AI In Regulatory Information Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 18.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Regulatory Information Management Market Analysis by Mordor Intelligence

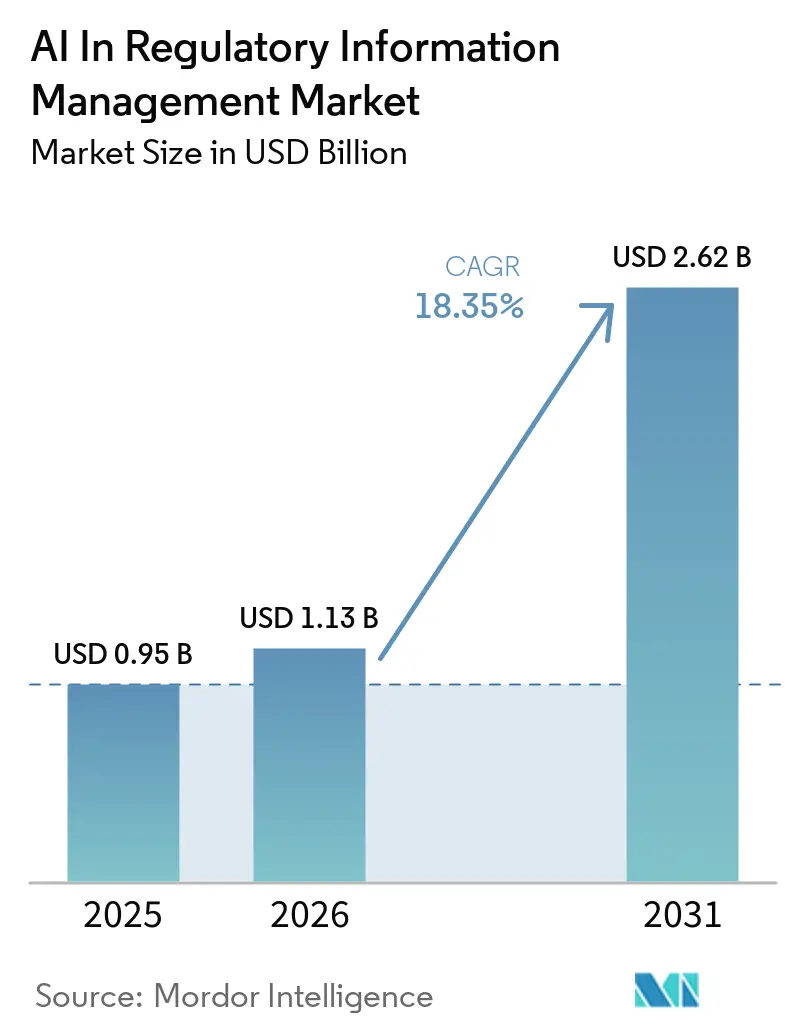

The AI In Regulatory Information Management Market size is projected to expand from USD 0.95 billion in 2025 and USD 1.13 billion in 2026 to USD 2.62 billion by 2031, registering a CAGR of 18.35% between 2026 to 2031.

This expansion reflects a structural shift in life sciences operations, where AI is moving from pilot programs into core systems that manage submissions, regulatory intelligence, and compliance work across many health authorities at the same time. Single dossiers now run to more than 100,000 pages, and global regulatory teams must adapt content for multiple jurisdictions with changing rules, which manual processes cannot handle at the pace now required. The FDA approved 143 NDAs and BLAs in fiscal 2025, while FAERS received more than 20 million adverse event reports in 2024, compared with 2.2 million in 2020, which strengthens the case for AI-enabled triage and workflow automation. Japan made eCTD 4.0 the exclusive format for new drug applications from April 2026, and China issued formal implementation opinions for “AI + Drug Regulation” in 2026 with phased goals through 2035, which supports broader adoption across the AI in regulatory information management market. Validation demands, explainability requirements, and weak legacy metadata still slow implementation, but those same conditions favor vendors that already offer validated architectures, audit trails, and strong data remediation support.

Key Report Takeaways

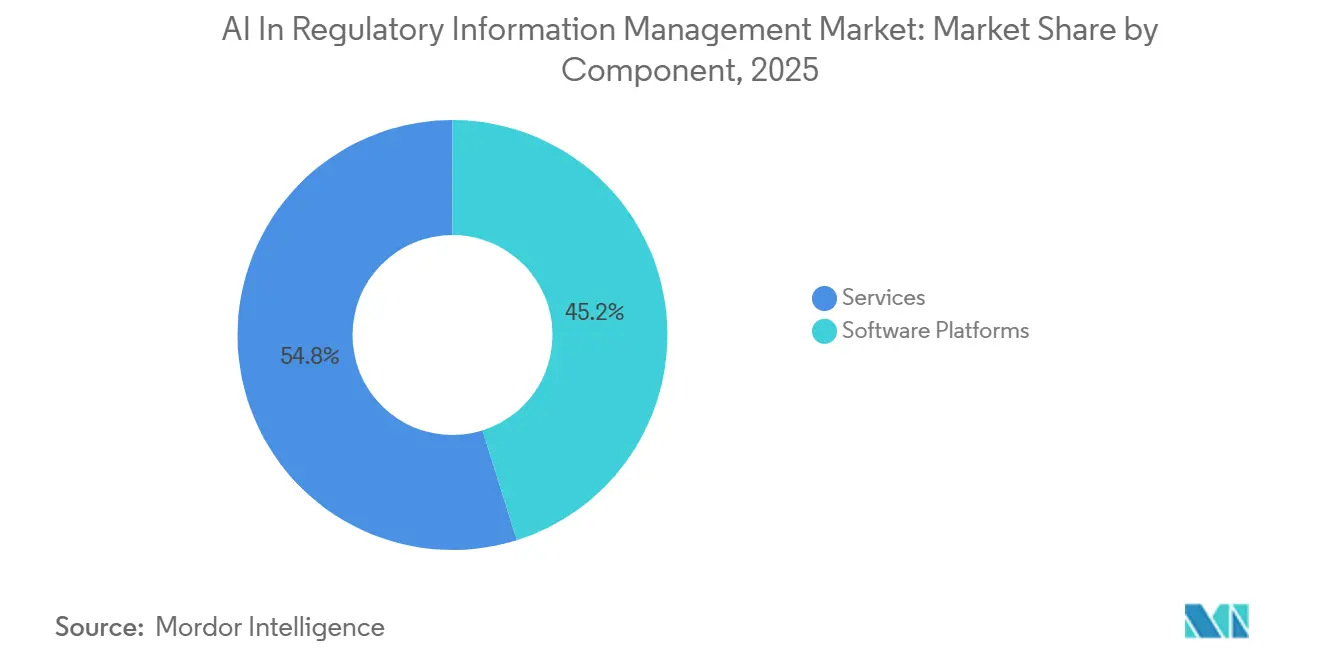

- By component, Software Platforms held 45.16% in 2025, while Services is forecast to expand at 20.88% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 38.17% in 2025, while on-premises deployment is projected to grow at 19.12% CAGR through 2031.

- By AI capability, NLP and document intelligence held 39.29% in 2025, while predictive analytics and risk scoring is projected to advance at 20.19% CAGR through 2031.

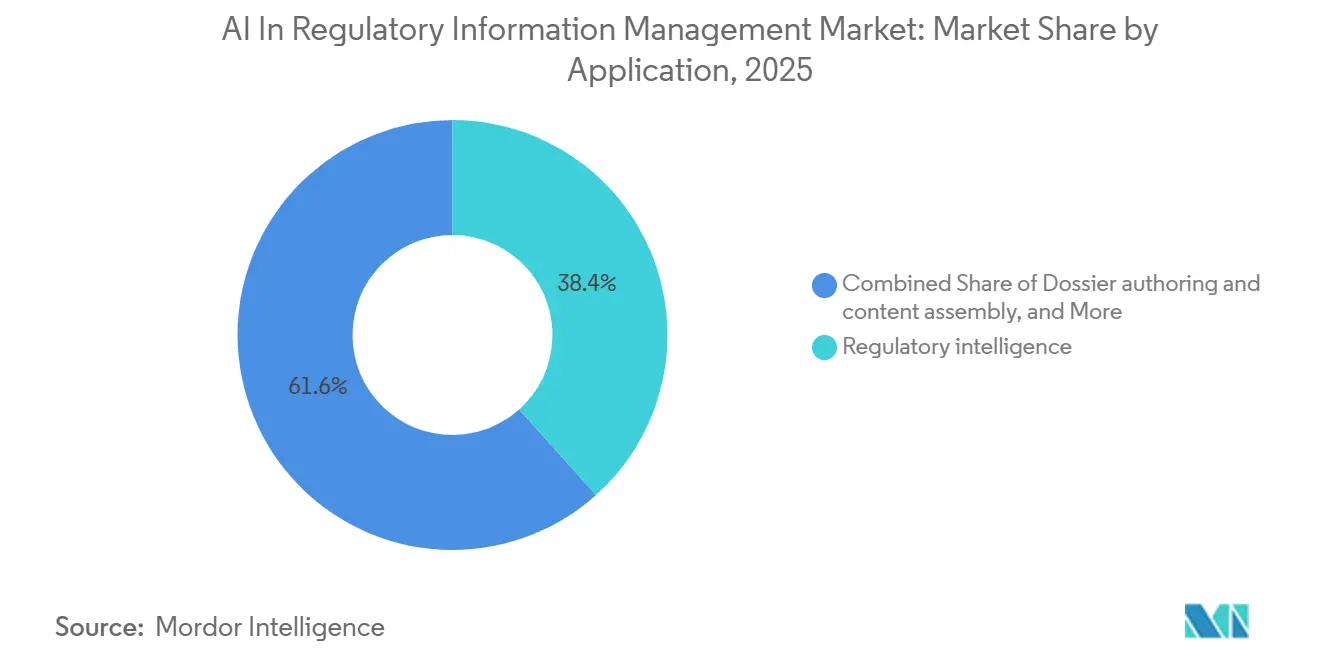

- By application, regulatory intelligence accounted for 38.37% in 2025, while data migration and master data stewardship is projected to grow at 21.33% CAGR through 2031.

- By end user, pharmaceutical companies held 36.72% in 2025, while medical device and diagnostics companies are forecast to expand at 20.33% CAGR through 2031.

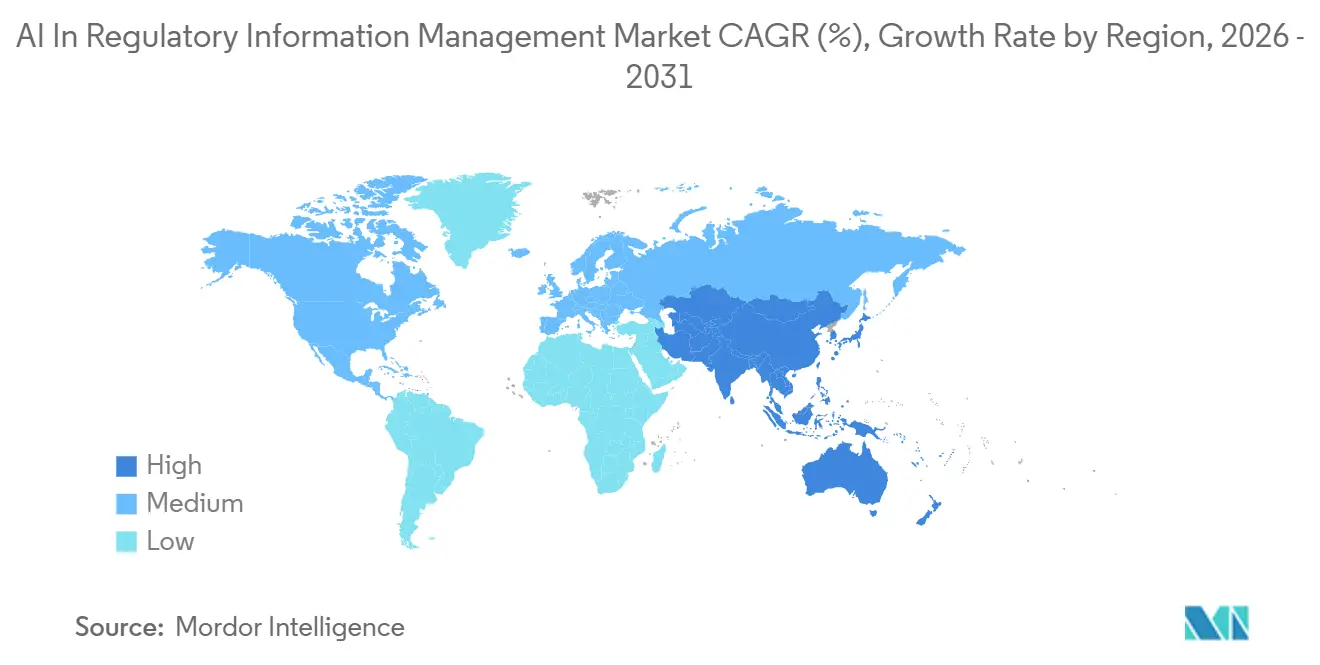

- By geography, North America held 39.18% in 2025, while Asia-Pacific is projected to grow at 19.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Regulatory Information Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Submission and Variation Volumes | +2.5% | Global, highest intensity in North America and Europe | Short term (≤ 2 years) |

| Pressure to Shorten Dossier Cycle Times | +2.8% | Global, concentrated in PDUFA- and EMA-governed markets | Short term (≤ 2 years) |

| Cloud-native RIM Consolidation Programs | +2.2% | North America and Europe, early adoption in core APAC markets | Medium term (2-4 years) |

| Continuous Regulatory Intelligence Automation | +1.8% | Global | Short term (≤ 2 years) |

| eCTD 4.0 and IDMP Structured-data Readiness | +3.0% | North America, EU, Japan, with spillover to South Korea, Canada, and Australia | Medium term (2-4 years) |

| Health-authority Query Mining and Response Reuse | +1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Submission and Variation Volumes: A Scale Problem Beyond Manual Capacity

The AI in regulatory information management market is being driven by a workload curve that manual teams cannot absorb at current filing volumes. The FDA approved 143 NDAs and BLAs in fiscal 2025, and FAERS received more than 20 million adverse event reports in 2024, which shows how sharply regulated content volumes have expanded. Each approval also creates follow-on variations, renewals, labeling updates, and commitment tracking work, so the regulatory burden extends well beyond the first submission milestone. Large pharmaceutical teams already manage hundreds of submissions each month, which makes scale, speed, and internal consistency more difficult to maintain with manual methods alone. This is pushing regulatory groups to shift effort away from repetitive document production and toward scientific judgment, review strategy, and issue resolution. The result is recurring demand for AI-enabled RIM tools because the workload driver is structural and not limited to one temporary automation cycle.

Pressure to Shorten Dossier Cycle Times: Competitive Windows Measured in Weeks

The AI in regulatory information management market is also benefiting from stronger pressure to shorten drafting, review, and publishing timelines. Review windows are commercially important, so companies want earlier draft completion, cleaner cross-functional coordination, and fewer late-stage rework cycles. IBM said its Regulate.AI platform reduced regulatory writer time by 50% to 60%, while Yseop and Indegene both advanced automation roadmaps aimed at faster medical writing and dossier preparation[1]IBM, “Enabling Acceleration of Collaborative Regulatory Authoring with Regulate.AI,” IBM, ibm.com. Faster authoring also improves quality because teams can spend more time reviewing scientific logic and less time repairing inconsistencies across modules. That matters because inconsistencies across sections often trigger questions, information requests, and avoidable review friction. Vendors that combine authoring, version control, reuse, and publishing inside a validated workflow are therefore gaining stronger attention than stand-alone drafting tools.

eCTD 4.0 and IDMP Structured-data Readiness: Infrastructure for the AI-Native Submission Era

The shift from document-centered filing to structured, data-centered submission models is a major force behind the AI in regulatory information management market. PMDA made eCTD 4.0 the exclusive format for new drug applications from April 2026, and EMA’s 2026 to 2028 data and AI workplan reinforces a wider move toward data-first regulatory operations[2]European Medicines Agency, “Network Data Steering Group Workplan 2026-2028 Data and Artificial Intelligence in Medicines Regulation,” EMA, ema.europa.eu. AI cannot automate reliably when metadata is inconsistent, so structured fields, controlled vocabularies, and harmonized product master data are becoming operational necessities rather than optional upgrades. IDMP-oriented enrichment work is therefore concentrating near-term spending among companies that need cleaner product data before broader automation can work at scale. This creates a compounding effect because each increment of structured data improves automation across submission planning, lifecycle tracking, and variation management. Vendors that were designed around data models instead of document storage are better placed to benefit as these standards take hold.

Continuous Regulatory Intelligence Automation: From Reactive Monitoring to Proactive Risk Management

The AI in regulatory information management market is increasingly shaped by the need to monitor rule changes across many authorities, languages, and document types. Global regulatory monitoring now spans hundreds of sources, and manual review struggles to keep pace with update frequency, language diversity, and changing format requirements. ArisGlobal reported 90% accuracy and 50% faster processing in a GenAI-enabled regulatory intelligence pilot, while Clarivate launched an AI-powered Regulatory Assistant covering 38 languages, 80-plus countries, and 328,000-plus curated regulatory documents. China’s NMPA Information Centre had already published AI application work for drug regulation, and the 2026 implementation opinions elevated intelligent regulatory intelligence agents into a national priority. Multilingual semantic mapping is now a real competitive advantage because important updates arrive in Japanese, Chinese, and many local languages that legacy English-first databases do not cover well. That is why regulatory intelligence is moving from a passive monitoring task toward a proactive risk-management layer inside enterprise RIM programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GxP Validation and AI Governance Burden | -2.0% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Fragmented Global Data Standards | -1.8% | Global, most pronounced in Asia-Pacific and MEA | Medium term (2-4 years) |

| Explainability During Inspections and HA Challenge | -1.2% | North America and Europe | Medium term (2-4 years) |

| Weak Metadata Governance in Legacy RIM Estates | -1.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GxP Validation and AI Governance Burden: A Compliance Architecture Mismatch

The AI in regulatory information management market still faces a governance burden because many validation models were built for deterministic software and not for probabilistic AI outputs. The FDA’s January 2025 draft guidance introduced a seven-step credibility framework for AI used to support regulatory decision-making for drugs and biological products, which increases evidence, testing, and documentation expectations. EMA’s reflection paper on AI in the medicinal product lifecycle also makes clear that AI use needs risk-based controls, human oversight, traceability, and a documented lifecycle approach. These requirements slow implementation in quality-critical workflows because companies must validate both the system and the role of its outputs in regulated decisions. That doubles governance work for many use cases and raises the bar for new entrants that lack established compliance processes. The burden does not stop adoption, but it does favor vendors that can offer locked models, audit trails, and inspection-ready evidence packages.

Fragmented Global Data Standards: An Obstacle Embedded in Foundational Infrastructure

The AI in regulatory information management market is also constrained by fragmented data standards across jurisdictions. Japan’s 2026 eCTD 4.0 mandate, Europe’s data and AI workplan, and China’s phased AI regulation agenda all point to modernization, but they do not create one shared implementation path. Differences in data models, vocabularies, and submission expectations mean companies still need to tailor content and workflows market by market. That weakens the promise of out-of-the-box multi-country automation and increases the amount of customer-specific configuration required. The problem is more visible in complex product categories where definitions, manufacturing changes, and lifecycle rules vary across authorities. This extends migration timelines, raises implementation costs, and keeps configurable regulatory platforms more relevant than generic AI solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground as Enterprises Prioritize Platform Value Realization

Software Platforms held 45.16% of the AI in regulatory information management market share in 2025, while Services is projected to expand at 20.88% CAGR through 2031. Platform demand remained strongest among large biopharma companies that had already centralized submission, registration, and intelligence workflows on cloud RIM suites. Veeva said more than 450 companies, including 19 of the top 20 global biopharma firms, operated on its RIM platform in 2025, which shows how deeply unified enterprise platforms are already embedded in the top tier. That depth of adoption gives software vendors a strong installed base, but it also means the largest accounts are less open to net-new license displacement than they were earlier in the digitization cycle. As a result, the software layer remains strategically central in the AI in regulatory information management market, but its growth now depends more on added capability depth than on pure seat expansion.

Services are growing faster because many companies still need outside support to make those platforms work at enterprise scale. GxP-ready implementation, migration design, validation, taxonomy cleanup, and operating model redesign all require skills that many regulatory teams do not hold internally. Mid-sized biopharma companies and emerging sponsors also rely on service partners for publishing, dossier preparation, and regulatory intelligence operations when internal teams are lean. This makes value realization a bigger spending priority than software ownership alone, especially after the initial platform decision has already been made. In the AI in regulatory information management industry, this keeps services as the clearest growth outlet because enterprise demand is shifting from platform acquisition toward platform activation and sustained usage.

By Deployment Mode: On-premises Rebound Signals Data Sovereignty Pressures

Cloud-based deployment accounted for 38.17% of the AI in regulatory information management market size by deployment in 2025, while on-premises deployment is projected to grow at 19.12% CAGR through 2031. Cloud remained the largest model because it supports unified workflows, easier updates, and stronger reuse across submission management, intelligence, and collaboration tasks. EMA’s Scientific Explorer data protection notice stated in March 2026 that processing takes place within EU-region Azure servers and that EMA data is not stored or used to retrain AI models, which reflects the type of documented cloud controls that regulated users now expect. That kind of operating model supports cloud adoption because it shows that region-specific processing controls can be built into AI-enabled regulatory environments. The cloud lead in the AI in regulatory information management market therefore remains intact, especially for multinational organizations that want shared workflows across business units and countries.

The faster growth of on-premises deployment looks counterintuitive at first, but it aligns with data residency, sovereignty, and cross-border transfer concerns in several jurisdictions. Companies filing across China, India, parts of the Middle East, and other sensitive markets often need tighter local control over submission-related product information and supporting records. Hybrid architecture is therefore becoming the practical middle ground because it allows central workflow orchestration while keeping some regulated data stores under local control. This makes deployment mode a regulatory design choice and not just an IT preference, especially for global companies that must satisfy conflicting national requirements. The same pattern also helps explain why the AI in regulatory information management market continues to support multiple deployment models rather than converging quickly toward a single standard.

By AI Capability: Agentic Automation Advances Beyond NLP Foundations

NLP and document intelligence held 39.29% of the market in 2025, while predictive analytics and risk scoring is forecast to grow at 20.19% CAGR through 2031. NLP and document intelligence still form the base layer because they handle classification, metadata extraction, document comparison, and consistency checks that many regulatory teams need immediately. The FDA’s FY 2025 report showing 143 NDAs and BLAs approved underlines why risk triage and intelligent workload prioritization have become more relevant inside complex filing portfolios. Generative authoring has also moved beyond experimentation, with Indegene launching NEXT Medical Writing Automation in 2025 and Veeva scheduling AI agents across all its applications from August 2026[3]Indegene, “Indegene Launches NEXT Medical Writing Automation,” Indegene, indegene.com. Clarivate’s Regulatory Assistant adds another layer by showing that search, retrieval, and multilingual understanding are now part of the same competitive stack.

Predictive analytics and risk scoring are growing faster because companies want to anticipate health authority questions, detect weak sections earlier, and prioritize review resources across portfolios. These tools are especially valuable when approval pathways are competitive and when teams must decide which risks deserve early escalation. Knowledge graphs and semantic search are also becoming more important because they let regulatory teams reuse evidence, precedents, and authority interactions across products and markets. Workflow orchestration and agentic automation still contribute a smaller share of current revenue, but vendor investment is high because they promise broader step-by-step automation across regulated workflows. In the AI in regulatory information management industry, that means the revenue base still rests on NLP, but future differentiation is moving toward systems that can reason across data, documents, and actions instead of only processing text.

By Application: Intelligence Anchors Spending While Data Stewardship Emerges as the Growth Leader

Regulatory intelligence represented 38.37% of the AI in regulatory information management market size by application in 2025, while data migration and master data stewardship is projected to grow at 21.33% CAGR through 2031. Intelligence leads because submission planning, labeling decisions, variation strategy, and authority interaction management all depend on current and correctly interpreted regulatory information. ArisGlobal reported 90% accuracy and 50% faster processing in connected regulatory intelligence monitoring, while Clarivate launched a multilingual assistant covering 38 languages and 80-plus countries, which reinforces the central role of intelligence in daily RIM work. This is why intelligence continues to anchor spending across the AI in regulatory information management market even as newer use cases get more public attention. Without a dependable intelligence layer, downstream automation in authoring, publishing, and commitments management loses both accuracy and business value.

Data migration and master data stewardship are growing faster because many companies are still moving from siloed or regional systems into unified cloud RIM environments. Those migrations only deliver value when product records, metadata, and submission histories are clean enough to support automation across markets. Dossier authoring and content assembly are becoming more visible use cases, but they still depend on reliable source content, reusable data, and clear document relationships underneath. Pharmacovigilance and safety reporting also keep pressure high, as FAERS volumes remain very large and Parexel’s 2026 acquisition of Vitrana shows that workflow technology is becoming part of service-led safety operations. In the AI in regulatory information management industry, that makes data stewardship the fastest-growing application because it is the enabling layer that determines how much value every other workflow can actually capture.

By End User: Pharmaceutical Incumbents Anchor Demand as Medtech Emerges as the Growth Catalyst

Pharmaceutical companies held 36.72% in 2025, while medical device and diagnostics companies are projected to grow at 20.33% CAGR through 2031. Pharmaceutical companies led because they had already spent years building eCTD infrastructure, central regulatory teams, and enterprise-grade RIM environments. They also face broad product portfolios, frequent variations, and high submission complexity, which makes AI-enabled reuse and consistency checking financially meaningful. Medical device and diagnostics companies are growing faster because documentation, lifecycle tracking, and post-market obligations are becoming more data intensive across regions. That pushes medtech firms toward platforms and services that can standardize records, automate routine workflows, and improve response speed when requirements change.

Biotechnology companies form a distinct demand group because smaller teams need highly automated tools that reduce manual effort without requiring large in-house regulatory operations. That makes cloud-native delivery, usage-based pricing, and simpler implementation models more attractive than heavy enterprise deployments in many biotech settings. Other end users include CROs, government authorities, and specialty manufacturers that need configurable workflows for portfolio tracking, registration management, and cross-market coordination. Parexel’s acquisition activity in 2026 also shows how CROs are trying to expand from labor-based service delivery into technology-enabled workflow ownership. The end-user mix in the AI in regulatory information management market therefore stays broad, but growth is strongest where AI helps lean teams cope with heavier compliance workloads and tighter regulatory expectations.

Geography Analysis

North America accounted for 39.18% of the AI in regulatory information management market share in 2025. The region led because it combined the FDA’s mature eCTD ecosystem, tight review timelines, and the world’s deepest concentration of large pharmaceutical and biotech R&D operations. The FDA’s January 2025 draft guidance on AI credibility in drug and biological product submissions also gave the market a clearer regulatory framework, which supports more structured vendor and sponsor investment. North America also has a dense vendor base that includes Veeva, IQVIA, Clarivate, Indegene, and multiple AI-native startups, which shortens product feedback loops and supports faster feature development. This combination of regulatory formality, enterprise buying power, and vendor proximity keeps North America central to the AI in regulatory information management market even as other regions accelerate.

Europe is one of the most mandate-driven regional blocks in the AI in regulatory information management market. EMA completed its cloud migration in 2024, adopted the NDSG 2026 to 2028 workplan in early 2026, and launched the AI-enabled Scientific Explorer tool to national competent authorities in March 2026, which shows active institutional participation in AI adoption. The region also concentrates structured-data work because marketing authorization holders must improve product data quality and governance to support broader digital regulatory operations. Germany, France, and the United Kingdom lead adoption because they combine major pharma R&D activity with strong engineering and service talent around regulatory systems. Italy and Spain add secondary growth potential as manufacturing, pharmacovigilance, and lifecycle management obligations continue to widen the need for digital regulatory control.

Asia-Pacific is projected to expand at 19.36% CAGR through 2031, making it the fastest-growing regional outlook within the AI in regulatory information management market size by geography. PMDA published its AI utilization action plan in October 2025, began using generative AI in operations from April 2026, and made eCTD 4.0 mandatory for new drug applications from the same month, which signals synchronized modernization in Japan. China’s 2026 implementation opinions and the NMPA Information Centre’s work on large language models in drug regulation show that institutional AI readiness is moving beyond policy language into operational systems. South Korea and Australia remain smaller but established markets, while South America and the Middle East and Africa are still earlier-stage markets that are usually served through services-led support for multinational registration portfolios.

Competitive Landscape

The AI in regulatory information management market is moderately consolidated at the enterprise cloud platform layer and fragmented across services, regulatory intelligence, and point-solution tools. Veeva said more than 450 companies, including 19 of the top 20 global biopharma firms, used its RIM platform in 2025, which shows how concentrated the reference architecture has become among the largest accounts. That concentration is important, but it does not define the whole market because service providers, niche AI vendors, and regional specialists still compete aggressively for narrower workflow needs. Competitive differentiation is now shifting toward AI depth, explainability, multilingual reach, and the ability to automate connected steps rather than only manage documents. This is why platform vendors across the AI in regulatory information management market are adding agents, semantic search, and reusable intelligence directly into their core environments.

Veeva announced that AI Agents would be released across all Veeva applications in August 2026, which makes agentic automation a platform-level product feature and not just an add-on experiment. ArisGlobal launched its Explainable Data Intelligence architecture in February 2026 and expanded the NavaX Agents suite in March 2026, which shows a strategy focused on connected intelligence across regulatory, clinical, safety, and quality systems. Clarivate launched its Cortellis Regulatory Assistant in 2025, and RegASK joined the Veeva AI Partner Program in April 2026, which shows that ecosystem position now matters alongside native application capability. These moves are raising the competitive bar because customers increasingly want platforms that combine data, intelligence, action, and compliance evidence in one operating model. They also shorten the distance between core RIM systems and specialized AI applications, which makes platform ecosystems harder for smaller stand-alone entrants to ignore.

White-space opportunities still exist in multilingual emerging-market intelligence, AI-led master data remediation, and workflow tools that bridge weak legacy data to standards-ready output. Those gaps matter because many enterprise platforms still assume cleaner source data than customers actually possess. Services-layer competition is also intensifying as CROs and technology partners push deeper into software-enabled workflow ownership. Parexel’s April 2026 acquisition of Vitrana is a clear example of that strategy because it extended the company’s technology depth in AI-enabled pharmacovigilance operations. This leaves the AI in regulatory information management market open to targeted innovation in narrow use cases, even though leadership at the enterprise platform layer remains harder to displace.

AI In Regulatory Information Management Industry Leaders

Veeva Systems

IQVIA

ArisGlobal

Ennov

FREYR / Freya Fusion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Parexel acquired Vitrana, an AI-enabled pharmacovigilance technology provider, expanding end-to-end case processing capabilities; Vitrana's platform reduces case processing time by 60% and manual reconciliation by 75% for over 30 customers and will operate as "Vitrana, a Parexel Company" during phased integration.

- April 2026: Weave Bio and Parexel launched an AI-native NDA submission platform covering the full drug development lifecycle, enabling authoring speeds 60% faster than traditional timelines; Parexel holds a period of exclusivity as the sole CRO with access to co-developed AI submission templates.

Global AI In Regulatory Information Management Market Report Scope

As per the scope of the report, AI in regulatory information management (RIM) refers to the use of artificial intelligence technologies to streamline, automate, and enhance the processes involved in managing regulatory information within the pharmaceutical, biotech, and healthcare industries.

The segmentation for the AI in regulatory information management market is categorized by component, deployment mode, AI capability, application, end user, and geography. By component, the market is divided into software platforms and services. By deployment mode, it includes cloud-based, on-premises, and hybrid solutions. The AI capability segmentation covers natural language processing and document intelligence, generative AI authoring and summarization, regulatory knowledge graph and semantic search, predictive analytics and risk scoring, and workflow orchestration and agentic automation. By application, the market is segmented into regulatory intelligence, dossier authoring and content assembly, regulatory submissions and publishing, product registration and approvals, labeling and artwork change management, health authority interactions and commitments management, data migration and master data stewardship, and pharmacovigilance and safety reporting. The end user segmentation includes pharmaceutical companies, biotechnology firms, medical device and diagnostics companies, and other users.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software Platforms |

| Services |

| Cloud-based |

| On-premises |

| Hybrid |

| Natural language processing and document intelligence |

| Generative AI authoring and summarization |

| Regulatory knowledge graph and semantic search |

| Predictive analytics and risk scoring |

| Workflow orchestration and agentic automation |

| Regulatory intelligence |

| Dossier authoring and content assembly |

| Regulatory submissions and publishing |

| Product registration and approvals |

| Labeling and artwork change management |

| Health authority interactions and commitments management |

| Data migration and master data stewardship |

| Pharmacovigilance and safety reporting |

| Pharmaceutical companies |

| Biotechnology companies |

| Medical device and diagnostics companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platforms | |

| Services | ||

| By Deployment Mode | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By AI Capability | Natural language processing and document intelligence | |

| Generative AI authoring and summarization | ||

| Regulatory knowledge graph and semantic search | ||

| Predictive analytics and risk scoring | ||

| Workflow orchestration and agentic automation | ||

| By Application | Regulatory intelligence | |

| Dossier authoring and content assembly | ||

| Regulatory submissions and publishing | ||

| Product registration and approvals | ||

| Labeling and artwork change management | ||

| Health authority interactions and commitments management | ||

| Data migration and master data stewardship | ||

| Pharmacovigilance and safety reporting | ||

| By End User | Pharmaceutical companies | |

| Biotechnology companies | ||

| Medical device and diagnostics companies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in regulatory information management through 2031?

Growth is being driven by rising submission volumes, the move to eCTD 4.0 and structured data, faster dossier cycle expectations, and the need to monitor regulations across many authorities and languages.

How large will AI in regulatory information management become by 2031?

The AI in regulatory information management market is forecast to reach USD 2.62 billion by 2031 from USD 1.13 billion in 2026, growing at 18.35% CAGR over 2026-2031.

Which application area is growing the fastest?

Data migration and master data stewardship is the fastest-growing application, with a projected 21.33% CAGR through 2031, because legacy data quality still limits automation in many organizations.

Which region leads adoption today and which one is growing fastest?

North America led with 39.18% share in 2025, while Asia-Pacific is projected to expand at 19.36% CAGR through 2031 due to active regulatory modernization in Japan and China.

Why are services growing faster than software platforms?

Services are forecast to grow at 20.88% CAGR because companies need implementation, validation, migration, and managed regulatory support to realize value from RIM platforms at scale.

What is the main challenge slowing broader AI deployment in regulated workflows?

The main challenge is governance and validation, because authorities now expect stronger credibility, traceability, and oversight evidence before AI outputs can support regulated decisions.

Page last updated on: