AI-Powered Mental Health Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

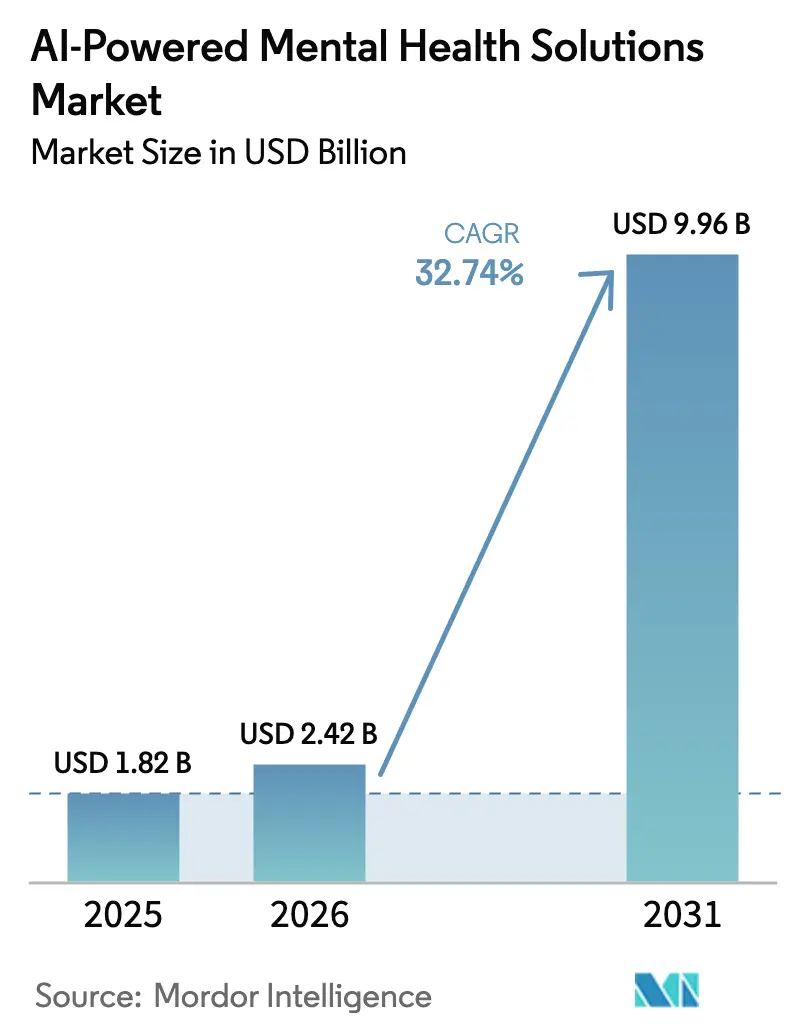

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 9.96 Billion |

| Growth Rate (2026 - 2031) | 32.74% CAGR |

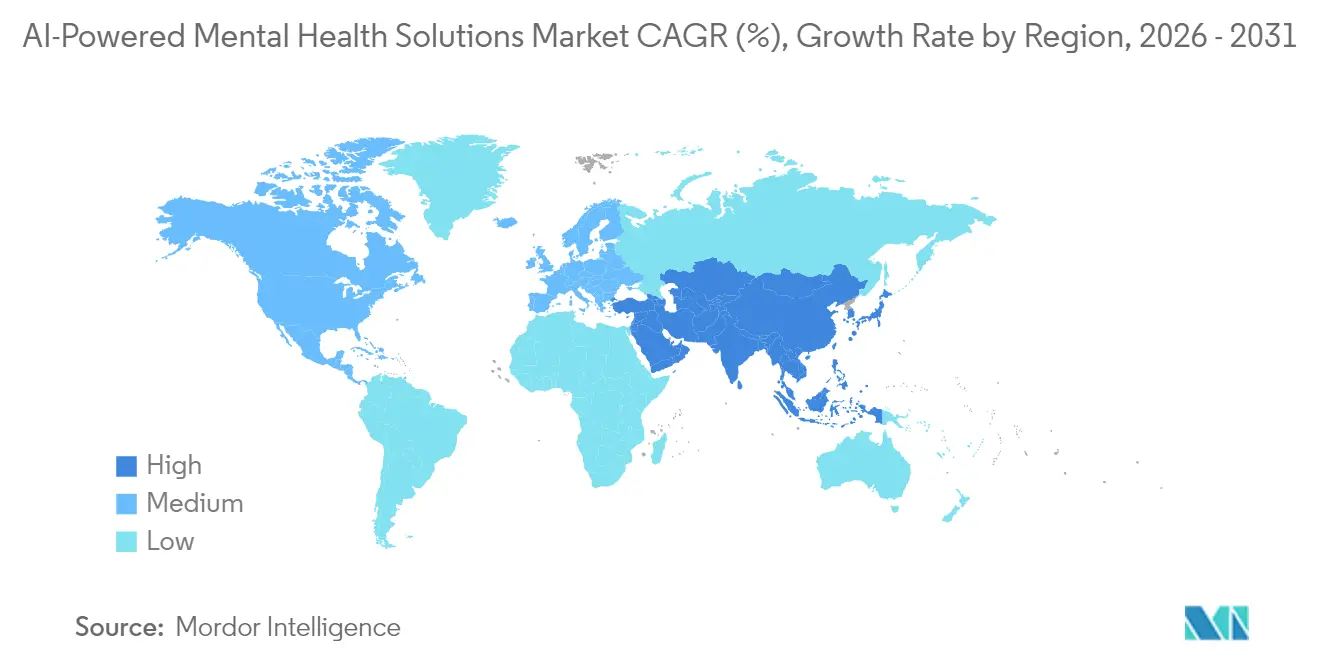

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Powered Mental Health Solutions Market Analysis by Mordor Intelligence

The AI-Powered Mental Health Solutions Market size is expected to grow from USD 1.82 billion in 2025 to USD 2.42 billion in 2026 and is forecast to reach USD 9.96 billion by 2031 at 32.74% CAGR over 2026-2031.

Explosive expansion reflects mounting global disease burden, Medicare’s proposed reimbursement codes, and large-language-model breakthroughs that shorten development timelines for prescription digital therapeutics. Enterprises accelerate benefit adoption after audits show 71% of employees experience stress-related productivity losses. Meanwhile, multimodal emotional-AI sensors inside wearables detect crises up to 7.2 days before human recognition with 89.3% accuracy. Regional dynamics remain pivotal:

Key Report Takeaways

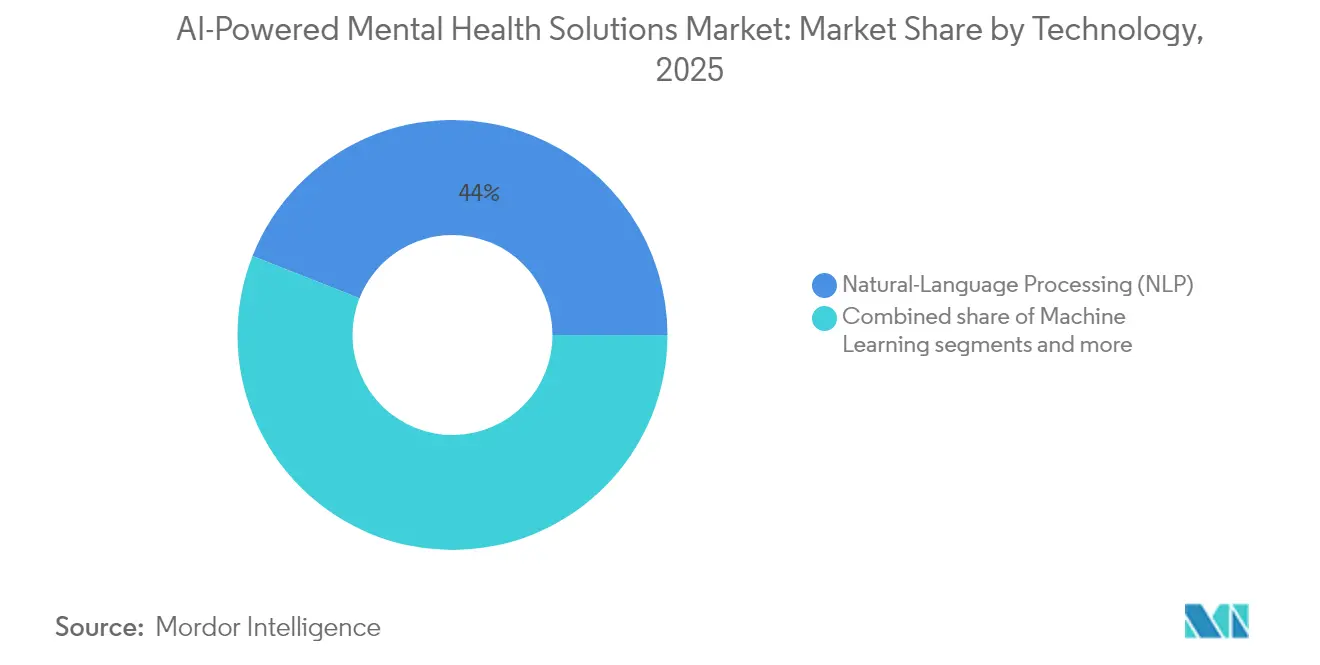

- By technology, Natural Language Processing captured 44.02% of AI powered mental health solutions market share in 2025; Machine Learning is advancing at a 34.36% CAGR through 2031.

- By solution type, Treatment Personalization commanded 39.02% of the AI powered mental health solutions market size in 2025, while Diagnostics Assistance is projected to expand at a 34.78% CAGR.

- By deployment mode, cloud-based platforms controlled 55.32% revenue in 2025 and are forecast to grow at a 34.89% CAGR to 2031.

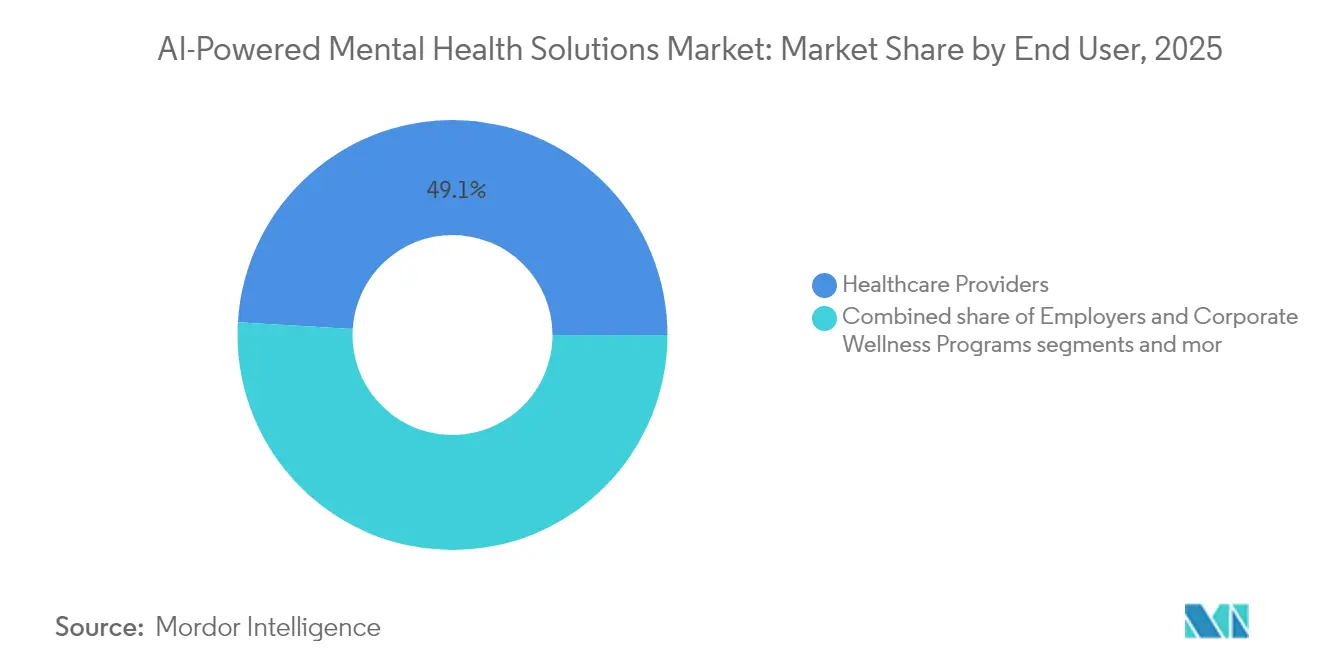

- By end user, hospitals and clinics held 49.05% share in 2025; research institutions register the fastest growth with a 34.72% CAGR.

- By geography, North America contributed 41.42% revenue in 2025, whereas Asia-Pacific is expected to post a 34.41% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI-Powered Mental Health Solutions Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid proliferation of AI-driven mental-health mobile apps | +8.2% | Global, with concentration in North America & APAC | Short term (≤ 2 years) |

| Reimbursement expansion for digital therapeutics | +7.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Enterprise demand for workforce-wellness AI platforms | +6.8% | Global, led by North America corporate sector | Short term (≤ 2 years) |

| Integration of multimodal emotional-AI sensors in wearables | +5.9% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Foundation-model fine-tuning for psychotherapy chatbots | +4.7% | Global, with R&D concentration in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of AI-Driven Mental-Health Mobile Apps

More than 10 000 mental-health apps now incorporate AI, compared with fewer than 1 000 five years ago. Randomized trials show Therabot and similar tools achieve symptom reductions comparable to human therapy across major depressive, generalized-anxiety, and feeding disorders. Twenty-four percent of U.S. adults already use LLMs for emotional support, marking a shift among help-averse demographics. Employers document 12% productivity gains and 67% retention improvements after deploying mindfulness apps that include AI-generated coping exercises. FDA breakthrough-device designations for mobile therapeutics such as Wysa’s chronic-pain module legitimize app-based care inside clinical workflows.

Reimbursement Expansion for Digital Therapeutics

Medicare’s 2025 fee schedule introduces three new billing codes for providers integrating digital mental-health tools. The U.S. Food and Drug Administration and the Centers for Medicare & Medicaid Services now pilot outcomes-based payment models: reimbursement is tied to functional-improvement endpoints, signaling durable revenue streams. Germany, France, the U.K., and Belgium use DiGA-style frameworks that fund artificial-intelligence-enabled therapeutics once clinical-evidence thresholds are met. Vendors respond by launching large phase-III trials; Rejoyn secured U.S. clearance on the strength of cognitive-control training data. Payer support expands service reach to underserved Medicaid and rural populations.

Enterprise Demand for Workforce-Wellness AI Platforms

Corporate absenteeism linked to stress costs USD 300 billion annually, prompting boards to prioritize AI monitoring and triage software. Natural-language analytics embedded in collaboration tools spot burnout indicators and trigger outreach by licensed counselors. Johns Hopkins’ Balance program screened 56 442 staff and found 53% moderate-or-higher risk, validating AI risk stratification at scale. Headspace’s pivot from meditation to insurer-paid therapy underscores employer demand for end-to-end behavioral-health solutions. Cloud delivery accelerates rollouts across hybrid workforces.

Integration of Multimodal Emotional-AI Sensors in Wearables

Wearables blending facial-expression analytics, electrodermal activity, and EEG reach real-time emotion-recognition accuracy of 99.3%. Combined with chatbots, these devices deliver just-in-time interventions when biometric thresholds predict distress. Skin-potential variance differentiates major-depressive disorder from controls with 78% accuracy, indicating path to non-invasive diagnostics. Regulators tighten privacy rules: the EU AI Act and HIPAA push vendors toward on-device processing and federated learning. Early payer pilots reimburse continuous-monitoring bundles as hospital-avoidance tools.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical validation gap for algorithmic recommendations | -4.3% | Global, particularly stringent in EU & North America | Medium term (2-4 years) |

| Fragmented data privacy regulations | -3.8% | Global, with varying intensity across jurisdictions | Long term (≥ 4 years) |

| Bias risks in emotion-AI training datasets | -2.9% | Global, with heightened scrutiny in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Clinical Validation Gap for Algorithmic Recommendations

Diagnostic accuracy for AI mental-health tools ranges 21–100%, unsettling regulators. The FDA now demands pharmaceutical-grade evidence; small firms partner with universities to manage trial costs. Bias studies show model reliability drops in diverse cohorts, compelling developers to expand datasets. Clinicians remain wary until reproducible outcomes appear in peer-reviewed journals, slowing hospital procurement cycles despite patient enthusiasm.

Fragmented Data-Privacy Regulations

The EU AI Act classifies most mental-health AI as high risk, mandating conformity assessments from February 2025. Vendors juggling HIPAA in the U.S. and GDPR in Europe must architect dual data flows. Italy’s EUR 5 million fine against Replika signals enforcement zeal. Conflicting erasure and retention mandates escalate engineering costs. The proposed EU Charter of Digital Patients’ Rights adds governance layers that limit fully autonomous decision-making.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Machine Learning Drives Innovation

The AI powered mental health solutions market saw Natural Language Processing hold 44.02% revenue in 2025, yet Machine Learning is growing at 34.36% CAGR. A multimodal EEG-and-speech classifier achieved 97.53% depression-diagnosis accuracy. Vendor road maps increasingly converge affective computing, predictive analytics, and LLM chat to create full-stack platforms. Hospitals note shorter triage times when AI chatbots collect structured patient histories before clinician review. Cloud hyperscalers integrate mental-health APIs into existing health-data ecosystems, boosting the AI powered mental health solutions market size attached to Machine Learning modules.

Emergent transformer models run inside virtual private clouds to meet data-sovereignty demands. Predictive-analytics dashboards benchmark workforce mood, enabling proactive resource allocation. More than 30 funding rounds now target bespoke therapy LLMs, underscoring data-asset primacy over algorithm novelty. Competitive advantage will accrue to vendors that certify under ISO/IEC safety standards and negotiate payer reimbursement at scale.

By Solution Type: Diagnostics Acceleration

Treatment Personalization held 39.02% revenue in 2025; Diagnostics Assistance is projected to register the highest 34.78% CAGR. A voice-biomarker tool flags moderate-to-severe depression within 25 seconds at 71.3% sensitivity and 73.5% specificity. Early identification lowers downstream costs, attracting payer interest. Monitoring and Management suites pair wearable data with chat-based coaching for continuous feedback loops. Virtual-reality exposure therapy products deliver compelling PTSD outcomes, expanding “Other Applications” within the AI powered mental health solutions market.

Providers prefer integrated solutions that span screening, personalization, and relapse prevention. Vendors focus pipelines on high-burden conditions such as migraine (CT-132) and schizophrenia negative symptoms (CT-155), banking on clear regulatory pathways to secure premium pricing.

By Deployment Mode: Cloud Dominance Persists

Cloud deployments accounted for 55.32% of 2025 revenue and maintain a 34.89% CAGR, underscoring scalability benefits. HITRUST- and FedRAMP-certified hyperscalers offer encryption and role-based access that satisfy audits. Small clinics favor subscription models over on-premise capital expense. Hybrid architectures emerge for defense clients requiring local processing. Region-partitioned instances address AI-Act localization rules, broadening the AI powered mental health solutions market appeal.

No-code toolkits let clinicians design screening flows without programming backgrounds. Patient engagement rises 40% once platforms enable multi-device access. Freeing capital from servers to clinical trials accelerates evidence generation necessary for reimbursement.

By End User: Research Institutions Accelerate

Hospitals and clinics generated 49.05% demand in 2025, while research institutions lead growth at 34.72% CAGR. NIH-funded trials report 60% depression-symptom reduction after AI-guided CBT delivered over four weeks. Academic endorsements boost vendor credibility during regulatory review. Employer programs now cover 17 million lives via integrated measurement suites that quantify behavioral-health progress. Direct-to-consumer apps attract younger demographics who prefer self-service over office visits.

Government hotlines deploy multilingual chatbots to bridge clinician shortages in rural zones. Payers pilot value-based contracts that reimburse only when AI interventions deliver measured outcomes, spurring vendors to embed analytics dashboards for transparent reporting.

By Mental-Health Condition: PTSD Solutions Surge

Depression retained 37.63% share in 2025, yet PTSD products are poised for 35.12% CAGR amid geopolitical conflict. Virtual-reality exposure combined with emotion tracking outperforms group therapy, cutting session counts by 30%. Anxiety solutions integrate predictive analytics for early nudges that avert symptom escalation.

Stress-management modules dominate corporate rollouts, channeling wearable alerts into coping micro-lessons. Substance-use disorder platforms leverage deep-learning on electronic medical-record data to deliver 48-hour relapse warnings. Niche offerings around eating disorders and neurodivergence gain traction through domain-specific datasets.

Geography Analysis

North America generated 41.42% revenue in 2025, fueled by FDA clearances (Rejoyn, SleepioRx) and Medicare’s reimbursement roadmap. Venture capital remains abundant: Slingshot AI raised USD 30 million to develop therapy-specific LLMs.

Europe sets global standards through the EU AI Act and GDPR. Germany’s DiGA catalog reimburses more than 40 digital therapeutics. Italy’s EUR 5 million Replika fine highlights enforcement strength. Limbic secured USD 14.7 million to integrate AI clinical decision support into electronic health records.

Asia-Pacific leads growth at 34.41% CAGR. Mental disorders contribute 5% of disability-adjusted life years region-wide. China matches the U.S. in digital-therapeutics approvals; South Korean GPT-4-powered chatbots receive high empathy ratings. Localization strategies—language adaptation and culturally sensitive prompt engineering—differentiate offerings.

South America faces projected GDP losses of USD 7.3 trillion from 2020-2050 due to mental-health and non-communicable diseases. Ministries in Brazil and Colombia pilot AI chatlines on low-cost mobile platforms. In the Middle East and Africa, SMS-based AI screening tools reach areas with limited broadband; sub-Saharan prevalence rates of 26.9% depression indicate sizable unmet need.

Competitive Landscape

The AI powered mental health solutions market exhibits moderate fragmentation with accelerating consolidation. Teladoc bought UpLift for USD 30 million to support its BetterHelp unit after a revenue slump. April Health merged with Wysa, combining chatbots and live therapy to scale blended-care models. Woebot’s 2025 app closure contrasts sharply with Spring Health’s USD 3.3 billion valuation, illustrating bifurcation between evidence-rich platforms and under-capitalized peers.

Competitive edge relies on proprietary datasets, clinician-friendly interfaces, and regulatory clearances. FDA-cleared therapeutics like CT-132 for migraine and CT-155 for schizophrenia attract insurer contracts. Vendors blending AI triage with human oversight satisfy regulators, positioning them for payer partnerships.

Strategic alliancs with cloud providers and EHR vendors streamline deployment. Performance metrics—engagement, remission rates, and cost savings—now decide contract renewals more than feature sets. Market entrants must therefore bring clinical efficacy and privacy compliance to remain competitive within the AI powered mental health solutions market.

AI-Powered Mental Health Solutions Industry Leaders

Woebot Health

Wysa Ltd

Lyra Health, Inc

Talkspace

Cognoa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Slingshot AI launched Ash, a therapy-specific LLM.

- May 2025: Mentaily raised USD 3 million for AI assessment tools

Global AI-Powered Mental Health Solutions Market Report Scope

As per the scope of the report, the AI-powered mental health solutions market is witnessing a transformative shift, leveraging AI to enhance and revolutionize mental health care delivery. This sector combines innovative advanced technologies with mental health expertise to offer personalized, accessible, and effective solutions for individuals seeking support.

The AI-powered mental health solutions market is segmented by software solutions (machine learning (ML) models, natural language processing (NLP), and other software solutions), components (software-as-a-service and hardware), applications (diagnostics assistance, treatment personalization, monitoring and management, and other applications), end users (hospitals and clinics, mental health centers, research institutions and institutional sales, and other end users), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Machine Learning |

| Natural-Language Processing (NLP) |

| Emotion AI/ Affective Computing |

| Predictive Analytics |

| Others Software Solutions |

| Diagnostics Assistance |

| Treatment Personalization |

| Monitoring and Management |

| Other Applications |

| Other Solutions |

| Cloud-Based |

| On-Premise |

| Individuals |

| Employers & Corporate Wellness Programs |

| Healthcare Providers |

| Payers |

| Government & Non-Profit Organizations |

| Depression |

| Anxiety Disorders |

| Stress Management |

| Post-Traumatic Stress Disorder (PTSD) |

| Substance-Use Disorders |

| Other Conditions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Machine Learning | |

| Natural-Language Processing (NLP) | ||

| Emotion AI/ Affective Computing | ||

| Predictive Analytics | ||

| Others Software Solutions | ||

| By Solution Type | Diagnostics Assistance | |

| Treatment Personalization | ||

| Monitoring and Management | ||

| Other Applications | ||

| Other Solutions | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By End User | Individuals | |

| Employers & Corporate Wellness Programs | ||

| Healthcare Providers | ||

| Payers | ||

| Government & Non-Profit Organizations | ||

| By Mental-Health Condition | Depression | |

| Anxiety Disorders | ||

| Stress Management | ||

| Post-Traumatic Stress Disorder (PTSD) | ||

| Substance-Use Disorders | ||

| Other Conditions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the AI powered mental health solutions market in 2026?

The AI powered mental health solutions market size is USD 2.42 billion in 2026 and is projected to grow at a 32.74% CAGR over 2026-2031.

Which technology is expanding the quickest?

Machine Learning systems are advancing at a 34.36% CAGR, the fastest among core technologies.

What motivates companies to buy AI mental-health platforms?

Firms report lower absenteeism and higher retention after deploying AI monitoring and coaching, turning mental-health spending into measurable productivity gains.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to lead with a 34.41% CAGR as mobile-first deployments address rising mental-health burdens.

What U.S. policy change accelerates adoption?

Medicare´s new billing codes for digital mental-health treatments, slated for 2025, establish secure reimbursement pathways for providers.

How are wearables reshaping mental-health care delivery?

Sensors detecting emotion and physiological stress combine with chatbots to provide personalized interventions, achieving up to 99.3% emotion-recognition accuracy and enabling preventive care.

Page last updated on: