Aircraft Micro Turbine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

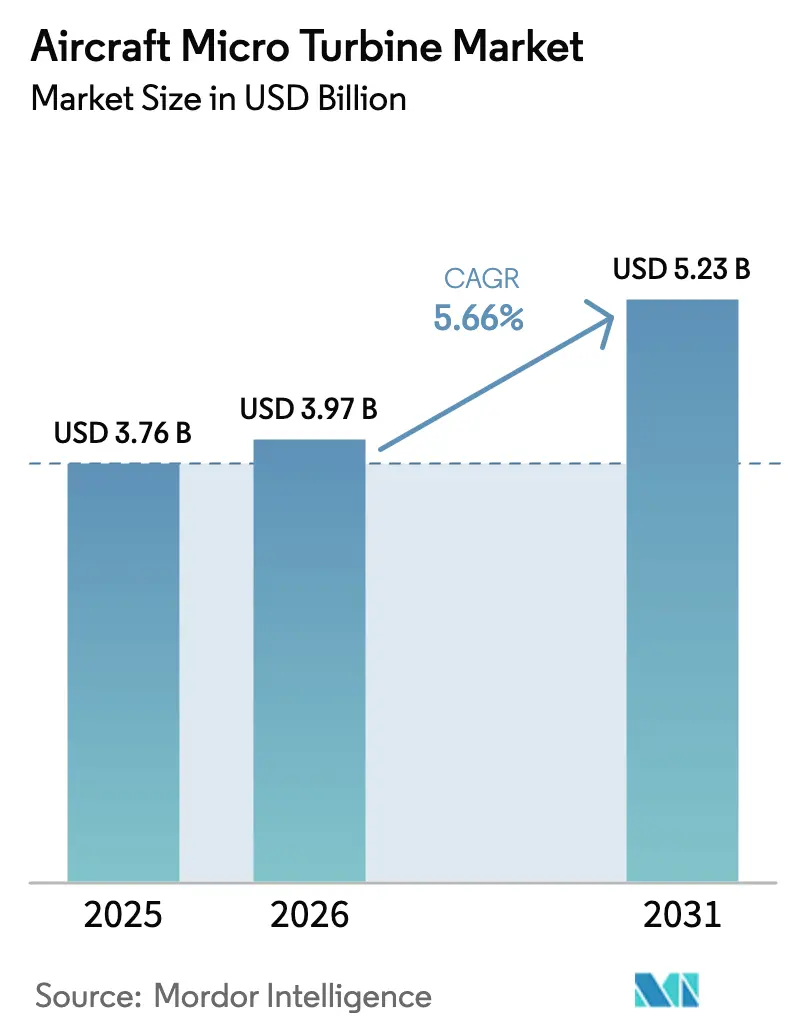

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Micro Turbine Market Analysis by Mordor Intelligence

The aircraft micro turbine market size was valued at USD 3.76 billion in 2025 and estimated to grow from USD 3.97 billion in 2026 to reach USD 5.23 billion by 2031, at a CAGR of 5.66% during the forecast period (2026-2031). Robust defense spending on attritable drones, the urgency to decarbonize regional fleets, and fast-evolving hybrid-electric architectures underpin this expansion. OEMs scale turbines as range extenders for eVTOL projects, while commercial operators adopt power-dense units to overcome battery-only endurance limits. On the supply side, additive-manufacturing breakthroughs shorten development cycles and mitigate legacy bottlenecks that have curbed engine availability. Certification momentum—evidenced by the FAA’s powered-lift rule and EASA’s VTOL framework—also improves market visibility for investors and accelerates time-to-market for innovators.

Key Report Takeaways

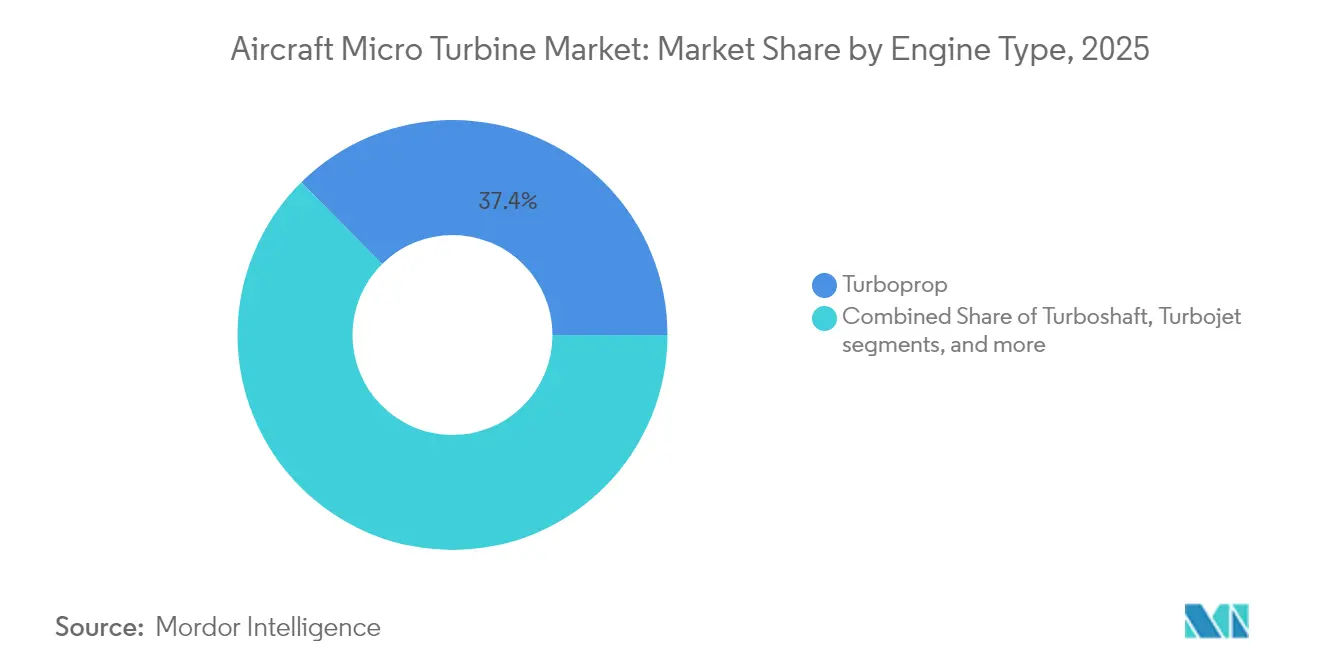

- By engine type, turboprop configurations led with 37.42% of the aircraft micro turbine market share in 2025, while turboshaft variants are expanding at a 7.36% CAGR through 2031.

- By power output, 60 to 90 kW systems accounted for 45.12% of the aircraft micro turbine market size in 2025; systems above 90 kW are projected to grow at a 6.47% CAGR to 2031.

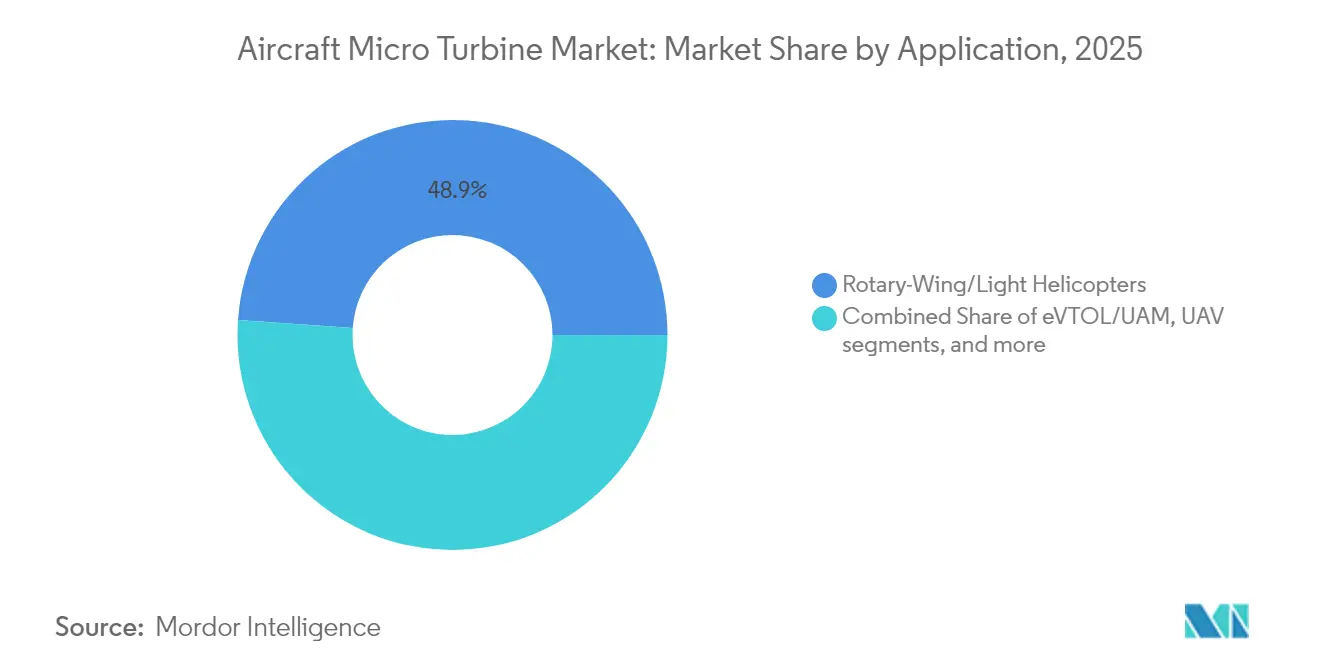

- By application, rotary-wing platforms captured 48.88% of the aircraft micro turbine market share in 2025; unmanned aerial vehicles are advancing at an 8.10% CAGR to 2031.

- By end user, commercial aviation held 42.76% of 2025 revenue, whereas UAV OEMs are forecasted to post a 6.98% CAGR through 2031.

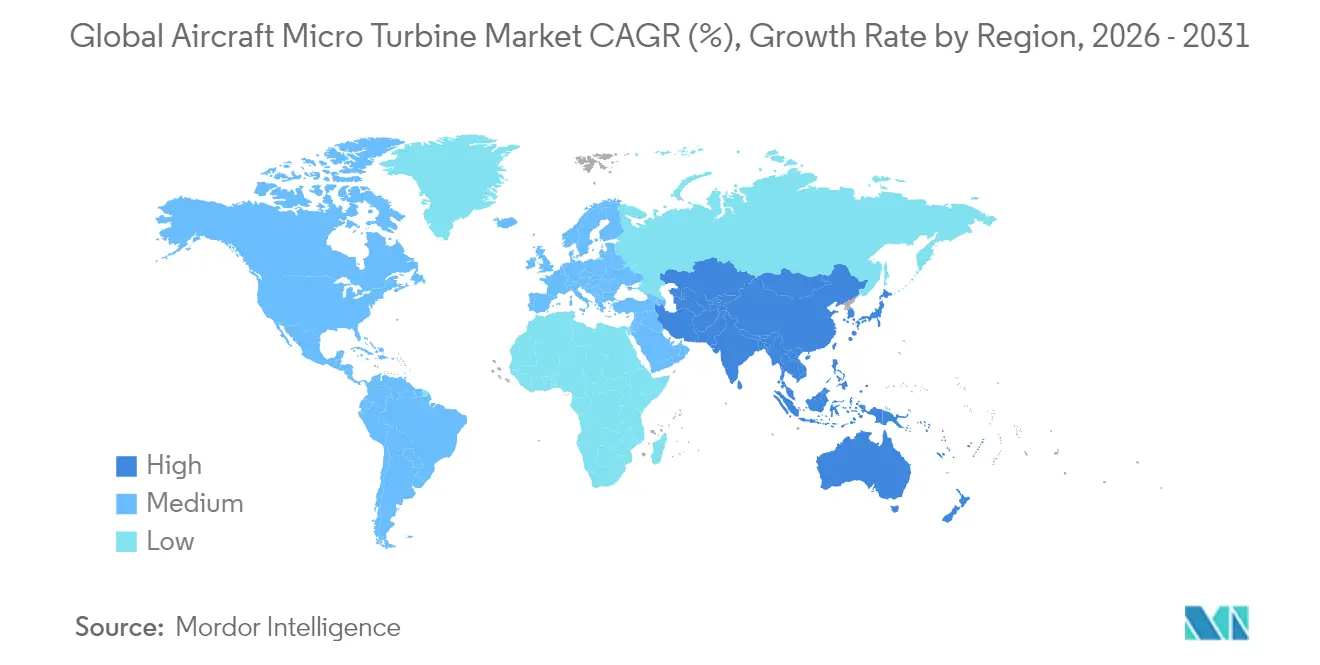

- North America maintained 39.05% regional dominance in 2025, but Asia-Pacific is the fastest-growing geography at 7.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Micro Turbine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing deployment of endurance-focused UAVs | +1.2% | Global (North America and Asia-Pacific focus) | Medium term (2-4 years) |

| Rise of hybrid-electric range extenders for eVTOL/UAM | +0.9% | North America and EU expanding to Asia-Pacific | Long term (≥ 4 years) |

| Superior power-to-weight and multi-fuel capability vs piston engines | +0.8% | Global | Short term (≤ 2 years) |

| Fleet renewal of trainer and light aircraft | +0.7% | North America and EU | Medium term (2-4 years) |

| Defense demand for attritable drones | 1.1% | North America, with spillover to allied nations | Short term (≤ 2 years) |

| Adoption of micro-turbine APUs in more-electric regional aircraft | 0.6% | Global, led by commercial aviation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Deployment of Endurance-Focused UAVs

Extended-mission drones dominate new procurement cycles as operators require flight times beyond eight hours. The USAF’s ATTAM program awarded USD 12.7 million to Kratos in 2024 to develop attritable engines, confirming federal commitment to long-loiter platforms.[1]Valerie Insinna, “Kratos wins USAF task order for attritable engines,” defensenews.com Commercial operators in pipeline inspection and precision agriculture share the same endurance imperative, and micro turbines satisfy this demand by burning heavy fuels available at remote sites. Lower vibration levels lengthen sensor life, while simplified maintenance schedules reduce downtime across high-utilization fleets.

Rise of Hybrid-Electric Range Extenders for eVTOL/UAM

Honda’s 2024 test of a gas-turbine hybrid for eVTOL aircraft validated micro turbines as viable range extenders.[2]Graham Warwick, “Honda validates gas-turbine hybrid for eVTOL,” aviationweek.com Urban air mobility developers use these units to triple practical range without breaching weight budgets. Regulatory clarity arrived in 2025 when the FAA integrated powered-lift aircraft into the National Airspace System, streamlining certification. Hybrid architectures also allay public reliability concerns by providing redundant power in case of battery faults.

Superior Power-to-Weight and Multi-Fuel Capability versus Piston Engines

Micro turbines deliver two-to-threefold higher power-to-weight ratios and sustain output at altitude. Turbotech’s R90 regenerative turboprop matches piston fuel burn while retaining turbine reliability.[3]Ian J. Twombly, “Turbotech R90 aims piston fuel burn,” aopa.org Universal fuel compatibility lets military operators simplify logistics using diesel, Jet-A, or sustainable aviation fuels without hardware change. Reduced vibration mitigates airframe fatigue and improves ISR sensor clarity during high-endurance missions.

Fleet Renewal of Trainer and Light Aircraft

The US Navy chose the T-54A program to swap aging piston trainers for modern turbine platforms, cutting maintenance hours and fuel burn. GE Aerospace’s Catalyst, certified in 2025, offers a 16:1 pressure ratio and 18% lower fuel consumption, making it the first clean-sheet turboprop in decades. Flight schools gain curricula aligned with commercial turbine operations, while operators hedge against tightening emission rules by adopting more efficient powerplants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and maintenance cost | −0.8% | Global | Short term (≤ 2 years) |

| Certification pathway uncertainty | −0.6% | Global (North America and EU) | Medium term (2-4 years) |

| Additive-manufacturing capacity bottlenecks for hot-section parts | −0.4% | Advanced manufacturing regions | Medium term (2-4 years) |

| Competition from lightweight hydrogen fuel cells | −0.3% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Maintenance Cost

Retail prices near USD 100,000 place turbines at a 3-5× premium to equivalent piston engines, as highlighted by Turbotech’s R90 offering. Specialized tooling and hot-section overhauls that can cost 40% of engine value exacerbate total ownership expenses. Global maintenance-capacity shortages are projected to peak in 2026, elevating hourly service rates and limiting adoption in cost-sensitive sectors like flight training and recreational aviation.

Certification Pathway Uncertainty

While the FAA’s powered-lift rule bridged a major gap, hybrid-electric systems still navigate overlapping turbine and battery standards that extend development by up to 18 months. European and US rules diverge on endurance testing for autonomous platforms, complicating global rollout plans. Attritable drones face a grey zone where legacy durability metrics inflate certification costs despite limited life-cycle intent, stalling fast-track fielding for emerging defense needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Turboprop Dominance with Turboshaft Momentum

Turboprops accounted for 37.42% of 2025 revenue, underscoring their entrenched role in trainers, light commuters, and endurance UAVs. This share positions turboprops as the single largest slice of the aircraft micro turbine market, benefiting from ready certification pathways and commodity propeller technology. Turboshaft units, however, advance at a 7.36% CAGR through 2031 as civil and parapublic rotorcraft orders rebound and hybrid-electric distributors favor shaft power. Turbojet designs populate high-speed reconnaissance drones but remain fuel-hungry for broader uptake.

Turbofan and recuperated variants occupy smaller technical niches but offer upside as heat-recovery systems elevate thermal efficiency. China's AES100 turboshaft entered production in 2025, signaling Asia-Pacific's capacity to erode Western lead times. The long-term shift toward shaft-coupled propulsion and regenerative cycles will reshape the aircraft micro turbine market as eVTOL, tiltrotor, and regional hybrid projects demand higher efficiency under strict emission ceilings.

By Power Output Rating: Mid-Range Sweet Spot with High-Power Upswing

Engines rated 60 to 90 kW delivered 45.12% of 2025 sales, anchoring the aircraft micro turbine market size for mainstream UAVs and light aircraft, where weight margins are narrow. System maturity reduces integration risk, letting OEMs meet aggressive entry-into-service dates without redesigning thermal management. Demand above 90 kW is scaling at 6.47% CAGR as heavy-lift UAVs, short-haul cargo planes, and distributed hybrid-electric demonstrators progress from prototype to low-rate production.

Sub-30 kW units cater to specialized ISR drones, while 30 to 60 kW platforms target trainer retrofits and lower-power tiltrotors. Power-scaling challenges center on thermal limits and gearbox mass, encouraging the adoption of ceramic matrix composites and additive-manufactured diffusers. FAA-funded CLEEN III projects that a 90 kW turbogenerator can cut block fuel up to 30% on regional flights, hinting at steep growth potential once program risk retires.

By Application: Rotorcraft Lead as UAVs Accelerate

Rotorcraft platforms retained 48.88% of the 2025 value, reflecting decades of turbine integration and the rotorcraft fleet’s sustained need for high power-to-weight ratios. The sector is buoyed by air-ambulance renewals and light military helicopter replacements that prize efficient hot-and-high performance. UAVs are the fastest-rising application at an 8.10% CAGR, driven by military attritable programs and commercial BVLOS demand. High-density power enables payload expansion without sacrificing range, a pivotal advantage over battery-centric propulsion.

Fixed-wing light aircraft continue steady buying cycles as flight schools modernize aluminum trainers. Though nascent, eVTOL projects are set to multiply post-2027 once early certification hurdles clear. Auxiliary power units for more-electric regional aircraft present incremental demand, especially where on-ground emission caps restrict turbine idle-time use.

By End User: Commercial Stability and UAV OEM Upsurge

Commercial aviation captured 42.76% of 2025 turnover, giving airlines and training providers the largest stake in the aircraft micro turbine market. Reliability metrics honed in airline service translate to favorable financing and residual-value profiles, cementing commercial dominance for the near term. UAV OEMs, however, outpace all peers with a 6.98% CAGR through 2031 as defense and infrastructure operators standardize on turbine-powered drones for multi-day missions.

Defense programs sustain baseline demand across ISR, loitering munitions, and swarming concepts. General aviation buyers favor turbines for situational-awareness flights and aerial work, whereas ruggedness and fuel flexibility justify higher capex. Research institutes round out the landscape by field-testing recuperated cycles, alternative fuels, and AI-driven engine-health monitoring that will influence mainstream adoption paths.

Geography Analysis

North America held 39.05% of 2025 revenue, supported by the USAF’s deep attritable drone pipeline, GE and Honeywell’s extensive supplier bases, and Mexico’s low-cost aerostructure clusters. Certification bodies, government R&D funding, and aftermarket MRO density create formidable entry barriers for foreign challengers.

Asia-Pacific is the most dynamic region, projected at 7.32% CAGR to 2031. China’s AES100 turboshaft license heralds indigenous capability in 1,000 kW class engines, while India accelerates under “Make in India” to close propulsion gaps for UAVs and light transport aircraft. Japan leverages Mitsubishi Heavy Industries’ partnership with Rolls-Royce to co-develop advanced turbogenerators, and Australia channels defense procurement into sovereign drone programs to secure supply chains.

Europe remains a powerhouse, home to Safran, Rolls-Royce, and Turbotech. Clean-Aviation funding steers investment toward hybrid-electric and hydrogen-ready micro turbines, incentivizing ultra-low-emission designs that exceed ICAO CO₂ standards. Eastern Europe’s growing MRO footprint and the Middle East’s airport expansion create reciprocal demand for export-friendly engines and aftermarket services, though geopolitical risks temper near-term scale-up.

Competitive Landscape

Market concentration is moderate. Safran, Honeywell, and RTX Corporation leverage long-cycle expertise, global support networks, and vertically integrated supply chains to secure high-volume contracts. Rolls-Royce adapts its Advance2 core for attritable engines, bridging legacy technology with low-unit-cost mandates.[4]Rolls-Royce plc, “Advance2 attritable engine core demonstration,” rolls-royce.com

Specialist firms exploit white-space niches. PBS Group focuses on small turboshafts for light helicopters, while Turbotech pioneers recuperated cycles to rival piston efficiency. UAV Turbines targets hybrid-electric drones with sub-100 kW outputs, and Sierra Turbines employs additive manufacturing to eliminate 95% of conventional part counts, cutting lead times during supply crunches.

Competitive advantage now tilts toward firms mastering certification labyrinths and additive-manufactured hot sections. Companies that guarantee on-time delivery poach share as primes grapple with supply shortages. Cost pressure from attributable programs forces incumbents to redesign for manufacturability, inviting partnerships with agile start-ups versed in low-cost composite casings and printed fuel nozzles. The shift from lifetime durability to acceptable disposability marks a structural rewrite of turbomachinery economics.

Aircraft Micro Turbine Industry Leaders

Safran Power Units (Safran SA)

Honeywell International Inc.

Kratos Defense & Security Solutions, Inc.

PBS AEROSPACE Inc.

UAV Turbines, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: China’s AECC received a production license for the AES100 turboshaft engine, its first fully indigenous civil design exceeding 1,000 kW.

- March 2025: Aerospace secured FAA certification for the Catalyst turboprop, boasting an industry-best 16:1 pressure ratio and 18% lower fuel burn.

- June 2024: Rolls-Royce and ITP Aero signed an MoU to develop cost-effective Wingman engines for European remote carriers.

- January 2024: Turbotech and Safran tested the first hydrogen-powered gas turbine engine for light aviation applications.

Global Aircraft Micro Turbine Market Report Scope

Microturbine engines are a hybrid power source for small unmanned aerial vehicles and VTOLs. It is used for stationary energy generation applications. These are the combustion turbine that produces both heat and electricity on a relatively small scale.

The aircraft microturbine market is segmented based on engine type, end-user, distribution channel, and geography. By engine type, the market is segmented into turboshaft, turboprop, and turbojet. By end user, the market is segmented into commercial and military. By distribution channel, the market is classified as OEM and aftermarket. The market sizing and forecasts have been provided in value (USD million).

| Turbojet |

| Turboshaft |

| Turboprop |

| Turbofan |

| Recuperated/Regenerative |

| Less than 30 kW |

| 30 to 60 kW |

| 60 to 90 kW |

| Greater than 90 kW |

| Unmanned Aerial Vehicles (UAVs) |

| Manned Light Fixed-Wing Aircraft |

| Rotary-Wing/Light Helicopters |

| eVTOL/Urban Air Mobility (UAM) |

| Aircraft Auxiliary Power Units (APUs) |

| Military and Defense |

| Commercial Aviation |

| General Aviation |

| UAV OEMs/Drone Operators |

| Research and Experimental |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Engine Type | Turbojet | ||

| Turboshaft | |||

| Turboprop | |||

| Turbofan | |||

| Recuperated/Regenerative | |||

| By Power Output Rating | Less than 30 kW | ||

| 30 to 60 kW | |||

| 60 to 90 kW | |||

| Greater than 90 kW | |||

| By Application | Unmanned Aerial Vehicles (UAVs) | ||

| Manned Light Fixed-Wing Aircraft | |||

| Rotary-Wing/Light Helicopters | |||

| eVTOL/Urban Air Mobility (UAM) | |||

| Aircraft Auxiliary Power Units (APUs) | |||

| By End User | Military and Defense | ||

| Commercial Aviation | |||

| General Aviation | |||

| UAV OEMs/Drone Operators | |||

| Research and Experimental | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the aircraft micro turbine market?

The aircraft micro turbine market stands at USD 3.97 billion in 2026 and is forecast to reach USD 5.23 billion by 2031.

Which engine configuration leads the market today?

Turboprop engines hold 37.42% of 2025 revenue, making them the dominant configuration.

Which application segment is expanding fastest?

Unmanned aerial vehicles are growing at an 8.10% CAGR through 2031 due to defense attritable programs and long-endurance commercial missions.

Why are hybrid-electric range extenders important for eVTOL aircraft?

Micro turbines acting as range extenders mitigate battery energy-density limits, tripling usable range while keeping vehicle weight within certification ceilings.

What is the biggest restraint hampering adoption?

High acquisition and maintenance costs—up to five times that of comparable piston engines—remain the principal barrier for cost-sensitive operators.

Which region will grow quickest over the next five years?

Asia-Pacific is projected to expand at a 7.32% CAGR, led by China’s indigenous turbine programs and India’s Make-in-India propulsion initiatives.

Page last updated on: