AI In Laboratory Information Management Systems (LIMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 406.88 Million |

| Market Size (2031) | USD 863.83 Million |

| Growth Rate (2026 - 2031) | 16.25% CAGR |

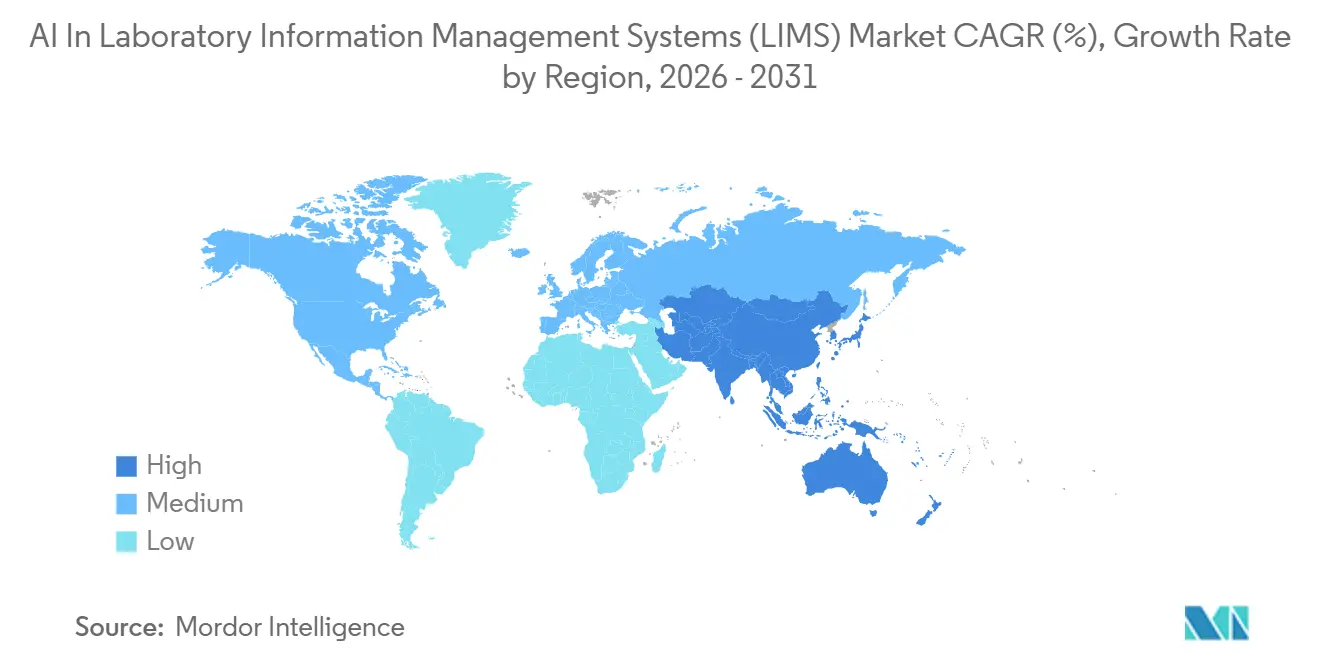

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Laboratory Information Management Systems (LIMS) Market Analysis by Mordor Intelligence

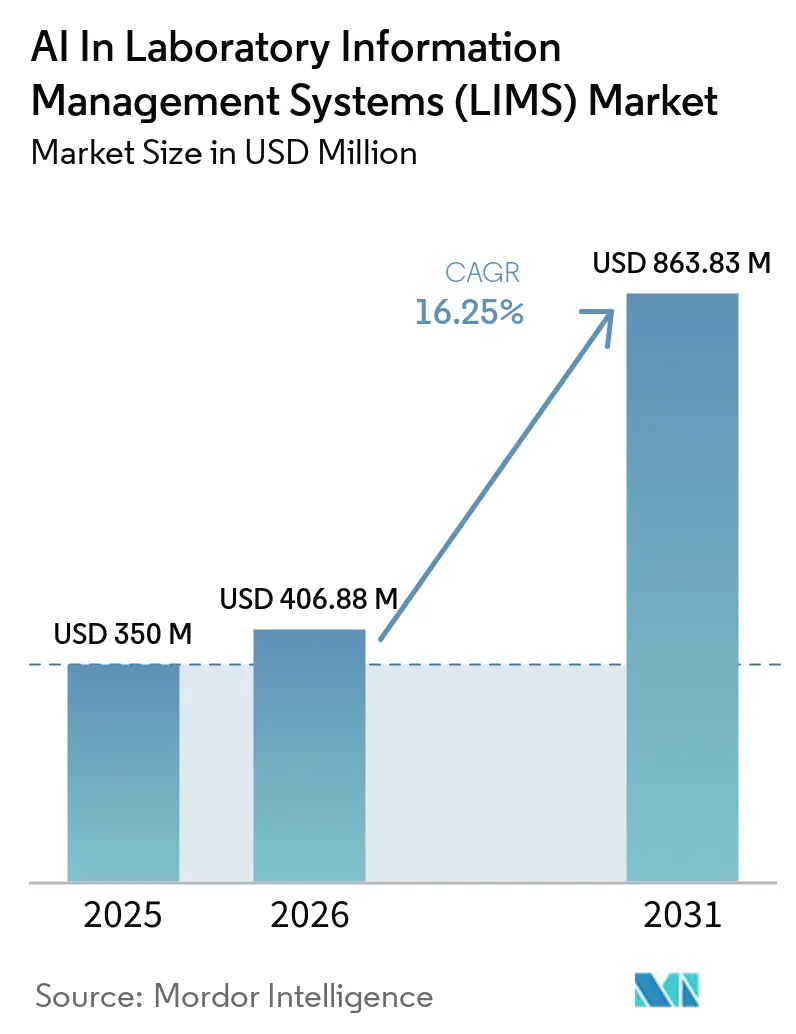

The AI in Laboratory Information Management Systems (LIMS) Market size is expected to grow from USD 350 million in 2025 to USD 406.88 million in 2026 and is forecast to reach USD 863.83 million by 2031 at 16.25% CAGR over 2026-2031. The market is moving from basic recordkeeping toward decision support, as regulated laboratories want systems that can interpret data, prioritize exceptions, and shorten review cycles. Adoption is also being supported by rising pressure on pharmaceutical and biotechnology laboratories to improve throughput without adding the same level of manual analytical effort. A survey cited at the March 2026 launch of LabVantage Cortex stated that more than 75% of laboratories planned to implement AI or machine learning within 2 years, which indicates that the AI in LIMS market is shifting beyond pilot projects into broader operational deployment. Competitive intensity is rising as incumbent LIMS vendors embed agentic AI, newer cloud-based suppliers build AI-first laboratory platforms, and instrument companies expand their software layers to capture more workflow value. Even so, the AI in LIMS market still faces slower rollout in regulated environments because validation expectations, legacy system constraints, and fragmented laboratory data pipelines make production deployment harder than pilot deployment.

Key Report Takeaways

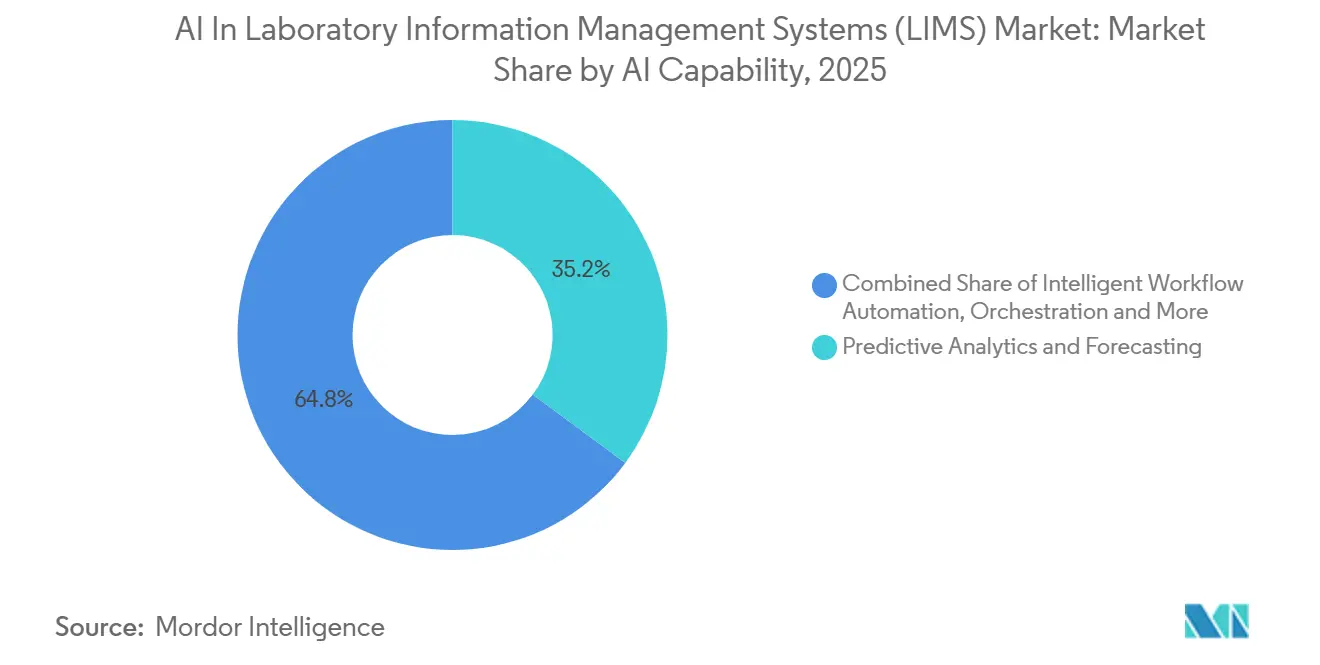

- By AI capability, Predictive Analytics and Forecasting led with 35.16% share in 2025, while Intelligent Workflow Automation and Orchestration is projected to grow at 18.88% CAGR through 2031.

- By component, AI-Enabled LIMS Platform Software held 65.17% share in 2025, while Services is forecast to expand at 17.12% CAGR through 2031.

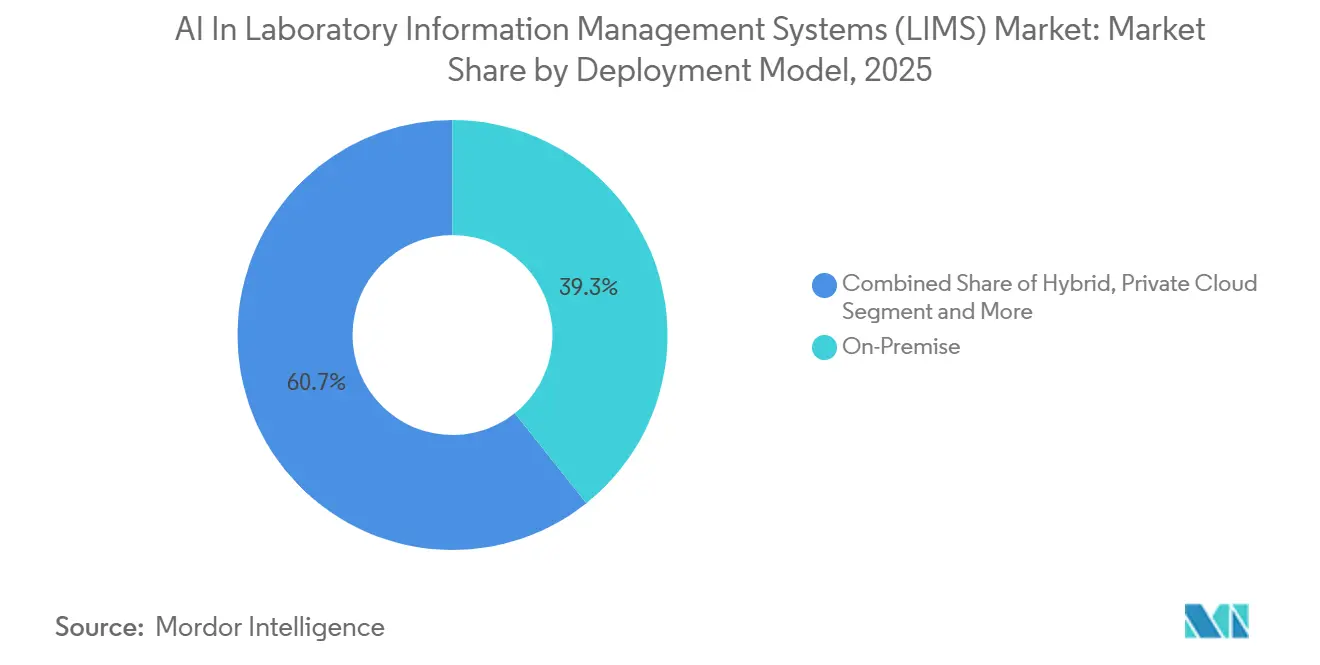

- By deployment model, On-Premise accounted for 39.29% share in 2025, while Hybrid is projected to advance at 18.19% CAGR through 2031.

- By laboratory type, Pharmaceutical and Biotechnology Laboratories represented 35.37% share in 2025, while Biobanks and Genomics Laboratories are expected to grow at 19.33% CAGR through 2031.

- By geography, North America captured 38.18% share in 2025, while Asia-Pacific is forecast to record the fastest regional growth at 17.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Laboratory Information Management Systems (LIMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Embedded AI Copilots for Analyst Productivity | +2.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Cloud-Native LIMS Modernization for AI-Ready Workflows | +2.5% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Multi-Omics and High-Throughput Data Complexity | +3.2% | Global, with high concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Smart Lab Automation and Closed-Loop Orchestration | +2.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Predictive Quality Monitoring and Compliance Automation | +2.1% | Global, strongest in pharma-heavy markets in North America and Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Multi-Site Standardization Across Pharma, CRO, and Diagnostics Networks | +1.8% | Global, with emphasis on the United States, Europe, and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Embedded AI Copilots for Review-by-Exception and Analyst Productivity

The AI in LIMS market is seeing its fastest near-term pull from copilots that move scientists and analysts away from repetitive review and toward exception handling. That matters because high-volume quality control laboratories still spend large amounts of time searching records, checking deviations, and moving across separate informatics tools. Sapio Sciences integrated Anthropic's Claude Cowork into the Sapio Platform in April 2026, which gave scientists one conversational interface to query, analyze, and act on LIMS and ELN data with traceability and user attribution[1]Sapio Sciences, “Sapio Sciences Brings Claude Cowork to the Lab,” Sapio Sciences, sapiosciences.com.

LigoLab also states that its AI agent roadmap supports natural language interaction for laboratory operations, which shows that plain-language access is becoming part of the product baseline rather than a premium add-on. As the copilot layer spreads across the AI in LIMS market, the advantage is likely to shift toward vendors that pair language interfaces with structured laboratory context, auditability, and actionability inside validated workflows. This is also changing buyer expectations, because laboratories no longer want AI that only summarizes records, they want AI that can retrieve the right context and support compliant action inside routine work.

Growing Multi-Omics and High-Throughput Data Complexity

The market is also being pushed forward by the growing volume and diversity of multi-omics and high-throughput laboratory data. Classical LIMS architectures were built to track samples and methods, but they were not designed to harmonize transcriptomic, proteomic, epigenomic, and sequencing outputs at the scale now being generated by national and enterprise research programs. Illumina launched Connected Multiomics v1.1 in February 2026 with AI-guided workflow suggestions learned from expert-created pipelines, which reduced the need for deep bioinformatics knowledge when designing integrated analyses[2]Illumina, “Bringing AI-Guided Exploration to Multiomics Analysis,” Illumina Developer, illumina.com.

Sapio Sciences and Ultima Genomics formed a partnership in September 2025 to combine ultra-high-throughput sequencing with AI-driven LIMS workflows, which reflects growing demand for scalable and traceable multi-omics execution. A 2025 paper in Quantitative Biology found that normalization, imputation, and cross-modality harmonization remain the central barriers in multi-omics integration, which aligns well with the parts of the AI in LIMS market that focus on embedded analytical assistance. Singapore's PRECISE-SG100K program also reported nearly 50,000 whole-genome sequences through a LIMS-mediated cloud pipeline, with AI-driven quality control helping reduce turnaround time by more than 3-fold after workflow optimization.

Smart Lab Automation and Closed-Loop Workflow Orchestration

The AI in LIMS market is moving beyond data interpretation and into orchestration, where software can coordinate instruments, recommend next steps, and support closed-loop execution. This change is important because laboratories increasingly want one operational layer that can manage connected workflows rather than a set of disconnected instrument and informatics tools. LabVantage launched its Cortex platform in March 2026 as a cloud-native SaaS system that integrates agentic AI, predictive analytics, and IoT connectivity into core LIMS functions.

A 2025 Scientific Reports study showed how an autonomous laboratory system used Bayesian optimization to improve microbial culture conditions through iterative design-build-test-learn cycles, which supports the wider move toward AI-managed experimentation. Shimadzu's Autonomous Labo program also shows how instrument manufacturers are entering the orchestration layer by linking AI, robotics, and chromatography workflows for biotechnology use cases. As that model spreads through the AI in LIMS market, standalone platforms will need deeper instrument connectivity and stronger workflow control if they want to remain the primary coordination layer inside modern laboratories.

Predictive Quality Monitoring and Compliance Automation

The market is benefiting from predictive quality tools that help laboratories spot risk before a deviation becomes a release problem or an instrument failure. This use case is attractive because quality teams understand the operational cost of rework, batch delay, and reactive troubleshooting, which makes return on investment easier to justify. Waters described in 2025 how AI-driven predictive and prescriptive analytics can use LC-MS telemetry to detect conditions that lead to clogs, leaks, and other failures before they escalate.

AmpleLogic also states that its AI-enabled LIMS supports stability prediction and shelf-life forecasting, with reported reductions of up to 40% in shelf-life determination time when compared with conventional approaches. These capabilities fit well with the AI in LIMS market because they translate raw analytical signals into earlier action, which helps laboratories move from retrospective review to anticipatory quality management. Vendors that can pair predictive outputs with clear traceability, review controls, and validated change management are likely to gain stronger trust in regulated deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GxP Validation Burden for AI-Enabled Workflows | -2.1% | Global, most pronounced in North America and Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Legacy LIMS, LIS, and Instrument Integration Debt | -1.9% | Global, strongest in established pharmaceutical markets | Long term (≥ 4 years) |

| Weak Metadata Provenance and Model Drift Risk | -1.4% | Global | Medium term (2-4 years) |

| Restricted Use of Adaptive and Generative AI in Regulated Decisions | -1.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GxP Validation Burden for AI-Enabled Workflows

The market continues to face resistance from the validation burden tied to regulated laboratory software. Laboratories in pharmaceutical manufacturing and related settings cannot treat AI functions like ordinary user-interface upgrades because these functions can influence review, exception handling, stability interpretation, and release support. The main difficulty is that adaptive or model-driven behavior does not fit as neatly into legacy validation routines that were built for static and deterministic software. That creates slower approval cycles, more documentation work, and more caution from quality teams that do not yet have mature internal governance for AI oversight. The result is that the AI in LIMS market often advances first in lower-risk workflows, while more critical use cases move more slowly into production. This effect is strongest in risk-averse buyers, especially where compliance teams want clearer rules on model monitoring, revalidation triggers, and sustained human review before scaling beyond limited deployments.

Legacy LIMS, LIS, and Instrument Integration Debt

The AI in LIMS market is also constrained by the integration debt accumulated across older LIMS, LIS, instrument software, spreadsheets, and local laboratory data stores. Many organizations still run validated environments that were built around proprietary interfaces, rigid data models, and site-specific workflows, which makes AI-ready data access costly and slow. Even when buyers want to move quickly, they often discover that analytical records, metadata, and execution context are spread across disconnected systems that were never designed for shared automation. That makes it harder to build dependable models, harder to maintain data lineage, and harder to standardize workflows across sites or business units. The AI in LIMS market therefore depends not only on better models, but also on the less visible work of API enablement, workflow harmonization, and structured metadata capture. Until those foundations improve, many laboratories will keep experimenting with AI at the edge while postponing broader operational deployment inside core regulated environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By AI Capability: Predictive Analytics Anchors Value While Orchestration Gains Momentum

Predictive Analytics and Forecasting held 35.16% of the AI in LIMS market share in 2025, which made it the largest capability segment by a clear margin. Its lead reflects the fact that quality control trending, stability modeling, and instrument failure prediction already map to measurable laboratory outcomes such as fewer disruptions and faster review. The AI in LIMS market has favored this capability because supervised models perform well when data histories are large and prediction targets are clearly defined. Waters showed in 2025 that telemetry-based forecasting can shift LC-MS maintenance from reactive interventions to planned action, which supports both uptime and resource efficiency. That makes predictive use cases easier to justify than more open-ended generative use cases, especially in regulated settings where credibility and traceability matter.

Intelligent Workflow Automation and Orchestration is the fastest-growing capability in the AI in LIMS market, with an 18.88% CAGR projected through 2031. Growth is being driven by rising interest in agentic systems that can coordinate steps across LIMS, ELN, instruments, and connected lab devices rather than only generate alerts or summaries. LabVantage Cortex illustrates this direction by embedding agentic AI into the LIMS operating layer so that tasks such as worksheet support, sample management, stability study coordination, and automated monitoring can happen within one platform context. The broader AI in LIMS market is also seeing continued growth in anomaly detection, knowledge retrieval, semantic search, and copilot functions because scientific teams want faster access to context across expanding data estates. Over time, capability selection is likely to favor tools that can combine interpretable prediction, workflow action, and governed deployment rather than offering isolated AI features without operational depth.

By Component: Platform Software Dominates but Services Growth Signals Deployment Complexity

AI-Enabled LIMS Platform Software accounted for 65.17% of the AI in LIMS market size in 2025, which shows that buyers still place the highest value on upgrading the core informatics layer. This pattern suggests that AI is being purchased less as a separate bolt-on and more as part of a broader platform refresh that expands contract value and vendor lock-in. In the AI in LIMS industry, that favors suppliers that already control sample records, audit trails, workflow logic, and user permissions because those assets shape how effectively AI can be embedded. Sapio Sciences positioned its platform around conversational interaction across laboratory data, while LabVantage introduced a cloud-native platform that embeds agentic functions into core laboratory operations. Those moves reinforce the idea that platform ownership remains central to long-term value capture.

Services is forecast to expand at 17.12% CAGR through 2031, which makes it the fastest-growing component in the AI in LIMS market. That growth reflects the practical reality that implementation, validation, workflow redesign, and ongoing model governance still require specialist support that many laboratories do not have internally. Service demand is especially strong when organizations are deploying across multiple sites, linking instruments and upstream systems, or trying to maintain clear compliance evidence during rollout. The AI in LIMS market therefore does not behave like a simple software scaling story, because operational success still depends on data preparation, qualification work, user training, and post-deployment oversight. Models, copilots, and analytics modules are gaining traction, but they remain constrained when customers lack clean data structures, validated integration patterns, or clear rules for where AI may influence regulated actions.

By Deployment Model: On-Premise Holds Ground as Hybrid Captures Strategic Middle Ground

On-Premise retained 39.29% share in 2025, which kept it as the largest deployment model in the AI in LIMS market. Its resilience reflects the lasting importance of data sovereignty, validated infrastructure, and direct control over environments that manage patient-linked, batch-linked, or other sensitive regulated records. This is not simply a temporary delay in cloud migration, because many laboratories still see public multi-tenant environments as harder to align with internal compliance expectations for critical records. LDB Labordatenbank explicitly promotes AI integration with EU-resident model options, which shows how infrastructure location and governance remain active buying criteria in European regulated settings. In practical terms, the AI in LIMS market continues to give on-premise deployments a strong base wherever compliance risk, localization concerns, or conservative validation policies outweigh the appeal of faster cloud deployment.

Hybrid is the fastest-growing model, with an 18.19% CAGR expected through 2031, because it offers a middle path between control and flexibility. Organizations can keep GxP-critical records and validated workflows in tightly governed environments while still using cloud resources for inference, analytics, and broader computational workloads. Sciagen describes this mixed architecture as a useful path for life sciences groups that want AI acceleration without immediately moving their most sensitive operational data into shared cloud environments. Public cloud and single-tenant private cloud models remain relevant in research-oriented biotechnology and genomics settings where speed, scalability, and API openness matter more than the deepest compliance constraints. Across the AI in LIMS market, hybrid is gaining ground because it matches the actual transition path many laboratories prefer, which is partial cloud enablement rather than abrupt full migration.

By Laboratory Type: Pharma Labs Lead While Biobanks Drive the Next Innovation Wave

Pharmaceutical and Biotechnology Laboratories represented 35.37% of the market in 2025, which made them the largest laboratory type in the AI in LIMS market. Their leading position reflects higher regulatory complexity, larger informatics budgets, and stronger economic incentives to improve review efficiency, stability planning, and release support. AmpleLogic states that AI-enabled stability forecasting in LIMS can reduce shelf-life determination time by up to 40%, which helps explain why pharmaceutical environments remain a prime early adopter group. The AI in LIMS industry also sees steady interest from CROs and CDMOs because these organizations must manage multiple sponsor expectations while keeping workflows standardized across sites and customers. Clinical diagnostics and molecular laboratories are also expanding AI use beyond image analysis and toward result validation, workflow monitoring, and operational analytics as data volumes continue to rise.

Biobanks and Genomics Laboratories are projected to grow at 19.33% CAGR through 2031, making them the fastest-growing laboratory type in the AI in LIMS market. The growth case is tied to national genomics programs, high-throughput sequencing, and large specimen repositories that generate more records and metadata than legacy biobank systems were built to handle. Illumina's recent multiomics tooling and the Sapio Sciences partnership with Ultima Genomics both reflect the shift toward scalable platforms that can support AI-guided workflow design and high-throughput multi-omics execution. Academic and translational research laboratories also contribute to growth through publicly funded programs, though procurement cycles and budget control often limit deployment speed when compared with commercial life sciences users. As specimen volumes and modality complexity rise, the AI in LIMS market is likely to see genomics-oriented laboratories shape some of the next major requirements for data harmonization, automation, and AI-ready infrastructure.

Geography Analysis

North America held 38.18% of the AI in LIMS market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense concentration of pharmaceutical manufacturers, CROs, large genomics programs, and established laboratory informatics suppliers. The AI in LIMS market is especially deep in the United States because buyers there combine strong spending capacity with strict expectations around quality, auditability, and workflow control. Large multi-site laboratory networks in the United States and Canada are also pushing standardization projects that make AI-driven harmonization more valuable across distributed testing environments. These factors continue to support the region's lead even as deployment still moves carefully in the most regulated use cases.

Europe remained a significant part of the AI in LIMS market, led by Germany, the United Kingdom, and France. Regional demand is shaped by the need to satisfy both regulated pharmaceutical data controls and strong data protection requirements, which favors architectures with clear residency and governance options. LDB Labordatenbank highlights EU-resident AI model choices, while dialog EDV promotes laboratory software aligned with secure and structured deployment needs, which reflects how local compliance preferences influence vendor positioning. The AI in LIMS market in Europe therefore rewards suppliers that can balance AI functionality with infrastructure confidence, documentation discipline, and lower-friction validation. That balance should keep the region commercially important even if adoption remains more measured than in less regulated research settings.

Asia-Pacific is the fastest-growing geography in the AI in LIMS market, with a 17.36% CAGR projected through 2031. Growth is being supported by pharmaceutical expansion in India, genomics investment in China and South Korea, and precision medicine and automation initiatives in Japan and Australia. Shimadzu's Autonomous Labo work in Japan shows how the region is not only adopting AI-enabled laboratory software but also building tighter links among instruments, robotics, and optimization workflows[3]Shimadzu Corporation, “Autonomous Labo, Smart Eco Lab,” Shimadzu Corporation, shimadzu.com. South America and the Middle East and Africa are still earlier in the adoption cycle, yet both regions are seeing incremental demand from pharmaceutical manufacturing growth, clinical trial expansion, and healthcare digitalization programs. Even with a smaller current base, these regions add long-term opportunity for the AI in LIMS market where laboratory modernization agendas align with stronger digital infrastructure.

Competitive Landscape

The AI in LIMS market remains moderately fragmented, with no single supplier controlling a dominant position across all laboratory types, use cases, and regions. A leading tier of established informatics vendors includes LabWare, LabVantage Solutions, Thermo Fisher Scientific, Revvity Signals, and Dassault Systèmes BIOVIA, especially in GxP-oriented pharmaceutical settings where installed base, validation experience, and workflow depth matter most. Competition in the AI in LIMS market is now centered on how deeply AI is embedded in the platform, how broadly the vendor can support different laboratory types, and how quickly the system can be deployed in a validated environment. Incumbents still benefit from long-standing sample management footprints and strong switching costs, but they now face pressure from newer suppliers that were designed around cloud delivery, open APIs, and more flexible data models. This keeps the competitive field active rather than settled.

A second layer of competition is coming from AI-native and research-focused platforms that are targeting parts of the AI in LIMS market where deployment speed and modern architecture matter more than the deepest compliance heritage. Benchling, Sapio Sciences, Scispot, L7 Informatics, and eLabNext are positioned well in R&D, genomics, and translational settings where users want faster rollout and easier connectivity. Sapio Sciences strengthened that position in April 2026 by integrating Anthropic's Claude Cowork into the Sapio Platform so users could query and act on LIMS and ELN data from one conversational layer. LabVantage also advanced its competitive position in March 2026 with Cortex, which brought agentic AI, predictive analytics, and IoT connectivity directly into its LIMS architecture. These moves show that the AI in LIMS market is rewarding vendors that can offer AI as a native operating layer rather than a detached assistant.

Instrument and life sciences technology companies are also expanding the competitive boundary of the AI in LIMS market by using partnerships to move closer to orchestration and laboratory decision support. Thermo Fisher announced a strategic collaboration with NVIDIA in January 2026 to develop AI-enabled scientific instrumentation and lab-in-the-loop capabilities, which shows how instrument leaders are seeking a larger software role. Revvity also introduced a new AI software offering for preclinical imaging analysis in late 2025, reinforcing how adjacent technology providers are widening their AI portfolios. The result is a competitive structure where platform incumbents, AI-native informatics providers, and instrumentation companies are all trying to shape the next control point in laboratory operations.

AI In Laboratory Information Management Systems (LIMS) Industry Leaders

STARLIMS Corporation

LabVantage Solutions

Thermo Fisher Scientific

LabWare

Sapio Sciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sapio Sciences integrated Anthropic's Claude Cowork via the Model Context Protocol into the Sapio Platform, enabling scientists to query, analyze, and act on LIMS and ELN data through a single conversational interface with full traceability and user attribution Sapio Sciences.

- March 2026: LabVantage Solutions launched LabVantage Cortex, a multi-tenant, cloud-native SaaS platform integrating agentic AI, predictive analytics, and IoT connectivity into its core LIMS, the system features AI agents for worksheet assistance, sample management, stability studies, and automated compliance monitoring aligned with FDA, EMA, and ISO standards Business Wire, March 5, 2026.

Global AI In Laboratory Information Management Systems (LIMS) Market Report Scope

As per the scope of the report, AI in Laboratory Information Management Systems (LIMS) refers to the integration and application of artificial intelligence technologies within LIMS to enhance data management, automation, decision-making, and workflow optimization in laboratory environments.

The segmentation for the AI in laboratory information management systems market is categorized by AI capability, component, deployment model, laboratory type, and geography. By AI capability, the market includes forecasting and predictive analytics, review-by-exception and anomaly detection, natural language assistance and generative AI copilots, orchestration and intelligent workflow automation, semantic search and knowledge retrieval, and risk scoring and quality signal detection. By component, the segmentation covers platform software for AI-enabled LIMS, analytics modules, copilots, and AI models, as well as services. By deployment model, the market is divided into on-premise, single-tenant private cloud, multi-tenant public cloud SaaS, and hybrid models. By laboratory type, the segmentation includes biotechnology and pharmaceutical laboratories, CDMOs and CROs, molecular and clinical diagnostics laboratories, genomics and biobanks laboratories, translational and academic research laboratories, and other types of laboratories.

By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Predictive Analytics and Forecasting |

| Anomaly Detection and Review-by-Exception |

| Generative AI Copilots and Natural Language Assistance |

| Intelligent Workflow Automation and Orchestration |

| Knowledge Retrieval and Semantic Search |

| Quality Signal Detection and Risk Scoring |

| AI-Enabled LIMS Platform Software |

| AI Models, Copilots, and Analytics Modules |

| Services |

| On-Premise |

| Private Cloud / Single-Tenant |

| Public Cloud / Multi-Tenant SaaS |

| Hybrid |

| Pharmaceutical and Biotechnology Laboratories |

| CROs and CDMOs |

| Clinical Diagnostics and Molecular Laboratories |

| Biobanks and Genomics Laboratories |

| Academic and Translational Research Laboratories |

| Other Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By AI Capability | Predictive Analytics and Forecasting | |

| Anomaly Detection and Review-by-Exception | ||

| Generative AI Copilots and Natural Language Assistance | ||

| Intelligent Workflow Automation and Orchestration | ||

| Knowledge Retrieval and Semantic Search | ||

| Quality Signal Detection and Risk Scoring | ||

| By Component | AI-Enabled LIMS Platform Software | |

| AI Models, Copilots, and Analytics Modules | ||

| Services | ||

| By Deployment Model | On-Premise | |

| Private Cloud / Single-Tenant | ||

| Public Cloud / Multi-Tenant SaaS | ||

| Hybrid | ||

| By Laboratory Type | Pharmaceutical and Biotechnology Laboratories | |

| CROs and CDMOs | ||

| Clinical Diagnostics and Molecular Laboratories | ||

| Biobanks and Genomics Laboratories | ||

| Academic and Translational Research Laboratories | ||

| Other Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in LIMS through 2031?

Growth is being supported by rising demand for analyst productivity tools, multi-omics data management, predictive quality monitoring, and workflow orchestration. The AI in LIMS market is forecast to grow from USD 406.88 million in 2026 to USD 863.83 million by 2031 at a 16.25% CAGR.

Which AI capability holds the leading position in laboratory informatics today?

Predictive Analytics and Forecasting led with 35.16% share in 2025. It remains the most established capability because it aligns well with stability modeling, quality control trending, and instrument failure prediction.

Which deployment model is growing fastest for regulated laboratories?

Hybrid deployment is growing fastest at 18.19% CAGR through 2031. It is gaining traction because laboratories can keep critical GxP data in controlled environments while using cloud resources for AI inference and analytics.

Why does on-premise infrastructure still matter in this space?

On-Premise remained the largest deployment model with 39.29% share in 2025. Many regulated laboratories still prefer direct control over infrastructure, data residency, and validated environments for sensitive records and release-related workflows.

Which laboratory type offers the strongest future opportunity?

Biobanks and Genomics Laboratories are the fastest-growing laboratory type with a 19.33% CAGR through 2031. Their growth is tied to national genomics programs, large specimen volumes, and the need for AI-ready platforms that can manage complex multi-omics workflows.

Which region is likely to expand fastest over the forecast period?

Asia-Pacific is projected to record the fastest regional growth at 17.36% CAGR through 2031. Expansion in pharmaceutical manufacturing, genomics infrastructure, and precision medicine programs is lifting demand across Japan, China, South Korea, India, and Australia.

Page last updated on: