Airport Security Screening Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

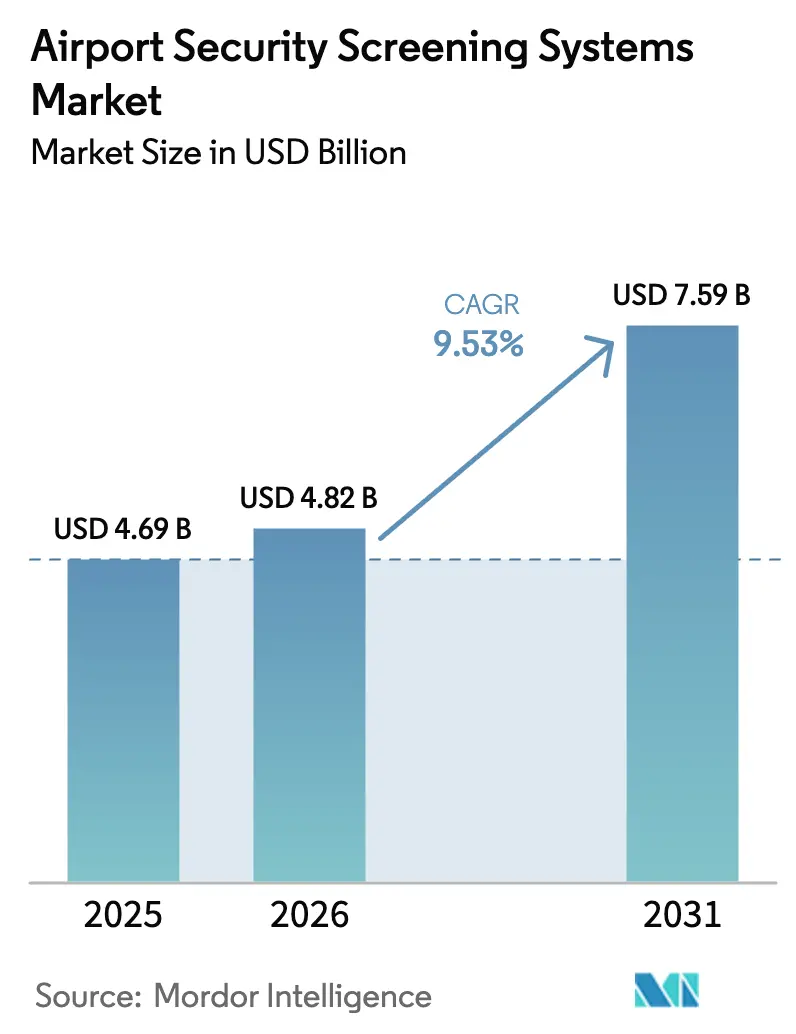

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 7.59 Billion |

| Growth Rate (2026 - 2031) | 9.53% CAGR |

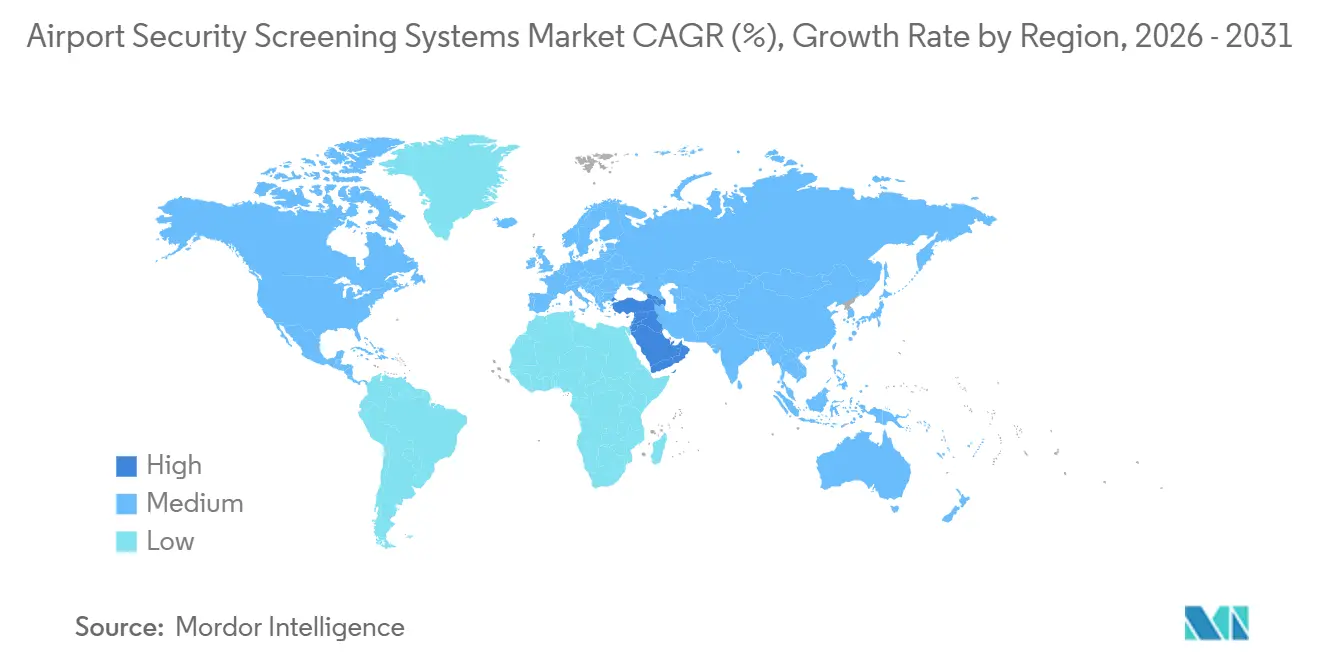

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Security Screening Systems Market Analysis by Mordor Intelligence

The airport security screening systems market size is expected to grow from USD 4.69 billion in 2025 to USD 4.82 billion in 2026 and is forecasted to reach USD 7.59 billion by 2031 at a 9.53% CAGR over 2026-2031. The market is shifting from reactive checkpoint operations to predictive and AI-augmented screening, as airports manage record passenger volumes with limited footprint expansion and prolonged aircraft delivery backlogs. Throughput optimization now centers on computed tomography (CT) scanners and automated lanes that eliminate manual divestment and reduce re-screening, strengthening the case for software-driven upgrades across large installed bases. Regulatory mandates in the United States and Europe hardwire CT adoption and biometric identity checks into procurement roadmaps, which concentrate near-term demand in North America and Europe while accelerating software interoperability under open-architecture standards. Vendor strategies increasingly emphasize recurring software and sustainment revenues as production constraints modulate the pace of new hardware installations.

Key Report Takeaways

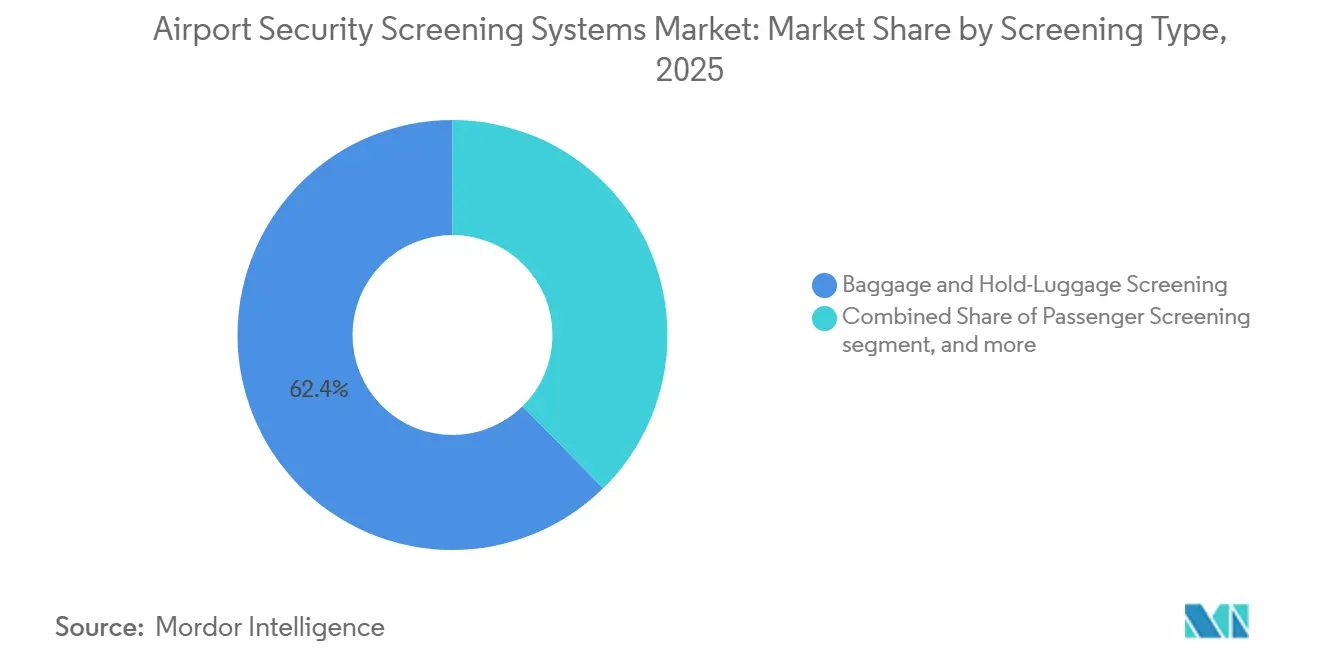

- By screening type, baggage and hold-luggage screening led with 62.36% revenue share in 2025, while cargo and vehicle screening is projected to expand at a 10.67% CAGR through 2031.

- By technology, X-ray screening systems held a 38.67% share in 2025, while computed tomography is forecasted to advance at an 11.25% CAGR.

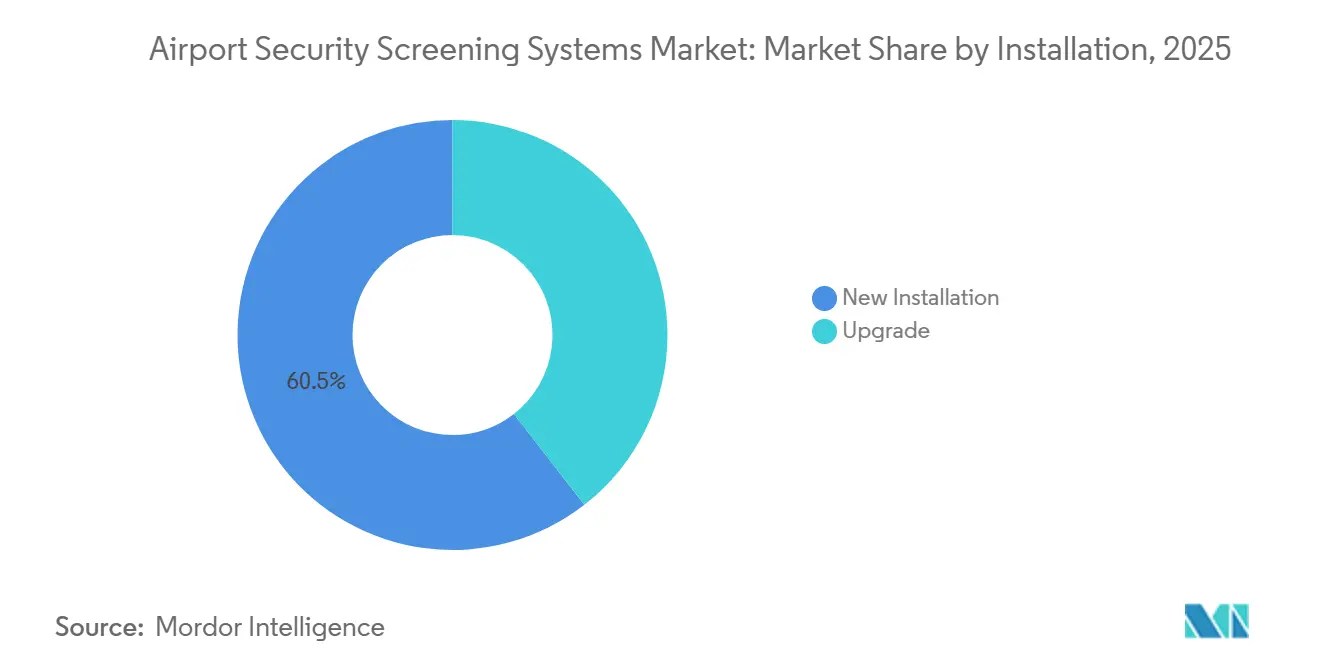

- By installation, new installations accounted for 60.51% of 2025 deployments, while upgrades are set to grow at a 10.49% CAGR.

- By airport size, medium airports captured 45.91% of 2025 installations, while large airports are projected to grow at a 10.93% CAGR.

- By geography, North America accounted for 40.77% of 2025 revenues, while the Middle East is expected to post a 11.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airport Security Screening Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global air-passenger traffic post-COVID recovery | +2.8% | Global, with Asia-Pacific and Middle East leading; North America lagging | Medium term (2-4 years) |

| Heightened terrorism threat and regulatory mandates (e.g., TSA ACSTL updates) | +2.1% | Global; US, EU core with spillover in Middle East and Asia-Pacific | Long term (≥ 4 years) |

| Mandatory transition from 2D X-ray to CT scanners in US and EU airports | +2.6% | North America and EU core; emerging in Middle East and South America | Medium term (2-4 years) |

| Adoption of AI-powered automated threat recognition to cut queue times | +1.4% | Global, early at flagship hubs; Tier-2 adoption post-2027 | Short term (≤ 2 years) |

| Shift to contact-less biometric screening for hygiene and throughput gains | +1.2% | North America, EU, Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Demand for centralized remote image analysis to optimise screener staffing | +0.9% | US national hubs, networked European airports, Middle East mega-hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Global Air-Passenger Traffic Post-COVID Recovery

Total full-year demand in 2025, measured in revenue passenger kilometers (RPKs), increased by 5.3% compared to 2024. Total capacity, measured in available seat kilometers (ASK), grew by 5.2% in 2025.[1] International Air Transport Association, “Strong 2025 Passenger Demand Masks Ongoing Capacity Constraints,” IATA, iata.org IATA shows demand momentum, with regional variation: Asia-Pacific leads, while North America trends slower, shaping deployment priorities for screening capacity. Airports are using CT-based carry-on scanning and automated lanes to eliminate the need to divest electronics and liquids, reducing handling steps and stabilizing lane throughput. Where terminal expansion lags, operators lean on algorithmic enhancements and remote analysis centers to lift effective capacity without physical space increases. The net effect supports sustained investment in CT, credential authentication, and open-architecture software that streamlines decisions under peak loads.

Heightened Terrorism Threat and Regulatory Mandates

Regulatory updates in the US tightened technology qualification for air-cargo screening, with the latest ACSTL versions advancing CT-based EDS standards and scheduling sunset dates for legacy visual image devices.[2]Transportation Security Administration, “Non-SSI Air Cargo Screening Technology List (ACSTL),” TSA, tsa.gov In Europe, the Entry/Exit System went live in October 2025. It will be fully deployed by April 2026 for all non-EU nationals, mandating biometric enrollment at external borders and increasing investments in kiosks and data security controls. The EES workflow embeds identity checks into the passenger flow, which raises the case for integrating checkpoints between screening lanes and border-control systems. In the US, a final rule expanded biometric collection for departing aliens across airports, seaports, and land crossings, thereby extending the relevant infrastructure footprint into terminals. These measures set sustained demand patterns for EDS, CT, and biometric integration under privacy-by-design mandates.

Mandatory Transition from 2D X-ray to CT Scanners in US and EU Airports

Checkpoint CT is embedded in US procurement schedules through multi-year programs that authorize hundreds of base-, mid-, and full-size units to replace 2D systems as production ramps allow. Capital plans cite industry production constraints and prioritize staged deployment, with sustainment budget allocations covering software and logistics support across the installed base. European airports are standardizing on CT as member states refresh cabin-baggage rules and align data-protection controls around biometric workflows and edge processing. Leading hubs have committed multi-year budgets for lane conversions that improve detection and allow liquids and electronics to remain in-bag at scale. Vendors now pair CT hardware with certified AI modules that deliver automated prohibited-item detection and reduce false alarms.

Adoption of AI-Powered Automated Threat Recognition

Algorithm deployments now address checkpoint pain points by lifting detection accuracy while lowering false alarms and manual inspections. Certification of AI modules for CT platforms enables airports to implement software-first improvements that align with open-architecture requirements, such as TSA’s Open Platform Software Library. Partnerships between scanning OEMs and AI specialists aim to unify the detection of weapons, liquids, narcotics, and currency within common interfaces and remote-view workflows. Remote analysis centers connect smaller airports to large-hub demand to balance staffing, thereby raising overall system utilization during daily peaks. The effect is shorter dwell times and greater consistency in lane operations as passenger volumes grow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and long procurement cycles for CT and MMW equipment | -1.8% | Global, acute in Tier-2 and Tier-3 airports across South America, Africa, Southeast Asia | Long term (≥ 4 years) |

| Privacy and health concerns over advanced imaging/biometric data storage | -0.9% | North America and EU with regional variation | Medium term (2-4 years) |

| Semiconductor and detector-grade crystal supply constraints delaying roll-outs | -0.7% | Global supply-chain bottlenecks | Short term (≤ 2 years) |

| Labor-union push-back against job loss from full-automation of lanes | -0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Long Procurement Cycles

Full-size CT units cost more than earlier-generation dual-view systems, which elevates upfront budgets for airports with constrained capital plans. Many operators respond with retrofit kits and algorithm upgrades that extend the useful life and defer full replacements, shifting near-term spending to software and sustainment. Multi-year logistics contracts underscore the need for higher uptime and lifecycle support for large fleets, which further complicates deployment calendars. In Europe, multi-airport programs phase CT adoption over several years as lane conversions and staff certifications proceed in waves. These factors lengthen procurement cycles and space installation windows even where regulatory deadlines are in place.

Privacy and Health Concerns Over Advanced Imaging

Biometric data is regulated as special-category personal data in Europe and requires explicit consent, strict purpose limits, and minimal retention, which raises compliance investment and operational controls. In the US, a patchwork of state laws and proposed federal legislation seeks to regulate biometric collection and opt-out rights, which shape deployment design and passenger experience.[3]Senator Jeff Merkley, “Traveler Privacy Protection Act of 2025,” U.S. Senate, merkley.senate.gov Airports must align checkpoint identity programs with border-control systems that use facial images and fingerprints, as mandated by federal law, while protecting against misuse and overreach. European data-protection authorities have imposed suspensions for insufficient safeguards at individual airports, keeping privacy-by-design at the center of project planning. These rules require robust governance that balances passenger throughput goals with lawful processing and audit trails.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screening Type: Cargo Surges as E-Commerce Outpaces Legacy Passenger Screening

Baggage and hold-luggage screening accounted for 62.36% of 2025 revenues, underpinned by inline EDS mandates and multi-year funding for the Electronic Baggage Screening Program. This subsegment reflects a stable replacement cycle in basements and inline conveyors, where civil works and lane integration pace modernization. Airports favor algorithmic upgrades that increase detection and reduce false alarms on existing machines, which raises the return on installed assets. Passenger screening is advancing rapidly in terms of innovation, as CT carry-on scanners and automated screening lanes increase hourly throughput while eliminating manual divestment steps. Touchless identity programs further streamline checkpoints when combined with credential authentication and risk-based screening.

Cargo and vehicle screening is the fastest subsegment with a 10.67% CAGR through 2031, supported by e-commerce parcel growth and customs programs that prioritize radiation identification and explosives trace detection. US cargo-screening and international deployments add capacity through portal systems and integrated trace units under turnkey contracts. As production limits slow checkpoint CT rollouts, software portability and open interfaces enable best-of-breed analytics to spread across lanes and cargo facilities. Airports that coordinate remote adjudication across networks gain staffing leverage and decision-making consistency, thereby increasing the appeal of centralized resolution rooms.

By Technology: CT Ascends While Dual-View X-Ray Fights Obsolescence Through Algorithm Retrofits

X-ray and dual-view systems retained a 38.67% share in 2025 due to installed-base inertia and conveyor compatibility, yet many units face parts obsolescence over the plan period. OEMs extend life through modular kits that add dual-energy analysis and AI-based detection to legacy tunnels, which provides a cost-effective bridge to CT. As European checkpoints phase in CT and align data safeguards, the 2-D approach sunsets in carry-on applications at large hubs. Dual-view retains utility in specific secondary or oversize lanes where throughput and cost profiles remain favorable.

Computed tomography (CT) is projected to grow at a 11.25% CAGR as multi-award programs expand the number of base-, mid-, and full-size checkpoint units and drive software certification for automated detection. National capital plans highlight production constraints and allocate spending for sustainment to keep systems operational as deliveries scale. Millimeter-wave AIT remains critical for on-person screening with algorithm updates that reduce false alarms and streamline the pat-down process. As biometric e-gates and credential authentication systems take over identity checks, metal detectors and manual ID verification play reduced roles inside modernized lanes.

By Installation: Upgrades Accelerate as Airports Retrofit Legacy Systems to Defer Full-Scale Replacement

New installations accounted for 60.51% of 2025 deployments, driven by multi-terminal CT carry-on investments at leading hubs and next-generation hold-baggage screening in Asia and the Middle East. Program planning across regions ties lane conversions to workforce training and operational trials that validate AI models in live conditions. Large hubs drive adoption first, while mid-tier airports follow once sustainment budgets and retrofit paths address the realities of the installed base.

Upgrades grow at a 10.49% CAGR as airports prioritize algorithm enhancements and dual-energy retrofits that deliver meaningful detection gains at a fraction of the cost of a complete CT replacement. TSA’s budget lines for AT, CPSS, and CAT show a strong sustainment and software posture that supports phased modernization. Open-architecture requirements, such as OPSL, enable third-party algorithms to run on incumbent platforms, reducing vendor lock-in and enabling targeted capability upgrades. These dynamics keep upgrade activity high even when new-installation funds are constrained, supporting consistent fleet performance and availability.

By Airport Size: Large Hubs Automate Faster While Medium Airports Dominate Installations by Volume

Medium airports accounted for 45.91% of 2025 installations, underscoring the need to add screening capacity ahead of full traffic rebounds and to meet emerging regulatory standards. These airports blend mid-size CT deployments with retrofit kits and algorithm enhancements that fit budget cycles. Procurement pacing reflects staffing transitions, operator certifications, and coordination with federal sustainment frameworks. Their approach balances compliance and cost control while aligning with open-architecture software strategies.

Large airports are the fastest growers, with a 10.93% CAGR through 2031, as integrated automated lanes and remote resolution rooms increase throughput at peak times. Remote screening platforms connect multiple terminals and offsite centers, pushing images to trained analysts in real time and maintaining flow control during demand spikes. Small airports benefit from networked staffing models that tap underused capacity to support hub operations during concentrated banks. This mix of local and remote analysis accelerates learning curves and spreads best practices across airport networks.

Geography Analysis

North America accounted for 40.77% of 2025 revenues, as TSA appropriations supported checkpoint property screening, CT, and credential authentication programs, as well as a long-term sustainment contract. Passenger traffic recovery trailed global averages, compressing upgrade urgency at some smaller airports, while large hubs advanced biometric e-gates and automated lanes to offset staffing pressure. Procurement and sustainment programs maintained focus on uptime, cybersecurity, and predictive maintenance to ensure availability across a diverse fleet. The region’s posture reinforces software-centric improvements and open-architecture compliance to future-proof investments.

Europe accelerated CT adoption while implementing the Schengen Entry/Exit System, which requires biometric enrollment for non-EU travelers and places data-protection controls at the core of deployments. Member states moved on lane conversions at large hubs with multi-year budgets and aligned privacy-by-design requirements for facial recognition systems and storage practices. Individual airport projects combined CT installations, automated tray return systems, and software-certified AI modules for prohibited-item detection. National timelines varied, but investment intensity rose at primary hubs while some regional airports deferred conversions pending funding.

The Middle East is set to be the fastest-growing region, with a 11.87% CAGR through 2031, as hubs invest in CT-based carry-on screening and integrated cargo solutions under turnkey contracts. Regional industrial policy includes local assembly of security screening equipment, strengthening supply resilience, and after-sales support. Asia-Pacific momentum is reinforced by hub projects that implement remote baggage screening across sovereign systems using DICOS-compliant data exchange, reducing connection times and extending centralized adjudication models. South America and Africa rarely experience above-average traffic growth, and budget constraints favor retrofit strategies and portable trace detection for remote checkpoints.

Competitive Landscape

The top five suppliers account for a major share of revenues, with Smiths Detection Group Ltd. at the top and Rapiscan Systems, Inc. (OSI Systems, Inc.), Leidos, Inc., Teledyne FLIR LLC, and Nuctech Company Ltd. comprising the remainder, while open-architecture policies reduce traditional lock-in. OPSL enables airports to deploy third-party algorithms across incumbent scanners, which supports software competition and recurring revenue models for vendors. Partnerships pair CT platforms with AI solutions to enhance prohibited-item detection and reduce false alarms. Several OEMs report certification milestones for automated detection modules that can be deployed as upgrades.

Remote screening is a strategic focus as airports decouple image analysis from the checkpoint footprint, which increases staffing flexibility and throughput. Cross-border implementations demonstrate DICOS-standardized data exchange and reduced passenger connection times in live operations, which validates the centralized adjudication model. Turnkey cargo and checkpoint awards in the Middle East illustrate demand for integrated solutions that combine CT carry-on scanning, cargo portals, and explosives trace detection. These moves broaden addressable revenue pools and embed lifecycle services into national aviation programs.

Service and sustainment are expanding as revenue pillars alongside product shipments, reflected in multi-year logistics contracts that include predictive maintenance and cybersecurity. Vendors report rising service revenue as installed bases grow, while product growth continues in CT, cargo systems, and trace detection. Leadership additions and government contract wins demonstrate alignment with regulatory priorities and the convergence of aviation security with broader network and information security requirements.

Airport Security Screening Systems Industry Leaders

Smiths Detection Group Ltd.

Rapiscan Systems, Inc. (OSI Systems, Inc.)

Leidos, Inc.

Teledyne FLIR LLC

Nuctech Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Smiths Detection announced the deployment of its HI-SCAN 6040 CTiX 3D X-ray scanners at London Heathrow Airport as part of a GBP 1 billion (USD 1.37 billion) technology upgrade. This development makes Heathrow the largest airport to fully modernize its security screening process. The CT technology enables passengers to keep liquids and electronics in their hand luggage, improving security efficiency, reducing queues, and enhancing the travel experience across all terminals.

- October 2025: Smiths Detection launched its new airport security solution, the SDX 10080 SCT, in Munich. This high-speed CT scanner incorporates advanced dual-energy technology and an optional high-resolution dual-view line scanner, enabling faster baggage processing, enhanced threat detection, and scalable capabilities designed for future requirements.

Global Airport Security Screening Systems Market Report Scope

Airport security screening systems employ specialized, multi-layered technologies to detect prohibited items, such as weapons, explosives, and liquids, on passengers and in their luggage, thereby ensuring aviation safety.

The airport security screening systems market is segmented by screening type, technology, installation, airport size, and geography. By screening type, the market is segmented into passenger screening, baggage and hold-luggage screening, and cargo and vehicle screening. By technology, the market is segmented into X-ray screening systems, computed tomography (CT), millimeter-wave and advanced imaging technology (AIT), metal detectors, explosives trace detection (ETD), and biometric screening. By installation, the market is segmented into new installation and upgrade. By airport size, the market is segmented into large airports (over 30 million passengers per annum), medium airports (10 to 29 million passengers per annum), and small airports (less than 10 million passengers per annum). The report also covers the market sizes and forecasts for the airport security screening systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Passenger Screening |

| Baggage and Hold-Luggage Screening |

| Cargo and Vehicle Screening |

| X-Ray Screening Systems |

| Computed Tomography (CT) |

| Millimeter‑Wave and Advanced Imaging Technology (AIT) |

| Metal Detectors |

| Explosives Trace Detection (ETD) |

| Biometric Screening |

| New Installation |

| Upgrade |

| Large (Greater than 30 million passengers per annum) |

| Medium (10 to 29 million passengers per annum) |

| Small (Less than 10 million passengers per annum) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Screening Type | Passenger Screening | ||

| Baggage and Hold-Luggage Screening | |||

| Cargo and Vehicle Screening | |||

| By Technology | X-Ray Screening Systems | ||

| Computed Tomography (CT) | |||

| Millimeter‑Wave and Advanced Imaging Technology (AIT) | |||

| Metal Detectors | |||

| Explosives Trace Detection (ETD) | |||

| Biometric Screening | |||

| By Installation | New Installation | ||

| Upgrade | |||

| By Airport Size | Large (Greater than 30 million passengers per annum) | ||

| Medium (10 to 29 million passengers per annum) | |||

| Small (Less than 10 million passengers per annum) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current airport security screening systems market size and growth outlook to 2031?

The airport security screening systems market size is USD 4.69 billion in 2025 and is projected to reach USD 7.59 billion by 2031 at a 9.53% CAGR.

Which segments are leading and which are growing fastest within this space

Baggage and hold-luggage screening leads by revenue at 62.36% in 2025, while cargo and vehicle screening records the fastest growth with a 10.67% CAGR through 2031.

How are regulations shaping checkpoint technology choices in 2026

US programs fund CT adoption and sustainment, while the EU’s Entry/Exit System embeds biometric enrollment at borders, both of which steer airports toward CT, EDS, and integrated biometric workflows.

What role does AI play in improving lane throughput and detection

Certified AI modules for CT platforms reduce false alarms and support automated prohibited-item detection, and remote screening enables offsite resolution that stabilizes throughput at peak times.

Which regions are setting the pace for deployments

North America leads in spend and fleet sustainment, while the Middle East shows the fastest growth on the back of CT carry-on investments and turnkey cargo projects.

How are airports balancing high CT capex with budget limits

Many operators favor retrofit kits and AI upgrades on existing systems to defer full replacement, supported by open-architecture standards and long-term sustainment contracts.

Page last updated on: