Commercial Aircraft Windows And Windshields Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

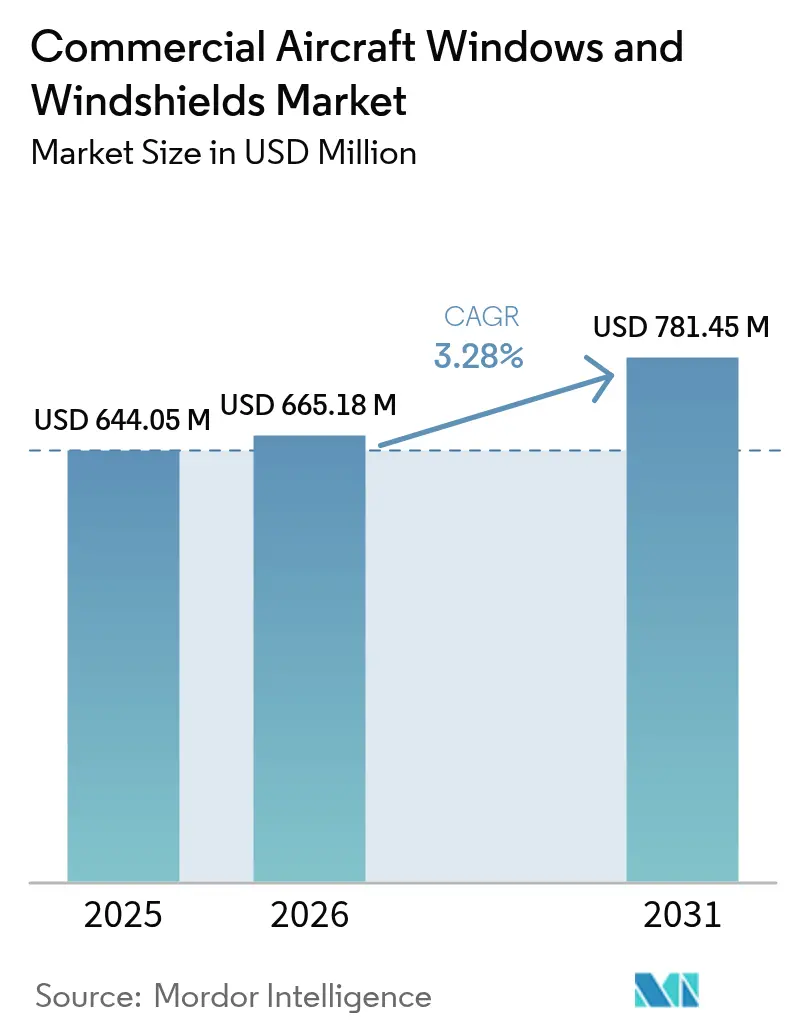

| Market Size (2026) | USD 665.18 Million |

| Market Size (2031) | USD 781.45 Million |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

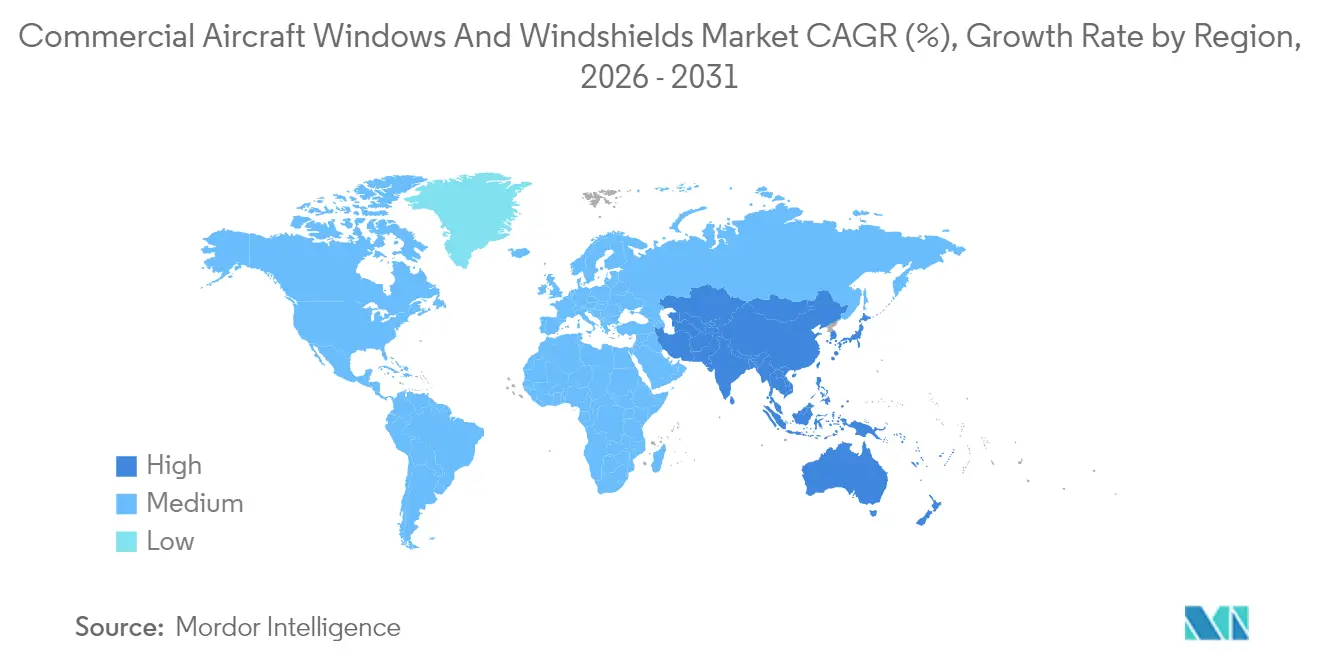

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

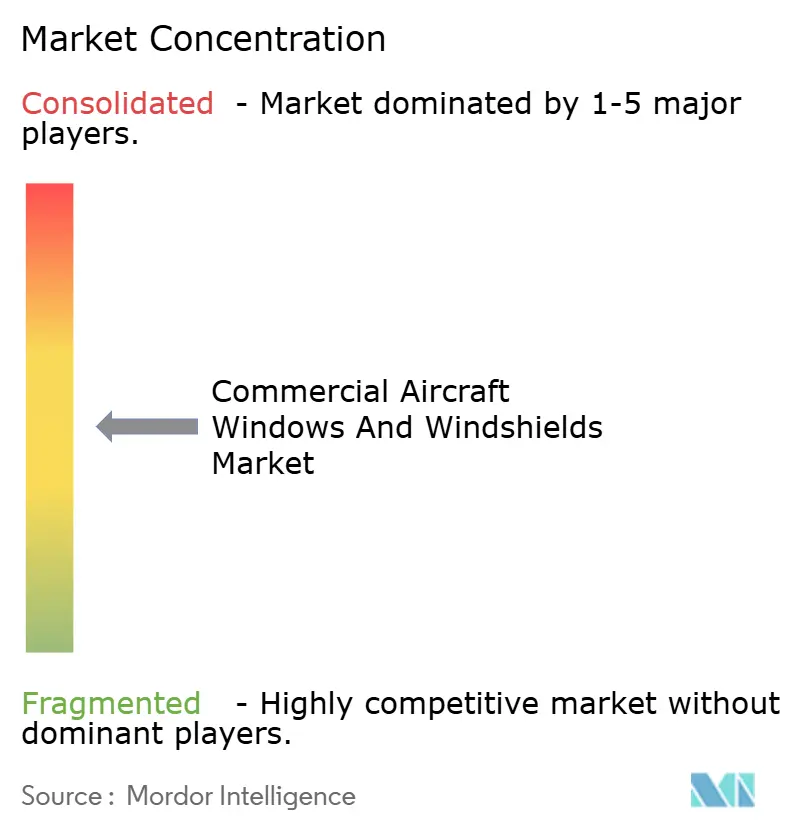

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Windows And Windshields Market Analysis by Mordor Intelligence

The commercial aircraft windows and windshields market size was valued at USD 644.05 million in 2025 and estimated to grow from USD 665.18 million in 2026 to reach USD 781.45 million by 2031, at a CAGR of 3.28% during the forecast period (2026-2031). Continued fleet growth, rising retrofits, and rapid material innovation sustain demand despite lingering supply‐chain constraints. Airlines prioritize lighter windows that help trim fuel burn, while premium carriers install dimmable and panoramic solutions that boost customer experience. Regulatory pressure from the FAA and EASA drives more frequent windshield replacement cycles, and the multi-year production backlogs at Airbus and Boeing incentivize tier-1 suppliers to expand capacity. At the same time, certification costs and shortages of specialty glass and resins limit the pace at which new technologies scale.

Key Report Takeaways

- By aircraft type, narrowbody aircraft led with 61.78% of the commercial aircraft windows and windshields market share in 2025, while the segment is projected to expand at a 6.12% CAGR to 2031.

- By application, cabin windows accounted for a 64.86% market share in 2025, whereas cockpit windshields are advancing at a 6.05% CAGR through 2031.

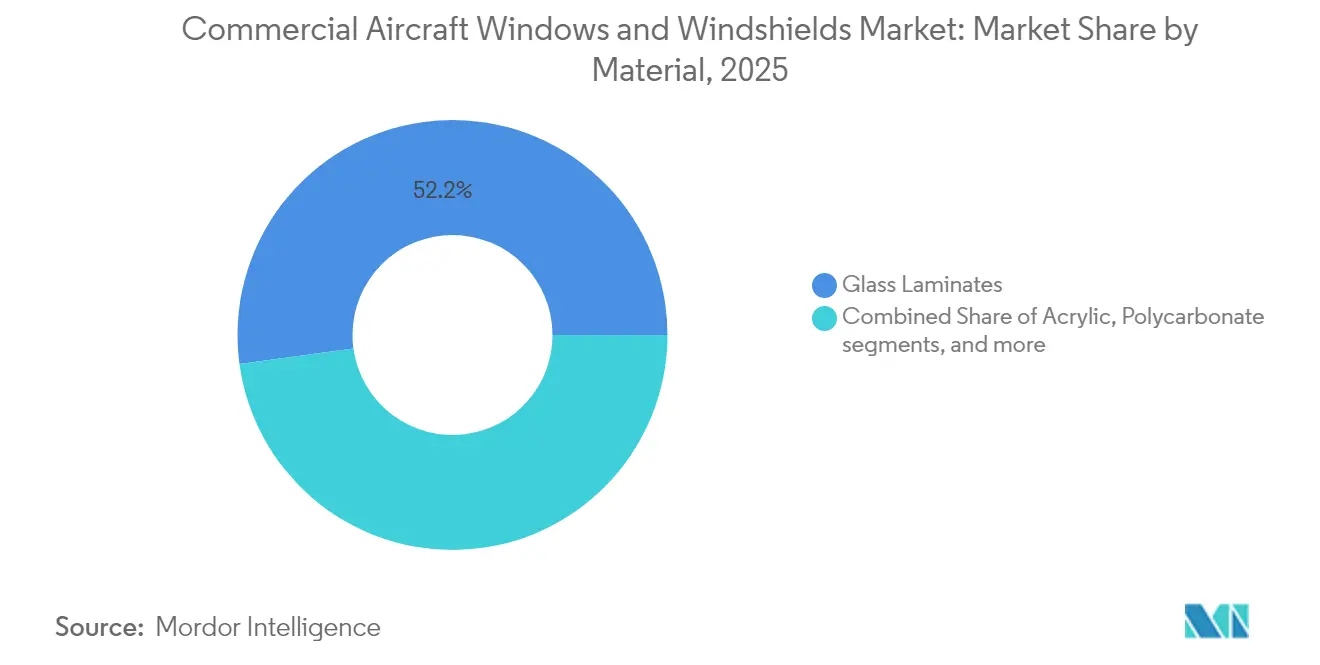

- By material, glass laminates dominated the commercial aircraft windows and windshields market, with 52.15% of the share in 2025; polycarbonate is forecasted to grow at a 6.75% CAGR to 2031.

- By technology, conventional multi-layer laminates captured 69.75% revenue share in 2025, yet electrochromic smart windows are set to surge at an 7.72% CAGR during 2026-2031.

- By end market, OEM installations held 56.05% of the commercial aircraft windows and windshields market size in 2025, while the aftermarket is expected to register a 5.88% CAGR.

- By geography, North America led with 34.25% revenue share in 2025; Asia-Pacific is forecasted to expand at an 7.75% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Windows And Windshields Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for larger panoramic cabin windows | +0.8 | Global, emphasis on premium carriers in North America and Europe | Medium term (3-4 years) |

| Acceleration of electrochromic smart windshield adoption | +1.2 | North America and Europe, growing adoption in Asia | Medium term (3-4 years) |

| Increasing production backlog at Boeing and Airbus | +0.6 | Global, concentration in manufacturing hubs | Short term (≤ 2 years) |

| Stringent FAA and EASA bird-strike and thermal-shock standards | +0.9 | Global, stricter enforcement in North America and Europe | Short term (≤ 2 years) |

| Lightweight acrylic and polycarbonate adoption | +0.7 | Global, early adoption in North America and Europe | Medium term (3-4 years) |

| Airline fleet modernization programs in Asia and Middle East | +1.0 | Asia-Pacific and Middle East | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Larger Panoramic Cabin Windows

Airlines view larger windows as a brand differentiator that can lift high-yield ticket sales. Airbus integrated oversized apertures on the A350 and redesigned A320 sidewalls to let more daylight flood the cabin, which improves the perception of space and reduces jet-lag-related fatigue.[1]Airbus, “A350 Cabin Highlights Enhanced Passenger Experience,” airbus.com Suppliers have responded with stronger thin-glass laminates that preserve structural integrity at greater dimensions while trimming weight. Tinted coatings and hydrophobic layers keep clarity high even after repeated cleaning cycles. Premium carriers retrofit older widebodies with upgraded window surrounds that support bigger panes and LED mood lighting. These upgrades raise cabin refurbishment costs but extend airframe service life. Consequently, panoramic designs move from novelty to mainstream line-fit options on new single-aisle programs.

Acceleration of Electrochromic Smart Windshield Adoption

Electronically dimmable solutions, once confined to business jets, are entering large commercial platforms. Gentex’s latest devices block 99.9% of light and reach full-clear in 90 seconds, a feature now line-fit on the B787 and selected A321XLR deliveries.[2]Gentex Corporation, “Advanced Dimmable Device Portfolio Debuts at CES 2025,” gentex.comLaboratory tests show infrared rejection of 77.3% and visible transmittance from 39.2% to 56.4%, which lowers cockpit heat load and cuts air-conditioning draw. Embedding thin-film solar collectors along the windshield perimeter powers tint cycles without tapping aircraft buses. Airlines that install the technology in premium cabins report higher Net Promoter Scores and faster turnarounds because blinds are no longer needed. As certification precedents accumulate, suppliers expect the cost per window to fall, driving wider adoption on narrowbody fleets.

Increasing Production Backlog at Boeing and Airbus Stimulating Tier-1 Suppliers

Airbus A320neo slots remain sold until 2030, and regulatory audits cap Boeing’s B737 output growth. This visibility enables window and windshield manufacturers to commit capital to new autoclaves and laser-trimming lines. PPG Industries reported a record aerospace coatings backlog worth USD 290 million and double-digit organic sales growth in 2024. Expanded capacity shortens lead times and supports the shift to advanced laminates and smart coatings. Suppliers also leverage the backlog to negotiate longer contracts that stabilize raw-material supply and encourage joint R&D with airframers.

Lightweight Acrylic and Polycarbonate Adoption for Fuel-Burn Reduction

Polycarbonate weighs up to 40% less than chemically toughened glass and absorbs 200 times the impact before cracking. The material is therefore gaining share in regional jets where every kilogram translates into measurable fuel savings. Samyang’s PFAS-free flame-retardant grade meets V-0 on UL 94 and offers high transparency at thin gauges.[3]Samyang Corporation, “PFAS-Free Flame-Retardant Polycarbonate Datasheet,” plasticstoday.com Operators of high-cycle aircraft report inspection intervals extended by 8-10% because polycarbonate endures ramp debris better than traditional panes. Weight savings are also compounded when airlines pair lighter windows with composite sidewalls, highlighting the system-level payoff of material substitution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain constraints in specialty materials | -0.9 | Global, severe impact in regions distant from manufacturing centers | Short term (≤ 2 years) |

| High certification and qualification costs | -0.6 | Global, greater impact on smaller manufacturers | Long term (≥ 5 years) |

| Volatile OEM production rates | -0.5 | Global, varying impact based on OEM relationships | Short term (≤ 2 years) |

| Limited repair capabilities outside North America and Europe | -0.3 | Asia-Pacific, Latin America, and Africa | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Constraints in Specialty Materials

Chemically toughened glass substrates and interlayer resins rely on a few plants in North America and Europe. Pandemic-era disruptions still ripple through procurement schedules, limiting batch sizes and driving spot price spikes. Narrowbody ramp-ups have forced tier-2 laminators to juggle allocation across multiple OEM lines, which elongates lead times. Freight bottlenecks add risk when climate-controlled containers are unavailable. Some airlines, therefore, pre-buy replacement panes and hold inventory, tying up working capital. Researchers explore recycled glass cullet and bio-based resins to diversify feedstocks, yet commercial volumes remain small.

High Certification and Qualification Costs Hindering New Technologies

Every new smart-glass formulation must pass FAA bird-strike, thermal-shock, and pressure-differential tests. The latest FAA rulemaking requires system-level Safety Assessments and ongoing Certification Maintenance Requirements. Full test campaigns can exceed USD 8 million per windshield type, deterring smaller innovators. Time-to-market stretches beyond 36 months, eroding first-mover advantage. Tier-1 suppliers mitigate this burden by co-funding programs with OEMs, but niche applications still face hurdles. Consequently, many material startups pivot to business aviation first, delaying benefits for high-volume single-aisle jets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody Dominance Underpins Future Growth

The narrowbody segment contributed 61.78% of the market share of commercial aircraft windows and windshields in 2025 and will expand at a 6.12% CAGR through 2031. A320neo and B737 MAX families continue to capture orders from low-cost carriers prioritizing short-haul, point-to-point service. Each single-aisle airframe houses fewer panes than a twin-aisle, yet the fleet’s huge installed base secures the bulk of revenue. Retrofits add dimmable solutions on high-yield rows and reinforce frames for larger apertures. Widebody aircraft keep a smaller slice but deliver high value per shipset because the A350 and B787 specify oversized panoramic windows that fetch premium pricing. Regional jets and turboprops leverage lightweight polycarbonate to widen range and improve block-time economics, while freighters opt for rugged glass that resists handling damage. Long-term, conceptual windowless cabins could trim weight further, yet certification complexity suggests a gradual evolution rather than a sudden switch.

Narrowbody momentum benefits the commercial aircraft windows and windshields market size because single-aisle programs dominate order backlogs. Greater shipset volumes incentivize suppliers to automate lamination and coating lines, which lowers unit cost and unlocks smart features for entry-level cabins. Customers weigh marginal fuel savings against acquisition premiums, so adopting electrochromic panes follows a top-down pattern starting with flagship carriers. Still, rising OEM production targets ensure even conservative airlines refresh their inventory. Widebody deliveries concentrate in international hubs where brand positioning matters more, sustaining demand for the largest dimmable windows on ultra-long-range variants.

By Application: Cabin Windows Rule While Cockpit Upgrades Accelerate

Cabin windows accounted for 64.86% of the commercial aircraft and windshields market size in 2025 due to a four-to-six-per-row geometry across all seats. Retrofits that install crew-controlled aerBlade shades or embed OLED lighting underline the cabin’s importance in brand differentiation. Advancements in anti-smudge coatings keep clarity high despite frequent passenger contact and cleaning cycles. Cockpit windshields post the fastest segment CAGR of 6.05%, given stricter bird-strike tolerance and emerging augmented-reality overlays. Honeywell and NXP’s collaboration on large-area cockpit displays increases optical load, pushing window makers to refine conductive coatings for better EMI shielding.UV-blocking technology further protects pilots on high-latitude routes, addressing occupational health mandates.

The replacement interval for cockpit glass narrows when compliance standards tighten, magnifying aftermarket revenue. Certification rules demand redundant heating elements to prevent ice build-up, which raises the bill of materials but enhances operational safety. Airlines balance these costs by synchronizing windshield swaps with scheduled engine overhauls, optimizing downtime. Cabin pane turnover is slower, yet fleet-wide retrofit programs can spur lumpy order spikes. As sustainability metrics gain regulatory teeth, lighter planes emerge as an attractive lever to cut per-trip emissions.

By Material: Glass Laminates Still Lead but Polycarbonate Gains Pace

Glass laminates retained 52.15% market share in 2025 thanks to proven optical fidelity and decades of flight hours. Gentex’s thin-glass laminate, 25% quieter than polycarbonate, finds favor on premium cabins that charge for acoustic comfort. However, polycarbonate’s 6.75% CAGR reflects airlines’ push for fuel savings. The new PFAS-free grade from Samyang meets stringent flame-retardant norms and slides into existing tooling with minimal adjustments. Acrylic remains relevant where cost sensitivity outweighs weight concerns, especially on short-life regional aircraft. Composite sandwich structures form a niche for military transports and future spaceplanes that need high thermal shock tolerance. Nanostitched carbon nanotube reinforcements under investigation at MIT promise to blend ultralight weight with crack resistance, potentially rewriting material hierarchies after 2030.

Material choice shapes maintenance cycles. Glass offers superior scratch resistance but shatters when hit by ramp debris, whereas polycarbonate scratches faster yet survives impacts. Airlines increasingly specify hybrid solutions: an inner PC layer for toughness and outer glass for clarity. Such architectures raise lamination complexity, benefiting suppliers with interlayer chemistry expertise. Environmental regulation may soon phase out older fluorinated coatings, nudging the market toward next-generation UV-absorbing films that rely on metal-oxide nanoparticles.

By Technology: Conventional Systems Remain Core as Electrochromic Surges

Conventional multi-layer laminates held 69.75% revenue share in 2025 by established supply chains and amortized certification. These panes integrate embedded heaters, moisture barriers, and UV filters in a stack familiar to airlines and regulators. Heated and anti-ice variations guard against crystal formation in cold soak conditions, aided by hydrophobic films like NANOMYTE neicorporation.com. Despite dominance, conventional systems grow slowly because the feature set is mature. Conversely, electrochromic windows post a torrid 7.72% CAGR, with riding breakthroughs in durable conductive polymers and low-voltage switching. Collins Aerospace demonstrated virtual windows for windowless suites that broadcast real-time exterior video, hinting at future cabin flexibility. UV/IR-coated panes slot between basic and smart variants, helping low-cost carriers drop cabin temperature and reduce air-conditioning draw in hot climates.

Certification pathways for electrochromic technology shorten as regulators accept prior test data, cutting costs for each new size. Airlines use variable opacity to impose sleep cycles on red-eye flights and manage glare during taxi. Ground crews appreciate that windows tint automatically under strong ramp sunlight, protecting interior fabrics. Suppliers now bundle predictive maintenance algorithms that analyze switching speed degradation, enabling proactive swap-outs before failures interrupt service.

By End Market: OEM Installations Dominate but Aftermarket Growth Outpaces

OEM line-fit captured 56.05% of sales in 2025 because windows are shipped installed on every new aircraft. Yet the aftermarket registers a 5.88% CAGR, exceeding OEM growth as operators extend service life and refresh cabins instead of placing new orders. Emirates exemplifies the retrofit wave with plans to upgrade 71 widebodies, adding dimmable windows and refreshed trim. MRO providers respond by expanding hangar footprints; AAR’s Oklahoma City site adds 80,000 sq ft to handle all B737 variants beginning in 2026. Window OEMs partner with repair stations to stock kits regionally, minimizing transit times. Certified repair capability outside North America and Europe remains limited, creating an opportunity for Asian independents if they navigate local regulatory frameworks.

OEM demand stays solid owing to long order books, but supply-chain snarls may shift some revenue into later years. By contrast, aftermarket work orders can be flexed within weeks, offering suppliers a buffer when line-fit schedules are delayed. Airlines also compress cabin downtime by combining window swaps with seat-back screen upgrades, creating bundled contracts exceeding USD 2 million per aircraft.

Geography Analysis

North America controlled 34.25% of the commercial aircraft windows and windshields market in 2025, buoyed by its dense airframe manufacturing ecosystem and extensive MRO capacity. FAA regulations compel quicker windshield replacement, expanding local demand. PPG’s aerospace backlog and Gentex’s dimmable glass pipeline underscore the region’s technology pull. Canada complements the US with composite research hubs that refine polycarbonate bonding techniques.

Asia-Pacific is the fastest mover, advancing at an 7.75% CAGR through 2031. Boeing foresees India and South Asia quadrupling their fleet by 2043, requiring 2,835 new airplanes. Local carriers adopt the latest cabin standards to woo middle-class travelers, so dimmable and panoramic panes see quicker line-fit. Multiple OEMs have site repair centers near Guangzhou, Hyderabad, and Nagoya to shorten turnaround times. Yet, material imports face longer logistics lead times, magnifying the impact of resin shortages.

Europe retains a strong share anchored by Airbus production in Toulouse and Hamburg. The bloc’s climate policies accelerate the adoption of lighter materials that shrink per-trip emissions. Suppliers there pioneer resource-efficient glass melting processes and lead recycling standards that could become global benchmarks. Middle Eastern carriers such as Emirates invest in large-scale retrofits that rely on European-built kits, sustaining cross-regional flows. Africa lags in fleet size but offers a greenfield opportunity for local repair stations as intra-continental connectivity rises. Latin America shows steady expansion driven by Brazilian regional jets and MRO clusters around São José dos Campos.

Regulatory Landscape

Commercial aircraft windows and windshields are certified under FAA 14 CFR Part 25 and EASA CS-25 requirements, with key glazing provisions including 14 CFR 25.775 (windshields and windows) and 14 CFR 25.773 (pilot compartment view). These rules frame compliance around pressure-differential and aerodynamic load capability, optical quality, and resistance to hazards such as bird impact on pilot-facing panes. In turn, they influence material selection (glass laminates, polycarbonate, and hybrid stacks) and heater integration for anti-ice performance.

For novel glazing features and cabin interior glass applications, certification can expand through Special Conditions (14 CFR 21.16) and type certification basis amendments under 14 CFR 21.101, adding tests around fragmentation and glass-throw risks. Continued airworthiness is managed through FAA and EASA Airworthiness Directives that can mandate inspections and electrical checks for specific windshield configurations, reinforcing recurring demand for compliant replacements and repairs in both OEM and aftermarket channels.

Value Chain Analysis

The value chain begins with specialty inputs (mineral glass, stretched acrylic, polycarbonate, PVB/TPU interlayers, and transparent conductive coatings such as ITO), followed by forming, lamination, coating, and integration of functions such as heaters, hydrophobic layers, and EMI-shielding films. Qualified Tier-1 transparency manufacturers then supply shipsets to aircraft OEM final assembly lines and to certified aftermarket channels. Repair stations and MROs perform removals, inspections, and replacements under approved data and documentation.

A key structural feature is supplier concentration in qualified materials and processes, which keeps switching costs high and leaves the chain exposed to bottlenecks when specialty resins, coatings, or autoclave capacity are constrained. The chain also shows regionalization tied to supply assurance requirements. For example, Rostec-linked Obninsk Research and Production Enterprise Technologiya supplying import-substituted cockpit glazing for the MC-21 program contrasts with Western programs that rely heavily on long-qualified ecosystems in North America and Europe. Disruptions at processing facilities can propagate quickly due to tight qualification windows, making dual-sourcing, regional stocking, and closer OEM-supplier planning central to lead-time control.

Competitive Landscape

The commercial aircraft windows and windshields market is moderately concentrated. PPG Industries Inc., Gentex Corporation, GKN Aerospace Services Ltd., and NORDAM Group LLC anchor the top tier with deep process know-how in transparent laminates and integrated shading systems. PPG posted double-digit organic aerospace growth and a USD 290 million backlog in 2024, signaling firm demand. GKN invests USD 55 million in a new San Diego repair hub to support global MRO flows. Gentex unveiled large-area dimmable panels that merge electrochromic layers with self-powered controllers at CES 2025, reinforcing its domain leadership.

Second-tier players differentiate through specialty resins, rapid autoclave cycles, or regional presence. Samyang’s PFAS-free polycarbonate targets exacting flame norms, while Vision Systems focuses on retrofit kits for business jets and narrowbodies. Material breakthroughs such as nanostitched composites could lower barriers for newcomers with cross-fertilization from automotive glazing. Competitive dynamics are shaped by intellectual property around coating chemistries and the ability to navigate certification funnels cost-effectively.

Tier-1 suppliers increasingly integrate vertical capabilities, from polymer synthesis to final assembly, to hedge against supply-chain shocks. Some experiments with additive manufacturing of spacer frames to cut lead times. Digital twins of windshield life-cycle performance inform airlines on optimal replacement scheduling, creating service revenue for vendors. The consolidation trend may accelerate as private equity sees stable cash flows tied to OEM backlogs and long-term MRO contracts.

Commercial Aircraft Windows And Windshields Industry Leaders

PPG Industries Inc.

GKN Aerospace Services Ltd.

Saint-Gobain Aerospace

Gentex Corporation

NORDAM Group LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated in technology upgrades that reduce cabin heat load and weight or add cockpit functionality, while still fitting FAA and EASA glazing requirements. Electrochromic architectures already demonstrated on large commercial platforms, such as Boeing widebody applications, support broader line-fit and retrofit discussions, and they pull through demand for transparent conductive coatings, robust interlayers, and reliability-focused test and inspection services.

A second whitespace area is multifunction glazing that combines display and sensing capability into transparent surfaces. In April 2026, ZEISS launched a micro-optical and holographic display technology platform for aerospace OEMs aimed at embedding digital data into transparent cabin and cockpit surfaces. That development increases demand for glazing suppliers that can support optical performance, anti-glare control, EMI management, and maintainability. At the same time, operator attention to compliance and in-service durability is tightening, including an Airbus May 2026 safety warning against attaching unapproved accessories to cockpit windows due to thermal-stress cracking risk. This raises demand for certified retrofit kits, approved mounting solutions, and improved maintenance practices for cockpit transparencies.

Recent Industry Developments

- June 2026: PPG Industries Inc. highlighted aerospace innovations across transparencies-related coatings and sealants during an Aerospace business deep dive and reinforced its focus on investing in innovation and capacity to support multi-year aerospace demand. The emphasis on customer productivity and throughput aligns with industry pressure to shorten lead times for qualified glazing stacks amid OEM backlogs and retrofit activity.

- September 2025: Saint-Gobain Aerospace renewed a long-standing exclusive distribution agreement with Satair covering cabin windows for Airbus and ATR aircraft, and expanded exclusivity for cockpit windows distribution in Asia Pacific, South Asia, and China. The renewal strengthens regional availability and simplifies aftermarket procurement for operators and MROs that need certified replacement transparencies on short notice.

- October 2024: Saint-Gobain Aerospace inaugurated a new cabin-window production line at its Saint-Jean-d’Illac site in Gironde, France, with stated capacity of 60,000 units per year dedicated to Airbus programs. The added line capacity supports higher-rate single-aisle output and increases resilience against intermittent shortages of qualified cabin-window assemblies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of windows and windshields used on commercial passenger aircraft, counted across new aircraft deliveries and ongoing replacement needs in service. Revenue is captured for transparency products supplied into certified commercial aircraft programs and their maintenance cycles.

Scope exclusions: military aircraft, business jets, helicopters, and UAV applications are excluded from the market boundary.

Segmentation Overview

- By Aircraft Type

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- Freighter/Converted Freighter Aircraft

- By Application

- Cabin Windows

- Cockpit Windshields

- By Material

- Glass Laminates

- Acrylic

- Polycarbonate

- Hybrid/Composite Sandwich Structures

- By Technology

- Conventional Multi-Layer Laminates

- Electrochromic/Dimmable Smart Windows

- Heated/Anti-Ice Windows

- UV and IR-Coated Windows

- By End Market

- OEM

- Aftermarket (MRO and Retrofit)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the commercial aircraft build and fleet picture, since windows and windshields follow aircraft output and in-service usage patterns. We referenced public aviation statistics and regulatory material, including FAA airworthiness and certification resources, EASA publications, ICAO air transport indicators, and IATA traffic and fleet commentary, to frame utilization and replacement intensity.

To translate that demand context into a value model, we also drew on customs and trade statistics, patent databases for material and coating trends, and peer reviewed aerospace materials journals for adoption timing of new transparency technologies. Company filings, investor presentations, association websites, and credible press were reviewed as well, and a paid subscription for company financials and news was used selectively to sanity-check revenue ranges and program exposures. These sources are illustrative, and other public references were also used for data collection, cross checking, and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with OEM and aftermarket participants, component specialists, and aviation MRO focused respondents. This helped tighten assumptions around fitment rates and replacement cycles. Coverage was balanced across major aircraft manufacturing and operating regions, and the questions were designed to confirm what drives orders, including fleet age mix, utilization levels, and maintenance triggers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 17% | APAC: 46% |

| Mid tier: 40% | Functional/Unit leaders: 29% | EMEA: 30% |

| Smaller Players: 21% | Managers: 54% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction that ties the addressable pool to commercial aircraft deliveries and the active fleet, then applies program level fitment and replacement behavior to arrive at annual unit needs. After shaping the demand pool, value was derived using average selling price bands for cockpit windshields and cabin windows. These were adjusted for aircraft type mix and for the split between line-fit and replacement demand.

To keep the model practical, we relied on inputs that can be refreshed each cycle, including commercial aircraft production and delivery trends, fleet in-service counts and utilization (flight hours and cycles), windshield replacement intervals driven by damage and maintenance checks, window count per aircraft type, and the adoption pace of higher value features such as coatings and heating layers. Selective bottom-up approximations were used as checks, including sampling supplier capacity signals, comparing implied unit volumes against deliveries, and using channel checks on typical pricing movement, which helps correct for gaps where public data is limited.

For forecasting, we used scenario analysis around aircraft delivery ramps, traffic recovery, and maintenance activity. Replacement driven demand was then smoothed to avoid overreacting to single-year delivery spikes. Assumptions showing wide variance in interviews, such as replacement timing under different utilization profiles, were treated as ranges and reconciled before the final forecast line was set.

Data Validation & Update Cycle

Validation is handled through multiple checks, starting with consistency tests between implied units, aircraft deliveries, and in-service fleet signals, then followed by reasonableness checks on pricing and mix. When an outlier appears, the related assumptions are revisited, and targeted re-contacts are triggered to confirm whether the change reflects a real market shift or a modeling artifact.

Before sign-off, the model and narrative are reviewed in steps by analysts to reduce logic breaks and ensure definitions are applied consistently across years and regions. Reports are refreshed annually, with interim updates when material events occur, and a fresh final pass is completed right before delivery so clients get the latest view.

Mordor Intelligence's Commercial Aircraft Windows and Windshields Market Size Measured Against Other Published Estimates

Published market sizes for commercial aircraft windows and windshields can differ even when the product sounds the same, because the study boundary and the baseline year are not always aligned. Variations also come from how line-fit demand is combined with aftermarket replacement, and whether the sizing is anchored to aircraft production signals or to broader aerospace spending proxies.

Replacement cadence linked to flight cycles, aircraft delivery counts, and the OEM versus aftermarket split are the evidence points that keep Mordor Intelligence's estimate aligned to certified commercial passenger aircraft demand, rather than to wider aircraft coverage or a looser revenue proxy. When these drivers are treated differently, gaps show up quickly, especially in years where deliveries and maintenance intensity move in opposite directions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 665.18 M (2026) | |

| Trade Publisher A | USD 576.00 M (2024) | Uses a different base year and frames the market around a 2024 baseline with a separate CAGR period, which shifts the value even if the long-run endpoint is similar. The mix across aircraft categories and pricing bands is not clearly tied back to delivery and replacement drivers in the summary view. |

| Industry News Release B | USD 685.50 M (2024) | Covers aircraft windows and windshields more broadly, which can pull in non-commercial aircraft demand depending on how the scope is applied. The estimate also reflects a different timing for currency and pricing assumptions, which can lift the stated value for the same calendar year. |

Across the three figures, the spread is mainly explained by base-year selection and whether the demand pool is restricted to commercial passenger aircraft with defined delivery and replacement drivers. By keeping the steps traceable to fleet, utilization, and replacement logic, the final number stays easier to reproduce and to update when deliveries or maintenance behavior changes.

Key Questions Answered in the Report

What is the current size of the commercial aircraft windows & windshields market?

The market stands at USD 665.18 million in 2026 and is projected to reach USD 781.45 million by 2031, registering a 3.28% CAGR.

Which aircraft segment drives the highest demand for windows and windshields?

Narrowbody jets dominate with 61.78% market share in 2025, supported by strong A320neo and B737 MAX orderbooks.

Why are electrochromic windows growing so quickly?

Airlines adopt dimmable panes to enhance passenger comfort and reduce cabin heat load, yielding a 7.72% CAGR for the technology segment.

How does material choice impact fuel efficiency?

Polycarbonate panes weigh up to 40% less than glass, cutting fuel burn and driving a 6.75% CAGR for the material segment.

What regions offer the strongest growth prospects?

Asia-Pacific leads with a 7.75% CAGR thanks to fleet expansion in India, China, and Southeast Asia.

Page last updated on: