Military Aviation Maintenance, Repair, And Overhaul Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 45.75 Billion |

| Market Size (2031) | USD 51.75 Billion |

| Growth Rate (2026 - 2031) | 2.50% CAGR |

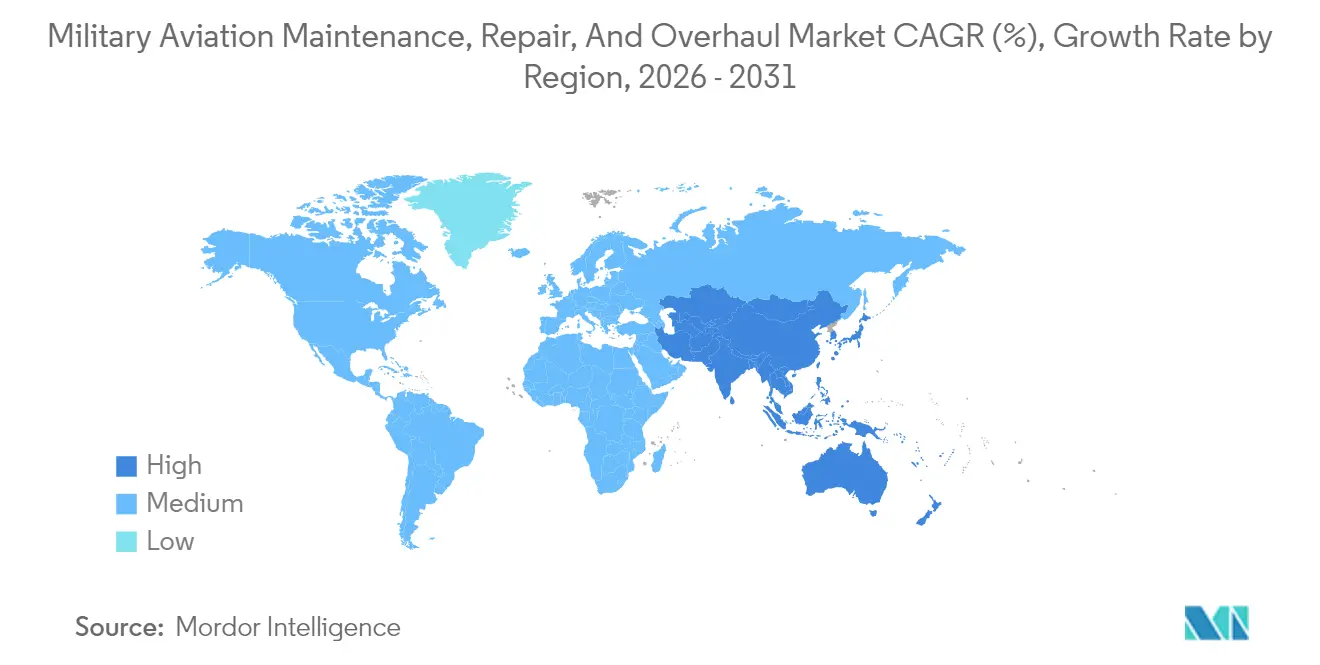

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

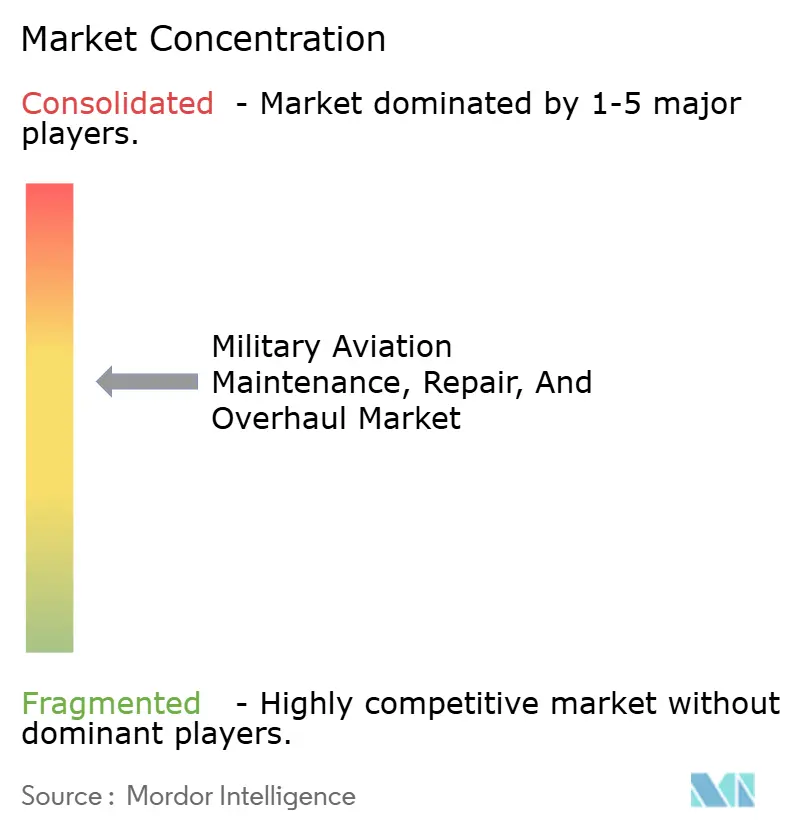

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Aviation Maintenance, Repair, And Overhaul Market Analysis by Mordor Intelligence

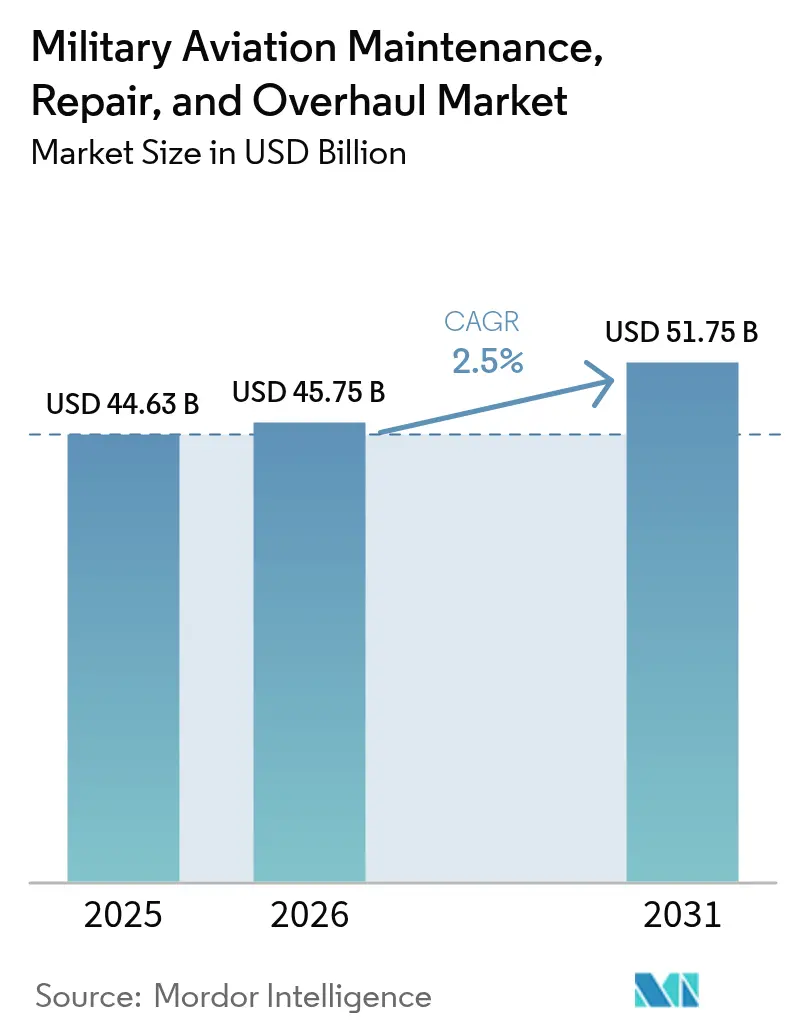

The military aviation MRO market size in 2026 is estimated at USD 45.75 billion, growing from 2025 value of USD 44.63 billion with 2031 projections showing USD 51.75 billion, growing at 2.5% CAGR over 2026-2031. This measured expansion reflects a mature yet indispensable sector reshaped by aging fleets, fleet-life extension initiatives, and heightened geopolitical tensions.[1]Source: SIPRI, “World military expenditure reaches new record high,” sipri.org Accelerated modernization programs for legacy aircraft, sustained investment in digital twin technology, and the proliferation of unmanned platforms are altering maintenance requirements and opening new provider revenue opportunities. Meanwhile, persistent supply-chain fragility and a looming skilled-labor shortage threaten to constrain capacity, pushing operators to adopt predictive maintenance and performance-based logistics (PBL) to maintain readiness at lower cost. These structural shifts underpin a gradual move toward outsourced services, with independent providers gaining traction as defense ministries seek cost efficiency without compromising security. Together, these dynamics reinforce a steady outlook for the military aviation MRO market through the decade's end.

Key Report Takeaways

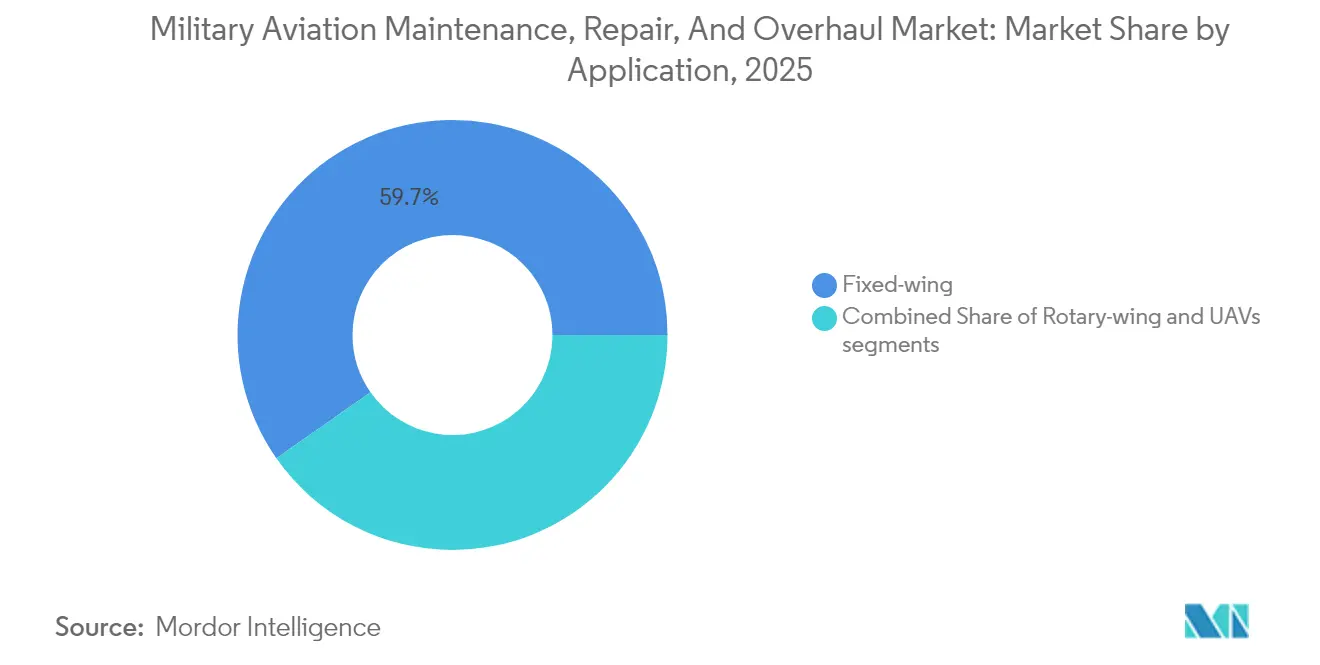

- By application, fixed-wing aircraft held 59.72% of the military aviation MRO market share in 2025, while unmanned aerial vehicles (UAVs) are forecasted to grow at a 6.58% CAGR through 2031.

- By MRO type, engine overhaul commanded a 42.12% share of the military aviation MRO market in 2025, whereas component repair and overhaul are advancing at a 3.39% CAGR to 2031.

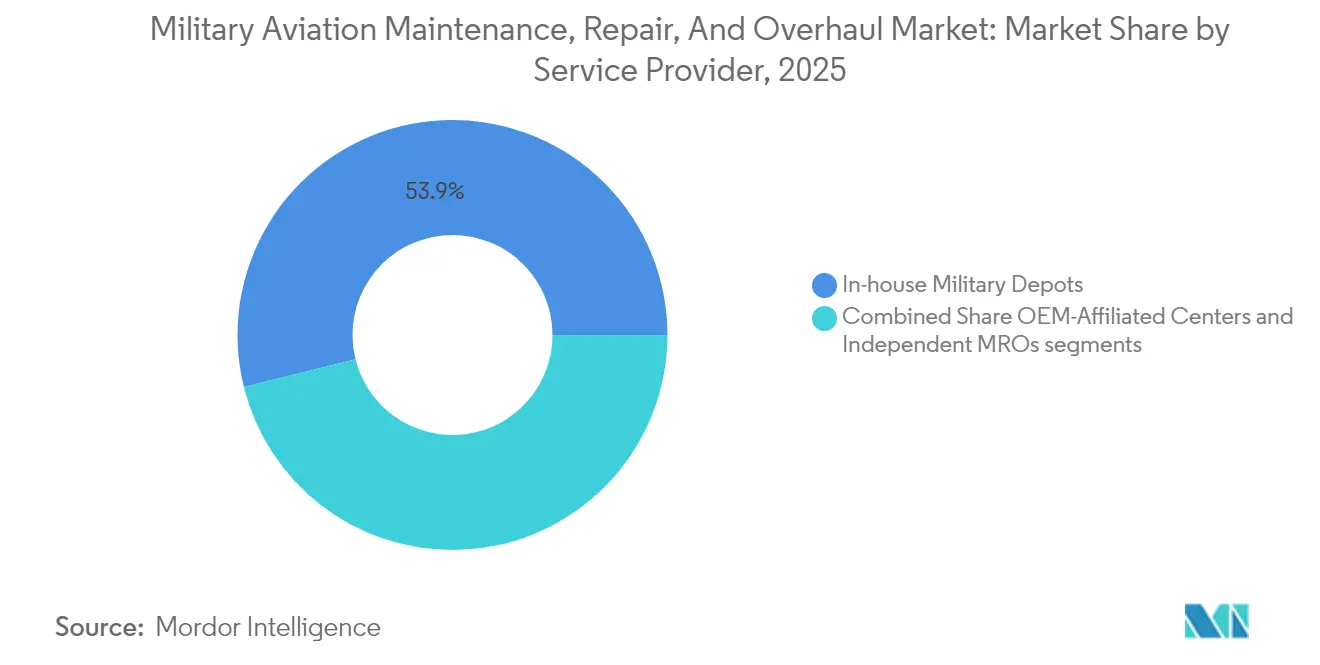

- By service provider, in-house military depots retained a 53.88% share in 2025; independent MROs record the fastest 4.08% CAGR through 2031.

- By end-user, the Air Force led with a 61.85% share in 2025, while Army Aviation is expanding at a 3.28% CAGR to 2031.

- By geography, North America held a 37.35% share in 2025, and Asia-Pacific is projected to rise at a 4.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Military Aviation Maintenance, Repair, And Overhaul Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fleet-life extension programs | +0.5% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Expansion of multinational readiness agreements | +0.4% | APAC core, spill-over to Europe and MEA | Medium term (2-4 years) |

| Growth in defense spending of emerging Asia-Pacific nations | +0.3% | Asia-Pacific, secondary effects in MEA | Medium term (2-4 years) |

| OEM digital-twin–enabled service packages | +0.2% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Increased rotorcraft usage for special operations | +0.1% | Global, concentrated in North America and APAC | Medium term (2-4 years) |

| Sustainability mandates driving engine retrofits | +0.2% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Fleet-Life Extension Programs Drive Sustained MRO Demand

Fleet-life extension initiatives are now the backbone of sustainment planning for legacy bombers, tankers, and fighters worldwide, reflecting a pragmatic strategy that blends fiscal prudence with readiness assurance. Operators view modernization contracts for platforms such as the B-52 and KC-135 as a hedge against the budget and schedule risk inherent in clean-sheet aircraft development.[2]Source: Harry McNeil, “Northrop Grumman lands $7bn contract for B-2 revamp,” Airforce-Technology, airforce-technology.com Extending service to 2050 obliges depots to perform deep structural remediation, corrosion mitigation, and mission-system upgrades that often surpass original manufacturing tolerances. Work scopes routinely include complete rewiring, composite panel replacement, and radar-absorbent-material refreshes to preserve low-observable performance. Such labor-intensive projects absorb skilled technicians for months, keeping hangars full even during procurement downturns. As modernization cascades through global fleets, specialized providers capable of managing obsolescence, parts reclamation, and digital records integration secure predictable, multi-year revenue streams that anchor overall MRO growth.

Multinational Defense Agreements Expand Interoperability Requirements

Allied readiness frameworks now mandate standard maintenance protocols, technical documentation, shared inventories, and reframing sustainment from an isolated national task to a collective security prerequisite. The F-35 global support solution, with regional hubs in Australia and Europe, shows how pooling heavy-maintenance events lowers per-flight-hour cost while guaranteeing surge capacity during crises.[3]Source: Paco Milhiet, “US Air Power in the Indo-Pacific Region,” Revue Défense Nationale, defnat.com Establishing common tooling and certification standards lets technicians traverse national lines without redundant training, accelerating turnaround times for coalition squadrons. Nonetheless, strict technology-transfer rules compel providers to balance openness with safeguarding sensitive data. Certification bodies must harmonize software-validation procedures so upgrades released by one country remain airworthy across partner fleets. For independent MROs, aligning cybersecurity, export-control compliance, and sovereign supply-chain preferences is becoming a competitive differentiator. The net result is a larger, more stable work package that depends on trust, transparency, and proven performance across multiple jurisdictions.

APAC Defense Spending Surge Accelerates Regional MRO Growth

Defense ministries across Asia-Pacific are channeling record budgets toward new airframes and the infrastructure needed to sustain them, rapidly maturing local MRO ecosystems. Japan’s 21% outlay jump funds indigenous depot upgrades, while India’s USD 2.34 billion MiG-29 overhaul joint venture anchors a broader initiative to attract high-value sustainment work. Governments offer tax concessions, bonded logistics zones, and streamlined customs rules to entice OEMs to establish forward repair centers that shorten parts pipelines by weeks. Apprenticeship programs with technical universities ensure a domestic technician pool, easing historical reliance on expatriate labor. Regional tensions around the South China Sea incentivize redundant capacity near potential flashpoints, promoting investments in hardened hangars and mobile diagnostic labs. Collectively, these policies reallocate global maintenance throughput eastward, challenging the traditional dominance enjoyed by North American and European depots and redefining competitive baselines for turnaround time and cost.

Digital Twin Technology Revolutionizes Predictive Maintenance

Pixel-perfect virtual replicas of aircraft merge sensor telemetry, historical maintenance logs, and mission profiles to forecast component degradation with high fidelity. Commanders gain a real-time view of fleet health, letting planners schedule interventions when performance trends signal impending failure, not when calendars dictate. Early adopters report double-digit gains in aircraft availability, a critical edge during high-tempo operations. Savings accrue from avoiding unnecessary teardowns and ordering parts only when predictive analytics trigger alerts, cutting inventory carrying costs. Digital twins also streamline airworthiness certification; software patches and configuration changes can be assessed virtually before line implementation, slashing ground time. Providers that master data cleansing, model training, and secure cloud hosting are poised to dominate new PBL contracts that tie compensation to measurable uptime rather than labor hours booked.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain fragility for defense-grade spares | -0.3% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Skilled-labor shortages at depot-level facilities | -0.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Budget-cycle unpredictability in Western Europe | -0.2% | Europe, secondary effects in allied nations | Medium term (2-4 years) |

| Export-control restrictions on critical avionics | -0.1% | Global, concentrated impact on international MRO | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerabilities Constrain MRO Capacity

Single-source suppliers and aging tooling create brittle supply networks where minor disruptions cascade into months-long aircraft on-ground incidents. Critical forgings for legacy engines may originate from only one qualified vendor, whose unexpected outage can immobilize entire fleets. Long lead times compel operators to stockpile rotables, yet warehouse expansions inflate overhead and capital locked in inventory. Export-license delays add unpredictability for multinational programs, especially when geopolitical tensions tighten licensing scrutiny. Depots explore additive manufacturing for non-flight-critical parts to counteract risk, though certification hurdles remain formidable. Digital traceability platforms are being introduced to monitor supplier health, flagging early signs of capacity shortfall. Until diversified sources, advanced forecasting, and additive solutions scale, supply-chain fragility will remain the most immediate brake on MRO throughput and revenue realization.

Workforce Shortages Threaten Maintenance Capacity

Retirements among baby-boomer technicians and a tepid inflow of certified graduates combine to stretch shop-floor staffing ratios to critical lows. Security-clearance prerequisites lengthen onboarding timelines, while modern avionics demand proficiency in fiber-optic terminations, software diagnostics, and composite repairs skills absent from many traditional A&P curricula. Competitive commercial aviation wages lure experienced mechanics away from military contracts, compounding shortages. Depots respond with accelerated apprenticeship pipelines, tuition-reimbursement packages, and augmented-reality work instructions that let junior staff perform tasks previously reserved for veterans. Remote technical assistance from OEM engineers further mitigates experience gaps but introduces cybersecurity and bandwidth concerns. Unless retention incentives, automation, and targeted training scale rapidly, personnel scarcity will cap hangar utilization rates and restrain the sector’s ability to capitalize fully on rising demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Evolving Platform Mix Shapes Demand Patterns

Fixed-wing fleets dominated 59.72% of the 2025 military aviation MRO market size owing to large inventories of combat and transport aircraft that require routine heavy checks and periodic avionics refreshes. UAVs, however, represent the fastest-growing segment with a 6.58% CAGR, reflecting strategic investments in swarm-enabled autonomy under the Pentagon’s Replicator initiative.

While fixed-wing platforms will maintain the largest maintenance workload, UAV growth forces providers to adapt to high-volume, rapid-turn processes distinct from depot-level overhauls. Rotary-wing demand remains stable, especially for special-operations-configured UH-60 and MH-47 variants that require classified hangar access and accelerated turnaround. The resulting platform mix calls for flexible capacity planning so providers can capture rising UAV volumes without jeopardizing legacy airframe support, sustaining a balanced expansion across the military aviation MRO market.

By MRO Type: Propulsion Dominates but Components Lead on Growth

Engine overhaul captured 42.12% of 2025 revenue, underscoring how propulsion systems account for the single largest maintenance spend and carry stringent performance and certification standards. Component repair and overhaul is projected to pace the field at a 3.39% CAGR, driven by digital-twin-informed diagnostics that lower inspection costs and enable targeted part replacements.

Airframe maintenance demand is steady as service-life extensions require structural reinforcement, corrosion control, and composite repairs. The shift limits line maintenance growth and military aviation MRO market penetration to condition-based scheduling, yet remains critical for forward-deployed readiness. Performance-based contracts continue to bundle multiple service types, allowing providers to leverage efficiencies across shop specialties and deepen military aviation MRO market penetration.

By Service Provider: Outsourcing Momentum Builds

In-house depots controlled 53.88% of 2025 revenue, reflecting the military's preference for organic capability and security. Nevertheless, independent MROs are set to expand at a 4.08% CAGR due to their competitive cost structures and niche expertise.

OEM-affiliated centers leverage proprietary data and parts access to offer turnkey support, but right-to-repair initiatives threaten to erode exclusivity and open the field. Depots are adopting commercial best practices and digital tools that raise productivity to stay relevant. This evolving mix of providers enriches the military aviation MRO market landscape and gives defense ministries more sourcing flexibility.

By End-User: Rotorcraft Operations Fuel Army Growth

The Air Force accounted for 61.85% of 2025 spending, upheld by high-value strategic bombers, air refuelers, and stealth fighters whose complex upkeep drives premium labor and parts requirements. Army Aviation, buoyed by increased rotorcraft deployments for special operations and multi-domain deterrence, is expected to grow at a 3.28% CAGR through 2031.

Naval Aviation maintains a stable share rooted in carrier-borne jets and maritime patrol aircraft that face harsh saltwater corrosion. Cross-service interoperability is also rising, enabling shared logistics hubs and joint procurement of spares that lower life-cycle cost. These dynamics enlarge the military aviation MRO market while encouraging standardized processes across end-user communities.

Geography Analysis

North America’s 37.35% share is rooted in the US’ inventory of more than 13,000 military aircraft, underpinned by large-scale contracts such as Boeing’s USD 2.3 billion C-17 sustainment award. However, chronic parts shortages and a looming technician retirement wave threaten to erode productivity, compelling service branches to accelerate digital-twin adoption and invest in workforce development. Canada’s partnership with L3Harris to establish an F-35 depot illustrates how allied cooperation reinforces continental readiness.

Asia-Pacific is the most dynamic arena, expanding at a 4.32% CAGR as regional powers respond to heightened geopolitical risk. Japan increased its 2024 defense budget by 21% to USD 55.3 billion, and India’s USD 2.34 billion MiG-29 upgrade venture demonstrates a deliberate pivot toward indigenous sustainment capability. China’s steady USD 314 billion allocation represents a substantial underlying driver even without direct market participation by Western contractors. These factors collectively elevate the region’s importance to the military aviation MRO market over the forecast horizon.

Europe sustains a mature yet opportunity-rich environment. The ReArm Europe initiative earmarks EUR 800 billion (USD 938.57 billion) for defense, yet implementation hinges on political alignment and supplier capacity. Recent moves, such as F-16 MRO capability expansion in Slovakia, signal the gradual decentralization of sustainment within NATO. Environmental regulations also compel European operators to embark on engine retrofit campaigns, extending mid-life platforms while advancing emission-reduction goals. These developments keep Europe relevant in the evolving military aviation MRO market, though actual growth may trail headline funding commitments.

Regulatory Landscape

In the United States, military aviation MRO is governed by service-level maintenance policy and Department of Defense sustainment directives that influence how work is divided between organic depots and commercial providers. DoDI 4151.24 (Depot Source of Repair Assignment Determination Process) sets the DSOR decision framework for new weapon systems. Naval Aviation Maintenance Program guidance (COMNAVAIRFORINST 4790.2, revised in 2024) establishes readiness and availability-related maintenance processes that flow down to fleet, intermediate, and depot activities.

In Europe, airworthiness and maintenance rules continue to converge through civil and military harmonization initiatives. Commission Regulation (EU) No 1321/2014 (as recast) and EASA updates such as ED Decision 2026/005/R provide the baseline for continuing airworthiness and acceptable means of compliance. The European Defence Agency MAWA Forum also maintains EMAR standards (including EMAR 145 and EMAR 21 updates during 2025), which participating defense authorities use to standardize military maintenance organization approvals and certification practices across allied fleets.

Value Chain Analysis

The military aviation MRO value chain begins with OEMs and design authorities (airframe and engine primes) that control technical data, configuration baselines, and many proprietary repair procedures, then extends to tier suppliers for engines, avionics, and rotables. Maintenance execution occurs through in-house military depots, OEM-affiliated centers, and independent MROs. Material flow typically runs from parts manufacturers and distributors into base and depot inventories, with repair loops returning serviceable rotables back into shared pools. Long-lead defense-grade spares and obsolescence management remain central constraints on throughput for both legacy platforms and modern mission systems.

Contracting and logistics structures shape how value is captured. Performance-based logistics and long-term sustainment awards increasingly bundle planning, supply-chain management, and maintenance execution, as shown in large fleet support packages such as the UK Ministry of Defence rotary-wing support award to Boeing Defence UK (879 million GBP, April 2026) and the French DMAe CAROLUS contract awarded to Sabena technics for the Franco-German C-130J/KC-130J fleet (10-year contract, January 2026). On the distribution and procurement side, mechanisms such as the April 2025 AAR and U.S. Defense Logistics Agency Aviation Supply Chain Alliance illustrate how centralized quoting and procurement execution are used to improve parts availability and reduce readiness-impacting delays.

Competitive Landscape

The military aviation MRO market displays moderate consolidation centered on aerospace primes that bundle manufacturing with long-term sustainment. Boeing, Lockheed Martin, and Northrop Grumman leverage proprietary data, global facilities, and vertically integrated supply chains to secure high-value, multi-year contracts such as Northrop’s USD 7 billion B-2 modernization package. Yet independent specialists like AAR demonstrate that focused expertise and lean cost structures can win niche awards, evidenced by its USD 1.2 billion P-8A engine deal.

Technology adoption is a key differentiator. Providers offering AI-enabled prognostics and digital twin analytics deliver double-digit availability gains, giving them a pricing and performance edge when bidding on availability-based contracts. Supply-chain resiliency initiatives, including dual-sourcing critical spares and additive manufacturing of low-volume parts, are gaining traction as operators attempt to mitigate lead-time volatility. Workforce development has also become strategic; firms partner with technical colleges and offer retention bonuses to secure scarce licensed mechanics.

Regulatory shifts, especially right-to-repair efforts, could rebalance power toward independent shops by mandating broader access to technical data. Meanwhile, the surge in unmanned systems opens white-space for agile entrants capable of servicing high-production-rate drones. The competitive environment intensifies as traditional incumbents defend their share while newcomers exploit technology and policy changes to penetrate the military aviation MRO market.

Military Aviation Maintenance, Repair, And Overhaul Industry Leaders

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

BAE Systems plc

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regionalization of heavy maintenance and component support is a visible whitespace as operators look to shorten logistics tails and expand coalition surge capacity, particularly for transport and special-mission fleets. 2026 signals include Indonesia's plan to develop Kertajati International Airport as a regional C-130 Hercules maintenance hub (May 2026), Malaysia's A400M MRO collaboration via an Airod-Airbus Defence and Space MoU (April 2026), and India's broader private-sector involvement in defense sustainment, including a GMR Aero Technic agreement with Boeing Defence India for P-8I heavy maintenance at Hyderabad (May 2026). These moves broaden the addressable market for independent and OEM-affiliated providers that can support certified facilities, secure data handling, and export-control-compliant workflows.

Opportunity also concentrates in data-enabled sustainment, multi-supplier repair networks, and capacity additions that directly address readiness bottlenecks. The U.S. Air Force KC-46 component repair and exchange awards, spread across 28 companies (June 2026), reflect a procurement pattern designed to diversify repair capacity and reduce single-point material risk. Branch-level planning documents such as the U.S. Marine Corps Aviation Sustainment Plan (2026) highlight demand-based sustainment and digital data-enabled systems for distributed operations. For providers, these trends support investments in predictive maintenance, secure digital-thread integration, and geographically distributed repair capability, alongside workforce development programs that increase induction rates at both depots and private shops.

Recent Industry Developments

- July 2026: RTX (Pratt & Whitney) acquired Amsterdam-based Aiir Innovations to integrate AI-assisted borescope inspection software across its global MRO operations. The acquisition supports engine inspection automation and standardizes diagnostic workflows that can reduce inspection variability and accelerate engine return-to-service across both military and commercial programs.

- April 2026: Lockheed Martin received a Pentagon award with a ceiling of up to USD 1.9 billion to continue the C-130J Maintenance and Aircrew Training System (MATS) program under a long-term IDIQ structure. By bundling sustainment and training system support, the award reinforces multi-year fleet readiness planning and provides a scaled support pathway for operators flying the C-130J.

- September 2024: Lockheed Martin and Tata Advanced Systems announced an agreement to expand C-130J Super Hercules opportunities in India, extending industrial collaboration around the platform. The partnership supports localization of sustainment-related capability and strengthens the regional basis for transport aircraft support as Indian fleet utilization increases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of maintenance, repair, overhaul, and modification work that keeps military aircraft mission-ready, including scheduled inspections and corrective fixes across airframes, engines, and onboard systems. Sizing is captured in USD for the global market, then cross-validated using regional activity patterns.

Scope exclusions: Excludes new aircraft procurement and one-time manufacturing sales that are not tied to in-service MRO work packages.

Segmentation Overview

- By Application

- Fixed-wing

- Combat Aircraft

- Transport and Tanker Aircraft

- Special Mission Aircraft

- Others

- Rotary-wing

- Utility/Transport Helicopters

- Attack Helicopters

- Unmanned Aerial Vehicles (UAVs)

- Fixed-wing

- By MRO Type

- Engine Overhaul

- Airframe Maintenance

- Component Repair and Overhaul

- Line Maintenance

- By Service Provider

- OEM-Affiliated Centers

- Independent MROs

- In-house Military Depots

- By End-User

- Air Force

- Naval Aviation

- Army Aviation

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- Israel

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work begins by mapping the fleet and sustainment context, so the model is anchored to what is actually operated and funded. We use public defense budget documents, national audit office reports, and readiness-related publications where available to understand how MRO demand behaves over time.

For cross-checks, we refer to reputable public sources such as Stockholm International Peace Research Institute defense spending series, World Bank macro indicators (inflation and exchange rates), OECD macro series, national statistical agencies, and defense ministry procurement portals that publish contract notices and program updates. We also review company annual reports, investor presentations, and airworthiness and maintenance guidance published by civil and military authorities (kept here mainly as terminology references), along with peer-reviewed aerospace sustainment papers. Paid subscriptions are used selectively for company financials and news screening, plus aerospace and aviation databases that help validate platform inventories and modernization timelines. The sources listed here are illustrative only, and many other public documents and references were used for collection and cross-checking.

Primary Interviews and Surveys

Primary inputs come from expert interviews and structured surveys with MRO providers, component repair specialists, depot-level maintenance stakeholders, and program-side experts who track sustainment plans. These discussions confirm utilization patterns, the typical induction intervals for heavy maintenance, modernization and modification timing, and what work is contracted out versus retained in-house. We then apply region-level checks across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | APAC: 39% |

| Mid tier: 59% | Functional/Unit leaders: 30% | EMEA: 35% |

| Smaller Players: 14% | Managers: 56% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing is built using a top-down and bottom-up approach. Defense sustainment spend, active fleet counts, and maintenance intensity are used to reconstruct the yearly demand pool for military aviation MRO. After the demand pool is formed, it is split across major work scopes such as engine overhaul, airframe maintenance, component repairs and modifications, and field maintenance, then cross-checked against platform mix and regional operating patterns.

To keep the model practical, we treat a few market fingerprints as key inputs. These include active aircraft inventory by type (fixed-wing, rotary-wing, and UAVs), average annual flight hours or mission tempo proxies, planned depot induction cycles, major upgrade and modification timelines, and parts replacement intensity for high-wear systems. Where public data is thin, we use interview-led ranges and then narrow them using known budget ceilings and observed maintenance cadence.

Forecasting is done mainly through scenario analysis tied to fleet modernization schedules, readiness targets, and expected budget direction. The scenarios are then tested with selective bottom-up approximations. These checks include sampled cost-per-induction logic for engines and airframes, simple volume times average service value for common work packages, and channel checks on aftermarket parts flow, which helps avoid overstating spend in years with fewer shop visits.

Data Validation & Update Cycle

Validation is done by triangulating model outputs against independent signals such as defense budget line items, fleet size changes, depot capacity signals, and known upgrade schedules, and then tracking any variance that does not fit the operating narrative. If an outlier appears, we re-check currency timing, inflation assumptions, and whether a large multi-year sustainment award has been treated as annualized or booked in a single year.

Before sign-off, outputs go through multiple analyst review passes so aircraft counts, maintenance intensity, and regional splits stay consistent with the stated assumptions. Reports refresh annually, and interim updates are made when a material event shifts demand, such as a major readiness push, fleet grounding, or a large modernization program. Right before delivery, an analyst performs a fresh pass of recent public releases so clients receive the latest updated view.

Mordor Intelligence's Military Aviation Maintenance Repair and Overhaul Market Size Compared Against Other Published Estimates

Published market sizes for military aviation MRO can look far apart even when they appear to cover similar services, because the service basket and counting rules are rarely identical. Differences usually come from what aircraft are included, whether depot work is treated as a service market, and how multi-year sustainment awards are converted into annual values.

New aircraft production spares and initial provisioning are often bundled into broader defense aerospace spend, and they sit outside Mordor Intelligence's scope because only in-service maintenance, repair, overhaul, and modification work packages are counted. Some estimates also expand totals by treating wide sustainment demand as fully addressable MRO, while others compress the number by using conservative utilization and overhaul cycle assumptions. Currency conversion timing and refresh cadence can add another layer, especially when budget revisions and readiness shifts happen mid-year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 45.75 B (2026) | |

| Global Consultancy A | USD 131.40 B (2025) | Uses a broader military aircraft MRO framing that can scale up totals by blending a wider set of platforms and sustainment categories, and it may reflect demand-style totals rather than a tighter MRO service-only view. |

| Industry Publisher B | USD 42.95 B (2025) | Uses an earlier base year and a different forecast window, and it may apply conservative assumptions on utilization and induction timing, which can reduce the annualized value even if long-term growth is similar. |

Looking across the figures, the spread is mainly explained by scope additions into procurement-adjacent spend and by how annual values are normalized from multi-year programs. Our checks around fleet activity, depot cadence, and budget realism keep the total traceable to clear drivers, and that makes it easier to repeat the sizing when inputs change.

Key Questions Answered in the Report

What is the current global value of military aviation MRO spending?

Global defense organizations are projected to spend USD 45.75 billion on MRO activities in 2026.

How fast is unmanned aerial vehicle maintenance demand growing?

UAV sustainment requirements are expanding at a 6.58% CAGR through 2031, the fastest rate among all platform types.

Which region is expected to see the highest growth in military aviation MRO by 2031?

Asia-Pacific leads with a projected 4.32% CAGR as rising defense budgets and new facilities shift workshare eastward.

Why are life-extension programs critical for defense aviation budgets?

Extending aircraft like the B-52 and KC-135 costs far less than new procurement, yet drives steady depot demand for deep structural, avionics, and engine upgrades.

How are digital twins improving maintenance efficiency?

Digital-twin analytics cut unnecessary inspections, lowering maintenance costs by up to 25% while boosting aircraft availability 10-15%.

What is the main challenge limiting depot throughput in the next two years?

Supply-chain fragility exacerbated by single-source parts and 200-day engine turnaround times poses the most immediate brake on hangar capacity despite robust demand.

Page last updated on: