Market Overview

| Study Period | 2019 - 2031 |

|---|---|

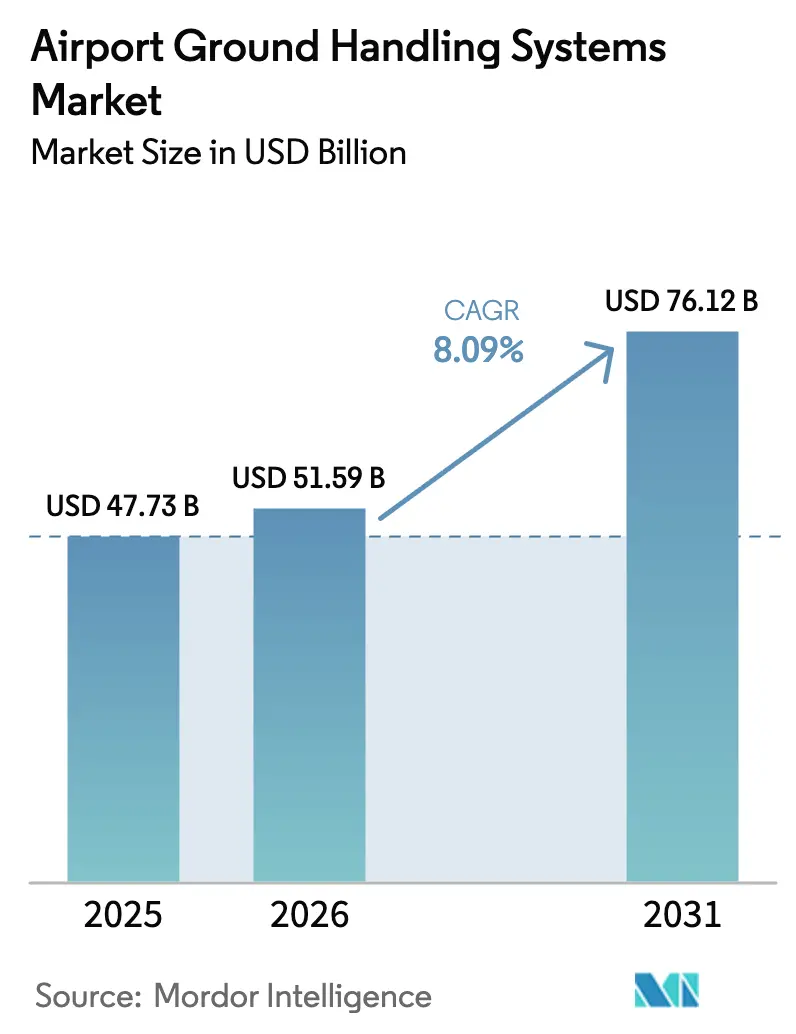

| Market Size (2026) | USD 51.59 Billion |

| Market Size (2031) | USD 76.12 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Ground Handling Systems Market Analysis by Mordor Intelligence

The airport ground handling systems market size is expected to grow from USD 47.73 billion in 2025 to USD 51.59 billion in 2026 and is forecasted to reach USD 76.12 billion by 2031 at 8.09% CAGR over 2026-2031. This growth rhythm mirrors that of slot-constrained hubs, which favor larger aircraft, stricter green-airport mandates, and biometric passenger flows that compress dwell times and boost equipment productivity. The rapid electrification of ground support equipment (GSE) is driving down the cost of lithium-ion (Li-ion) batteries and shortening airports' payback periods to 2 years. At the same time, 5G-enabled asset tracking enhances uptime and reduces maintenance bills. Pooled fleets and GSE-as-a-Service contracts are smoothing the capital expenditure cycles for handlers facing razor-thin margins. Hydrogen pilots, though nascent, are emerging as a hedge against cold-weather battery limits, and autonomous tractors are starting to chip away at apron labor bottlenecks, despite union pushback. Together, these forces reinforce the medium-term upside for the airport ground handling systems market, as airlines anchor their network strategies on quicker turnarounds and lower Scope 3 emissions.

Key Report Takeaways

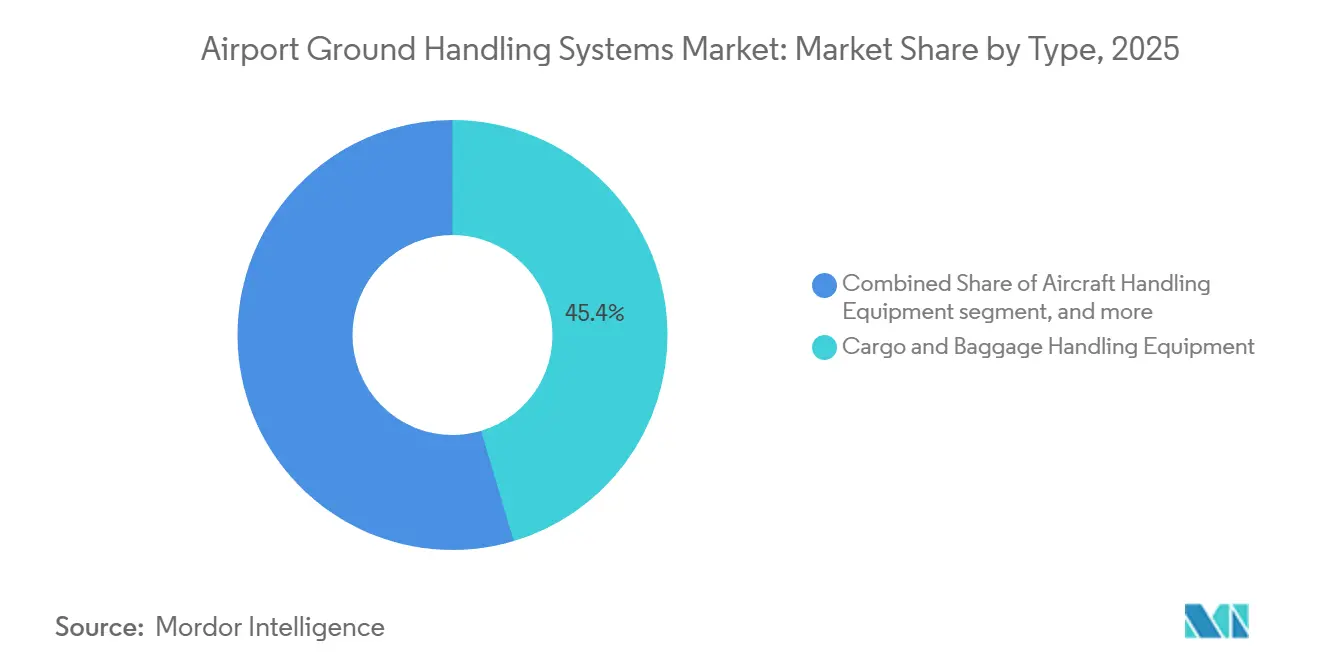

- By type, cargo and baggage handling equipment led the airport ground handling systems market, accounting for 45.40% of the market in 2025. In contrast, passenger handling equipment is forecasted to advance at an 8.98% CAGR through 2031.

- By power source, non-electric platforms accounted for 59.20% of the airport ground handling systems market share in 2025, while electric variants are expected to expand at a 10.05% CAGR through 2031.

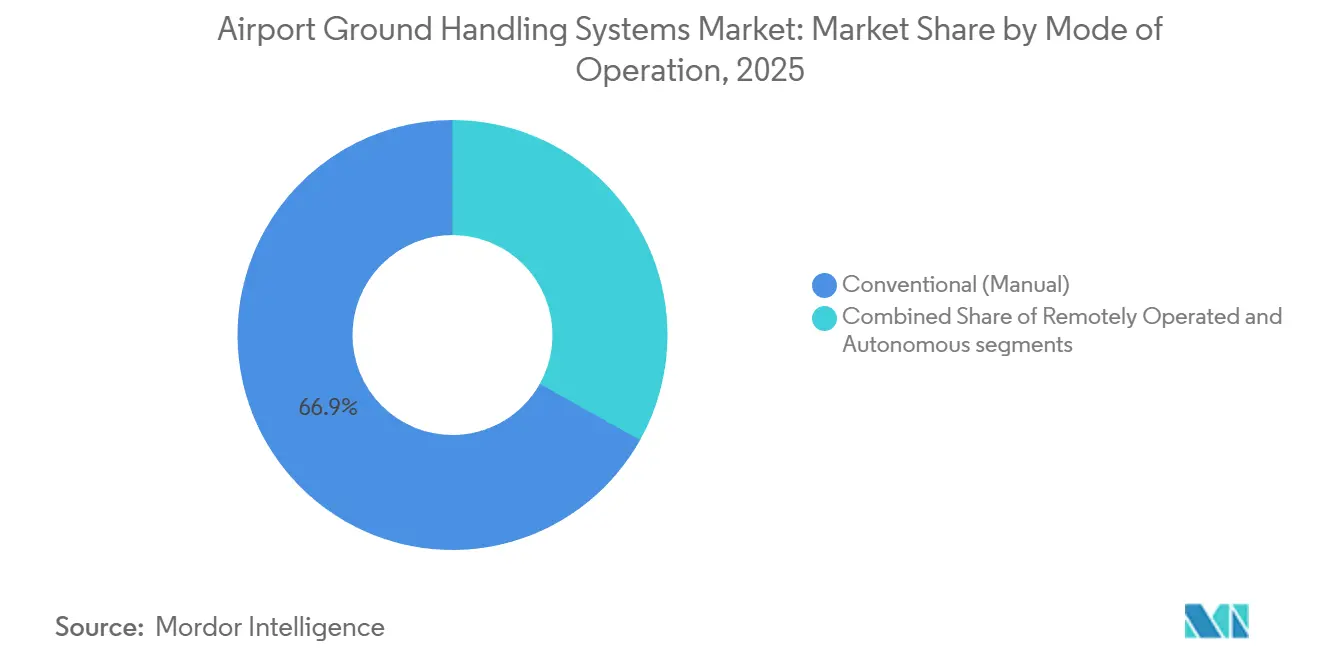

- By mode of operation, conventional manual systems accounted for 66.87% in 2025; autonomous units are projected to record the fastest CAGR of 11.35% from 2026 to 2031.

- By end user, commercial airports accounted for 75.84% in 2025; military installations showed the strongest growth, with a 9.40% CAGR, as defense forces modernized their tactical air-lift support.

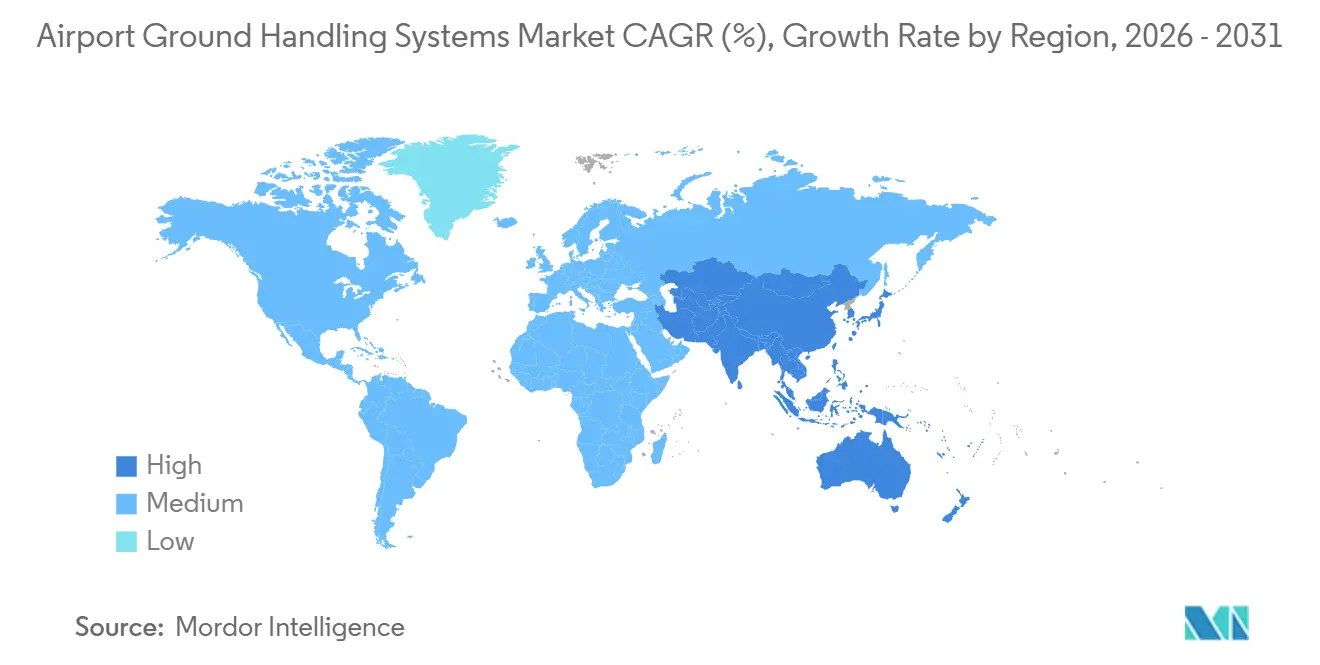

- By geography, the Asia-Pacific region captured 40.54% in 2025 and is set to grow at an 8.90% CAGR through 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airport Ground Handling Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet up-gauging at slot-constrained hubs | +1.4% | North America, Europe, Middle East | Medium term (2-4 years) |

| Surge in green-airport capex programs | +1.6% | Europe, North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Low-touch passenger processes | +0.9% | Global | Short term (≤ 2 years) |

| 5G-enabled asset-tracking and predictive maintenance | +1.1% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) |

| On-airport hydrogen infrastructure pilots | +0.7% | Western Europe, select North America & Asia-Pacific sites | Long term (≥ 4 years) |

| Expansion of GSE-as-a-Service leasing and pooling models | +1.2% | North America, Europe, global secondary hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet Up-Gauging at Slot-Constrained Hubs

Major hubs in London, New York, Tokyo, and Dubai are currently experiencing a shortage of hourly slots, prompting airlines to switch from narrow-body to wide-body aircraft that can carry heavier cargo pallets and accommodate more passengers. This shift boosts demand for high-torque pushback tractors, dual-aisle boarding bridges, and wider cargo loaders that can service A380 and B777X frames without bottlenecks.[1]Source: International Air Transport Association, “Slot Guidelines 2024,” iata.org Heathrow’s Terminal 5 expansion concluded in 2025 with 18 extra wide-body loaders and 12 electric tractors dedicated to A380 operations. Mid-tier Asia-Pacific airports are following the trend, retrofitting their fields for A321XLR use on long, thin routes. OEMs have responded with reinforced chassis, torque-vectoring drivetrains, and modular lift decks to handle the extra mass, all of which increase per-unit GSE prices and improve airlines' throughput metrics. As carriers continue to densify their fleets, the airport ground handling systems market experiences steady replacement cycles and the upselling of premium capacity units.

Surge in Green-Airport Capex Programs

More than 200 European airports have signed ACI Europe’s NetZero 2050 pledge, baking electrification into every capital plan. EASA regulations issued in March 2025 now require any new GSE purchased within the European Union (EU) to deliver lifecycle emissions 40% lower than 2020 baselines.[2]Source: European Union Aviation Safety Agency, “Environmental Protection Requirements,” easa.europa.eu Schiphol earmarked EUR 500 million (USD 586.62 million) for 2024-2028 to electrify its entire fleet and run hydrogen pilots, while the US EPA’s Clean Ports Program allocated USD 3 billion for similar projects at 55 US sites. Bundled vendor financing that wraps equipment, chargers, and multiyear maintenance allows airports to clear budget hurdles and accelerates conversion pipelines. These macro-level sustainability promises provide producers of electric tractors, apron buses, and charging systems for airport ground handling systems with long-term revenue visibility.

Low-Touch Passenger Processes (e.g., Biometrics)

Facial-recognition boarding gates and contactless bag drops reduce the average processing time from 45 minutes to under 25, freeing up gate space and enabling airports to handle more traffic with the same staff count. The US CBP reported a 98% match rate across 32 gateways in 2024, reducing manual checks and enabling staff redeployment to critical turnaround services, such as fueling and catering. Middle Eastern hubs have invested more than USD 200 million in biometric corridors, reducing the demand for additional passenger bridges per aircraft stand. These gains back the 8.98% CAGR in passenger-handling equipment as airports specify IoT-ready boarding bridges that sync real-time occupancy with resource-planning apps. The knock-on effect is higher day-of-operations flexibility and sharper gate reassignment factors that compound throughput and buoy spending in the airport ground handling systems market.

5G-Enabled Asset Tracking and Predictive Maintenance

By year-end 2024, eighteen airports had operational private 5G networks, enabling centimeter-grade tracking of tractors, loaders, and carts. Changi’s pilot fitted 120 vehicles with vibration and thermal sensors, reducing unplanned downtime by 22% and extending fleet life by 18 months. New FAA spectrum guidance secured the 3.7-3.98 GHz band for airport-owned networks, opening the US market for similar deployments. Predictive algorithms alert technicians before battery degradation crosses critical thresholds, a breakthrough that reinforces the use of electric GSE. Airports adopting 5G also tighten driverless vehicle geofencing, enabling stepwise autonomy rollouts and further embedding connectivity as the backbone of the airport ground handling systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical airport capex linked to traffic volatility | -0.8% | Global, heavier in emerging & secondary airports | Short term (≤ 2 years) |

| ROI uncertainty for fully-electric GSE in cold climates | -0.6% | Canada, Northern US, Scandinavia, Russia | Medium term (2-4 years) |

| Air-side labor union resistance to autonomy | -0.5% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| PFAS regulations impacting AFFF-based de-icers | -0.4% | North America, Europe, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyclical Airport Capex Linked to Traffic Volatility

Passenger volumes are expected to recover to 94% of 2019 levels by 2024; however, 38% of airports have postponed GSE purchases to conserve cash and service pandemic-related debt.[3]Source: ACI World, “Airport Economics Survey 2024,” aci.aero FAA records show that US regional airports with fewer than 5 million passengers trimmed their GSE budgets by 22% in 2024, with many diverting funds to urgent runway repairs instead. Emerging-market gateways face additional exchange-rate and credit-rating risks, which can delay electric conversions despite lower lifetime costs. OEM order books thus ride an uneven curve, explaining the -0.8% pull on the airport ground handling systems market. Vendors counter by offering pay-by-hour leases, but volume gaps persist until traffic stabilizes and balance sheets heal.

ROI Uncertainty for Fully-Electric GSE in Cold Climates

Battery capacity falls 20-40% below -10 °C, compelling mid-shift charging that upends turnaround deadlines. Airports like Calgary added heated enclosures that cost USD 15,000-25,000 per tractor, stretching payback beyond five years when diesel prices hover below USD 1.20 per liter. Flux Power’s insulated packs retain 85% of their capacity at -20 °C but weigh 12% more, reducing payload and necessitating chassis reinforcements. For northern operators with six-month winters, these economics temper buying intentions, reducing the airport ground handling systems market CAGR by 0.6 points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cargo Dominance Meets Passenger-Handling Acceleration

Cargo and baggage handling equipment commanded 45.40% of the airport ground handling systems market in 2025 and remains the backbone at hub-and-spoke airports that rely on fast ULD transfers. Growth in cross-border e-commerce supports higher loader counts, while automated baggage carousels integrate directly with warehouse systems, lifting throughput without extra headcount. Passenger-handling gear, however, is on a sharper trajectory, rising at an 8.98% CAGR through 2031. Touch-free boarding bridges, modular stairs, and electric apron buses align well with biometric flows and net-zero pledges, thereby extending wallet share for vendors with IoT-ready modules. Combined, these shifts reinforce diversification in the airport ground handling systems market and open margin-rich upgrade cycles.

Passenger-handling equipment also faces more stringent energy-efficiency mandates. ADELTE’s regenerative-braking bridge, launched in 2024, cuts energy use by 25% and already counts multiple EU airport orders. Cargo specialists answer with electric tugs and solar-assisted dollies to capture decarbonization budgets. Ancillary ramp equipment, such as de-icing rigs, that face regulatory headwinds remains mission-critical at northern stations. This contrast creates a bifurcated demand curve, but overall unit sales sustain volume, keeping the airport ground handling systems market vibrant across all product flavors.

By Power Source: Electric Surge Amid Non-Electric Inertia

Non-electric fleets accounted for 59.20% in 2025, primarily comprising diesel units purchased before stricter sustainability rules took effect. Airports lacking chargers often opt for liquid fuels due to their reliability and lower upfront costs. Electric fleets are projected to grow at a CAGR of 10.05% through 2031 as battery prices drop to USD 115 per kWh in 2024, bringing two-year paybacks into sight. Some hubs choose hybrids as a bridge, cutting fuel use by 35% without range anxiety. The airport ground handling systems market size for electric variants thus expands rapidly, even as diesel fleets remain prevalent in regions where state aid or green bonds are scarce.

Public-private chargers accelerate adoption. JFK Terminal 4 installed 48 Level 3 posts under a USD 12 million grant, reducing overnight charging windows by 70%. EASA’s 2025 rule, which requires any new EU purchase to post 40% fewer lifecycle emissions, cements electric GSE as the default option. California’s Clean Fleets rule and similar mandates elsewhere tighten timelines, so producers of battery packs, inverters, and fleet-management software lock onto a clear demand runway within the airport ground handling systems market.

By Mode of Operation: Autonomy’s Long Runway

Manual operation still dominates, accounting for 66.87% in 2025, thanks to the complexity of marshaling and cargo lash-down tasks, where human judgment excels. Remotely operated setups are now in pilot stages in Singapore and Hong Kong, enabling baggage carts to be moved by joystick from control towers and achieving a 15% increase in productivity. Autonomous vehicles trail but notch the fastest growth at 11.35% CAGR. Tokyo Haneda’s Level 4 tractor began commercial pushbacks in December 2025, proving sub-meter accuracy under live traffic.

FAA Bulletin 25-02, published in May 2025, outlines safety protocols that enable more US airports to test driverless loaders soon. Europe’s Schiphol now runs autonomous crew buses and baggage robots on geo-fenced corridors, reporting 30% labor-cost savings. Labor resistance persists, but phased rollouts, remote-operator retraining, and kill-switch redundancies smooth the path. These technology milestones foster a vibrant supplier ecosystem and sustain momentum in the airport ground handling systems market, which is dedicated to autonomy.

By End User: Commercial Airports Lead, Military Modernizes

Commercial gateways accounted for 75.84% of 2025 spending, channeling post-pandemic recovery funds into electric fleets, passenger biometrics, and pooled-asset platforms. Hub operators secure multiyear, volume-discount deals that lock in service, chargers, and analytics. Military fields, although smaller, are projected to log a 9.40% CAGR to 2031 as defense agencies pursue energy resilience and rapid-deployment targets. The US Air Force placed a USD 180 million order for electric tractors at 12 bases in 2024, reflecting a shift toward lower fuel consumption.

NATO’s Air Base Resilience Initiative steers EUR 400 million (USD 471.86 million) to Eastern Europe for dual-use, hardened GSE able to run on renewable microgrids. Dual-use vendors, such as Mototok, supply tug models that are standard for airlines and air forces, sharing R&D costs and accelerating unit sales. With civil-military technology spillovers growing, the airport ground handling systems market keeps a broad pipeline that buffers cyclical swings.

Geography Analysis

The Asia-Pacific led the airport ground handling systems market with a 40.54% share in 2025 and is expected to maintain an 8.90% CAGR through 2031. China plans 200 new airports by 2035, and Beijing Daxing's Phase 2 alone requires more than 800 GSE units, including 120 electric tractors and 60 automated baggage trains. India's Navi Mumbai International will debut with a fully electric fleet, aligning with the Airports Authority's green guidelines. Japan aims to achieve 30% autonomous penetration in major fields by 2030, underscoring the region's tech-forward appetite.

North America retains heavyweight status via regulation-driven electrification. The FAA's Airport Improvement Program disbursed USD 3.18 billion in 2024, earmarking 22% for GSE charging projects. Clean Ports grants inject another USD 3 billion, while California's Advanced Clean Fleets rule sets a 2030 zero-emission deadline, which pressures suppliers to scale up quickly. Canada and northern states are testing heated-battery solutions to counter winter performance dips, ensuring demand for premium, cold-resilient packs.

Europe follows closely, locked onto the ACI NetZero 2050 commitment that demands 50% electric GSE by 2030. Schiphol budgets EUR 500 million (USD 586.62 million), Heathrow dedicates GBP 400 million (USD 537.91 million), and Frankfurt commits to hydrogen pilots, each shaping vendor order books for the decade to come. The Middle East shows outsized ambitions. Saudi Arabia's King Salman International plans a hydrogen-ready, fully automated fleet exceeding 1,200 units by 2030. Dubai Airports invests USD 150 million from 2024 to 2026 to protect its transfer-hub edge through faster biometrics and electric apron buses.

South America and Africa trail in absolute numbers, but harvest concessional finance. The Inter-American Development Bank's USD 200 million Green Airports Facility supports electrification at Brazilian, Colombian, and Chilean hubs, as well as Rwanda's Kigali project. Changi Airports International commits to electric fleets under an African Development Bank climate loan. These funds de-risk upgrades for capital-constrained operators, providing a toehold for equipment makers eyeing new territory in the airport ground handling systems market.

Regulatory Landscape

Airport ground handling systems operate under an increasingly formal safety-oversight framework anchored on ICAO Standards and Recommended Practices (SARPs) and their national transposition. ICAO Annex 14, Volume I, Amendment 18 includes provisions requiring States to regularly assess the impact of ground handling operations on aviation safety and to establish criteria for safety oversight. This shifts more ground handling activities from guidance-led practices toward auditable state oversight programs.

At the operator level, IATA continues to push procedural harmonization through its Ground Operations Manual (IGOM). The 2026 edition became effective in January 2026 and standardizes key turnaround processes, including refined chocking practices and electronic signature protocols, used by airlines and ground handling service providers across jurisdictions. In Europe, new European Commission ground handling regulations entering into force in March 2025 reinforce state oversight and safe ground operations requirements, and the UK Civil Aviation Authority has been advancing ground handling regulation work derived from ICAO SARPs through its ground handling program and consultation activities.

Value Chain Analysis

The airport ground handling systems value chain starts with raw materials and components, including steel structures, hydraulics, electric drivetrains, batteries, power electronics, sensors, and connectivity modules. OEMs then design and manufacture GSE and fixed equipment such as boarding bridges, baggage systems, and cargo systems. Integration follows for charging infrastructure, telematics, and fleet-management software.

Commercialization is driven through direct airport and airline tenders, ground handling service providers (GHSPs), and specialized leasing and pooling operators. Aftermarket services, including spares, maintenance, refurbishment, and battery lifecycle management, are increasingly bundled into multi-year uptime or availability contracts. Operational deployment is shaped by airport-side common-use infrastructure and handler or airline service-level requirements across ramp, passenger, baggage, and cargo activities, and partnerships show how value is created across the chain: dnata signed an MoU in July 2025 to become the first ground handler in International Airlines Group (IAG) Preferred Partner Programme, aligning handler capabilities with airline network needs and standardization. Technology providers are also moving into operations through pilots, including Swissport and Aurrigo International plc launching a global pilot of autonomous ground handling solutions at Zurich Airport in 2025 using digital simulation and live autonomous electric vehicle trials, tightening the feedback loop between equipment design, software, and airside processes.

Competitive Landscape

The airport ground handling systems market was moderately fragmented in 2025. Oshkosh AeroTech reported a 17% increase in segment revenue, reaching USD 1.2 billion in 2024. Electric variants accounted for 33% of new orders, offering two-year payback periods when considering fuel savings and carbon credits. Alvest’s TLD brand maintained a strong presence in Europe, and Platinum Equity’s 2024 acquisition positioned the company for the global rollout of its leasing services.

Textron’s Tug Technologies achieved USD 1.9 billion in revenue in 2024, driven by pooled-fleet contracts that help airlines manage budget fluctuations caused by traffic variability. Smaller firms, such as Mototok in electric towbar-less tugs, Vestergaard in fuel-cell de-icers, and JLC Group in modular loaders, focused on addressing specific technology gaps left by larger, diversified competitors. Consolidators are increasingly integrating hardware with software solutions. For example, Oshkosh incorporates real-time telematics through its iOPS suite to secure data-driven contracts. At the same time, Daifuku utilizes AI-based route optimization, resulting in a 12% reduction in baggage cart usage at Changi Airport.

Regulatory compliance remains a key competitive factor. Companies that achieve early certification for EASA diesel-phase-out or FAA fluoride-free foam standards gain an advantage in securing tenders. Circular-economy practices are gaining momentum, with offerings that include battery leasing, refurbishment, and end-of-life recycling. Providers that ensure comprehensive lifecycle management stand out as airports increasingly evaluate supply-chain emissions and disposal responsibilities. These strategic shifts highlight the growing importance of integrated, service-oriented solutions in the airport ground handling systems market.

Digital integrators are collaborating with OEMs to embed sensor technologies and subscription-based telematics into their offerings. Predictive maintenance algorithms have emerged as a key differentiator in multi-year service contracts, transitioning revenue models from one-time sales to performance-based uptime guarantees. Suppliers capable of quantifying CO2 savings and delivering platform-agnostic autonomous solutions are gaining procurement preference, particularly under airports’ ESG scoring frameworks.

Airport Ground Handling Systems Industry Leaders

Tug Technologies Corporation (Textron Inc.)

Air T Inc.

Oshkosh AeroTech (Oshkosh Corporation)

Dabico Airport Solutions

Alvest Group Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrification and common-use infrastructure create a clearer whitespace around airport-wide charging buildouts, high-duty-cycle electric GSE, and managed services that reduce handler capex while improving utilization. In 2026, procurement tied to large hubs shows how equipment purchases are being bundled into broader modernization plans: SATS awarded contracts covering more than 200 motorized GSE units to suppliers including Guinault, TLD, and Weihai Guangtai as part of a S$250 million investment. Guinault also signed a five-year contract with SATS to supply motorized units such as GPUs, ASUs, and ACUs, expanding addressable demand for OEMs and integrators that can deliver hardware plus chargers, commissioning, and multi-year maintenance under performance-linked terms.

Autonomy, pooling, and data standards are widening opportunities for software-enabled ground operations and cross-handler asset sharing, especially at congested hubs where turnaround minutes translate into capacity. TCR finalized a strategic partnership with JetBlue in 2026 to manage GSE services and provide full-service rentals across three major US airports, which supports the continued shift toward GSE-as-a-Service and fleet pooling models. Airline and airport programs also point to niches for specialized electric operations in remote or constrained locations, including LATAM implementing a 100% electric, combustion-free ramp operation at Mataveri International Airport (Rapa Nui) in 2026, and Schiphol initiating operations of an electric TaxiBot in 2026, expanding the scope from stand equipment to gate-to-runway movement solutions.

Recent Industry Developments

- July 2026: Textron GSE introduced the TUG MX4 Electric Baggage Tractor, expanding its electric ground support portfolio for baggage and ramp operations. The launch strengthens OEM lineups for airports and handlers standardizing around battery-electric fleets and increases competitive pressure on incumbents in the high-volume baggage tractor segment.

- June 2026: Oshkosh AeroTech delivered the 300th Atlas cargo loader to the Royal Netherlands Air and Space Force at Eindhoven Air Base. The milestone points to continued defense demand for specialized ground support equipment and supports production scale advantages that can carry over into commercial cargo-loader programs.

- January 2026: Oshkosh AeroTech delivered the 7,000th LEKTRO 88i electric towbarless aircraft tractor to Atlantic Aviation at Miami/Opa-Locka Executive Airport. The deployment highlights sustained adoption of electric towbarless tractors in fixed-base operator environments, reinforcing aftermarket and service revenue tied to installed electric fleets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this sizing, the airport ground handling systems market covers revenue generated from equipment and systems used to support aircraft turnaround on the ground, including passenger, baggage, and cargo handling activities from arrival at gate to departure.

Scope exclusions: The model excludes helicopter pad operations, offshore platforms, and stand-alone maintenance and repair work that is not part of airport ground handling system revenues.

Segmentation Overview

- By Type

- Aircraft Handling Equipment

- Passenger Handling Equipment

- Cargo and Baggage Handling Equipment

- Ramp and Support Equipment

- By Power Source

- Non-electric

- Electric

- Hybrid

- By Mode of Operation

- Conventional (Manual)

- Remotely Operated

- Autonomous

- By End User

- Commercial Airports

- Military Airports

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the initial demand picture, and establish practical cross-checks before assumptions were discussed in interviews. We mainly leaned on public aviation traffic and infrastructure indicators, since these track equipment needs better than broad industrial datasets.

Sources reviewed included publications and data series such as ICAO and IATA air traffic indicators, ACI airport traffic and capacity updates, FAA airport activity data, and Eurostat transport statistics, along with customs and trade releases where relevant for major equipment categories. We also reviewed annual reports and investor presentations from listed ecosystem participants, airport authority disclosures, and trusted aviation press to understand replacement cycles, electrification activity, and procurement patterns. In a few places, paid subscriptions for company financials and for patent screening were used to confirm timelines and filter out one-off news signals. This list is illustrative, and other sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on what airports actually buy and pay for, and how spend splits between new builds, expansions, and replacement demand. We spoke with airport operations stakeholders, ground handling service providers, and equipment and system suppliers across major regions, then used their input to check adoption rates for electric units, remotely operated functions, and automation in baggage and cargo flows.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 21% | APAC: 53% |

| Mid tier: 46% | Functional/Unit leaders: 19% | EMEA: 29% |

| Smaller Players: 22% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

Sizing started with a top-down build that links airport traffic and infrastructure activity to ground handling system demand, then converts that demand into value using typical fleet sizes and replacement behavior for major equipment groups. In practice, indicators such as passenger and cargo throughput, aircraft movements, airport expansion projects, average turnaround intensity at commercial airports, and electrification penetration of ground support equipment were used as main inputs, then adjusted by regional mix and airport type.

After forming totals, we added selective bottom-up checks to keep values realistic, including supplier revenue sampling, average selling price ranges for key equipment sets, and channel checks on procurement timing. Where direct visibility was limited in smaller countries, we used proxy airports with similar traffic profiles, scaled using movements and cargo ratios, and then applied interview-led corrections. Forecasting used scenario analysis anchored to expected traffic growth, fleet modernization, and policy-driven electrification, and then stress-tested with short-cycle smoothing on recent airport activity trends to avoid overreacting to a single-year spike.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final totals match real-world operating signals. We compared the model against independent metrics such as aircraft movements growth, airport capacity additions, and known procurement waves in ground support equipment, and then investigated variances that fell outside expected bands.

Before sign-off, assumptions were reviewed step-by-step, and follow-up calls were triggered when interview feedback disagreed with the desk-based view or when a region showed unusual price or volume behavior. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp traffic resets, major regulation changes tied to emissions, or large airport expansion announcements. Right before delivery, the latest public indicators are rechecked so clients receive an updated view.

Mordor Intelligence's Airport Ground Handling Systems Market Size Compared Against Other Published Estimates

Published market sizes for airport ground handling systems can differ even when the topic label looks the same, since authors do not always count the same revenue streams or the same airport coverage. Differences in whether services are included, how electric conversion is priced over time, and which year is treated as the starting point usually create most of the spread.

In this market, the biggest gaps often come from mixing general airport services with equipment and systems spend, or from using aggressive traffic recovery curves without checking them against procurement lead times and replacement cycles. Currency timing also matters because a large share of spend is tied to imported equipment, and the conversion year can shift the stated USD total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 47.73 B (2025) | |

| Global Consultancy A | USD 42.31 B (2025) | Uses a narrower interpretation centered on equipment demand signals, with more conservative adoption rates for electrified units and less explicit uplift for automation in baggage and cargo handling. |

| Industry Publisher B | USD 51.00 B (2025) | Blends a faster traffic rebound path into spend assumptions and applies higher average price progression, which can pull forward value that may only materialize after procurement cycles complete. |

The table shows that most of the variation is explained by how quickly technology upgrades are assumed to happen and whether pricing is allowed to rise ahead of actual replacement activity. When equipment, integrated system revenues, and contract scope are counted only when tied to airport ground handling operations (and not mixed with broader airport services), the estimate stays traceable to traffic, movements, and replacement logic, a scoping choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the airport ground handling systems market?

The airport ground handling systems market is valued at USD 51.59 billion in 2026 and is forecasted to climb to USD 76.12 billion by 2031, reflecting an 8.09% CAGR.

Which region leads spending on ground handling systems?

Asia-Pacific holds 40.54% of global revenue as of 2025, propelled by large-scale airport construction in China and India.

How fast are electric ground support vehicles growing?

Electric platforms are advancing at a 10.05% CAGR through 2031, supported by falling battery prices and green-airport mandates.

Which equipment type is expanding the quickest?

Passenger-handling equipment, such as modular boarding bridges and electric apron buses, is growing at an 8.98% CAGR on rising biometric adoption.

What are the main barriers to autonomous GSE?

Labor-union safeguards, cold-weather battery degradation, and the need for redundant safety systems slow broad deployment of driverless units.

How do leasing models affect procurement?

GSE-as-a-Service and pooled-fleet arrangements cut upfront capex, raise asset utilization to nearly 80%, and accelerate electric-fleet rollouts.

Page last updated on: