AI In Track And Trace Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

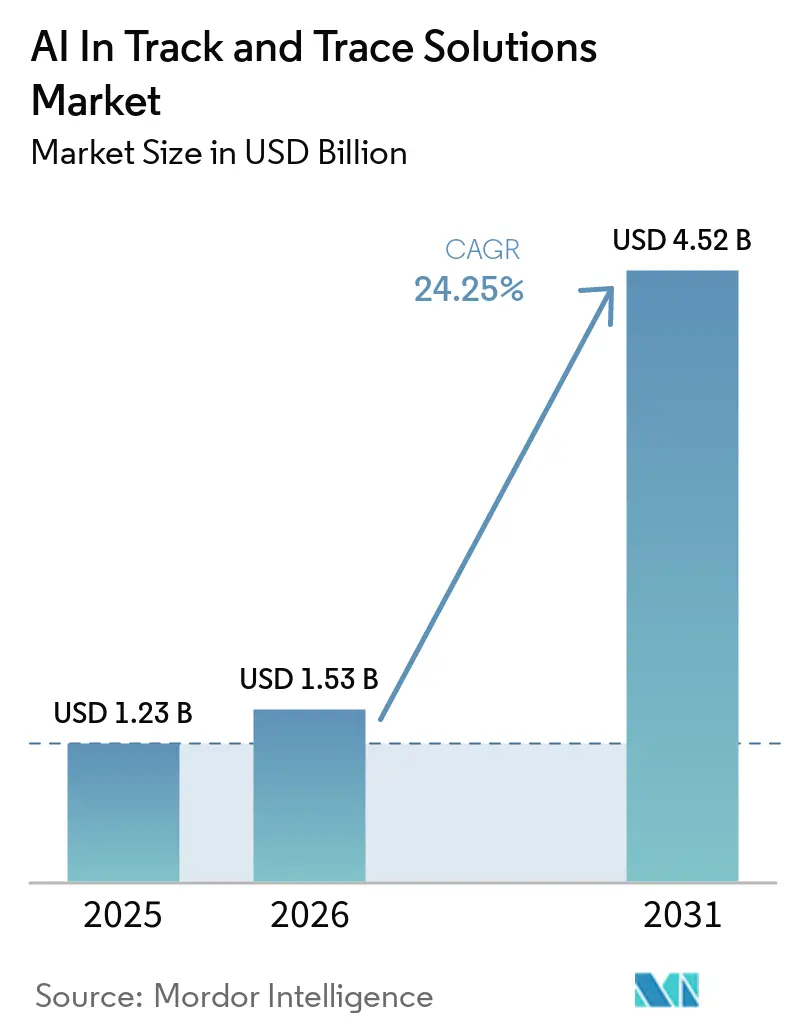

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 4.52 Billion |

| Growth Rate (2026 - 2031) | 24.25% CAGR |

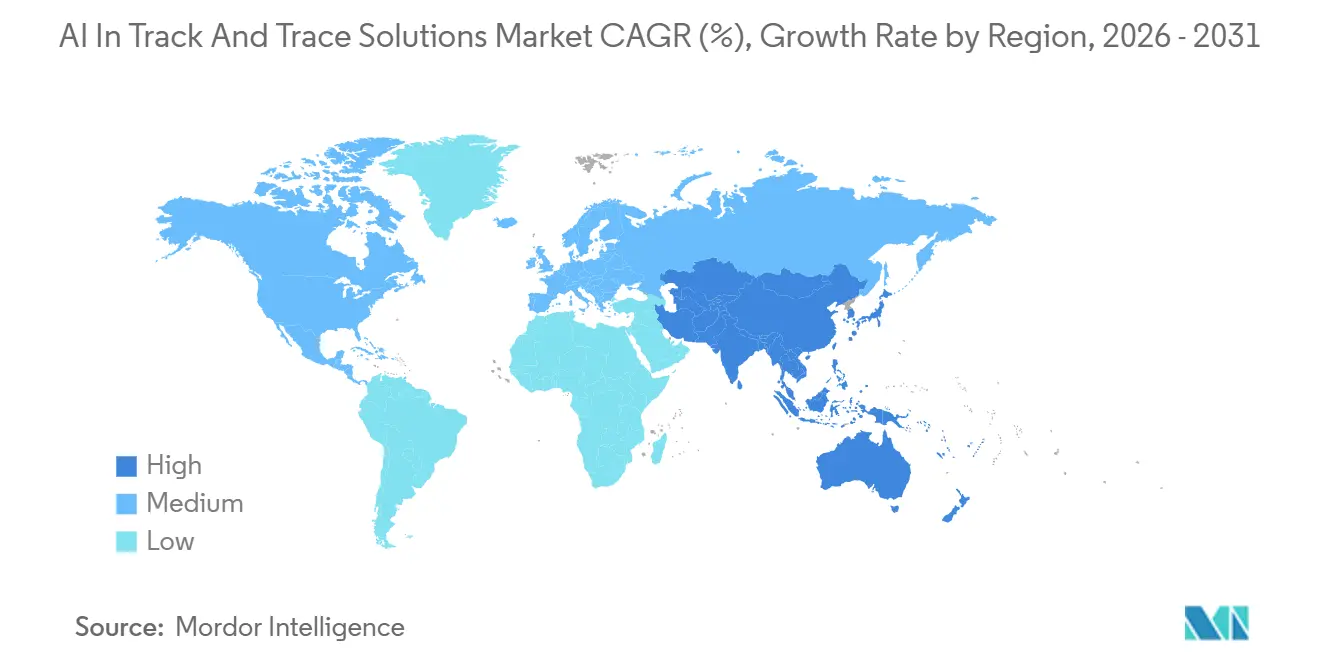

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Track And Trace Solutions Market Analysis by Mordor Intelligence

The AI In Track And Trace Solutions Market size is projected to expand from USD 1.23 billion in 2025 and USD 1.53 billion in 2026 to USD 4.52 billion by 2031, registering a CAGR of 24.25% between 2026 to 2031.

Regulatory deadlines across the United States and Europe are moving track and trace from a compliance cost center into a broader data platform that supports operating decisions across pharmaceuticals, consumer goods, and industrial categories. North America led revenue in 2025 because the region already had mature serialization infrastructure under DSCSA, while Asia-Pacific is set to expand fastest as national frameworks across China, India, Japan, and South Korea move closer to common operating practice. Software platforms held the largest component share, and the fastest application area is shifting toward supply chain visibility and exception management, which shows that buyers now want network event intelligence rather than only unit-level coding. Event volumes are now large enough to support predictive models for demand planning, counterfeit detection, and more precise recalls, with TraceLink reporting more than 7 billion regulated transactions across over 310,000 trading partners in 2025. Competition is tightening between full-stack platform vendors and specialists, but high retrofit costs of USD 150,000 to USD 400,000 per packaging line and fragmented standards still slow adoption among smaller manufacturers.

Key Report Takeaways

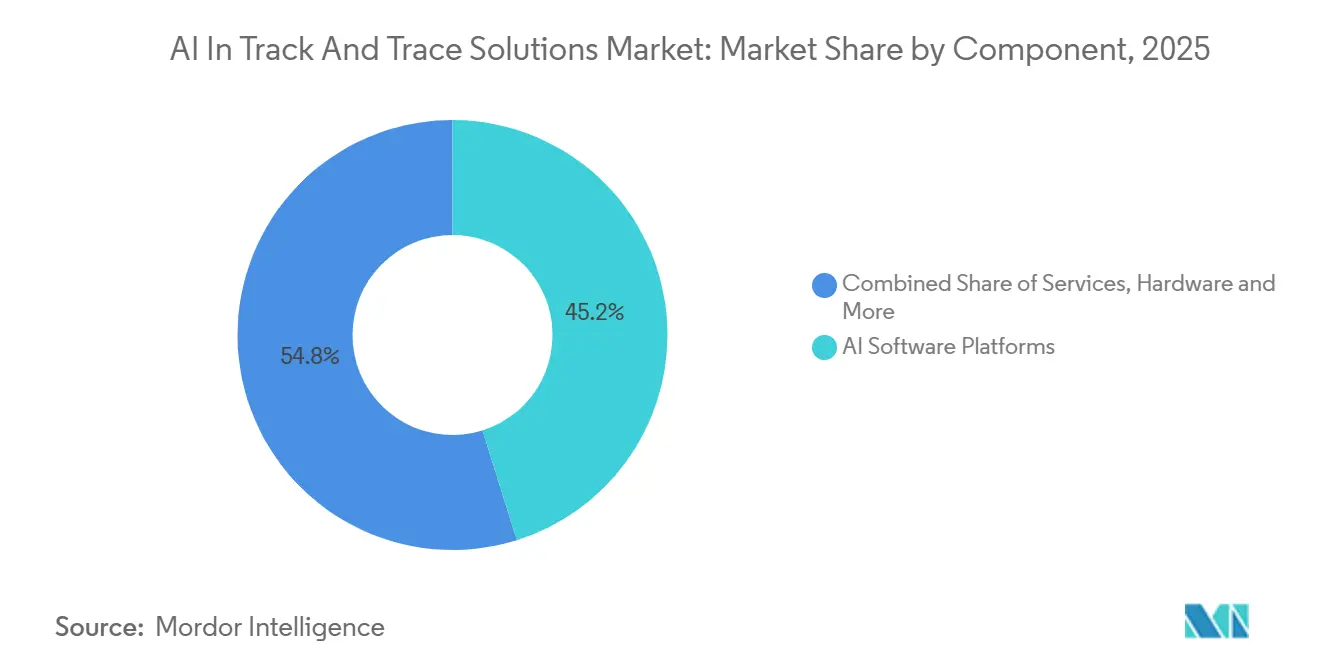

- By component, AI Software Platforms held 45.2% of the AI in track and trace solutions market size in 2025, while Services is projected to expand at 26.9% CAGR through 2031.

- By technology and data carrier, 2D Barcodes and DataMatrix accounted for 35.2% revenue share in 2025, while IoT Sensors and Environmental Monitoring is forecast to grow at 28.1% CAGR through 2031.

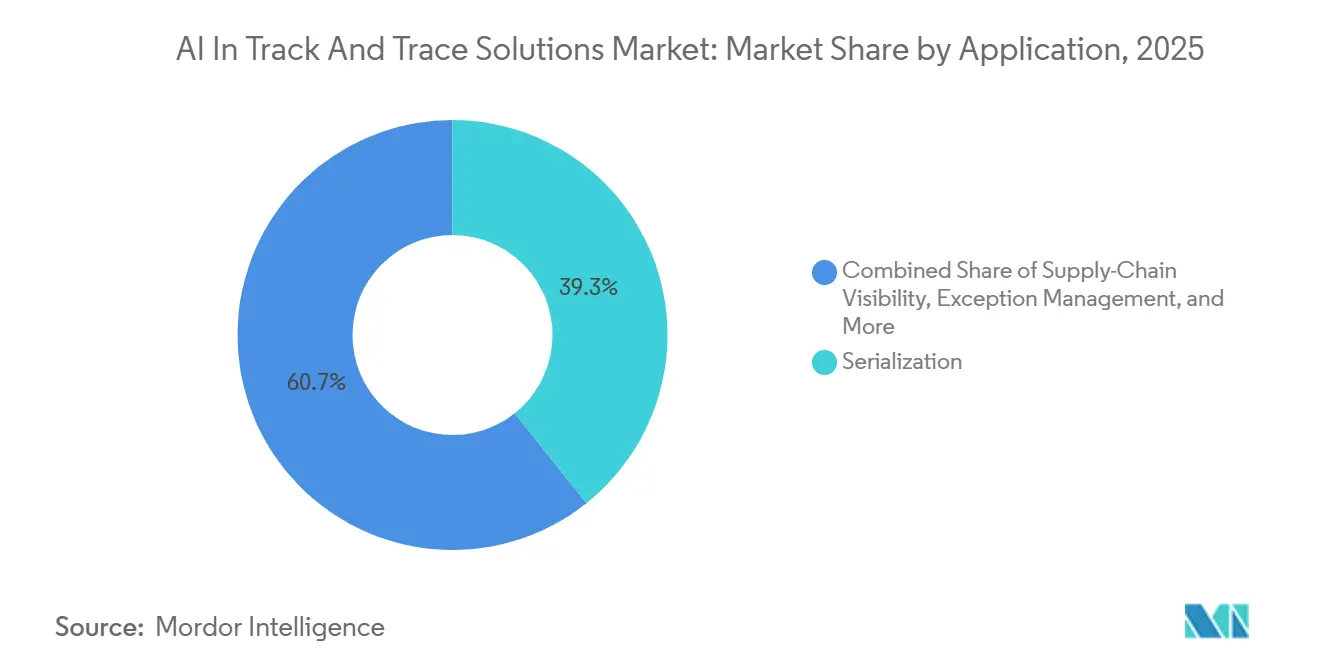

- By application and workflow, Serialization represented 39.3% of the AI in track and trace solutions market size in 2025, while Supply-Chain Visibility and Exception Management is advancing at 29.2% CAGR through 2031.

- By end-use industry, Pharmaceuticals and Biopharmaceuticals held 38.4% of the AI in track and trace solutions market share in 2025, while Consumer Goods and Cosmetics recorded the highest projected CAGR at 26.3% through 2031.

- By geography, North America held 38.2% revenue share in 2025, while Asia-Pacific is forecast to expand at 26.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Track And Trace Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global serialization and traceability mandates | +5.5% | Global, most acute in North America and EU | Short term (≤ 2 years) |

| Counterfeit, diversion, and recall-risk pressure | +4.2% | Global, highest in APAC and LMIC markets | Medium term (2-4 years) |

| Shift from compliance to cloud visibility and analytics | +3.5% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| RFID, 2D code, and machine-vision upgrades | +2.8% | Global | Short term (≤ 2 years) |

| GS1 Sunrise 2027 and 2D barcode migration | +2.3% | Global, EU and North America lead, APAC follows | Short term (≤ 2 years) |

| Digital product passport expansion beyond pharma | +1.8% | EU primary, spill-over to UK and export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Serialization and Traceability Mandates

The AI in track and trace solutions market is being pushed first by law, because federal and regional serialization rules directly trigger procurement cycles. DSCSA enforcement milestones covered manufacturers in May 2025, wholesale distributors in August 2025, and large dispensers in November 2025, which kept spending active across the supply chain during the year. In the AI in track and trace solutions market, data exchange success rates between manufacturers and distributors reached 90%-95% by mid-2025, but exception handling and master data problems still caused many of the remaining failures. This means the same regulatory burden that forced compliance is also creating the large event datasets needed for anomaly detection and more precise recalls. FDA surveillance activity stayed high in FY 2025, with more than 50 DSCSA inspections conducted alongside CGMP audits, which supports continued spending through the small-dispenser deadline in November 2026[1]U.S. Food & Drug Administration, “Office of Compliance 2025 Annual Report,” U.S. Food & Drug Administration, fda.gov.

GS1 Sunrise 2027 and 2D Barcode Migration

The market is also being shaped by the move from 1D to 2D codes across retail and packaged goods. GS1 Sunrise 2027 requires compliant retail point-of-sale systems to be able to read 2D barcodes by December 31, 2027, and that requirement is already affecting packaging plans in 2026[2]GS1 US, “Retail Shift: UPC to 2D Barcodes by 2027 on Packaging,” GS1 US, gs1us.org. In the AI in track and trace solutions market, brands in the dual-marking phase are finding that 2D codes can carry serial numbers, batch data, and expiry dates in one carrier, which turns each scan into a traceability event. That richer data structure creates direct demand for AI print verification and machine vision inspection at production-line speed. The same carrier logic also supports upcoming EU battery passport requirements from February 2027, so packaging investment can serve more than one mandate at the same time.

Counterfeit, Diversion, and Recall-Risk Pressure

The AI in track and trace solutions market is gaining support from anti-counterfeit and recall-control spending as much as from regulation. WHO stated in December 2024 that 1 in 10 medical products in low- and middle-income countries is substandard or falsified, which keeps traceability relevant even after years of serialization rollout. In the AI in track and trace solutions market, this pressure is opening a distinct role for behavioral anomaly detection, because platforms can compare duplicate serial numbers across regions, unusual border scan clusters, and abnormal shipment velocity patterns. OECD reported that global trade in fake goods reached USD 467 billion in 2021 data released in 2025, which shows the scale of the commercial loss that brands are trying to control through better track and trace systems. This keeps demand broad, because buyers now treat counterfeit prevention and recall precision as ongoing operating needs rather than one-time compliance projects.

Digital Product Passport Expansion Beyond Pharma

The market is moving into new sectors because the EU Digital Product Passport framework extends traceability beyond medicines. Regulation 2024/1781 entered into force in July 2024 and set the direction for passports across physical goods sold in the EU, beginning with batteries from February 18, 2027 and then extending to more categories through delegated acts expected from 2026 to 2029. In the AI in track and trace solutions market, that matters because the DPP model requires a QR code or RFID and NFC tag linked to a structured digital record, which is effectively a serialization stack for sectors that did not previously need one. Harmonized technical standards are expected by the end of 2026, which gives brands limited preparation time before the first broader obligations arrive. The result is a new deployment wave in consumer goods, cosmetics, electronics, and industrial products, where vendors with pharma-grade experience are trying to reposition early.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and validation costs | -4.5% | Global, most acute for SMEs in APAC and MEA | Short term (≤ 2 years) |

| Fragmented standards and legacy-system interoperability | -3.2% | Global, most complex in multi-market APAC and MEA deployments | Medium term (2-4 years) |

| DSCSA and FSMA data-quality and partner-readiness gaps | -2.1% | North America primary | Short term (≤ 2 years) |

| Cybersecurity and data-governance burden for shared event networks | -2.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Validation Costs

The AI in track and trace solutions market still faces a hard cost barrier at the packaging line. Line-level retrofits cost USD 150,000 to USD 400,000 per line, and that remains difficult for small and mid-sized manufacturers that need several lines upgraded at once. In the AI in track and trace solutions market, the burden rises further because IQ, OQ, PQ, and computer system validation work can add 30%-50% to total project cost under regulated conditions. RFID chipset prices also rose 40%-60% in 2024, which made hardware planning more difficult just as new mandates were expanding the addressable base. Buyers are responding by reviewing supplier geography and near-shoring options, but those choices still add qualification time and delay deployment.

Fragmented Standards and Legacy-System Interoperability

The market also faces slower adoption because multinational manufacturers still manage too many parallel compliance architectures. DSCSA, EU FMD, Russia’s Chestny ZNAK, China’s NMPA system, and national frameworks in Saudi Arabia, Brazil, and India use different data formats, reporting rules, and authentication methods. In the AI in track and trace solutions market, that means one manufacturer can maintain several separate stacks with separate ERP integrations and reconciliation workflows for the same product family. Legacy on-premise systems also lack the interfaces needed to ingest real-time serialization events without extra middleware, which became clear during DSCSA activation across trading partners. GS1 identifiers help provide a common language, but national deviations still force custom development in APAC and the Middle East, and that weakens the promise of standardized deployment[3]Advanco, “Global Harmonisation Efforts for Track and Trace,” Advanco, advanco.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: AI Platforms Consolidate the Value Stack

The market showed a clear tilt toward software in 2025, with AI Software Platforms holding 45.2% share. In the AI in track and trace solutions market, that mix reflects a reversal in enterprise buying behavior because orchestration layers are now often purchased before hardware rollouts are fully complete. Buyers are placing more value on multi-enterprise connectivity, workflow control, and data reuse than on stand-alone line equipment. This keeps the AI in track and trace solutions industry focused on software layers that can scale across partners without repeated site-level development.

The market is also seeing the Services segment grow fastest at 26.9% CAGR through 2031 as cloud delivery replaces older on-premise models. Managed subscriptions that bundle software, validation support, and partner onboarding are gaining ground because many users want continuous compliance support rather than one-time installation. Hardware and Edge Capture Systems still matter at the line for printing, inspection, and scanning, but their share is falling as downstream software captures more value from the event stream. TraceLink’s OPUS platform showed how that value can extend beyond serialization, with 16 transaction types across 5 business orchestrations and 182 live transactions in 2025. The AI in track and trace solutions industry is therefore rewarding vendors that can monetize network activity after the compliance event is recorded.

By Technology / Data Carrier: 2D Codes Lead, Sensor Layers Expand Fast

The market remained anchored by 2D Barcodes and DataMatrix, which held 35.2% share in 2025. That position is being reinforced by GS1 Sunrise 2027, which is pushing retailers and brands to update packaging and scanning infrastructure across global supply chains. In the AI in track and trace solutions market, 2D codes matter because they let one label carry more identity data, more expiry data, and more event data without a full change in package format. This also supports the shift toward consumer-facing traceability where a single scan can serve compliance, product information, and authentication.

The market is expanding fastest in IoT Sensors and Environmental Monitoring, which is projected to grow at 28.1% CAGR through 2031. That growth is tied to cold-chain control in biologics, vaccines, and temperature-sensitive consumer goods, where condition monitoring matters as much as identity capture. The Identiv and Tag-N-Trac partnership launched in April 2025 combined BLE smart labels with the RELATIVITY SaaS platform for real-time cold-chain tracking and later won a 2025 IoT platform award. RFID and NFC are also progressing in regulated use cases, with a Michigan State pilot reporting full traceability across a simulated pharmaceutical supply chain using GS1 interoperability standards in June 2025. AI computer vision is scaling alongside these carriers, with Cognex positioning its In-Sight 8900 series for code inspection and audit-trail needs in regulated manufacturing.

By Application / Workflow: Serialization Anchors Revenue While Visibility Accelerates

The market still draws its largest workflow revenue from Serialization, which accounted for 39.3% of revenue in 2025. That base remains durable because DSCSA and EU FMD programs created multi-year compliance cycles that still require ongoing operating support. In the AI in track and trace solutions market, Supply-Chain Visibility and Exception Management is now the faster lane, with 29.2% CAGR projected through 2031 as buyers extend these systems into logistics, procurement, and commercial coordination. The shift shows that users no longer want traceability data to stop at regulatory reporting. They want the same event stream to help reduce disruptions and improve operating response.

The market also shows why installed compliance platforms retain influence, because SAP ATTP was deployed across 18 of the top 20 global pharmaceutical manufacturers by August 2025. Aggregation is gaining importance because parent-child data exchange between trading partners is becoming commercially necessary once EPCIS-based interoperability is active. Verification and authentication workflows are moving into consumer-facing packaging, where NFC tamper detection and cryptographic QR codes are becoming more common in cosmetics and medical devices. Compliance reporting and recall management are also changing, because AI-assisted exception triage can support batch and region-level precision recalls instead of broader product withdrawal. This keeps the AI in track and trace solutions market centered on workflows that cut waste as well as risk.

By End-use Industry: Pharma Leads, Consumer Goods Gains Speed

The AI in track and trace solutions market remained led by Pharmaceuticals and Biopharmaceuticals, which held 38.4% of AI in track and trace solutions market share in 2025. That lead reflects the weight of DSCSA and EU FMD, along with tighter enforcement environments across China, India, South Korea, and Japan. In the AI in track and trace solutions market, Consumer Goods and Cosmetics is growing fastest at 26.3% CAGR through 2031 because GS1 Sunrise 2027 and EU product passport rules are pushing non-pharma brands into traceability programs. The growth profile differs from pharma because many consumer brands use serialization not only for compliance but also for product origin, sustainability, and loyalty interactions. This is one of the clearest points where the AI in track and trace solutions market is broadening beyond its original regulated base.

The market is also finding steady demand from medical devices and adjacent sectors. Medical devices are subject to UDI rules under FDA and EU MDR frameworks, so identity capture and verification remain necessary across device, case, and carton levels. Other end users widen the demand pool further, including food and beverage under FSMA 204 and industrial categories that will be affected by ESPR-linked passport requirements. That means the addressable base is becoming more diverse, even though pharmaceuticals still provide the anchor share. The AI in track and trace solutions market is therefore evolving from a pharma-heavy use case into a broader cross-industry operating layer.

Geography Analysis

The market was led by North America with 38.2% revenue share in 2025. The region’s lead came from the most mature pharmaceutical serialization regime, where DSCSA created a long procurement cycle across manufacturers, distributors, and dispensers. In the AI in track and trace solutions market, North American buyers are now moving beyond basic compliance toward optimization uses such as predictive analytics, agentic orchestration, and broader enterprise visibility. FDA’s Office of Compliance completed more than 50 DSCSA surveillance inspections in FY 2025 and kept enforcement pressure visible, which supports continued spending after go-live.

The market is expanding fastest in Asia-Pacific at 26.4% CAGR through 2031. The region benefits from staggered policy maturity across China, India, Japan, South Korea, Thailand, and Indonesia, because overlapping compliance cycles create repeated purchase windows rather than one single wave. India’s February 2025 move to consolidate pharmaceutical export traceability under CDSCO simplified the compliance path and strengthened demand for GS1-aligned platforms. China’s NMPA drug traceability system is also supporting demand for exception management and EPCIS-compatible deployments in a very large manufacturing base. In the AI in track and trace solutions market, greenfield pharmaceutical investment in Southeast Asia gives some suppliers a clean starting point without the legacy retrofit burden seen in older markets.

The market also holds a significant position in Europe, where EU FMD maturity remains high and compliance rates in major markets exceeded 95% in 2025. The more important next step is the Digital Product Passport under ESPR, which starts with batteries in February 2027 and then extends to other categories through delegated acts planned for 2026 and 2027. This creates a new buying cycle across consumer goods, electronics, and industrial manufacturers that did not previously need full serialization stacks. OPTEL’s February 2026 partnership with Techno Service for Egyptian Drug Authority compliance also shows how the Middle East and Africa are building national traceability systems, while Brazil and Saudi Arabia remain active emerging pockets outside the main European core.

Competitive Landscape

The market is moderately consolidated in platform software and more fragmented in hardware and services. Full-stack vendors hold an advantage because buyers increasingly want one provider to support audit trails, data exchange, edge capture, and cloud workflow management. In the AI in track and trace solutions market, SAP, TraceLink, and OPTEL remain central names in the platform tier because they combine installed compliance relationships with broader orchestration capabilities. SAP stated that ATTP was deployed across 18 of the top 20 global pharmaceutical manufacturers, while SAP ICH connected more than 6,000 entities and processed 1.5 million messages per month.

The market is also separating vendors by the strength of their network effects. TraceLink reported 7 billion regulated transactions in 2025 and 971% year-over-year growth in MINT live links, which shows how event volume can make a platform harder to displace once partner connectivity is established. OPTEL is competing with a compliance-led posture through its VerifyBrand SaaS platform, AI-powered vision inspection, ISO 27001 certification, and SOC 2 Type II attestation. Hardware-oriented suppliers are trying to move up the stack as well. Zebra’s March 2025 collaboration with Merck KGaA linked Zebra’s TC58 mobile computer with Merck’s M-Trust SEC-Reader to create verified product-origin data. Antares Vision added its AI-GO visual inspection module in 2025, and Crane NXT later completed a 32.4% stake acquisition in Antares Vision Group, which underlined the value of combining machine vision with traceability software.

The market still leaves room for niche growth even as larger vendors deepen their positions. Honeywell’s April 2026 sale of its Productivity Solutions and Services division to Brady Corporation suggested that established AIDC vendors without a clear AI position may prefer exit over direct competition. In the AI in track and trace solutions market, the clearest open spaces are managed serialization services for SMEs in APAC and MEA, EPCIS exception management across multi-hub networks, and Digital Product Passport-ready offerings for non-pharma sectors. Those gaps are meaningful because the next wave of buyers includes companies with less internal regulatory and systems capacity than large global pharmaceutical manufacturers.

AI In Track And Trace Solutions Industry Leaders

OPTEL Group

SAP

TraceLink Inc.

Zebra Technologies

Antares Vision Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: OPTEL and Kaster Technologies partnered to bring AI-driven production planning to the pharmaceutical industry. By combining demand signals with serialization event data, they aim to make batch scheduling more efficient and reduce waste.

- February 2026: Zebra Technologies launched the AI-powered TC501 and TC701 mobile computers for logistics. These devices feature on-device AI that enables real-time barcode decoding, OCR, and scan verification, making warehouse operations faster and more accurate.

Global AI In Track And Trace Solutions Market Report Scope

As per the scope of the report, AI in track and trace solutions refers to the use of Artificial Intelligence technologies to enhance the processes of tracking and tracing products, shipments, or assets throughout the supply chain. These solutions leverage AI algorithms, machine learning, and data analytics to improve accuracy, efficiency, and transparency in monitoring the movement and status of items from origin to destination.

The segmentation for AI in the track and trace solutions market is categorized by component, technology/data carrier, application/workflow, end-use industry, and geography. By component, the market includes AI software platforms, hardware and edge capture systems, and services. By technology/data carrier, it encompasses 2D barcodes and DataMatrix, RFID and NFC, AI computer vision, OCR, and OCV, IoT sensors and environmental monitoring, and EPCIS, event repositories, and blockchain. By application/workflow, the segmentation covers serialization, aggregation, verification and authentication, compliance reporting and recall management, and supply-chain visibility and exception management. By end-use industry, the market is divided into pharmaceuticals and biopharmaceuticals, medical devices, consumer goods and cosmetics, and others.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| AI Software Platforms |

| Hardware and Edge Capture Systems |

| Services |

| 2D Barcodes and DataMatrix |

| RFID and NFC |

| AI Computer Vision, OCR, and OCV |

| IoT Sensors and Environmental Monitoring |

| EPCIS, Event Repositories, and Blockchain |

| Serialization |

| Aggregation |

| Verification and Authentication |

| Compliance Reporting and Recall Management |

| Supply-Chain Visibility and Exception Management |

| Pharmaceuticals and Biopharmaceuticals |

| Medical Devices |

| Consumer Goods and Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | AI Software Platforms | |

| Hardware and Edge Capture Systems | ||

| Services | ||

| By Technology / Data Carrier | 2D Barcodes and DataMatrix | |

| RFID and NFC | ||

| AI Computer Vision, OCR, and OCV | ||

| IoT Sensors and Environmental Monitoring | ||

| EPCIS, Event Repositories, and Blockchain | ||

| By Application / Workflow | Serialization | |

| Aggregation | ||

| Verification and Authentication | ||

| Compliance Reporting and Recall Management | ||

| Supply-Chain Visibility and Exception Management | ||

| By End-use Industry | Pharmaceuticals and Biopharmaceuticals | |

| Medical Devices | ||

| Consumer Goods and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current outlook for AI in track and trace solutions?

The AI in track and trace solutions market is projected to move from USD 1.53 billion in 2026 to USD 4.52 billion by 2031 at a 24.25% CAGR, with growth supported by regulation, data visibility needs, and broader product passport rollout.

Why is North America leading revenue in 2025?

North America held 38.2% of revenue in 2025 because DSCSA created the most mature serialization environment, and buyers are now adding analytics and orchestration on top of that installed base.

Which region is growing fastest through 2031?

Asia-Pacific is forecast to grow at 26.4% CAGR through 2031 as China, India, Japan, South Korea, and other markets move through overlapping traceability upgrades.

Which component type is leading adoption?

AI Software Platforms led with 45.2% share in 2025 because buyers are prioritizing orchestration, partner connectivity, and event-data reuse over stand-alone hardware purchases.

What is the fastest-growing application area?

Supply-Chain Visibility and Exception Management is projected to expand at 29.2% CAGR through 2031 as companies use traceability data for logistics control, recall precision, and operating response.

Why are consumer goods and cosmetics gaining momentum?

Consumer Goods and Cosmetics is projected to grow at 26.3% CAGR through 2031 because GS1 Sunrise 2027 and EU Digital Product Passport rules are pushing non-pharma brands to add traceability and consumer-facing authentication.

Page last updated on: