Commercial Aircraft Air Data Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.20 Billion |

| Growth Rate (2025 - 2030) | 5.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Air Data Systems Market Analysis by Mordor Intelligence

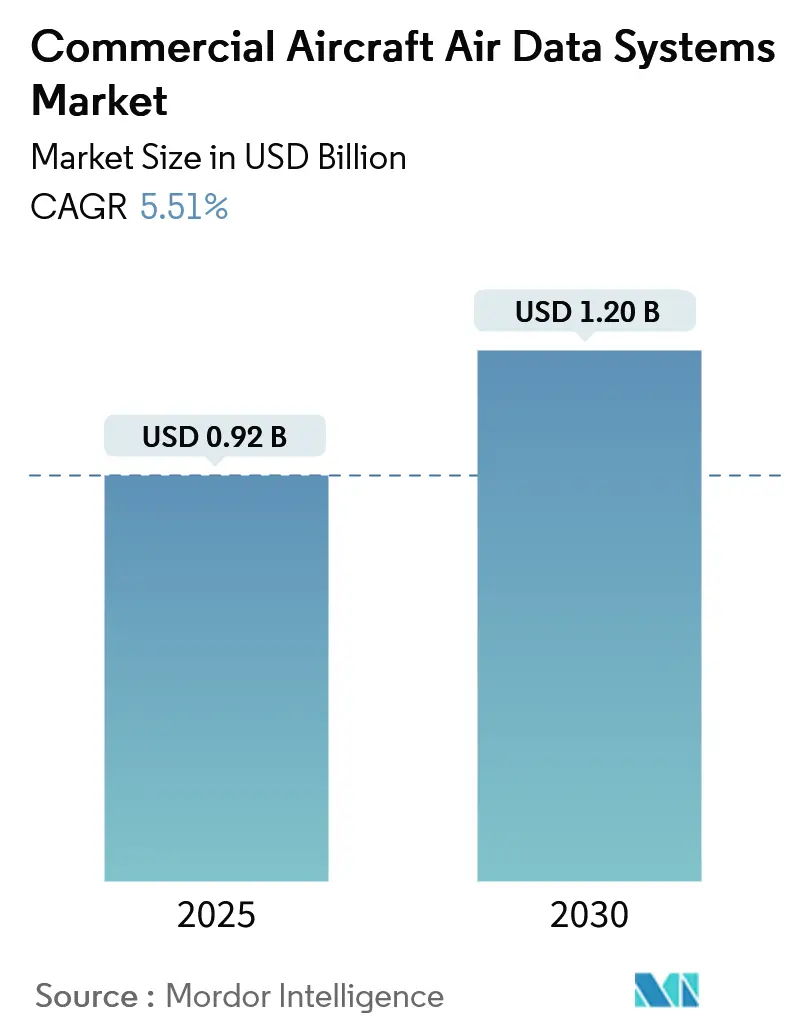

The Commercial Aircraft Air Data Systems Market size is estimated at USD 0.92 billion in 2025, and is expected to reach USD 1.20 billion by 2030, at a CAGR of 5.51% during the forecast period (2025-2030).

The Commercial Aircraft Air Data Systems Market size is estimated at USD 0.92 billion in 2025, and is expected to reach USD 1.20 billion by 2030, at a CAGR of 5.51% during the forecast period (2025-2030).

Air data systems are crucial in aircraft flight control, providing precise measurements across a broad spectrum of angles of attack and airspeed. The primary driver for the air data systems market is the surging global demand for new aircraft, both from commercial airlines and military forces. Moreover, heightened R&D investments to craft cutting-edge air data systems are poised to further bolster the market's trajectory.

Additionally, the growing adoption of next-generation technologies, such as artificial intelligence (AI), cloud computing, and real-time data monitoring, is driving the market's expansion. Companies in the air data system sector are consistently enhancing their offerings with the latest tech to meet evolving customer demands. A persistent challenge for manufacturers exists in crafting systems that efficiently handle diverse data types, formats, and structures.

Global Commercial Aircraft Air Data Systems Market Trends and Insights

The Commercial Segment is Expected to Dominate Market Share During the Forecast Period

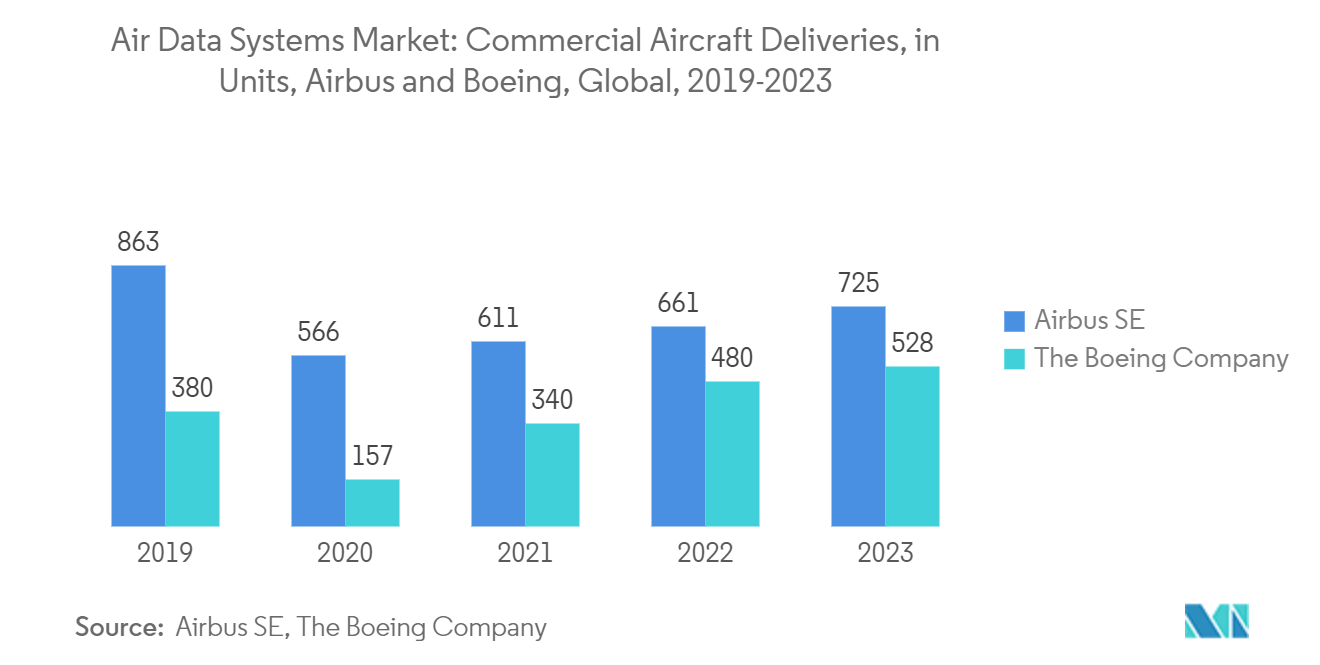

In recent years, air traffic has surged, fueling a heightened demand for new aircraft and bolstering expenditures in the aviation sector. The International Air Transport Association (IATA) projects global air travelers to hit 4 billion by 2024. Boeing's Commercial Market Outlook 2023-2042 forecasts a need for over 42,000 new commercial aircraft, encompassing both passenger and cargo planes, over the next two decades.

The commercial aviation sector, buoyed by a sharp uptick in air passenger traffic, saw robust growth. This surge translated into major order upticks for Airbus and Boeing, the industry's leading OEMs. In 2023, Airbus notched 735 global commercial aircraft deliveries and secured 2,094 new orders. Meanwhile, Boeing delivered 528 commercial airplanes. Notably, the recertification of the B737 MAX models reignited demand for this aircraft family. The market is poised for further growth with a rising number of new orders and increasing deliveries.

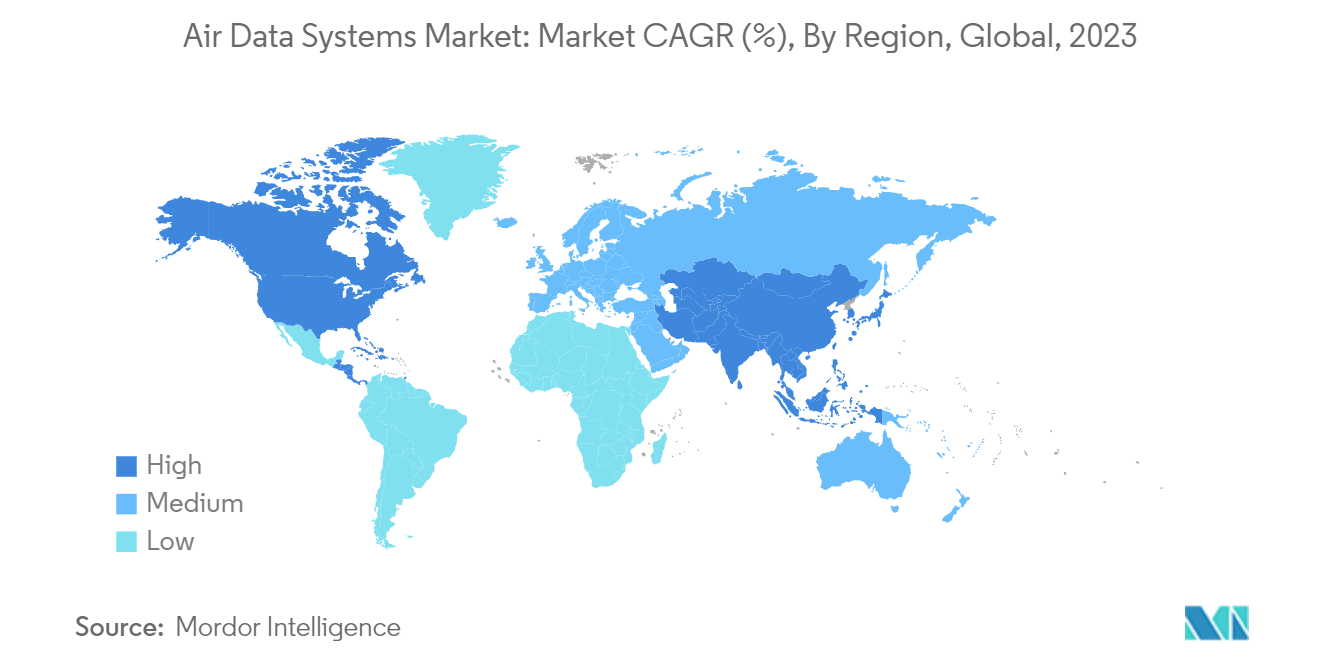

Asia-Pacific is Expected to Experience the Highest Growth During the Forecast Period

During the forecast period, Asia-Pacific is poised for significant growth, driven primarily by heightened procurement of commercial aircraft in nations such as China, India, Indonesia, Vietnam, and Thailand. Rising air traffic has compelled regional airlines to bolster their fleets with next-gen aircraft. For instance, in November 2022, seven leasing companies collectively inked a deal with the Commercial Aircraft Corporation of China (COMAC) for 300 new C919 planes and 30 ARJ21 aircraft.

Further underlining this trend, in December 2023, Tata group-owned Air India signed a contract with Airbus to purchase 140 A321neo, 70 A320neo, 20 A350-900, and 20 A350-1000 aircraft. For instance, China is investing heavily in advanced fighter aircraft, bolstering its AEW&C and bomber capabilities. Meanwhile, Japan is phasing out its aging F-4 fleet with substantial purchases of F-35A fighters. South Korea is diversifying its fleet with indigenous (KF-X) and foreign-made (F-35A) aircraft. This surge in aircraft procurement is fueling the demand for air data systems, further propelling the market's growth.

Competitive Landscape

The air data systems market is consolidated due to a few players holding significant shares. Some prominent players in the market are Honeywell International Inc., RTX Corporation, Curtiss-Wright Corporation, AMETEK Inc., and Meggitt Ltd.

Companies are investing significantly in the research and development of air data systems and are launching new products to increase their market share. Collins Aerospace, an RTX Corporation company, launched the latest SmartProbe Air Data Systems generation. It integrates sensing probes, pressure sensors, and powerful air data computer processing to provide all critical air data parameters, including pitot and static pressure, air, speed, altitude, angle of attack, and sideslip.

Commercial Aircraft Air Data Systems Industry Leaders

Honeywell International Inc.

RTX Corporation

Curtiss-Wright Corporation

AMETEK, Inc.

Meggitt Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Air India selected Collins Aerospace for a full suite of avionics hardware for its expanding B737 MAX fleet. Under the contract, the company would provide communication, navigation, surveillance equipment, and air data sensors to enhance Air India's fleet's safety, fuel efficiency, and operational performance.

- November 2023: Inertial Labs launched a new high-performing Inertial Navigation System (INS) that seamlessly integrates with other external sensors. Air Data Computer (ADC) calculates and provides air data parameters, including altitude, air speed, air density, outside air temperature (OAT), and windspeed for avionic applications.

Global Commercial Aircraft Air Data Systems Market Report Scope

Air data systems offer precise data on critical metrics like vertical speed, pressure altitude, and true airspeed, which are crucial for safe aircraft operation. Components like angle of attack (AOA), pilot-static probes, stall protection systems, and air temperature sensors form integral parts of these systems.

The air data systems market is segmented based on application, component, and geography. By application, the market is segmented into military and commercial. By component, the market is segmented into electronic units, probes, and sensors. The report also covers the market sizes and forecasts for the air data systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Commercial |

| Military |

| Electronic Units |

| Probes |

| Sensors |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East and Africa |

| Application | Commercial | |

| Military | ||

| Component | Electronic Units | |

| Probes | ||

| Sensors | ||

| Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Latin America | Brazil | |

| Rest of Latin America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Air Data Systems Market?

The Air Data Systems Market size is expected to reach USD 0.92 billion in 2025 and grow at a CAGR of 5.51% to reach USD 1.20 billion by 2030.

What is the current Air Data Systems Market size?

In 2025, the Air Data Systems Market size is expected to reach USD 0.92 billion.

Who are the key players in Air Data Systems Market?

Honeywell International Inc., RTX Corporation, Curtiss-Wright Corporation, AMETEK, Inc. and Meggitt Ltd. are the major companies operating in the Air Data Systems Market.

Which is the fastest growing region in Air Data Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Air Data Systems Market?

In 2025, the North America accounts for the largest market share in Air Data Systems Market.

What years does this Air Data Systems Market cover, and what was the market size in 2024?

In 2024, the Air Data Systems Market size was estimated at USD 0.87 billion. The report covers the Air Data Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Air Data Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: