Commercial Aircraft Lavatory System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

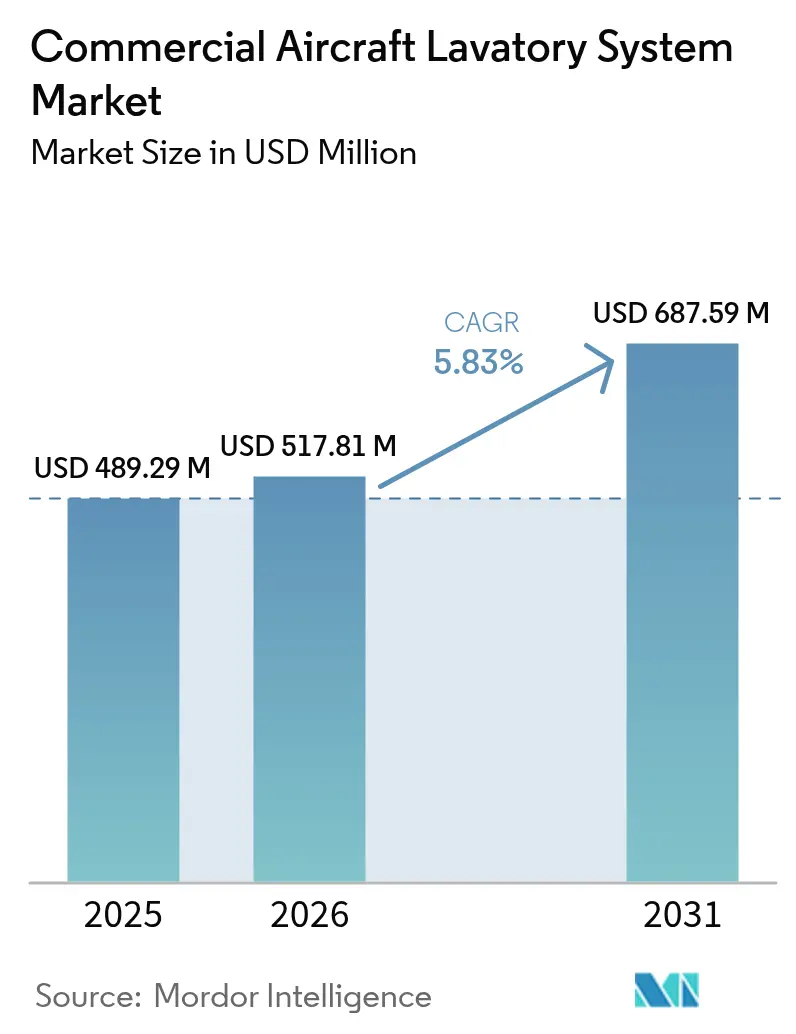

| Market Size (2026) | USD 517.81 Million |

| Market Size (2031) | USD 687.59 Million |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Lavatory System Market Analysis by Mordor Intelligence

The commercial aircraft lavatory system market size is expected to grow from USD 489.29 million in 2025 to USD 517.81 million in 2026 and is forecast to reach USD 687.59 million by 2031 at 5.83% CAGR over 2026-2031. Steady backlogs for single-aisle programs, airline demand for hygiene upgrades, and new mandates for accessibility are expected to propel near-term growth. Touchless fixtures move from niche to mainstream as fleet operators target reduced maintenance and faster turnarounds. Cabin densification pressures designers to deliver lighter, slimmer modules without compromising functionality. Retrofit opportunities expand because airlines favor extending asset life while meeting rules for passengers with reduced mobility. Supply-chain bottlenecks and certification timelines are the primary headwinds, yet tier-one suppliers continue to secure long-term contracts that lock in pricing and technology roadmaps.

Key Report Takeaways

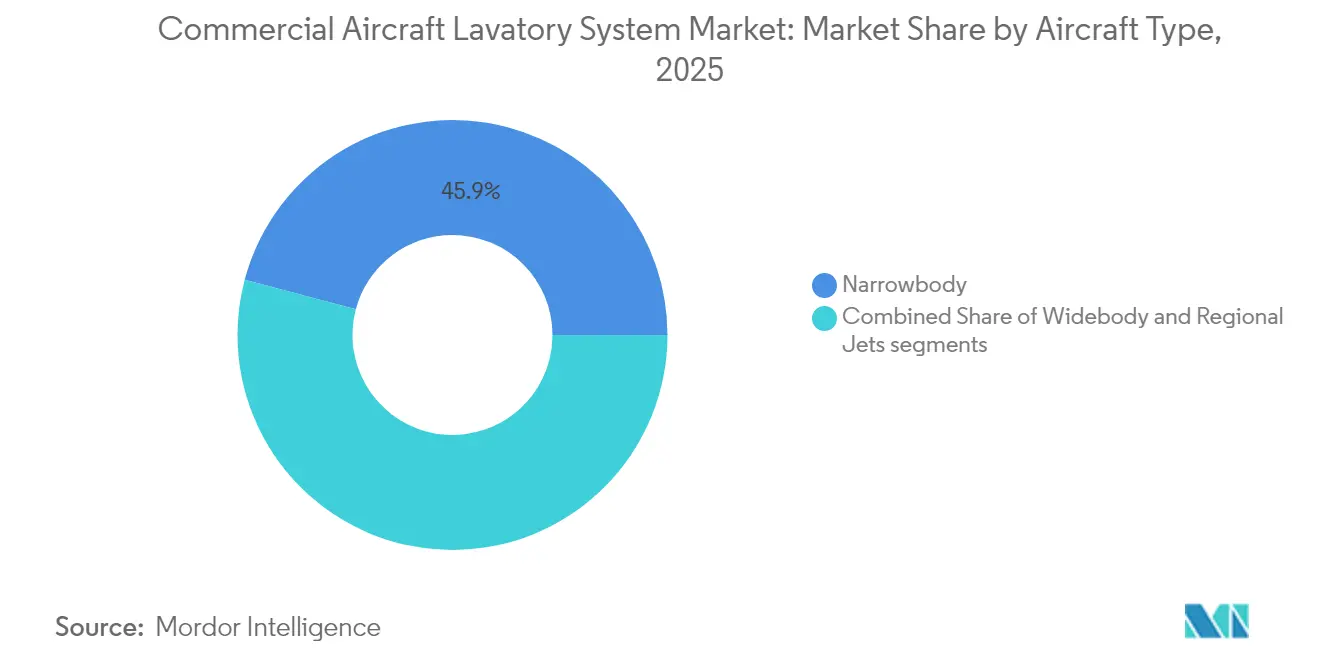

- By aircraft type, narrowbody platforms led with 45.87% revenue share in 2025, while regional jets posted the fastest projected 6.86% CAGR to 2031.

- By lavatory technology, vacuum systems held an 82.31% share in 2025, whereas hybrid solutions are forecasted to climb at a 7.39% CAGR through 2031.

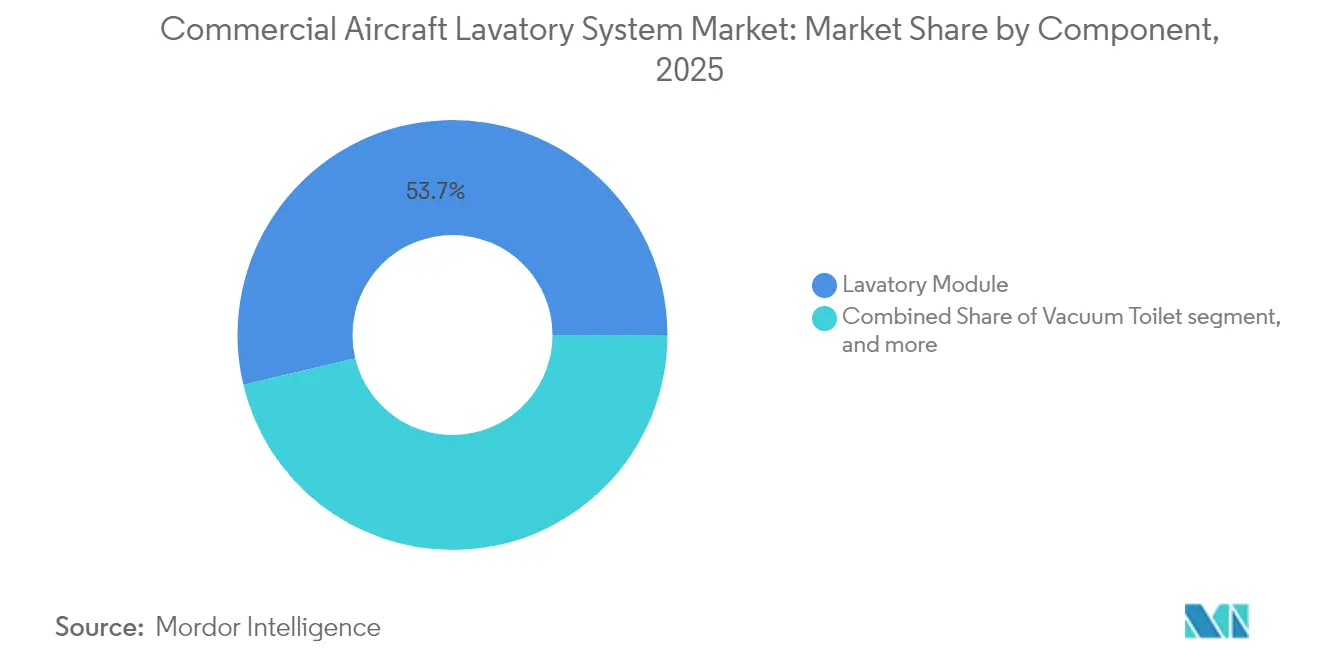

- By component, lavatory modules commanded a 53.72% share in 2025, while sinks, faucets, and accessories are set to expand at a 6.35% CAGR to 2031.

- By fit type, linefit installations accounted for 62.64% of the commercial aircraft lavatory system market share in 2025, while retrofit activities are projected to advance at a 7.05% CAGR through 2031.

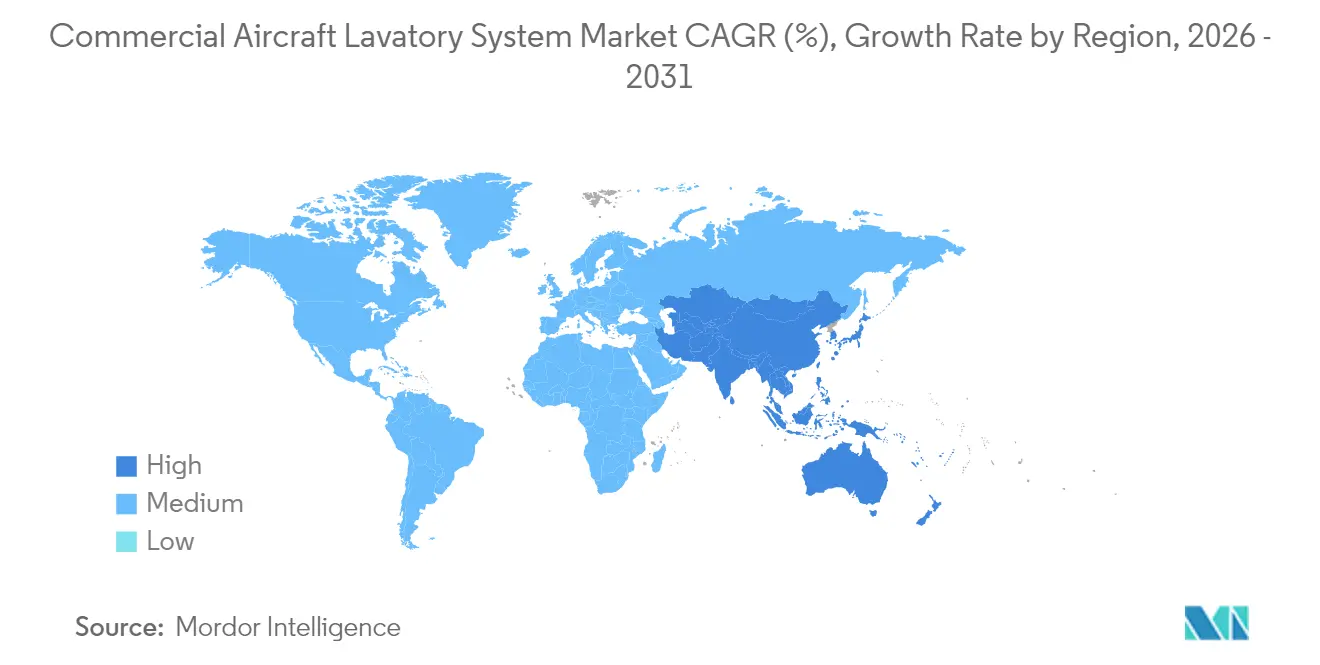

- By geography, North America contributed 33.55% of the revenue in 2025, whereas the Asia-Pacific region is on track for a 6.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Lavatory System Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased airline adoption of touchless lavatory technologies | +1.2% | Global, early uptake in North America and Europe | Short term (≤ 2 years) |

| Sustained growth in single-aisle aircraft deliveries over the long term | +0.8% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Rising demand for lavatory retrofits to support Person-with-Reduced-Mobility (PRM) accessibility standards | +0.6% | North America and EU | Medium term (2-4 years) |

| Cabin densification trends driving demand for space-efficient lavatory designs | +0.4% | Global high-density routes | Medium term (2-4 years) |

| Mandates promoting water-efficient vacuum toilet technologies | +0.3% | EU and North America | Long term (≥ 4 years) |

| Industry shift toward circular economy with recyclable lavatory module designs | +0.2% | Led by EU, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Airline Adoption of Touchless Lavatory Technologies

Airlines accelerated trials of sensor-based faucets, flush actuators, and waste lids after 2020, and most tier-one carriers now require touch-free options on all new deliveries. Collins Aerospace will begin shipping fully modular, touchless units for the B737 program in early 2025, providing operators with a catalog solution that reduces retrofit downtime.[1]Collins Aerospace, “Boeing Selects Collins as Next-Generation Lavatory Supplier,” collinsaerospace.com JAMCO Corporation holds the majority of wide-body lavatories and embeds contactless fixtures across B777 and B787 lines. Airlines perceive added value in lower cleaning cycles and fewer unserviceable events, which feed directly into on-time performance metrics. OEMs report that kits integrating micro-LED mood lighting and antimicrobial finishes command price premiums yet face minimal resistance from buyers. Certification pathways for sensor assemblies are established, so near-term barriers are primarily related to supply logistics rather than regulatory issues.

Sustained Growth in Single-Aisle Aircraft Deliveries Over the Long Term

Boeing delivered 348 airplanes in 2024, and Airbus shipped 766 units, filling order books that now extend over a decade in some variants.[2] Airbus, “Airbus Reports 766 Commercial Aircraft Deliveries in 2024,” aircraft.airbus.com Lavatory system vendors, therefore, enjoy multi-year production visibility that supports tooling investment. Single-aisle jets increasingly cover 1,500-3,000-mile sectors, and higher time-in-seat drives passenger demand for larger facilities. Embraer’s 20-year outlook predicts 10,500 sub-150-seat deliveries, which broadens the addressable fleet for compact lavatory modules. Sustained throughput appears resilient to temporary supply chain friction as airlines pay escalated prices to secure slots.

Rising Demand for Lavatory Retrofits to Support PRM Accessibility Standards

The US Department of Transportation (DoT) requires an accessible lavatory on every new single-aisle aircraft with 125 or more seats delivered after October 2026. European Regulation 1107/2006 enforces parallel guidelines for carriers operating within the European Union. Diehl’s Space³ concept, which widens the doorway to 36 inches, exemplifies modular designs that enlarge the compartment only when needed. Airlines favor retrofit kits that maintain seat count, using plug-and-play door mechanisms and collapsible partitions. Demand is strongest in North America, where rule enforcement dates are imminent, yet EU carriers are rapidly aligning to avoid patchwork fleets.

Cabin Densification Trends Driving Demand for Space-Efficient Lavatory Designs

Low-cost operators push seat counts to the structural limit, as demonstrated by the 197-seat B737 MAX 200 layout. Airbus answered with Smart Lav for the A320 family, which relocates systems to reclaim floor area. Lavatory suppliers now ship ultra-slim shrouds, lighter toilet bowls, and shared wall plumbing fixtures that meet the 95th percentile male occupancy envelope. A 25-pound weight savings per aircraft translates into fuel advantages that airlines quantify in route bids. The densification strategy is most acute on short-haul routes, and vendors optimize installation speed to align with 40-minute turnarounds.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weight constraints limiting the integration of advanced lavatory features | −0.5% | Global | Short term (≤ 2 years) |

| Certification delays for next-generation antimicrobial and hygiene materials | −0.4% | Global | Medium term (2-4 years) |

| Capital expenditure delays by airlines due to macroeconomic uncertainty | −0.3% | Emerging markets | Short term (≤ 2 years) |

| Onboard potable water limitations affecting ultra-long-haul lavatory operations | −0.2% | Worldwide long-haul routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Weight Constraints Limiting the Integration of Advanced Lavatory Features

Fuel burn increases by about 0.3% for every 100 pounds carried on short-haul sectors, allowing weight penalties to offset the economic benefits of upgraded interiors. Airlines frequently adopt water load planning to cut 440 lbs tied to overfilling tanks, but this strategy sets a hard ceiling on new feature mass. Collins Aerospace’s Agile vacuum unit trims structural weight by 50% without sacrificing reliability across 30 million flight hours. Boeing’s recycled carbon panels shave 25 lbs per 737 shipset yet involve complex lay-up processes that constrain output.

Certification Delays for Next-Generation Antimicrobial and Hygiene Materials

New ISO 7581:2023 protocols require dry-state efficacy testing, extending validation timelines for embedded biocides. The FAA also proposes performance-based fire rules that add another layer of test permutations. Recaro predicts approval for recycled foams no earlier than late 2024, illustrating typical delay horizons. With uncertainty surrounding certification costs and timing, airlines are postponing orders for touchless ultraviolet lighting and self-cleaning coatings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbody Dominance Drives Market Momentum

Narrowbody aircraft controlled 45.87% of the commercial aircraft lavatory system market share in 2025, a lead from record A320 and 737 output and rising use on routes exceeding 3,000 miles. Regional jets provide the highest 6.86% CAGR because carriers deploy sub-150-seat equipment to match fluctuating demand while preserving schedule frequency. The commercial aircraft lavatory system market size for narrowbody platforms is projected to grow consistently through 2031 as backlog conversion accelerates.

Growth factors differ across segments. Single-aisle types feature slimmer wall structures, which require lavatory modules that fit snugly within the tighter fuselage contours. Collins Aerospace’s linefit agreement for the B737 family secures forward commitment through 2034. Widebody fleets concentrate on retrofit because cabin refresh cycles align with heavy checks around year 8. JAMCO leverages its exclusive positions on the B787 and B777 to test new bidet functions that could be migrated into single-aisle models later in the decade. Regional OEMs are increasingly adopting standard part numbers that enable cross-family stocking, thereby lowering operator inventory.

By Lavatory Technology: Vacuum Systems Lead Innovation Wave

Vacuum solutions contributed 82.31% revenue in 2025, confirming their status as the default selection for most new builds. Airlines favor these systems because they use 80% less water, thereby reducing block fuel burn and maintenance costs. Hybrid architectures are expected to expand at a 7.39% CAGR as airlines trial Diehl’s greywater reuse module, which redirects hand-wash drainage for flushing, resulting in a 210 kg reduction on long-haul rotations. Prototype data indicate a payback period of 18 months for twin-aisle fleets.

The commercial aircraft lavatory system market continues to see R&D efforts focused on improving pump efficiency and controlling odors. Collins Aerospace’s Agile platform records a 50% weight reduction compared with legacy bowls while maintaining 30 million flight hours of reliability. Competitive responses include modular ejector pumps that share parts across biz-jet and commercial lines, lowering cost. Recirculating technology holds a small share for niche operators needing increased flush counts on very short segments where water uplift is less critical.

By Component: Lavatory Modules Drive Integration Trends

Lavatory modules accounted for 53.72% of 2025 revenue, as OEMs and airlines prefer one-piece monuments that expedite assembly. The commercial aircraft lavatory system market size associated with modules is expected to rise as widebody upgrades line up for 2026 dock slots. Growth in sinks, faucets, and accessories at a 6.35% CAGR reflects heightened hygiene expectations that emerged during the pandemic. Touchless spigots, sensor-operated soap dispensers, and anti-splash basins are among the most recent additions to linefit specifications.

Component vendors underscore interchangeability. Airbus selected standardized plumbing harnesses on the A350 retrofit program, reducing installation hours by 30%. JAMCO integrates LED mood lighting into faucets, raising perceived cabin quality without adding bulk. Modular fasteners allow technicians to swap bowls in under one hour, a vital metric for low-cost carriers operating tight schedules.

By Fit Type: Retrofit Growth Accelerates Fleet Modernization

Linefit installations accounted for 62.64% of 2025 revenue and are expected to remain dominant, thanks to a guaranteed backlog conversion at Airbus and Boeing. However, retrofits will advance at 7.05% CAGR through 2031 because airlines cannot wait for new slots and must comply with accessibility mandates on current hulls. Safran’s Aircraft Interiors division posted 25.2% sales growth in 2024, mostly from retrofit service orders that bundled lavatory, galley, and seat upgrades.

Retrofit kits prioritize minimal downtime. Collins produces a B737 Advanced Lavatory package that ships as a single crate with pre-wired electrical and data looms, enabling overnight hangar swaps. Airlines target annualized returns through ancillary revenue such as premium-economy upgrades linked to improved cabin ambiance. A robust PMA ecosystem further reduces costs by authorizing third-party parts that meet the exact specifications.

Geography Analysis

North America generated 33.55% of the revenue in 2025, following the acceleration of fleet standardization programs by carriers that integrate touchless fixtures and meet future accessibility deadlines. The commercial aircraft lavatory system market benefits from Boeing’s domestic manufacturing base and a dense MRO network that supports rapid retrofit execution. New US regulations promote technology adoption, ensuring that replacement cycles remain brisk even during periods of macroeconomic volatility.

The Asia-Pacific region exhibits the highest 6.74% CAGR outlook, as regional traffic rebounds to pre-2020 levels and carriers like IndiGo, AirAsia, and China Eastern firm orders for hundreds of single-aisle units. Mixed-fleet strategies couple narrowbodies with regional jets, expanding the installed base for compact lavatory solutions. Domestic suppliers emerge in China, yet quality benchmarks keep Western vendors active through joint ventures. Nations like India establish soft rules that encourage accessible cabin designs, thereby reinforcing the retrofit potential across older fleets.

Europe’s share remains sizable, underpinned by robust environmental regulations and incentives for a circular economy. EU operators are leading trials of recyclable flax composites, which align with upcoming disclosure requirements under the Corporate Sustainability Reporting Directive. The Middle East registers double-digit twin-aisle orders that favor premium lavatory monuments with custom finishes. Africa experiences sporadic growth tied to fleet renewals by Ethiopian Airlines and others, yet limited MRO capacity moderates the velocity of retrofits.

Competitive Landscape

The commercial aircraft lavatory system market exhibits moderate consolidation, with RTX Corporation, Safran Group, and JAMCO Corporation collectively accounting for the majority of the market revenue. Collins Aerospace, a part of RTX Corporation, leverages vertically integrated vacuum pumps, module structures, and aftermarket services to anchor supplier positions at Boeing and Airbus lines. Safran records a 25.2% expansion in interior revenue in 2024 by bundling galleys and lavatories, creating package deals that are attractive to full-service carriers.[4]Safran, “Safran Reports Full-Year 2024 Results,” safran-group.com JAMCO Corporation secures a 50% widebody share through sole-source deals on the B787 and B777 programs, ensuring steady retrofit demand when first-generation Dreamliners enter heavy maintenance checks.

Second-tier firms, such as Diehl Stiftung & Co. KG and Lufthansa Technik AG, compete on niche features, including greywater reuse, antibacterial coatings, and lightweight composites. Regulatory certification intensifies barriers to entry, and the lengthy approval processes of the FAA and EASA discourage smaller contenders. PMA parts introduce cost competition, mainly in consumables such as valves or seats, rather than full monuments.

Supply chain disruptions persist. Natixis reports that lead times are extending to 30 months for specific avionics and composite materials, forcing airlines to pre-purchase spares. Vendors with diversified sourcing across Asia and Europe mitigate delays and capture incremental market share. Strategic actions include Safran’s acquisition of electromechanical actuation assets from Woodward, enhancing vertical control over water and waste actuators.

Commercial Aircraft Lavatory System Industry Leaders

Safran Group

JAMCO Corporation

Diehl Stiftung & Co. KG

Geven SpA

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Deutsche Aircraft and Satys Cabin signed an agreement to supply lavatory assemblies for the D328eco aircraft.

- April 2024: Jamco Corporation unveiled a next-generation lavatory to address accessibility challenges for PRMs.

Global Commercial Aircraft Lavatory System Market Report Scope

An aircraft lavatory system, often called an aircraft restroom or airplane toilet, is a specialized onboard facility for passengers and crew members to relieve themselves during a flight. These lavatory systems are compact and equipped with fixtures such as toilets, sinks, and amenities to ensure hygiene and convenience within the limited space available on commercial aircraft. They play a crucial role in enhancing the overall in-flight experience for passengers and are subject to strict regulatory standards to maintain safety and sanitation in aviation.

The commercial aircraft lavatory system market is segmented by aircraft type and geography. Based on the aircraft type, the market is segmented into narrow-body, wide-body, and regional jets. The report also covers the market sizes and forecasts for the commercial aircraft lavatory system market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Narrowbody |

| Widebody |

| Regional Jets |

| Vacuum |

| Recirculating |

| Hybrid/Others |

| Lavatory Module |

| Vacuum Toilet |

| Water and Waste Management System |

| Sinks, Faucets, and Accessories |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| By Lavatory Technology | Vacuum | ||

| Recirculating | |||

| Hybrid/Others | |||

| By Component | Lavatory Module | ||

| Vacuum Toilet | |||

| Water and Waste Management System | |||

| Sinks, Faucets, and Accessories | |||

| By Fit Type | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the commercial aircraft lavatory system market?

The commercial aircraft lavatory system market size is USD 517.81 million in 2026.

How fast will demand grow through 2031?

Forecasts indicate a 5.83% CAGR, reaching USD 687.59 million by 2031.

Which aircraft type currently generates the most lavatory system revenue?

Narrowbody platforms lead with 45.87% share in 2025.

Why are retrofit programs accelerating now?

Airlines must comply with new accessibility mandates and favor shorter ground times, making quick-install retrofit kits attractive.

Which region is expected to post the highest growth rate?

Asia-Pacific, projected at a 6.74% CAGR through 2031 due to large order backlogs and fleet expansions.

Who are the key suppliers dominating this space?

Collins Aerospace (RTX Corporation), Safran, and JAMCO Corporation collectively capture more than half of total revenue.

Page last updated on: