Special Mission Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

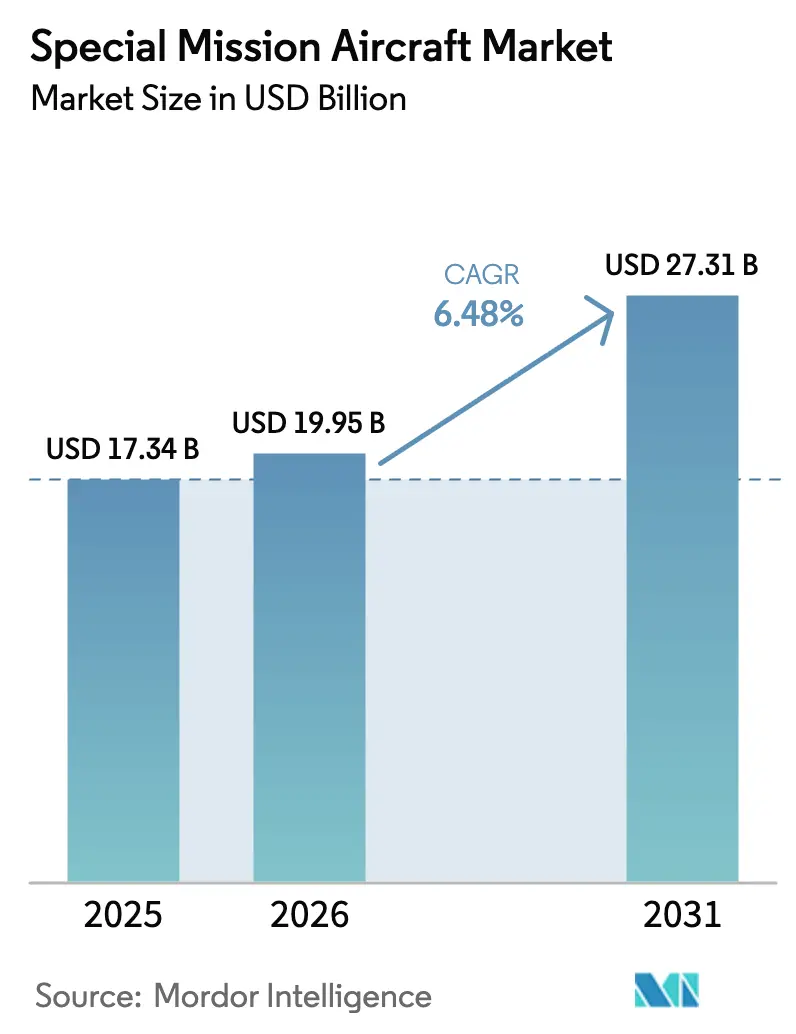

| Market Size (2026) | USD 19.95 Billion |

| Market Size (2031) | USD 27.31 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

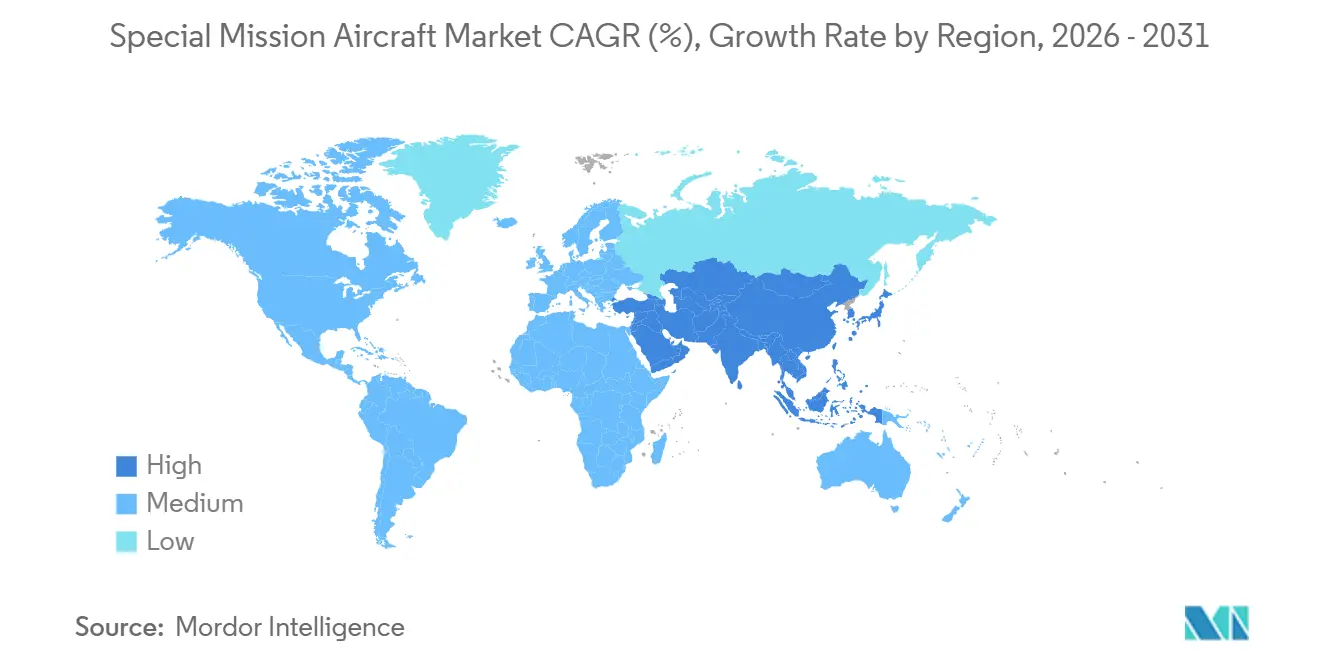

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

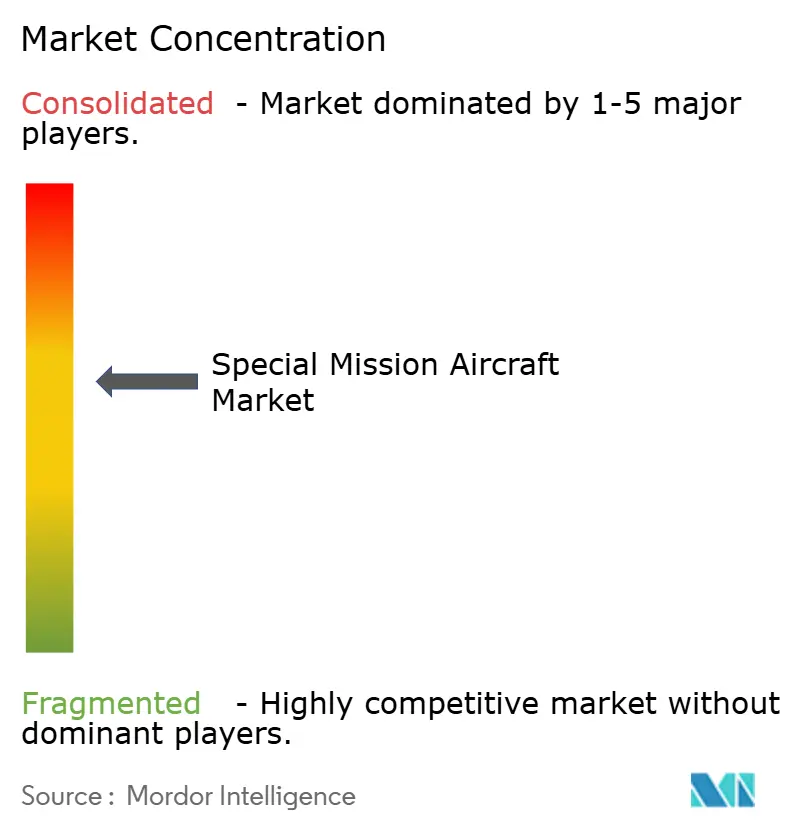

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Special Mission Aircraft Market Analysis by Mordor Intelligence

The special mission aircraft market size is expected to grow from USD 18.66 billion in 2025 to USD 19.95 billion in 2026 and is forecasted to reach USD 27.31 billion by 2031 at a 6.48% CAGR over 2026-2031. Sustained budget expansion for multi-domain ISR capabilities, accelerated replacement of aging fleets, and rapid adoption of HALE and MALE UAVs underpin this trajectory. The US defense spending on airborne ISR and EW programs climbed 7.2% year over year in FY2025, while modular mission suites that rely on open architectures have compressed integration timelines by half, enabling faster fielding of new sensors. Business jet conversions, coupled with leasing options that cap acquisition risk, lower the entry barrier for emerging operators and civil agencies. Global UAV procurements continue to diversify end-user demand, providing persistent coverage at an operating cost roughly one-third that of comparable manned platforms.

Key Report Takeaways

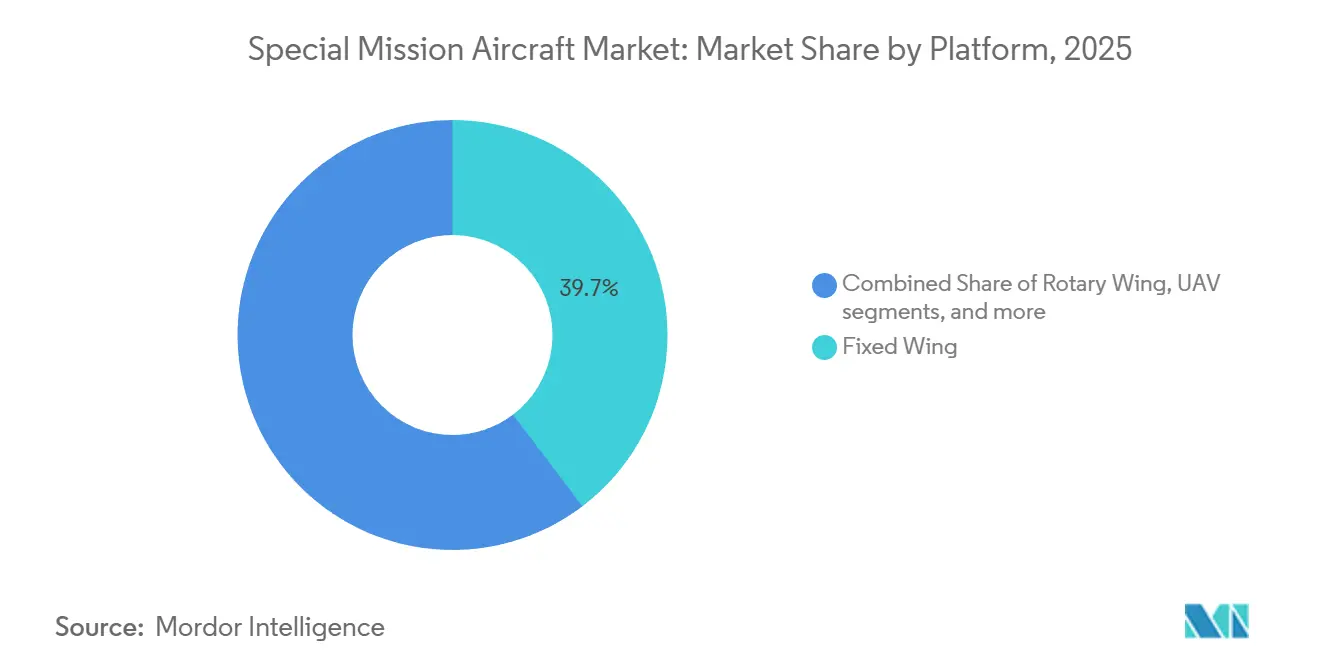

- By platform, fixed-wing aircraft led with 39.67% revenue share in 2025; unmanned aerial vehicles (UAVs) are projected to expand at a 12.21% CAGR to 2031.

- By application, intelligence, surveillance, and reconnaissance (ISR) held 55.42% of the 2025 value; electronic warfare (EW) and signals intelligence (SIGINT) are forecasted to grow at an 8.89% CAGR through 2031.

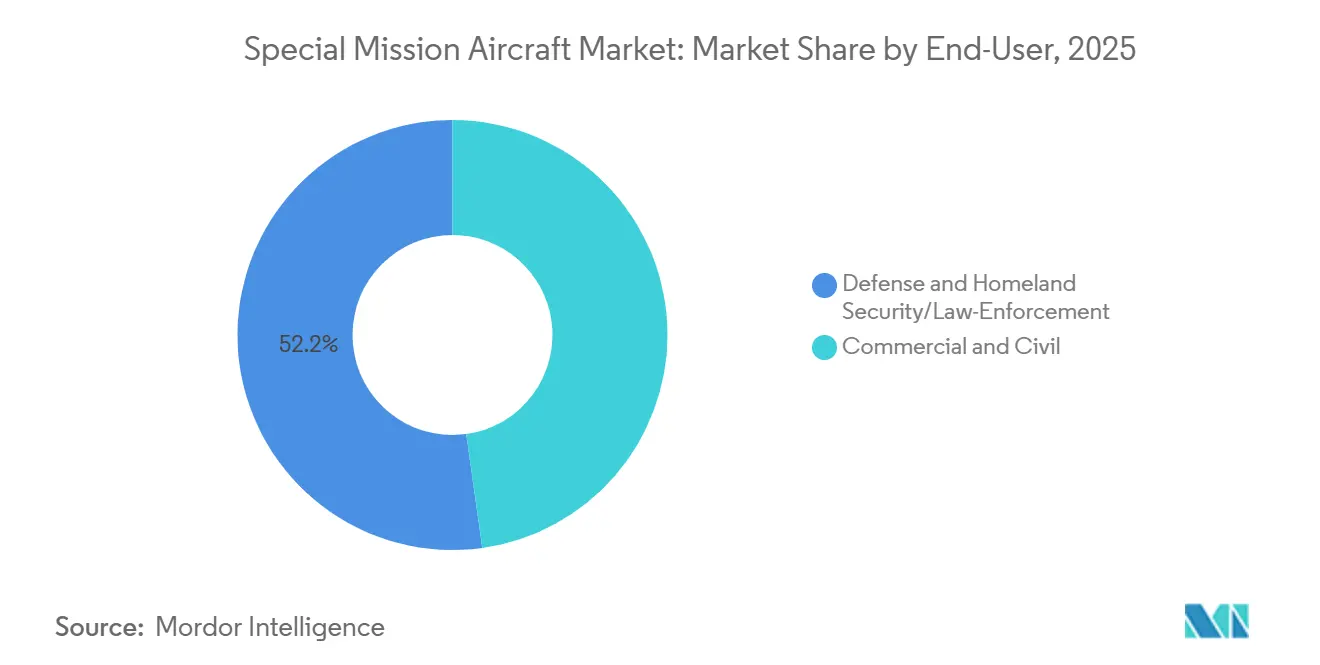

- By end user, defense and homeland security accounted for 52.21% of 2025 spending; the commercial and civil segment is expected to advance at a 7.75% CAGR to 2031.

- By geography, North America accounted for 41.56% of the 2025 revenue; the Asia-Pacific region is expected to post the fastest regional CAGR of 8.51% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Special Mission Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating multi-domain ISR budgets | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Fleet-replacement cycle for legacy P-3/C-130 and CN-235 families | +1.5% | North America, Europe, Japan, Australia | Long term (≥ 4 years) |

| Accelerated uptake of HALE/MALE UAVs for cost-effective missions | +1.2% | Early adoption in North America, Asia-Pacific | Short term (≤ 2 years) |

| AI-ready modular mission suites slashing integration lead-times | +0.9% | North America, Europe, spillover to Middle East and Asia-Pacific | Medium term (2-4 years) |

| Expansion of business jet conversions lowering total cost of ownership | +0.7% | Middle East, Asia-Pacific, smaller European nations | Medium term (2-4 years) |

| Turnkey leasing by specialist lessors enabling small nation entry | +0.5% | Africa, South America, Southeast Asia, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Multi-Domain ISR Budgets Drive Spend

Defense ministries across the NATO and Indo-Pacific regions increased ISR allocations in 2025, reflecting the imperative for real-time cross-domain awareness in the Special Mission Aircraft Market. The US earmarked USD 13.9 billion for airborne ISR and EW programs in fiscal 2025, a clear signal of sustained funding momentum. Japan, the UK, and Australia mirrored this trend with budget approvals for P-1, P-8A, E-7 Wedgetail, and MQ-4C Triton fleets. These appropriations drive steady orders for new airframes and mid-life avionics retrofits. Open-system architectures make it easier to layer AI engines that fuse multi-spectral data, raising the value proposition of every delivered platform. As budgets lock in multi-year procurement lines, suppliers secure forward revenue and scale production lines to meet widened demand horizons.

Fleet Replacement Cycle Accelerates Platform Modernization

Cold War-era patrol and transport airframes entered retirement in 2024-2025, forcing operators to select lower-maintenance successors. The final P-3C Orion squadron was decommissioned by the US Navy in December 2024, marking the complete transition to the P-8A Poseidon, a jet variant with a 30% greater mission radius. Spain and Canada initiated competitions or awards to replace CN-235 and CP-140 fleets, prioritizing modular mission bays and open-architecture avionics. Operators now demand compliance with VICTORY standards and high-bandwidth data buses to avoid future obsolescence. Replacement projects ripple through supply chains, uplifting sensor, data-link, and training providers. The resulting procurement wave underpins a predictable backlog that supports the special mission aircraft market through the next decade.

Accelerated Uptake of HALE/MALE UAVs Transforms Economics

Persistent surveillance at lower hourly cost positions HALE and MALE UAVs as prime alternatives to crewed aircraft. General Atomics delivered 24 MQ-9B SeaGuardian systems in 2025, each capable of more than 30-hour sorties and certified for operations in unsegregated airspace. Northrop Grumman extended the RQ-4 Global Hawk service life to 2035 with a fresh sensor upgrade award in March 2025.[1]Northrop Grumman, “Northrop Grumman Awarded RQ-4 Sensor Upgrade Contract,” northropgrumman.com Budget-constrained governments can now double daily coverage at one-third the cost of a crewed operation, shifting acquisition priorities toward ground control stations and satellite links. As attrition risk in contested zones increases, unmanned systems are absorbing missions that once required multi-crew patrols. This modality reshapes training pipelines, sustainment models, and command-and-control (C2) doctrine, reinforcing the growth outlook for the special mission aircraft market.

AI-Ready Modular Mission Suites Slashing Integration Lead Times

Open-architecture mission suites embedded with AI processors reduced integration schedules from two years to under 12 months. L3Harris implemented its SkyVision AI package on a Bombardier Global 6500 in 2025, achieving operational readiness in 11 months, half the legacy benchmark.[2] L3Harris Technologies, “L3Harris Unveils SkyVision AI Mission Suite,” l3harris.com Israel Aerospace Industries and Rafael incorporated change-detection algorithms within new ISR pods, enabling onboard anomaly recognition and reducing bandwidth loads. Faster cycles would allow operators to field new sensor combinations without requiring prolonged depot visits. Standardized interfaces compliant with STANAG 4586 foster an ecosystem where sensor providers compete on capability, not connector pin-outs. This modularity enhances residual value, enticing lessors to expand fleets dedicated to special missions and broadening finance options across emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Procurement deferrals amid fiscal tightening | -1.1% | Western Europe, North America, debt-constrained emerging markets | Short term (≤ 2 years) |

| High-end A2/AD bubbles reducing manned-platform survivability | -0.8% | Asia-Pacific (South China Sea, Taiwan Strait), Eastern Europe | Medium term (2-4 years) |

| LEO-satellite constellations substituting some airborne tasks | -0.4% | Global; early impact in maritime and border surveillance | Medium term (2-4 years) |

| ITAR/dual-use export controls on advanced sensor payloads | -0.6% | Global; exports from North America to non-allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-End A2/AD Systems Shift Platform Preferences

Integrated air-defense systems equipped with long-range surface-to-air missiles shrink safe operating envelopes for crewed ISR aircraft. RAND modeling indicates that attrition risks exceed 15% for manned platforms that venture within 300 nautical miles of contested coastlines in a high-intensity scenario. NATO standoff tactics now emphasize RC-135 and E-7 Wedgetail flights beyond enemy missile arcs, delegating near-shore persistence to MQ-4C Triton UAVs. The broader adoption of crewless assets mitigates pilot survivability concerns, yet introduces new requirements for satellite bandwidth and cyber-secure command links. For the special mission aircraft market, the shift tempers demand for heavy crewed variants while stimulating orders for electronic-warfare escorts and low-observable sensor pods that can operate outside denial zones.

ITAR and Dual-Use Export Controls on Advanced Sensor Payloads

In the Special Mission Aircraft Market,Stringent export-control regimes continue to slow deliveries of high-end sensors to customers lacking deep defense partnerships with the United States or the European Union. License denials for synthetic-aperture radar packages during 2024-2025 forced several Middle Eastern buyers to accept downgraded payloads, which increased program timelines and costs. EU dual-use rules that took effect in January 2025 added extensive end-use documentation to electro-optical systems containing automated target-tracking algorithms. Israel Aerospace Industries reported USD 120 million in deferred revenue tied to export approvals for radar pods in 2024, underscoring cash-flow sensitivity to regulatory pacing. As a result, emerging economies invest in indigenous sensor development, fragmenting the global supplier base and tempering export-driven growth for Western primes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: UAV Surge Reshapes Fleet Mix

Unmanned aerial vehicles (UAVs), the fastest-growing platform group, are forecasted to register a 12.21% CAGR to 2031, reflecting expanding roles in persistent maritime and border surveillance. Fixed-wing aircraft retained the largest share in 2025 at 39.67%, anchored by the P-8A Poseidon and C-295 Persuader fleets, which deliver multi-mission versatility and extended logistical pedigrees.[3]Boeing, “P-8 Poseidon,” boeing.com The special mission aircraft market share for fixed-wing platforms highlights entrenched fleet preferences among maritime nations. Still, the growing appeal of UAV cost advantages is shifting procurement roadmaps in favor of remotely piloted options.

The special mission aircraft market size captured by UAVs is expected to expand as regulatory bodies approve unsegregated airspace operations, as evidenced by the Civil Aviation Authority certificate issued to the MQ-9B in 2024. Rotary-wing assets sustain niche relevance in search-and-rescue and shipboard roles, while hybrid and optionally piloted concepts gain exploratory funding from border agencies. Business-jet conversions such as the G550 CAEW deliver rapid capability without new-type certification burdens, appealing to countries with small fleets and limited training pipelines. Suppliers that offer modular cabins and open avionics stand to capture upgrade cycles as threat environments evolve.

By Application: Electronic Warfare Gains Pace

ISR constituted 55.42% of 2025 revenue, remaining the backbone of fleet tasking, as maritime, border, and counter-terror missions require persistent sensor coverage. The special mission aircraft market size attached to ISR will remain high, as naval and coast guard commanders rely on wide-area radar, electro-optical turrets, and automatic identification systems to monitor exclusive economic zones.

EW and SIGINT roles, set to compound at an annual rate of 8.89%, reflect rising spectrum congestion and the adversary's deployment of frequency-agile radars. The EC-37B Compass Call program embodies this shift, integrating cognitive jamming algorithms that autonomously tailor waveforms in real time.[4] L3Harris Technologies, “L3Harris Awarded EC-37B Compass Call Contract,” l3harris.com ASW remains steady, buoyed by advances in sonobuoys that enable single-aircraft prosecutorial loops. Airborne early warning (AEW) assets are gaining traction as NATO and Asia-Pacific operators seek command and control (C2) resilience. Emergency services demand grows within civil agencies as wildfires, hurricanes, and floods drive the adoption of multi-sensor turboprops that switch missions through palletized consoles.

By End User: Commercial Participation Expands

Defense and homeland security customers accounted for 52.21% of the 2025 value, reflecting consistent funding for sovereignty protection and alliance commitments. The special mission aircraft market size remains defense-led. Yet, compound expansion favors commercial and civil agencies as they pursue cost-effective aerial data collection for environmental stewardship and critical-infrastructure oversight.

The commercial and civil segment is expected to grow at 7.75% through 2031, driven by contracts such as wildfire monitoring in California and Norway’s coastal traffic surveillance service, which was awarded in 2025. As regulatory frameworks mature for beyond-visual-line-of-sight (BVLOS) flights, energy, insurance, and disaster-response organizations are increasingly procuring turnkey UAV services rather than owning and operating their own fleets. Integrators that package aircraft, ground stations, and data analytics under a service contract will unlock new addressable revenue and reduce sensitivity to cyclic defense budgets.

Geography Analysis

North America retained leadership with 41.56% of 2025 revenue, supported by the US and Canadian procurement lines that bundle platform acquisition with substantial domestic industrial offsets. The region benefits from a deep vendor ecosystem, secure financing, and dedicated military research funding. Fleet modernization of the P-8A Poseidon, E-7 Wedgetail, and RC-135 variants dominates demand, while Customs and Border Protection's UAV operations illustrate expanding homeland security roles. The special mission aircraft market share in North America highlights the region's established industrial base and rapid fielding cycles.

Asia-Pacific delivers the most dynamic growth outlook, projected at an 8.51% CAGR. Drivers include India's additional P-8I orders, South Korea's expansion of the P-8A, and Australia's combined MQ-4C Triton and P-8A force structure. Japan continues to enhance its indigenous P-1 fleet, integrating upgraded sonar processing and electronic support suites. Rising maritime disputes across the Indo-Pacific catalyze new ISR requirements among Southeast Asian nations, spurring both manned and unmanned acquisitions. European demand advances at a steadier clip, buoyed by collaborative NATO programs such as the E-7 Wedgetail and P-8A Poseidon buys by the United Kingdom, Germany, and Norway. Modernization of France's Atlantique 2 and Italy's ATR 72MP fleets sustains revenue from sensor and mission-system upgrades. Central and Eastern European states focus on airborne signals-intelligence packages integrated onto turboprop transports, striking a balance between cost and rapid fieldability.

The Middle East and Africa channel selective capital into high-end platforms, typified by the United Arab Emirates' GlobalEye fleet, which fuses AEW&C, maritime surveillance, and ground-moving-target indication in a single airframe. Saudi Arabia expanded its CN-235 maritime-patrol inventory, optimizing littoral domain awareness and anti-smuggling efforts. South America remains modest in scale, but Brazil's C-390 Millennium search-and-rescue deliveries inject regional production and support into Embraer's supply chain, illustrating the rising prominence of domestic platforms.

Competitive Landscape

The special mission aircraft market shows moderate concentration. RTX Corporation, The Boeing Company, and Lockheed Martin Corporation maintain extensive portfolios encompassing maritime patrol, AEW, and C2. General Atomics dominates the HALE/MALE niche, leveraging rapid iterative development and its success in exporting these systems. RTX Corporation leveraged the merger of Collins Aerospace with Raytheon Intelligence & Space to create bundled radar, EW, and communication offerings that lower integration risk for buyers. The Boeing Company scaled P-8A production to meet overlapping orders from the United States, Australia, and Canada, benefiting from block-buy efficiencies and standard training pipelines. Lockheed Martin collaborated with Embraer on a maritime-surveillance variant of the C-390 Millennium, broadening access to South American and African markets.

Mission-system integrators, such as L3Harris Technologies, Inc. and Sierra Nevada Company, LLC, exploit the demand for rapid conversions of commercial airframes, often completing turnkey ISR solutions in under one year. Turkish Aerospace Industries and Korea Aerospace Industries position as disruptors, offering indigenous patrol and ISR platforms that bypass ITAR constraints. Leasing specialists expand their managed fleets, enabling government customers to deploy surveillance assets without capital expenditure or long depreciation cycles.

Technology differentiation focuses on cognitive electronic warfare algorithms, AI-enabled sensor fusion, and open standards that enable future upgrades without requiring airframe recertification. L3Harris Technologies, Inc., filed 14 patents on adaptive jamming between 2023 and 2025, illustrating the innovation race for frequency-agile countermeasures. Vendor roadmaps indicate an increase in onboard processing that filters data at the edge, thereby reducing bandwidth loads and enabling faster kill-chain decisions. Partnerships between primes and cloud analytics firms will likely shape the next frontier of value creation within the special mission aircraft market.

Special Mission Aircraft Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Northrop Grumman Corporation

Bombardier Inc.

Dassault Aviation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Sweden signed an agreement to procure four C-390 Millennium multi-mission aircraft from Brazilian aerospace company Embraer, supporting operations such as cargo transport, troop deployment, medical evacuation, and humanitarian missions.

- July 2025: L3Harris Technologies, Inc. received a USD 300 million contract from Italy to supply two Gulfstream G550 aircraft equipped with an advanced electromagnetic warfare system.

- July 2024: Diamond Aircraft signed a contract to supply three DA62 MPP aerial surveillance aircraft to the Greek Ministry of Climate Crisis and Civil Protection for firefighting, SAR, and aerial surveillance using advanced electro-optical systems.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the special-mission aircraft (SMA) market as the annual revenue generated from new-build or professionally converted fixed-wing, rotary-wing, and UAV platforms that are purpose-equipped with ISR, maritime patrol, electronic-warfare, AEW&C, or emergency-response payloads, together with the mission-system integration work that makes such aircraft operational.

Exclusions include trainer aircraft used solely for basic flight instruction, unmanned cargo drones, and aftermarket component repairs that do not alter mission capability; these are outside the scope.

Segmentation Overview

- By Platform

- Fixed Wing

- Rotary Wing

- Unmanned Aerial Vehicle (UAV)

- Hybrid/Other Platforms

- By Application

- Intelligence, Surveillance and Reconnaissance (ISR)

- Maritime Patrol and Anti-Submarine Warfare (ASW)

- Electronic Warfare (EW) and Signals Intelligence (SIGINT)

- Airborne Early Warning & Control (AEW&C)

- Emergency Services (Medevac, Disaster Management, Search and Rescue, etc.)

- By End User

- Defense and Homeland Security/Law-Enforcement

- Commercial and Civil

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed senior program officers in North America, Europe, and Asia-Pacific, airborne-ISR squadron planners, and mission-system integrators. Their insights on typical conversion lead-times, sensor fit-rates, and regional funding outlooks verified secondary-data assumptions and anchored price-volume pairs in our model.

Desk Research

Mordor analysts begin by mapping global SMA fleets and orders using open datasets from bodies such as SIPRI, NATO, the US Congressional Budget Service, and UN Comtrade; these clarify procurement volumes, trade flows, and defense-capital allocations. We supplement them with civil-aviation registries, EASA/FAA type-certificate records, and air-framer investor filings, which reveal platform backlogs and average sale prices. Paid libraries including Aviation Week (program status), D&B Hoovers (contract values), and Questel (sensor-suite patent trends) help refine cost curves and technology penetration. The sources listed illustrate the breadth of material consulted and are not exhaustive.

Market-Sizing & Forecasting

A top-down build draws on declared defense-capital budgets, historical spend-to-deliver ratios, and fleet-age triggers, which are then balanced with selective bottom-up checks, sampled OEM deliveries, integrator revenues, and average sale price × volume calculations to close gaps. Key market fingerprints include (1) annual ISR flight-hour growth, (2) share of defense budgets earmarked for multi-domain command-and-control, (3) business-jet airframe conversion rates, (4) HALE/MALE UAV procurement lines, and (5) maritime-surveillance sortie density. A multivariate regression model links these drivers to observed SMA spending and projects demand through 2030; scenario analysis adjusts for currency swings and emergent conflict flashpoints.

Data Validation & Update Cycle

Outputs undergo variance checks against independent fleet tallies, price audits, and time-series trend breaks before senior analyst sign-off. Models refresh each year, with interim updates triggered by material contract wins or geopolitical events; a final pre-publication review ensures clients receive the latest view.

Credibility Anchor: Why Our Special Mission Aircraft Figures Command Reliability

Published estimates often diverge because firms choose different platform mixes, pricing baselines, or refresh cadences.

Key gap drivers include whether UAV conversions are counted, how retrofit labor is priced, exchange-rate timing, and whether cancelled programs remain in the base year. Mordor reports only awarded budgets and aircraft accepted into service, applies rolling 12-month average ASPs, and updates currency effects quarterly, reducing volatility seen elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.73 B (2025) | Mordor Intelligence | |

| USD 18.60 B (2025) | Regional Consultancy A | Includes projected but unfunded fleet renewals |

| USD 18.63 B (2025) | Global Consultancy B | Uses list prices without integration cost normalization |

| USD 17.19 B (2024) | Trade Journal C | Omits UAV segment and applies 2024 exchange rates |

External publications place 2024-2025 values between USD 17.19 B and USD 18.63 B. The comparison highlights how Mordor's strict scope discipline, verified ASPs, and frequent refresh cycle deliver a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

How large is the special mission aircraft market in 2026?

The special mission aircraft market size reached USD 19.95 billion in 2026 and is projected to climb to USD 27.31 billion by 2031 at a 6.48% CAGR.

Which platform segment holds the largest revenue share?

Fixed-wing aircraft led with 39.67% of 2025 revenue, anchored by P-8A Poseidon and similar maritime-patrol variants.

Which platform segment is growing the fastest?

Unmanned aerial vehicles (UAVs) are forecasted to expand at a 12.21% CAGR through 2031 as operators seek persistent coverage at lower hourly cost.

Which region will see the highest growth?

Asia-Pacific is expected to register the fastest regional CAGR at 8.51%, driven by procurement in India, Japan, Australia, and South Korea.

What restrains near-term growth?

Budget deferrals in Europe and export-control limitations on advanced sensors delay some programs, trimming about 1.3 percentage points from near-term CAGR.

What is the biggest application area?

Intelligence, surveillance, and reconnaissance (ISR) remain dominant, accounting for 55.42% of 2025 market value and continuing to attract funding.

Page last updated on: