Airport Runway Safety Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

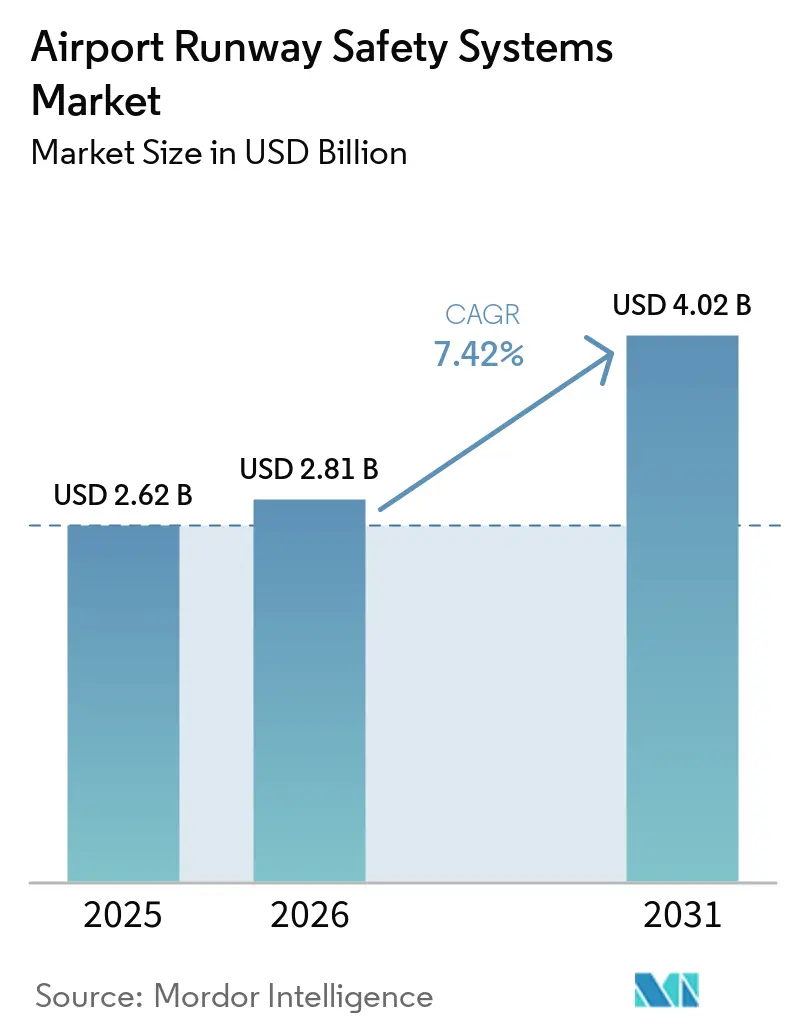

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

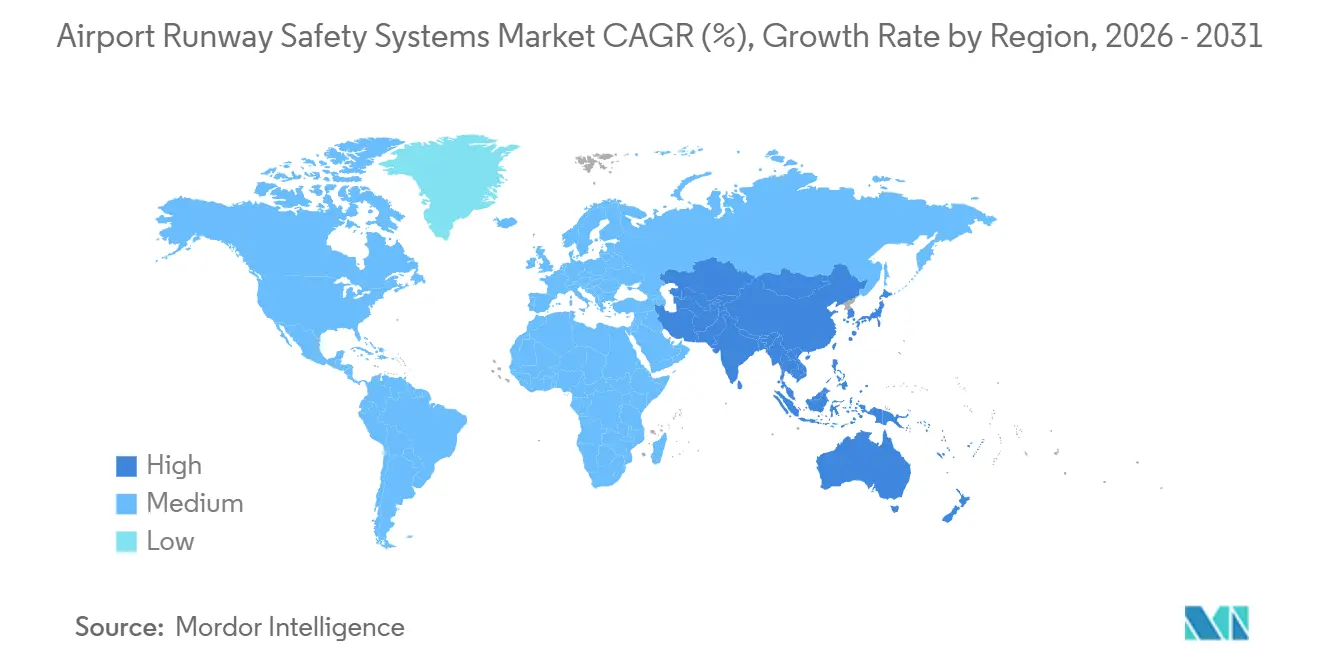

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Runway Safety Systems Market Analysis by Mordor Intelligence

The airport runway safety systems market size is expected to grow from USD 2.62 billion in 2025 to USD 2.81 billion in 2026 and is forecast to reach USD 4.02 billion by 2031 at a 7.42% CAGR over 2026-2031. Runway incursions and related accident categories rose between 2023 and 2024, which kept the airport runway safety systems market in sharp focus for operators and regulators in 2026. In the airport runway safety systems market, policy signals now favor standards-based rollouts, with the FAA’s plan to equip 74 US airports by the end of 2026 guiding procurement schedules and budgets. Technology stacks that blend radar, LiDAR, cooperative ADS-B, and AI analytics are gaining selection preference, as programs in the airport runway safety systems market push for unified situational awareness with lower lifecycle costs. This shift also favors cloud-native deployments, where FAA Surface Awareness Initiative projects illustrate a faster path to fielding capabilities in the airport runway safety systems market.

Key Report Takeaways

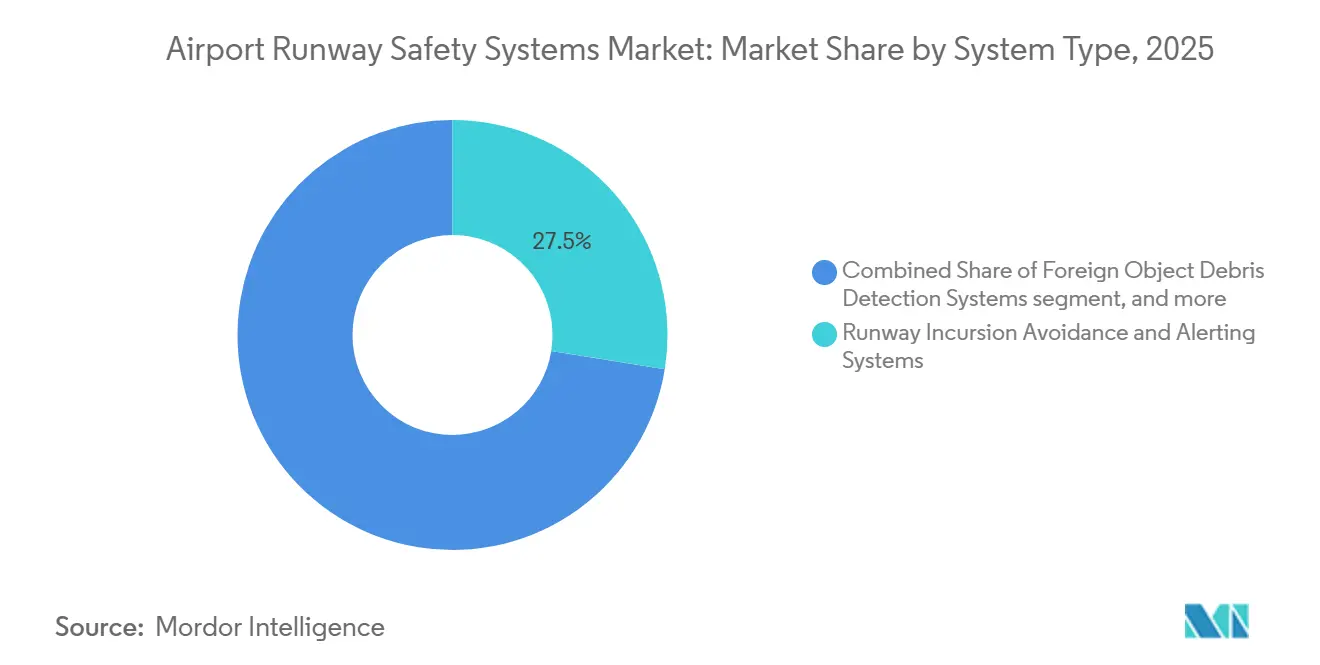

- By system type, runway incursion avoidance and alerting systems accounted for a 27.54% share of the airport runway safety systems market in 2025, while foreign object debris detection is projected to expand at an 8.15% CAGR through 2031.

- By technology, radar accounted for a 33.45% share of the airport runway safety systems market in 2025, while LiDAR is forecasted to record an 8.26% CAGR through 2031.

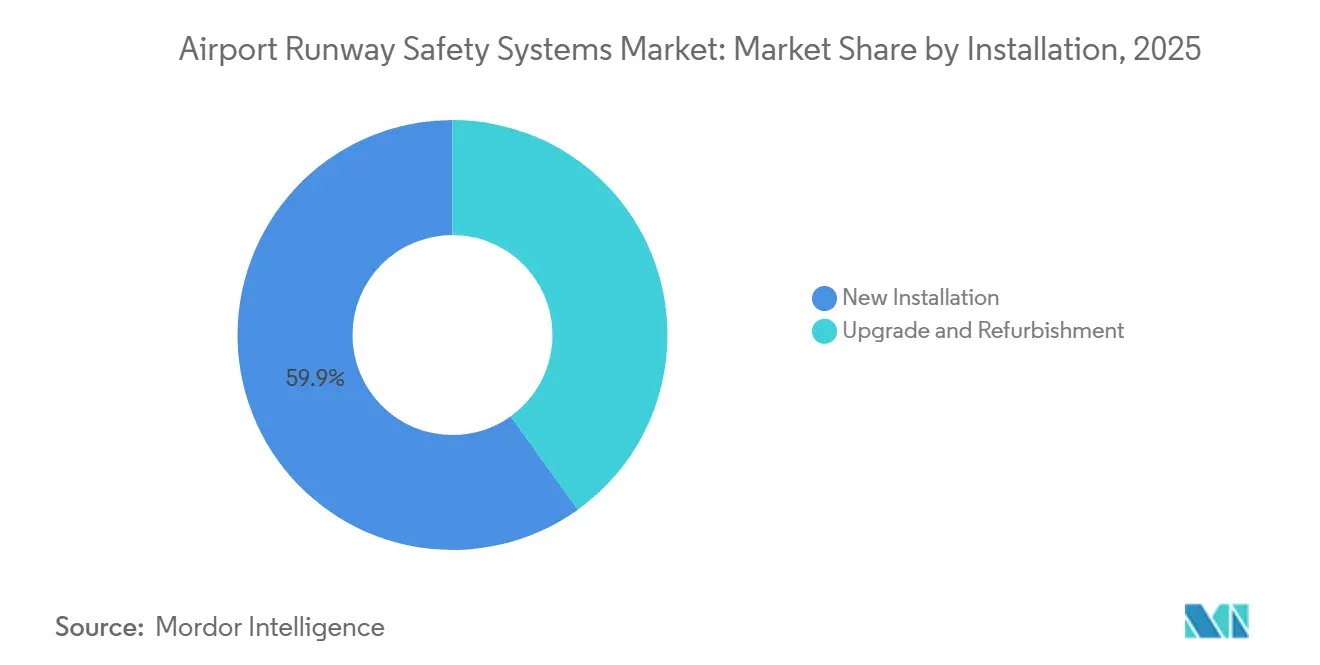

- By installation, new installations accounted for 59.91% of the airport runway safety systems market in 2025 and are projected to grow at a 7.86% CAGR through 2031.

- By end user, commercial airports held 77.23% share of the airport runway safety systems market in 2025, while the segment is projected to advance at an 8.02% CAGR through 2031.

- By geography, North America led the airport runway safety systems market with a 34.56% share in 2025, while Asia-Pacific is projected to post the fastest regional growth at an 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airport Runway Safety Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global air traffic and runway throughput necessitating safety enhancements | +2.1% | Global, particularly Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Stringent international aviation safety regulations driving system adoption | +1.8% | Global, with concentrated enforcement in North America and EU | Medium term (2-4 years) |

| Acceleration of airport modernization and smart infrastructure initiatives | +1.5% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Increased deployment of advanced surface movement and surveillance technologies | +1.3% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing incidence of foreign object debris (FOD) events triggering demand for automated detection systems | +1.2% | Global, with high adoption at major hubs | Short term (≤ 2 years) |

| Integration of AI and data analytics for predictive runway risk management | +0.9% | Early gains in North America and EU, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Air Traffic and Runway Throughput Necessitating Safety Enhancements

Passenger volumes and operations growth sustain demand for layered surveillance, alerting, and cockpit situational awareness tools in the airport runway safety systems market. Airports Council International reported rising traffic in 2024, which is driving higher runway movement density and reinforcing the need for automated conflict detection paired with controller tools. FAA incident data underline how increased operations concentrate risk at busier surfaces, which supports investments in surface awareness and runway status logic. To maintain throughput, new runways and taxiway reconfigurations at major hubs require parallel upgrades to surface movement systems to keep separation standards intact under peak loads. The airport runway safety systems market also benefits from high-frequency training use cases, in which controllers and pilots depend on consistent alerting across varied weather and traffic conditions that exceed manual monitoring limits. This environment sustains a purchasing focus on systems that shorten detection-to-alert intervals and that integrate with tower tools and cockpit advisories without adding controller workload.

Stringent International Aviation Safety Regulations Driving System Adoption

Regulatory programs are compressing decision cycles as safety technology moves from discretionary purchases to mandated capability sets in the airport runway safety systems market. The FAA’s plan to deploy runway incursion devices to 74 US airports by the end of 2026 shows how policy can set a definitive timeline for fielding surface awareness tools.[1]Federal Aviation Administration, “FAA Launches Final Initiative of Runway Safety Portfolio,” Federal Aviation Administration, faa.gov ICAO has elevated runway incursion reduction in multilateral safety planning, underscoring the need to deploy surveillance and alerting capabilities that scale with traffic growth. This momentum benefits established vendors that can absorb certification overhead and align engineering artifacts with audit-ready documentation in the airport runway safety systems market. Operators also use these rule sets to justify reallocation of budget toward multi-sensor fusion platforms that deliver incident-prevention outcomes in regulated environments.

Increased Deployment of Advanced Surface Movement and Surveillance Technologies

Hardware renewal and sensor fusion are reshaping baseline capabilities in the airport runway safety systems market. The FAA awarded Saab AB contracts to modernize surface movement radars at 44 US airports, replacing aging units with solid-state technology designed for higher reliability and lower lifecycle costs. Thales continues to field the RSM NG secondary surveillance radar paired with ADS-B support, a configuration that scales to high target volumes and multiple data outputs for complex airspace.[2]Thales Group, “Thales launches the best-in-class simultaneous civil and military secondary surveillance air traffic radar, the RSM NG / IFF,” Thales Group, thalesgroup.com These platform choices illustrate why the airport runway safety systems market now favors architectures that blend radar, cooperative surveillance, and data fusion. They also show how maintenance risk and obsolescence are managed through modularity, redundancy, and software-defined feature growth in mission-critical environments. With replacement cycles active at major hubs, integrators prioritize systems that maintain service continuity during cutover and that meet evolving cybersecurity criteria without extensive hardware swaps.

Integration of AI and Data Analytics for Predictive Runway Risk Management

Machine learning (ML) is moving the airport runway safety systems market from reactive alerting toward predictive and prescriptive support for tower and cockpit decisions. NASA-backed research published in 2025 validated the use of conservative Q-learning for runway configuration assistance, demonstrating strong compliance with safety constraints in realistic simulations at heavy-traffic airports. Honeywell's SURF-A concept integrates GPS with ADS-B to create cockpit conflict alerts that extend situational awareness beyond the controller's line of sight. Southwest Airlines is enabling SmartRunway and SmartLanding across its B737 fleet to expand stabilized approach and runway awareness cues across diverse operating conditions. Airports are also testing AI-driven perception around aircraft stands, where LiDAR and video analytics can detect debris and ground equipment within safety envelopes before arrivals. As these systems connect to surface surveillance, incident prevention becomes a continuous outcome, which raises the quality threshold across the airport runway safety systems market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment requirements and uncertain ROI for smaller airports | -1.4% | Regional and low-traffic airports, particularly in North America | Medium term (2-4 years) |

| Integration challenges with aging airport infrastructure and legacy systems | -0.9% | North America, Europe | Medium term (2-4 years) |

| Limited funding availability for regional and low-traffic airports | -0.8% | Developing regions, rural airports | Long term (≥ 4 years) |

| Rising cybersecurity risks associated with digital runway safety systems | -0.5% | Global, with acute concerns in critical infrastructure sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements and Uncertain ROI for Smaller Airports

Capital intensity and operating budget constraints make it harder for smaller airports to fund comprehensive surface movement and alerting systems. Even when hardware costs fall, program expenses still include integration, vehicle equipage, staff training, and cybersecurity, which stretch limited funds over several budget cycles. Cloud-native approaches, such as FAA-backed Surface Awareness Initiative deployments, can reduce upfront costs and installation time, helping more sites adopt surface situational awareness without large radar infrastructure. Cooperative ADS-B-based systems simplify installation and enable deployment within 90 days in towered environments, reducing scheduling complexity and service disruption risks. However, recurring fees and cyber compliance requirements pose challenges for smaller operators, who must prioritize revenue-generating initiatives over non-essential system upgrades. This dynamic encourages a modular approach where airports add capabilities in phases tied to operational profiles and seasonal peak patterns.

Rising Cybersecurity Risks Associated with Digital Runway Safety Systems

Digital runway safety systems depend on connected networks, which expand the attack surface and raise assurance requirements. The FAA proposed new cybersecurity criteria for aircraft systems that require risk identification, layered mitigations, and instructions for continued airworthiness, and this standard of care is influencing expectations for ground-based platforms as well. EASA’s information security rules integrate supply chain assurance and vulnerability management into certification pathways, obligating airports and providers to validate end-to-end integrity. A 2025 advisory highlighted a vulnerability in collision-avoidance signaling that could trigger erroneous advisories under spoofed inputs, underscoring the criticality of authentication and resilience measures across RF-dependent functions. These requirements add work to systems engineering and support activities in the airport runway safety systems market, including hardening network segments and adopting zero-trust patterns. For buyers and vendors, cyber assurance planning is now part of the selection checklist and the maintenance playbook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: FOD Detection Systems Lead Innovation Pipeline

Runway incursion avoidance and alerting systems held the largest share of the airport runway safety systems market at 27.54% in 2025, supported by the FAA’s push to add runway incursion devices and programs that enhance cockpit and tower situational awareness. The airport runway safety systems market continues to expand its alerting layer by using GPS and cooperative surveillance signals in cockpit and tower tools, thereby reducing reaction time during complex surface movements. Foreign object debris detection is the fastest-growing system type, with an 8.15% CAGR through 2031, reflecting operator demand for automated runway sweeps and high-confidence detection thresholds under low-visibility conditions. A growing share of deployments pairs fixed optical sensors with ML classification to pinpoint debris, dispatch crews, and log closure timelines for continuous improvement, which aligns with the airport runway safety systems market trend toward predictive field operations. Surface movement surveillance and guidance systems remain a core layer, while cloud-hosted variants shorten installation windows and simplify scaling across multi-airport networks.

Procurement choices now reflect lifecycle thinking with more airports seeking modular systems that integrate with lighting, markings, and vehicle tracking. Large hubs continue to upgrade their surveillance and safety logic, while mid-sized airports adopt ADS-B-based awareness to build toward full A-SMGCS capability over time. Standalone runway lighting and signage are being integrated into broader platforms so operators can adjust and verify configurations under automation rules that align with movement states. Arresting systems and pavement monitoring grow as runways expand and resurfacing cycles accelerate, with LiDAR and vision-based inspection adding measurable gains in inspection reliability. Across these categories, the airport runway safety systems market favors interoperable stacks that enable continuous improvement, with new data informing operating procedures and predictive maintenance after each event or sweep. This approach supports better on-time performance and incident prevention without overloading the controller or crew workflows.

By Technology: LiDAR Disrupts Radar’s Incumbency Advantage

Radar commanded 33.45% share of the technology mix in 2025, while LiDAR is projected to grow at 8.26% through 2031 as airports prioritize millimeter-grade surface awareness and adverse-weather reliability. The airport runway safety systems market has long relied on secondary surveillance radar for surface and approach monitoring, and next-generation units now handle high target volumes and multiple output streams to support complex traffic. LiDAR complements radar by detecting fine debris and surface anomalies at short range with high positional accuracy, which improves both FOD response and apron safety programs. Infrared and optical systems extend detection to night and low-visibility conditions, while AI models improve classification confidence for debris, wildlife, and ground equipment around the movement area. Cooperative ADS-B technologies are being fielded to expand surface situational awareness at towered airports that lack legacy radar coverage, with FAA programs demonstrating rapid deployment and controller usability. The result is an airport runway safety systems market that increasingly favors sensor fusion, where radar confirms targets at range while LiDAR and optical inputs resolve close-in hazards.

Integration priorities now include data fusion platforms that normalize feeds and apply safety logic in accordance with established operational concepts. Airports and ANSPs want technology choices that maintain performance under interference and cyber stress, while providing audit trails and maintenance diagnostics that simplify compliance. Vendors address these needs with modular components, redundant architectures, and cloud-enabled analytics that scale across multiple airports without the need for bespoke infrastructure. As AI models mature, edge processing on cameras and sensors reduces latency and network load, aligning with controller requirements for timely, trustworthy alerts. The airport runway safety systems market continues to converge sensing and analytics so operators can capture full lifecycle value from each data point, from hazard detection to post-incident review. This mix supports more effective safety assurance and shorter intervals between detection and mitigation.

By Installation: New Installations Dominate but Upgrades Gain Momentum

New installations accounted for 59.91% of deployments in 2025 and are projected to grow at 7.86% through 2031, reflecting the growing number of greenfield sites specifying integrated safety ecosystems from the outset. Airports that plan new runways and terminals embed surface movement systems, status lights, and integrated alerting in the base design to avoid retrofit complexity. The airport runway safety systems market also benefits from upgrade cycles at large existing hubs, where older radars and processors are being replaced with solid-state units that carry redundancy and modular serviceability. FAA-backed modernization underscores how replacement programs reduce maintenance loads and improve uptime, directly supporting incident prevention at high-density airports. Parallel cockpit safety enhancements, such as SURF-A and SmartRunway logic, extend the protection layer into flight decks and close gaps in tower-cockpit awareness.[3]Honeywell Aerospace, “SURF-A Surface Alerts,” Honeywell Aerospace, honeywell.com

Upgrade demand is expanding as operators weigh cost, downtime, and cyber posture in tandem. Cloud-native, cooperative surveillance deployments enable airports to stage capability growth, adding coverage and alerting with minimal fieldwork or service interruptions. This sequencing supports return on investment by aligning capital outlays with traffic growth and safety performance targets. New-build and retrofit paths are converging on the same destination, where A-SMGCS Level 3 or Level 4 services guide routing and conflict detection within unified operational concepts. The airport runway safety systems market reflects that convergence by prioritizing sensor fusion, scalable data platforms, and lifecycle support contracts that ensure performance over multi-year horizons. Vendors that can deliver in phases while preserving long-term optionality hold an advantage during multi-airport rollouts.

By End User: Commercial Airports Drive Volume, Military Adds Complexity

Commercial airports held 77.23% share in 2025 and are projected to grow at 8.02% through 2031, supported by sustained passenger traffic growth and expansions at major hubs. Airlines and operators continue to emphasize incident prevention during peak operations, which keeps surface surveillance, runway status logic, and cockpit alerting high on the list of priorities in the airport runway safety systems market. As commercial facilities raise throughput, they pair hardware renewal with data-driven processes, so alerts feed dispatch and inspection workflows. An emphasis on safety culture and automation is now common at Tier 1 airports, where operational resilience is essential for on-time performance. Cloud-enabled surface awareness helps mid-market airports improve baseline visibility, shorten deployment timelines, and reduce maintenance tasks compared with legacy radar estates.

Military requirements shape a parallel track that often influences commercial standards. Defense programs demand hardened software environments, strict certification artifacts, and secure networking that align with modernized OT security practices, driving the adoption of software-defined architectures and real-time operating systems with determinism and safety credentials that can be extended to dual-use scenarios. Over time, these controls flow into commercial procurements, especially where critical infrastructure requirements mirror national security standards. The airport runway safety systems industry is therefore shaped by both commercial and military patterns, with cross-pollination evident in cyber hardening and mission assurance. Vendors that engineer to a higher bar and thoroughly document compliance are positioned to serve both end users.

Geography Analysis

North America maintained leadership with a 34.56% share in 2025, while Asia-Pacific is projected to grow at 8.21% through 2031, underscoring divergent regional maturity across the airport runway safety systems market. US programs that target runway incursion reduction and surface awareness upgrades point procurement toward rapid deployments that fill surveillance gaps at towered airports. Modernization contracts that replace older radars with solid-state units address reliability and maintenance risks at the busiest hubs. These moves pair with cockpit alerting systems that extend safety coverage and align flight crew awareness with tower advisories in the airport runway safety systems market. Together, they produce a layered protection model that scales with operational growth without increasing incident risk in proportion.

Asia-Pacific’s forecast growth reflects network expansions and new runways that adopt integrated safety ecosystems during design. Program choices emphasize A-SMGCS routing and guidance, multi-sensor fusion, and data platforms that support predictive maintenance for airport runway safety systems. LiDAR and optical analytics complement radar in low-visibility conditions, which is important for all-weather operations at busy hubs. Cooperative surveillance fills deployment gaps and accelerates coverage for towered airports without legacy radar estates. Over time, these investments build a balanced stack in which automated detection and alerting help controllers maintain consistent response times during peak flows. Thus, the airport runway safety systems market expects faster growth in capabilities across Asia-Pacific’s expanding networks.

Europe’s trajectory is defined by stringent cyber and information security obligations that now shape solution architectures from the outset. The PART-IS regime requires risk assessments and supplier vetting, which influence integration timelines and the depth of documentation in the airport runway safety systems market. Hubs and networks maintain multi-technology approaches, pairing proven radar with ADS-B and optical sensing to achieve redundancy. Life cycle contracts with extended maintenance windows are common, reflecting a preference for measurable reliability gains and phased feature growth. Across the Middle East and other growth regions, greenfield projects often target turnkey systems with high levels of automation, which sets a high-specification baseline at opening. These approaches converge worldwide on the same objective: a unified surface picture that lowers incident probability through faster sensing and clearer alerts in the airport runway safety systems market.

Competitive Landscape

The supplier ecosystem shows moderate fragmentation. Tier-one aerospace groups such as Honeywell International Inc., Saab AB, and Leonardo S.p.A. command the radar and surveillance segments by leveraging scale and integrated product portfolios. Tier 1 integrators, cloud-native disruptors, and niche specialists define the competitive pattern in 2026. Honeywell International Inc. continues to expand cockpit alerting with SURF-A and SmartRunway, which helps airlines improve runway and approach awareness without waiting for ground infrastructure upgrades. Southwest Airlines is activating SmartRunway and SmartLanding across its B737 fleet, signaling strong airline support for cockpit-based safety augmentation in parallel with airport upgrades. These moves reinforce the role of established primes that combine installed base leverage, certification depth, and extended support in the airport runway safety systems market.

Cloud-native providers target cost and time-to-field as primary differentiators. Saab’s Aerobahn-based Surface Awareness Initiative deployments add controller-facing maps and alerts using cooperative ADS-B and cloud processing, with install cycles measured in weeks rather than months. The vendor also secured contracts to replace legacy surface movement radars with modern solid-state systems at 44 large US airports, underscoring the dual strategy of cloud-first awareness and hardware modernization, where radar remains essential. uAvionix expands cooperative surveillance to towered airports that lack traditional radar, which addresses a sizeable addressable base while aligning with FAA program priorities in the airport runway safety systems market. These offerings show how SaaS, modular sensors, and managed services are reshaping deployment economics.

Niche specialists continue to advance single-technology performance while integrating into larger stacks. AI-driven FOD detection solutions now offer fixed deployments with targeted classification and precision mapping, shortening debris-clearance cycles and enabling predictive maintenance at scale. LiDAR-perception platforms help detect both hazards and ground service conflicts, improving turnaround safety without extending block times. Vendors that demonstrate cyber robustness and documentation quality will gain selection preference, given the rising audit burden now surrounding integrated systems in the airport runway safety systems market. Over time, the balance of contract value continues to shift toward lifecycle services and outcomes-based agreements that align incentives around incident reduction.

Airport Runway Safety Systems Industry Leaders

Honeywell International Inc.

Leonardo S.p.A.

Saab AB

Indra Sistemas S.A.

ADB SAFEGATE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Southwest Airlines selected Honeywell runway safety technology. Southwest Airlines is implementing Honeywell’s SmartRunway and SmartLanding software across its B737 fleet. These systems are designed to enhance runway safety and operational efficiency by addressing potential landing and runway risks.

- June 2025: The US Federal Aviation Administration (FAA) awarded Saab AB a contract to implement its Aerobahn Runway and Surface Safety service across 26 additional US airports. The contract is part of the FAA's Surface Awareness Initiative (SAI) Block 3 deployment, which aims to improve runway safety through technological solutions.

- March 2025: The FAA announced its plans to install enhanced safety technology at 74 airports by the end of 2026 to detect runway incursions by implementing the Runway Incursion Device, which serves as a memory aid for air traffic controllers by indicating runway occupancy status.

Global Airport Runway Safety Systems Market Report Scope

Airport runway safety systems comprise technologies and equipment designed to prevent runway incursions, excursions, and ground collisions during aircraft operations. These systems improve situational awareness, facilitate real-time monitoring, and ensure safe aircraft movement in all weather and visibility conditions. Essential components include runway lighting, surface movement radar, runway status lights, and FOD detection systems.

The airport runway safety systems market is segmented by system type, technology, installation, end user, and geography. By system type, the market is segmented into runway incursion avoidance and alerting systems, surface movement surveillance and guidance systems, foreign object debris (FOD) detection systems, runway lighting and signage, pavement monitoring and management systems, and runway arrestor beds. By technology, the market is segmented into radar, LiDARs, infrared/optical, and others. By installation, the market is segmented into new installations, and upgrade and refubrishment. By end user, the market is segmented into commercial airports and military airports. The report also covers the market sizes and forecasts for major countries across the regions. For each segment, the market size is provided in terms of value (USD).

| Runway Incursion Avoidance and Alerting Systems |

| Surface Movement Surveillance and Guidance Systems |

| Foreign Object Debris (FOD) Detection Systems |

| Runway Lighting and Signage |

| Pavement Monitoring and Management Systems |

| Runway Arrestor Bed |

| Radar |

| LiDARs |

| Infrared/Optical |

| Others |

| New Installation |

| Upgrade and Refubrishment |

| Commercial Airports |

| Military Airports |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System Type | Runway Incursion Avoidance and Alerting Systems | ||

| Surface Movement Surveillance and Guidance Systems | |||

| Foreign Object Debris (FOD) Detection Systems | |||

| Runway Lighting and Signage | |||

| Pavement Monitoring and Management Systems | |||

| Runway Arrestor Bed | |||

| By Technology | Radar | ||

| LiDARs | |||

| Infrared/Optical | |||

| Others | |||

| By Installation | New Installation | ||

| Upgrade and Refubrishment | |||

| By End User | Commercial Airports | ||

| Military Airports | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook of the airport runway safety systems market?

The airport runway safety systems market size is USD 2.62 billion in 2025, reaching USD 2.81 billion in 2026 and USD 4.02 billion by 2031 at a 7.42% CAGR.

Which technology areas are shaping buying decisions most in 2026?

Multi-sensor fusion across radar, LiDAR, cooperative ADS-B, and AI analytics is shaping choices because it raises detection confidence and reduces lifecycle costs.

How are regulations influencing deployment timelines for runway safety?

FAA programs and EASA PART-IS requirements are accelerating deployments by combining safety targets with information security obligations that guide procurement and system design.

What segments lead the airport runway safety systems market and where is the fastest growth?

Runway incursion avoidance and alerting holds the largest share, while FOD detection and LiDAR technology record the fastest growth through 2031.

How do new installations compare with upgrade projects in spending share?

New deployments accounted for 59.91% of 2025 spending and grow at 7.86% CAGR, reflecting greenfield airport builds and regulatory mandates for first-time installations.

Page last updated on: