Airborne Countermeasure System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

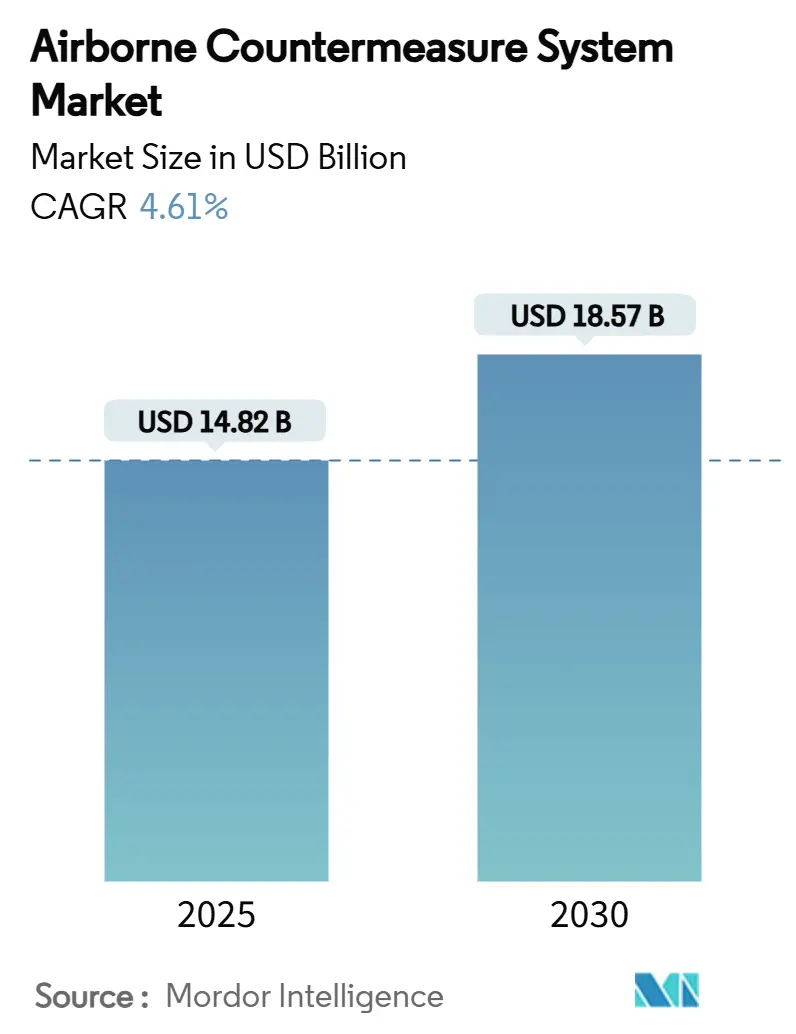

| Market Size (2025) | USD 14.82 Billion |

| Market Size (2030) | USD 18.57 Billion |

| Growth Rate (2025 - 2030) | 4.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airborne Countermeasure System Market Analysis by Mordor Intelligence

The airborne countermeasure system market size reached USD 14.82 billion in 2025 and is forecast to climb to USD 18.57 billion by 2030, reflecting a 4.61% CAGR. Growth stems from sustained investment in electronic warfare, rising integration of software-defined radios, and the move toward modular open-system architectures that simplify upgrades. North American modernization programs and Asia-Pacific force expansions underpin demand, while rapid adoption of artificial intelligence (AI) algorithms is reshaping threat-response cycles. Program backlogs at leading prime contractors suggest steady medium-term revenue visibility; however, supply-chain fragility surrounding specialty semiconductors and gallium compounds continues to loom over production schedules.

Key Report Takeaways

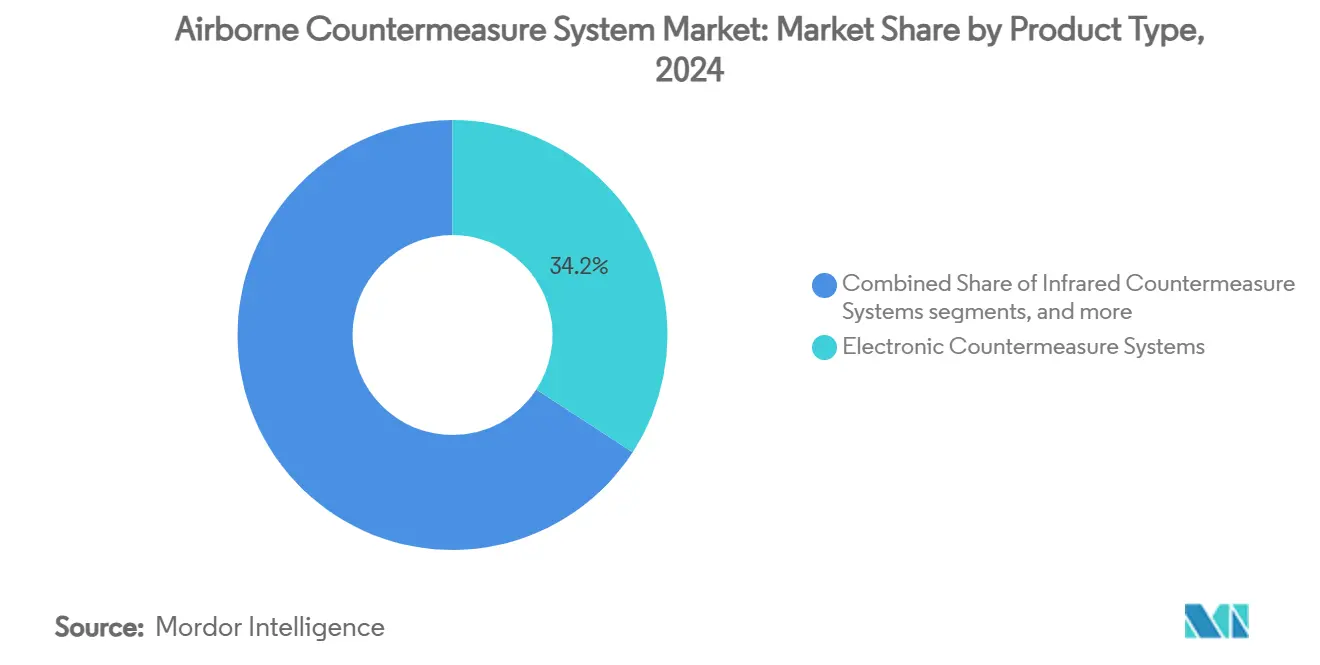

- By product type, electronic countermeasure systems accounted for 34.18% of the airborne countermeasure system market share in 2024, whereas directed-energy countermeasures are expected to advance at a 7.21% CAGR to 2030.

- By platform, military aircraft commanded 60.75% of the airborne countermeasure system market share in 2024, while unmanned aerial vehicles (UAVs) are projected to advance at an 8.10% CAGR through 2030.

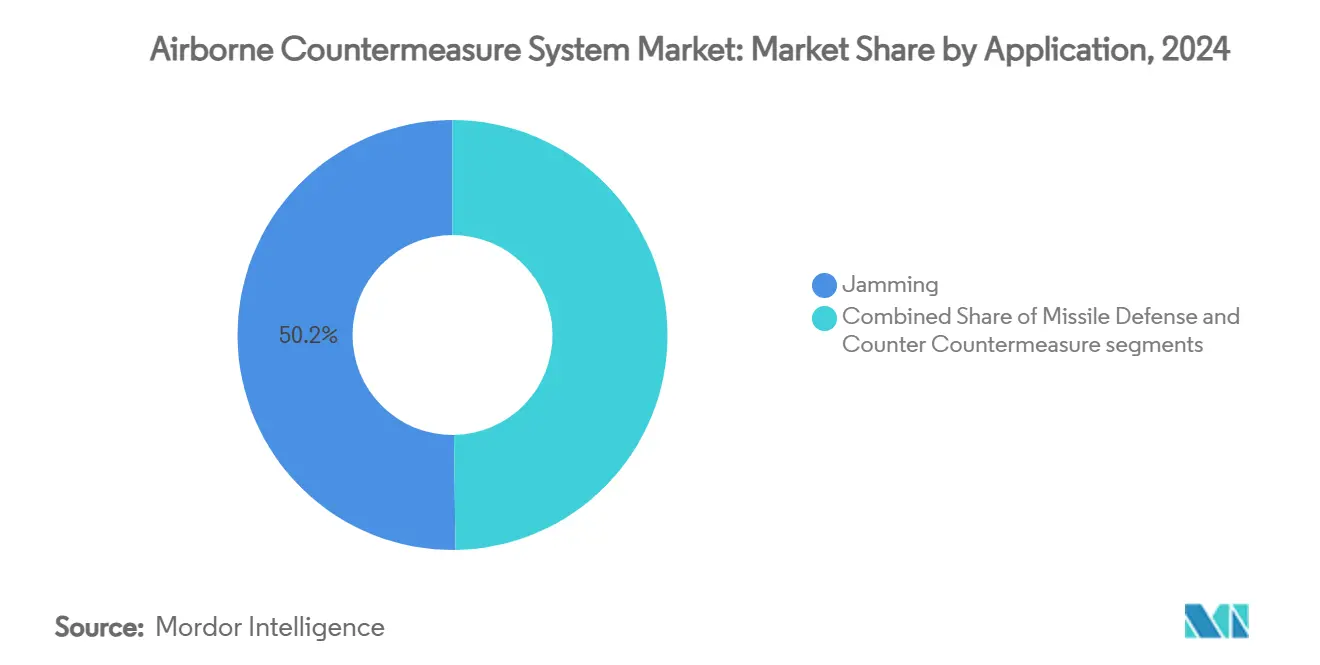

- By application, jamming accounted for 50.22% of the airborne countermeasure system market size in 2024, whereas counter-countermeasure capabilities are poised to grow at a 5.76% CAGR.

- By fit, linefit installations held 52.10% of the airborne countermeasure system market size in 2024; retrofit integration is projected to rise at a 6.27% CAGR.

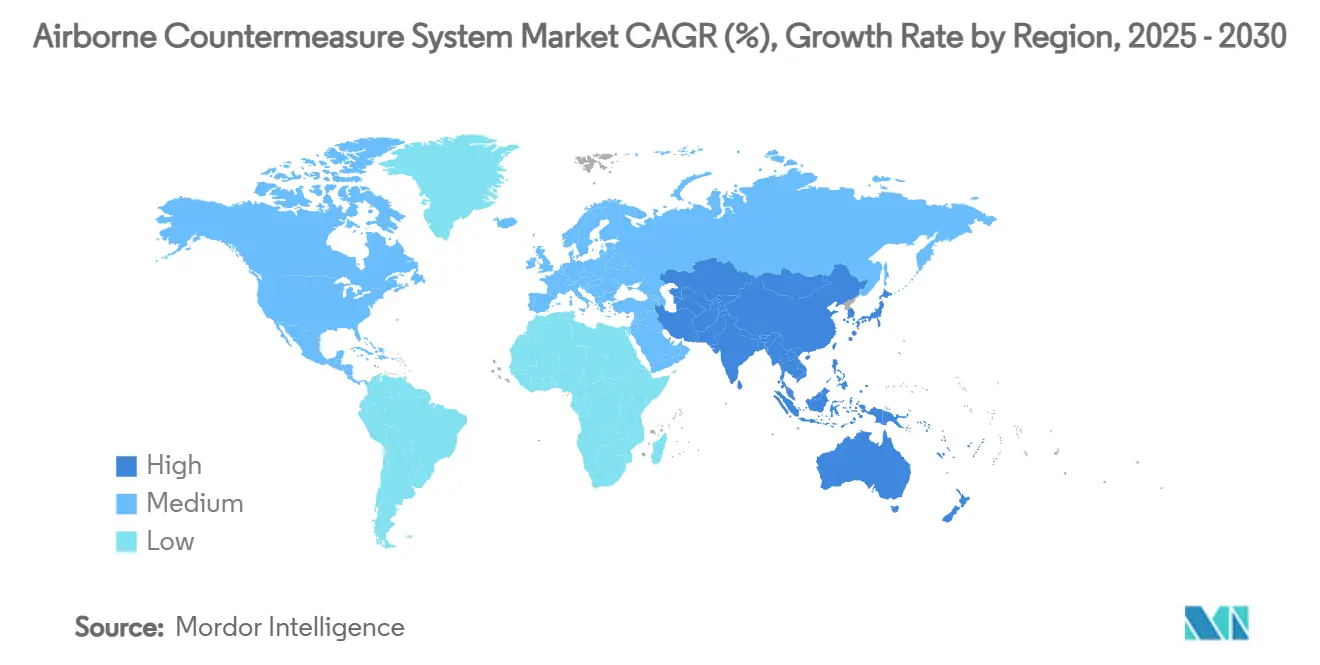

- By geography, North America represented 37.80% of 2024 revenues. Yet, Asia-Pacific is forecasted to experience escalating complexity and frequency of radar-guided threats, which is expected to lead to growth at a 6.80% CAGR through 2030.

Global Airborne Countermeasure System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating complexity and frequency of radar-guided threats | +1.5% | Eastern Europe, South China Sea, global | Medium term (2-4 years) |

| Expanded defense spending on aircraft survivability and EW upgrades | +1.2% | North America, EU, Asia-Pacific | Long term (≥ 4 years) |

| Accelerated acquisition of advanced-generation combat aircraft platforms | +0.8% | Global | Long term (≥ 4 years) |

| Rising geopolitical instability prompting rapid deployment of countermeasure technologies | +0.7% | Asia-Pacific, Middle East and Africa | Short term (≤ 2 years) |

| Widespread use of low-cost loitering munitions fueling demand for responsive onboard jamming capabilities | +0.6% | Ukraine, Middle East, global | Medium term (2-4 years) |

| Adoption of modular open-system architectures enabling seamless countermeasure system upgrades | +0.4% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Complexity and Frequency of Radar-Guided Threats

Russian electronic warfare (EW) successes against precision-guided munitions in Ukraine have underscored the pace at which radar-guided threats are evolving. Adversary sensors now operate across wide frequency bands and shift waveforms on demand, prompting suppliers to develop wideband jammers paired with AI-driven signal-processing engines. Lockheed Martin’s counter-drone suite shows how onboard machine learning (ML) models can detect, classify, and jam adaptive radars in milliseconds.[1]D. Fretay, “Lockheed Martin Introduces AI-Driven Counter-Drone Technology,” Army Recognition, armyrecognition.com Operational testing in the South China Sea and Eastern Europe validates the requirement for flexible architectures that support quick software updates. As a result, cognitive EW functions are transitioning from research labs into production programs across the airborne countermeasure system market.

Expanded Defense Spending on Aircraft Survivability and Electronic-Warfare Upgrades

Global military outlays rose to USD 2.49 trillion in 2024, and the momentum directly fuels aircraft survivability budgets.[2]Stockholm International Peace Research Institute, “World Military Expenditure Reaches USD 2.49 Trillion,” sipri.org The US Navy awarded L3Harris USD 587 million for its Next Generation Jammer-Low Band pod as part of a larger push to refresh EA-18G Growler fleets. In the Asia-Pacific region, Japan increased its defense budget by 21% to USD 55.3 billion, allocating funds to electronic-warfare avionics. European demand mirrors this trend: Saab secured orders for Arexis suites on German Eurofighters, signaling NATO’s commitment to joint survivability standards. These sustained allocations create multi-year revenue pipelines that buffer prime contractors from cyclical spending shocks.

Rising Geopolitical Instability Prompting Rapid Deployment of Countermeasure Technologies

Urgent operational needs are compressing acquisition cycles. Taiwan’s USD 360.2 million order for loitering munitions underscores the region’s commitment to fielding responsive defenses within tighter timelines. During Red Sea security patrols, Greece demonstrated operational maturity by neutralizing aerial threats with the CENTAUR counter-UAS system, validating non-kinetic intercept concepts in live missions. A similar urgency underpins Canada’s CAD 169 million (USD 123.12 million) drone defense purchase from CACI, reflecting the broader adoption of ready-to-field solutions. Vendors that rapidly ship proven, interoperable kits enjoy a bidding advantage across the airborne countermeasure system market.

Widespread Use of Low-Cost Loitering Munitions Fueling Demand for Responsive Onboard Jamming Capabilities

The surge in low-cost Shahed-136-class drones has forced air forces to reconsider cost curves: interceptors worth millions of dollars are being expended against targets priced in the thousands. The US LUCAS kamikaze-drone program responds with an open-architecture design that permits EW payload swaps aligned with mission needs. Flight-test feedback indicates that onboard jammers can simultaneously disrupt multiple inbound drones, thereby reducing engagement costs and conserving kinetic assets for higher-value threats. Consequently, manufacturers are embedding multiband jamming antennas and compact power-amplifier modules as baseline features within new aircraft production lots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated acquisition and system integration costs | −0.9% | Global | Long term (≥ 4 years) |

| Strict SWaP constraints on UAVs and compact airborne platforms | −0.7% | Asia-Pacific, North America, global | Medium term (2-4 years) |

| Prolonged procurement timelines in defense acquisition processes | −0.5% | North America, EU | Long term (≥ 4 years) |

| Increasing electromagnetic spectrum congestion reducing jamming effectiveness | −0.3% | Contested zones worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Acquisition and System-Integration Costs

Complex electronics, inflation, and semiconductor shortages are driving up program costs. US Department of Defense analysts warn of a potential USD 100 billion decline in purchasing power within five years, compelling agencies to prioritize select capabilities over full-fleet upgrades. Integration challenges add friction: L3Harris’s Viper Shield suite required multi-year interoperability testing with APG-83 radar systems before the first flight in 2025. Tariffs and export controls on critical chips, particularly those based on gallium, lengthen lead times and increase material costs. Together, these pressures temper the otherwise robust outlook for the airborne countermeasure system market.

Increasing Electromagnetic-Spectrum Congestion Reducing Jamming Effectiveness

Urban build-outs of 5G, satellite internet constellations, and expanded military networks create congested operating environments that dilute the potency of jamming. Modern countermeasure suites must now include real-time spectrum-analysis tools capable of locating opportunistic “quiet” gaps and shifting energy precisely where needed. AI-enabled managers allocate power dynamically, preserving mission effectiveness while avoiding interference with civilian communications. Field trials on the next-generation Growler aircraft indicate that software-defined radios, operating with agile beam-forming antennas, can restore disruption efficacy without breaching regulatory emission limits. Continued R&D investment in big data analytics remains essential for maintaining dominance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electronic Systems Lead as Directed Energy Emerges

Electronic countermeasure systems generated the largest revenue contribution, accounting for 34.18% of 2024 sales within the airborne countermeasure system market. Adoption is driven by mature gallium-nitride (GaN) transmitters and software-defined radios that enable swift reprogramming against new emitters. Over the 2025-2030 period, incremental software updates are expected to sustain relevance without necessitating costly hardware swaps, thereby reinforcing the stickiness of the installed base for leading primes.

Directed-energy countermeasure solutions are posting the fastest growth, registering a 7.21% CAGR as laser-based defensive pods transition from prototypes to limited operational capabilities on naval aircraft. Smaller power-storage modules and advanced thermal-management subsystems are lowering platform-integration barriers, driving new orders from US Navy aviation commands. Infrared countermeasure suites and expendable decoys continue to enjoy baseline demand, buoyed by US Air Force and US Navy contracts for BriteCloud 218 and similar payloads. Together, these product clusters underpin a resilient trajectory for the airborne countermeasure system market.

By Platform: Military Aircraft Dominance with UAV Acceleration

Military fixed-wing fleets accounted for 60.75% of 2024 spending, anchored by F-15EX, F-16 Block 70/72, and F/A-18 Block III retrofit cycles. Fighter upgrade packages increasingly bundle wideband jammers, threat-warning receivers, and expendable decoys into unified kits to streamline certification and logistics. Transport and special-mission aircraft increase volume through fleet-wide sustainment plans, such as the Royal Moroccan Air Force C-130 project, which was awarded in 2025.

Unmanned aerial vehicles (UAVs) represent the most dynamic platform category, expanding at an 8.10% CAGR. Rising investment in medium-altitude long-endurance (MALE) UAVs by Indo-Pacific air forces is sharpening requirements for lightweight, low-power jamming solutions. Advances in miniaturized GaN amplifiers and conformal antennas enable manufacturers to meet stringent size, weight, and power criteria without compromising range. Therefore, the airborne countermeasure system market sees parallel demand curves: large retrofit contracts on legacy crewed aircraft and brisk new-start programs centered on autonomous platforms.

By Application: Jamming Leadership with Counter-Countermeasure Growth

Jamming maintained its leadership position, accounting for 50.22% of the 2024 airborne countermeasure system market revenues. Multiband pods that degrade radar, communications, and navigation channels remain the cornerstone of airborne self-protection doctrine. Northrop Grumman’s USD 176 million Radio Frequency Countermeasure award exemplifies sustained US Air Force commitment to wide-bandwidth electronic-attack capabilities.

Counter-countermeasure (CCM) functions are the fastest-growing application, posting a 5.76% CAGR. These modules detect hostile jamming and adapt waveforms in real-time, an imperative as adversaries integrate frequency-hopping and AI-enabled deception tactics. Advanced CCM suites protect friendly datalinks from inadvertent interference, supporting joint all-domain command and control (JADC2) ambitions. The dual emphasis on offensive jamming and defensive CCM continues to broaden solution portfolios for prime contractors, reinforcing the robustness of the airborne countermeasure system market.

By Fit: Linefit Dominance with Retrofit Acceleration

Linefit programs dominated 2024 revenue with a 52.10% share, reflecting a design-for-survivability philosophy among new aircraft manufacturers. Clean-sheet platforms, such as South Korea’s KF-21, incorporate distributed-aperture arrays and embedded self-protection electronics from inception, thereby reducing the need for later modifications. The pivot toward factory-integrated solutions locks in multi-decade sustainment revenue and underscores the structural strength of the airborne countermeasure system market.

Retrofit work packages are projected to accelerate at a 6.27% CAGR as airframes such as the B-52 continue to receive survivability upgrades under contracts valued at up to USD 947 million. Retrofitting extends platform relevance without incurring replacement costs, a model that governments are adopting as they balance strategic needs against fiscal realities. Engineering complexity, however, creates lucrative high-margin opportunities for integrators skilled at merging new digital architectures into analog-era avionics.

Geography Analysis

North America remained the most significant contributor at 37.80% in 2024, lifted by the US Department of Defense's intensive EW recapitalization agenda. In North America, the USD 587 million Next Generation Jammer contract, Boeing's USD 615 million electronic protection award, and Canada's CAD 169 million (approximately USD 123.12 million) counter-drone initiative illustrate the scale of regional investment. The US airborne countermeasure system market is expected to maintain mid-single-digit growth as block-upgrade pathways for F-35, B-21, and future vertical-lift programs advance.

The Asia-Pacific is the fastest-expanding theatre, registering a 6.80% CAGR. Japan's record USD 55.3 billion defense budget, Taiwan's purchase of loitering munitions, and India's orders for electronic-warfare retrofitting illustrate rising regional commitments to electromagnetic-spectrum superiority. Indigenous fighter developments, such as KF-21, infuse the domestic supply chain. Australia's multibillion-dollar AUKUS framework promises additional airborne EW upgrades across maritime patrol and strike aircraft. Collectively, these drivers sustain an outsized share of incremental global spending.

Europe balances mature capability sets with renewed Germany's Eurofighter Arexis, Greece's operational deployment of CENTAUR counter-UAS, and Italy's support for F-35 decoy programs, confirming steady pipeline visibility. NATO-wide interoperability standards encourage members to adopt common architecture choices, such as SOSA, thereby simplifying the transfer of technology across the Atlantic. In the Middle East and Africa, persistent conflicts and asymmetric aerial threats are driving spending toward integrated self-protection suites, thereby gradually expanding the regional footprint in the airborne countermeasure system market.

Competitive Landscape

The airborne countermeasure system market is moderately consolidated, with the top five suppliers accounting for over 50% of the 2024 revenue. Strategic differentiation hinges on delivering modular, software-upgradable architectures that shrink design-cycle times. L3Harris Technologies, Inc., buoyed by multiple wins exceeding USD 1 billion from the US Navy and Air Force, exemplifies the scale advantages in mission-system integration. Lockheed Martin is carving white-space positions through AI-enabled counter-drone portfolios that promise real-time orchestration of sensors and effectors.

The pace of technology adoption drives market share shifts more than production volume. Suppliers investing in GaN, digital radio-frequency memory, and cognitive-EW algorithms are capturing high-margin follow-on upgrade contracts. The 2025 acquisition of Ultra Maritime’s Signature Management and Power business by ESCO Technologies for USD 550 million illustrates ongoing consolidation among component specialists aiming to secure proprietary intellectual property crucial for signature-management subsystems.[3]ESCO Technologies, “ESCO to Acquire Ultra Maritime Unit for USD 550 Million,” investing.com Meanwhile, supply-chain resilience has become a competitive criterion following China’s curbs on gallium exports; prime contractors are qualifying alternative materials and dual-sourcing to hedge geopolitical risk.

Emerging entrants include software-defined radio start-ups offering open-standard hardware aligned to CMOSS and SOSA specifications. Their agile development cycles attract tier-one primes seeking to plug capability gaps without lengthy in-house R&D. Certification rigor and integration complexity continue to favor incumbents with established flight-test infrastructure, sustaining a moderate concentration profile for the airborne countermeasure systems market.

Airborne Countermeasure System Industry Leaders

BAE Systems plc

RTX Corporation

Lockheed Martin Corporation

Israel Aerospace Industries Ltd.

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: BAE Systems completed the delivery of 400 2-Color Advanced Warning Systems (2CAWS) to the US Army under the Limited Interim Missile Warning System (LIMWS) program. The system, engineered for utility, heavy-lift, and attack helicopters, demonstrated combat effectiveness in countering missile threats and protecting Army personnel.

- February 2024: BAE Systems secured USD 114 million in Foreign Military Sales (FMS) contracts from the US Army for AN/AAR-57 Common Missile Warning Systems (CMWS). These systems safeguard their fleets and newly acquired aircraft, including AH-64 Apache, CH-47 Chinook, and UH-60 Black Hawk helicopters.

- January 2024: The US Department of Defense (DoD) awarded Northrop Grumman a USD 16.5 million contract to install LAIRCM Generation 3 Pods on KC-135 aircraft. Using a high-intensity laser beam, the system detects incoming infrared missiles from MANPADS systems, evaluates threats, and neutralizes the missile's heat-seeking component.

Global Airborne Countermeasure System Market Report Scope

| Electronic Countermeasure Systems |

| Infrared Countermeasure Systems |

| Directed Energy Countermeasure Systems |

| Expendable and Towed Decoys |

| Chaff and Flare Dispensers |

| Missile Warning Systems |

| Laser Warning Receivers |

| Integrated Self-Protection Suites |

| Military Aircraft | Fighter Aircraft |

| Special Mission Aircraft | |

| Transport Aircraft | |

| Trainer Aircraft | |

| Military Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

| Jamming |

| Missile Defense |

| Counter Countermeasure |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Electronic Countermeasure Systems | ||

| Infrared Countermeasure Systems | |||

| Directed Energy Countermeasure Systems | |||

| Expendable and Towed Decoys | |||

| Chaff and Flare Dispensers | |||

| Missile Warning Systems | |||

| Laser Warning Receivers | |||

| Integrated Self-Protection Suites | |||

| By Platform | Military Aircraft | Fighter Aircraft | |

| Special Mission Aircraft | |||

| Transport Aircraft | |||

| Trainer Aircraft | |||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Application | Jamming | ||

| Missile Defense | |||

| Counter Countermeasure | |||

| By Fit | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the airborne countermeasure system market?

The airborne countermeasure system market size stands at USD 14.82 billion in 2025 and is projected to reach USD 18.57 billion by 2030, reflecting a 4.61% CAGR.

Which product segment leads the market today?

Electronic countermeasure systems hold the top position with 34.18% of 2024 revenue.

Why is Asia-Pacific the fastest-growing region?

Rising defense budgets, including Japan’s 21% increase and Taiwan’s accelerated procurement, coupled with indigenous fighter programs drive a 6.80% CAGR for the region.

How are unmanned aerial vehicles influencing demand?

UAV fleets require lightweight jamming and self-protection suites, pushing the platform segment to an 8.10% CAGR.

What technologies will shape competitive advantage through 2030?

GaN power amplifiers, AI-enabled cognitive electronic-warfare algorithms, and modular open-system architectures are the key differentiators across upcoming contracts.

Page last updated on: