City Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

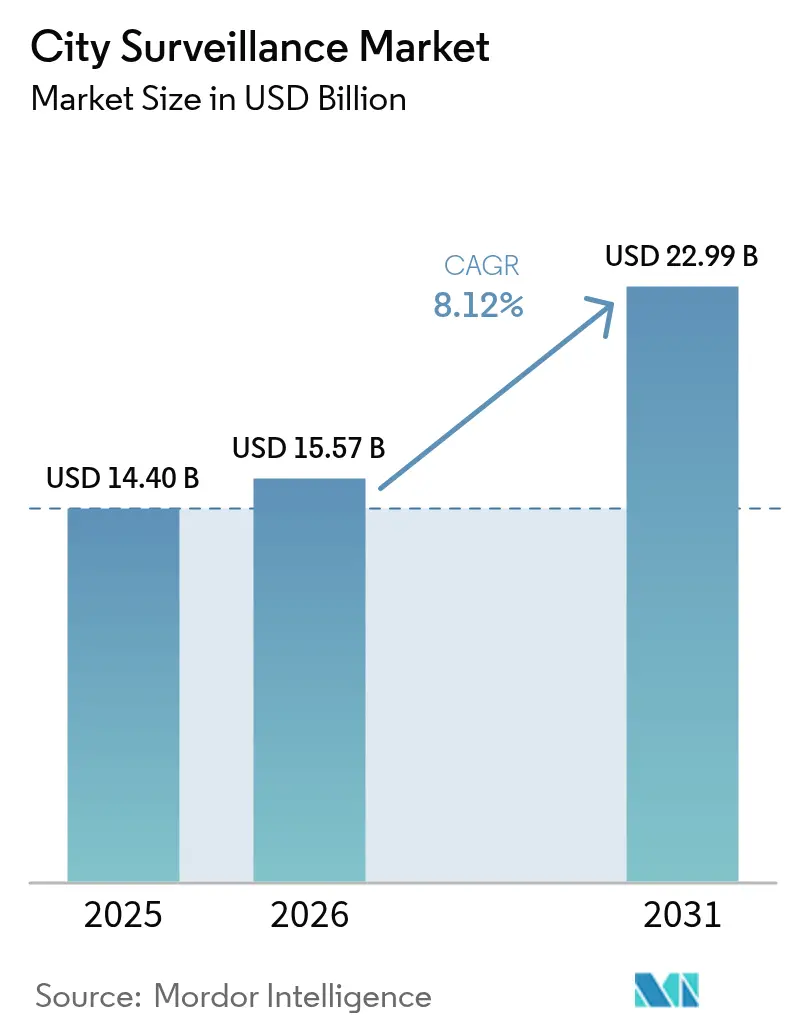

| Market Size (2026) | USD 15.57 Billion |

| Market Size (2031) | USD 22.99 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

City Surveillance Market Analysis by Mordor Intelligence

city surveillance market size in 2026 is estimated at USD 15.57 billion, growing from 2025 value of USD 14.40 billion with 2031 projections showing USD 22.99 billion, growing at 8.12% CAGR over 2026-2031. Rising allocations for integrated video networks, the sharp decline in IP camera prices, and the rapid maturation of edge analytics form the core growth engines that shape the current competitive dynamic of the city surveillance market. Mid-sized municipalities now justify capital outlays through measurable reductions in crime, lower incident response times, and new revenue streams from traffic violation enforcement. Vendors differentiate less on hardware specifications and more on cybersecurity, privacy compliance, and AI-led software ecosystems that convert video feeds into actionable insights. Partnerships between camera makers and cloud hyperscalers continue to expand the scope of solutions, while 5G adoption accelerates wireless deployments in dense, retrofit-intensive city cores.

Key Report Takeaways

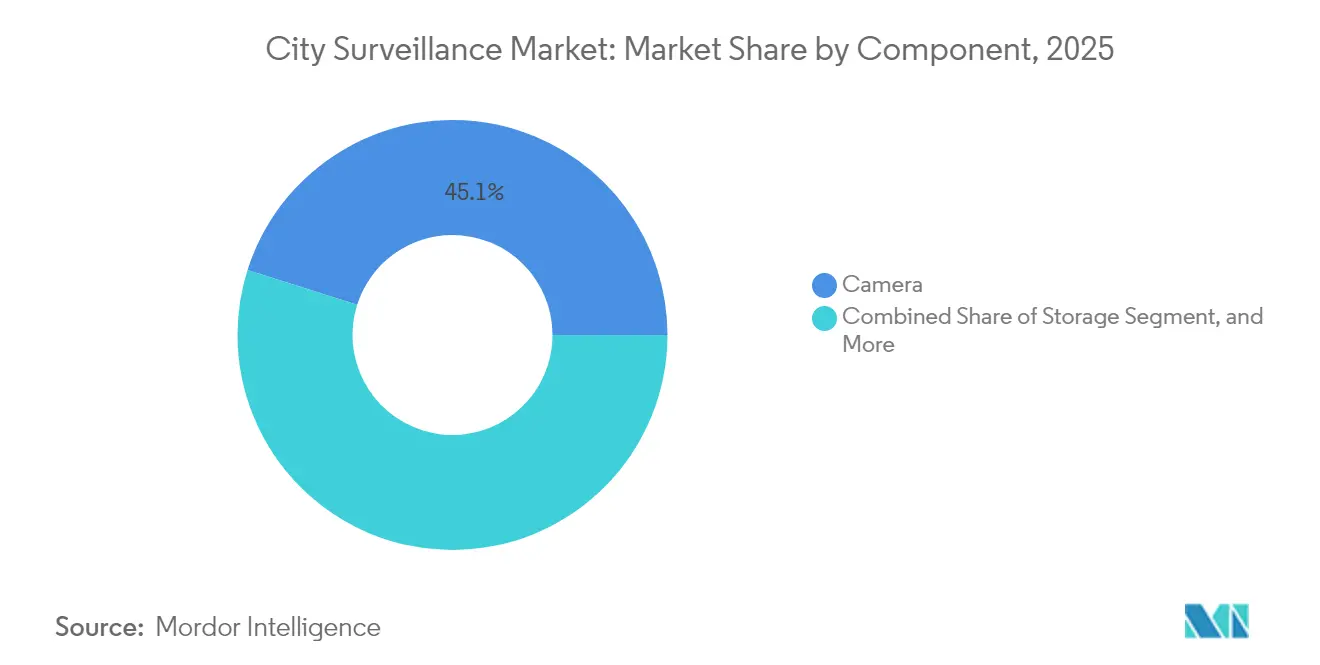

- By component, camera systems held a 45.12% share of the city surveillance market in 2025, while video analytics is forecast to advance at a 9.02% CAGR to 2031.

- By deployment mode, on-premise installations accounted for 61.74% of the city surveillance market size in 2025; cloud solutions are projected to record the highest CAGR of 9.29% through 2031.

- By camera connectivity, wired networks captured 66.10% of the city surveillance market share in 2025, whereas wireless nodes are projected to expand at a 9.74% CAGR between 2026-2031.

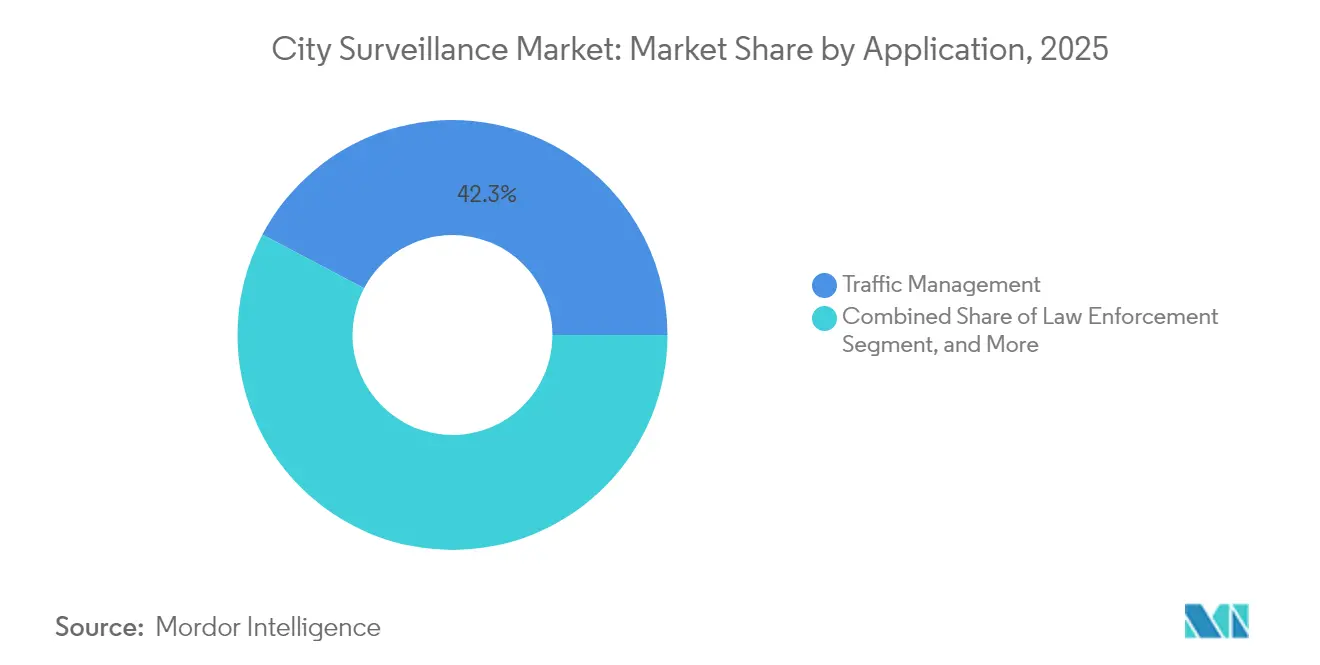

- By application, traffic management led with a 42.26% revenue share in 2025; public transportation hubs are poised for the fastest growth, with a 8.83% CAGR through 2031.

- By end user, municipal authorities commanded 38.21% of spending in 2025, while transportation agencies are projected to grow at a 8.96% CAGR to 2031.

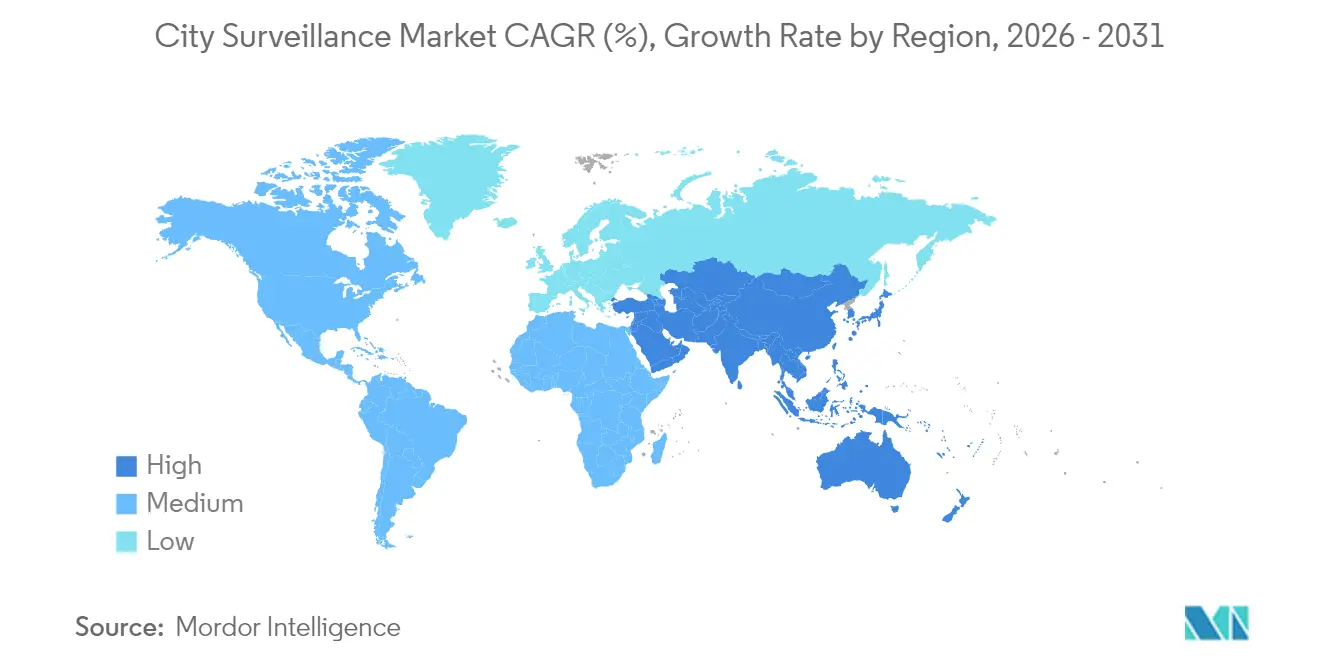

- By geography, Asia-Pacific contributed 35.05% of market revenue in 2025; the Middle East and Africa region is projected to register a 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global City Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Spending on Urban Security Infrastructure | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Declining IP Camera Prices and Enhanced Video Analytics | +1.8% | Global, particularly Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Growing Terrorism and Crime Concerns in Mega-Cities | +1.5% | Global urban centers, especially high-density metropolitan areas | Long term (≥ 4 years) |

| Expansion of Smart City Budgets for Integrated Surveillance | +1.4% | Asia-Pacific, Middle East, with selective North American cities | Medium term (2-4 years) |

| Edge AI Chips Cutting Bandwidth Costs | +1.0% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Smart Lighting Poles Embedding Camera Modules | +0.7% | Europe, North America, select Asia-Pacific cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Spending on Urban Security Infrastructure

Escalating crime and higher terrorism threat assessments prompted cities to earmark USD 3.2 billion for camera-network upgrades during 2024, with Detroit’s Project Green Light alone channeling USD 7 million toward integrated video feeds that link public and privately owned sites.[1]City of Detroit, “Project Green Light Expansion Program,” detroitmi.gov Similar budget expansions are visible in Barcelona, where EUR 50 million (USD 54.5 million) funded a camera grid that merges security, traffic flow, and environmental monitoring functions. Federal and regional grant programs, including the U.S. Community Oriented Policing Services, continue to de-risk large-scale procurements for municipalities that lack discretionary capital. The resulting demand pipeline favors platform vendors that supply end-to-end solutions and provide documented return-on-safety metrics, thereby reinforcing the growth trajectory of the city surveillance market.

Declining IP-Camera Prices and Enhanced Video Analytics

A component cost erosion of 15-20% per year has shifted procurement criteria from image resolution to embedded intelligence, enabling budget-constrained cities to deploy 4K cameras with on-device analytics. San Francisco achieved a 40% total cost of ownership reduction after migrating to edge-enabled units that automatically classify events and reduce storage requirements.[2]San Francisco Police Department, “Video Analytics Cost Reduction Report,” sanfranciscopolice.org As AI inference now executes on camera chipsets, municipalities capture real-time insights while trimming bandwidth loads by up to 90%. The affordability-intelligence nexus is expected to keep the city surveillance market on a robust expansion path through 2030.

Growing Terrorism and Crime Concerns in Mega-Cities

Global property and violent crime climbed 12% in 2024, with incidents heavily concentrated in metros housing over 1 million residents.[3]U.S. Department of Homeland Security, “Urban Security Threat Assessment 2024,” dhs.gov São Paulo’s 20,000-camera predictive-policing platform cut offenses in monitored districts by 18%, illustrating tangible benefits that justify expansion. Such data-backed successes persuade other mega-cities to allocate larger surveillance budgets, amplifying unit shipments and strengthening recurring-service revenue within the city surveillance market.

Expansion of Smart-City Budgets for Integrated Surveillance

Smart-city outlays totaled USD 189 billion in 2024, with surveillance systems receiving 8-12% of the pool as cities recognize video data as a foundation for multiple municipal services. Seoul’s USD 2.8 billion Digital New Deal anchors cameras as multipurpose sensors for public safety, traffic optimization, and disaster management. This multi-utility approach widens the buyer base and accelerates platform upgrades, reinforcing the long-term demand outlook across the city surveillance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Privacy Regulations and Public Opposition | -1.2% | Europe, North America, with emerging concerns in Asia-Pacific | Long term (≥ 4 years) |

| Rising Cybersecurity Vulnerabilities in IoT Cameras | -0.8% | Global, with acute impact in connected infrastructure deployments | Medium term (2-4 years) |

| Shortage of Skilled Video Analytics Personnel | -0.6% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Interoperability Gaps with Legacy Public Safety Systems | -0.4% | North America, Europe, mature markets with existing infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Privacy Regulations and Public Opposition

The European Union’s AI Act restricts real-time biometric identification, driving compliance costs that can add 20% to project budgets. GDPR enforcement actions against municipalities increased threefold in 2024, with an average fine of EUR 2.8 million (USD 3.05 million) for mishandling surveillance data. Citizen activism has delayed or canceled camera deployments in 15 major European cities, forcing local governments to apply privacy-by-design principles that lengthen roll-out timelines and limit feature sets, thereby tempering the growth of the city surveillance market.

Rising Cybersecurity Vulnerabilities in IoT Cameras

Reported firmware flaws affecting 2.3 million IP cameras in 2024 prompted Austin and Portland to pause expansion plans after data breaches exposed policing footage. The new European Cyber Resilience Act mandates now require security-by-design certification, which extends development cycles and raises vendor qualification hurdles. Municipal buyers are increasingly stipulating end-to-end encryption, regular vulnerability audits, and vendor-borne liability, all of which introduce procurement friction that can slow the adoption of city surveillance markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Analytics Drive Intelligence Revolution

Camera hardware accounted for 45.12% of city surveillance market revenue in 2025, affirming its status as the indispensable capture layer. Video analytics platforms, however, are projected to deliver a 9.02% CAGR, the fastest among components, as municipalities shift from passive recording to real-time intelligence. The city surveillance market size for video analytics is set to expand rapidly because on-device inference reduces bandwidth and storage costs while enhancing situational awareness.

Storage arrays face share erosion as edge analytics retains only critical metadata, curbing long-term archiving volumes. Software vendors differentiate through GDPR-compliant anonymization, automated redaction, and open APIs that integrate with traffic and environmental sensors. These attributes position analytics firms to command premium pricing and shape procurement criteria, reinforcing their emerging dominance within the city surveillance market.

By Deployment Mode: Cloud Adoption Accelerates

On-premise solutions controlled 61.74% of the city surveillance market share in 2025, reflecting legacy investments and a perception of greater data custody. Cloud deployments, however, are forecast to post a 9.29% CAGR, buoyed by elastic storage, automatic software updates, and lower lifecycle costs. Hybrid models bridge real-time local processing with cloud analytics, enabling large cities like Phoenix to store high-resolution footage for extended periods without expanding on-site hardware.

Regulatory stringency is paradoxically accelerating migration, as certified cloud providers offer encryption, audit trails, and compliance documentation that surpass most municipal IT budgets. As these concerns ease, the city surveillance market gains a fresh layer of recurring, software-as-a-service revenue, further diversifying vendor income streams.

By Camera Connectivity: Wireless Gains Momentum

Wired links dominated the market, accounting for 66.10% of revenue in 2025, particularly in greenfield infrastructure, where fiber is laid concurrently with other utilities. Wireless nodes, supported by 5G and low-power solar options, are projected to expand at a 9.74% CAGR, thanks to quick roll-outs in heritage districts where trenching is cost-prohibitive. The city surveillance market size for wireless cameras now expands not merely on convenience but also on resilience, as mesh topologies reroute data when individual nodes fail.

Municipalities deploy wireless units for temporary event security and rapid-response crime-hotspot coverage. Battery-assisted solar panels enhance operational autonomy, while remote firmware updates ensure cyber defenses remain current. These advantages ensure wireless connectivity will capture incremental share, particularly in the Middle East and Africa, where greenfield smart-city projects favor flexible infrastructure.

By Application: Transportation Security Leads Growth

Traffic-management solutions accounted for 42.26% of revenue in 2025, underpinning automated violation enforcement and congestion analytics that help cities recoup their camera investments through fines. Public transportation hubs are expected to rise at the fastest rate, with a 8.83% CAGR, as mass transit operators integrate passenger flow monitoring with threat detection. The city surveillance market size allocated to transit security continues to expand further with multimodal hubs seeking unified views across rail, bus, and metro assets.

Law enforcement applications increasingly harness AI to shift from reactive forensics to predictive patrolling, while critical infrastructure surveillance adds redundant cybersecurity overlays to protect energy and water assets. These developments illustrate how application diversity underpins the city surveillance market’s resilience across budget cycles.

By End User: Municipal Authorities Lead Investment

Municipal authorities represented 38.21% of spending in 2025 and will remain the anchor customer set through 2031. Transportation agencies, projected to grow at a 8.96% CAGR, recognize the operational gains from converging surveillance with fare-collection and asset-management data. The city surveillance market share for utilities also rises as power and water companies confront new physical-security mandates for grid resilience.

Police departments now partner with traffic and emergency services on unified video platforms, creating joint procurement pools that command volume discounts. Educational and healthcare institutions are increasingly connecting to municipal video networks, signaling a long-term trend toward regional surveillance grids that pool assets and analytics budgets.

Geography Analysis

The Asia-Pacific region dominated with 35.05% of 2025 revenue and is forecasted to grow at an 8.46% CAGR through 2031. China’s high-density urban surveillance programs and India’s USD 15 billion Smart Cities Mission anchor the region’s demand pipeline. Singapore’s Smart Nation initiative already interconnects 200,000 cameras with citywide analytics to manage traffic, crowd density, and environmental monitoring. Australia committed AUD 500 million (USD 335 million) in 2024 toward privacy-compliant transport hub security, while Japan’s aging population dynamics drive AI-based anomaly detection to assist emergency response.

North America recorded sustained upgrades, with U.S. municipalities allocating USD 3.2 billion for modernization in 2024. Federal infrastructure bills subsidize smaller cities, while Canadian metropolitan areas pilot hybrid-cloud deployments that meet local data-sovereignty requirements. Europe’s 7.84% projected CAGR reflects GDPR-driven equipment refresh cycles and the AI Act’s technical-compliance impetus. The city surveillance market size expansion across these mature regions is steadier but underpinned by mandatory cybersecurity and privacy overhauls. The Middle East and Africa are projected to record a 8.92% CAGR, powered by megaprojects such as Saudi Arabia’s NEOM and the UAE’s national digital-city programs. Qatar repurposes 2022 World Cup infrastructure into multi-agency surveillance grids, while Nigeria’s USD 200 million urban security outlay underscores the rising demand in sub-Saharan Africa. South America is experiencing emergent growth, as evidenced by Brazil’s USD 800 million smart-city commitments and Argentina’s integration of surveillance with 911-call centers. Currency volatility and procurement red tape temper volume but not strategic intent, signaling a gradual uptick in the city surveillance market.

Competitive Landscape

The five leading suppliers accounted for approximately 45% of global revenue in 2024, positioning the market at a moderate level of concentration. Regulatory curbs on Chinese brands in the U.S. and parts of Europe have created a white space for Axis Communications, Bosch, and Hanwha Vision, which emphasize GDPR conformity and cybersecurity hardening. Motorola Solutions’ 2024 acquisition of analytics specialist Calipsa strengthens its software stack, while Honeywell augments its video-management platform with cloud connectors and zero-trust security layers.

Edge-AI capabilities, encryption depth, and open-platform interoperability now serve as purchase triggers more than frame rate or pixel density. Cisco expands its smart-city platform to fold video feeds into IoT dashboards, competing head-to-head with Amazon Web Services in the municipal cloud segment. Analytics-only vendors enter via software-subscription models, challenging hardware-centric incumbents by decoupling intelligence from proprietary devices.

Strategic alliances intensify: Axis-Microsoft co-engineering, Genetec-Azure cloud pipelines, and Bosch-AWS data-lake optimizations highlight an ecosystem approach that reshapes buyer expectations. With vendor margins leaning increasingly toward services and recurring licenses, the city surveillance market is transitioning from unit-shipment competition to platform-lifecycle domination.

City Surveillance Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd.

Zhejiang Dahua Technology Co., Ltd.

Axis Communications AB (Canon Inc.)

Robert Bosch GmbH – Bosch Security and Safety Systems

Motorola Solutions, Inc. – Avigilon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Axis Communications entered a USD 200 million partnership with Microsoft Azure to build cloud-native surveillance platforms for smart cities. The joint solutions combine integrated AI analytics with GDPR-compliant data handling and aim to meet rising municipal demand for hybrid-cloud video networks.

- September 2025: Bosch Security Systems won a USD 180 million contract from the German Federal Ministry of Interior to modernize surveillance at 50 major transit hubs. The project relies on behavioral-analytics software and automated threat detection, marking the largest single surveillance upgrade so far in Europe under the EU AI Act.

- August 2025: Hanwha Vision acquired Israeli AI firm BriefCam for USD 150 million, adding real-time crowd-behavior and predictive-threat analytics to its municipal product portfolio. The deal sharpens Hanwha’s edge in the fast-growing video-analytics space.

- July 2025: Motorola Solutions committed USD 300 million to build a surveillance-camera plant in Poland that will employ 1,200 workers. The facility focuses on cybersecurity-hardened devices for European cities and helps buyers comply with the region’s Cyber Resilience Act while reducing reliance on Asian supply chains.

Global City Surveillance Market Report Scope

The city surveillance systems incorporate various hardware and software. Hardware systems include one or more IP cameras on a network that sends the captured video or audio information to a particular place. The captured images are live monitored or transmitted to a central location for recording and storage. Government agencies increasingly use these for monitoring, traffic management, and crime prevention. Some components of city surveillance systems covered in the study have been segmented by cameras, storage, video management systems, and video analytics. The market for the study defines the revenues generated from the sale and installation of city surveillance systems in various regions.

The City Surveillance Market is segmented by Component (Camera, Storage, Video Management System, Video Analytics) and Geography. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Camera |

| Storage |

| Video Management System |

| Video Analytics |

| On-Premise |

| Cloud |

| Hybrid |

| Wired |

| Wireless |

| Traffic Management |

| Law Enforcement |

| Critical Infrastructure Protection |

| Public Transportation Hubs |

| Other Application |

| Municipal Authorities |

| Police Departments |

| Transportation Agencies |

| Utilities |

| Other End User |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Camera | ||

| Storage | |||

| Video Management System | |||

| Video Analytics | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Camera Connectivity | Wired | ||

| Wireless | |||

| By Application | Traffic Management | ||

| Law Enforcement | |||

| Critical Infrastructure Protection | |||

| Public Transportation Hubs | |||

| Other Application | |||

| By End User | Municipal Authorities | ||

| Police Departments | |||

| Transportation Agencies | |||

| Utilities | |||

| Other End User | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the global city surveillance market in 2026?

The city surveillance market size stands at USD 15.57 billion in 2026.

What is the projected CAGR for city-wide surveillance spending through 2031?

Spending is forecast to rise at an 8.12% CAGR between 2026 and 2031.

Which region currently leads city-camera deployments?

Asia-Pacific holds 35.05% of revenue, the largest regional share.

Which application segment is growing fastest?

Surveillance for public transportation hubs is projected to advance at a 8.83% CAGR.

What deployment model is gaining traction over on-premise setups?

Cloud-based and hybrid deployments together form the fastest-growing approach, with cloud alone forecast at a 9.29% CAGR.

Which regulatory trend most affects future camera roll-outs in Europe?

Which regulatory trend most affects future camera roll-outs in Europe?

Page last updated on: