Airborne SATCOM Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.19 Billion |

| Market Size (2030) | USD 8.46 Billion |

| Growth Rate (2025 - 2030) | 6.45% CAGR |

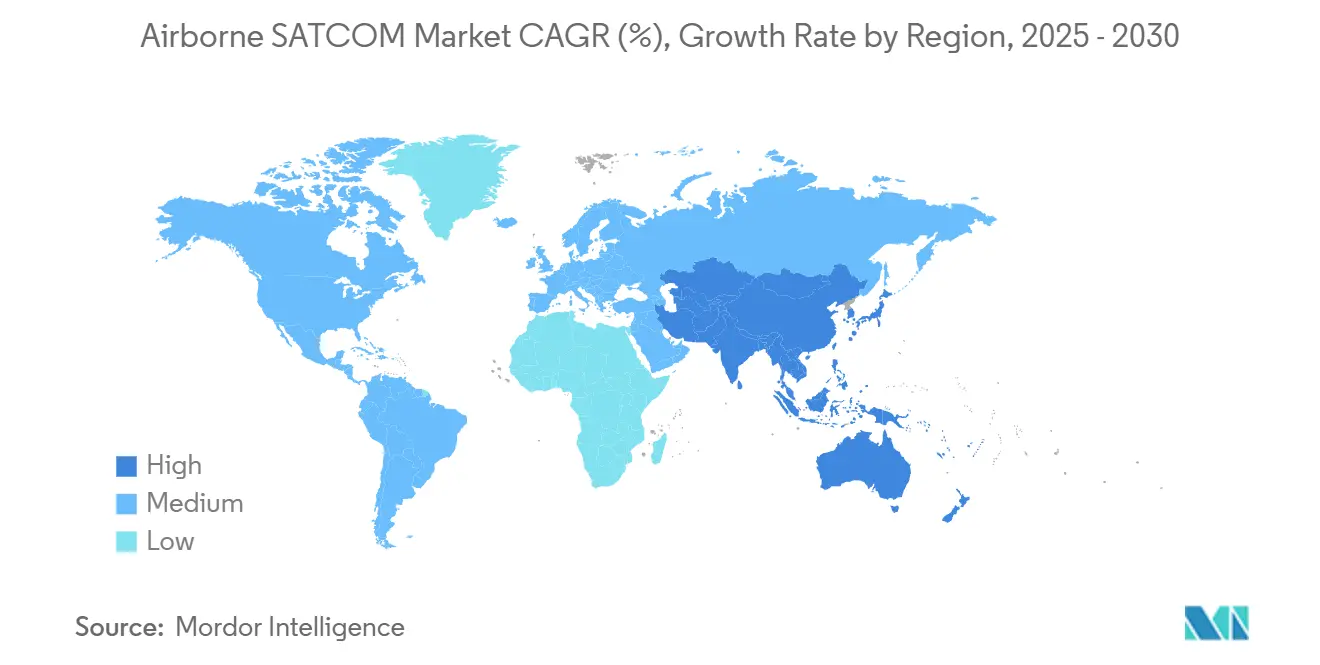

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

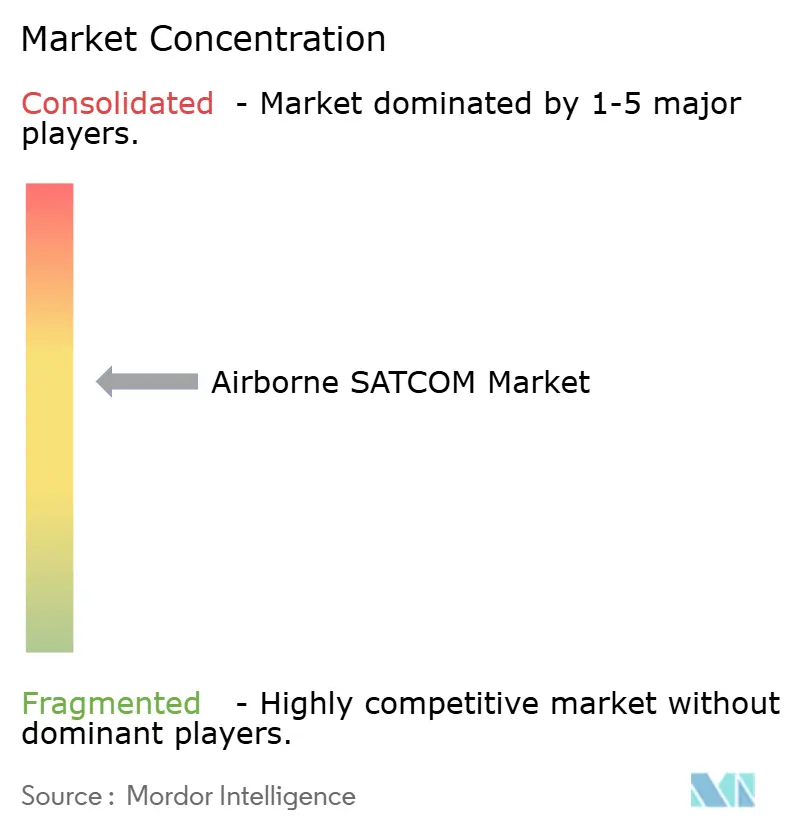

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airborne SATCOM Market Analysis by Mordor Intelligence

The airborne SATCOM market size is USD 6.19 billion in 2025 and is forecasted to reach USD 8.46 billion by 2030, reflecting a CAGR of 6.45%. Momentum stems from the accelerating adoption of multi-orbit connectivity that blends low-earth orbit (LEO), medium-earth orbit (MEO), and geostationary orbit (GEO) networks for high-throughput, low-latency service across commercial, military, and unmanned aircraft. Airlines prioritize passenger experience and operational data streams, while defense users demand jam-resistant, secure links that support multi-domain operations. Ongoing fleet renewal, International Civil Aviation Organization (ICAO) tracking mandates, and rapid unmanned aerial vehicle (UAV) deployment reinforce steady equipment retrofits and line-fits. Component suppliers benefit from software-defined radio (SDR) migration, which enables frequency-agile performance amid spectrum scarcity. Near-term headwinds include tight gallium-nitride (GaN) amplifier supply and elevated bandwidth costs. Yet, sustained investment in flat-panel antennas and network orchestration keeps the airborne SATCOM market on a solid growth trajectory.

Key Report Takeaways

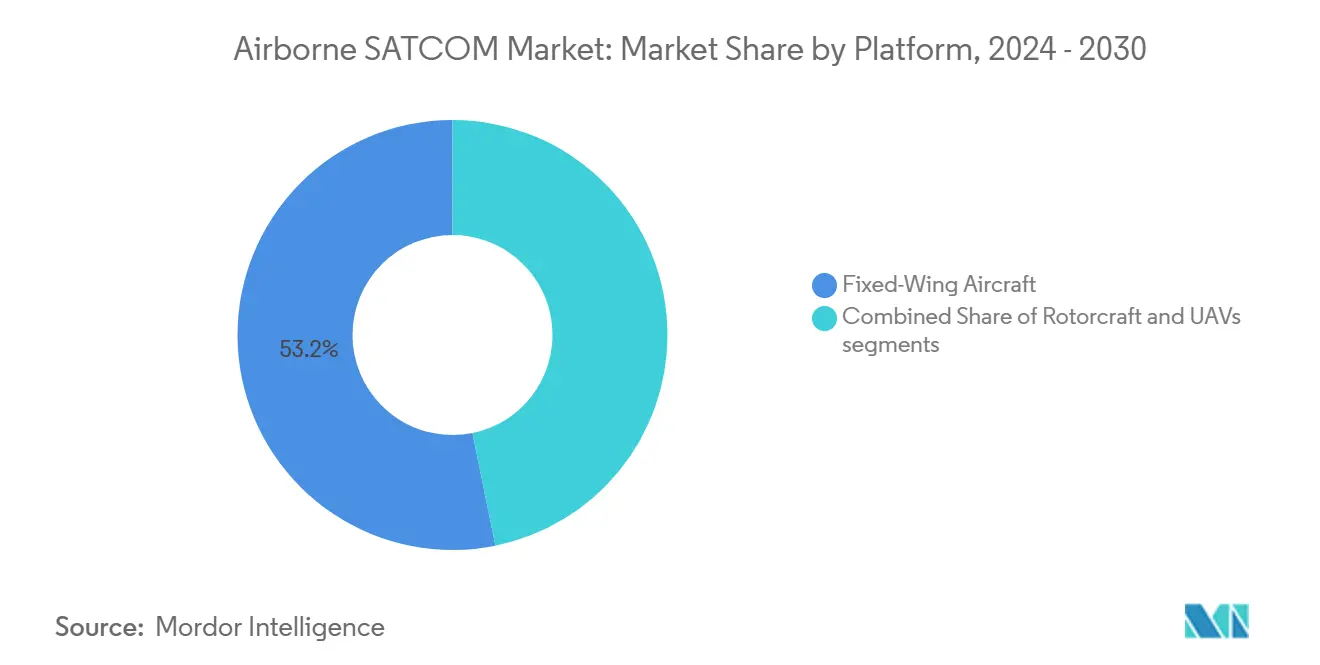

- By platform, fixed-wing aircraft held 53.20% of the airborne SATCOM market share in 2024, while UAVs advanced at a 9.32% CAGR through 2030.

- By component, transceivers commanded a 26.78% share of the airborne SATCOM market size in 2024; modems and routers posted the fastest 8.34% CAGR to 2030.

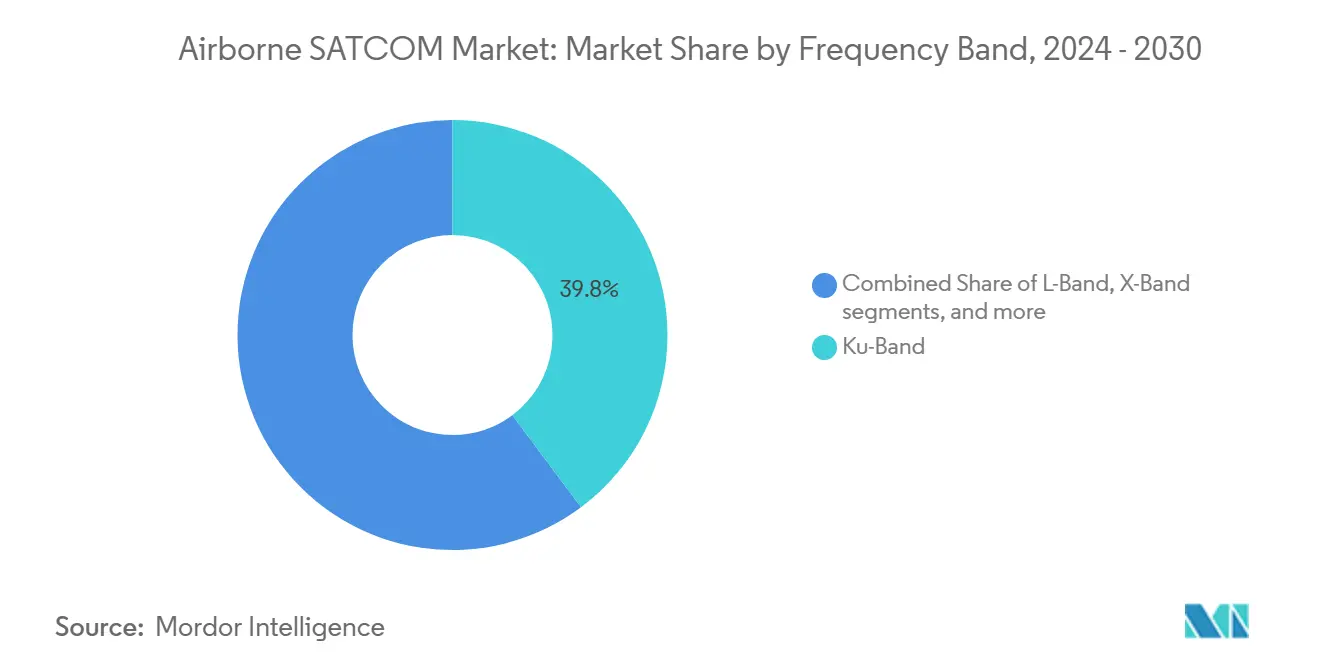

- By frequency band, Ku-band accounted for a 39.80% share of the airborne SATCOM market in 2024, whereas Ka-band led growth at a 9.74% CAGR.

- By installation type, new installations captured a 53.70% share of the airborne SATCOM market in 2024, and retrofit activity expanded at a 7.65% CAGR.

- By end user, government and defense represented a 58.30% share of the airborne SATCOM market in 2024; commercial operators recorded a 7.90% CAGR.

- By geography, North America contributed a 46.80% share of the airborne SATCOM market in 2024, while Asia-Pacific accelerated at an 8.90% CAGR.

Global Airborne SATCOM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for in-flight passenger connectivity | +1.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Fleet modernization across commercial and military aviation | +1.5% | Global, concentrated in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| UAV proliferation demanding BLOS SATCOM links | +1.2% | Global, led by North America and Europe defense markets | Medium term (2-4 years) |

| Shift to multi-orbit (LEO-MEO-GEO) hybrid networks | +1.0% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| AI-optimized flat-panel phased-array antennas | +0.7% | Global, technology leaders in North America and Asia-Pacific | Medium term (2-4 years) |

| ICAO's Global Aeronautical Distress and Safety System (GADSS) global tracking mandate | +0.5% | Global, with regulatory compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for In-Flight Passenger Connectivity

Airlines report that 73% of business travelers consider onboard internet essential, placing connectivity at the heart of post-pandemic service differentiation. Retrofit activity spans single-aisle and twin-aisle fleets as carriers seek uniform global coverage and consistent speeds. Hybrid multi-orbit architectures allocate bandwidth dynamically to manage cost while enhancing latency-sensitive applications. Panasonic Avionics validated LEO-GEO switching at 193 Mbps, proving commercially viable throughput.[1]Source: Panasonic Avionics, “Milestone in multi-orbit satellite connectivity testing,” MilitaryAerospace.com Operational benefits extend beyond passenger welfare, enabling real-time aircraft health monitoring, predictive maintenance, and optimized flight paths that lower fuel burn. As cabin Wi-Fi shifts from premium to baseline amenity, airlines accelerate forward-fit commitments with airframers to future-proof new deliveries.

Fleet Modernization Across Commercial and Military Aviation

Commercial airlines replace aging wide-bodies and regional jets, integrating lighter flat-panel antennas that cut drag and offer simpler maintenance. Military recapitalization programs embed software-defined terminals within avionics suites, safeguarding communications in contested airspace and enhancing multi-band agility. The US Department of Defense (DoD) Enterprise SATCOM strategy pushes procurements featuring anti-jamming and cyber protection. Weight, power, and space constraints guide avionics selection, favoring integrated line-replaceable units. Regulatory compliance with DO-160 and ARINC standards ensures global interoperability, supporting civil and defense applications. Combined commercial-military demand drives economies of scale, reducing unit prices and shortening innovation cycles.

UAV Proliferation Demanding BLOS SATCOM Links

Defense UAVs require uninterrupted high-bandwidth video and sensor streams for ISR missions beyond terrestrial radio range. Recent contracts exceeding USD 11 million underscore continuing military investment in secure, low-size, weight, and power (SWaP) terminals. Civil UAV operators in energy, agriculture, and logistics similarly seek cost-effective satellite backhaul as beyond visual line of sight (BVLOS) regulations mature. Technical progress centers on compact phased-array antennas and efficient power amplifiers that satisfy small airframe payload limits. Commercial LEO constellations offer lower latency and bandwidth pricing, expanding addressable missions. Market entrants with scalable terminal designs gain an edge as UAV fleets multiply across defense and commercial sectors.

Shift to Multi-Orbit (LEO-MEO-GEO) Hybrid Networks

Operators balance latency, throughput, and coverage by steering traffic among orbits via intelligent software controllers. Eutelsat began operational LEO-GEO aviation services in 2025 with over 100 certified antennas flying.[2]Source: Erica Marchand, “Eutelsat expands airborne internet with operational LEO service for aircraft,” SpaceDaily, spacedaily.com Integrated terminals negotiate seamless handoffs, sustaining virtual private network (VPN) sessions and streaming quality even during polar or equatorial crossings. Military users value orbit diversity for resilience against jamming or satellite outages. Network orchestration leverages AI to predict congestion and preempt handovers, maximizing spectral efficiency. Hybrid architectures reshape procurement criteria, rewarding vendors that deliver open-architecture modems and field-upgradable antennas.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and satellite bandwidth costs | -1.2% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Spectrum and airworthiness certification delays | -0.8% | Global, with regional regulatory variations | Short term (≤ 2 years) |

| Cyber-jamming/spoofing vulnerability | -0.6% | Global, heightened in contested regions | Long term (≥ 4 years) |

| GaN amplifier supply-chain tightness | -0.4% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Satellite Bandwidth Costs

Flat-panel antenna hardware can exceed USD 500,000 per aircraft, while monthly bandwidth fees vary widely by usage tier.[3]Source: Fusion Worldwide, “The Greensheet: December 2024,” fusionww.com Smaller carriers and charter operators face more extended payback periods, hindering adoption. Semiconductor shortages inflate modem and amplifier prices, prompting some airlines to defer upgrades. Vendors explore equipment-as-a-service models and performance-based contracts to ease capital constraints. Software-defined hardware promises future savings through over-the-air feature unlocks but requires upfront R&D investment. Until bandwidth unit costs trend lower through constellation scale-up, pricing pressure remains a meaningful brake on near-term growth.

Spectrum and Air-Worthiness Certification Delays

Next-generation terminals must clear electromagnetic compatibility and cybersecurity evaluations that can stretch 18–24 months under FAA or EASA oversight. Frequency coordination through ITU adds complexity for multi-orbit systems that straddle diverse allocations. Program delays elevate project risk and deter early adopters sensitive to entry-into-service windows. Efforts to streamline supplemental-type certificate processes and mutual recognition agreements may shorten cycle times, yet progress hinges on sustained regulator-industry collaboration. Vendors with pre-approved linefit offerings gain a competitive advantage, especially in fast-growing Asia-Pacific fleets seeking rapid deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: UAVs Advance Rapidly

Fixed-wing aircraft dominated the airborne SATCOM market share at 53.20% in 2024, underpinned by resilient commercial and military fleets. UAV demand, however, is projected to post a 9.32% CAGR through 2030, outpacing all other platforms as both defense and civilian operators seek continuous command links. The airborne SATCOM market size for UAVs benefits from compact, lightweight terminals that meet stringent SWaP thresholds yet support HD video and sensor data. Rotorcraft adoption revolves around SAR, offshore logistics, and medical evacuation missions where ground infrastructure is sparse.

Software-defined radios allow standard hardware across platforms, simplifying inventory and certification. Military UAV contracts, such as Gilat’s USD 11 million award, affirm sustained procurement cycles. Civil UAV use cases grow as regulators formalize BVLOS corridors, broadening addressable airframes. Suppliers capable of delivering scalable, ruggedized solutions that align with diverse payload limits and accelerate cross-platform penetration in the airborne SATCOM market.

By Component: Transceivers Anchor Software-Defined Evolution

Transceivers secured 26.78% of the airborne SATCOM market share in 2024, reflecting their central role in frequency-agile connectivity. Modems and routers exhibit an 8.34% CAGR to 2030 as onboard network management becomes more sophisticated. The airborne SATCOM market size associated with phased-array antennas climbs steadily as electronically steered designs replace mechanical dishes. Integrated terminals bundle RF front-ends, modems, and beam steering logic, reducing line-replaceable units and installation hours.

Open-architecture standards encourage lifecycle upgrades without wholesale replacement, a boon to retrofit programs. Supply-chain tightness in GaN power amplifiers influences sourcing strategies, with some OEMs qualifying dual suppliers to mitigate risk. The transition toward multi-band, software-defined solutions positions transceivers as pivotal enablers of hybrid orbit operation, cementing their leading share within the airborne SATCOM market.

By Frequency Band: Ka-Band Leads Throughput Race

Ka-band systems are forecast to advance at 9.74% CAGR, outpacing other frequency segments as airlines and defense agencies prioritize streaming video, cloud access, and high-rate ISR feeds. Ku-band will retain a 39.80% share of the airborne SATCOM market size in 2024, benefiting from dense satellite coverage and mature economics. L-band remains essential for backup and safety services, while X-band addresses specialized military requirements.

Multi-band antennas empower dynamic frequency selection, optimizing for latency, weather attenuation, and cost. Research prototypes demonstrate simultaneous multi-band phased-array operation, promising seamless handovers without mechanical elements. Regulatory spectrum auctions and ITU allocations will influence regional uptake, yet Ka-band’s capacity advantage keeps it the fastest-growing slice of the airborne SATCOM market.

By Installation Type: Retrofit Gains Momentum

New builds accounted for 53.70% of the airborne SATCOM market share in 2024 as OEMs delivered connectivity-ready airframes. Retrofit programs, however, clock a 7.65% CAGR as operators upgrade mid-life fleets to meet passenger and regulatory mandates. Modular, pre-wired kits minimize downtime and alleviate hangar capacity bottlenecks. The airborne SATCOM market size associated with retrofits grows as airlines extend service life beyond 10 years, deferring capex-heavy fleet replacement.

Turnkey integrators bundle equipment, STC engineering, and certification support, appealing to carriers lacking in-house modification teams. For defense fleets, retrofit offers cost-effective insertion of anti-jam features without grounding assets for prolonged periods. Supply-chain predictability and standardized interfaces remain critical success factors as retrofit demand broadens across aircraft categories.

By End User: Defense Remains Dominant

Government and defense users held 58.30% of the airborne SATCOM market share in 2024, reflecting sovereign imperatives for secure, resilient communication. Commercial aviation posted a 7.90% CAGR through 2030, driven by passenger connectivity and operational data analytics. The airborne SATCOM industry benefits from technology spillover, with commercial stakeholders adopting military-grade encryption and redundancy features.

Viasat’s USD 568 million contract illustrates defense commitment to tactical gateways and airborne terminals. Commercial airlines, meanwhile, leverage real-time EFB updates and predictive maintenance feeds to boost efficiency. Cross-sector convergence accelerates component cost reduction, yet ITAR restrictions and export controls continue to shape international collaborations within the airborne SATCOM market.

Geography Analysis

North America led the airborne SATCOM market with 46.80% share in 2024, buoyed by robust defense budgets, early multi-orbit adoption, and a large commercial fleet base. Suppliers benefit from clear FAA certification pathways and a dense network of teleports that enhance service quality. Defense modernization programs, including Next-Gen Jam-Resilient terminals, sustain volume for US primes and their partner ecosystem.

Europe follows with mature avionics manufacturing, stringent EASA standards, and growing airline retrofits focused on passenger experience. Multi-country defense initiatives, such as the EU’s IRIS² constellation, reinforce demand for interoperable terminals. Regional MRO hubs accelerate retrofit throughput, while national carrier alliances negotiate pooled bandwidth contracts to reduce per-aircraft costs.

Asia-Pacific exhibits the fastest 8.90% CAGR, driven by rising middle-class travel, rapid LCC expansion, and military modernization across Japan, South Korea, India, and Australia. Governments invest in domestic satellite constellations and ground segment infrastructure to strengthen strategic autonomy. Emerging Southeast Asian carriers prioritize flexible leasing models to overcome CAPEX barriers, while defense budgets allocate funds to ISR-capable UAVs requiring SATCOM backhaul. The Middle East and Africa encounter steady adoption tied to hub airport development and resource sector logistics. In contrast, South America sees a gradual uptake constrained by macroeconomic volatility yet supported by government connectivity initiatives in remote regions.

Competitive Landscape

The airborne SATCOM market demonstrates moderate consolidation anchored by diversified aerospace majors and focused connectivity specialists. Top players integrate antennas, modems, and managed services, leveraging long-term line-fit positions and defense relationships. Gogo’s USD 375 million purchase of Satcom Direct increases combined revenue to USD 890 million and broadens multi-orbit, multi-band offerings. Gilat’s USD 98 million acquisition of Stellar Blu enhances electronically steered antenna capabilities for business aviation and military fleets.

Technology differentiation centers on AI-optimized beam steering, cyber-secure waveforms, and open-architecture SDR platforms. Vendors race to certify LEO-enabled terminals, with Eutelsat and Panasonic Avionics fielding the first commercial installations in 2025. Supply-chain resilience, particularly for GaN devices, influences cost and delivery, prompting some suppliers to integrate amplifier production vertically.

White-space opportunities include direct-to-cell satellite links for logistical asset tracking and software-defined terminals that enable over-the-air feature unlocks. Competitive dynamics will evolve as additional LEO constellations achieve operational status and defense agencies scale demand for resilient, multi-orbit solutions. Companies that marry network services with certified airborne hardware stand to consolidate share within the airborne SATCOM market.

Airborne SATCOM Industry Leaders

Honeywell International Inc.

Thales Group

Viasat, Inc.

RTX Corporation

General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Avantel Limited secured a USD 1.15 million order from Hindustan Aeronautics Limited (HAL) for airborne satellite communication equipment. The technology solutions provider will supply HAL, a public-sector aerospace and defense company under India's Ministry of Defence (MoD), with indigenous Satcom systems.

- July 2024: Orbit Communication Systems Ltd. partnered with Viasat Inc. to develop advanced SATCOM multi-purpose terminals for airborne platforms. The collaboration includes engineering and supplying terminals integrating with Viasat's global Ka-band networks, enhancing connectivity management across satellite networks. Orbit plans to develop next-generation airborne SATCOM systems that integrate with Viasat's global Ka-band networks, including the ViaSat-3 and Global Xpress (GX) networks. These systems will be compatible with military Ka-band HCX steerable beams and designated WGS-ready terminals. The MPT systems will enable network consolidation with seamless switching capabilities.

Global Airborne SATCOM Market Report Scope

| Fixed-Wing Aircraft | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| General Aviation | Business Jets | |

| Piston and Turbo Aircraft | ||

| Military Aviation | Fighter Jets | |

| Transport Aircraft | ||

| Special Mission Aircraft | ||

| Others | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| SATCOM Terminals |

| Transceivers |

| Airborne Radio |

| Modems and Routers |

| SATCOM Radomes |

| L-Band |

| X-Band |

| Ku-Band |

| Ka-Band |

| Multi-Band/Others |

| New Installation |

| Retrofit |

| Government and Defense |

| Commercial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Fixed-Wing Aircraft | Commercial Aviation | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| General Aviation | Business Jets | ||

| Piston and Turbo Aircraft | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Special Mission Aircraft | |||

| Others | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Component | SATCOM Terminals | ||

| Transceivers | |||

| Airborne Radio | |||

| Modems and Routers | |||

| SATCOM Radomes | |||

| By Frequency Band | L-Band | ||

| X-Band | |||

| Ku-Band | |||

| Ka-Band | |||

| Multi-Band/Others | |||

| By Installation Type | New Installation | ||

| Retrofit | |||

| By End User | Government and Defense | ||

| Commercial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the airborne SATCOM market?

The airborne SATCOM market size is USD 6.19 billion in 2025 and is forecast to reach USD 8.46 billion by 2030, reflecting a CAGR of 6.45%.

Which platform segment is growing the fastest?

UAVs record a 9.32% CAGR through 2030 as both defense and commercial operators expand autonomous missions.

Why is Ka-band attracting attention?

Ka-band offers higher capacity and advances at 9.74% CAGR, ideal for passenger internet and data-intensive ISR feeds.

How significant is the defense sector in this market?

Government and defense users command 58.30% share, underscoring their priority for secure, resilient communication links.

What is driving retrofit demand?

Airlines and militaries upgrade in-service aircraft to meet connectivity mandates, fueling a 7.65% CAGR for retrofit installations.

Which region is expected to grow the quickest?

Asia-Pacific posts an 8.90% CAGR to 2030, propelled by commercial fleet expansion and regional defense modernization.

Page last updated on: