Shoe Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

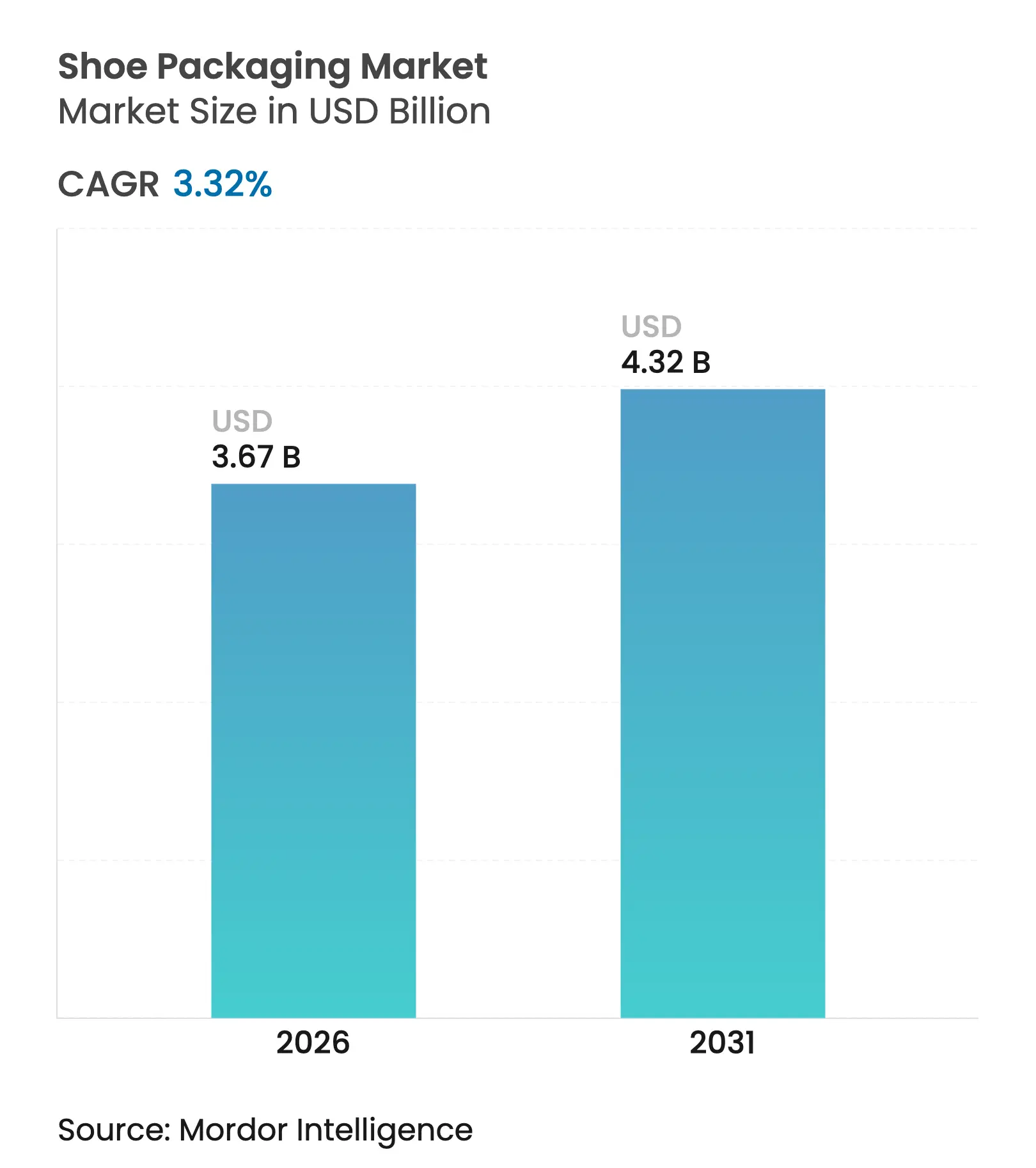

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 4.32 Billion |

| Growth Rate (2026 - 2031) | 3.32 % CAGR |

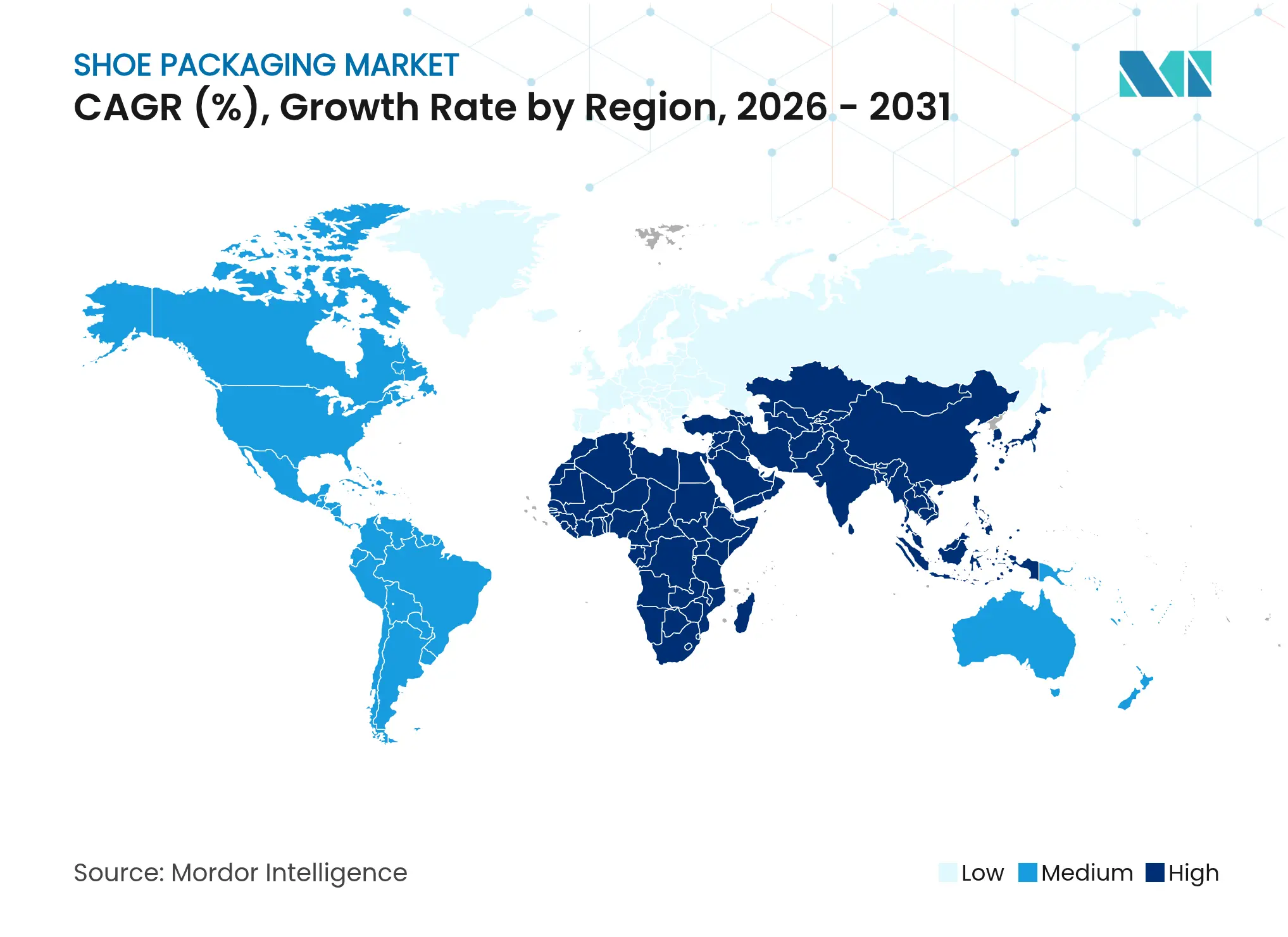

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

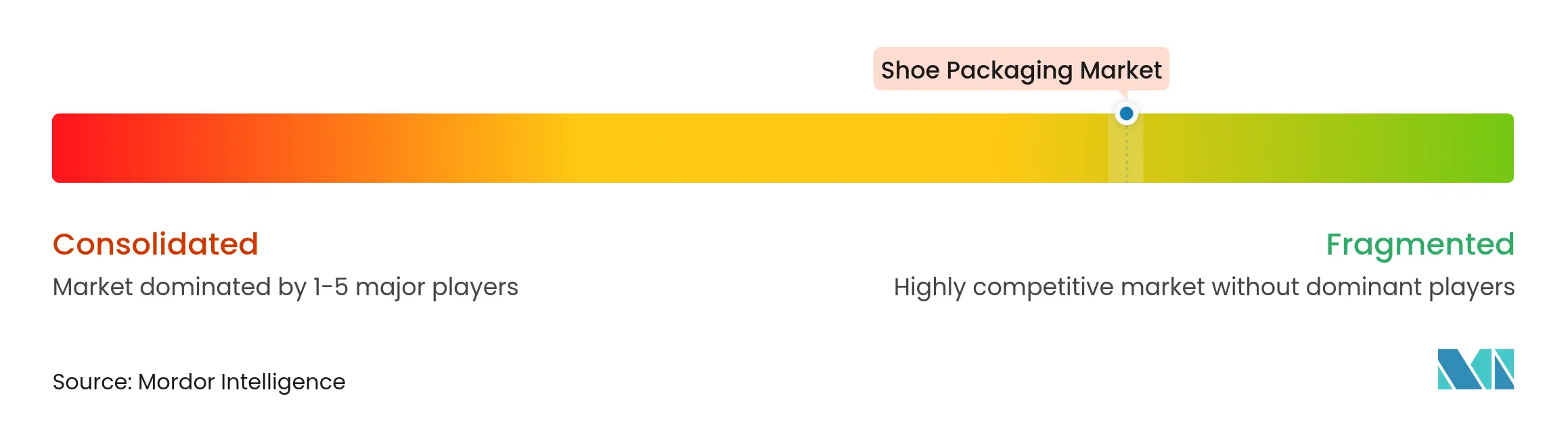

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Shoe Packaging Market Analysis by Mordor Intelligence

Shoe packaging market size in 2026 is estimated at USD 3.67 billion, growing from 2025 value of USD 3.55 billion with 2031 projections showing USD 4.32 billion, growing at 3.32% CAGR over 2026-2031. Moderate expansion reflects maturing demand, stricter environmental rules, and shifts in e-commerce that influence material choices, automation levels, and smart-tag adoption. European recyclability mandates, California’s extended producer responsibility programs, and rising pulp prices are reshaping supplier strategies. Athletic and athleisure footwear growth keeps volumes elevated, while luxury pairs fuel premium formats that integrate NFC authentication. Asia-Pacific holds production leadership, but volatile fiber costs and labor tightness encourage robotics and one-box systems that reduce waste and freight. Across regions, the shoe packaging market is evolving toward circularity, mono-material construction, and digital tracking to satisfy regulators and eco-conscious buyers alike.

Key Report Takeaways

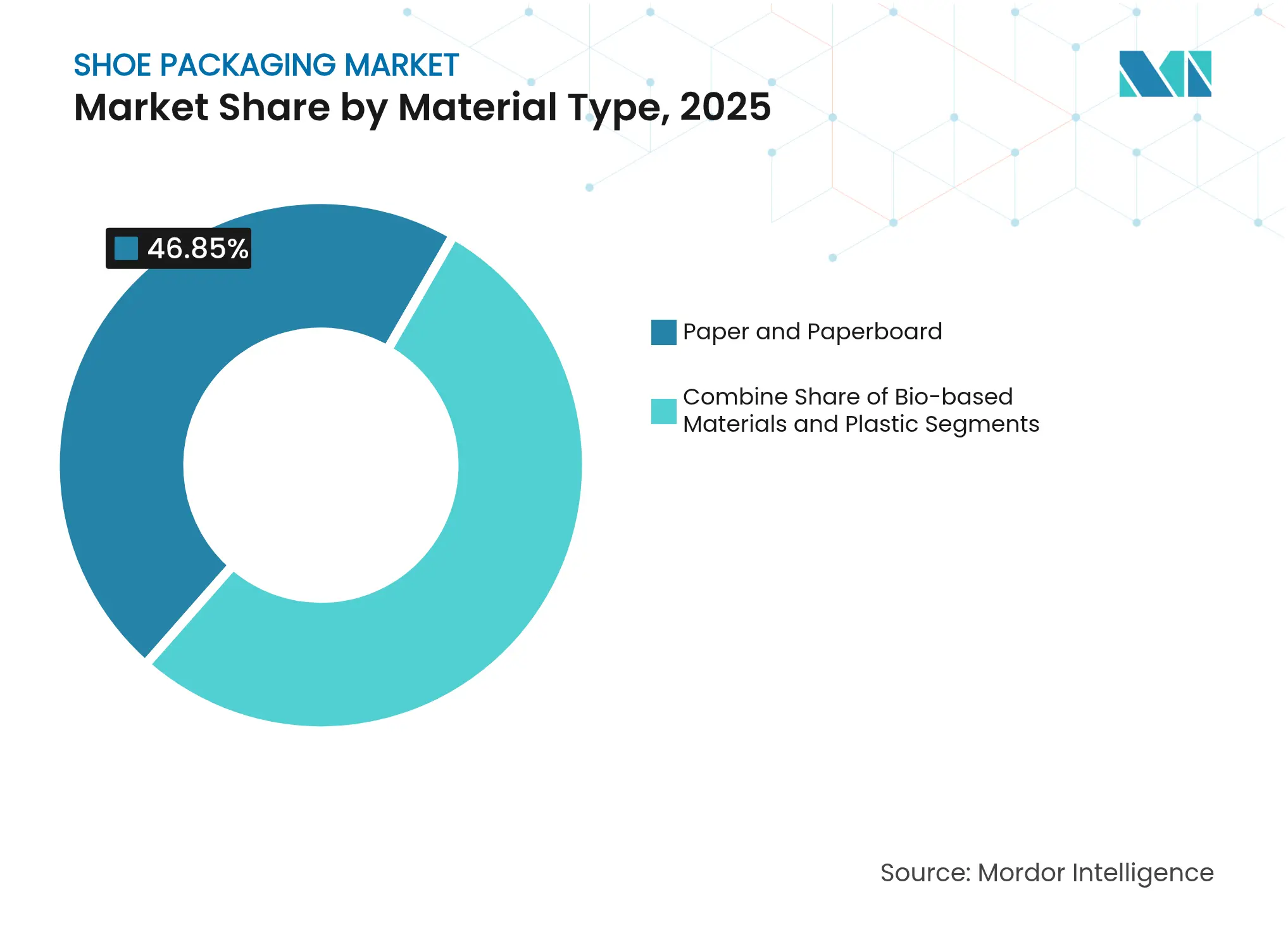

- By material type: Paper and paperboard captured 46.85% of shoe packaging market share in 2025; bio-based alternatives are advancing at 7.02% CAGR to 2031.

- By product type: Boxes and cartons held 71.6% revenue share of the shoe packaging market in 2025, while wraps record the fastest CAGR at 6.12% through 2031.

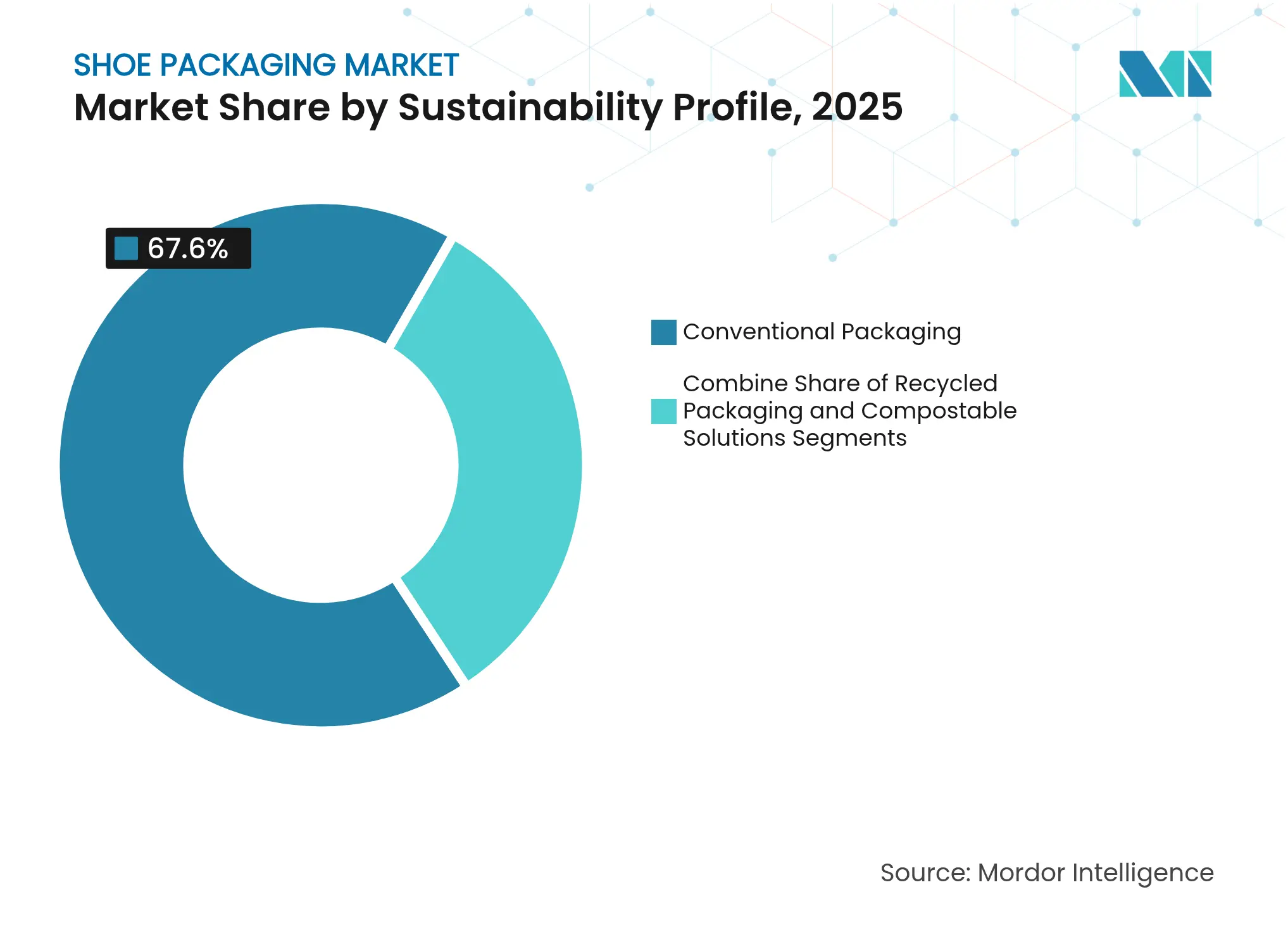

- By sustainability profile: Conventional formats represented 67.60% of the shoe packaging market size in 2025; compostable and reusable solutions are expanding 5.95% annually.

- By footwear category: Athletic footwear packaging led with 58.05% share of the shoe packaging market size in 2025; luxury and designer packaging posts the highest 5.18% CAGR to 2031.

- By geography: Asia-Pacific dominated with a 45.10% shoe packaging market share in 2025 and is growing 6.85% a year.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Shoe Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

E-commerce footwear boom E-commerce footwear boom | +1.2% | Global, strongest in North America & Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, strongest in North America & Asia-Pacific | Impact Timeline:Medium term (2-4 years) |

Sustainability legislation and eco-conscious buyers Sustainability legislation and eco-conscious buyers | +0.8% | EU & North America core, spreading to Asia-Pacific | Long term (≥ 4 years) | |||

Athletic and athleisure footwear proliferation Athletic and athleisure footwear proliferation | +0.6% | Global, strongest in North America & Europe | Medium term (2-4 years) | |||

Brand switch to mono-material “One-Box” shipping Brand switch to mono-material “One-Box” shipping | +0.4% | North America & EU, pilots in Asia-Pacific | Short term (≤ 2 years) | |||

NFC / smart-tag shoe boxes combat counterfeits NFC / smart-tag shoe boxes combat counterfeits | +0.3% | Global, priority in luxury markets | Medium term (2-4 years) | |||

Advent of mushroom-based bio-packaging Advent of mushroom-based bio-packaging | +0.2% | EU & North America, R&D in Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

E-commerce Footwear Boom

Online footwear now accounts for 74% of global pairs sold, turning every shipped box into a brand billboard. Purpose-built right-sizing platforms such as Ranpak’s Cut’it EVO enable four lid profiles from one machine, trimming air space and freight bills. Global e-commerce packaging is projected at USD 124.9 billion by 2029, up from USD 77.4 billion in 2024. Asia-Pacific absorbs more than half that volume, so its factories invest heavily in auto-gluers and vision-guided robots to lift throughput. Smart labels further differentiate merchants while streamlining returns, reinforcing medium-term uplift to the shoe packaging market.

Sustainability Legislation and Eco-conscious Buyers

The EU Ecodesign for Sustainable Products Regulation names footwear among its top priorities and makes recyclability a legal must-have by 2028. California’s Fashion Environmental Accountability Act forces multibillion-dollar brands to disclose packaging footprints from 2026. Parallel bans on PFAS and mandatory 30% recycled PET content spur substrate substitution and drive bio-based demand. Shoppers are willing to pay premiums; Caleres, for instance, hit 100% “environmentally preferred” packaging three years early. Although cost hurdles linger, regulatory pressure keeps sustainable options on a steep adoption curve that adds 0.8 percentage points to the forecast CAGR.

Athletic and Athleisure Footwear Proliferation

Performance silhouettes with complex 3D-printed lattices, such as Adidas’ Climacool, require reinforced structures that still delight unboxing. [1]Adidas, “3D Printed Climacool,” adidas.comCustomization programs create SKU proliferation, pushing converters to digital print lines for late-stage variation. Circular design also enters athletics: ASICS’ Nimbus MIRAI invites returns for disassembly, so the pack must enable take-back logistics. Premium price tolerance lets brands embed RFID or tamper seals, raising average unit value and supporting a 0.6% CAGR lift for the shoe packaging market.

Brand Switch to Mono-material “One-Box” Shipping

Nike’s One Box merges shipper and display carton, halving packaging weight for single online orders while keeping brand aesthetics. Converse follows with a 100% recycled variant that doubles as closet storage. Early adopters report freight savings and faster pick-pack flows, though durability testing and consumer education remain hurdles. Successful pilots drive broader upgrades that add 0.4 percentage points to growth as copycats multiply across the shoe packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile pulp and linerboard prices Volatile pulp and linerboard prices | −0.7% | Global, acute in North America & Europe | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:−0.7% | Geographic Relevance:Global, acute in North America & Europe | Impact Timeline:Short term (≤ 2 years) |

Plastic curbs and compliance costs Plastic curbs and compliance costs | −0.5% | EU & North America, expanding globally | Medium term (2-4 years) | |||

Reverse-logistics reuse programs cut volumes Reverse-logistics reuse programs cut volumes | −0.3% | North America & EU, pilots in Asia-Pacific | Medium term (2-4 years) | |||

Automation CAPEX barrier for SME factories Automation CAPEX barrier for SME factories | −0.4% | Global, especially developing markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Pulp and Linerboard Prices

Corrugated board jumped USD 70 per ton in January 2025 after strikes at Nordic mills tightened virgin fiber supply. International Paper and Georgia-Pacific pushed similar hikes, doubling US fiber costs versus 2023. SMEs lack long contracts, squeezing margins and delaying innovation spend. While recycled content can ease dependency, Europe’s deforestation law may limit fiber flow, keeping pricing choppy and shaving 0.7 points off forecast expansion.

Plastic Curbs and Compliance Costs

California SB 54 demands a 25% single-use plastic cut by 2032, and the EU bans PFAS in food-contact packs while mandating 30% recycled PET by 2030. Reporting fees and redesign cycles lift operating costs, especially for exporters juggling divergent rules. Substitution toward bio-circular polymers carries premiums that some budget lines cannot absorb, trimming mid-term CAGR by 0.5 points.

Segment Analysis

By Material Type: Bio-based Disruption Challenges Paper Dominance

Paper and paperboard accounted for 46.85% of shoe packaging market share in 2025, supported by global recycling streams and competitive cost. Corrugated board’s USD 70-per-ton spike, however, is pushing converters to pulp blends and agro-waste fibers that lower virgin demand. Bio-based substrates such as mushroom composites grow at 7.02% CAGR, reflecting tight alignment with ESPR and North American PFAS bans. Plastic retains niche roles in moisture-proof liners, yet brands switch to post-consumer PET to comply with 30% recycled mandates. Mushroom mycelium delivers cushioning comparable to expanded foams, widening its appeal for premium pairs.

Scaling challenges persist, but brands pilot limited runs for storytelling and ESG credits. ISA TanTec’s HyphaLite-TC shows commercial promise with cradle-to-gate carbon savings, and freeze-thaw processing achieves tensile benchmarks once exclusive to synthetics. Conventional fiber mills now invest in fungiculture labs to hedge future demand. Taken together, the material transition underpins medium-term resilience for the shoe packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Wrap Innovation Gains on Box Leadership

Boxes and cartons held 71.6% of the shoe packaging market in 2025, anchored by display value and stacking efficiency. Nike’s One Box proves mono-material shippers can cut fiber by 51% for single orders while upholding brand cues. Growth of wraps at 6.12% CAGR is propelled by plant-based films and Kengos’ ships-in-own-container design that removes tape and void fill. Inserts evolve into smart trays embedding RFID to authenticate limited releases, raising per-package value.

Unit economics matter: wraps use 20% less board weight and feed automated lines faster, suiting high-velocity online pairs. Carton suppliers respond with adaptive flaps and tear-strips that maintain retail presentation yet survive courier hubs. Diversifying form factors ensures the shoe packaging market stays responsive to omni-channel demands.

By Sustainability Profile: Circular Options Chip at Conventional Volume

Conventional formats still made up 67.60% of the shoe packaging market size in 2025, but ESG metrics turn the spotlight on compostable and reusable systems expanding 5.95% annually. Caleres reports 70% recycled fiber in cartons and 100% PCR content in bags after shifting to a One Planet sourcing template. PUMA raised recycled polyester use to 62%, integrating packs into a broader circular play. Reusable totes now rotate between warehouses and retail, lowering new-carton demand yet building customer loyalty.

Performance gaps narrow: new starch-based coatings withstand 10 transit cycles, and water-based inks enable curbside recycling. Regulatory credits and landfill levies help offset premiums, cementing momentum for greener alternatives across the shoe packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Footwear Category: Athletic Rules Volume, Luxury Leads Growth

Athletic lines commanded 58.05% share in 2025 thanks to sustained sneaker demand and performance-driven branding. Mass drops require high-speed auto-packing, while limited editions justify NFC-enabled collectors’ cases. Luxury pairs post a 5.18% CAGR to 2031 as labels elevate the unboxing ritual with rigid boards, foil deboss, and mushroom-leather wraps. Casual shoes emphasize cost-down but lean into mono-material recyclability, and kids’ lines add child-safe inks and playful QR codes.

Return programs for worn trainers, like ASICS’ Nimbus MIRAI, demand resealable boxes designed for two-way logistics. Such complexity raises the engineering bar and keeps packaging central to product experience, reinforcing long-term opportunity within the shoe packaging market.

Geography Analysis

Asia-Pacific controlled 45.10% of revenue in 2025 and is advancing 6.85% annually on the back of China’s and India’s vast manufacturing bases and booming e-commerce. Nike, Adidas, and Puma channeled USD 4.53 billion into supplier clusters in Tamil Nadu, adding 50,000 jobs and fresh demand for localized packs. India’s broader packaging sector is slated to hit USD 204.81 billion in 2025 at 26.7% CAGR, elevating domestic converters. Robotic gluing lines proliferate as factories counter labor gaps and speed up one-box formats.

North America’s regulatory mosaic, spearheaded by California SB 54 and textile recovery bills, forces multi-tier compliance. Brands reroute supply chains toward Mexico and the US Southeast to dodge ocean freight volatility, lifting regional pack demand for near-shored sneakers. Smart-tag pilots scale fast as retailers seek inventory accuracy and anti-fraud tools.

Europe’s Packaging and Packaging Waste Regulation requires recyclability by 2028, pushing mono-material designs and bio-based trials. Luxury houses leveraging Portuguese manufacturing gain speed-to-market advantages, lowering transport emissions. Think! Shoes earned Austria’s Eco-label for pack redesigns that meet 95% recyclability thresholds.

Emerging Middle East, Africa, and South America markets grow from a low base yet benefit from urbanization and online shopping adoption. Infrastructure gaps hinder recycling loops, but multinationals partner with local collectors to secure post-consumer fiber.

Supply-chain diversification amid geopolitical tensions accelerates factory investment in Vietnam, Indonesia, and Brazil, spreading the footprint of the shoe packaging market.

Competitive Landscape

Market Concentration

Global leadership centers on integrated giants such as Smurfit WestRock and International Paper, which leverage mill-to-box verticals and global footprints. Their scale guards fiber access and funds R&D in automation and smart tags. Mondi teamed with CMC Packaging Automation to deliver auto-right-sized e-commerce lines that cut void by 25%. [3]Mondi, “Automated E-commerce Packaging,” mondigroup.com Corrugated majors also hedge pulp price swings with recycled capacity upgrades.

Disruptors attack niches: Packsize partners with Henkel on Eco-Pax bio-hot-melt adhesives, trimming greenhouse gases by 32% across 340 million boxes. [4]Packsize, “Eco-Pax Adhesive,” packsize.com SMX supplies NFC coatings that toughen chips for courier rough-handling, winning pilots with luxury sneaker labels. Mushroom-material startups attract venture capital for biotech substrates that promise home composting.

Competition intensifies in Asia-Pacific where hundreds of mid-sized plants chase OEM contracts. Robotics adoption separates winners, as vision-guided pickers raise output by 20% at similar labor counts. Patent trends show footwear brands designing packs into automated upper-assembly lines, hinting at longer-term insourcing that could reshape buyer-supplier dynamics within the shoe packaging market.

Shoe Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mondi and CMC launched an on-demand e-commerce line that sizes every shoe box to order, slashing fiber and filler waste.

- February 2025: Dow introduced bio-circular resins for footwear packs through a collaboration with Porto Indonesia Sejahtera.

- December 2024: SMX released chip-protective coatings that extend NFC life and fight counterfeits in premium shoe packaging.

- April 2024: Fast Feet Grinded opened Europe’s first shoe-recycling plant, supporting closed-loop packaging reuse.

Table of Contents for Shoe Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1E-commerce footwear boom

- 4.2.2Sustainability legislation and eco-conscious buyers

- 4.2.3Athletic and athleisure footwear proliferation

- 4.2.4Brand switch to mono-material “One-Box” shipping

- 4.2.5NFC / smart-tag shoe boxes combat counterfeits

- 4.2.6Advent of mushroom-based bio-packaging

- 4.3Market Restraints

- 4.3.1Volatile pulp and linerboard prices

- 4.3.2Plastic curbs and compliance costs

- 4.3.3Reverse-logistics reuse programs cut volumes

- 4.3.4Automation CAPEX barrier for SME factories

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material Type

- 5.1.1Plastic

- 5.1.2Paper and Paperboard

- 5.1.3Bio-based Materials (Mushroom, Pulp, Ocean Plastic)

- 5.2By Product Type

- 5.2.1Boxes and Cartons

- 5.2.2Bags

- 5.2.3Wraps

- 5.2.4Inserts and Accessories

- 5.3By Sustainability Profile??

- 5.3.1Conventional Packaging

- 5.3.2Eco-Friendly / Recycled Packaging

- 5.3.3Compostable / Re-usable Solutions

- 5.4By Footwear Category

- 5.4.1Athletic

- 5.4.2Casual

- 5.4.3Luxury and Designer

- 5.4.4Kids' Footwear

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Smurfit WestRock

- 6.4.2International Paper (DS Smith)

- 6.4.3Mondi Group

- 6.4.4PackQueen

- 6.4.5Packman Packaging

- 6.4.6PakFactory

- 6.4.7Unipack AD

- 6.4.8MARBER SRL

- 6.4.9Packtek

- 6.4.10Pratt Industries

- 6.4.11OXO Packaging

- 6.4.12My Box Printer

- 6.4.13CustomBoxline

- 6.4.14BoxesGen

- 6.4.15Better Packaging Co.

- 6.4.16Royal Packers

- 6.4.17M.K. Packaging

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Shoe Packaging Market Report Scope

Shoe packaging involves crafting and producing customized shoe boxes to meet specific brands' needs, styles, and visual preferences. This tailored approach empowers shoe manufacturers and retailers to craft packaging that reflects their brand's essence and elevates the overall presentation of their footwear. Customization options include various materials, colors, designs, and finishes, allowing for a wide range of creative and functional packaging solutions. Additionally, personalized shoe boxes can enhance the unboxing experience for customers, adding value and reinforcing brand loyalty.

The Shoe Packaging Market is segmented by material type (plastics and paper and paperboard), product type (bags, wraps, boxes, and cartons), and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, and Rest of Europe], Asia Pacific [China, India, Japan, Australia and New Zealand, and Rest of Asia Pacific], Latin America [Brazil, Mexico, Argentina, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market sizes and forecasts are in terms of revenue (USD) for all the above segments.