Explosive Trace Detection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

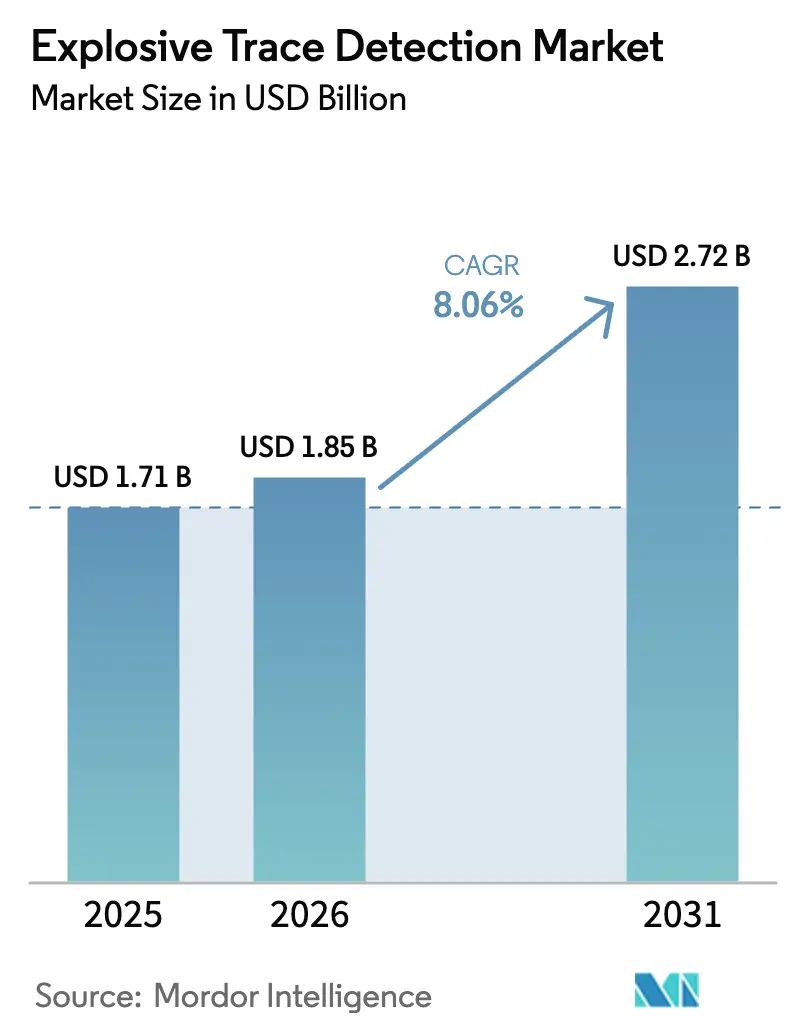

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

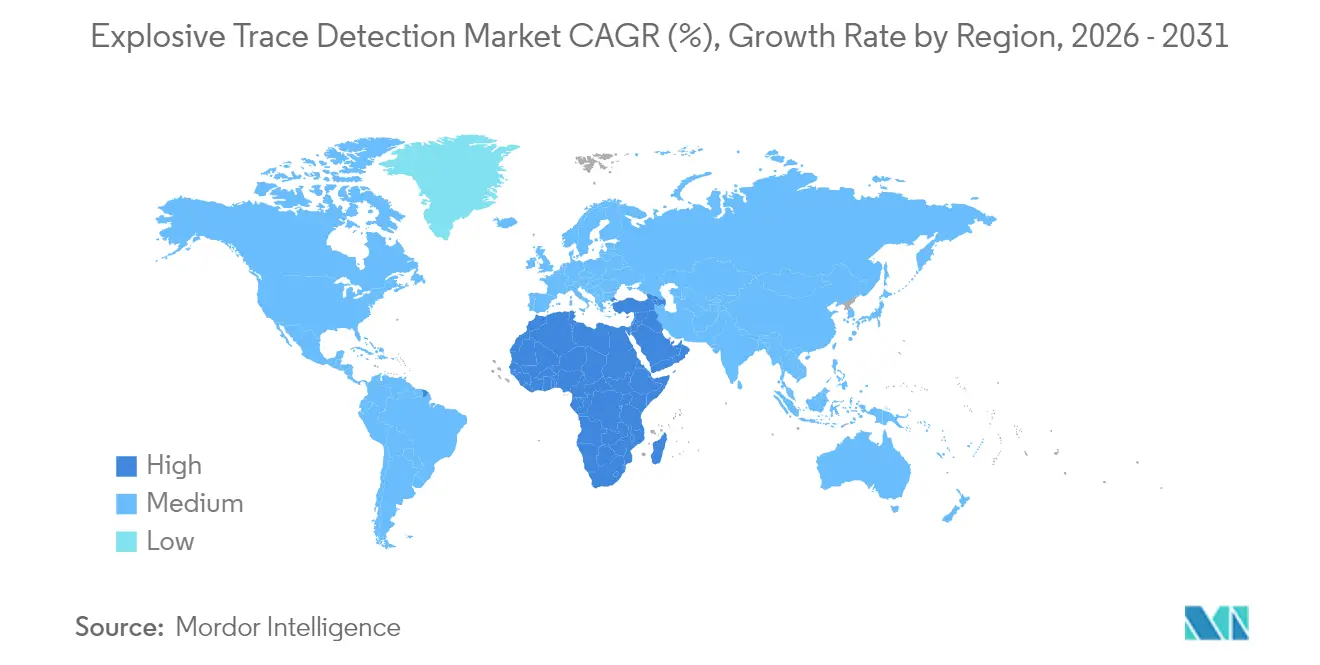

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Explosive Trace Detection Market Analysis by Mordor Intelligence

The explosive trace detection market size was valued at USD 1.71 billion in 2025 and estimated to grow from USD 1.85 billion in 2026 to reach USD 2.72 billion by 2031, at a CAGR of 8.06% during the forecast period (2026-2031). Intensifying global security threats, stricter aviation and cargo regulations, and rapid airport infrastructure investments form the backbone of current demand. Uptake accelerates further because artificial-intelligence-driven false-alarm reduction trims checkpoint delays, while dual-mode vapor–particle sensors extend coverage to drones and automated kiosks. The European Union’s mandate for 100% cargo explosive trace detection (ETD) by 2026, the US Transportation Security Administration (TSA) five-year ETD funding program, and the Middle East’s airport megaprojects reinforce a cycle of procurement upgrades that benefits both incumbent suppliers and emerging innovators.

Key Report Takeaways

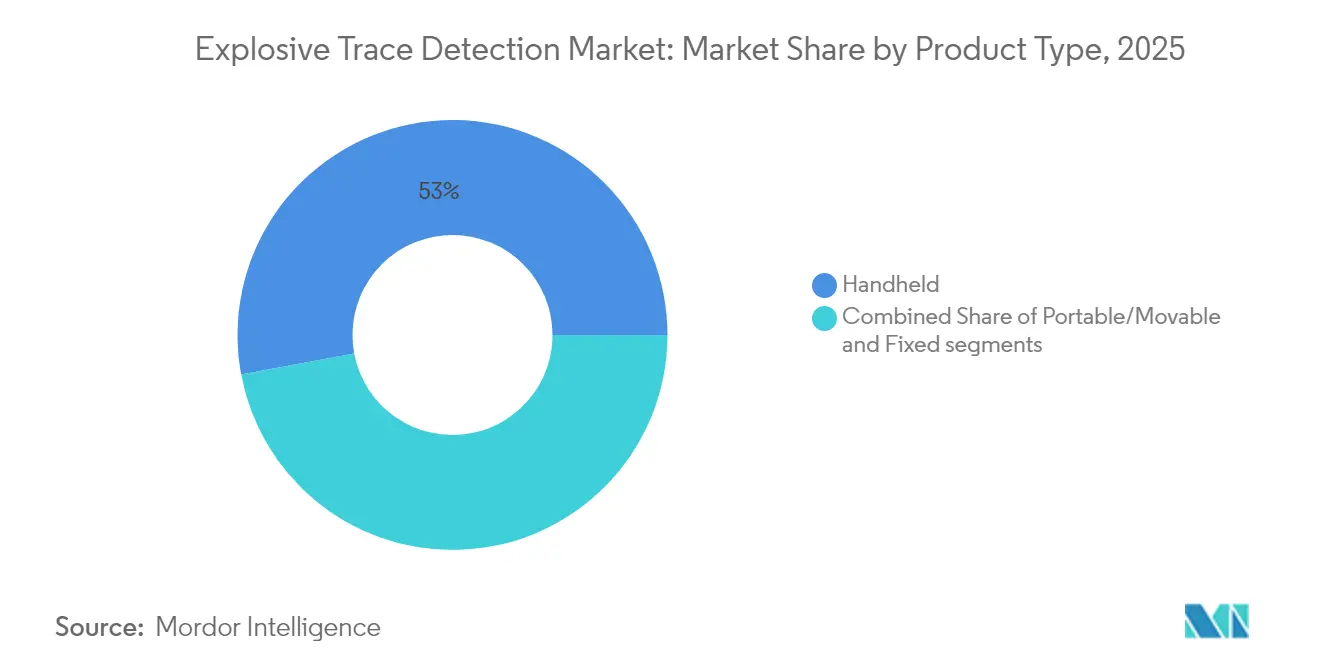

- By product type, handheld systems led with 52.95% revenue in 2025, whereas portable/movable units are projected to grow at a 10.28% CAGR through 2031.

- By detection technology, ion mobility spectrometry captured 57.30% of the explosive trace detection market share in 2025, while Raman and FTIR spectroscopy are set to expand at a 10.37% CAGR during 2026-2031.

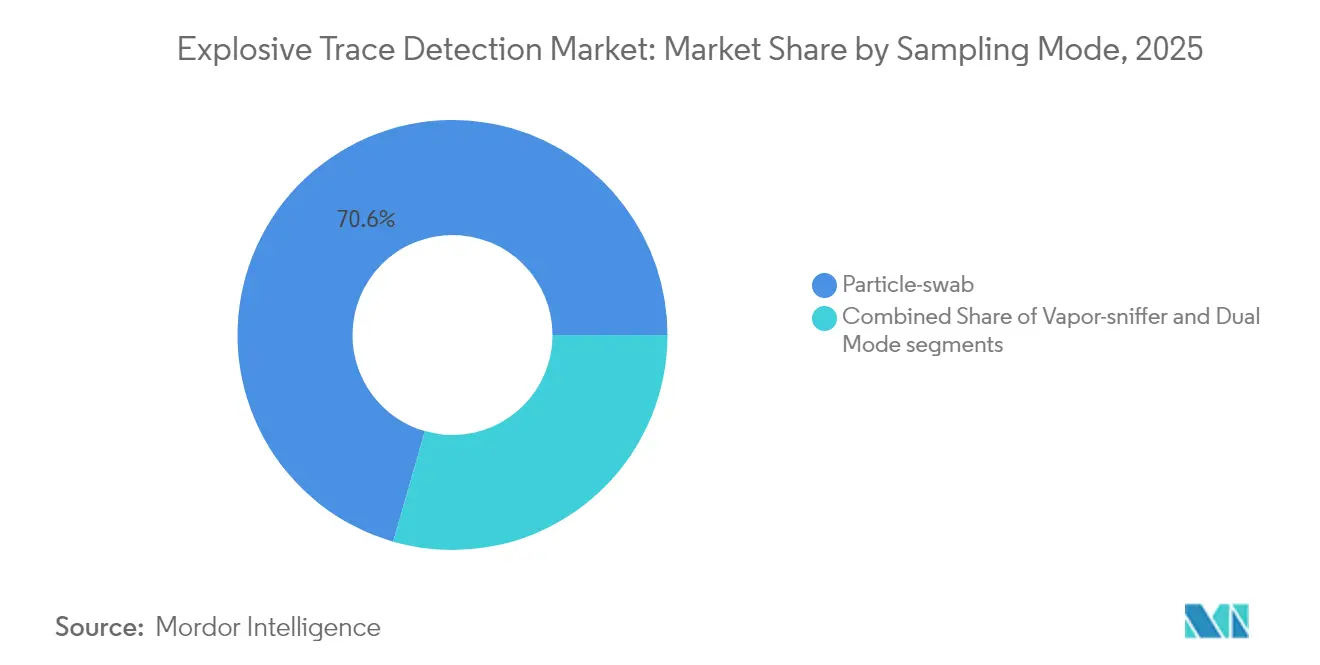

- By sampling mode, particle-swab methods had a 70.55% share of the explosive trace detection market in 2025; dual-mode systems are advancing at a 11.86% CAGR to 2031.

- By end-use sector, commercial applications held 43.05% of 2025 revenue, but cargo and logistics are forecasted to record the fastest 9.79% CAGR up to 2031.

- By geography, North America remained the largest regional market with 42.10% share in 2025, whereas the Middle East and Africa region is poised for a 10.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Explosive Trace Detection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled false-alarm reduction in IMS analyzers | +1.8% | Global, early uptake in North America and EU | Medium term (2–4 years) |

| Mandated 100% cargo ETD screening in EU-27 (2026) | +1.2% | Europe, spillover to global trade routes | Short term (≤ 2 years) |

| Miniaturized dual-mode vapor/particle sensors for drones | +0.9% | Global, defense-heavy regions | Long term (≥ 4 years) |

| Rising airport infrastructure upgrades in Asia | +1.1% | APAC core, expanding to MEA | Medium term (2–4 years) |

| Defense modernization programs | +1.3% | North America, Europe, APAC corridors | Long term (≥ 4 years) |

| Growing demand for contact-less ETD kiosks post-COVID | +0.8% | Global, high-traffic airports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-enabled false-alarm reduction in IMS analyzers

Machine-learning engines embedded in IMS units lower nuisance alarms by up to 40% while retaining detection sensitivity.[1]Source: U.S. Department of Homeland Security, “Emergency Management of Tomorrow: AI Landscape Assessment,” dhs.gov Security agencies value the throughput gains because every false alert historically halts lanes and stresses staff. DHS allocated USD 418 million in FY 2025 for AI-enhanced screening, accelerating retrofits across TSA checkpoints. System integrators now bundle neural-network software updates with service contracts, creating new recurring revenue streams for suppliers while improving passenger experience.

Mandated 100% cargo ETD screening in EU-27 (2026)

The European Commission’s directive forces all air, sea, and land cargo operators to implement ETD screening, driving a procurement wave for thousands of portable and fixed units.[2]Source: European Commission, “Aviation Security Policy,” ec.europa.eu Logistics firms originally concerned about compliance costs are forging leasing deals with OEMs that package equipment, consumables, and remote diagnostics. Non-EU shippers serving European trade lanes adopt identical protocols, effectively globalising the rule set.

Miniaturized dual-mode vapor/particle sensors for drones

Sensor miniaturization enables rotary-wing drones to sniff for traces within denied areas at standoff range. Hybrid bio-electronic designs using silkworm-moth antennae deliver higher sensitivity than conventional MEMS arrays. The US Army SBIR program funds quantum-magnetometer payloads that detect person-borne IEDs, signaling military confidence in aerial ETD’s strategic value.

Rising airport infrastructure upgrades in Asia

Asia-Pacific’s USD 1 trillion pipeline of new terminals and runways requires mass deployment of next-generation ETD lanes. Projects in India, Hong Kong, and Gulf states specify CT X-ray baggage systems paired with high-throughput trace detectors capable of screening 10,000 passengers per hour. OEMs are forming localisation joint ventures to meet offset clauses demanding local manufacturing content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short replacement cycle of consumable swabs | -0.7% | Global, high-volume sites | Short term (≤ 2 years) |

| Lack of global standard for nanogram detection limits | -0.5% | Global, fragmented regulations | Medium term (2–4 years) |

| Supply-chain bottlenecks in semiconductor gases | -0.9% | Global, Asia-Pacific fabs | Short term (≤ 2 years) |

| High total cost of ownership for multi-modal units | -0.6% | Global, budget-constrained users | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short replacement cycle of consumable swabs

Single-use swabs priced between USD 2 and USD 15 accumulate significant recurrent expenditures at checkpoints that screen thousands. TSA-approved consumables are proprietary, locking agencies into specific vendors and reducing price competition. MIT’s chemically modified swabs boost sensitivity but raise per-unit costs, intensifying budget pressure.

High total cost of ownership for multi-modal units

Multi-modal detectors that combine IMS, Raman, and mass spectrometry cost up to USD 100,000 each and require annual service contracts exceeding 15% of the capital price. Smaller airports often defer upgrades or choose single-technology units, slowing overall adoption despite superior threat coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portability Drives Market Evolution

Handheld detectors generated the largest revenue in 2025, accounting for 52.95% of the explosive trace detection market. They appeal to security teams that require mobility within terminals, border checkpoints, and special-event venues. Nevertheless, portable/movable systems are forecast to grow at 10.28% CAGR as longer-life batteries, AI-enhanced analytics, and ruggedised casings make cart-mounted platforms attractive for rapid-deployment scenarios. Bruker RoadRunner and Smiths Detection Sabre 5000 illustrate the trend toward shrinking size without sacrificing sensitivity. Fixed units retain demand in high-volume cargo lines and critical infrastructure, where 24/7 automation justifies the investment.

Operational priorities are shifting. Buyers now evaluate battery swap times, user-interface simplicity, and remote-software update capability alongside baseline detection limits. The explosive trace detection market size for portable units is projected to expand from an estimated USD 460 million in 2025 to almost USD 829 million by 2031, underscoring how portability and throughput align with evolving security doctrines. Handheld devices will remain dominant but will face incremental feature upgrades such as embedded 5G modules for cloud analytics and biometric operator log-in.

By Detection Technology: Spectroscopy Innovation Accelerates

Ion mobility spectrometry maintained 57.30% market presence in 2025, benefiting from decades of regulatory acceptance and sub-minute analysis speed. The explosive trace detection market size tied to IMS platforms will continue to rise, yet Raman and FTIR spectrometers represent the fastest growing niche with a 10.37% CAGR. Their ability to deliver molecular fingerprints reduces false positives linked to common household chemicals, saving secondary-screening labor. Rigaku's TSA-funded R&D demonstrates government trust in Raman to identify new homemade explosive compositions.

Market adoption patterns suggest convergence rather than replacement. OEMs champion hybrid IMS-Raman models that automatically cross-verify alarms, delivering speed and specificity. Mass spectrometry, led by 908 Devices' handheld mass-spec unit, begins to carve out space in forensic and military operations where mission success justifies higher price points. Spectroscopy-only units' explosive trace detection market share could reach double digits by 2031 as algorithmic refinements slash analysis time.

By Sampling Mode: Dual-Mode Systems Gain Momentum

Particle-swab sampling dominated with a 70.55% share in 2025, reflecting ICAO and TSA procedural norms. Even so, vapor-sniffer technology is appealing for stand-off interrogating suspicious vehicles or baggage. Dual-mode architectures that fuse both approaches scale at 11.86% CAGR because they curb operational blind spots. For example, operators can screen external packages by vapor first, then collect swab samples only if elevated risk indicators are triggered.

The model simplifies workflow and boosts lane throughput by reducing unnecessary swab consumption, thereby mitigating the restraint of recurring consumable costs. Field data show dual-mode detectors cut rescreen rates by 20%, improving passenger experience and elevating security perception. The explosive trace detection market size allocated to dual-mode configurations is forecast to triple between 2025 and 2031, assisted by software that dynamically selects the optimal mode based on perceived threat probability.

By End-Use Sector: Cargo Logistics Drives Growth

Commercial aviation remained the top purchaser with 43.05% revenue in 2025, spurred by airport modernisation across Asia and North America. Yet the cargo and logistics sector records the highest 9.79% CAGR because mandatory 100% screening regulations take effect in Europe and are mirrored by trade partners worldwide. Large freight forwarders and express couriers invest in high-throughput conveyor-integrated ETD lanes that can clear 500 consignments per hour.

Defence agencies continue to procure ruggedized handheld units as part of force-protection kits. The explosive trace detection industry sees growth in critical-infrastructure protection, such as power plants and stadiums that integrate fixed ETD portals into access-control systems. Law-enforcement bomb squads embrace pocket-sized detectors able to provide presumptive identification on-scene, shortening evacuation timelines.

Geography Analysis

North America commanded 42.10% revenue in 2025, anchored by TSA’s USD 229.2 million budget and Leidos’ USD 2.6 billion equipment sustainment contract. The region remains a reliable replacement market, with airlines emphasising total cost of ownership and regulatory compliance over disruptive innovation. Europe follows, propelled by the cargo-screening mandate that imposes tight 2026 deadlines on operators.

Asia-Pacific contributes outsized unit volumes as mega-airports open runways and satellite terminals. India’s plan for 220 new airports by 2035 and Hong Kong’s USD 800 million security upgrade highlight the runway expansion wave. The Middle East and Africa register the most rapid expansion at 10.18% CAGR, supported by the USD 35 billion Al Maktoum and USD 50 billion Riyadh hub projects that specify next-generation screening lanes. Latin America witnesses steady yet slower procurement due to budget constraints, often relying on surplus or refurbished equipment. Regional technology preferences differ. North American buyers favor AI-enabled false-alarm suppression, European agencies prioritise ECAC certification harmonisation, Asian airports seek integrated contactless kiosks, and Middle Eastern operators demand high-capacity, dual-energy mobile systems for cargo.

Competitive Landscape

The explosive trace detection market is moderately concentrated. Smiths Detection, Leidos, OSI Systems, Bruker, and 908 Devices comprise the top tier. Smiths Detection reported double-digit organic growth in Q3 2025 on next-generation CTX installations and aims for 6–8% full-year growth. Leidos reinforced its service dominance by winning an eight-year TSA contract worth up to USD 2.6 billion that covers 12,000 ETD units nationwide.

Competition hinges on AI analytics, operator-friendly design, and total cost of ownership. Startups push mass-spectrometry and bio-sensor breakthroughs that pledge higher specificity at lower running costs. Incumbents counter by integrating those sensors into modular platforms, protecting installed footprints with retrofittable upgrades. After-sales service networks and global certification portfolios remain decisive because airport authorities seldom accept unproven vendors.

Mergers and intellectual-property licensing are bridging gaps. Smiths Detection licenses Raman algorithms from Rigaku to expand its portable line, while OSI Systems bundles cloud-based analytics with Eagle mobile units, offering predictive-maintenance dashboards that cut downtime. Patent depth around ion-mobility cell design and drop-resistant vapor inlets form sustained entry barriers for latecomers.

Explosive Trace Detection Industry Leaders

Smiths Detection Group Ltd.

Rapiscan Systems, Inc.

Teledyne Technologies Incorporated

Bruker Corporation

Leidos Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Astrotech Corporation and its subsidiary, 1st Detect Corporation, secured a USD 1.29 million R&D contract from the US Department of Homeland Security to develop the TRACER 1000 explosives detection system. The 30-month project, divided into two phases, aims to enhance detection capabilities against evolving threats, focusing on scalable security solutions using mass spectrometry technology.

- January 2025: Leidos secured a checkpoint sustainment contract with TSA worth up to USD 2.6 billion to maintain 12,000 security units across 430 airports.

Global Explosive Trace Detection Market Report Scope

Explosive trace detection (ETD) is a technology used to detect explosives of small magnitude. These detectors are used to screen baggage and passengers at commercial, military, and government facilities.

The explosive trace detection market is segmented based on product, end-use, and geography. By product, the market is segmented into a handheld, portable/movable, and fixed. By end-use, the market is segmented into commercial, defense, and others. The other segment consists of security agencies such as law enforcement, public safety, homeland security, etc. The market sizing and forecasts have been provided in value (USD million).

| Handheld |

| Portable/Movable |

| Fixed |

| Ion Mobility Spectrometry (IMS) |

| Mass Spectrometry (MS) |

| Raman and FTIR Spectroscopy |

| Differential Ion Trap Mobility |

| Colorimetric and Chemiluminescence |

| Particle-swab |

| Vapor-sniffer |

| Dual Mode |

| Commercial |

| Defense |

| Critical Infrastructure and Law Enforcement |

| Cargo and Logistics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Handheld | ||

| Portable/Movable | |||

| Fixed | |||

| By Detection Technology | Ion Mobility Spectrometry (IMS) | ||

| Mass Spectrometry (MS) | |||

| Raman and FTIR Spectroscopy | |||

| Differential Ion Trap Mobility | |||

| Colorimetric and Chemiluminescence | |||

| By Sampling Mode | Particle-swab | ||

| Vapor-sniffer | |||

| Dual Mode | |||

| By End Use Sector | Commercial | ||

| Defense | |||

| Critical Infrastructure and Law Enforcement | |||

| Cargo and Logistics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the explosive trace detection market?

The explosive trace detection market stands at USD 1.85 billion in 2026 and is projected to rise to USD 2.72 billion by 2031.

Which product category leads the explosive trace detection market?

Handheld detectors hold the lead, capturing 52.95% revenue in 2025 thanks to their operational flexibility.

Why is the cargo and logistics sector growing fastest?

A European Union mandate requiring 100% cargo ETD by 2026 pushes global logistics firms to invest, resulting in a 9.79% forecast CAGR for this segment.

Which region will experience the quickest growth in explosive trace detection spending?

The Middle East and Africa region is expected to expand at a 10.18% CAGR through 2031, driven by multi-billion-dollar airport megaprojects.

How are artificial-intelligence tools improving explosive trace detection systems?

AI-enabled algorithms cut false-alarm rates by up to 40%, accelerating passenger throughput while maintaining sensitivity.

What is the biggest operational cost restraint for explosive trace detection operators?

The recurring purchase of single-use consumable swabs, priced between USD 2 and USD 15 each, significantly inflates total cost of ownership for high-volume checkpoints.

Page last updated on: