Brick Carton Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

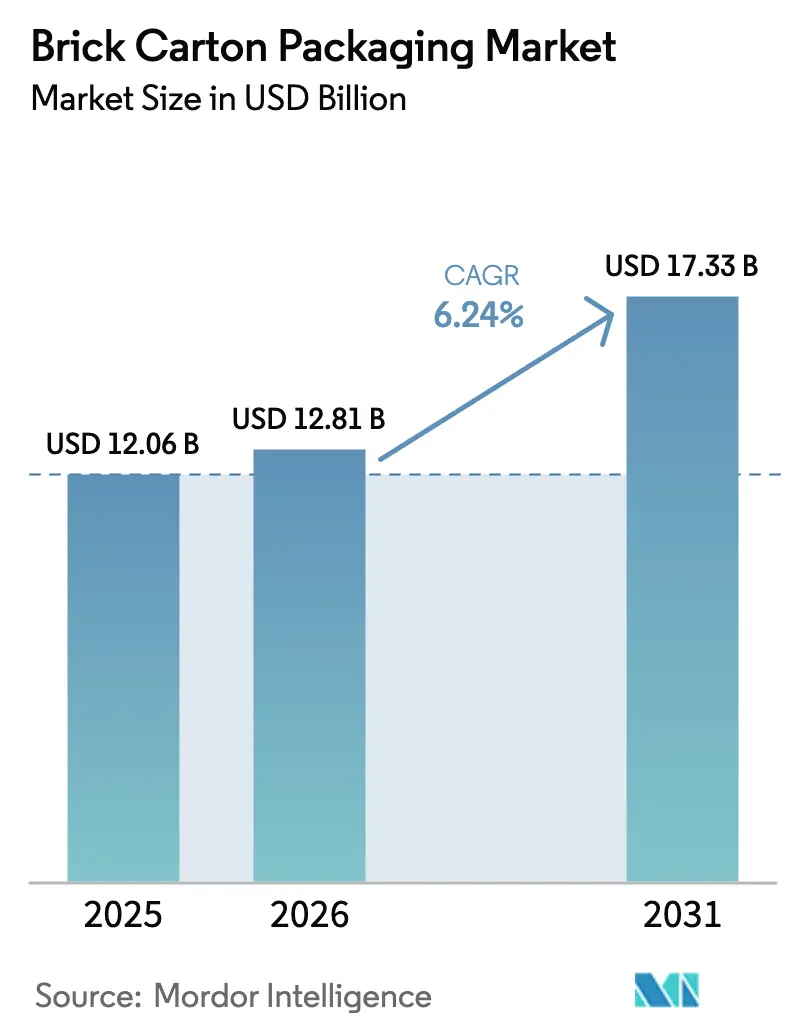

| Market Size (2026) | USD 12.81 Billion |

| Market Size (2031) | USD 17.33 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brick Carton Packaging Market Analysis by Mordor Intelligence

The brick carton packaging market size was valued at USD 12.06 billion in 2025 and estimated to grow from USD 12.81 billion in 2026 to reach USD 17.33 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031). Rising Extended Producer Responsibility (EPR) fees that reward lightweight formats, combined with the European Union’s mandate for 100% recyclable packaging by 2030, form the regulatory backbone that sustains growth. Producers are capitalizing on a surge in aseptic filling investments, steady consumer migration away from rigid plastics, and multilayer barrier innovations that respond to aluminum-foil shortages. The brick carton packaging market also benefits from AI-enabled filling-line automation that improves uptime and cost efficiency, allowing converters and fast-moving consumer-goods brands to introduce new SKUs with shorter commercial lead times. Competitive intensity is pronounced: Tetra Pak, SIG Group, and Elopak use proprietary material science and filling technology to secure long-term contracts with dairy, beverage, and premium personal-care brands. Asia-Pacific remains the growth engine as Vietnam, China, and India rapidly modernize processing facilities, while Europe’s stringent regulations provide a favorable compliance-driven pull for fiber-based formats.

Key Report Takeaways

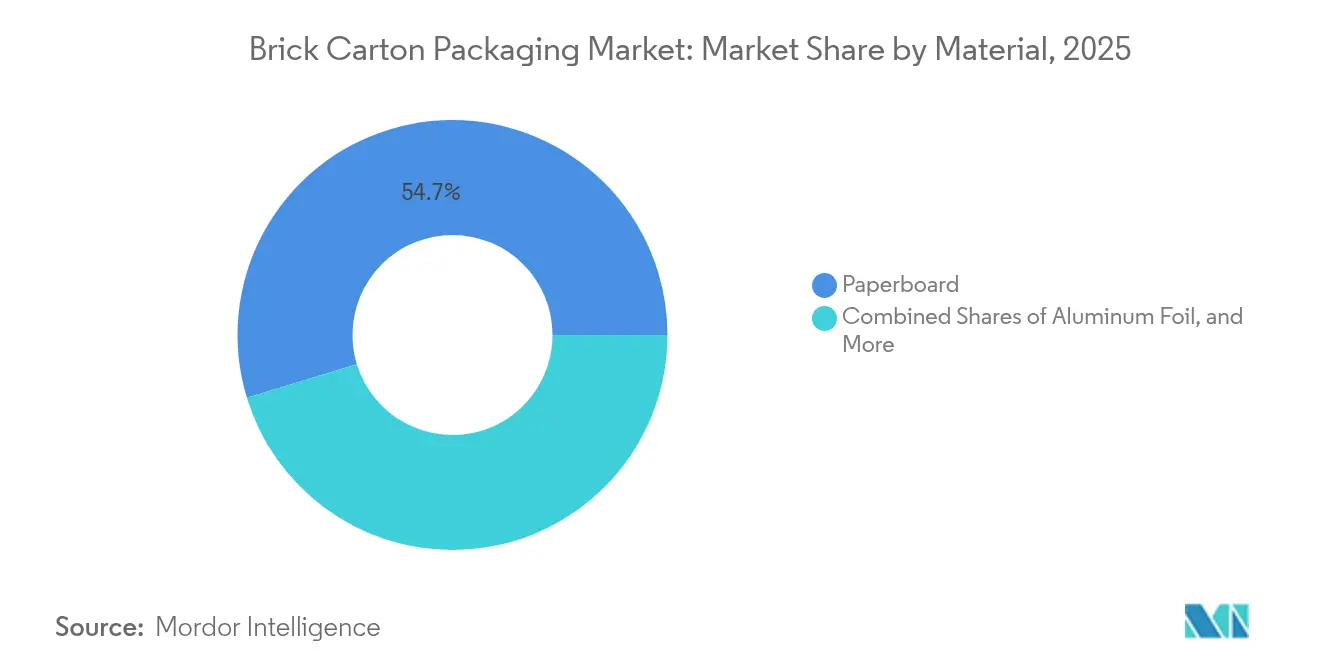

- By material, paperboard led with 54.72% revenue share in 2025, whereas aluminum-foil-based structures are projected to climb at a 9.32% CAGR to 2031.

- By opening/closure type, twist caps captured 35.12% of the brick carton packaging market share in 2025, while straw-hole variants are forecast to post an 8.22% CAGR through 2031.

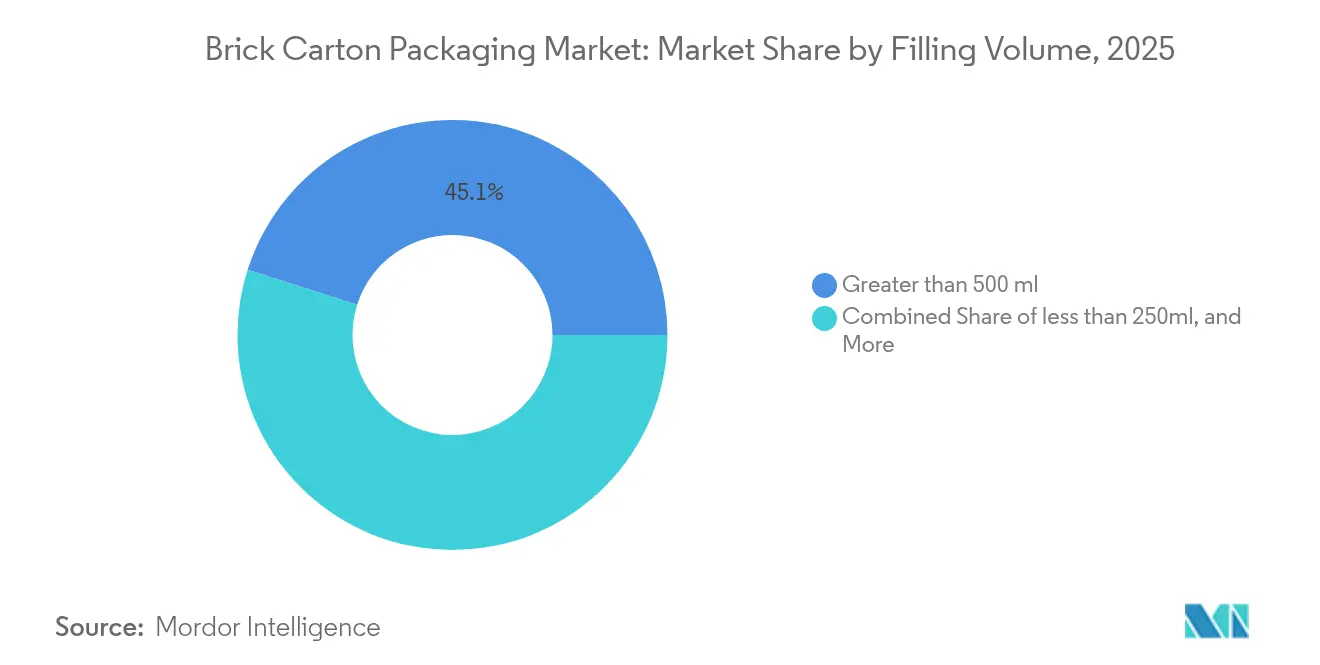

- By filling volume, packs above 500 ml accounted for 45.10% of the brick carton packaging market size in 2025; formats below 250 ml are estimated to expand at an 7.86% CAGR between 2026 and 2031.

- By end-user industry, food and beverages contributed 55.73% of 2025 revenue; cosmetics and personal care is the fastest-growing customer set at a 9.76% CAGR.

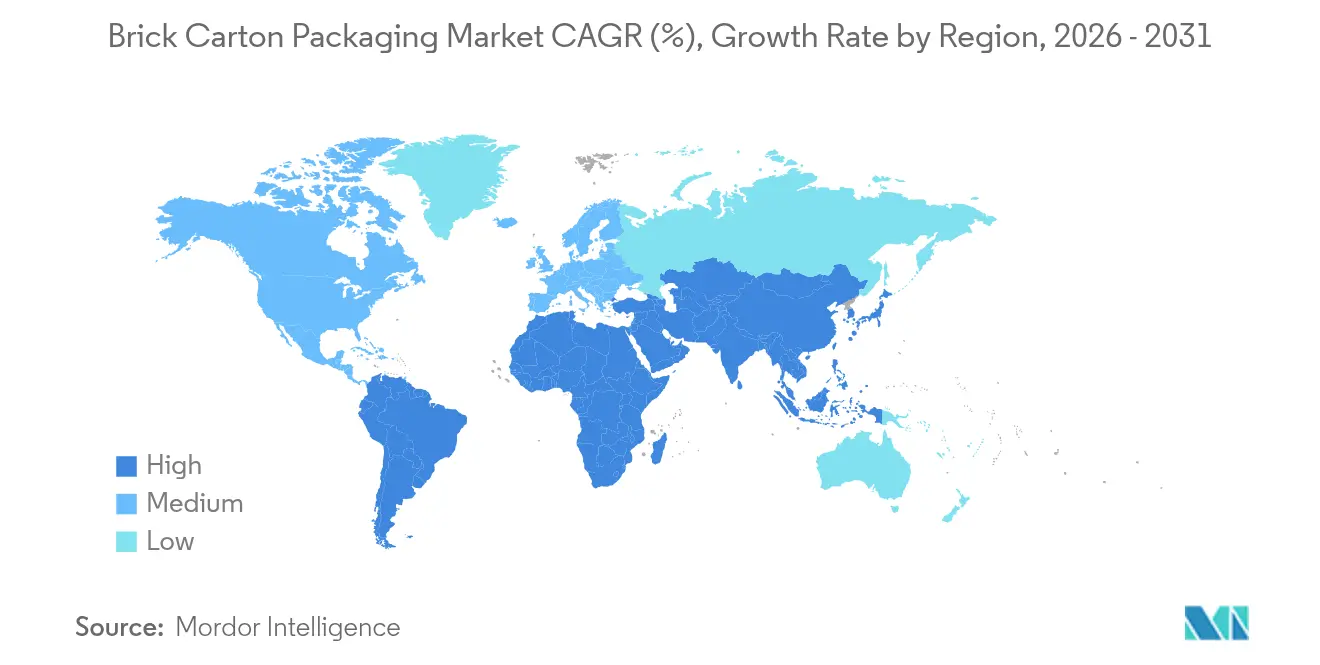

- By geography, Asia-Pacific held 38.05% of global revenue in 2025, doubling as the fastest-growing region at 9.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Brick Carton Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aseptic packaging demand surge in dairy and beverage sectors | +1.8% | Global, with early gains in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising demand for cost-effective packs in developing economies | +1.2% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Sustainability shift from plastics to paper-based cartons | +2.1% | Europe & North America leading, global adoption | Medium term (2-4 years) |

| Aluminium foil supply crunch spurring multilayer barrier innovation | +0.9% | Global supply chain impact, innovation centers in Europe/US | Short term (≤ 2 years) |

| AI-enabled filling-line automation cuts downtime and boosts ROI | +0.7% | Developed markets initially, expanding to emerging economies | Long term (≥ 4 years) |

| EPR fee structures favouring lightweight brick cartons | +1.4% | Europe, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aseptic demand surge in dairy and beverage sectors

The aseptic packaging boom lifts every layer of the brick carton packaging market by lowering distribution costs and extending shelf life. Berglandmilch’s SIG SmileBig 24 line processes 24,000 packs per hour, showcasing how scale economies reduce per-unit costs while meeting strict Food and Drug Administration sterility standards. Brands avoid refrigerated storage, cutting logistics spending by up to 40%, and can penetrate rural markets where cold chains remain underdeveloped. North American dairies that once favored high-density polyethylene gallons now retrofit plants with aseptic fillers, underscoring a global shift toward ambient shelf-stable formats. The result is a steady replacement cycle for legacy lines and a pipeline of machinery orders that favors market incumbents with proven technology credentials. The uptrend also spills into functional drinks and plant-based beverages, helping the brick carton packaging market gain traction among start-ups that rely on extended shelf life to secure nationwide listings.

Rising demand for cost-effective packs in developing economies

Emerging-market converters view brick cartons as a gateway to reduce material input costs while meeting circular-economy obligations. Vietnam’s paper packaging sector, projected at USD 3.5 billion by 2026, exemplifies the 9.73% annual growth that underpins long-run demand for entry-level aseptic fillers. Governments link EPR compliance fees to recyclability performance, making fiber-rich structures financially attractive for family-run dairies and juice bottlers. Indonesia’s PT Amandina Bumi Nusantara demonstrates how locally sourced recycled PET supports circular supply chains, freeing up capital for carton line investments. Where labor is inexpensive, converters absorb the incremental complexity of multi-layer assembly while capturing margin through lower raw-material tonnage. This virtuous cost loop sustains the brick carton packaging market in regions with per-capita incomes still below the global average.

Sustainability shift from plastics to paper-based cartons

Europe’s ban on PFAS in food contact materials and its 2030 recyclability mandate remodel purchasing criteria for multinational brands[1]Packaging Law, “The New EU Packaging and Packaging Waste Regulation – Highlights and Challenges Ahead,” packaginglaw.com. Mondelēz, Saica Group, and Finland’s VTT showcase how cellulose-based barrier films can replace traditional polymers without compromising oxygen transmission performance. United Kingdom EPR fees tiered by pack weight further tip the scale toward light, fiber-heavy constructions[2]UK Government, “Extended Producer Responsibility for Packaging: 2025 base fees,” gov.uk . As major consumer-goods companies race to meet virgin-plastic elimination pledges, brick carton conversions accelerate not only in dairy but also in soups, culinary sauces, and even shelf-stable cosmetics. The brick carton packaging market thereby captures sustainability-driven budget reallocations that previously favored flexible pouches.

Aluminum-foil supply crunch spurring multilayer innovation

Intermittent foil shortages, aggravated by European energy volatility, push converters to develop high-barrier polymer coatings that reach oxygen transmission levels below 0.1 cm³/m²·d·bar. SIG’s 2025 aluminum-free, 80%-paper aseptic structure cuts carbon footprints by 61% and removes a critical supply-chain chokepoint. Kraft Heinz’s USD 25,000-100,000 innovation grants accelerate academic-industry collaboration on dead-fold substitutes that pass FDA migration testing. Accelerated R&D shortens product-development cycles, enabling new material launches in under two years, half the historical norm, and adding dynamism to the brick carton packaging market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET bottle & flex-pouch substitution risk | −1.1% | Global, notably in beverages | Medium term (2-4 years) |

| Size constraints limiting secondary household use | −0.6% | Global; higher in cost-sensitive economies | Long term (≥ 4 years) |

| LDPE & aluminum laminate price volatility | −0.9% | Global; Asia-Pacific hubs acute | Short term (≤ 2 years) |

| Recycling-infrastructure gaps in emerging markets | −0.8% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PET bottle and flex-pouch substitution risk

Flexible pouches champion a superior product-to-package ratio, while recycled PET bottles now claim 56.4% material recovery in Brazil [3]MDPI, “Post-Consumer Recycled PET: A Comprehensive Review of Food and Beverage Packaging Safety in Brazil,” mdpi.com. Brands exploit these credentials—along with cost-savings from lighter secondary packaging to switch certain juice, water, and condiment lines away from cartons. Coca-Cola Indonesia’s 3,000 tpm rPET plant illustrates how supply-chain verticalization makes bottle-grade flakes more price competitive. Still, brick carton producers defend share in premium SKU niches, citing tamper evidence, mechanical rigidity, and billboard shelf presence.

Recycling-infrastructure gaps in emerging economies

EPR rules in Vietnam set 20% recycling quotas yet offer limited municipal collection coverage, imposing costly take-back obligations on importers. Tetra Pak’s Carton Council grants for AI-enabled MRF optical sorters help bridge the gap, but capital requirements remain high. Kenya’s 2024 EPR framework demands four-year recovery plans, yet enforcement capacity and on-ground processing assets lag targets. The resulting compliance uncertainty tempers investment enthusiasm, creating pockets of under-penetration for the brick carton packaging market until infrastructure catches up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paperboard Anchors Growth Amid Foil Innovation

Paperboard captured 54.72% of 2025 revenue, reflecting its role as the structure carrier for nearly every commercial specification in the brick carton packaging market. The segment benefits directly from EPR fee frameworks that assign lower levies to mono-material or fiber-dominant packs, which in turn lowers producer compliance spend and improves unit economics. Over the forecast period, the brick carton packaging market size for paperboard formats is projected to rise in line with overall market CAGR, keeping its majority stake intact. Converter upgrades such as inline digital printheadsallow rapid SKU changes without plate swaps, helping brands localize on-pack promotions and maximize consumer engagement in cluttered retail aisles.

Aluminum foil, though afflicted by supply tightness, registers the fastest-growing slice at a 9.32% CAGR as multilayer composite suppliers race to preserve high-barrier performance in shelf-stable soups, broths, and infant formulas. SIG’s 80% paper, aluminum-free alternative becomes the template for next-generation structures that promise lower carbon intensity without sacrificing migration safety. LDPE remains entrenched as the inner-sealing medium but confronts regulatory headwinds; experiments with bio-based PE and water-borne acrylic coatings illustrate a mid-decade shift toward drop-in replacements that meet heat-seal requirements. Polymer-based barriers that rely on nanoclay or EVOH layers allow oxygen permeability comparable to foil while enabling simplified recycling streams, padding the competitive moat for carton converters vis-à-vis multilayer flexibles.

By Opening/Closure Type: Ergonomic Resealability Sets the Pace

Twist caps held 35.12% share in 2025 because families value resealable, leak-resistant functionality during multi-serve consumption. Large-format milk, juice, and plant-based dairy applications especially rely on twist closures to maintain freshness, underpinning their outsized role in the brick carton packaging market. Molded-in-place threading technology cuts changeover downtime, enabling high-speed fillers to switch volumes without mechanical recalibration. Every incremental design tweak such as lightweight cap geometry reduces resin use and supports brand sustainability narratives.

Straw-hole closures grow at an 8.22% CAGR as on-the-go drinking, children’s nutritional beverages, and functional shot categories multiply SKUs. Consumer preference for one-handed convenience nudges small-volume beverage producers toward straw-fit formats. Meanwhile, carton manufacturers tailor pull-tab membranes and predictive tear lines to mitigate product drips, aiming to win shelf space that previously defaulted to PET mini-bottles. Clip closures cater to premium juices, broths, and ready-to-drink coffee, where tamper evidence and shelf stand-out matter more than stripping out grams of material. Growing e-commerce penetration also drives demand for closures that prevent leakage during last-mile handling, widening the value proposition of resealable caps in the brick carton packaging market.

By Filling Volume: Household Economies Versus Grab-and-Go Premiumization

Volumes above 500 ml commanded 45.10% of global turnover in 2025, reflecting grocery shopping patterns where families seek bulk packs to reduce per-serving cost. The brick carton packaging market size for this volume tier is expected to remain sturdy because the product-to-package ratio minimizes waste and meets carbon-footprint disclosure requirements at the retail level. Large volumes also integrate smoothly into automated case-packers, cutting per-pallet logistics cost and complementing club-store channels that prioritize pallet efficiency.

Sub-250 ml formats showcase an 7.86% CAGR, dovetailing with higher urban density, smaller household sizes, and premium single-serve segments. Energy drinks, protein shots, and cold-brewed coffee leverage brick cartons to signal premium positioning, aided by high-fidelity digital printing that supports limited-edition artwork. Between the extremes, the 250-500 ml tier captures versatile occasions: it is small enough for impulse buys yet large enough to justify unit pricing without steep per-liter premiums. Advances in servo-controlled filling valves grant fillers the ability to handle all three volume zones with little downtime, letting co-packers flex capacity based on seasonality and promotional cycles an operational win that resonates across the brick carton packaging market.

By End-User Industry: Food Staples Dominate While Beauty Accelerates

Food and beverage companies accounted for 55.73% of market turnover in 2025 and remain the anchor revenue pillar. Dairy maintains pole position because shelf-stable milk offers rural retailers a viable alternative where refrigeration is unreliable. Juice, broth, and plant-based beverages expand carton penetration as brands chase clean-label claims; paper-based walls obviate light exposure, preserving vitamin content and flavor integrity. Moreover, aseptic logistics slash cold-chain emissions, helping grocery chains trim Scope 3 carbon disclosures and elevating the overall attractiveness of the brick carton packaging market.

Cosmetics and personal care register the fastest ascent, at a 9.76% CAGR, as prestige brands migrate toners, micellar waters, and refill concentrates into slimline cartons. DS Smith’s TailorTemp solution demonstrates temperature-controlled capabilities, revealing how pharmaceuticals and beauty SKUs can exploit cartons for transit-sensitive content. Carton embossing and foil-stamp options grant luxury aesthetics without forfeiting recyclability, allowing brands to advertise sustainability without diluting premium cues. Nutraceutical drinkables and pediatric suspensions complete the crossover, tapping tamper-evident screw caps to assure dosing fidelity another subtle yet potent driver embedded in the brick carton packaging market.

Geography Analysis

Asia-Pacific led with a 38.05% revenue slice in 2025 and commands the highest regional CAGR at 9.55% through 2031. The confluence of rapid urbanization, rising middle classes, and escalating packaged-food penetration underpins this momentum. Vietnam’s paper-packaging expansion exemplifies the tide, complemented by Chinese dairy conglomerates and Indian juice start-ups securing local bottling partnerships to sidestep import tariffs. Meanwhile, Indonesia’s advanced PET recycling demonstrates regional readiness to integrate circular raw-material streams that cascade economic benefits back into carton-line investment.

Europe follows as the second-largest territory, powered by stringent legislation that effectively ring-fences demand. The EU Packaging and Packaging Waste Regulation requires 100% recyclability, nudging retailers to favor fiber-based shelves, a policy windfall that channels volume toward the brick carton packaging market. Germany’s dual-system fees and the United Kingdom’s plastic packaging tax push supermarket private labels to pivot large-format milk and soup into cartons. Stora Enso’s EUR 2,362 million Q1 2025 sales and Mondi’s EUR 200 million recycled containerboard investment highlight how local fiber giants scale capacity to meet converter demand .

Competitive Landscape

Tetra Pak, SIG Group, and Elopak dominate by combining proprietary filling systems, barrier technologies, and holistic recycling initiatives. Tetra Pak unveiled the A1 1100 filling machine and Direct UHT modules at PACK EXPO 2024, underscoring its ambition to embed end-to-end solutions that cut energy use by 30% versus legacy lines. SIG Group’s aluminum-free full-barrier advance not only addresses supply bottlenecks but also resonates with brand owners chasing scope-3 emission reductions, yielding a competitive moat around intellectual-property-protected materials.

Elopak’s Pure-Pak investments secure multi-year conversion contracts with Hochwald Foods and Žemaitijos pienas, underlining a strategic pivot to plastic displacement in European fluid dairy.The firm’s Q2 2024 revenue lift of EUR 288.4 million is a case study in how carton upgrades can capture volume where supermarkets impose plastic-reduction scorecards. Billerud and Stora Enso diversify revenue by supplying coated sack papers and formed-fiber trays, augmenting their cartonboard portfolio and reinforcing vertical integration in the brick carton packaging industry.

Digitalization also drives rivalry. AI-enabled vision systems on SIG and Tetra Pak fillers detect micro-leaks at 7-millisecond intervals, slashing waste and enhancing overall equipment effectiveness—data points that brands now require in procurement tenders. Mid-tier regional converters differentiate via rapid artwork turnaround, cloud-connected proofing, and life-cycle assessment dashboards for retailers. The result is a multi-factorial battleground where speed to market, sustainability metrics, and capital-expenditure packages converge, shaping how the brick carton packaging market allocates future share.

________________________________________

Brick Carton Packaging Industry Leaders

International Paper

Mondi plc

Amcor plc

Huhtamaki Oyj

Tetra Pak Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mondi committed EUR 200 million to a recycled containerboard mill in Duino, Italy, aimed at strengthening circular fiber supply for European converters.

- January 2025: DS Smith introduced TailorTemp at PharmaPack Europe, a fiber-based thermal pack that trims CO₂ by 40% while maintaining 36-hour cold-chain integrity.

- January 2025: Amcor secured a European patent for AmFiber Performance Paper, surpassing 80% fiber content while achieving high barrier properties suitable for nutrition powders.

- November 2024: Stora Enso divested its Sunila site to AALTO Development, retaining tenancy for its Lignode battery-material pilot, signaling a strategic focus on bio-based barrier coatings.

Global Brick Carton Packaging Market Report Scope

The brick-carton packaging market encompasses a versatile and customizable packaging solution crafted from paperboard, aluminum, and Low Density Polyethylene (LDPE). This packaging method is a shield, safeguarding products from external contaminants and moisture while extending their shelf life. The key characteristic of brick-carton packaging lies in its adaptability, allowing manufacturers to tailor the packaging according to the specific needs of their products.

The brick carton packaging market is segmented by material (paperboard, low-density polyethylene (LDPE), aluminum), by type (cut, clip, straw hole, twist, king twist), by end-user (food & beverages, cosmetics, pharmaceutical, nutraceutical, chemical, others) and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France. Italy, Rest of Europe], Asia Pacific [China, India, Japan. Rest of Asia Pacific], Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Paperboard |

| Low-Density Polyethylene (LDPE) |

| Aluminum Foil |

| Other Material |

| Cut |

| Clip |

| Straw Hole |

| Twist |

| Other Closure Type |

| Less than 250 ml |

| 250 - 500 ml |

| More than 500 ml |

| Food and Beverages |

| Dairy Products |

| Juices and Functional Drinks |

| Pharmaceuticals |

| Nutraceuticals |

| Cosmetics and Personal Care |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Paperboard | ||

| Low-Density Polyethylene (LDPE) | |||

| Aluminum Foil | |||

| Other Material | |||

| By Opening / Closure Type | Cut | ||

| Clip | |||

| Straw Hole | |||

| Twist | |||

| Other Closure Type | |||

| By Filling Volume | Less than 250 ml | ||

| 250 - 500 ml | |||

| More than 500 ml | |||

| By End-user Industry | Food and Beverages | ||

| Dairy Products | |||

| Juices and Functional Drinks | |||

| Pharmaceuticals | |||

| Nutraceuticals | |||

| Cosmetics and Personal Care | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the brick carton packaging market in 2026?

The brick carton packaging market stands at USD 12.81 billion in 2026, supported by rising EPR fees that favor lightweight, fiber-based structures.

What is the projected growth rate for brick carton cartons through 2031?

The market is forecast to expand at a 6.24% CAGR during the forecast period (2026-2031), reaching USD 17.33 billion by 2031.

Which region is growing fastest?

Asia-Pacific combines a 38.05% revenue stake with a 9.55% CAGR, driven by urbanization, rising disposable income, and modern retail expansion.

Which material innovation is reducing carbon footprints most?

SIG’s aluminum-free full-barrier carton, comprising over 80% paper content, cuts lifecycle emissions by 61% while maintaining shelf-life protection.

Page last updated on: