Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The United States Surveillance Analog Camera Market is Segmented by Camera Type (Bullet Cameras, Dome Cameras, and More), Technology (Thermal/Infrared Analog Cameras, Standard Definition, and More), Resolution (<2 Megapixel, 2–5 Megapixel, and More), and by End-User Industry (Government, BFSI, Healthcare, Transportation and Logistics, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

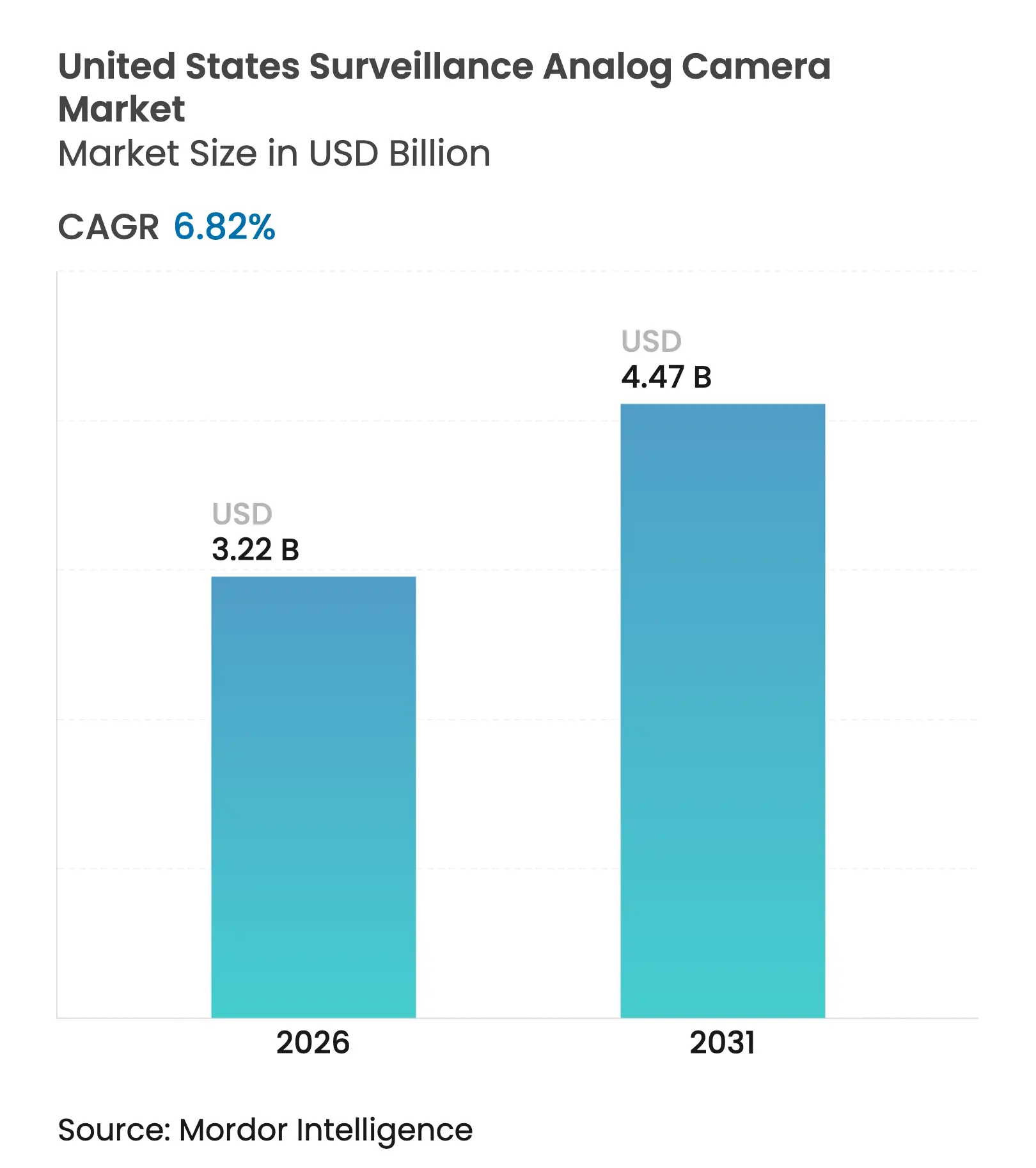

| Market Size (2026) | USD 3.22 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 6.82 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The United States Surveillance Analog Camera market size is expected to grow from USD 3.01 billion in 2025 to USD 3.22 billion in 2026 and is forecast to reach USD 4.47 billion by 2031 at 6.82% CAGR over 2026-2031. Sustained demand stems from federal facilities, municipal buildings, and small businesses that continue to rely on coaxial cabling, making incremental upgrades more economical than full IP replacements. Regulatory carve-outs under NDAA Section 889 have also redirected procurement toward domestically produced or approved models, underpinning revenue visibility for compliant manufacturers. [1]National Defense Industrial Association, “Section 889,” ndia.orgAt the same time, state cannabis-security mandates and hybrid DVR deployments among retailers are widening the addressable base for HD-over-Coax solutions. Energy-efficiency codes in coastal states and CHIPS-Act-related component shortages pose short-term headwinds, yet the operational simplicity, low-latency video, and lower total cost of ownership of analog deployments keep the value proposition intact for many end-users.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Persistence of Legacy Coaxial Infrastructure in Federal & Municipal Buildings Persistence of Legacy Coaxial Infrastructure in Federal & Municipal Buildings | +2.1% | National, with concentration in Washington D.C., state capitals, and major metropolitan areas | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:National, with concentration in Washington D.C., state capitals, and major metropolitan areas | Impact Timeline:Medium term (2-4 years) |

State Cannabis-Security Compliance Mandates Driving HD-over-Coax Adoption State Cannabis-Security Compliance Mandates Driving HD-over-Coax Adoption | +1.8% | States with legalized recreational cannabis (California, Colorado, Washington, Oregon, Nevada, etc.) | Short term (≤ 2 years) | |||

NDAA Section 889 Carve-outs Sustaining Analog Deployments in Critical Infrastructure NDAA Section 889 Carve-outs Sustaining Analog Deployments in Critical Infrastructure | +1.5% | National, with emphasis on federal facilities and critical infrastructure | Medium term (2-4 years) | |||

Hybrid DVR Upgrades Among U.S. SMB Retailers Seeking Low-Capex Video Analytics Hybrid DVR Upgrades Among U.S. SMB Retailers Seeking Low-Capex Video Analytics | +1.2% | National, with concentration in retail corridors of major metropolitan areas | Short term (≤ 2 years) | |||

Rising Copper Scrap Values Incentivizing Telco Re-use of Coax for Surveillance Rising Copper Scrap Values Incentivizing Telco Re-use of Coax for Surveillance | +0.9% | National, with emphasis on regions with extensive telecommunications infrastructure | Medium term (2-4 years) | |||

Analog Thermal Cameras for Remote Utility Substations with Limited Bandwidth Analog Thermal Cameras for Remote Utility Substations with Limited Bandwidth | +0.7% | National, with concentration in rural areas and regions with extensive utility infrastructure | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Persistence of Legacy Coaxial Infrastructure in Federal & Municipal Buildings

Large inventories of coaxial cabling installed before 2010 keep retrofit costs attractive, because rewiring a single drop can exceed USD 250, turning wholesale IP migration into a capital-intensive undertaking.[2]U.S. Department of Homeland Security, “CCTV Technology Handbook,” dhs.govBudget constraints direct facility managers toward NDAA-compliant DVRs such as Digital Watchdog’s VMAX A1 G4, which pushes 5-megapixel video over existing lines while layering AI analytics. These solutions extend asset life and defer disruptive construction work, supporting stable procurement pipelines through at least 2028.

State Cannabis-Security Compliance Mandates Driving HD-over-Coax Adoption

Recreational-use states obligate growers and retailers to archive continuous high-definition footage—examples include 45-day retention in Washington and 40 days in Colorado. HD-over-Coax cameras meet these thresholds at 30–40% lower capex than network upgrades, accelerating purchases among the 24 jurisdictions that now allow adult use. Rapid facility build-outs prioritize systems that can be installed within existing walls, positioning analog vendors as first-call suppliers.

NDAA Section 889 Carve-outs Sustaining Analog Deployments in Critical Infrastructure

The federal ban on certain Chinese surveillance brands has reshuffled sourcing patterns toward American and European manufacturers able to certify NDAA compliance. Approved analog portfolios from Pelco and Arecont Vision carry premium pricing yet face limited competition, cushioning margins. Critical infrastructure sites receive exemptions permitting phased replacements, creating an annuity-like revenue stream for compliant analog lines.

Hybrid DVR Upgrades Among U.S. SMB Retailers Seeking Low-Capex Video Analytics

Retailers require loss-prevention analytics without incurring full IP conversion costs. Hybrid DVRs integrate both analog and IP feeds and cost roughly 30% less than network-only solutions. They also unlock business intelligence features such as queue length monitoring, aligning security investments with merchandising outcomes, and improving return on capital.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

State & City Energy-Efficiency Codes Favoring PoE IP Cameras State & City Energy-Efficiency Codes Favoring PoE IP Cameras | -1.2% | California, New York, Massachusetts, and other states with stringent energy codes | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.2% | Geographic Relevance:California, New York, Massachusetts, and other states with stringent energy codes | Impact Timeline:Medium term (2-4 years) |

CHIPS-Act-Driven CCD Sensor Supply Shortages for Analog Cameras CHIPS-Act-Driven CCD Sensor Supply Shortages for Analog Cameras | -0.8% | National | Short term (≤ 2 years) | |||

FCC Entity List Bans Creating OEM Channel Disruptions FCC Entity List Bans Creating OEM Channel Disruptions | -0.6% | National, with particular impact on cost-sensitive market segments | Short term (≤ 2 years) | |||

Insurance Underwriters Elevating Minimum Resolution Standards to 1080p/4K Insurance Underwriters Elevating Minimum Resolution Standards to 1080p/4K | -0.5% | National, with emphasis on commercial and industrial applications | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

State & City Energy-Efficiency Codes Favoring PoE IP Cameras

Aggressive building-performance standards in California, New York, and Massachusetts increasingly reward low-power PoE cameras capable of Wake-on-Motion, trimming consumption by up to 30%. Traditional analog hardware uses discrete power supplies and typically exceeds emerging thresholds, pressuring public-sector bids toward IP. This regulatory push is expected to intensify as more states adopt the International Code Council’s guidance. [3]International Code Council, “Building Safety and Security Report,” iccsafe.org

CHIPS-Act-Driven CCD Sensor Supply Shortages for Analog Cameras

Fabrication capacity has shifted toward advanced nodes, squeezing the supply of mature-node CCD sensors essential for analog lines. The Semiconductor Industry Association notes that parts priced at USD 3 in 2024 have climbed 15–25%, eroding the price gap between analog and entry-level IP alternatives. [4]Semiconductor Industry Association, “Section 301 Legacy Investigation Comments,” semiconductors.orgAlthough domestic fabs funded by the CHIPS Act will add output, the lag is creating near-term procurement risk.

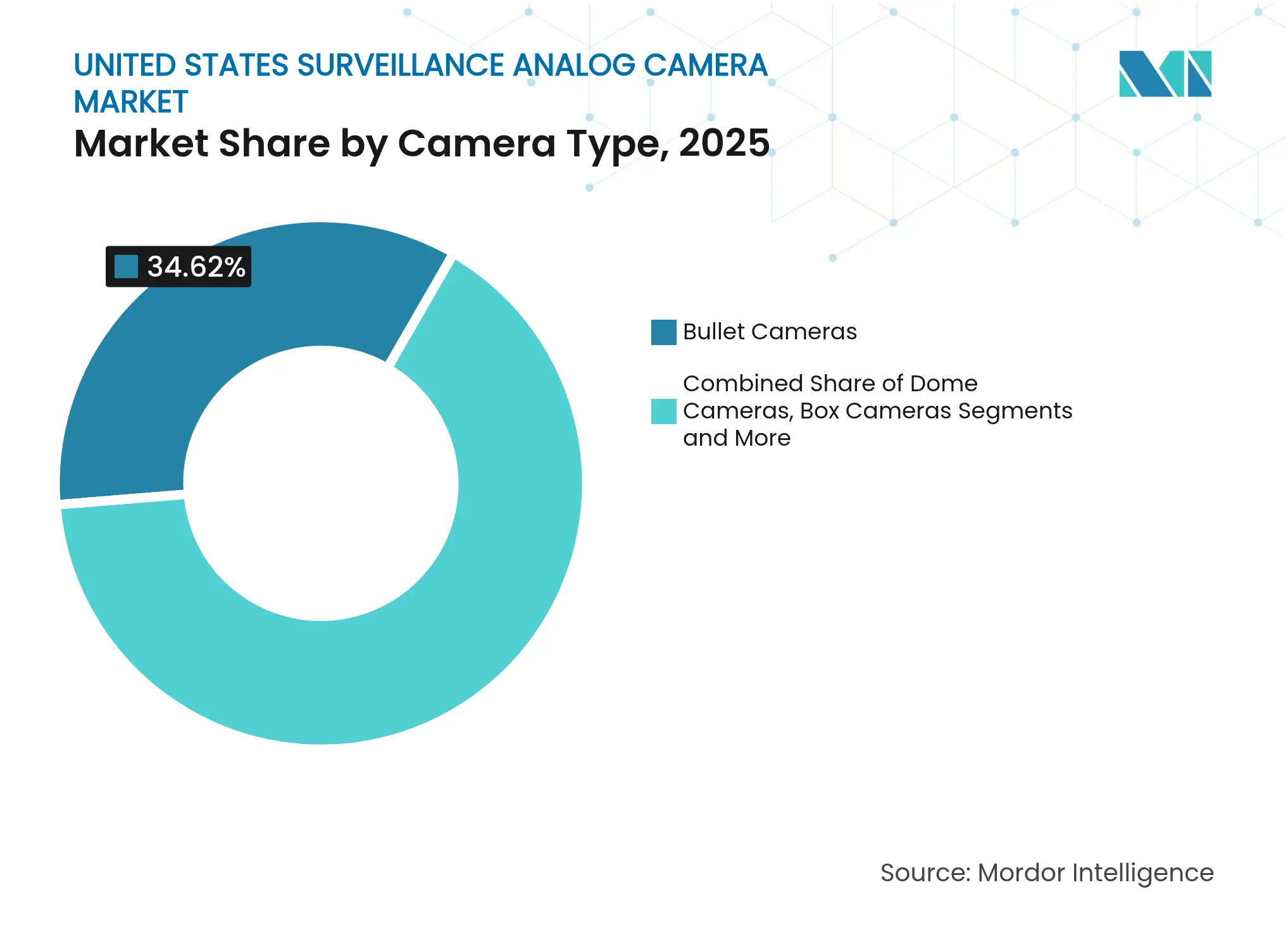

By Camera Type: PTZ Drives Premium Segment Growth

Bullet Cameras holds a 34.62% share of the United States Surveillance Analog Camera market. PTZ demand is climbing rapidly due to operator-controlled zoom and tracking that enable wider coverage with fewer endpoints. These features are prized by critical-infrastructure operators who must survey expansive zones and by retailers looking to counter organized retail crime. Vendors are integrating auto-tracking algorithms and starlight sensors, blurring the feature gap with IP devices.

PTZ’s 9.25% CAGR exceeds the overall United States Surveillance Analog Camera market because its functionality supports proactive incident response rather than passive monitoring. Bullet and dome formats, while lower-cost, are evolving through higher resolutions and vandal-resistant housings. Thermal variants employing metalens technology detect temperature anomalies and small gas leaks at five meters with a 0.2 sccm threshold. Covert units are penetrating loss-prevention programs where discretion is pivotal. This variety illustrates customer inclination to match form factor to risk profile instead of defaulting to the lowest price.

Note: Segment shares of all individual segments available upon report purchase

By Technology: HD Analog Maintains Market Leadership

HD Analog platforms captured 39.58% of the United States Surveillance Analog Camera market share in 2025 because they deliver 1080p video over legacy cabling. These deployments mitigate downtime and permit night-time changeovers, a critical advantage in 24-hour operations. AHD, HD-CVI, and HD-TVI protocols all support 500-meter runs without repeaters, preserving signal integrity in sprawling campuses.

Adoption of 4K/Ultra-HD solutions will accelerate at 7.12% CAGR as retailers and casinos require pixel density for facial recognition and license-plate analytics. Theia Technologies estimates compliance standards will soon stipulate 250 pixels per meter for positive identification. Standard-definition systems are relegated to budget-sensitive or non-critical zones. Thermal lines remain vital for perimeter and industrial monitoring where visibility is poor and early fire detection is mission-critical. The technology mix shows that the United States Surveillance Analog Camera market balances cost pragmatism with incremental innovation.

By Resolution: Higher Megapixel Cameras Gain Traction

Cameras in the 2–5 MP band represent 49.35% of share in the market share, providing clear imagery while limiting storage overhead. Hybrid DVRs can accommodate these bitrates without forklift-upgrading hard drives, easing adoption in small businesses. Coram AI pegs price premiums for 4K units at 30–50% versus 5 MP models, yet that spread is tightening as volumes scale.

Sensors above 5 MP are advancing at an 7.54% CAGR because customer experience teams want to zoom digitally without losing clarity for analytics. Conversely, sub-2 MP devices linger only in ancillary corridors or rural perimeter fences where coverage matters more than identification. The transition toward richer data streams underpins the long-term relevance of storage and compression innovation, with H.265 expected to become standard across the United States Surveillance Analog Camera market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

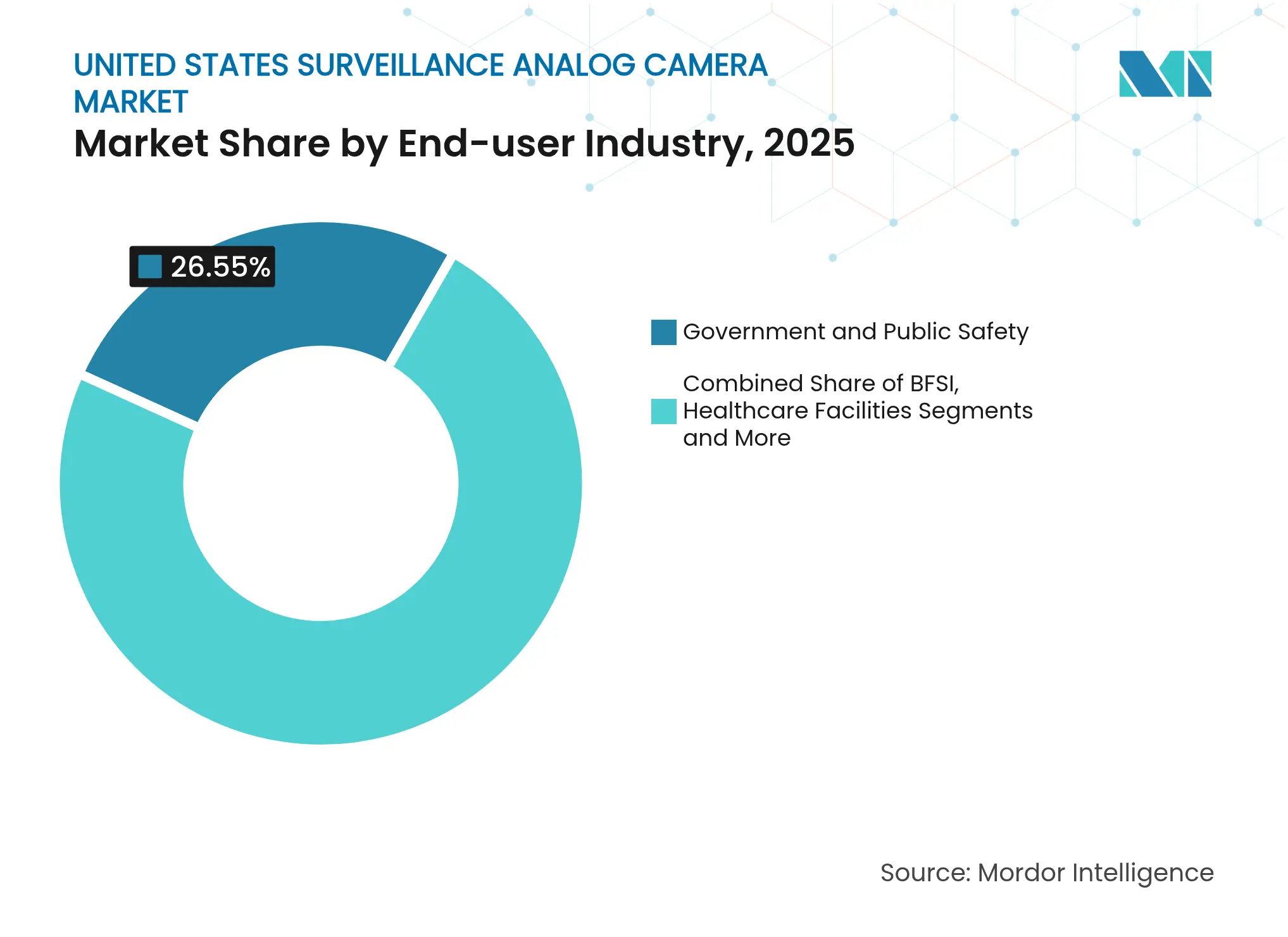

By End-user Industry: Retail Sector Drives Growth

Government and public safety facilities, accounting for 26.55% of the United States Surveillance Analog Camera market size in 2025, stick with analog due to entrenched coaxial networks and stringent procurement rules. Federal budgetary discipline favors phased upgrades that exploit existing wiring, a scenario amplified by the NDAA mandates that narrow the vendor pool.

Retail and hospitality will outpace all other verticals at an 8.18% CAGR. AI-ready hybrid recorders convert video into operational insights such as dwell time and staffing needs, repositioning surveillance from loss prevention to revenue enhancement. Banking, healthcare, and industrial users continue to value analog for its deterministic latency and minimal cyber-surface. Each vertical aligns camera mix, resolution, and firmware features with sector-specific compliance obligations, confirming that the United States Surveillance Analog Camera industry thrives on application specificity.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: E-commerce Disrupts Traditional Channels

Security distributors and VARs handle 59.12% of shipments, supplying engineering expertise and lifecycle services indispensable to federal and critical-infrastructure clients. Their bundled offerings reduce integration risk and compress deployment timelines. Direct manufacturer-integrator relationships secure large turnkey projects where tight coordination is essential.

Digital marketplaces are projected to capture an 7.86% CAGR as buyers grow comfortable configuring systems online and as logistics networks shorten delivery windows. Self-install kits for SMB customers include QR-code-based commissioning and cloud health checks, lowering service calls. Mass retailers and wholesale clubs serve the price-sensitive consumer micro-segment. The omnichannel shift compels legacy distributors to add value through design consultation and managed services to defend margins within the United States Surveillance Analog Camera market.

The Northeast combines mature infrastructure with financial-sector density, leading to steady retrofit volumes yet slower unit growth. Stringent energy regulations tilt new projects toward PoE, but historic properties often cannot justify rewiring costs, so compliant analog models continue to win bids in New York and Massachusetts.

The South and Southeast show the strongest unit momentum owing to population influx, large-format retail, and infrastructure expansion. Texas transportation specifications still reference analog interoperability requirements, reaffirming equipment viability for roadside and right-of-way deployments. Warm climates with high lightning incidence value the electrical isolation provided by coax.

The Western region presents mixed signals. California’s Title 24 codes disfavor high-wattage analog gear, while its cannabis sector stimulates HD-over-Coax demand because licensees must comply with stringent video quality and retention rules. Colorado mirrors this dynamic, creating a two-speed trajectory within the United States Surveillance Analog Camera market. The Midwest maintains balanced demand, using rugged analog units for agricultural and industrial monitoring where simplicity outweighs advanced analytics.

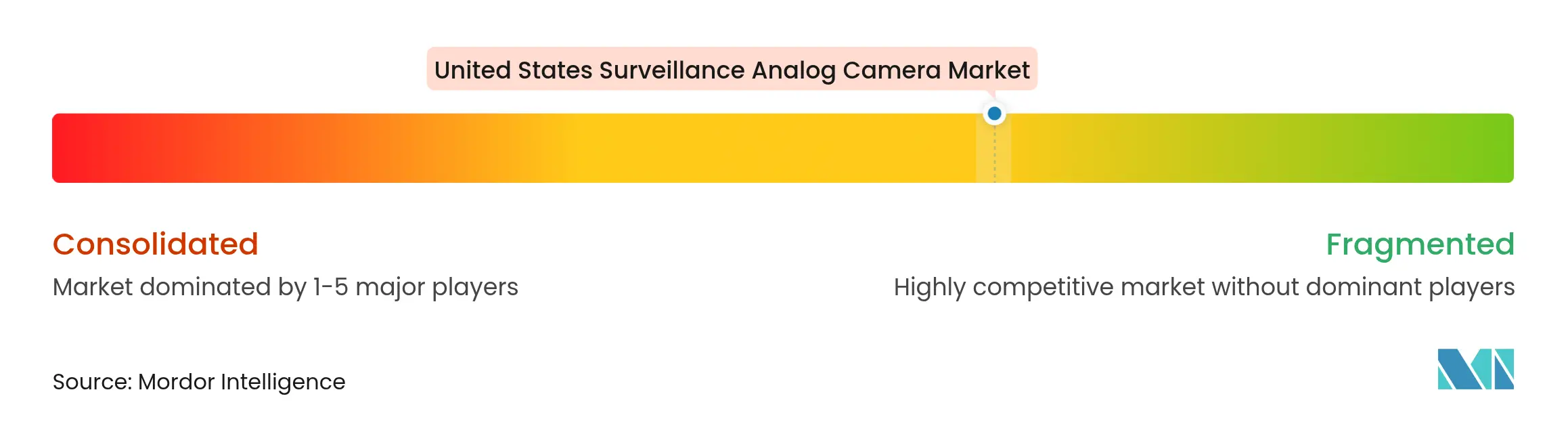

Market Concentration

Market structure is moderately fragmented. Johnson Controls, Bosch Security, and Pelco anchor the premium tier through NDAA-compliant portfolios, domestic manufacturing, and extensive integrator ecosystems. NDAA restrictions have sidelined Hikvision and Dahua from federal work, opening protective seams for mid-cap American brands.

Strategic moves revolve around vertical integration and analytics enablement. Bosch’s HD-over-Coax refresh incorporates edge analytics and H.265 streaming, narrowing the gap versus IP while preserving coax compatibility. Motorola Solutions’ acquisition of Avigilon’s analog assets broadens its public-safety platform, facilitating cross-selling of dispatch and command-center software. Johnson Controls is scaling domestic capacity by USD 75 million to de-risk supply chains and reduce lead times, an operations strategy that aligns with CHIPS-Act priorities.

Competitive intensity also migrates toward service models. Vendors bundle health-monitoring dashboards and firmware-lifecycle management to lock in annuity revenue and improve customer lifetime value. Niche innovators, including Teledyne FLIR and Hanwha Vision, address specialized needs from thermal perimeter defense to SMB channel reach. Overall, differentiation rests on compliance, analytics, and channel intimacy rather than pure hardware specs, reinforcing the evolving character of the United States Surveillance Analog Camera market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A surveillance analog camera is a security device that captures video footage in an analog format, typically transmitting signals over coaxial cables to a recording device or monitor. While they offer cost-effective solutions for basic security needs, analog cameras generally provide lower resolution compared to digital or IP cameras and have limited integration capabilities with advanced surveillance technologies.

The study tracks the revenue accrued through the sale of surveillance analog camera products by various players operating in the United States. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The US surveillance analog camera market is segmented by end-user industry (government, banking, healthcare, transportation & logistics, industrial, and other end-user Industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.