niche, serving high-security environments where non-ionizing exposure outweighs throughput constraints. Standardized performance benchmarks under the ECAC Common Evaluation Process now let multinational airport groups cross-license equipment, further widening the adoption runway for CT solutions.

Vendors differentiate primarily through AI overlays that lift legacy hardware into next-generation detection classes without forcing full replacements. For instance, Smiths Detection's partnership with NeuralGuard adds adaptive algorithms that boost prohibited-item recognition rates by double digits while holding operating costs flat. Such plug-in architectures favor operators seeking incremental upgrades to satisfy compliance audits without shuttering lanes for large-scale rebuilds. The resulting hybrid fleet's dual-energy X-ray at lower-risk lanes and CT at high-risk nodes optimizes capital allocation while maintaining security parity.

By Product Type: Cargo systems outpace baggage lanes

Baggage scanners contributed 49.70% to the airport scanner market size in 2024, retaining primacy because every departing passenger bag must pass through at least one imaging cycle. Yet cargo and vehicle platforms are accelerating at an 11.70% CAGR as e-commerce drives air-freight growth and customs agencies institute 100% screening rules on high-risk consignments. By 2030, these solutions are slated to command over one-quarter of product revenue as pallet-scale CT and automated threat recognition compress inspection times and reduce false positives.

Integrated checkpoint ecosystems such as Vanderlande’s Copenhagen project bundle baggage lanes, parallel image-analysis centers, and automated tray return systems into one turnkey contract, raising switching costs while guaranteeing 10-year service continuity. Metal detectors persist in emerging markets where acquisition budgets remain constrained; they serve as the first filter before high-resolution scans. Vendors able to combine low-cost walkthroughs with AI-enabled hold-baggage systems secure follow-on maintenance deals that can double original hardware revenue over the equipment life cycle.

By System Mobility: Portable units gain tactical relevance

Fixed installations account for 57.89% of global sales, and will stay indispensable because built-in conveyors and hard-wired power deliver the highest passenger throughput. Even so, portable scanners are climbing at a 10.90% CAGR as military airfields, seasonal terminals, and pop-up events require redeployable assets that fit freight elevators and run on generator power. Compact footprints and rapid calibration allow operators to establish fully functional lanes within 24 hours, a capability valued during terminal refurbishments and emergency surge operations.

Vehicle-mounted systems extend perimeter coverage by examining service vans, catering trucks, and fuel tankers before they cross the air-side boundary, closing a gap not addressed by checkpoint lanes. Drive-through and tunnel scanners handle cargo hubs where landside trucking merges with apron operations; their high-energy beams image entire tractor-trailers in under 30 seconds, preserving just-in-time schedules for integrator carriers. Airports with mixed passenger-cargo profiles increasingly deploy a layered mobility mix fixed at the core, vehicle-mounted on the perimeter, and portable for contingency, ensuring security resilience without duplicating capital spend.

By End User: Defense airports strengthen procurement

Commercial airports capture 85.30% of the airport security scanner market due to mandatory screening regulations tied to civil aviation safety . Traffic rebounds and queue-time targets continue to channel cash toward CT upgrades, automated tray return systems, and AI analytics that cut passenger divestiture steps. Funding levers such as the US Airport Improvement Program and Europe’s Connecting Europe Facility lower acquisition barriers for mid-tier hubs, widening the addressable base for manufacturers.

Military airports are advancing at a 9.55% CAGR and are projected to top USD 1.04 billion by 2030 as defense ministries harden installations in response to drone and insider threats. Procurement frameworks often stipulate domestic content and ruggedized designs, favoring suppliers capable of localized assembly and MIL-STD certifications. Commercial sites increasingly adopt defense-grade algorithms for behavioral analytics and insider-threat mitigation, illustrating bidirectional technology transfer that benefits vendors with dual-use clearances and long-term integrated-logistics support contracts.

Geography Analysis

North America held a 37.90% market share in 2024, leveraging the TSA’s blanket CT rollout and seven-year integrated logistics contracts that guarantee preventative maintenance and software updates. Innovation Checkpoint pilots at Las Vegas and Atlanta validate emerging self-service lanes and AI imaging modules, accelerating regulatory acceptance and shortening commercialization cycles. Federal grants under the Airport Improvement Program reimburse up to 75% of eligible security-capital costs, widening adoption beyond Tier 1 hubs.

Europe maintains a steady replacement cadence, prioritizing passenger experience. Frankfurt’s Rohde & Schwarz millimeter-wave deployment reduces pat-down referrals by more than 50%, while Milan Linate’s biometric FaceBoarding lane lets travelers clear security and boarding with a single enrollment. The ECAC Common Evaluation Process slashes certification timelines, enabling multi-airport groups to procure identical equipment under single-lot tenders and extract volume discounts.

Asia-Pacific posts the fastest 10.60% CAGR, propelled by mega-projects like Changi Terminal 5, Navi Mumbai International, and Sydney Terminal 2’s redevelopment, each embedding biometric and CT screening from the blueprint stage. Africa and the Middle East follow similar greenfield trajectories but adopt modular scanners to align capital outlay with phased passenger growth while conforming to ICAO Annex 17 security objectives. Regional suppliers establish in-country service hubs to curb tariff exposure and ensure sub-24-hour spare-parts delivery, a critical uptime metric in hot-and-humid operating environments.

Competitive Landscape

The market remains moderately fragmented. Smiths Detection secures loyalty through long-horizon service pacts, such as its seven-year US contract covering 486 CT units, which guarantees software refreshes and part replacements on a fixed-fee basis. OSI Systems strengthens stickiness by bundling 920CT imagers with automated tray-return conveyors, ensuring lane architecture remains proprietary for the system’s life span.

Leidos amplifies value by embedding SeeTrue AI into legacy fleets, lifting detection accuracy to 15 percentage points without new hardware, an approach attractive to budget-constrained operators. Vanderlande positions itself as a neutral lane-builder: its Copenhagen engagement delivered 20 automated lanes with vendor-agnostic scanner bays, future-proofing operators that anticipate multi-brand expansions. AI-first startups supply cloud-delivered analytics that retrofit on third-party imagery, chipping away at incumbents’ software share.

Chinese manufacturers are scaling cost-competitive CT lines for domestic megahubs, exerting downward price pressure globally, though export gains remain measured due to cybersecurity and supply-chain vetting hurdles. In Europe, Rohde & Schwarz leverages millimeter-wave domain expertise to secure privacy-sensitive contracts, while CEIA expands walkthrough metal-detector penetration in budget-conscious African terminals. Overall, software innovation and lifecycle-service depth count more than raw hardware specs, steadily redrawing the competitive map.

Airport Scanners Industry Leaders

Rapiscan Systems, Inc.

Leidos Holdings, Inc.

Nuctech Company Limited

Smiths Detection Group Ltd. (Smiths Group plc)

Rohde & Schwarz GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smiths Detection secured a contract with Dubai Aviation Engineering Projects (DAEP) to deploy advanced checkpoint screening solutions across all terminals at Dubai International Airport (DXB). This initiative aims to enhance security operations and improve the passenger experience at one of the world’s busiest airports.

- January 2024: Rohde & Schwarz secured a USD 10.9 million TSA contract to supply QPS201 UHD AIT security scanners to US airports. Using mmWave technology, these scanners ensure quick and accessible passenger screening. The system is deployed at major airports and meets TSA and ECAC standards for advanced security screening technology.

Global Airport Scanners Market Report Scope

| X-ray Scanners |

| Computed Tomography (CT) |

| Millimeter-wave (mmWave) Scanners |

| Terahertz Imaging Systems |

| Passenger Body Scanner |

| Baggage Scanner |

| Cargo and Vehicle Scanners |

| Walkthrough and Handheld Metal Detectors |

| Fixed |

| Portable |

| Vehicle Mounted |

| Drive-through/Tunnel Systems |

| Commercial Airport |

| Military Airport |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Technology | X-ray Scanners | ||

| Computed Tomography (CT) | |||

| Millimeter-wave (mmWave) Scanners | |||

| Terahertz Imaging Systems | |||

| By Product Type | Passenger Body Scanner | ||

| Baggage Scanner | |||

| Cargo and Vehicle Scanners | |||

| Walkthrough and Handheld Metal Detectors | |||

| By System Mobility | Fixed | ||

| Portable | |||

| Vehicle Mounted | |||

| Drive-through/Tunnel Systems | |||

| By End User | Commercial Airport | ||

| Military Airport | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the airport security scanner market in 2025?

The airport scanner market size stands at USD 4.61 billion in 2025 and is projected to reach USD 6.90 billion by 2030, registering an 8.40% CAGR over the forecast period.

Which technology segment is growing the fastest?

CT systems exhibit the highest growth at a 10.56% CAGR due to global regulatory mandates for advanced imaging.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest expansion, expected to post a 10.60% CAGR through 2030 on the back of large-scale airport construction.

What is driving demand for portable scanners?

Military modernization and temporary event security are fueling a 10.90% CAGR in portable systems by requiring redeployable screening assets.

How are AI solutions impacting airport security screening?

AI-driven automated threat recognition reduces manual image review, improves detection accuracy, and creates competitive advantages for vendors offering retrofit software.

Page last updated on: