Aviation Maintenance Repair And Overhaul (MRO) Software Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

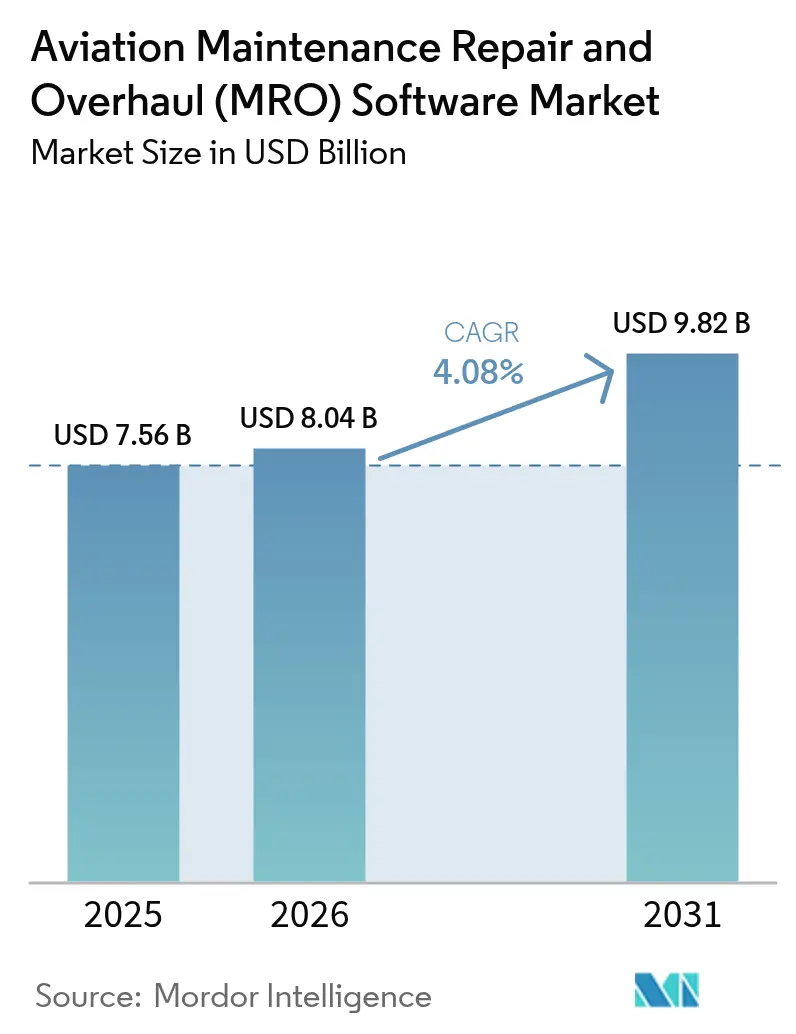

| Market Size (2026) | USD 8.04 Billion |

| Market Size (2031) | USD 9.82 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

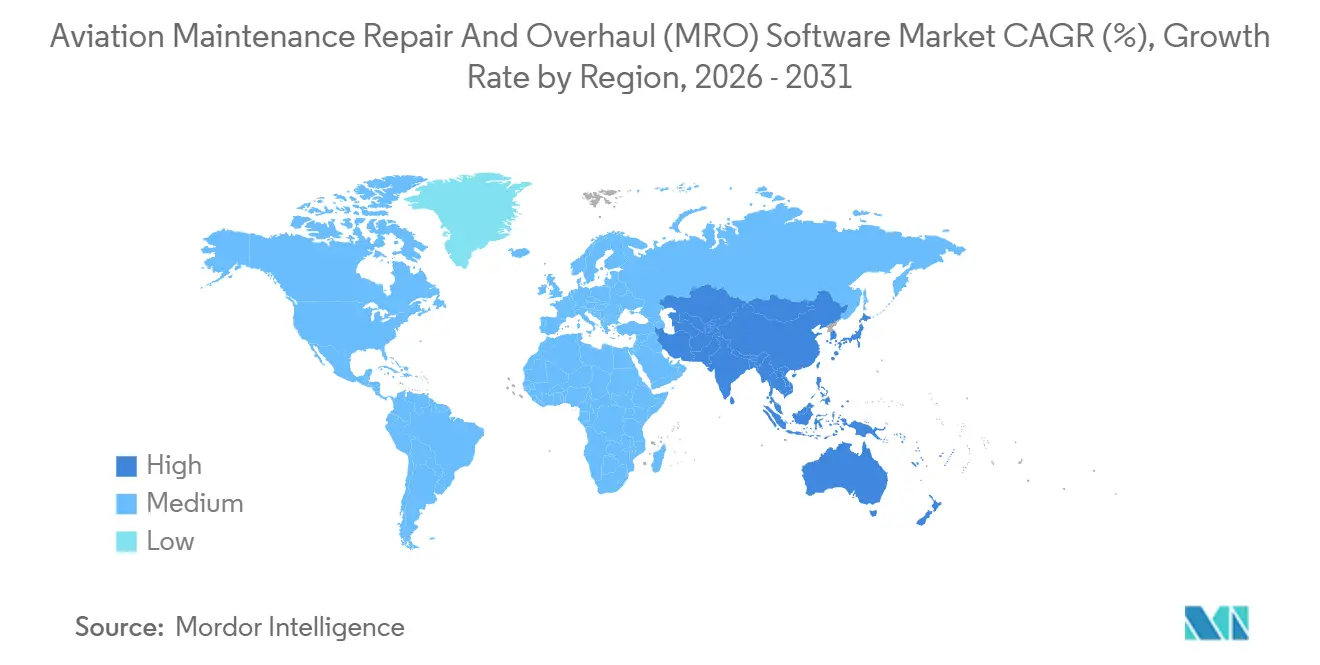

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Maintenance Repair And Overhaul (MRO) Software Market Analysis by Mordor Intelligence

The aviation maintenance, repair, and overhaul (MRO) software market size is expected to grow from USD 7.56 billion in 2025 to USD 8.04 billion in 2026 and is forecast to reach USD 9.82 billion by 2031 at a 4.08% CAGR over 2026-2031. This momentum reflects a structural shift as airlines, independent MROs, and OEMs digitize maintenance through predictive analytics and digital twin workflows, streamlining planning and improving dispatch reliability. Aging fleets and postponed maintenance checks from the pandemic period are leading to a concentration of heavy maintenance events between 2025 and 2027. This is driving increased demand for scheduling, inventory optimization, and paperless compliance solutions. Cloud adoption is rising as large operators document 25% to 30% reductions in five-year total cost of ownership with managed hosting, which strengthens the case for subscription pricing among carriers scaling narrowbody fleets.

Key Report Takeaways

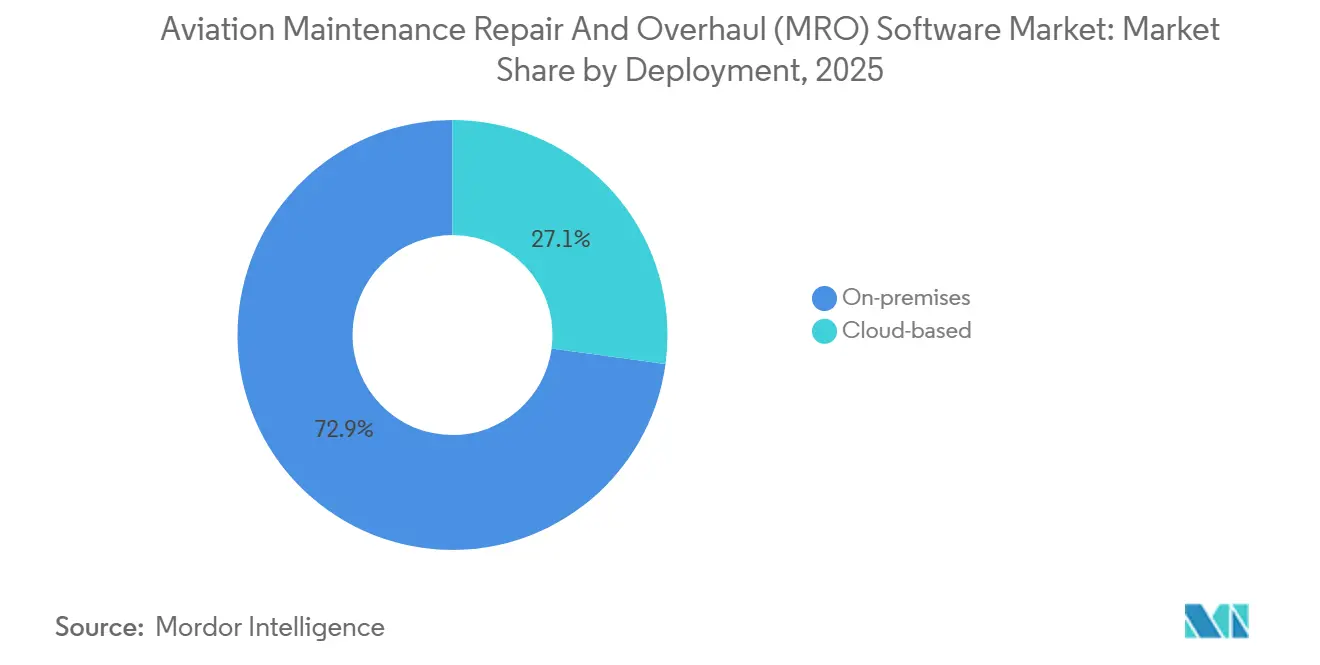

- By deployment, on-premises led the aviation maintenance, repair, and overhaul (MRO) software market with 72.85% market share in 2025, while cloud-based is projected to expand at a 5.98% CAGR through 2031.

- By end user, MROs held a 58.02% share in 2025, while airlines are projected to record the fastest growth at a 4.62% CAGR to 2031.

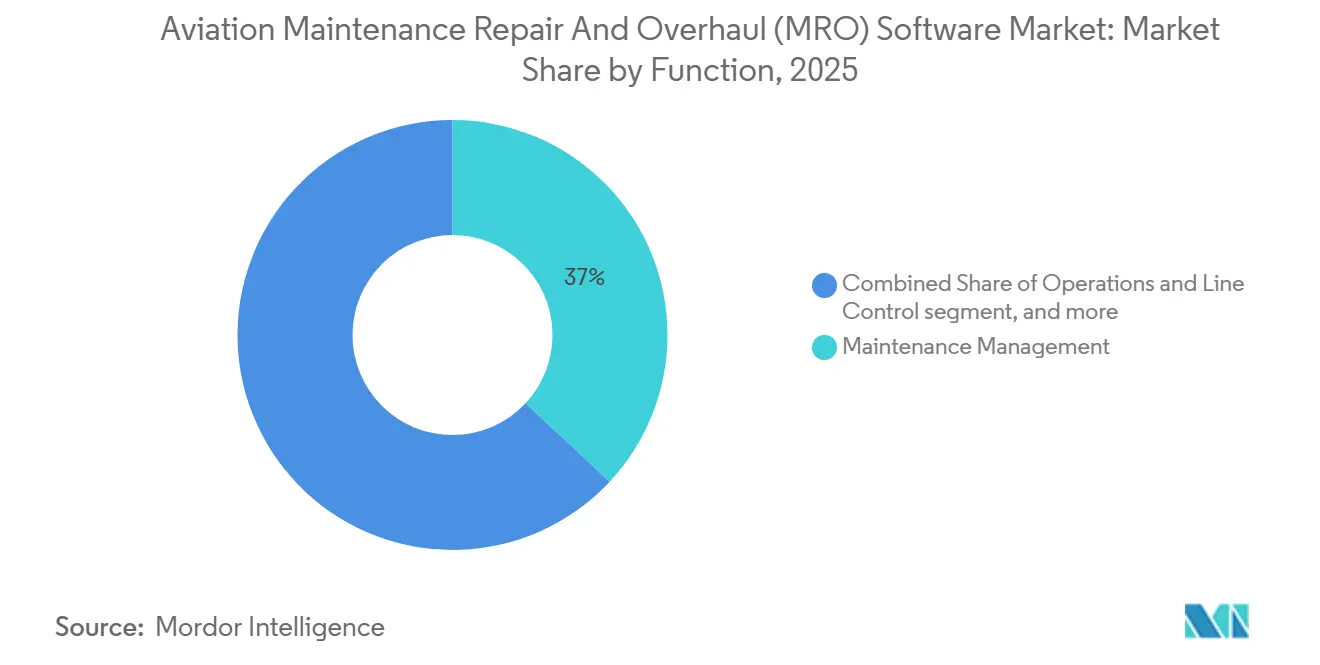

- By function, maintenance management accounted for 36.95% of the aviation maintenance, repair, and overhaul (MRO) software market in 2025, and predictive analytics and health monitoring are advancing at a 6.18% CAGR through 2031.

- By solution, software commanded 72.90% revenue share in 2025, while services are projected to grow at a 4.98% CAGR through 2031.

- By geography, North America retained 45.25% of the aviation MRO software market share in 2025, while Asia-Pacific is forecasted to post the highest growth at 4.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aviation Maintenance Repair And Overhaul (MRO) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SaaS adoption among LCCs | +0.8% | Global, with early gains in Asia-Pacific and Europe | Medium term (2-4 years) |

| Expansion of predictive maintenance analytics platforms | +1.1% | North America and EU core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Integration of digital-twin engines for real time health monitoring | +0.9% | Global, led by major OEMs and hub carriers | Long term (≥ 4 years) |

| Post-COVID fleet age spike raising heavy maintenance demand | +0.7% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| Ecosystem push for paperless compliance and e-signatures | +0.4% | North America and Europe, regulatory influence via FAA AC 120-78B and EASA Part-145 | Short term (≤ 2 years) |

| OEM warranty data liberation accelerating third-party MRO IT uptake | +0.3% | Global, particularly competitive MRO markets in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in SaaS Adoption Among LCCs

Low-cost carriers (LCCs) have historically limited IT capital expenditure. Yet, subscription models align with their cost discipline by shifting spend to operating budgets, automating updates, and enabling rapid scaling across decentralized line stations. Air India’s shift to cloud-only MRO hosting illustrates how large fleets can optimize managed environments for enhanced cost efficiency and operational agility, significantly reducing total cost of ownership over a multi-year period. Provisioning access in hours instead of weeks shortens time-to-value and reduces reliance on scarce integrators, which is essential for carriers expanding narrowbody capacity. Thai Airways’ 2026 selection of a cloud-hosted eMRO suite further signals that regional flag carriers are adopting SaaS to modernize maintenance with faster visibility into aircraft health.[1]AAR CORP., “Thai Airways Selects Trax and Aerostrat to Drive Its Digital MRO Transformation,” aarcorp.com As these deployments scale, vendors are improving multi-tenant security and compliance, lowering perceived risk, and expanding the market base for aviation MRO software.

Expansion of Predictive Maintenance Analytics Platforms

Predictive platforms use real-time flight and engine data to forecast component degradation, enabling operators to schedule interventions during planned downtime and avoid cancellations. OEMs and tier-one suppliers are embedding machine learning (ML) into maintenance records and decision support systems, reducing troubleshooting time and improving service-level performance at the line station and hangar. Integrating sensor data with asset management workflows enhances operational efficiency by reducing unscheduled events, improving dispatch reliability, and optimizing parts allocation through actionable alerts converted into work packages with defined material requirements. Outcome-based contracts, linking payments to availability metrics, are increasingly adopted in the Aviation MRO software market, reflecting evolving industry practices.

Integration of Digital-Twin Engines for Real-Time Health Monitoring

Digital twin engines simulate thermodynamic and vibration profiles, enabling scenario analysis and solution testing in software before deploying technician resources for implementation. Large OEMs and leading MROs operationalized twin-driven workflows that shorten planning cycles and aid root-cause analysis when anomalies arise. These models accelerate troubleshooting by connecting real-time telemetry with historical records and service bulletins, which improves the precision of fault isolation. With engines reporting more parameters per flight hour, centralized data lakes and curated feature stores are vital for sustaining model performance across diverse engine fleets. Digital twins are anticipated to reshape lifecycle economics and power-by-the-hour agreements, positioning analytics as a critical tool for margin optimization in the aviation maintenance, repair, and overhaul (MRO) software market.

Post-COVID Fleet Age Spike Raising Heavy-Maintenance Demand

Deferred retirements and high utilization have resulted in an aging global fleet, compressing structural C and D checks, underscoring the need for optimized slot management, proactive long-lead material planning, and mobile inspection tools to efficiently capture maintenance data, minimize rework, and maintain operational continuity. Condition-based software transitions operators from fixed-interval programs, deferring replacements until data validates wear thresholds, optimizing asset utilization, preserving operational life, and reducing unnecessary resource consumption. Vendors integrating predictive modules, change management, and technician training are strategically positioned to deliver comprehensive solutions that address operator demand and increase heavy-check requirements in the aviation maintenance, repair, and overhaul (MRO) software market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of certified MRO IT talent | -0.6% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Fragmented, legacy data silos impede AI scalability | -0.4% | Global, particularly operators with 1990s-era systems | Medium term (2-4 years) |

| Cybersecurity insurance premiums escalating for cloud MRO suites | -0.2% | Global, compliance factors include DO-326A/ED-202, SOC 2 Type II | Short term (≤ 2 years) |

| Tightening export-control rules on aircraft data schemas | -0.2% | Geopolitically sensitive regions, fragmentation in Russia, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Certified MRO IT Talent

Demand for technicians with both airworthiness credentials and modern IT skills is outpacing supply, which slows the rollout of analytics-heavy workflows. Carriers and MROs are increasingly partnering with vendors to secure managed services that cover data engineering, model retraining, and configuration updates. This approach reduces project risk but can raise dependency on external providers during critical maintenance seasons. Talent constraints also limit the pace of process redesign and change management, which are required to capture the full benefit of predictive tooling in the aviation maintenance, repair, and overhaul (MRO) software market.

Fragmented, Legacy Data Silos Impede AI Scalability

Many operators rely on outdated systems with limited interoperability, which restricts real-time data capture and complicates the implementation of analytics. Consolidating engineering and maintenance data into cloud platforms is becoming a prerequisite for rolling out predictive programs at fleet scale. Airlines and technology partners collaborate to reduce latency, standardize schemas, and create unified data lakes, enabling advanced analytics. The aviation maintenance, repair, and overhaul (MRO) software market faces inconsistent AI performance across fleets and functions until these foundational systems are fully implemented.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Migration Accelerates Despite On-Premises Entrenchment

On-premises deployments accounted for 72.85% of spending in 2025, while cloud-based solutions are projected to expand at a 5.98% CAGR as operators pivot toward subscription economics and managed hosting. Large flag carriers, defense users, and public sector operators still favor local hosting to satisfy data sovereignty and audit control needs. Yet they are adopting selective cloud-based analytics services that can be ring-fenced for security. As vendors achieve certification under recognized security frameworks and enhance observability, the adoption of hybrid footprints is becoming increasingly viable in maintenance hangars and line stations. Operators transitioning to managed environments have reported significant reductions in five-year total cost of ownership, enabling the reallocation of limited capital toward fleet expansion and increased heavy check capacity.

Cloud adoption spans both new entrants and incumbents that seek faster feature delivery without disruptive upgrade cycles. New airlines focusing on paperless operations from the outset are incorporating cloud mobility and e-signature capabilities into their daily processes. This approach strengthens the aviation maintenance, repair, and overhaul (MRO) software market by enabling vendors to enhance multi-tenant architectures to accommodate diverse fleets, distributed operations, and large-scale compliance requirements.

By End User: Airlines Verticalize to Reclaim Margin, MROs Defend Scale Advantage

Independent MROs accounted for 58.02% of the market in 2025, highlighting their role as multi-fleet integrators managing complex workflows and customer contracts across global facilities. Their growth is driven by cross-airframe expertise and standardized processes, supported by analytics, mobile inspections, and predictive material planning. Airlines remain the fastest-growing end-user group, with a 4.62% CAGR, as they bring heavy checks in-house to protect intellectual property, safeguard capacity, and capture margin that previously flowed to third parties. OEMs also anchor demand by bundling lifecycle platforms with service agreements that link software to performance outcomes.

Airlines are piloting AI assistants and mobile-first workflows to modernize legacy processes and accelerate decision-making in operations control centers. This focus on turnaround time reliability drives investments in sensor analytics and maintenance scheduling that cut out-of-service hours. Independent MROs require data portability and broad interface compatibility to support multiple lessors and operators while meeting warranty obligations. Vendors are addressing these needs by offering configurable platforms that integrate centralized airline strategies with the decentralized operations of third-party providers, ensuring efficiency and compliance in the aviation maintenance, repair, and overhaul (MRO) software market.

By Function: Predictive Analytics Outpaces Maintenance Management as AI Matures

Maintenance management accounted for 36.95% of 2025 spending as organizations continue to digitize core workflows, such as work orders, airworthiness directive tracking, planned schedules, and compliance reporting. The use of mobile task cards, photos, and point-of-work parts requisitions minimizes transcription errors and accelerates approvals, supporting line operations in maintaining aircraft schedules. Inventory and supply chain modules integrate usage forecasts with stock policies to improve fill rates and shelf-life management for time-sensitive components. Predictive analytics and health monitoring are the fastest-growing functions, with a 6.18% CAGR, as algorithms translate telemetry and maintenance history into remaining valid-life estimates and recommended interventions.

Real-time sensing platforms are feeding richer datasets into asset management to improve failure forecasts and enable condition-based decisions that defer removals until thresholds are met. Vendors are also using generative AI to extract structured records from unstructured technician notes, easing regulatory reporting and accelerating engineering analysis. Over time, predictive and prescriptive modules are expected to converge with core maintenance functions to provide unified planning and execution across fleets.

By Solution: Services Gain Share as AI Complexity Outpaces Internal Expertise

Software platforms captured 72.90% of revenue in 2025 because they serve as the systems of record for compliance, financial controls, and engineering authority throughout the maintenance lifecycle. Continuous-delivery roadmaps that push features quarterly are replacing multi-year upgrade cycles, which favors subscription contracts tied to feature uptake. Services are growing at a 4.98% CAGR as operators seek implementation support, data engineering, change management, and managed analytics to keep AI models current and effective in production. New AI modules require domain tuning and safety assurance, which extend service engagements and turn them into annuity relationships that scale with fleet size and data volume.

Evolving offerings include generative AI for automated record creation, predictive modules for cost anomaly detection, and workflow optimization that reduces handoffs and idle time. Vendors are packaging these capabilities with defined delivery milestones and performance targets so that operators can track realized benefits. Enhanced platform and service integration streamlines operations, effectively reducing complexity for line stations and heavy check facilities.

Geography Analysis

North America held 45.25% of the market share in 2025. Regional operators benefit from proximity to major enterprise software vendors and ongoing co-development programs that deliver early access to new modules. Delta Airlines streamlined its cloud infrastructure by integrating multiple data sources into a unified data lake, enabling machine learning (ML) capabilities without additional data center investments.[2]CAST Software, “Delta Air Lines and IBM Consulting Complete Massive Cloud Migration and Modernization,” learn.castsoftware.com Regulatory updates that recognize digital signatures have also enabled paperless workflows, accelerating approvals and strengthening audit trails in the aviation maintenance, repair, and overhaul (MRO) software market.

Asia-Pacific is forecasted to expand at a 4.70% CAGR as narrowbody order backlogs convert into deliveries and regional operators scale digital programs to onboard new aircraft types quickly. Air India’s adoption of cloud-only MRO hosting reflects the region’s shift from legacy systems to managed platforms, emphasizing operational efficiency and faster time-to-value in aviation infrastructure management.[3]Air India, “Air India moves entire IT Infrastructure to Cloud, closes historic Data Centres,” airindia.com Southeast Asian carriers are adopting cloud-hosted platforms to reduce data-center overhead and improve visibility across dispersed line stations, thereby reinforcing regional demand for aviation maintenance, repair, and overhaul (MRO) software.

Europe benefits from EASA encouragement of electronic records and from incumbent operators that invest in predictive maintenance, digital twins, and automated inventory engines. A Tier-1 MRO’s multi-year digital investment that integrates analytics across engineering, supply chain, and shops underscores long-term confidence in software-enabled value creation. The Middle East’s hub-and-spoke carriers are emphasizing heavy check optimization and supply chain integration to maintain high utilization, supported by sovereign cloud investments. South America is modernizing selectively, focusing on cloud records that meet lesser redelivery needs. At the same time, Brazil leads regional uptake with stable investment pipelines in the aviation maintenance, repair, and overhaul (MRO) software market.

Competitive Landscape

The aviation maintenance, repair, and overhaul (MRO) software market shows moderate concentration, with the top three vendors accounting for more than 30% of revenue in 2024 and the top five accounting for nearly half of global sales, as operators maintain multi-vendor strategies to avoid lock-in. Consolidation is accelerating around analytics capabilities and service delivery, highlighted by a 2024 acquisition that integrated a cloud-native MRO specialist into a broader enterprise asset management suite. Airlines and MROs are increasingly seeking bundled offerings that combine software with managed analytics, which shifts competitive advantage toward vendors with delivery depth and model retraining capacity.

Partnerships with hyperscalers are also reshaping the field by enabling low-latency analytics, unified data models, and global scalability. Vendors that deliver digital tasking on mobile devices and end-to-end paperless flows are winning with new entrants and with operators rebuilding fleets. Product roadmaps integrate generative AI, predictive modules, and optimization engines, streamlining processes and aligning maintenance strategies with operational constraints, as validated by recent collaborations in the aerospace and technology industries. Implementation, training, and change management are decisive because outcomes depend on frontline adoption and data quality at the point of maintenance in the aviation maintenance, repair, and overhaul (MRO) software market.

Emerging providers are differentiating with augmented-reality instructions and low-code extensibility that speed niche workflows such as component overhaul stations. Established players are revamping user experiences and unveiling APIs to bolster innovation spearheaded by airlines and MROs, all while upholding stringent governance. Customer preference for annuity-like engagements that include continuous AI model maintenance is reshaping revenue profiles and deepening customer-vendor relationships across the aviation maintenance, repair, and overhaul (MRO) software market. Competitive differentiation is increasingly measured by measurable reliability gains, audit-readiness, and speed to deploy modules that address current maintenance bottlenecks.

Aviation Maintenance Repair And Overhaul (MRO) Software Industry Leaders

IBM Corporation

Ramco Systems Ltd.

IFS Aktiebolag

Oracle Corporation

HCL Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Royal Navy is broadening its Motherlode analytics platform from helicopters to fixed-wing aircraft, including the P-8A Poseidon, E-2D Hawkeye, and Protector. This expansion leverages aircraft data for predictive maintenance, aiming to optimize operational readiness and improve availability across the Fleet Air Arm through advanced, data-driven decision-making.

- September 2025: OASES secured a contract to develop OASES Lumina, a web-native maintenance and engineering platform. The platform aims to provide enhanced performance, accessibility, and streamlined workflows for airlines, CAMOs, and MROs worldwide.

- August 2025: Ramco Systems signed a contract with United Aerospace Maintenance Company (UAMCO) Ltd to deploy its Aviation Software. UAMCO will utilize Ramco's integrated solution to optimize operations and materials management for LEAP engines.

Global Aviation Maintenance Repair And Overhaul (MRO) Software Market Report Scope

Maintenance, repair, and operations (MRO) software plays a pivotal role in the aviation sector, addressing its maintenance, repair, operations, and overhaul requirements. This software streamlines and monitors ongoing MRO activities in aviation, encompassing tasks such as inventory management, facilitating preventive and essential maintenance, creating and managing work orders, and ensuring regulatory compliance through meticulous tracking and documentation.

The aviation maintenance, repair, and overhaul (MRO) software market is segmented by deployment, end user, function, solution, and geography. By deployment, the market is segmented into cloud-based and on-premises. By end user, the market is classified into airlines, MROs, and OEMs. By function, the market is segmented into maintenance management, operations and line control, inventory and supply chain, and predictive analytics and health monitoring. By solution, the market is segmented into software and services. The report also covers the market sizes and forecasts for the aviation maintenance, repair, and overhaul (MRO) software market across different regions. For each segment, the market size is provided in terms of value (USD).

| Cloud-based |

| On-premises |

| Airlines |

| MROs |

| OEMs |

| Maintenance Management |

| Operations and Line Control |

| Inventory and Supply Chain |

| Predictive Analytics and Health Monitoring |

| Software |

| Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Deployment | Cloud-based | ||

| On-premises | |||

| By End User | Airlines | ||

| MROs | |||

| OEMs | |||

| By Function | Maintenance Management | ||

| Operations and Line Control | |||

| Inventory and Supply Chain | |||

| Predictive Analytics and Health Monitoring | |||

| By Solution | Software | ||

| Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the aviation maintenance, repair, and overhaul (MRO) software market size in 2026 and the forecast growth through 2031?

The aviation maintenance, repair, and overhaul (MRO) software market size is USD 8.04 billion in 2026, and it is projected to reach USD 9.82 billion by 2031 at a 4.08% CAGR.

Which deployment model is growing fastest in Aviation MRO software?

Cloud-based deployments are growing fastest, supported by subscription economics and documented 25% to 30% reductions in five-year total cost of ownership for large operators.

Which region leads spending and which region is growing fastest in this space?

North America leads with 45.25% of 2025 spending, while Asia-Pacific is projected to grow fastest at a 4.70% CAGR through 2031.

Which functional area is expanding quickest within Aviation MRO platforms?

Predictive analytics and health monitoring is the fastest-growing function, advancing at a 6.18% CAGR as operators adopt sensor-driven maintenance and ML.

How is consolidation shaping vendor strategies in Aviation MRO software?

Consolidation is concentrating analytics capabilities and service delivery, while partnerships with hyperscale's and OEMs are enabling faster feature releases and scalable data foundations.

What near-term factors will most influence adoption decisions?

Aging fleets and the clustering of heavy-check events, regulatory acceptance of e-signatures, and the availability of managed services for AI and data engineering will drive near-term adoption.

Page last updated on: