Airport Security Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

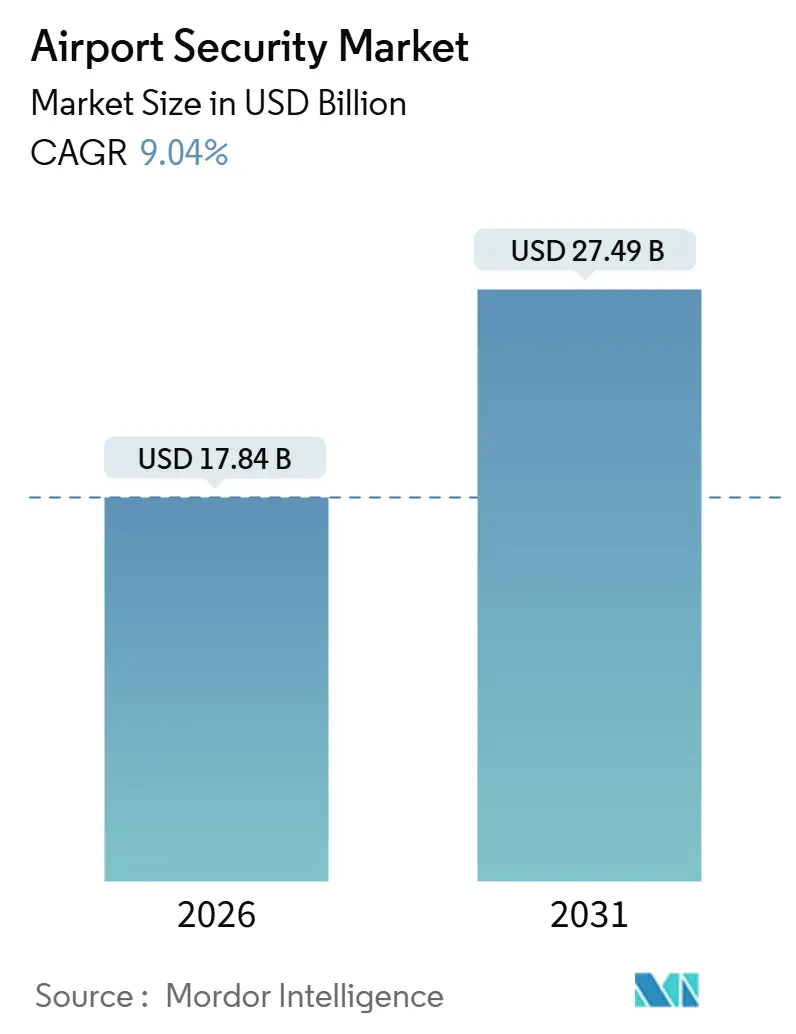

| Market Size (2026) | USD 17.84 Billion |

| Market Size (2031) | USD 27.49 Billion |

| Growth Rate (2026 - 2031) | 9.04% CAGR |

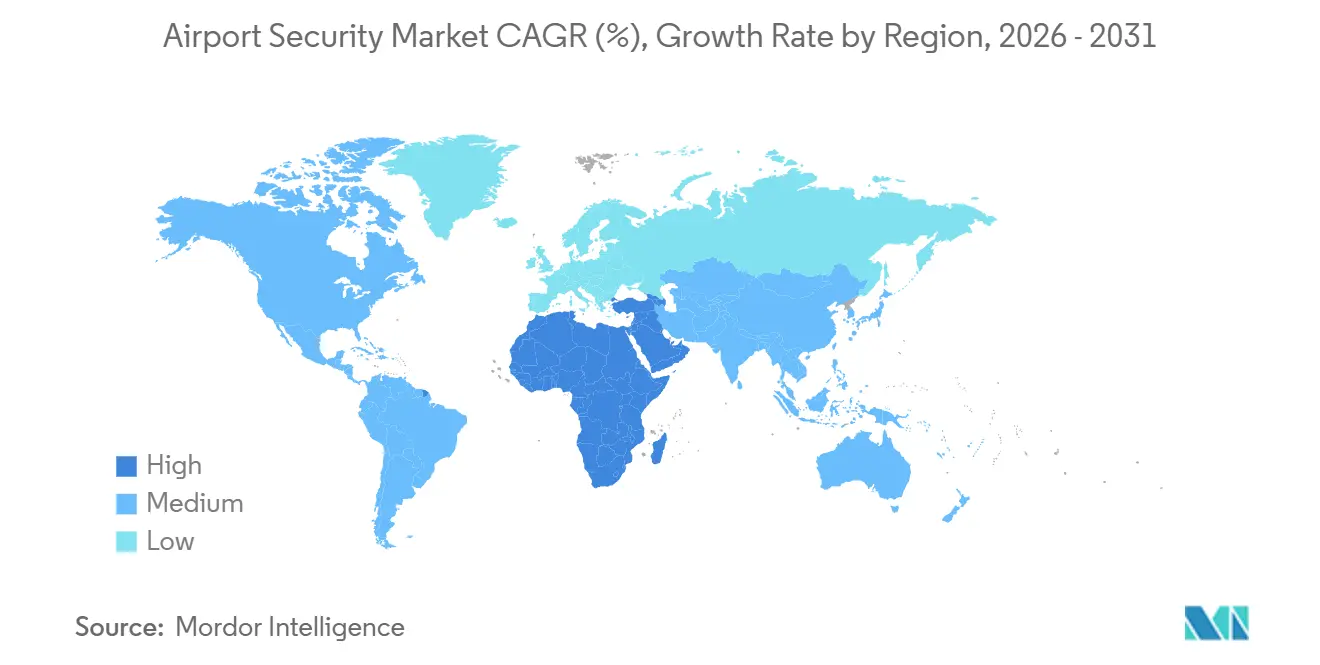

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Security Market Analysis by Mordor Intelligence

The airport security market size stood at USD 17.84 billion in 2026 and is projected to reach USD 27.49 billion by 2031, registering a 9.04% CAGR over the forecast period. Strong passenger recovery toward the 10 billion-traveler mark, rapid rollout of touchless biometric checkpoints, and mandates for cyber-physical resilience reposition security from a cost center to a revenue-protecting differentiator. Screening lanes are shifting to computed tomography (CT) scanners that allow liquids and laptops to remain in their bags. At the same time, credential-authentication kiosks verify faces against photo IDs in under two seconds, compressing curb-to-gate times and boosting retail spend. Integrated command centers stream edge data to the cloud for AI analytics that flag anomalies in real-time, allowing airports to redeploy staff from monitoring walls of cameras to resolving incidents. Mid-tier hubs are leapfrogging legacy systems with modular, cloud-native platforms procured as subscription services, shrinking integration cycles and aligning technology refresh with traffic growth. Regionally, the Asia-Pacific remains the revenue anchor. Still, the Middle East and Africa deliver the fastest compounded growth, as mega-projects, such as Riyadh’s King Salman International Airport, integrate seamless travel into master plans from the outset.

Key Report Takeaways

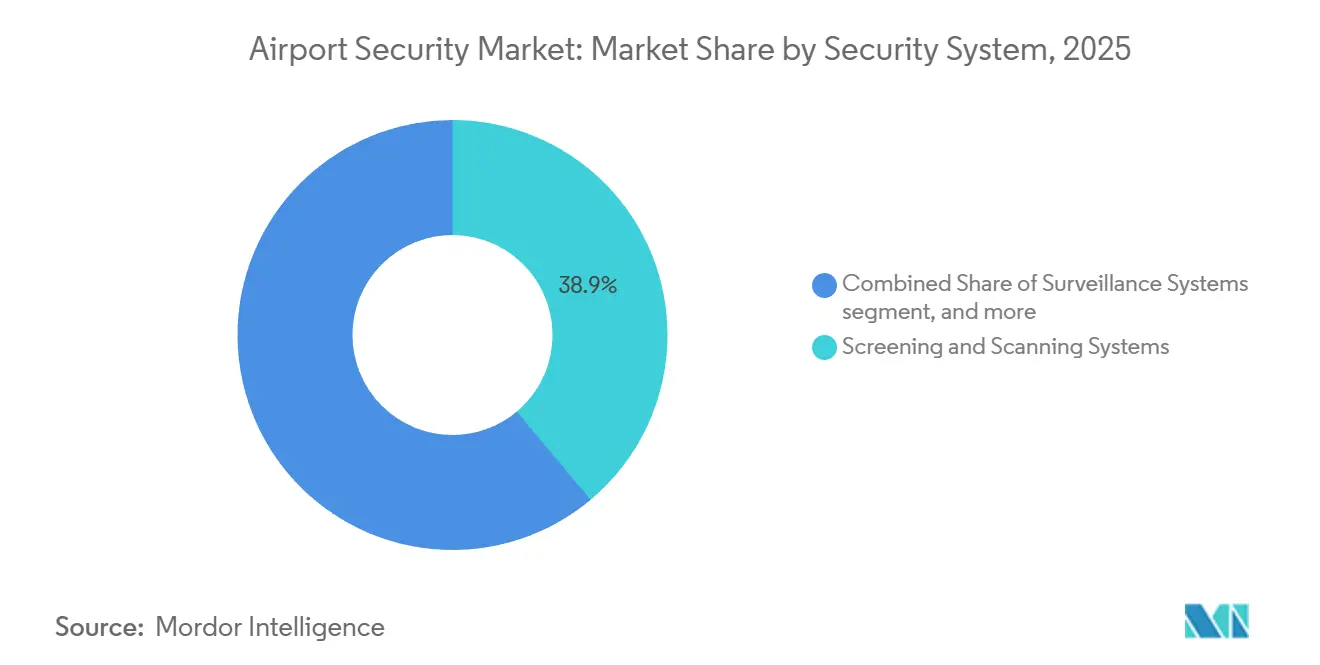

- By security system, screening and scanning accounted for a 38.90% share of the airport security market in 2025; access control and biometrics are forecasted to expand at a 10.75% CAGR through 2031.

- By airport size, hubs processing more than 50 million passengers captured 40.70% of the airport security market size in 2025, whereas the 15-30 million passenger tier is projected to advance at a 10.98% CAGR through 2031.

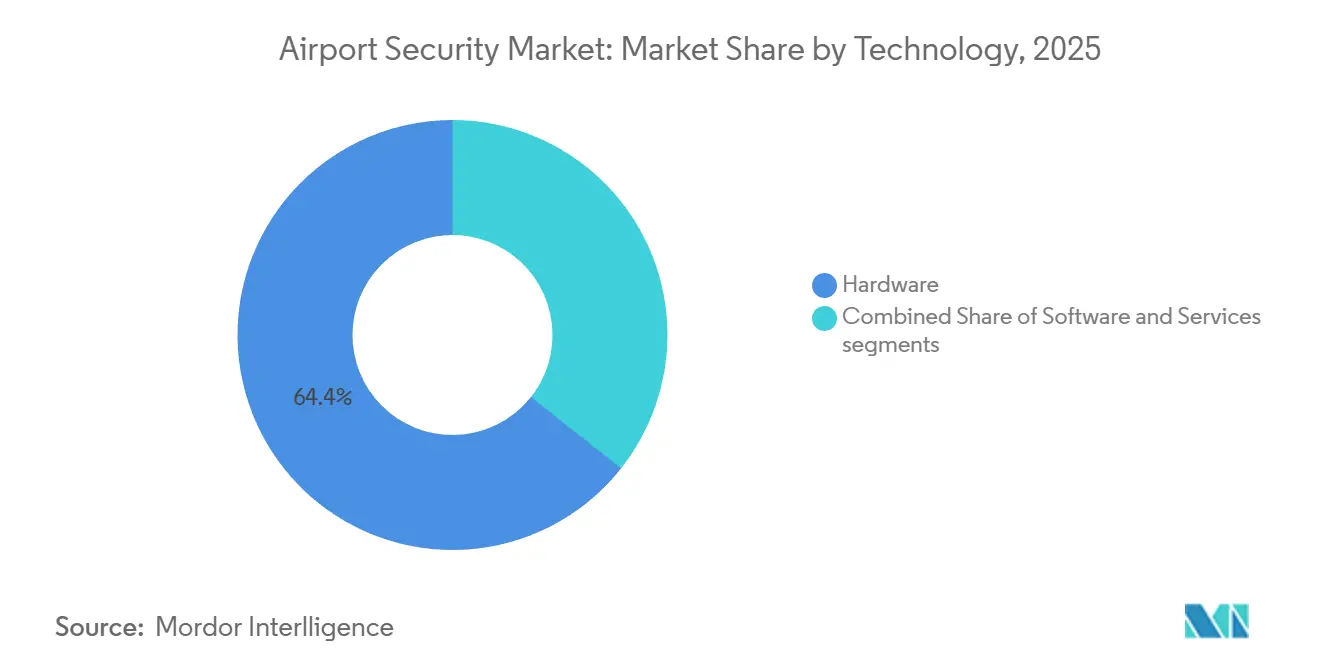

- By technology, hardware accounted for a 64.35% share of spending in 2025, and software is poised to grow at an 11.65% CAGR through 2031.

- By application, terminal zones accounted for 49.85% of 2025 revenue, while perimeter and restricted areas are projected to track a 12.50% CAGR to 2031.

- By geography, the Asia-Pacific region held 36.45% of global revenue in 2025, but the Middle East and Africa are projected to grow at an 11.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airport Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising passenger traffic and touchless screening | +1.8% | Global, APAC and Middle East lead | Medium term (2–4 years) |

| Harmonized international security regulations | +1.5% | Global | Long term (≥ 4 years) |

| Integrated command-and-control (C2) with AI analytics | +1.6% | North America and Europe first adopters | Medium term (2–4 years) |

| Cyber-physical convergence and cloud migration | +1.3% | Global | Long term (≥ 4 years) |

| Biometric One-ID and seamless travel initiatives | +1.9% | APAC core, spill-over to Middle East and Europe | Short term (≤ 2 years) |

| Drone and UAS threats lifting perimeter demand | +1.2% | North America and Middle East | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Passenger Traffic and Touchless Screening

Record volumes now rival pre-pandemic highs, pressuring checkpoints to clear travelers in minutes rather than hours. The TSA installed 2,054 credential-authentication units across 250 airports by October 2025 and plans 3,585 units by 2049, with each device matching a passenger’s face to an encrypted ID in two seconds.[1]Source: Department of Homeland Security Science & Technology Directorate, “AI-Enabled Screening White Paper,” dhs.gov CT scanners deployed at 645 lanes allow passengers to keep liquids in their bags, eliminating bottlenecks that once dampened duty-free sales. Asia-Pacific hubs pilot curb-to-gate flows of under ten minutes, creating a service benchmark that forces legacy airports to accelerate their biometric adoption. Airlines support the transformation, noting a 40% reduction in missed-connection claims at sites running eGates. Health and hygiene preferences that emerged during COVID-19 remain persistent, reinforcing airports’ push for no-touch modalities and maintaining momentum for equipment upgrades despite softer yields in some regions.

Harmonized International Security Regulations

ICAO Annex 17 provides the standard baseline, but national overlays have historically forced vendors to maintain multiple product lines. The ECAC Common Evaluation Process now grants a single clearance across 44 European states, compressing certification time from years to months.[2]Source: Transportation Security Administration, “TSA Technology Modernization,” tsa.gov In parallel, the forthcoming 14th edition of Annex 17 will enshrine digital travel credentials, nudging airports to converge on interoperable biometric standards. The TSA’s 100% explosive-trace requirement for checked baggage contrasts with the statistical sampling still allowed in parts of Europe; momentum favors global parity as risk-based screening formalizes. Harmonization expands the addressable tenders, attracts more bidders, and ultimately lowers unit prices. It increases the upfront cost for entrants that must satisfy intricate cyber-assurance clauses embedded in modern specifications.

Integrated Command-and-Control with AI Analytics

Daily screening generates more than 5.5 million X-ray images at US checkpoints alone, a volume that exceeds the capacity for manual review. Unified platforms now integrate CCTV, perimeter radar, and access-control alerts on cloud dashboards, which push only high-probability anomalies to operators, reducing false alarms by up to 35%. DHS science guidance encourages a shift toward measurement-centric AI that infers material density rather than searching for patterns, resulting in a double-digit percentage reduction in secondary bag checks. Airports subscribe to monthly algorithm updates, severing the historic tie between security innovation and five-year hardware refresh cycles. Shared models propagate threat intelligence across networks, meaning a weapon profile first detected in Dallas can trigger auto-rules in Dubai within hours, without requiring local code rewrites.

Cyber-Physical Convergence and Cloud Migration

Touchless journeys rely on data exchange between credential kiosks, airline DCS, and border control backends, dissolving decades-old air gaps in operational technology. TSA cyber directives now require airports to implement zero-trust segmentation, continuous monitoring, and incident-response plans that parallel those of the power grid. Hyperscale clouds offer resilient uptime but concentrate systemic risk; a regional outage at a single provider could simultaneously ground multiple hubs. 24/7 security operations center coverage is part of their offering. Hybrid architectures are emerging, with edge appliances that enable latency-sensitive inference on-site, while periodic batch analytics are shifted to the cloud. Vendors bundle managed detection and response, filling internal talent gaps and providing 24/7 security operations center coverage as part of their subscription fees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy certification and qualification cycles | -1.2% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Scarcity of skilled aviation security technologists | -0.9% | Global, high turnover in North America and Europe | Medium term (2–4 years) |

| Integration debt from legacy infrastructure | -1.0% | Mature markets | Long term (≥ 4 years) |

| Capex compression amid uneven traffic recovery | -0.8% | Europe and APAC hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Certification and Qualification Cycles

Bringing a new screening modality from prototype to checkpoint can take more than 30 months in the US, where devices must navigate lab tests, live trials, and fleet-wide pilots before being added to the Qualified Products List. Explosive detection for checked baggage faces even longer timelines due to the complexity of classified threat libraries. Europe’s ECAC process shortens the evaluation period but still spans two years. Incumbents exploit portfolio pre-qualification, launching incremental upgrades under existing certificates, while startups burn capital waiting for approvals. Airports delay orders until certificates are finalized, producing a demand valley that slows innovation and stalls return on R&D investment.

Scarcity of Skilled Aviation Security Technologists

Checkpoint automation replaces repetitive document checks with systems that demand higher digital fluency. TSA turnover exceeds 20% at some US hubs, making it challenging to build cumulative expertise. Cybersecurity specialists who can segment OT networks earn premium salaries in finance and healthcare, leaving public-sector airports understaffed. Vendors now bundle training into service contracts, while curricula often lag behind technology shifts. By the time staff master one interface, a next-generation release alters workflows. Dependence on vendor-managed operations increases, eroding institutional knowledge and complicating the integration of multiple vendors over the equipment's life cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security System: Biometrics Gain Momentum

Screening and scanning systems led the airport security market, accounting for 38.90% of the revenue in 2025, following the TSA's rollout of 645 CT lanes that allow passengers to leave liquids and electronics in their carry-ons. Access control and biometrics, however, are forecast to expand at a 10.75% CAGR through 2031 as airports replace manual ID checks with facial recognition, iris matching, and fingerprint verification. The push for seamless travel aligns with airlines' interest in shorter dwell times and higher ancillary revenue. Fingerprint readers remain prevalent for employee access due to cost advantages, but facial scanners dominate passenger flows because travelers do not need to pause to touch equipment. Iris technology has niche applications in restricted areas where false acceptance must approach zero; however, higher sensor costs restrain mass deployment. AI-powered surveillance enhances legacy cameras, alerting operators to instances of loitering, crowd density, or abandoned objects, thereby helping to offset labor shortages. Perimeter intrusion detection capitalizes on multilayer sensor arrays that detect drones, fence cuts, and ground vibrations. Fire and life-safety systems follow predictable replacement cycles, transitioning from Halon to clean-agent suppression in line with environmental regulations. At the same time, cybersecurity budgets rise to secure networks that once operated in isolation.

Second-generation command-and-control suites integrate these subsystems on cloud dashboards, allowing airports to subscribe to continuous software updates instead of multi-year hardware refreshes. Vendors market outcomes, promising queue times below ten minutes, rather than discrete equipment counts. This shift favors suppliers with extensive AI laboratories and large datasets to train models that flag anomalies with fewer false positives. Airports with legacy silos run middleware translators, but long-run economics favor full platform migrations that shed integration debt and deliver single-pane visibility into an expanding threat surface. The airport security market continues to reward solution providers that can balance open standards with turnkey delivery, ensuring airports avoid vendor lock-in while still meeting aggressive deployment timelines.

By Airport Size: Mid-Tier Hubs Move Fast

Hubs handling more than 50 million passengers held 40.70% of the airport security market size in 2025, reflecting capital concentration at gateways such as Dubai International and Beijing Daxing. Airports processing 15 to 30 million travelers are set to grow at the fastest rate, with a 10.98% CAGR, driven by modular cloud platforms that sidestep legacy integration pitfalls. Many mid-tier terminals have opened within the last decade, incorporating open-architecture cabling and IP cameras that support plug-and-play analytics without requiring re-wiring. Subscriptions convert upfront capital expenditures into operating predictable expenses, allowing these operators to scale security in line with traffic rather than making significant lump-sum investments.

Facilities with 5 to 15 million passengers often pursue vendor-managed service contracts, bundling equipment, software, and maintenance into a single per-passenger fee. This model transfers performance risk to suppliers, a compelling proposition for boards wary of technology obsolescence. Airports with fewer than 5 million passengers remain price-sensitive, purchasing metal detectors and 2D X-ray units until regulators compel them to upgrade to CT scanners. Conversely, hubs with 30 to 50 million passengers sit at a crossroads: their traffic justifies modernization, but 1990s-era infrastructure complicates adoption of AI-rich services. Incremental retrofits preserve continuity but prolong heterogeneous environments, whereas clean-sheet terminals in South-East Asia leapfrog with integrated biometric corridors and drone-aware perimeters from day one.

By Technology: Software Accelerates as Hardware Commoditizes

Hardware accounted for 64.35% of 2025 spending, including CT scanners, millimeter-wave portals, perimeter radars, and access gates. However, software revenue is expected to climb at an 11.65% CAGR through 2031, as AI, video analytics, and cloud orchestration deliver the actionable intelligence that end users value most.[3]Source: Department of Homeland Security S&T Directorate, “Measurement-Centric AI,” dhs.gov Measurement-centric AI now infers atomic number and density from image slices, lowering secondary bag pulls and shrinking staffing rosters. Subscription-based software lets vendors iterate monthly, compressing innovation cycles that once tracked hardware depreciation.

Services installation, training, and managed operations grow in lock-step with software, as airports outsource system upkeep to specialists who retain scarce cybersecurity and machine-learning talent. Outcome-based contracts align payments to performance metrics such as queue time or threat-detection rate. The approach reduces capex spikes but inflates opex lines, a shift finance departments manage via five-year rolling renewals. Vendors with vertical stacks that span hardware, software, and services can ensure interoperability. Still, airports mindful of lock-in negotiate data-ownership clauses that ensure algorithm portability at the end of the contract.

By Application: Perimeter Rapidly Scales

Terminal zones generated 49.85% of 2025 revenue, including housing screening lanes, biometric eGates, and surveillance clusters that are critical to passenger throughput. Perimeter and restricted areas, however, are forecast to post a 12.50% CAGR through 2031, as drone incursions, fuel farm sabotage risk, and regulatory focus shift spending beyond the terminal envelope. Multi-sensor arrays, combining radar, RF, optical, and acoustic detectors, classify drones within seconds, with AI identifying only credible threats to human operators. Airside deployments now integrate video analytics that alert ramp crews to foreign-object debris or unscheduled vehicle movements, cutting runway incursion risk and associated regulatory fines.

Landside nodes, parking decks, ride-share curbs, and public-transit portals deploy automatic number plate recognition and vehicle screening to prevent car-bomb attacks. Cargo facilities confront unique challenges; 100% screening mandates interact with diverse package shapes, driving the adoption of explosive-trace portals and canine patrols. Application spending ultimately tracks threat proximity: Middle Eastern airports allocate outsized budgets to perimeters due to geopolitical instability, while North American hubs emphasize terminal throughput to absorb rising traveler counts without expanding physical footprints.

Geography Analysis

Asian megahubs such as Beijing Daxing, Delhi Indira Gandhi, and Singapore Changi collectively accounted for more than one-third of the global airport security market revenue in 2025, reflecting sustained double-digit traffic growth and government-backed biometric mandates. India alone enrolled millions of domestic passengers into Digi Yatra, demonstrating a scalable cloud-native identity infrastructure that sidesteps legacy constraints. China’s five-year aviation plan earmarks cloud command centers for every gateway handling over 20 million fliers, embedding AI anomaly detection and drone-aware perimeters as baseline specifications. Regional low-cost carriers support security automation because faster boarding unlocks additional aircraft rotations, enhancing profitability.

The Middle East and Africa are projected to experience the fastest compounded growth, driven by state-funded mega-projects strategically positioned to capture east-west transfer traffic. Saudi Arabia’s King Salman International, budgeted at USD 31 billion, combines perimeter radar fences, biometric boarding, and cloud-hosted security orchestration from day zero. Qatar’s Hamad International adds AI-video modules that detect micro-crowd surges, preventing queue spill-back during pilgrimage peaks. African investment concentrates in South Africa, Kenya, and Morocco, often under vendor-financed contracts that align payments with passenger fees. Multilateral banks sponsor upgrades to regional gateways along the African Continental Free Trade Area trade corridors, bundling security modernization with cargo digitization programs.

North America’s mature infrastructure moderates growth, but it still contributes sizable annual budgets as the TSA upgrades its checkpoint CT and credential-authentication fleets. Federal grants co-finance perimeter drone-detection pilots in Miami and Los Angeles, creating reference sites for regional airports seeking to replicate layered defenses. Europe’s recovery lags behind its eastern peers, which pressures capital expenditures. However, harmonized certification under ECAC reduces procurement friction once financing aligns. Southern American hubs pursue phased modernization; São Paulo Guarulhos focuses on checkpoint automation, while Santiago de Chile invests in perimeter fiber optics after a 2024 cargo heist highlighted blind spots.

Competitive Landscape

The airport security market exhibits a moderate level of concentration, with diversified portfolios dominating the landscape, while specialist firms focus on niches such as AI, radar, and cyber defense. Five integrated suppliers, Smiths Detection, Rapiscan (OSI Systems), Leidos, Thales, and Honeywell, control a significant share of large-hub contracts. These companies leverage pre-qualified product families to streamline procurement processes. For instance, OSI Systems reported USD 294 million in revenue from its Security segment during Q1 of fiscal 2025, demonstrating hardware resilience despite margin pressures caused by the commoditization of scanners. Meanwhile, software and analytics remain fragmented, with startups offering API-ready modules for behavior detection, drone classification, and material recognition that integrate with existing hardware. Airports prefer this modular approach as it fosters innovation without rendering current assets obsolete, while also reducing vendor lock-in, which previously supported premium pricing models.

Strategic initiatives in the airport security market revolve around three primary approaches. Vertical integration involves hardware OEMs acquiring AI-focused companies to deliver comprehensive end-to-end solutions. For example, Honeywell's acquisition of Sine enhanced its visitor management capabilities. Geographic expansion sees Western incumbents partnering with local integrators to secure contracts in regions such as India, Indonesia, and Saudi Arabia, effectively navigating offset requirements. Outcome-based contracting is also gaining traction, with vendors guaranteeing lane throughput and system uptime, charging airports based on the number of passengers processed rather than upfront capital expenditures. This approach aligns vendor and airport interests but shifts performance risks to suppliers, favoring those with strong remote-support capabilities.

White-space opportunities are emerging in the convergence of cyber and physical security. Airports require solutions such as OT-specific firewalls, network segmentation, and incident-response orchestration, creating niches for specialists like Cyberbit and Claroty. Perimeter-intrusion detection remains a competitive area, with companies like Senstar integrating fence-mounted fiber optics with AI video analytics, and Rohde & Schwarz combining RF sensors for counter-drone defense. Additionally, patents related to biometric liveness verification and AI-driven threat scoring serve as critical intellectual property assets. The airport security industry continues to strike a balance between consolidation at the integrated-system level and the dynamic innovation driven by startups, ensuring a steady evolution of features and capabilities.

Airport Security Industry Leaders

Thales Group

Smiths Detection Group Ltd. (Smiths Group plc)

Leidos, Inc.

Rapiscan Systems, Inc. (OSI Systems, Inc.)

Honeywell International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: OSI Systems, Inc. secured a USD 36 million contract to deploy and maintain advanced airport screening solutions at a major international airport in the Middle East. This development underscores the growing demand for advanced aviation security technologies, driven by rising passenger volumes and evolving security threats. The inclusion of systems such as the Orion 920CT, Rapiscan TRS, Orion 935DX, and Itemiser 5X underscores the strategic emphasis on integrating advanced screening and detection capabilities. This contract positions OSI Systems as a key player in the global aviation security market, reflecting the industry's focus on operational efficiency and safety enhancements.

- February 2025: Leidos, Inc. and SeeTrue collaborated to enhance airport security and customs screening processes by utilizing AI algorithms designed to detect prohibited items.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the airport security market as every hardware, software, and managed-service layer that protects civilian passenger airports, from curbside to perimeter fences, covering screening, surveillance, access control and biometric systems, perimeter intrusion detection, fire-life safety sensors, cybersecurity gateways, and integrated command platforms.

Scope Exclusion: Solutions dedicated solely to cargo-only terminals, military airbases, or off-airport parking facilities lie outside the present scope.

Segmentation Overview

- By Security System

- Screening and Scanning Systems

- Surveillance Systems

- Access Control and Biometrics

- Fingerprint Recognition

- Facial Recognition

- Iris and Retina Recognition

- Perimeter Intrusion Detection Systems

- Fire and Life-Safety Systems

- Cybersecurity and Network Protection

- Command, Control, and Integration Platforms

- By Airport Size

- Less than 5 Million

- 5 to 15 Million

- 15 to 30 Million

- 30 to 50 Million

- More than 50 Million

- By Technology

- Hardware

- Software

- Services

- By Application

- Terminal

- Airside

- Landside

- Perimeter and Restricted Areas

- Cargo and Logistics Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed airport operations managers, security integrators, procurement heads, and regional regulators across North America, Europe, Asia-Pacific, and the Middle East. These conversations validated technology adoption curves, average selling prices, and retrofit timelines, helping us refine assumptions surfaced during desk work.

Desk Research

We began by gathering macro indicators and regulatory benchmarks through freely available sources such as ICAO's air-traffic statistics, TSA procurement notices, Eurocontrol capacity dashboards, UNWTO passenger forecasts, and national civil-aviation yearbooks. We then complemented those with company 10-Ks, airport authority annual reports, and news archives from Dow Jones Factiva. Additional insights on installed screening fleets were retrieved from patents via Questel and shipment records on Volza. This triangulation provided baseline volumes, spend patterns, and typical replacement cycles. The sources listed are illustrative; many others were consulted to confirm signals and address data gaps.

Market-Sizing & Forecasting

A hybrid top-down and bottom-up model was built. Passenger throughput, terminal floor area, and mandated screening lanes created a demand pool that we sized annually, which was then corroborated with sampled supplier revenue roll-ups and channel checks. Key variables like checked-bag growth, cybersecurity share of security budgets, biometrics penetration, capital-expenditure cycles, and unit ASP erosion drive the model. Multivariate regression augments trend extension, while scenario analysis adjusts for traffic shocks or regulatory shifts. Where bottom-up estimates lagged, we applied gap-fills using three-year moving averages and peer analogs.

Data Validation & Update Cycle

Every draft model passes anomaly scans and peer reviews before sign-off. We refresh the dataset each year, and interim updates are triggered when material events, such as large framework contracts, new ICAO mandates, or disruptive threats, alter demand trajectories.

Why Our Airport Security Baseline Is Dependable

Published values often diverge because providers apply different scopes, data years, and currency bases. By anchoring figures to passenger-level demand signals and refreshing them annually, Mordor Intelligence offers decision-makers a stable, transparent baseline.

Key gap drivers versus other publishers include their inclusion of off-airport access roads, blending of capital and operating spend, lighter primary validation, and less frequent model refreshes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.36 B (2025) | Mordor Intelligence | - |

| USD 17.25 B (2025) | Global Consultancy A | Broader scope; limited expert validation |

| USD 19.33 B (2024) | Regional Consultancy B | Capital + O&M blended; currency variances unadjusted |

| USD 19.08 B (2025) | Trade Journal C | Secondary-only sourcing; infrequent updates |

Taken together, the comparison shows that our disciplined scope selection, variable transparency, and yearly refresh cadence deliver a balanced midpoint clients can rely on for planning and vendor screening.

Key Questions Answered in the Report

How large is the airport security market in 2026 and what growth is expected?

The airport security market size is USD 17.84 billion in 2026 and is forecasted to reach USD 27.49 billion by 2031, reflecting a 9.04% CAGR.

Which security system segment is growing fastest?

Access control and biometrics are projected to post the highest 10.75% CAGR to 2031 as facial-recognition eGates replace manual ID checks at checkpoints.

Why are mid-tier airports adopting cloud-native security platforms?

Airports processing 15 to 30 million passengers lack heavy legacy infrastructure, so modular cloud tools let them modernize faster and scale spending with traffic volumes.

What drives the surge in perimeter-security spending?

Rising drone incursions and new counter-UAS mandates are pushing airports to add radar, RF, and AI-powered optical sensors around airfields, leading to a 12.50% CAGR in perimeter applications.

Which region will see the fastest airport security investment growth?

The Middle East and Africa are set for an 11.65% CAGR through 2031, anchored by mega-projects such as Saudi Arabia’s King Salman International Airport.

How are vendors adapting their business models?

Suppliers increasingly offer outcome-based contracts that tie payments to queue times or system uptime, shifting risk from airports to providers while encouraging continuous innovation.

Page last updated on: