Airport Services Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 186.67 Billion |

| Market Size (2031) | USD 421.70 Billion |

| Growth Rate (2026 - 2031) | 17.70% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Services Market Analysis by Mordor Intelligence

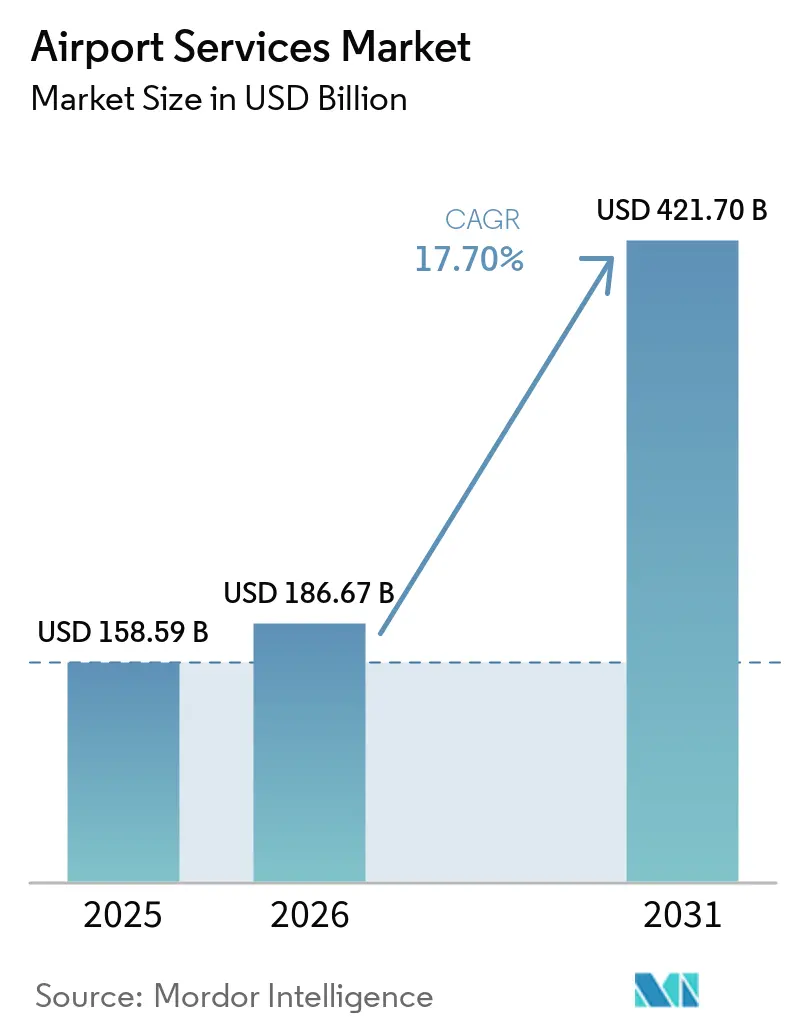

The airport services market size is expected to grow from USD 158.59 billion in 2025 to USD 186.67 billion in 2026 and is forecast to reach USD 421.70 billion by 2031 at 17.70% CAGR over 2026-2031. The airport services market is expanding on the back of a stronger traffic base, with global passenger volumes reaching 9.8 billion in 2025 and forecast to rise to 10.2 billion in 2026, which keeps demand high across terminal, ramp, cargo, and mobility services. Airline economics are also supporting this rise, as global airline revenues are projected to exceed USD 1.053 trillion in 2026, with passenger ticket revenues alone reaching USD 751 billion, which supports continued spending across the airport services value chain.[1] International Air Transport Association, “Airline Profitability Stabilizes with 3.9% Net Margin Expected in 2026,” IATA, iata.org The airport services market is also shifting away from a narrow dependence on aeronautical fees, as airports increasingly treat retail, cargo logistics, digital services, and landside mobility as core commercial levers. Regional growth is rebalancing toward Asia-Pacific and the Middle East, even as North America remains the largest base, shifting where new capacity, technology, and service contracts are awarded. Short-term cost pressure from fuel volatility and rising compliance obligations is tightening budgets. Still, it is also pushing operators in the airport services market toward automation, electrification, and broader revenue diversification.

Key Report Takeaways

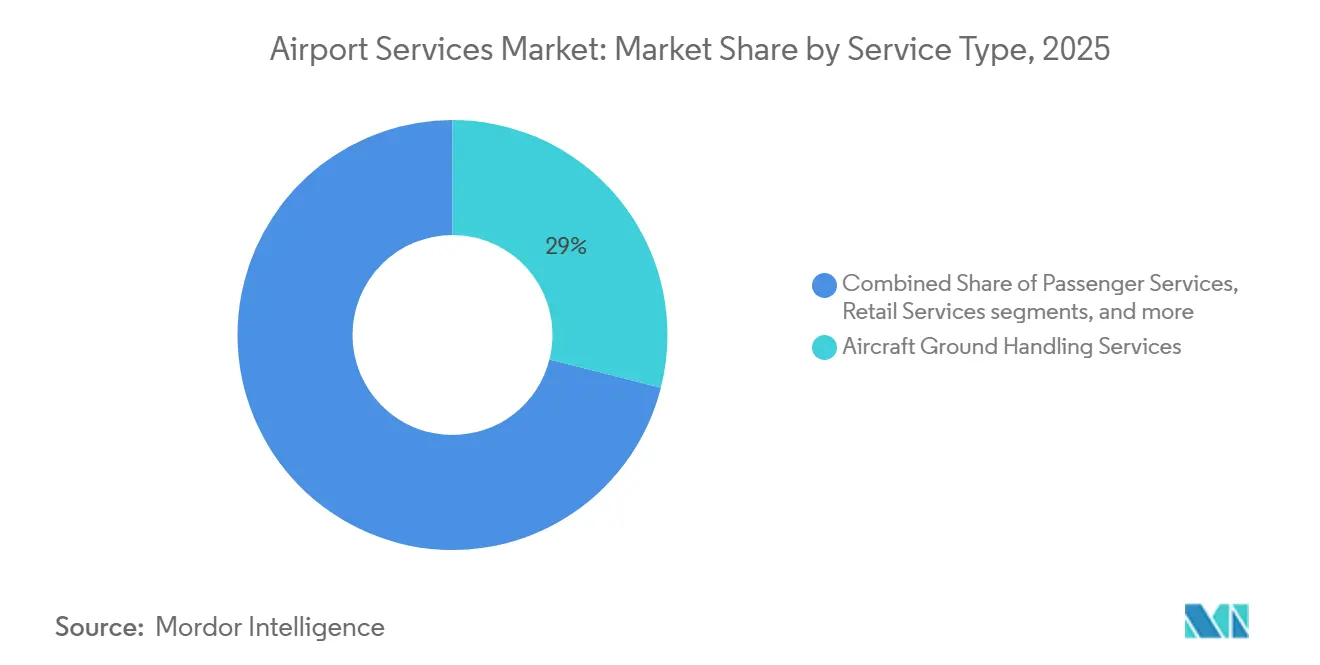

- By service type, aircraft ground handling services led with 28.95% revenue share in 2025, while baggage/cargo handling services are forecast to expand at an 18.88% CAGR through 2031.

- By revenue stream, aeronautical services held 58.27% of the airport services market in 2025, while non-aeronautical services are projected to grow at a 19.98% CAGR through 2031.

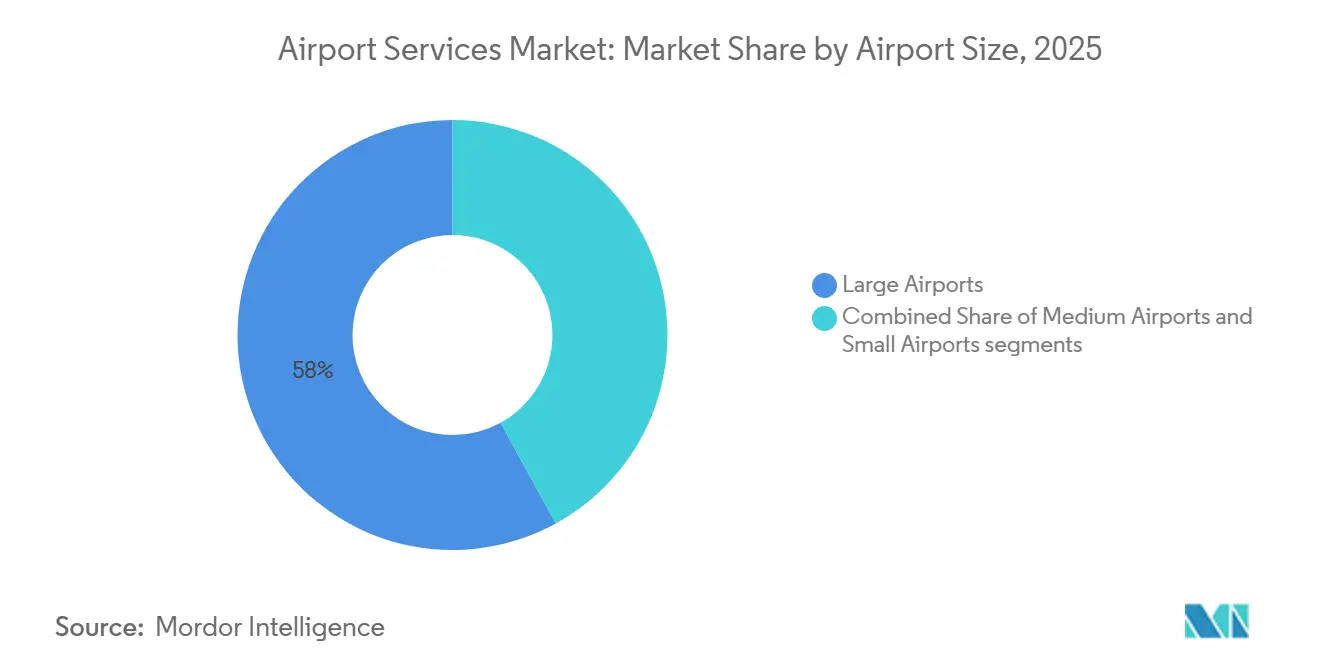

- By airport size, large airports accounted for 57.98% share in 2025, while small airports are forecast to grow at a 19.91% CAGR through 2031.

- By infrastructure type, brownfield airports captured 79.58% of the market share in 2025, while greenfield airports are projected to grow at a 20.68% CAGR through 2031.

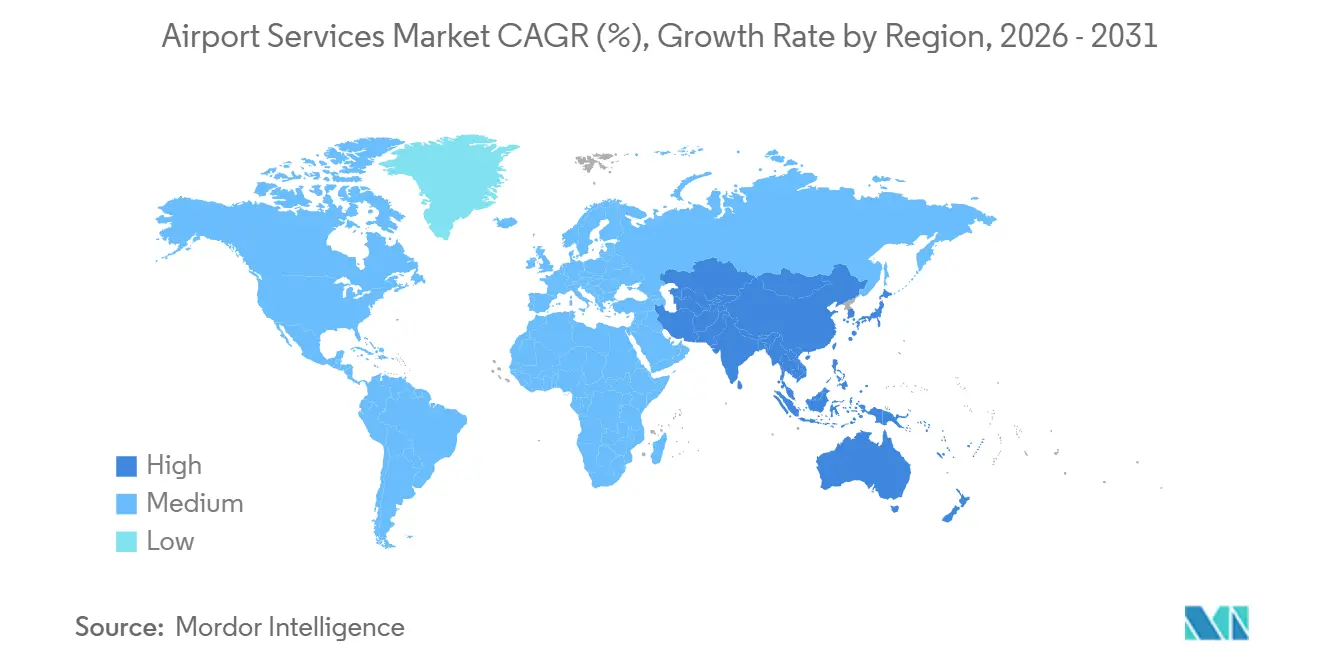

- By geography, North America held 39.78% of the airport services market in 2025, while Asia-Pacific is forecast to register the fastest growth at a 20.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airport Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging air passenger traffic in emerging Asia-Pacific and Middle East hubs | +4.8% | APAC, Middle East, with spill-over to Africa and Latin America | Medium term (2-4 years) |

| Expansion and modernization of airport infrastructure globally | +3.5% | Global, concentrated in APAC, Middle East, North America | Long term (≥ 4 years) |

| E-commerce-led growth in cross-border air cargo | +2.5% | APAC core, spill-over to Europe and Middle East | Short term (≤ 2 years) |

| Rising demand for ancillary non-aeronautical revenue streams | +2.2% | Global, with early gains in North America, Europe, and APAC hub airports | Medium term (2-4 years) |

| Integration of smart and digital airport technologies | +1.8% | Global, North America, APAC, and Middle East leading deployments | Medium term (2-4 years) |

| Sustainability-linked financing propelling ground support electrification | +1.2% | EU primary mandate zone, North America and APAC adopting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Air Passenger Traffic in Emerging Asia-Pacific and Middle East Hubs

The airport services market is being lifted by traffic growth, now more clearly centered in Asia-Pacific and the Middle East. Asia-Pacific RPK grew 7.8% in 2025, while Middle Eastern carriers posted 6.8% growth, both well ahead of North America at 0.4%.[2]International Air Transport Association, “Strong 2025 Passenger Demand Masks Ongoing Capacity Constraints,” IATA, iata.org IATA expects Asia-Pacific demand to rise by another 7.3% in 2026, keeping the region as the fastest-growing large aviation market. This volume increase directly lifts demand for passenger handling, turnaround support, baggage operations, and premium airport services at major hubs. It also raises pressure on constrained airports, where service revenues per passenger can rise faster because airlines and concession operators value speed and reliability more highly. In the airport services market, this creates stronger pricing power for operators serving busy gateway airports than for those focused only on underused secondary facilities.

E-commerce-Led Growth in Cross-border Air Cargo

The airport services market is also gaining momentum from cargo flows that are becoming more time-sensitive and e-commerce-driven. Global air cargo demand reached a record level in 2025, rising 3.4% year over year, with Asia-Europe demand up 10.3%. E-commerce is expected to account for 30% of total air cargo volumes by 2027, up from 20% in 2024, which is changing the operating mix at large freight gateways. In the airport services market, that shift favors automated sorting, express handling, and cargo terminals that can process fast parcel flows with lower dwell time. It also changes investment priorities, as airports now need greater digital coordination among airlines, handlers, and customs-facing processes. Cargo handling is therefore becoming a stronger growth engine than it was in the pre-e-commerce period.

Integration of Smart and Digital Airport Technologies

The airport services market is increasingly shaped by digital tools that help airports extract more throughput from existing infrastructure. Dallas Fort Worth International Airport committed USD 17.2 million in June 2025 to deploy a large 3D LiDAR spatial intelligence network across its terminals. Dubai International Airport has been investing in AI-driven facial recognition as it works toward handling 100 million passengers by 2026 without major new physical expansion. In the airport services market, these systems matter because they reduce congestion, improve gate and terminal planning, and support better passenger flow management. They also support commercial outcomes, since better dwell-time visibility can improve retail placement, lounge monetization, and digital engagement. Airports that connect operational technology with non-aeronautical revenue tools are likely to see faster payback than those that use digital systems solely for efficiency.

Sustainability-Linked Financing Propelling Ground Support Electrification

The airport services market is now seeing electrification move from a voluntary target to a capital planning priority. IATA states that electric GSE in an average EU country produces 35% to 52% less CO2 and 5.5 to 8.3 dB(A) lower noise emissions per turnaround than diesel equipment.[3]International Air Transport Association, “Electric GSE,” IATA, iata.org Menzies Aviation increased its electric GSE share from 22% in 2024 to 25% by the end of 2025, adding more than 620 electric assets across its network. A March 2026 study in Nature Communications found that full electrification of GSE at the largest US airports could push peak power demand to as much as 20 MW, suggesting on-site batteries and solar systems may be needed to avoid costly grid upgrades. That means the airport services market is not only buying cleaner equipment, it is also moving toward new financing and utility partnerships to support charging and energy management. Over time, operators that can combine electrified fleets with site-level power planning should gain an advantage in airport tenders where environmental compliance is becoming more important.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aviation fuel prices squeezing airline handling budgets | -3.5% | Global, most acute in Europe and Asia due to Hormuz supply disruption | Short term (≤ 2 years) |

| Acute skilled labor shortage in ground operations | -2.5% | Global, most acute in the Americas and Europe | Medium term (2-4 years) |

| High capital expenditure for advanced equipment and IT systems | -1.8% | Global, disproportionate impact on small and mid-sized handlers | Medium term (2-4 years) |

| Increasing ESG scrutiny inflating service costs | -1.5% | EU primary, North America and APAC adopting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Aviation Fuel Prices Squeezing Airline Handling Budgets

Fuel volatility is the most immediate financial restraint on the airport services market in 2026. Jet fuel prices nearly doubled between February and March 2026, with the global jet fuel index rising 95.2% to USD 195.2 per barrel after disruption around the Strait of Hormuz.[4]Nuran Erkul, “Jet Fuel Prices Double Amid Strait of Hormuz Blockade Paralyzing Supply Flows,” Anadolu Agency, aa.com.tr Airports Council International Europe warned that a systemic jet fuel shortage could affect the EU if normal flows did not resume. At the same time, the International Energy Agency estimated Europe had only six weeks of supply at that stage. When airlines face this kind of cost shock, they often trim marginal routes, reduce frequencies, and demand tighter handling costs from contractors. In the airport services market, revenue per aircraft movement is compressed while labor and equipment costs remain elevated. Ground handlers are especially exposed because they usually cannot recover inflation quickly without renegotiating contracts that may take many months to reopen.

Acute Skilled Labor Shortage in Ground Operations

The airport services market continues to face a labor problem that automation has not yet solved. Industry surveys in 2025 showed that 59% of air cargo workers had seriously considered leaving the sector, while turnover rates in US and UK ground handling operations were above 40%. The October 2025 US government shutdown also exposed labor fragility, with major staffing disruption contributing to a 5-hour ground stop at Austin-Bergstrom Airport and nearly 2,200 delays at Charlotte Douglas. In the airport services market, this shortage simultaneously affects punctuality, service quality, training costs, and safety-sensitive functions. It also creates a skills gap because workers leaving the sector are often replaced more slowly than systems are being modernized. Operators that invest early in structured retraining and certification are therefore likely to build a more durable service advantage than those relying only on short-term hiring.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cargo Handling Disrupts a Ground-Handling-Dominated Market

Aircraft ground handling services accounted for 28.95% of the airport services market in 2025, making it the largest service segment and the operational base for most airport activity. The segment remains central because every commercial flight depends on ramp handling, aircraft movement support, boarding support, and turnaround coordination. The airport services market still reflects this essential role, as airline hub strategies and preferred service partnerships continue to concentrate large handling volumes with established operators. Aircraft maintenance services also remain important because fleet aging and delivery delays are keeping aircraft in service for longer periods.

Baggage/cargo handling services are the fastest-growing segment, and their airport services market size is projected to expand at an 18.88% CAGR through 2031. That growth is tied closely to e-commerce flows, semiconductor shipments, and the rising need for fast sorting and transfer capacity. Retail services and food and beverage services, while smaller, are growing in importance because they support the broader shift toward commercial airport revenue. Car parking and landside mobility services are also becoming more integrated with rail, EV charging, and new airport access planning. Across the airport services industry, service differentiation is increasingly shaped by who can combine operational reliability with digital support for cargo and passengers.

By Revenue Stream: Commercial Ecosystems Outperform Traditional Aeronautical Fees

Aeronautical services represented 58.27% of the market in 2025 and remained the core contractual layer of airport economics. Landing fees, terminal charges, and related regulated charges still provide the largest revenue base for many airports. The airport services market continues to rely on this stream because it is embedded in airline-airport operating relationships and in regulated pricing structures. Even so, airline pushback to higher airport charges is limiting how far airports can depend on fee-led growth alone.

Non-aeronautical services are the fastest-growing revenue stream in the airport services market, with a 19.98% CAGR through 2031, reflecting a long-running shift toward retail, food and beverage, parking, lounges, and app-based commercial services. Airports are increasingly treating passenger dwell time as an asset that can be monetized more effectively through better layouts and digital engagement. That makes non-aeronautical activity a more resilient growth lever even when airline pricing remains contested. In the airport services industry, digital ancillary products are becoming more important because they scale more easily than traditional concession formats.

By Airport Size: Secondary Hubs Accelerate Under Connectivity Programs

Large airports captured 57.98% of the airport services market share in 2025, reflecting their role as the main gateways for long-haul traffic, premium passengers, and large-scale cargo. These airports also host the most complex service mix, including lounges, large retail footprints, dedicated freight facilities, and advanced passenger processing. The airport services market remains anchored in large airports because they handle the heaviest concentration of aircraft movements and service contracts. Their capital programs also continue to create long-cycle demand for specialized support services around active terminals and aprons.

Small airports are projected to grow at a 19.91% CAGR through 2031, making them the fastest-growing segment of airports by size. This growth is tied to new connectivity programs, traffic dispersion from congested hubs, and regional airport development in emerging economies. The airport services market is therefore broadening beyond major gateway hubs and creating more room for localized operators. Service standards and cost structures at small airports still differ sharply from those at large hubs because many smaller operators have lower automation and more variable labor intensity. That gap creates space for global companies to offer standardized service packages and technical support to regional airports.

By Infrastructure Type: Greenfield Builds Embed Future-Ready Advantage

Brownfield airports accounted for 79.58% of the market in 2025 and remained the dominant infrastructure type because most global aviation activity still runs through long-established hubs. Large brownfield projects continue to focus on expansion, modernization, and phased renewal while keeping live operations running. The airport services market depends heavily on these projects because they create steady demand for operational support, temporary capacity planning, and service deployment within active airport environments. Brownfield programs also favor providers that can operate within complex operational constraints without disrupting airline schedules.

Greenfield Airports are projected to grow at a 20.68% CAGR through 2031, which makes them the fastest-growing infrastructure type in the airport services market. This pipeline is concentrated in Asia-Pacific and the Middle East, where new airport capacity is being built at a pace that has little recent precedent. Greenfield projects matter because they allow operators to lock in service frameworks, technology standards, and equipment specifications from the start. That gives early participants a longer contract horizon and stronger influence over how airport operations are designed. Across the airport services industry, winning a greenfield mandate can be more strategic than adding capacity at a mature airport because it shapes the operating model for decades.

Geography Analysis

North America held 39.78% of the airport services market share in 2025 and remained the largest regional base. ACI-NA identified USD 173.9 billion in airport infrastructure needs for 2025 to 2029. The region is therefore investing heavily even though passenger growth is now much slower than in emerging regions. That is pushing the airport services market in North America toward modernization, technology deployment, and higher-value commercial services rather than simple volume expansion.

Asia-Pacific is the fastest-growing regional segment, and the airport services market size in the region is projected to expand at a 20.01% CAGR through 2031. The region accounted for 34.4% of global RPK in 2025, and its air cargo demand grew by 8.4%, well above the global average. ACI Asia-Pacific and the Middle East have identified USD 240 billion in planned airport infrastructure investment through 2035, which supports a long runway for service contracts across terminals, cargo, and airside systems. The airport services market in Asia-Pacific is also supported by higher load factors and tighter turnaround needs at major hubs, which raises the value of reliable ground handling and passenger flow management. This combination of traffic growth, airport construction, and operational intensity keeps the region at the center of future contract expansion.

Europe remained the second-largest regional market and entered 2026 with the highest absolute airline net profitability at USD 14 billion, supporting demand for a broad range of airport services. The airport services market in Europe is still shaped by higher regulatory complexity than most other regions, especially around emissions compliance and airport charging debates. The Middle East continues to stand out for hub-led expansion, with airline profit margins projected at 9.3% in 2026, which supports premium passenger and ground service demand. Africa also posted strong traffic momentum, with flight demand growth at 9.4% in 2025, which improves the medium-term outlook for service demand at developing gateways. South America is benefiting from traffic recovery and network expansion, but the airport services market there remains smaller and more uneven than in North America, Europe, and Asia-Pacific.

Competitive Landscape

The airport services market remains structurally fragmented, especially in ground operations, where more than 1,000 independent firms are active, and the top 3 players account for less than 30% of global market share. This fragmentation keeps pricing discipline uneven and leaves room for local operators in many airports. At the same time, the airport services market is consolidating through private equity-backed acquisitions and network expansion by large international groups. Swissport reported record revenue of EUR 3.9 billion (USD 4.59 million) in 2025, driven by growth across ground operations, cargo, and hospitality, underscoring the advantage of a diversified service portfolio.

The airport services market is also seeing increased ownership of equipment and network platforms. Lone Star Funds completed its acquisition of Alliance Ground International in March 2026, adding a large North American footprint and signaling continued capital interest in ground handling scale. Global Infrastructure Partners agreed to acquire TCR in March 2026, showing that airport GSE leasing is also being treated as a durable infrastructure-like asset class. In April 2026, gategroup reached an agreement to acquire an additional 51% stake in Cateringpor, taking full ownership and strengthening its global catering network. These moves show that scale, network reach, and service breadth are becoming more important in the airport services market than stand-alone local presence.

Technology is becoming another dividing line in the airport services market. The field still has low digital maturity, with limited use of predictive analytics and end-to-end operational visibility among many handlers. Operators that adopt data standards, automation, and cargo quality certifications are better placed to win premium contracts in pharma, semiconductor, and e-commerce cargo. Netcompany’s move to take full ownership of the Smarter Airports platform in May 2026 shows how technology firms are gaining a larger role in operational decision support at major airports. Veovo’s April 2026 agreement to acquire Dubai Technology Partners points in the same direction, as airport software vendors expand capabilities through specialist acquisitions. The competitive balance in the airport services market is therefore moving toward firms that combine physical operations, digital visibility, and long-term airport relationships.

Airport Services Industry Leaders

SATS Ltd.

Fraport Ground Services GmbH

dnata (The Emirates Group)

Swissport International AG

Aena S.M.E., S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Emirates broke ground on a USD 5.1 billion engineering complex at Dubai South, designed to be the world's largest aviation maintenance plant, capable of simultaneously servicing 28 wide-body aircraft. Delivering LEED Platinum certification, the facility signals the UAE's intent to anchor MRO market leadership for the next decade.

- March 2025: SATS and Vietnam Airlines signed an MoU to establish an air cargo hub at Long Thanh Airport in Vietnam.

- January 2025: Swissport International won a five-year ground handling contract with Lufthansa Group at London Heathrow, covering 40 daily flights and deploying 80% electric GSE.

Global Airport Services Market Report Scope

The airport services market is witnessing significant growth driven by increasing global air passenger traffic, advancements in airport infrastructure modernization, and rising demand for efficient ground handling, passenger processing, baggage management, and non-aeronautical commercial services. Airports are progressively implementing digital technologies, automation, biometrics, and smart airport solutions to enhance operational efficiency, passenger experience, and revenue generation. The report covers airport operational services for passenger movement, cargo handling, aircraft turnaround, terminal retail, mobility management, and airport infrastructure support. However, it excludes aircraft manufacturing, airline operations, air traffic control systems, military airport operations, and standalone aviation infrastructure construction activities not directly associated with airport service operations.

The airport services market is segmented by service type, revenue stream, airport size, infrastructure type, and geography. By service type, the market is segmented into aircraft ground handling services, aircraft maintenance services, passenger services, baggage and cargo handling services, car parking and landside mobility services, food and beverage services, retail services, and other airport support services. By revenue stream, it is categorized into aeronautical and non-aeronautical services. By airport size, the market is segmented into large, medium, and small airports. By infrastructure type, the market is segmented into greenfield and brownfield airports, and airport operations and service demand are assessed across global commercial aviation hubs. The report also covers the market sizes and forecasts for the airport services market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Aircraft Ground Handling Services |

| Aircraft Maintenance Services |

| Passenger Services |

| Baggage/Cargo Handling Services |

| Car Parking and Landside Mobility Services |

| Food and Beverage Service |

| Retail Services |

| Others |

| Aeronautical Services |

| Non-Aeronautical Services |

| Large Airports |

| Medium Airports |

| Small Airports |

| Greenfield Airports |

| Brownfield Airports |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Service Type | Aircraft Ground Handling Services | ||

| Aircraft Maintenance Services | |||

| Passenger Services | |||

| Baggage/Cargo Handling Services | |||

| Car Parking and Landside Mobility Services | |||

| Food and Beverage Service | |||

| Retail Services | |||

| Others | |||

| By Revenue Stream | Aeronautical Services | ||

| Non-Aeronautical Services | |||

| By Airport Size | Large Airports | ||

| Medium Airports | |||

| Small Airports | |||

| By Infrastructure Type | Greenfield Airports | ||

| Brownfield Airports | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected value of airport services by 2031?

The airport services market size is expected to grow from USD 158.59 billion in 2025 to USD 186.67 billion in 2026 and is forecast to reach USD 421.70 billion by 2031 at 17.70% CAGR over 2026-2031.

Which region leads global airport services demand today?

North America held the largest regional share in 2025 at 39.78%, supported by 981 million US enplanements and a large infrastructure pipeline.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to record the fastest growth at a 20.01% CAGR through 2031, supported by traffic growth, cargo expansion, and new airport investment.

Which service category is growing the fastest?

Baggage and cargo handling is the fastest-growing service type, with an 18.88% CAGR through 2031 as e-commerce and time-critical freight volumes rise.

Why are non-aeronautical revenues becoming more important for airports?

Non-aeronautical services are projected to grow at a 19.98% CAGR through 2031 as airports rely more on retail, food and beverage, parking, lounges, and digital ancillary services.

How concentrated is competition among airport service providers?

Competition is still fragmented, especially in ground handling, where over 1,000 firms operate and the top 3 players account for under 30% of global share.

Page last updated on: