Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 0.91 Trillion |

| Market Size (2031) | USD 1.17 Trillion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Infrastructure Market Analysis by Mordor Intelligence

The aviation infrastructure market size is expected to grow from USD 0.87 trillion in 2025 to USD 0.91 trillion in 2026 and is forecasted to reach USD 1,17 trillion by 2031 at a 5.13% CAGR over 2026-2031. Growth is supported by sovereign investments in green-field hubs across the Asia-Pacific and the Middle East, the retrofit cycle in mature economies, and airlines’ pivot to contactless processing, which pulls forward terminal automation spending. EPC contractors are reshaping their offerings around design-build-finance packages, while concession operators seek revenue certainty through 25–30-year leases that bundle aeronautical fees with retail upside. Lifecycle cost optimization, rather than headline capital outlay, is now the dominant procurement filter, elevating operations-and-maintenance (O&M) providers within the Aviation Infrastructure market. Fiscal volatility and skilled-labor gaps temper near-term momentum, yet dual-use military conversions and vertiport roll-outs widen the medium-term opportunity set.

Key Report Takeaways

- By infrastructure type, airside facilities led with 39.85% of the aviation infrastructure market share in 2025, while landside facilities are projected to expand at a 5.95% CAGR to 2031.

- By airport type, green-field projects captured 52.78% of 2025 spending, but brownfield upgrades are expected to grow at a 5.76% CAGR through 2031.

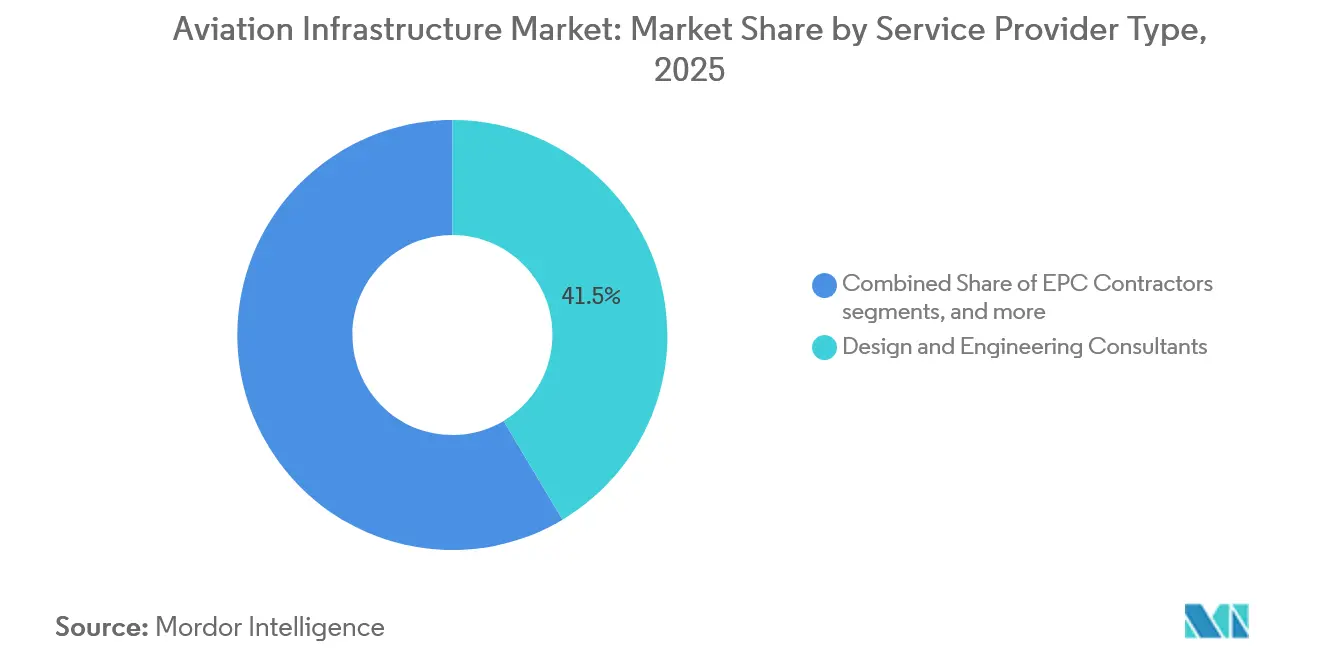

- By service provider type, design and engineering consultancies accounted for 41.45% of the 2025 revenue, whereas O&M specialists are forecast to post the fastest growth, with a 6.11% CAGR during 2026–2031.

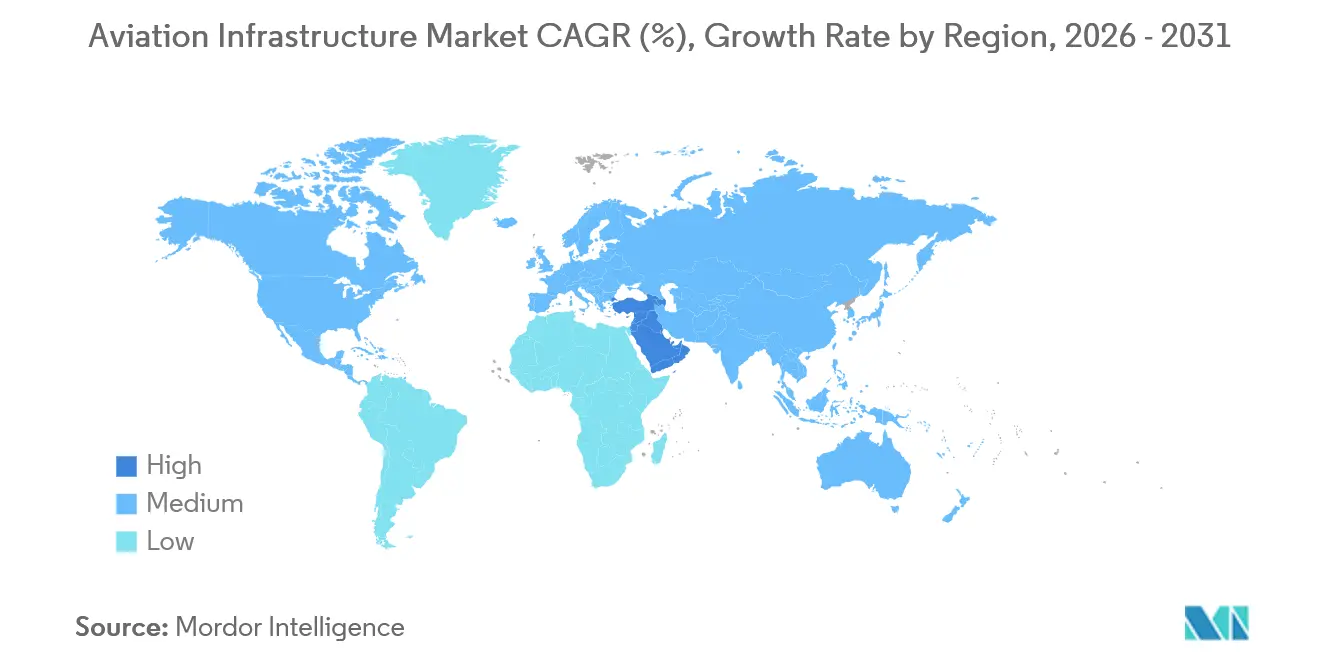

- By geography, the Asia-Pacific region held 37.87% of the 2025 value; the Middle East is projected to expand at a 6.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aviation Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR | Key Geography | Impact Timeline |

|---|---|---|---|

| Surge in green-field airport projects across APAC | +1.20% | Asia-Pacific, spill-over to Middle East | Medium term (2 – 4 years) |

| Modernization mandates for ageing North American terminals | +0.80% | North America and Europe | Short term (≤ 2 years) |

| Airline-led demand for contactless passenger processing | +0.60% | Global | Short term (≤ 2 years) |

| State stimulus for regional/secondary airports | +0.50% | North America, Europe, select APAC | Medium term (2 – 4 years) |

| Military dual-use infrastructure unlocking civil slots | +0.40% | North America, Japan, South Korea | Long term (≥ 4 years) |

| eVTOL vertiport network build-outs | +0.30% | North America, Europe, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Green-Field Airport Projects Across APAC

Beijing Daxing’s third runway pushed its design capacity to 100 million passengers in early 2025.[1]Civil Aviation Administration of China, “Statistics on Daxing Operations,” caac.gov.cn India’s Navi Mumbai International opened in October 2025 with an initial 20 million-passenger throughput and embedded high-speed-rail connectivity that links the site to central Mumbai in 25 minutes. Indonesia awarded a USD 4.2 billion EPC package for a new East Kalimantan airport in March 2025, linking the facility to a planned special economic zone cluster. The Philippines broke ground on the USD 15 billion Bulacan hub in June 2025, specifying on-site sustainable aviation-fuel (SAF) blending as a prerequisite for financing. ICAO’s 2027 SAF compliance trigger is accelerating the adoption of similar specifications across the region.

Modernization Mandates for Ageing North American Terminals

The US FAA disbursed USD 3.2 billion in 2025 under the Airport Infrastructure Grant program, prioritizing HVAC, baggage system, and gate bridge retrofits at terminals over 30 years old. Denver International completed a USD 770 million expansion in September 2025, adding 12 contact gates and eight computed tomography security lanes that cut the average screening time by 22%. Toronto Pearson launched a renovation in April 2025 to install biometric exits at Terminal 1, in compliance with Canadian border-control mandates. The TSA’s January 2025 directive, which compels Category X airports to install 3D scanners by December 2026, compresses procurement timelines and construction windows.

Airline-Led Demand for Contact-less Passenger Processing

Delta Air Lines activated biometric boarding across 15 US hubs in 2025, trimming gate dwell by nine minutes per wide-body flight. Emirates’ iris recognition at Dubai Terminal 3 now processes 2,400 passengers per hour, slashing immigration queues by 40%. IATA’s One ID framework is expected to have 28 participating airports by the end of 2025, with adopters citing 15% lower staffing costs and double-digit gains in satisfaction metrics.[2]International Air Transport Association, “One ID Progress Report 2025,” iata.org In 2025, Lufthansa invested to co-finance biometric infrastructure at Frankfurt and Munich, enabling three extra daily rotations per long-haul aircraft.

State Stimulus for Regional/Secondary Airports

Washington’s Infrastructure Investment and Jobs Act routed USD 5 billion to US regional airports through 2026, funding runway extensions at 23 facilities during 2025. Spain allocated EUR 351 million (USD 412.85 million) to upgrade 14 regional airports with LED taxiway lighting and CAT III instrument landing system upgrades. Japan deployed billions to expand eight secondary terminals, diverting leisure traffic from congested Haneda and Narita. Australia committed AUD 190 million for apron resurfacing and fire-station improvements at 11 regional gateways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR | Key Geography | Impact Timeline |

|---|---|---|---|

| Fiscal tightening curbing PPP funding pipelines | -0.70% | Europe, Latin America, select APAC | Short term (≤ 2 years) |

| Skilled labor shortages in specialized airside construction | -0.50% | North America, Europe, Australia | Medium term (2 – 4 years) |

| Volatile jet-fuel and terminal-access charges reducing airport CAPEX appetite | -0.40% | Global | Short term (≤ 2 years) |

| Local community opposition delaying runway extensions | -0.30% | Europe, North America | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Fiscal Tightening Curbing PPP Funding Pipelines

Euro-zone PPP deal flow fell 18% in 2025 as rate hikes pushed airport IRRs below pension-fund targets, shelving USD 6.2 billion of projects.[3]Financial Times, “European PPP Activity Slumps,” ft.com Gatwick withdrew a GBP 1.2 billion (USD 1.63 billion) second-runway plan in July 2025 after lenders priced debt above 7.5%, which would have required passenger-fee hikes of 22% to meet investment-grade metrics. Similarly India postponed four green-field tenders once capped aeronautical charges pulled modeled IRRs to 6.8%. Multilateral lenders partially fill the gap; the Asian Development Bank’s USD 450 million commitment to Vietnam and the Philippines comes with stringent SAF and carbon-offset covenants that raise project costs by 9%.

Skilled Labor Shortages in Specialized Air-Side Construction

US contractors face 14-month waits for certified airfield electricians and pavement engineers, which delays handovers and activates liquidated-damages clauses.[4]Associated General Contractors of America, “Workforce Survey 2025,” agc.org Britain’s Construction Industry Training Board pegged a 23,000-worker shortfall in 2025 as apprenticeship enrollment slipped 40% since 2020. Australian airfield crews command a 17% wage premium, which widens contractor cost bases and stretches schedules by up to nine months. FAA-accredited lighting-technician programs graduate just 340 students annually against a 680-technician need, underlining a structural gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure Type: Landside Gains on Retail and Automation

Landside assets are forecast to grow at 5.95% between 2026 and 2031, surpassing airside upgrades, despite runways and taxiways holding a 39.85% share of the aviation infrastructure market in 2025. The shift is underpinned by airports’ drive to offset aeronautical-fee pressure through retail concessions, premium parking, and automated baggage systems that cut mishandled-bag rates by 28% at early adopters such as Hong Kong International. Modular terminal builds, codified by AISC standards in 2024, trim on-site labor by 35% and shave a third off schedule durations.

Security infrastructure accelerates in response to the TSA’s 3D-scanner mandate, while EASA’s stringent fire-suppression rules for terminals exceeding 100,000 square meters intensify retrofit efforts. Amsterdam Schiphol’s EUR 45 million (USD 50.9 million) hydrant-system upgrade in May 2025 enables 30% SAF blends across all gates, attracting carriers with published carbon-reduction commitments. Electric ground-support fleets at Los Angeles International Airport eliminate 1.2 million liters of diesel annually, aligning with California's zero-emission timelines.

By Airport Type: Brownfield Expansions Accelerate

Although greenfield hubs accounted for 52.78% of the 2025 spend, brownfield programs are expected to outpace them at a 5.76% CAGR through 2031. Heathrow’s GBP 2.3 billion (USD 2.89 billion) Terminal 2 enlargement and Paris-CDG’s EUR 1.6 billion (USD 1.67 billion) Terminal 1 upgrade leverage existing airside footprints to avoid protracted land-use reviews. Brownfield timing constraints create night-shift premiums that inflate labor cost by 22% yet still undercut the multiyear permitting cycle facing green-field proposals.

Adaptive reuse is trending; in July 2025, Chicago O’Hare transformed a 1960s cargo shed into a nine-gate concourse, saving USD 140 million and preserving a historic structure. FAA continuous-safety auditing adds USD 2.8 million in inspection overhead for a typical 10-gate expansion; however, operators accept the premium to sidestep the hurdles associated with green-field land acquisition.

By Service Provider Type: O&M Providers Capture Lifecycle Value

Design consultancies commanded 41.45% of 2025 service revenue; however, O&M specialists are set to grow at a rate of 6.11% per year, as concession models prioritize lifecycle performance over the lowest-bid construction approach. VINCI’s 30-year Belgrade concession and Ferrovial’s 25-year Dalaman award illustrate the pivot, with earnings tied to passenger throughput and retail income rather than fixed availability payments.

EPC majors, such as Bechtel, are responding by bundling finance and 20-year maintenance guarantees, as evidenced by Bechtel's USD 1.4 billion JFK proposal in August 2025. Predictive-maintenance roll-outs, like Fraport’s IoT sensors that cut baggage-conveyor downtime by 34%, validate the O&M value proposition and underpin a service-driven margin profile.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 37.87% of the value; the Middle East represents the largest regional market in 2026 and is expected to expand at a 6.23% CAGR through 2031. Saudi Arabia’s USD 5.8 billion King Salman International contract aims to serve 120 million passengers by 2035, featuring a dedicated Hajj terminal and a SAF plant. The UAE’s USD 35 billion Al Maktoum expansion will add three runways and a 9 million-square-meter terminal by 2033, positioning Dubai for 260 million passengers a year.

Saudi Arabia’s USD 5.8 billion King Salman International contract aims to serve 120 million passengers by 2035, featuring a dedicated Hajj terminal and a SAF plant. The UAE’s USD 35 billion Al Maktoum expansion will add three runways and a 9 million-square-meter terminal by 2033, positioning Dubai for 260 million passengers a year.

North America held the second-largest % share in 2025, thanks to FAA grant-fuelled retrofits at Denver and Dallas-Fort Worth, while Europe’s 22% slice concentrates on noise-constrained brownfield projects at Heathrow, CDG, and Frankfurt. South America and Africa combined for 12% but drew multilateral backing; Viracopos and King Shaka projects illustrate the trend. The Gulf Cooperation Council’s unified airfield-design code, published in March 2025, cuts engineering spend by 14% across Saudi, UAE, and Qatari tenders.

Competitive Landscape

The aviation infrastructure market remains moderately concentrated, with the top 10 EPC and operator groups accounting for approximately 45% of the contract value. Hensel Phelps, Turner, and AECOM dominate North American terminals under FAA design-build frameworks, while VINCI and Ferrovial expand their concession portfolios to secure 25- to 30-year annuity streams. Chinese SOEs bundle turnkey EPC with concessional China Development Bank finance priced 150–200 basis points below commercial loans, accelerating Belt and Road airport build-outs.

Technology is a wedge; Bechtel’s 14 patents for prefabricated terminal modules slash on-site labor 40% and compress schedules to 22 months. Changi Airport’s digital twin re-optimizes gate allocation, lifting aircraft utilization by 7%. Skyports’ USD 85 million Series B funding positions it as a first-mover in vertiport networks across London, Los Angeles, and Singapore. Consolidation is accelerating; Royal BAM’s 60% stake in a Middle Eastern JV opens pre-qualified access to Saudi Arabia’s pipeline.

Aviation Infrastructure Industry Leaders

Hensel Phelps

Turner Construction Company

Austin Industries

AECOM

VINCI Airports

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Vinci Airports completed Phase 1A of its Cape Verde airport modernization program in 2025, delivering EUR 80 million (USD 93.37 million) in runway, terminal, apron, digital, and decarbonization upgrades, and announced further investments to support traffic growth that has risen 60% since 2022.

- September 2025: Hensel Phelps was chosen as the Construction Manager/General Contractor (CM/GC) for phased Concourse A and terminal improvements at Boise Airport, with a budget of up to USD 700 million. The project, scheduled for completion by 2029, includes adding gates, expanding baggage handling systems, constructing a central utility plant, and enhancing terminal capacity and passenger flow.

Global Aviation Infrastructure Market Report Scope

The aviation infrastructure market includes capital investments and contracted services for the planning, design, construction, upgrading, and modernization of physical and systems-based infrastructure essential for airport and air navigation operations. This market covers airside infrastructure (such as runways, taxiways, aprons, gates, air bridges, airfield lighting, and navigational aids), landside infrastructure (including passenger terminal facilities, baggage handling systems, ground access and parking infrastructure, and infrastructure-related retail and concessions), security and safety infrastructure (such as security screening systems, customs and immigration facilities, and fire and rescue stations), air traffic management systems, fuel infrastructure, and ground support equipment along with associated facilities. It focuses on infrastructure-related capital expenditure, excluding aircraft, airline operations, and non-infrastructure aviation services.

The market encompasses infrastructure development at both greenfield airports (newly developed airports) and brownfield airports (existing operational airports undergoing expansion, rehabilitation, or modernization). From a delivery standpoint, it encompasses activities performed by EPC contractors, design and engineering consultants, and operators and maintenance providers responsible for asset delivery, systems integration, and lifecycle operation and maintenance. The geographic scope is global, covering commercial, regional, and mixed-use civil aviation facilities.

By Infrastructure Type

| Airside Infrastructure | Runways |

| Taxiways | |

| Aprons | |

| Gates and Air Bridges | |

| Airfield Lighting and Navaids | |

| Landside Infrastructure | Passenger Terminal Facilities |

| Retail and Concessions | |

| Ground Access and Parking Infrastructure | |

| Baggage Handling Systems | |

| Security and Safety Infrastructure | Security Screening Systems |

| Customs and Immigration Facilities | |

| Fire and Rescue Stations | |

| Air Traffic Management Systems | |

| Fuel Infrastructure | |

| Ground Support Equipment and Services |

By Airport Type

| Greenfield Airport |

| Brownfield Airport |

By Service Provider Type

| EPC Contractors |

| Design and Engineering Consultants |

| Operators and Maintenance Providers |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Infrastructure Type | Airside Infrastructure | Runways | |

| Taxiways | |||

| Aprons | |||

| Gates and Air Bridges | |||

| Airfield Lighting and Navaids | |||

| Landside Infrastructure | Passenger Terminal Facilities | ||

| Retail and Concessions | |||

| Ground Access and Parking Infrastructure | |||

| Baggage Handling Systems | |||

| Security and Safety Infrastructure | Security Screening Systems | ||

| Customs and Immigration Facilities | |||

| Fire and Rescue Stations | |||

| Air Traffic Management Systems | |||

| Fuel Infrastructure | |||

| Ground Support Equipment and Services | |||

| By Airport Type | Greenfield Airport | ||

| Brownfield Airport | |||

| By Service Provider Type | EPC Contractors | ||

| Design and Engineering Consultants | |||

| Operators and Maintenance Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the Aviation Infrastructure market size in 2026 and what CAGR is expected through 2031?

The sector is valued at USD 0.91 trillion in 2026 and is projected to expand at a 5.13% CAGR to 2031.

Which region represents the largest market in 2026?

The Middle East is the largest regional market in 2026 and is projected to expand at a 6.23% CAGR on the back of mega-hub investments in Saudi Arabia, the UAE, and Qatar.

Why are landside facilities expected to outpace airside spending?

Airports aim to raise non-aeronautical revenue through retail, parking, and automated baggage systems, driving a 5.95% landside CAGR.

What proportion of 2025 investment went to green-field airports?

Green-field projects captured 52.78% of 2025 spending, led by large-scale builds in China, India, and Saudi Arabia.

How do long-term concessions influence service-provider dynamics?

Lifecycle-focused concessions shift emphasis to operations-and-maintenance specialists, who are forecast to grow 6.11% annually through 2031.

What is the primary funding risk facing new airport projects?

Higher interest rates have reduced PPP deal flow, pushing some projects below investor return thresholds and delaying USD 6.2 billion in planned expansions.

How are vertiports shaping future infrastructure plans?

Regulatory approvals for eVTOL services are prompting airports in Dubai, Los Angeles, and Munich to allocate land and capital for purpose-built vertiports.

Page last updated on: