Aircraft Filters Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

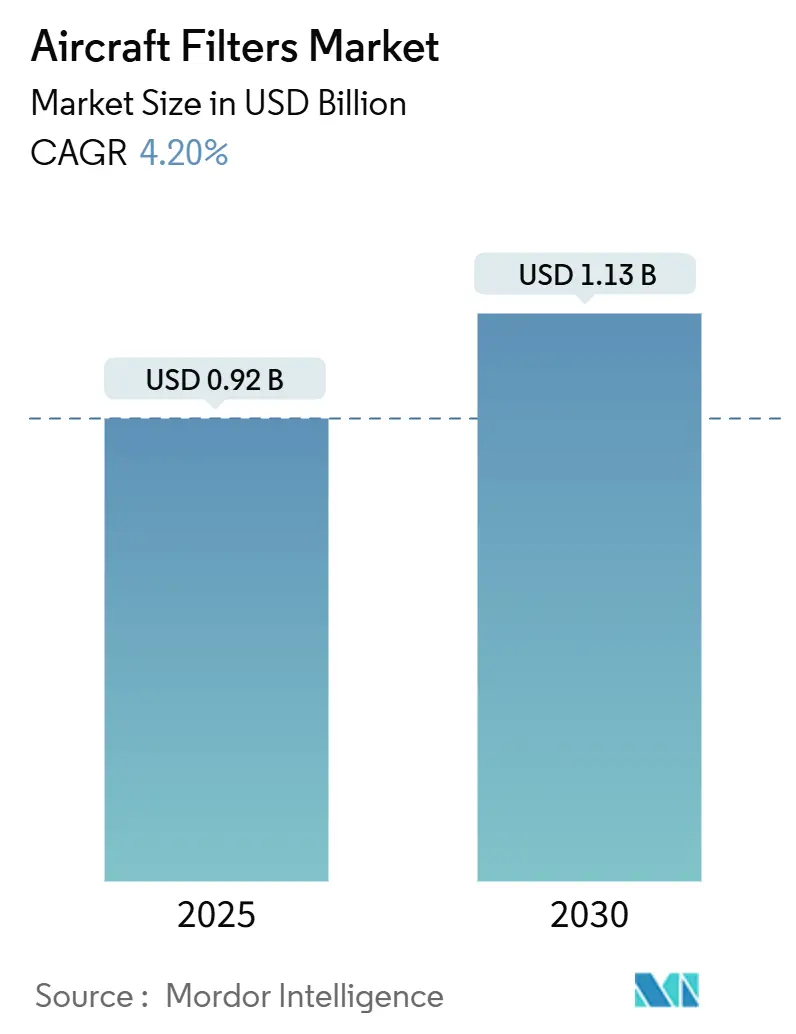

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.13 Billion |

| Growth Rate (2025 - 2030) | 4.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Filters Market Analysis by Mordor Intelligence

The aircraft filters market size is USD 0.92 billion in 2025 and is forecasted to advance at a 4.20% CAGR to USD 1.13 billion in 2030. Demand gains flow from rising fleet counts, stricter emissions and cabin-air rules, and the push toward sustainable aviation fuel and hydrogen propulsion. Commercial aviation continues to anchor consumption, military modernization sustains premium demand, and unmanned aerial systems (UAS) introduce new high-growth niches. Liquid filter innovation, activated-carbon media adoption, and digitalized maintenance practices reshape competitive positioning, while supply-chain resilience and certification expertise remain decisive differentiators. The aircraft filters market also benefits from pronounced aftermarket momentum as operators stretch asset life cycles and increase maintenance events.

Key Report Takeaways

- By filter type, air filters held 54.45% of the aircraft filters market share in 2024; liquid filters posted the fastest 4.56% CAGR through 2030.

- By material, glass fiber led with a 37.76% share in 2024, whereas activated carbon expanded the quickest at a 5.23% CAGR to 2030.

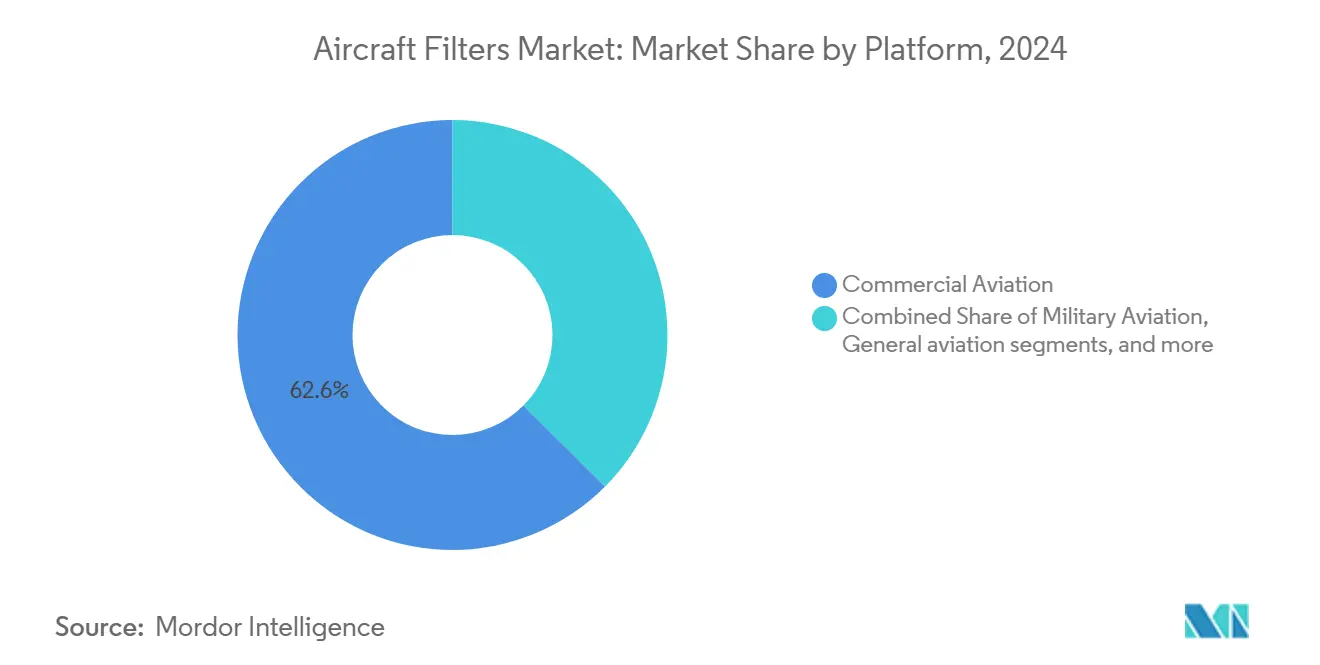

- By platform, commercial aircraft commanded 62.56% revenue in 2024; UAS remains the highest-growth slot with 6.21% CAGR through the forecast.

- By application, engine systems captured 28.54% of the aircraft filters market size in 2024, while cabin-air solutions recorded the strongest 4.75% CAGR outlook.

- By end user, OEM channels represented 53.24% of 2024 revenue, yet the aftermarket advances faster at 4.87% CAGR on extended service lives.

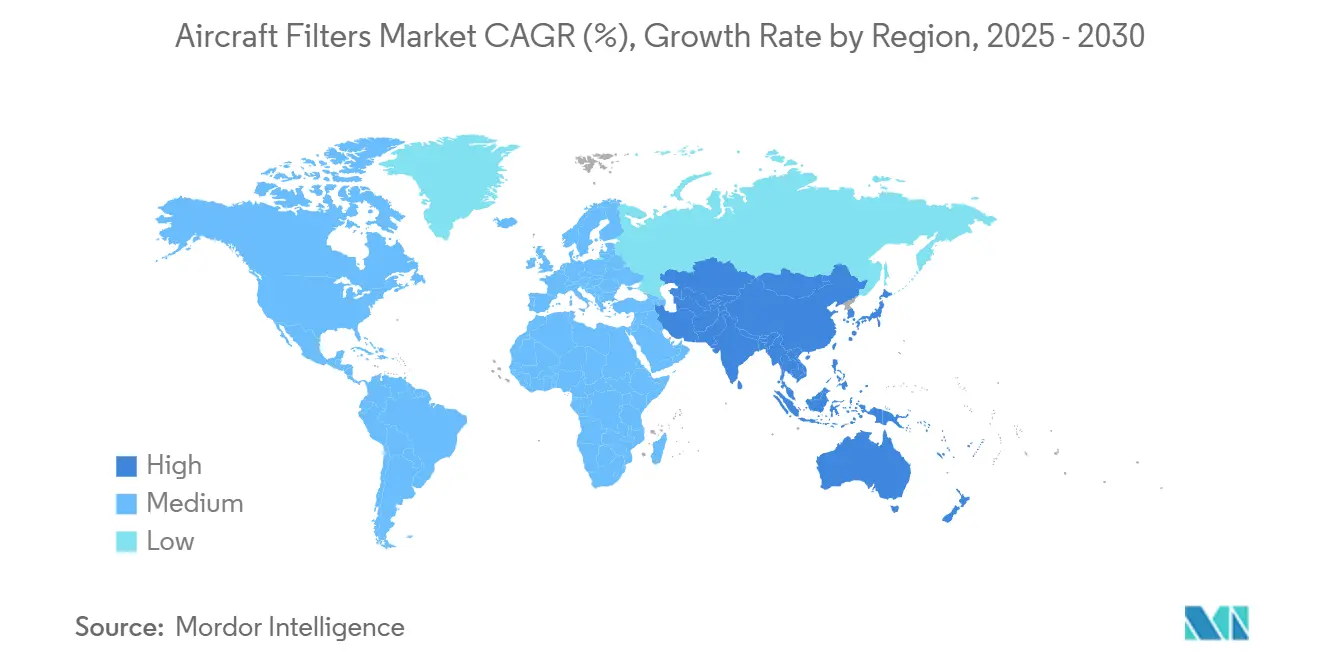

- By geography, North America led with a 27.67% 2024 share, and Asia-Pacific posts the leading 4.95% CAGR to 2030.

Global Aircraft Filters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global fleet size of commercial and military aircraft | +0.6% | Global with Asia-Pacific and North America emphasis | Medium term (2-4 years) |

| Implementation of stricter ICAO and FAA emissions regulations | +0.5% | North America and Europe drive adoption | Short term (≤ 2 years) |

| Ongoing growth in military modernization and procurement programs | +0.4% | North America, Europe, Asia-Pacific defense corridors | Long term (≥ 4 years) |

| Increasing demand for maintenance, repair, and overhaul (MRO) services | +0.3% | Global with Asia-Pacific MRO hub build-out | Medium term (2-4 years) |

| Transition toward sustainable aviation fuel (SAF) and hydrogen propulsion technologies | +0.3% | Europe and North America lead, Asia-Pacific follows | Long term (≥ 4 years) |

| Integration of advanced cabin air quality and health monitoring systems | +0.3% | Global, especially premium cabins | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Fleet Size of Commercial and Military Aircraft

Airframe deliveries continue to climb through 2030 as airlines update narrowbody fleets and defense ministries extend service lives of legacy fighters. Larger fleets translate directly into more filtration sets because each mainline jet carries over 20 filter elements across engines, cabins, hydraulics, fuel lines, and avionics. Modernization programs for platforms like the F-22 include upgraded environmental-control and filtration hardware to assure cockpit air quality during extended deployments. Filter replacement intervals typically run 500–2,000 flight hours, so fleet utilization rates amplify aftermarket volume. Supply-chain redundancy gains importance because a grounded wide-body can cost operators USD 150,000 per day in lost revenue, making ready filter availability a critical performance indicator.

Implementation of Stricter ICAO and FAA Emissions Regulations

Regulatory bodies are raising performance bars on particulate, sulfur, and volatile organic emissions. FAA’s 2024 system-safety assessment rule obliges design changes that eliminate latent failures, pushing filter makers to integrate health-monitoring sensors for early clog detection. Parallel nvPM limits from ICAO and coordinated updates by EASA harmonize certification thresholds and accelerate the global rollout of higher-efficiency media. Long-life elements that reduce maintenance frequency and support sustainable aviation fuel compatibility earn preference. Compliance costs challenge smaller enterprises and steadily shift market share toward incumbents with robust testing facilities.

Ongoing Growth in Military Modernization and Procurement Programs

Defense budgets continue to prioritize aircraft upgrades for electronic warfare, range extension, and crew protection. Military specifications exceed civil equivalents in shock, vibration, and temperature extremes, enabling premium pricing for specialized filters. Cross-domain operations heighten the need for chemically clean cabin environments during long missions, importing technology initially developed for commercial health monitoring. Security mandates reinforce domestic sourcing, tilting procurement toward local suppliers that can meet traceability standards. Lengthy acquisition timelines, however, underline the value of a mixed commercial-military portfolio to balance cash flow.

Increasing Demand for Maintenance, Repair, and Overhaul (MRO) Services

Global MRO activity has rebounded past pre-pandemic levels as airlines extend fleet life to buffer new-aircraft delivery delays. Flagship projects such as Air India’s Bengaluru mega hub and new Malaysian component factories shorten regional turnaround times and invite local filtration stocking points. Predictive-maintenance platforms move airlines from flight-hour replacement to condition-based swaps, allowing suppliers that embed sensors in filter housings to capture service contracts. Consolidation toward large-scale hangars boosts bargaining power, so component makers differentiate with rapid logistics and on-site technical teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in global aircraft production and delivery cycles | -0.3% | Major manufacturing hubs in North America and Europe | Short term (≤ 2 years) |

| High costs associated with product qualification and regulatory certification | -0.3% | Global with regional process variations | Medium term (2-4 years) |

| Supply chain disruptions affecting aerospace-grade alloy availability | -0.2% | Global; specialty metals hot spots | Short term (≤ 2 years) |

| Adoption of additive manufacturing reducing the frequency of filter replacements | -0.2% | Early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Global Aircraft Production and Delivery Cycles

Line-rate adjustments at Boeing and Airbus ripple down to Tier-2 component suppliers. Filters specific to one program cannot easily shift to others, so abrupt delivery cuts strand inventories and hamper cash flow. Risk-sharing partnerships and modular designs able to serve multiple platforms temper exposure but require upfront redesign investments. Suppliers now build flexible production cells and lean inventories but must still guarantee 24-hour AOG fulfillment.

Supply Chain Disruptions Affecting Aerospace-Grade Alloy Availability

Counterfeit titanium cases in 2024 prompted recalls and new documentation layers, increasing lead times and administrative costs.[1]United States Government Accountability Office, “Aviation Metals: Agency Actions Needed to Address Counterfeit Titanium,” gao.gov Specialized sintered alloys for high-temperature housings face geopolitical supply risks. Firms respond by qualifying alternate materials, dual-sourcing, and expanding on-site metallurgical testing, yet such actions inflate working capital and squeeze margins, especially in price-sensitive aftermarket channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filter Type: Liquid Filters Gain Ground on Sustainability Demands

Air filters commanded 54.45% revenue in 2024 thanks to mandatory installation across engines, cabins, and avionics bays. The aircraft filters market size for air filters is expected to grow steadily with fleet additions, yet growth trails the 4.56% CAGR logged by liquid filters. Liquid-stage demand accelerates because SAF blends and planned hydrogen propulsion require finer fuel-line, oil, and hydraulic filtration to manage unfamiliar contaminant profiles. Coalescing separator modules with on-board water-sensing electronics fetch premium pricing and open recurring retrofit sales for in-service fleets. Manufacturers increasingly integrate smart differential-pressure gauges that alert MRO crews before bypass events, reducing unscheduled removals.

Liquid-filter progress reflects rising penetration in bleed-air moisture-separator units and fuel-cell intake filters on developmental electric VTOL prototypes. As powered-lift regulations mature, these hybrid-electric aircraft will embed multiple small, high-throughput liquid and air filters to protect motors, inverters, and thermal loops. Suppliers capable of leveraging common media across both legacy turbines and new energy designs hold the potential to gain share in every sub-fleet the aircraft filters market serves.

By Material: Activated Carbon Surges on Cabin-Air Quality Focus

Glass fiber maintained a 37.76% share in 2024 as the long-standing, cost-effective choice for mechanical particulate removal. However, activated carbon’s 5.23% CAGR leads material growth because chemical adsorption addresses VOC and odor targets set by airlines and regulators. The aircraft filters market share for activated carbon elements rises disproportionally in premium cabin retrofits where carriers advertise “hospital-grade” air systems. Composite media bonding glass microfiber layers to carbon granules combines particulate and chemical removal, minimizing pressure drop penalties.

Aluminum casings remain vital where weight, corrosion resistance, and recyclability matter, while high-temperature alloy enclosures in engine oil filters defend against thermal cycling. Thermoplastics play a role in low-pressure return lines, but sustainability trends push R&D toward bio-based resins. Material selection now weighs supply chain resilience as much as performance; companies qualifying local extrusion and weaving facilities mitigate geopolitical risk and shorten replenishment lead times.

By Platform: Commercial Aircraft Dominates, UAS Chart the Fastest Climb

Commercial jets contributed 62.56% of 2024 revenue, underpinned by narrowbody fleet expansions serving dense regional networks. Widebody programs add value disproportionately because each aircraft features more filtration stages and higher capacity elements. Regional jet demand is steady on essential-air-service missions requiring reliable environmental control systems in rugged conditions.

UAS revenue is smaller today but scores a 6.21% CAGR through 2030, benefiting from defense ISR budgets, cargo drone pilots, and emerging passenger eVTOL craft. Hydrogen-powered drones for long-endurance maritime surveillance introduce ultrafine particulate and moisture filters to protect PEM stacks, broadening application depth. Military aviation provides a balanced stream of high-margin orders for NBC-rated cabin filters and high-shock hydraulic screens. In contrast, general aviation’s business jet refurbishments keep demand for quick-turn cabin and hydraulic elements.

By Application: Engine Systems Still Lead but Cabin Solutions Accelerate

Engine filtration held a 28.54% share in 2024, reflecting the criticality of air intake, oil, and fuel cleanliness in preventing compressor erosion and bearing wear. The aircraft filters market size for engines will continue expanding alongside aircraft deliveries, yet cabin-air solutions post a notable 4.75% CAGR. Cabin filters gain visibility as airlines leverage HEPA-plus-carbon packages to reassure travelers and comply with the ventilation rule 14 CFR 25.831.

Avionics cooling, hydraulic, and pneumatic circuits add niche pockets of growth as fly-by-wire penetration and higher-pressure hydraulic systems require finer filtration. Integrated health-monitoring modules that stream delta-pressure data into aircraft condition monitoring systems allow predictive maintenance and help manufacturers upsell analytics subscriptions.

By End User: Aftermarket Builds Velocity on Extended Service Lives

OEM installations secured 53.24% of 2024 turnover, but aftermarket CAGRs top 4.87% as airlines prolong aircraft retirement schedules and step up interior refurbishments. The aircraft filters market size connected to aftermarket replacements swells when utilization exceeds 12 flight hours daily, compressing replacement intervals. Retrofit campaigns that swap legacy fiberglass elements for combined HEPA-carbon cartridges create incremental revenue while improving cabin wellness scores.

Suppliers with global distribution and FAA/EASA Part-145 repair-station partnerships command favorable positions. Parker-Hannifin’s aerospace filtration backlog expanded sharply following the Meggitt acquisition, illustrating how consolidation can unlock cross-selling into broader systems packages. Digital twin pilots calculating real-time filter life aim to lower unscheduled removals, anchoring long-term service agreements that stabilize revenue.

Geography Analysis

North America retained a 27.67% share in 2024, bolstered by a dense operator base, stringent FAA oversight, and high defense outlays. Filter suppliers benefit from proximity to multiple widebody final-assembly lines and an extensive MRO ecosystem that requires rapid spare-parts logistics. Recent FAA rules on powered-lift integration and system safety assessment introduce near-term spikes in certification consulting demand. Military budgets sustain steady procurement of NBC-capable cabin filtration and desert-rated particle separators, keeping margins healthy.

Asia-Pacific exhibits the strongest 4.95% CAGR, propelled by fleet expansion in India, China, and fast-growing Southeast Asian markets. Air India’s USD 2.5 billion Bengaluru MRO campus and Malaysian component factories shorten lead times and open supplier localization pathways. Domestic aircraft programs in China drive in-country filter production under local-content rules, prompting joint ventures to transfer technology while maintaining export compliance. Strong regional cargo-drone pilots also accelerate niche UAS filter adoption.

Europe’s mature base registers modest growth yet leads sustainability policy. The SAF blend mandate and hydrogen aviation research grants create fertile ground for next-gen fuel and cryogenic filters. NATO modernization and industrial offsets ensure steady demand for combat-grade environmental control filters. Joint FAA-EASA cooperation on emerging technologies lessens duplicate testing for suppliers.[2]Federal Aviation Administration, “FAA and EASA Pledge Cooperation,” faa.gov

Smaller but strategic regions round out demand. The Middle East pushes high-cycle narrowbody utilization that elevates replacement volume, and harsh sand environments necessitate robust intake filters. South America’s rebound in tourism supports cabin-air system upgrades on aging fleets. Africa’s market remains nascent, but opportunities exist in humanitarian cargo drones that require light, high-efficiency filters operating in dusty conditions.

Competitive Landscape

The aircraft filters market exhibits moderate concentration. Parker-Hannifin Corporation strengthened its lead with the USD 6.8 billion Meggitt acquisition, creating a broad fluid-handling portfolio that bundles filtration with valves and thermal-management products.[3]Parker Hannifin, “Fiscal 2024 Fourth-Quarter Results,” parker.com Donaldson Company, Inc. posted 18.70% aerospace defense revenue growth in early 2025, leveraging proprietary synthetic media and a global distribution footprint.[4]Donaldson Company, “Second Quarter Fiscal 2025 Earnings,” donaldson.com Pall Corporation remains a key technology specialist in liquid-fuel microfiltration and hydraulic contamination control.

Strategic moves trend toward vertical integration and porous media acquisitions. IDEX Corporation closed its purchase of Mott Corporation to access sintered porous expertise suited for hydrogen and electric-propulsion filters. Thermo Fisher’s takeover of Solventum’s filtration unit signals crossover interest from life-science filtration into aerospace applications demanding bacterial and molecular adsorption.

Technology race themes include sensor-enabled “smart” elements that transmit health data, multi-layer media combining HEPA efficiency with VOC absorption, and all-metal additive-manufactured cages that endure wide temperature ranges. Incumbents face competitive incursions from electric-aircraft start-ups seeking compact, 3D-printed cooling filters. Certification remains a high entry barrier; new entrants often partner with incumbents to access DO-160 qualification labs.

Aircraft Filters Industry Leaders

Parker-Hannifin Corporation

Donaldson Company, Inc.

Freudenberg Filtration Technologies GmbH & Co. KG

Safran SA

Pall Corporation (Danaher Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Boeing Company and Donaldson Company, Inc. expanded their partnership by incorporating rotorcraft filtration products into Boeing's distribution portfolio.

- September 2023: AAR CORP. established a multi-year exclusive distribution agreement with Pall Corporation to provide aircraft filtration products to foreign military customers. Through this agreement, AAR manages the inventory, marketing, and distribution of Pall's filtration solutions, enhancing aftermarket support for defense aviation customers globally.

Global Aircraft Filters Market Report Scope

| Air Filters |

| Liquid Filters |

| Glass Fiber |

| Activated Carbon |

| Aluminum |

| Plastic |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Missions | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Systems | Civil and Commercial |

| Defense and Government |

| Engine |

| Cabin Air Filtration System |

| Avionics Cooling System |

| Hydraulic System |

| Fuel System |

| Pnuematic System |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Filter Type | Air Filters | ||

| Liquid Filters | |||

| By Material | Glass Fiber | ||

| Activated Carbon | |||

| Aluminum | |||

| Plastic | |||

| By Platform | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Missions | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| Unmanned Aerial Systems | Civil and Commercial | ||

| Defense and Government | |||

| By Application | Engine | ||

| Cabin Air Filtration System | |||

| Avionics Cooling System | |||

| Hydraulic System | |||

| Fuel System | |||

| Pnuematic System | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft filters market in 2025 and how fast is it growing?

The aircraft filters market was valued at USD 0.92 billion in 2025 and is forecasted to advance at a 4.20% CAGR to USD 1.13 billion in 2030.

Which filter type is growing the fastest?

Liquid filters record the highest growth with a 4.56% CAGR because sustainable aviation fuel and hydrogen systems need finer fuel filtration.

Why is activated carbon attracting interest in cabin applications?

Airlines deploy activated carbon layers to remove volatile organic compounds and odors, meeting stricter cabin-air standards and passenger health expectations.

What drives aftermarket demand for aircraft filters?

Extended aircraft service lives, higher utilization, and retrofit programs that add health-monitoring features push aftermarket growth at a 4.87% CAGR.

Which region offers the highest growth potential?

Asia-Pacific leads regional expansion with a 4.95% CAGR owing to fleet additions, new MRO hubs, and developing aerospace manufacturing capacity.

How are regulations influencing filter design?

FAA and ICAO rules on emissions, system safety, and powered lift vehicles mandate higher filtration efficiency and integrated health-monitoring sensors to preempt latent failures.

Page last updated on: