Postmarketing Surveillance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

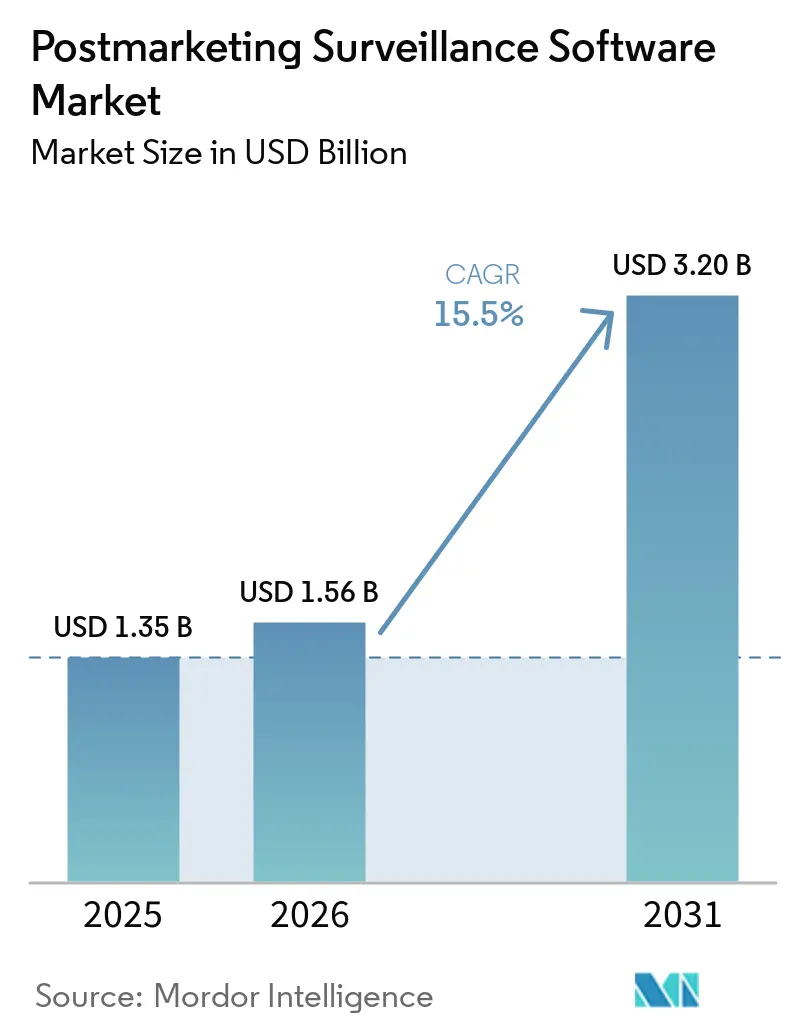

| Market Size (2026) | USD 1.56 Billion |

| Market Size (2031) | USD 3.20 Billion |

| Growth Rate (2026 - 2031) | 15.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Postmarketing Surveillance Software Market Analysis by Mordor Intelligence

The Postmarketing Surveillance Software Market size is expected to increase from USD 1.35 billion in 2025 to USD 1.56 billion in 2026 and reach USD 3.20 billion by 2031, growing at a CAGR of 15.5% over 2026-2031.

Regulatory agencies are increasingly requiring structured, near-real-time safety reporting, driving life-science companies to adopt fully digital pharmacovigilance workflows. Companies are also leveraging technology as a cost-saving measure, with major biopharma organizations targeting significant reductions in adverse-event processing expenses over the next five years. Cloud architectures are becoming the preferred choice for new deployments, as they convert capital expenses into flexible subscription models and simplify compliance validation across multiple regions. Automated intake, natural-language processing, and machine-learning-based signal detection have evolved from pilot concepts to standard features, emphasizing the importance of rapid AI model releases for product differentiation. Additionally, mergers between software vendors and contract safety organizations are transforming service availability, enabling turnkey outsourcing solutions for small and mid-sized innovators lacking internal compliance teams.

Key Report Takeaways

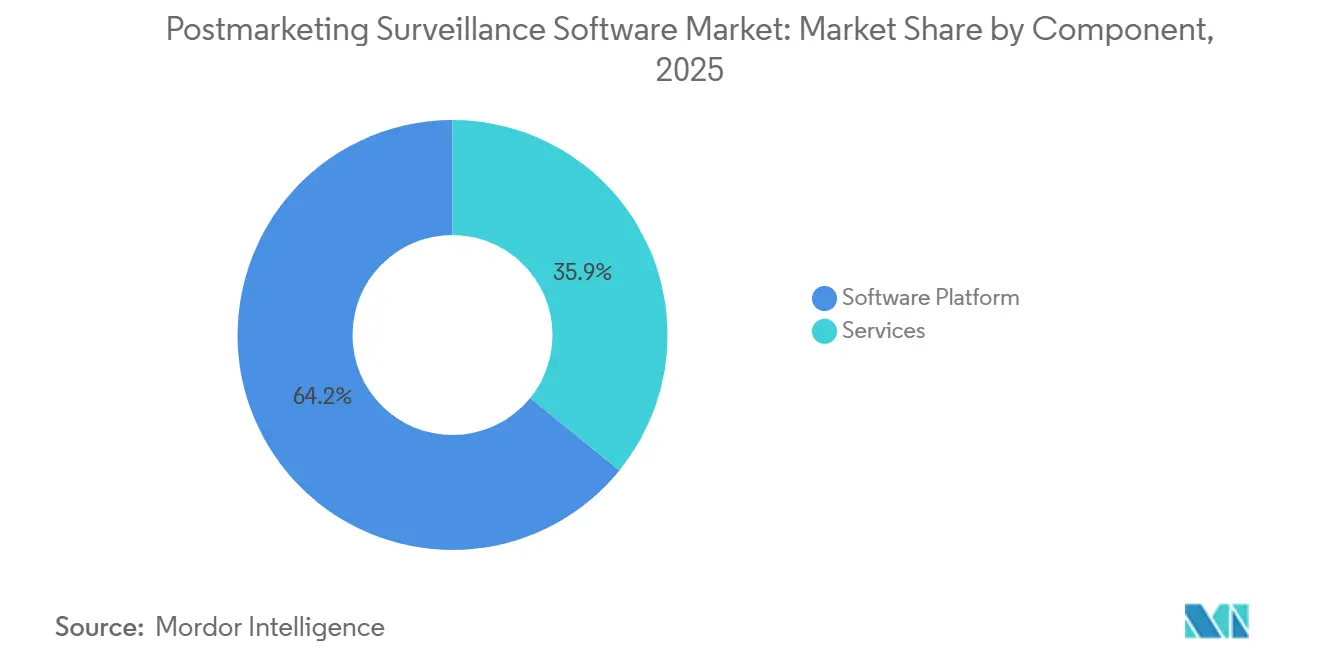

- By component, software platforms led with 64.15% of the postmarketing surveillance software market share in 2025. The services are forecasted to record the highest growth at a 15.95% CAGR through 2031.

- By deployment mode, cloud solutions captured 58.15% of the postmarketing surveillance software market size in 2025 and are expected to grow at a 16.15% CAGR from 2026 to 2031.

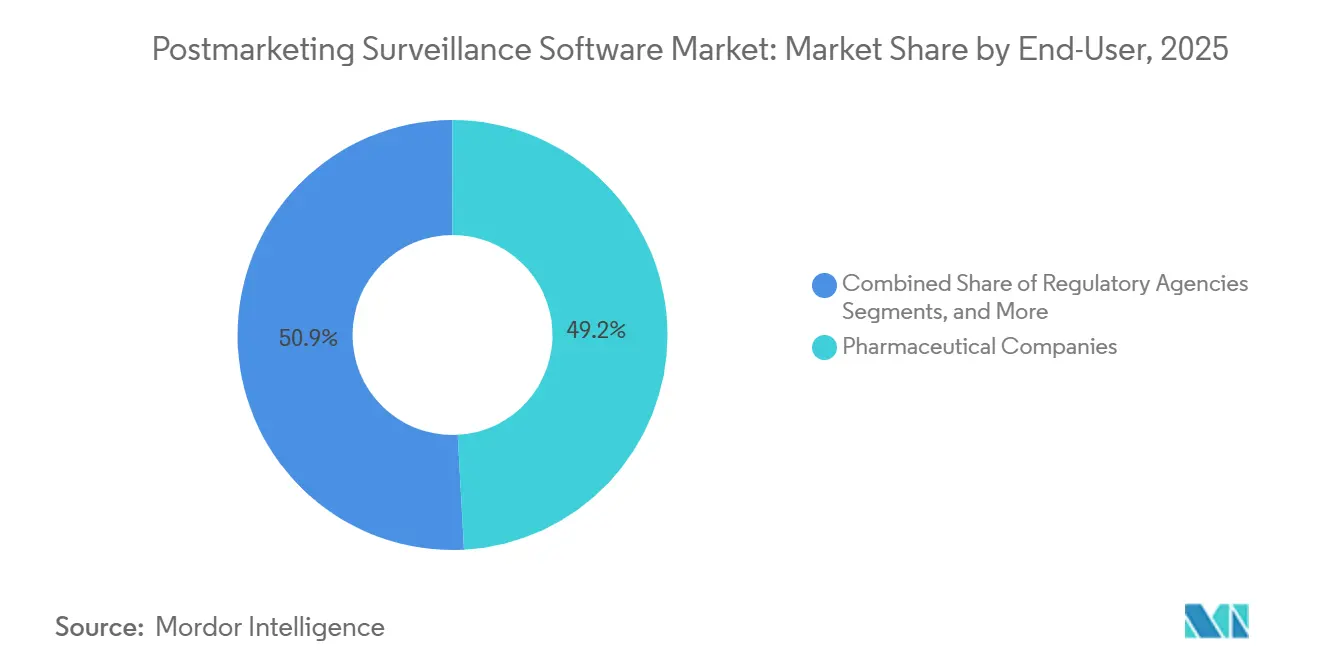

- By end-user, pharmaceutical companies controlled 49.15% of the postmarketing surveillance software market share in 2025, while contract research organizations is expected to grow at 15.75% CAGR to 2031.

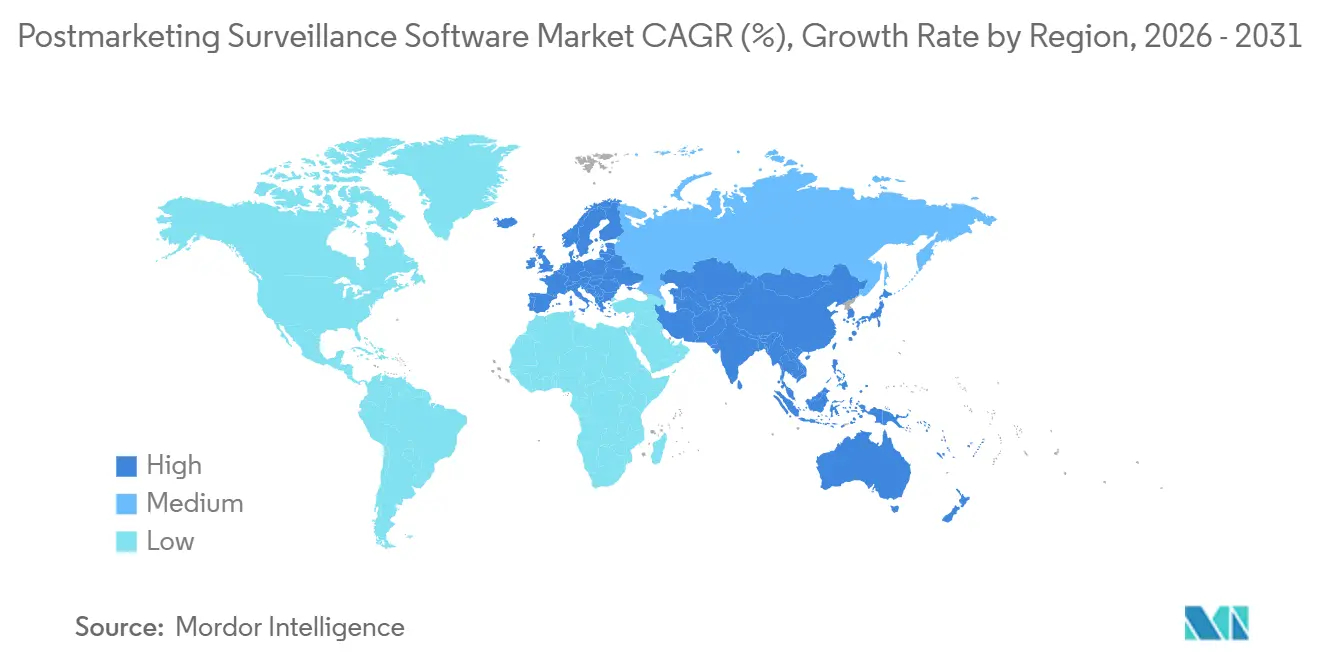

- By geography, North America dominated with 42.65% revenue share in 2025, whereas Asia-Pacific is expected to be the fastest-growing region at a 16.45% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Postmarketing Surveillance Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing Volume of Real-World Data Availability | +3.2% | Global, early traction in North America, EU, Asia-Pacific core markets | Medium term (2–4 years) |

| AI-Enabled Signal Detection Improves Speed & Accuracy | +3.8% | Global, led by North America and EU | Short term (≤2 years) |

| Regulatory Mandates for Proactive Pharmacovigilance | +4.1% | Global, driven by FDA, EMA, PMDA harmonization | Medium term (2–4 years) |

| Growing Complexity of Combination Products | +2.3% | North America, EU, spill-over to Asia-Pacific | Long term (≥4 years) |

| Expansion of Post-Authorization Safety Studies in Emerging Markets | +2.9% | Asia-Pacific, Latin America, Middle East | Medium term (2–4 years) |

| Decentralized Clinical Trial Models Feeding Post-Market Platforms | +3.5% | Global, strong adoption in North America and EU, growing in Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Volume of Real-World Data Availability

Surveillance platforms now directly receive data streams from hospitals, payers, and patients, significantly increasing the volume of analyzable adverse-event signals beyond traditional spontaneous reports. The FDA's 2025 guidance on real-world evidence, which eased the requirement for identifiable patient data in many submissions, has enabled the use of national registries and claims databases for routine safety analyses. Leading vendors have implemented automated extract-transform-load pipelines, pulling and normalizing both structured and unstructured records from electronic health-record networks in near real-time. A mid-cap biopharma highlighted the operational benefits of these richer data sources, reporting a 60% reduction in case-touch time after integrating claims feeds into its platform. However, data completeness remains a challenge, as wearable and registry information often include inconsistent dosage or timing details. While multiregional initiatives around ISO IDMP aim to enhance coding uniformity, full alignment is not expected before 2028.

AI-Enabled Signal Detection Improves Speed and Accuracy

Machine-learning models have outperformed traditional frequentist and Bayesian disproportionality statistics, achieving AUROC values nearing 0.97 in peer-reviewed studies. Sanofi's implementation of these models achieved 85% sensitivity and 75% specificity, reducing its signal-identification timeline by six months. Platforms like LifeSphere Advanced Signals have incorporated automated confounder adjustments, leading to a 40-50% reduction in false-positive workloads.[1]Oracle Corporation, “Safety One Argus 2026.1.01 Release Notes,” Oracle.com In response, regulators have initiated internal pilots; for instance, FDA's Project Elsa uses supervised transformers to summarize narrative text, flagging potential case duplicates while maintaining human oversight.[2]U.S. Food and Drug Administration, “ICH E2B(R3) Data Standards Mandate,” Federal Register, govinfo.gov This advancement significantly enhances reviewer productivity, enabling physicians to focus on causality assessments rather than data management tasks.

Regulatory Mandates for Proactive Pharmacovigilance

Launched in March 2026, the FDA's Adverse Event Monitoring System consolidates seven legacy datasets into a unified, AI-driven platform. This system now publishes safety information daily, replacing the previous quarterly updates and effectively reducing awareness latency by weeks.[3]U.S. Food and Drug Administration, “FDA Begins Real-Time Reporting of Adverse Event Data,” FDA.govSimilarly, Europe activated Regulation (EU) 2025/1466, integrating continuous EudraVigilance monitoring into company workflows and eliminating standalone signal-notification letters. These compliance mandates require database reconfigurations, the adoption of structured narratives, and staff retraining on XML validation. Consequently, firms are driving near-term software revenue by upgrading or replacing outdated systems. The shift to daily data refreshes intensifies the need for companies to automate analytics, as manual review cycles cannot keep pace with regulatory transparency.

Growing Complexity of Combination Products

Combination therapies, which integrate drugs, biologics, and devices, challenge safety teams to manage dual reporting pathways and multi-component causality. Recent FDA guidance has expanded the surveillance scope by classifying numerous software-as-a-medical-device products under postmarketing obligations. The long latency profiles of cell and gene therapies, often overlooked by traditional methods, have prompted firms to adopt hybrid systems that combine spontaneous reports with active registry monitoring. In response, vendors are offering configurable taxonomies that link device component identifiers with MedDRA preferred terms, streamlining the integrated case creation process.

Restraints Impact Analysis*

| RESTRAINT | % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Global Data Standards Hinder Interoperability | -1.4% | Global, acute in Asia-Pacific and MEA | Medium term (2–4 years) |

| High Upfront Integration Costs for Legacy IT Stacks | -1.1% | Global, pronounced in emerging markets | Short term (≤2 years) |

| Shortage of Qualified Safety Informatics Personnel | -1.6% | Global, especially North America and EU | Medium term (2–4 years) |

| Cyber-Security Concerns Over Cloud-Hosted Safety Data | -1.3% | Global, heightened in EU and Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Data Standards Hinder Interoperability

Efforts to achieve ICH alignment have not fully resolved regional discrepancies in narrative fields, timeline requirements, and controlled terminologies. Europe's ISO IDMP implementation is significantly ahead of the Asia-Pacific region, requiring global sponsors to adapt data elements to various regional formats. Additionally, they must manage version control due to MedDRA's biannual updates. This duplication places a strain on validation resources and extends system upgrade timelines. The challenge is further compounded when local regulators introduce country-specific elements that go beyond ICH guidance. Until these adoption gaps are addressed, companies will need to allocate additional resources to support dual validation workflows.

High Capital Investment Costs for Legacy IT Stacks

On-premise safety databases require substantial investments, including large server infrastructures, perpetual licenses, and dedicated IT teams. Upgrading these systems to support E2B(R3) messaging often incurs higher costs than adopting new cloud-based solutions. However, migrations can take up to 18 months, during which both legacy and new systems must operate concurrently. A leading biopharma company reported annual maintenance costs equating to 20% of the original purchase price, prompting its decision to transition to a cloud-based SaaS platform in late 2024. Mid-sized companies are increasingly outsourcing safety processing to avoid the high costs of upgrades, driving service revenue growth at a rate exceeding the overall market average.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Anchor Market Share, Services Accelerate on Outsourcing Momentum

In 2025, software platforms accounting for 64.15% of total expenditures. This trend underscores companies' preference for integrated solutions, combining case intake, regulatory reporting, and analytics. Highlighting the industry's evolution, Oracle’s Safety One Argus release demonstrates vendors' advancements, embedding machine-learning extractors that autonomously capture 90% of structured case data, eliminating the need for manual re-keying. While services took the remaining market share, they are poised to outpace software platforms, projecting a robust 15.95% CAGR. This shift is driven by sponsors' preference for variable-cost operating models over maintaining in-house teams. Furthermore, the momentum in outsourcing not only accelerates upgrades but also allows service providers to deploy new AI modules across multiple clients simultaneously, effectively distributing validation costs.

By Deployment Mode: Cloud Infrastructure Dominates Amid Regulatory Validation and SaaS Economics

In 2025, cloud deployments dominated, accounting for 58.15% of the postmarketing surveillance software market and buoyed by a robust 16.15% CAGR. The FDA's framework has clarified validation expectations for cloud vendors, effectively dismantling a long-standing barrier to adoption. Europe's endorsement is evident with the cloud-hosted EudraVigilance production environment, which has consistently released daily public data since August 2025.

As the justification for on-premise systems diminishes, their market share is set to dwindle. Even traditionally cautious sponsors are now embracing secure virtual-private-cloud deployments, ensuring compliance with regional data-sovereignty laws via country-specific availability zones. Vendors are increasingly phasing out on-premise code lines, urging customers to transition or risk non-compliance once legacy versions cease to receive crucial regulatory message schema updates.

By End-User: Pharmaceutical Companies Lead Utilization, CROs and PV Providers Drive Growth Through Scalable Services

In 2025, pharmaceutical companies held the major share of the postmarketing surveillance software market at 49.15%. This dominance stems from their non-delegable regulatory responsibilities. Yet, there's a noticeable shift: operational tasks are increasingly being outsourced to specialized service providers. This trend is underscored by major pharmaceutical announcements, with commitments to reallocate 30–50% of their workforce towards external partners by 2027. Contract research organizations and dedicated pharmacovigilance providers are set to expand at a 15.75% CAGR, capitalizing on economies of scale, especially when validating new AI modules or integrating updated ISO IDMP data elements. While biotechnology firms currently represent a smaller segment, they are witnessing the swiftest absolute growth. This surge is attributed to their focus on intricate biologics and gene therapies, necessitating ongoing, data-intensive safety monitoring.

Geography Analysis

In 2025, North America captured 42.65% of the postmarketing surveillance software market. The region leverages a first-mover advantage due to early FDA endorsements of AI and cloud validation frameworks. Additionally, its proximity to leading enterprise software vendors in the United States strengthens its market position. Domestic safety-software contracts often exceed annual values of USD 10 million, particularly when bundled with multi-year managed services, reflecting the substantial demand in North America.

Europe follows closely, supported by a significant installed base anchored in the EMA’s EudraVigilance ecosystem. The stringent requirements of the General Data Protection Regulation increase compliance complexity, driving demand for detailed audit trails and localized data residency. Many multinational sponsors maintain dual databases—one designed for FDA regulations and another tailored to EMA standards. This dual approach drives frequent system upgrades as both agencies align their daily data-release schedules.

Asia-Pacific is the fastest-growing region, with a 16.45% CAGR. Countries such as Japan, China, and India are aligning with ICH standards. China is upgrading its National Adverse Drug Reaction Monitoring System to attract international trials, prompting local sponsors to adopt ICH-compliant safety systems with bilingual reporting capabilities. India’s launch of an AI-driven ADR platform in 2024 demonstrates its commitment to digital surveillance, though its success depends on hospitals adopting electronic medical record systems. Smaller Southeast Asian markets typically rely on centralized outsourcing hubs in Singapore, where service providers manage safety obligations across ASEAN nations.

Competitive Landscape

Four suppliers, Oracle, Veeva, IQVIA, and ArisGlobal, dominate enterprise deployments, creating a moderately consolidated seller landscape. Between 2024 and 2026, each introduced generative-AI modules, reducing their product-refresh cycle to 9–12 months. In March 2026, Oracle's upgrade introduced advanced entity extraction capable of processing unstructured emails and scanned PDFs with 90% accuracy, significantly reducing manual intake tasks. Meanwhile, ArisGlobal's NavaX achieved a documented 17% efficiency improvement within three weeks at an early adopter.

IQVIA’s collaboration with Sanofi on Project ARTEMIS highlights the strategic value of integrated data assets. ARTEMIS combines IQVIA's commercial prescription data with AI algorithms, enhancing specificity in signal detection. Veeva leverages its comprehensive clinical and quality-management cloud to deliver cross-module process automation, positioning itself as a preferred solution for companies seeking to harmonize clinical-trial and post-market safety data.

Postmarketing Surveillance Software Industry Leaders

Ennov

Capgemini

IQVIA

ArisGlobal

Oracle

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oracle released Safety One Argus 2026.1.01, adding advanced machine-learning extraction for CIOMS forms and an updated extraction viewer that improves reviewer ergonomics.

- March 2026: The FDA launched the Adverse Event Monitoring System, consolidating seven legacy datasets into a unified platform that processes 6 million reports each year.

- December 2025: ArisGlobal announced enterprise go-live of LifeSphere NavaX, processing nearly 1 million cases with a 17% intake efficiency improvement.

- December 2025: CIOMS Working Group XIV issued the first international governance framework for artificial intelligence in pharmacovigilance.

Global Postmarketing Surveillance Software Market Report Scope

As per the scope of the report, postmarketing surveillance (PMS) software is a specialized digital platform designed to systematically collect, analyze, and report safety, quality, and performance data for pharmaceutical drugs and medical devices after they have been approved and released to the general public.

The postmarketing surveillance software market is segmented by component, deployment mode, end-user, and geography. By component, the market includes software platforms and services. By deployment mode, the market is segmented into on-premises and cloud-based solutions. By end-user, the market is categorized into pharmaceutical companies, biotechnology firms, medical device manufacturers, CROs & PV service providers, and regulatory agencies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software Platform |

| Services |

| On-premises |

| Cloud-based |

| Pharmaceutical Companies |

| Biotechnology Firms |

| Medical Device Manufacturers |

| CROs & PV Service Providers |

| Regulatory Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platform | |

| Services | ||

| By Deployment Mode | On-premises | |

| Cloud-based | ||

| By End-user | Pharmaceutical Companies | |

| Biotechnology Firms | ||

| Medical Device Manufacturers | ||

| CROs & PV Service Providers | ||

| Regulatory Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast size of the postmarketing surveillance software market by 2031?

The postmarketing surveillance software market size is expected to reach USD 3.20 billion by 2031, expanding at a 15.50% CAGR from 2026 to 2031.

Which component segment is growing the fastest?

Services, which include outsourced case processing and literature monitoring, are projected to grow at a 15.95% CAGR through 2031.

Why are cloud deployments gaining share?

Cloud platforms meet updated FDA and EMA validation rules, convert capital expense into operating expense, and enable rapid AI feature rollouts, driving a 16.15% CAGR for cloud deployments.

Which region shows the highest growth potential?

Asia-Pacific is advancing at a 16.45% CAGR as Japan, China, and India align with ICH standards and expand clinical trial volumes.

Who are the leading vendors in this space?

Oracle, Veeva, IQVIA, and ArisGlobal collectively account for the majority of enterprise deployments and continue to invest aggressively in generative-AI modules.

How are regulators influencing technology adoption?

Mandates such as FDA's daily FAERS publication and EMA's Regulation (EU) 2025/1466 compel firms to upgrade databases for structured, near-real-time reporting, accelerating software and service uptake.

Page last updated on: