AI Based Target Identification Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 26.94% CAGR |

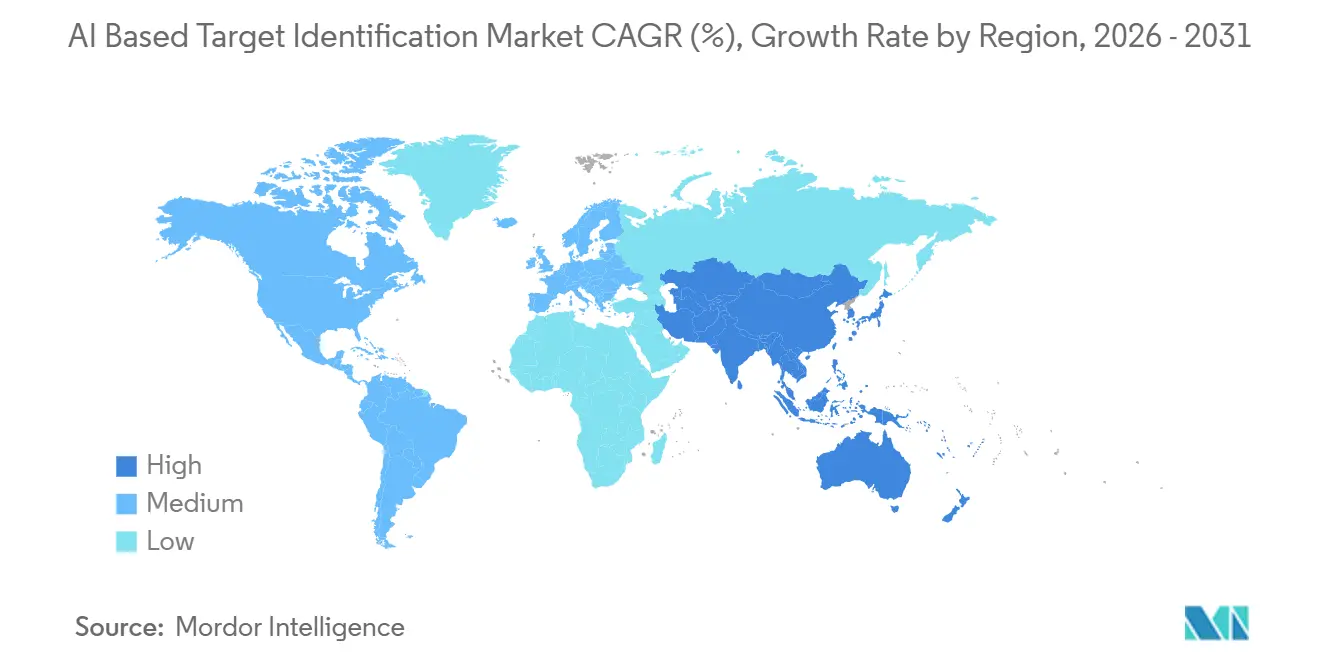

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Based Target Identification Market Analysis by Mordor Intelligence

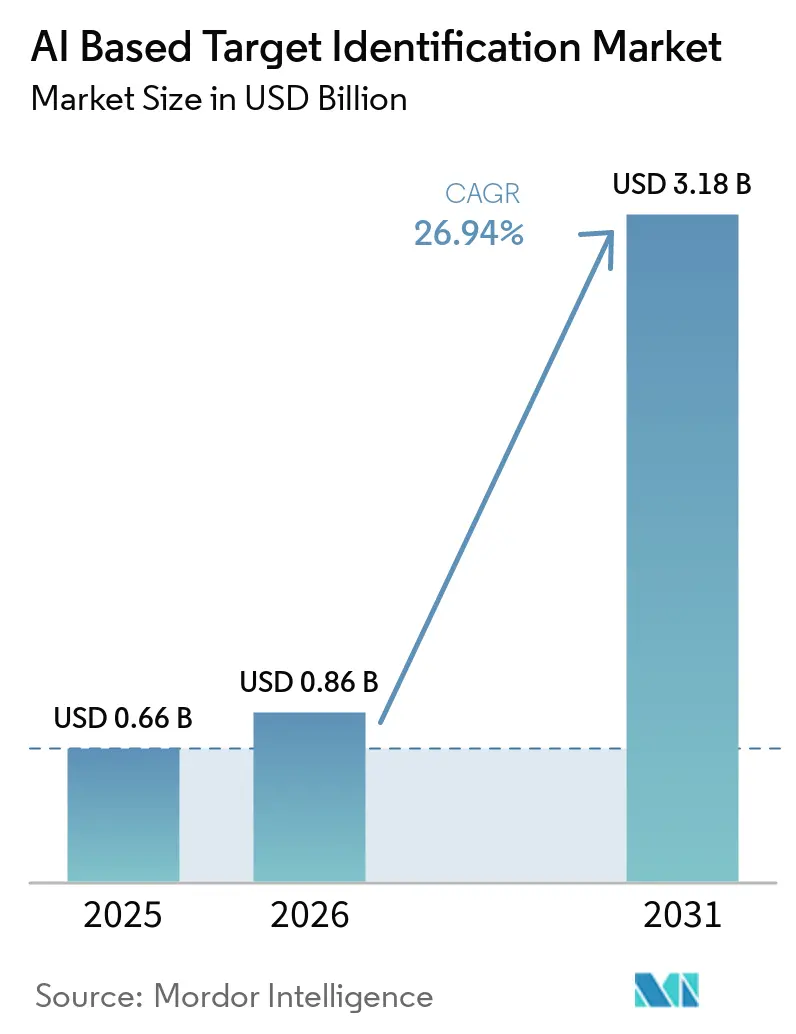

The AI Based Target Identification Market size was valued at USD 0.66 billion in 2025 and is estimated to grow from USD 0.86 billion in 2026 to reach USD 3.18 billion by 2031, at a CAGR of 26.94% during the forecast period (2026-2031).

Cloud hyperscaler offerings, foundation-model breakthroughs, and cross-industry collaborations are compressing discovery timelines, which is spurring adoption across oncology, neurology, and immunology. Biopharma is embedding generative AI into early research to relieve mounting R&D cost pressures, while contract research organizations (CROs) are pivoting toward AI-enabled discovery services. The competitive field remains fragmented, yet well-capitalized platforms that combine proprietary datasets with vertical wet-lab integration are pulling ahead. Regulatory agencies published joint AI principles in 2026 that emphasize governance and lifecycle management, nudging sponsors toward auditable model pipelines.

Key Report Takeaways

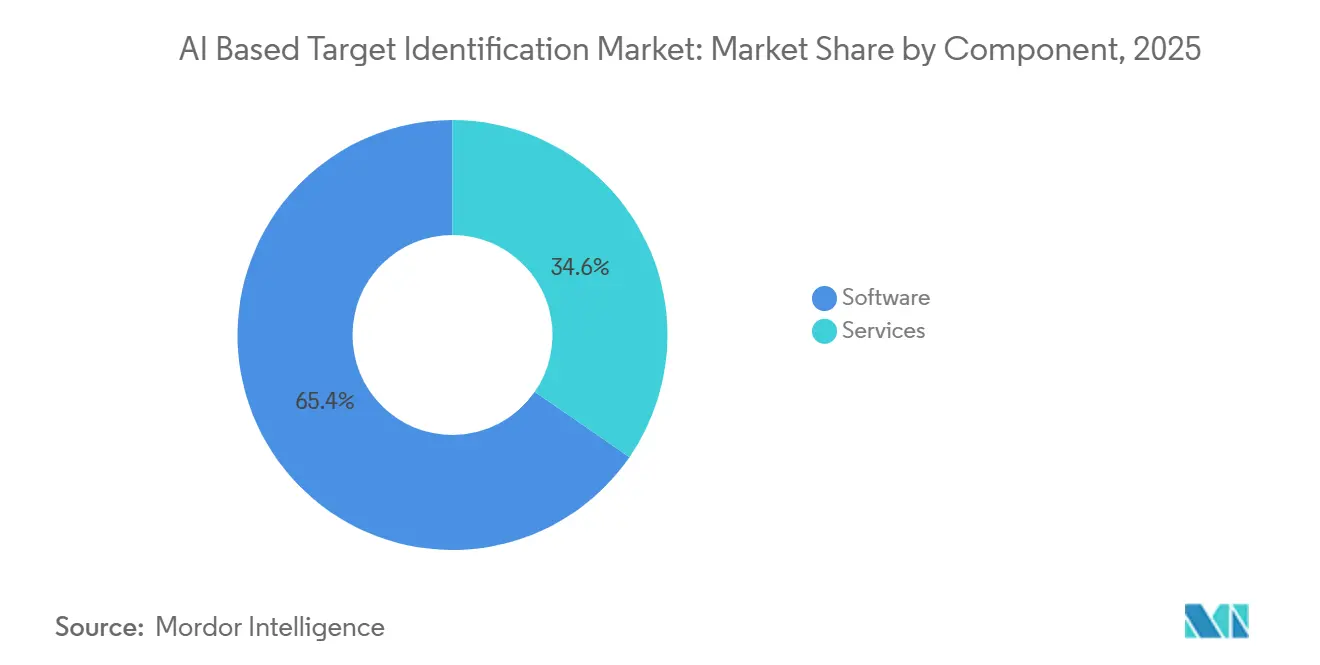

- By component, software accounted for 65.38% of the AI-based target identification market share in 2025, while services are projected to advance at a 27.21% CAGR through 2031.

- By technology, machine learning led with 45.17% of 2025 revenue; natural language processing is expected to grow at a 29.47% CAGR through 2031.

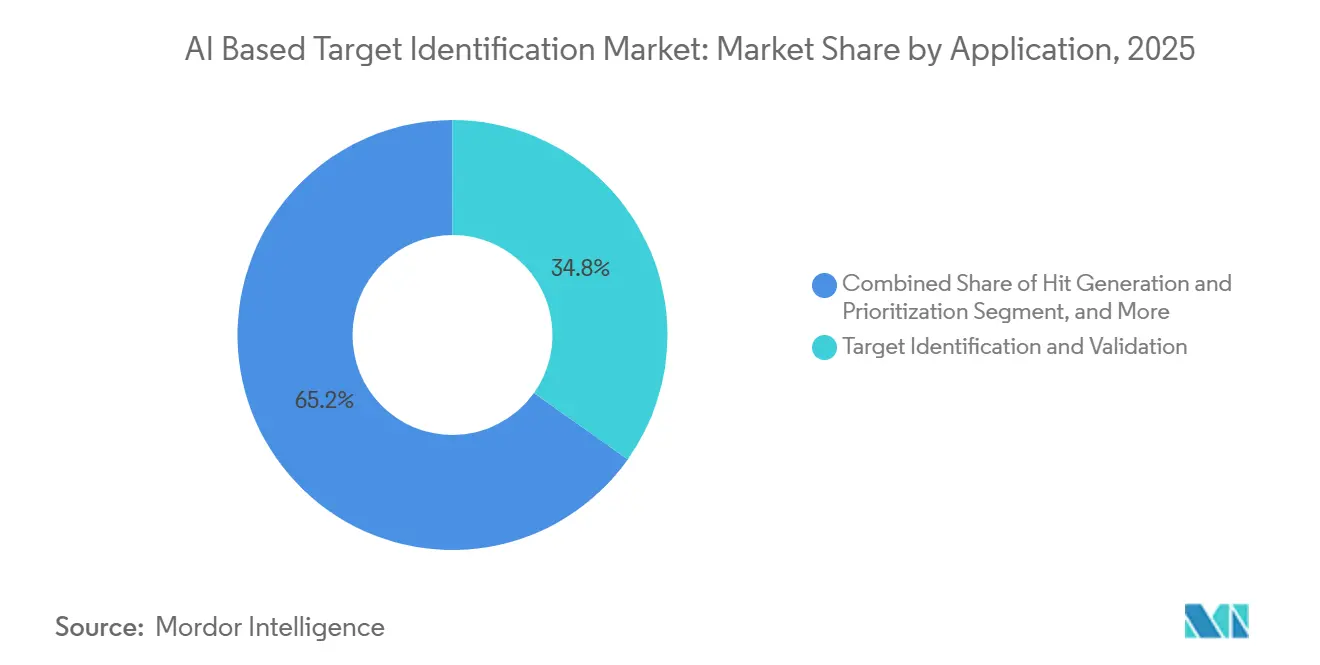

- By application, target identification and validation held 34.83% of the AI-based target identification market size in 2025, whereas hit generation is anticipated to expand at a 28.56% CAGR through 2031.

- By drug type, small molecules commanded 43.59% share of the AI-based target identification market size in 2025, while biologics are forecast to accelerate at a 29.85% CAGR through 2031.

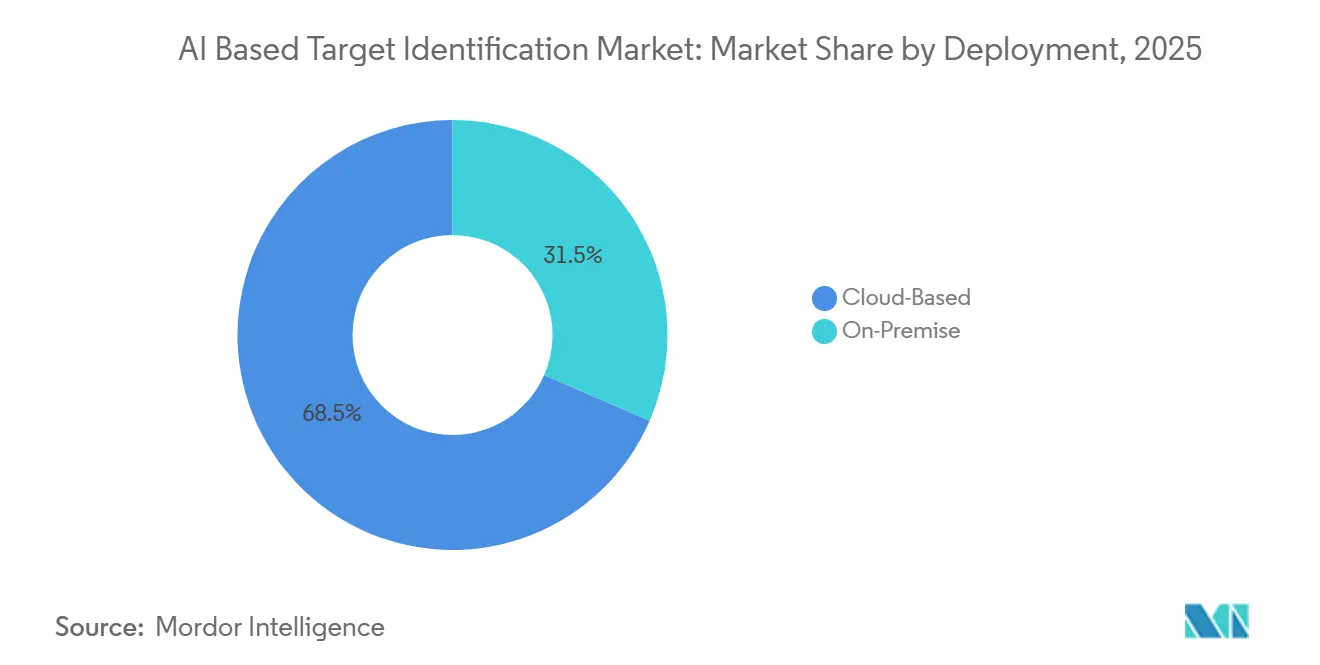

- By deployment, cloud-based solutions captured 68.47% share in 2025; on-premise investments are expected to climb at a 30.92% CAGR as pharma builds sovereign AI clusters.

- By data source, omics datasets represented 42.59% of utilization in 2025, yet EHR-driven evidence is projected to grow fastest at a 27.78% CAGR through 2031.

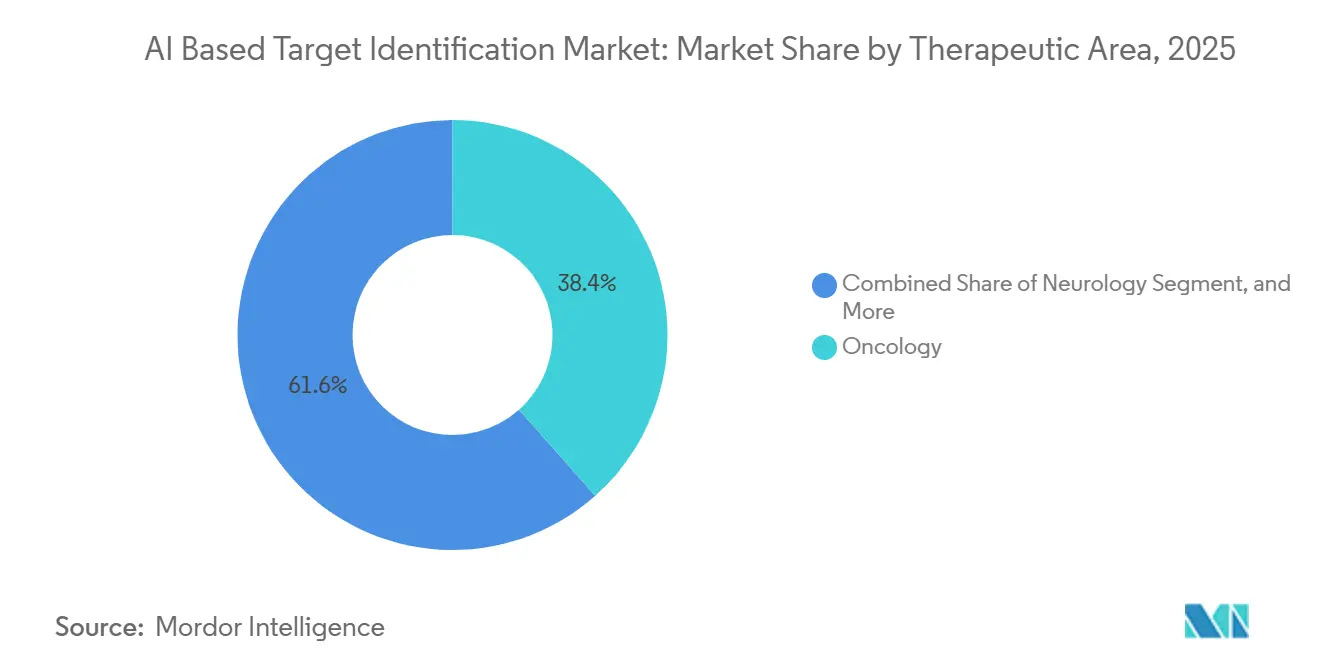

- By therapeutic area, oncology led with a 38.44% revenue share in 2025; neurology is forecast to post a 28.63% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies made up 48.51% of 2025 spending, while CROs are anticipated to register a 29.73% CAGR as they embed AI discovery into service portfolios.

- By geography, North America led with a 39.65% share in 2025; Asia-Pacific is expected to record the fastest regional CAGR of 30.24% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Based Target Identification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biopharma R&D Cost Pressures | +6.2% | North America, Europe | Medium term (2-4 years) |

| Expansion of High-Quality Biomedical Data Assets | +5.8% | North America, APAC | Long term (≥ 4 years) |

| Increasing Strategic Collaborations Between Pharma & AI Vendors | +5.4% | Global | Short term (≤ 2 years) |

| Advancements in Cloud Computing & Generative AI | +4.9% | North America, Europe | Medium term (2-4 years) |

| Accelerating Adoption of Foundation-Model-Powered Biology Platforms | +4.3% | North America, APAC | Medium term (2-4 years) |

| Venture Investment Shift toward Early-Target Risk Sharing | +3.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Biopharma R&D Cost Pressures

Escalating discovery expenditures are forcing companies to front-load computational validation before wet-lab synthesis. AI based target identification market participants now use in-silico screening to evaluate millions of target–ligand pairs within weeks, shrinking preclinical workflows from up to six years to under two. The USD 1 billion partnership between Eli Lilly and NVIDIA illustrates how integrated GPU clusters accelerate model iteration and lower marginal compute costs.[1]NVIDIA Corporation, “NVIDIA and Eli Lilly Announce USD 1 Billion AI Drug Discovery Partnership,” Cloud-delivered prediction services also let smaller biotechs adopt pay-per-inference pricing that aligns spend with milestones. Oncology and rare disease developers, where late-stage failure rates remain high, are the earliest adopters of this cost-containment strategy.

Expansion of High-Quality Biomedical Data Assets

Single-cell atlases, proteomic cohorts, and CRISPRi knockdown libraries are growing in scale and resolution, enabling foundation models to learn causal biology signals. Xaira Therapeutics trained its X-Cell model on 25.6 million perturbed transcriptomes, creating a 4.9 billion-parameter engine that predicts cellular responses to genetic perturbation.[2]Xaira Therapeutics, “X-Cell Foundation Model Release,” The Genetic and Neuropsychiatric Proteomics Consortium released data from 18,645 participants that link protein abundance to clinical phenotypes, giving neurology programs a human-centric evidence base. Continuous data generation through high-throughput phenomics and spatial transcriptomics forms a feedback loop where each cycle improves model accuracy.

Increasing Strategic Collaborations Between Pharma & AI Vendors

Licensing arrangements are shifting toward multi-year co-development deals with milestones and revenue share. In 2025, Incyte paid USD 30 million upfront to Genesis Therapeutics for small-molecule discovery against undisclosed targets, a structure that aligns incentives across the R&D continuum.[3]Genesis Therapeutics, “Genesis Therapeutics and Incyte Collaboration,” AstraZeneca’s USD 5.3 billion alliance with CSPC Pharmaceutical shows that Chinese AI biotechs are winning global mandates.[4]AstraZeneca, “AstraZeneca and CSPC Pharmaceutical Collaboration,” Vertical integration is emerging; Sanofi’s Toronto AI center embeds machine learning across discovery, manufacturing, and commercialization for end-to-end value capture.

Advancements in Cloud Computing & Generative AI

Hyperscalers are packaging omics data lakes, GPUs, and pre-trained biology models into single APIs. Amazon Web Services launched Bio Discovery in April 2026, lowering the barrier for mid-sized firms to run target identification without dedicated ML engineers. Generative diffusion models in NVIDIA’s BioNeMo toolkit can now propose de novo targets and ligands that fall outside the traditional druggable genome. While 68.47% of the AI based target identification market deployed cloud platforms in 2025, large pharma is complementing cloud inference with on-premise GPU clusters to assure data sovereignty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory & AI Explainability Challenges | -2.8% | North America, Europe | Medium term (2-4 years) |

| Data Fragmentation & Lack of Standards | -2.3% | Global | Long term (≥ 4 years) |

| Limited Availability of Clinically Validated Negative Data | -1.9% | Global | Long term (≥ 4 years) |

| Rising Cost of Premium AI Talent and GPU Scarcity | -1.7% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory & AI Explainability Challenges

The FDA and EMA issued joint AI principles in January 2026 that emphasize data governance and risk-based oversight but stop short of codifying test metrics for foundation models. Sponsors, therefore, face case-by-case negotiations on acceptable evidence, elevating compliance costs. Deep neural networks with billions of parameters remain black boxes; companies such as Exscientia generate human-readable rationales, yet this adds latency and may lower predictive accuracy. Divergent regional guidance further complicates global submissions.

Data Fragmentation & Lack of Standards

Inconsistent metadata and ontology misalignment hamper the large-scale integration of omics and clinical datasets. A Nature Methods audit found that 60% of public proteomics studies lacked reproducible preprocessing documentation, causing batch effects that confound model training. Electronic health record (EHR) adoption of FHIR remains under 40% in U.S. health systems, forcing vendors to build bespoke data pipelines. Pre-competitive consortia such as the Monarch Initiative provide ontology mapping tools, but industry uptake is modest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as CROs Integrate AI

Software retained 65.38% of 2025 revenue, yet services are set to grow at 27.21% CAGR through 2031 as CROs embed AI into discovery workflows. The AI based target identification market size for services is projected to expand rapidly as contract partners such as Infosys’ Indivi and Inotiv scale pay-per-target offerings. Traditional license fees of USD 0.5 million to USD 2 million per year are being augmented by end-to-end discovery contracts exceeding USD 10 million, lifting vendor lifetime value.

CRO adoption also addresses the talent scarcity restraint: mid-sized biotechs outsource computational biology to service providers rather than building in-house teams. Hybrid models are emerging; Exscientia offers both SaaS access and full-service target discovery, while Recursion’s OS 4.0 adds morphology-based profiling to partner projects. As services mature, margin pressure on pure-software vendors may intensify unless they differentiate with proprietary datasets.

By Technology: NLP Unlocks Hidden Target Hypotheses

Machine learning represented 45.17% of spending in 2025, but natural language processing (NLP) is climbing at 29.47% CAGR as it mines over 30 million PubMed abstracts and 15 million patents for latent associations. BioGPT, PubMedBERT, and other biomedical LLMs sift unstructured text to surface target-disease linkages that structured omics data miss. Computer vision contributes a smaller share, yet platforms such as Recursion analyze 50 billion cellular images to identify phenotype-driven targets.

The AI based target identification market share for NLP solutions is enlarging because literature-centric discovery scales cheaply once models are pre-trained. Convergence between NLP and generative diffusion models now allows reasoning across multi-modal inputs, accelerating hypothesis generation from months to days. Quantum machine learning remains experimental, with early pilots at Boehringer Ingelheim exploring protein folding algorithms on quantum hardware.

By Application: Hit Generation Accelerates as Generative Chemistry Matures

Target identification and validation held 34.83% of 2025 revenue, yet hit generation is forecast to advance at 28.56% CAGR through 2031. The AI based target identification market size for hit-generation tools is swelling because generative chemistry engines can design de novo molecules that meet binding and developability constraints concurrently. Insilico advanced three AI-generated compounds into clinical trials by 2025, validating the approach.

Drug repurposing gains traction as platforms link real-world evidence to existing molecules; BenevolentAI’s knowledge graph surfaced baricitinib for COVID-19, leading to emergency use authorization. Integrated safety prediction during target selection is becoming mandatory after the FDA urged sponsors to include in-silico toxicity assessments in the 2025 draft guidance.

By Drug Type: Biologics Surge as Diffusion Models Enable Protein Design

Small molecules accounted for 43.59% of 2025 revenue, but biologics are accelerating at 29.85% CAGR because diffusion and protein-language models can now design antibodies and enzymes from scratch. The AI based target identification market share for biologics is expanding as platforms such as Generate Biomedicines’ Chroma iteratively refine protein folds to achieve high-affinity binding.

Gene and cell therapy programs likewise benefit from AI-predicted antigen targets and persistence markers. PROTAC degraders remain niche, yet Exscientia and Captor Therapeutics are developing ternary-complex prediction algorithms to broaden the modality landscape.

By Deployment: On-Premise Gains as Pharma Builds Sovereign AI

Cloud platforms captured 68.47% of 2025 implementations, but on-premise clusters are projected to rise at 30.92% CAGR because large pharma seeks to lower compute unit costs and satisfy data-governance rules. The AI based target identification market size for on-premise solutions is swelling as Recursion’s BioHive-2 and Eli Lilly’s NVIDIA-powered clusters demonstrate 60% cost savings over cloud alternatives.

Hybrid architectures dominate new build-outs: firms train proprietary models on-premise and deploy inference in the cloud. AWS Bio Discovery enables such split deployment, reflecting hyperscaler adaptation to sovereignty demands.

By Data Source: EHR Integration Accelerates as Real-World Evidence Validates Targets

Omics datasets held 42.59% utilization in 2025, yet electronic health record (EHR) data is growing at 27.18% CAGR as payers and regulators demand human-centric validation. Integration of longitudinal clinical phenotypes with molecular profiles improves target–disease linkage confidence and drives neurology advances. Veeda Lifesciences’ collaboration with Mango Sciences illustrates how AI matches patient subgroups to molecular mechanisms.

The AI based target identification market share for multi-modal data models is set to rise as privacy-preserving learning techniques mature. FHIR standard adoption remains a hurdle, yet progress is accelerating under regulatory pressure for interoperable data.

By Therapeutic Area: Neurology Gains as Foundation Models Decode Synaptic Proteomics

Oncology dominated with 38.44% revenue share in 2025, but neurology will expand at 28.63% CAGR through 2031 because single-cell and proteomic atlases are unraveling brain-specific biology. The AI based target identification market size for neurology programs is swelling as Verge Genomics pushes ALS and Parkinson’s candidates into trials.

Immunology continues to attract AI investment to solve T-cell exhaustion, while infectious-disease platforms such as Evaxion identify antigen targets for next-generation vaccines. Emerging rare-disease initiatives rely on patient advocacy consortia to fund bespoke datasets.

By End User: CROs Absorb AI Discovery into Service Portfolios

Pharmaceutical & biotechnology companies represented 48.51% of 2025 spending, yet CROs are poised for the fastest 29.73% CAGR growth. The AI based target identification industry is seeing CROs migrate upstream from assay execution to AI-driven hypothesis generation. PSI CRO’s SYNETIC platform covers 500,000 institutions and cuts trial cycle time by 18%.

Academic institutes leverage open-source LLMs such as GPT-Rosalind to draft grant proposals and mine literature at scale, though limited compute budgets constrain full adoption. Government research agencies back AI discovery in neglected tropical diseases, widening the technology’s social impact.

Geography Analysis

North America held 39.55% of 2025 revenue, supported by FDA regulatory leadership, venture capital density, and hyperscaler infrastructure. Eli Lilly’s USD 1 billion NVIDIA collaboration showcases Silicon Valley’s GPU advantage. Canada positions itself as a cost-effective AI hub through favorable R&D tax incentives backing Sanofi’s Toronto center. Mexico remains oriented to trial execution but is attracting near-shoring discovery spend.

Asia-Pacific is projected to grow at 35.24% CAGR, propelled by China’s sovereign AI strategy, Japan’s pharma-AI alliances, and India’s CRO modernization. XtalPi’s 201% revenue jump in 2025 proves the commercial viability of full-stack AI discovery. AstraZeneca’s USD 5.3 billion CSPC deal signals global validation of Chinese AI platforms. India’s Veeda-Mango tie-up blends EHR phenotypes with molecular datasets to win multinational business.

Europe maintains a significant share, guided by the EMA reflection paper that balances innovation with explainability. Germany’s Boehringer Ingelheim is piloting quantum protein algorithms, while the United Kingdom’s BenevolentAI progresses multiple candidates into preclinical validation. GCC states invest in sovereign life-science clusters under the NEOM umbrella to diversify oil economies. South America remains the smallest region, yet Brazil’s rare-disease initiatives are beginning to incorporate AI target discovery.

Competitive Landscape

Recursion runs the world’s largest phenomics dataset with 50 billion images and 2.5 million experiments, granting a scale moat. Insilico Medicine advanced three AI-designed molecules into clinical testing, demonstrating end-to-end capability. NVIDIA and AWS commoditize baseline target screening through BioNeMo and Bio Discovery, pressuring niche vendors to differentiate via therapeutic depth or proprietary data.

Consolidation is underway: Anthropic bought Coefficient Bio for USD 400 million in April 2026, integrating LLM expertise into biology pipelines. Patents cluster around generative chemistry and protein language models; Exscientia holds rights to AI-designed PROTAC architectures. Compliance costs tied to FDA explainability guidance may trigger further mergers as under-capitalized startups seek scale partners.

AI Based Target Identification Industry Leaders

Arpeggio Bio

Atomwise Inc.

Exscientia PLC

Insilico Medicine Inc.

Recursion Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Anthropic acquired Coefficient Bio for USD 400 million, marking the first purchase of a drug-discovery firm by a large language model developer.

- April 2026: AWS launched Bio Discovery, bundling foundation models, omics lakes and GPU clusters into a single API.

- April 2026: Crown Bioscience partnered with Turbine AI to unite target prediction with organoid validation, aiming to cut preclinical timelines by 40%.

Global AI Based Target Identification Market Report Scope

As per the scope of the report, AI based target identification refers to the use of artificial intelligence technologies such as machine learning, deep learning, and computational biology to discover and prioritize biological targets (genes, proteins, or pathways) involved in diseases. It analyzes large-scale datasets like genomics, proteomics, and clinical data to identify disease mechanisms and potential drug targets faster and more accurately than traditional methods. This approach helps reduce drug discovery time, cost, and failure rates by improving early-stage decision-making in pharmaceutical R&D.

The AI based target identification market is segmented by component, technology, application, drug type, deployment, data source, therapeutic area, end user, and geography. By component, the market is segmented into software and services. By technology, the market is segmented into machine learning, natural language processing (NLP), computer vision, quantum machine learning, and others. By application, the market is segmented into target identification & validation, hit generation & prioritization, drug repurposing, pre-clinical safety & toxicity assessment, and others. By drug type, the market is segmented into small molecules, biologics, gene & cell therapies, protac's & degraders, and others. By deployment, the market is segmented into cloud-based and on-premise. By data source, the market is segmented into omics datasets, EHR & clinical data, real-world & Cclaims data, and others. By therapeutic area, the market is segmented into oncology, neurology, immunology, infectious diseases, and others. By end user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, contract research organizations (CROs), and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Software |

| Services |

| Machine Learning |

| Natural Language Processing (NLP) |

| Computer Vision |

| Quantum Machine Learning |

| Others |

| Target Identification & Validation |

| Hit Generation & Prioritization |

| Drug Repurposing |

| Pre-clinical Safety & Toxicity Assessment |

| Others |

| Small Molecules |

| Biologics |

| Gene & Cell Therapies |

| PROTACs & Degraders |

| Others |

| Cloud-Based |

| On-Premise |

| Omics Datasets |

| EHR & Clinical Data |

| Real-world & Claims Data |

| Others |

| Oncology |

| Neurology |

| Immunology |

| Infectious Diseases |

| Others |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Technology | Machine Learning | |

| Natural Language Processing (NLP) | ||

| Computer Vision | ||

| Quantum Machine Learning | ||

| Others | ||

| By Application | Target Identification & Validation | |

| Hit Generation & Prioritization | ||

| Drug Repurposing | ||

| Pre-clinical Safety & Toxicity Assessment | ||

| Others | ||

| By Drug Type | Small Molecules | |

| Biologics | ||

| Gene & Cell Therapies | ||

| PROTACs & Degraders | ||

| Others | ||

| By Deployment | Cloud-Based | |

| On-Premise | ||

| By Data Source | Omics Datasets | |

| EHR & Clinical Data | ||

| Real-world & Claims Data | ||

| Others | ||

| By Therapeutic Area | Oncology | |

| Neurology | ||

| Immunology | ||

| Infectious Diseases | ||

| Others | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Contract Research Organizations (CROs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the AI based target identification market expected to grow?

It is projected to rise from USD 0.86 billion in 2026 to USD 3.18 billion by 2031, reflecting a 26.94% CAGR over 2026-2031.

Which technology segment is expanding the quickest?

Natural language processing is forecast to post a 29.47% CAGR to 2031 as it mines patents and literature for hidden target associations.

Why are biologics gaining share in AI-driven discovery?

Diffusion and protein-language models can now design antibodies and enzymes de-novo, propelling biologics to a 29.85% CAGR through 2031.

What is driving CRO adoption of AI discovery platforms?

CROs embed AI to move upstream in the value chain, delivering end-to-end target services and achieving a 29.73% CAGR growth rate.

Which region will see the fastest market growth?

Asia-Pacific is set to expand at 30.24% CAGR due to China’s sovereign AI push and rising Japanese and Indian partnerships.

How are regulators addressing AI explainability?

The FDA and EMA issued ten joint principles in 2026 that stress data governance and lifecycle oversight but leave validation metrics to case-by-case negotiation.

Page last updated on: