AI In Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

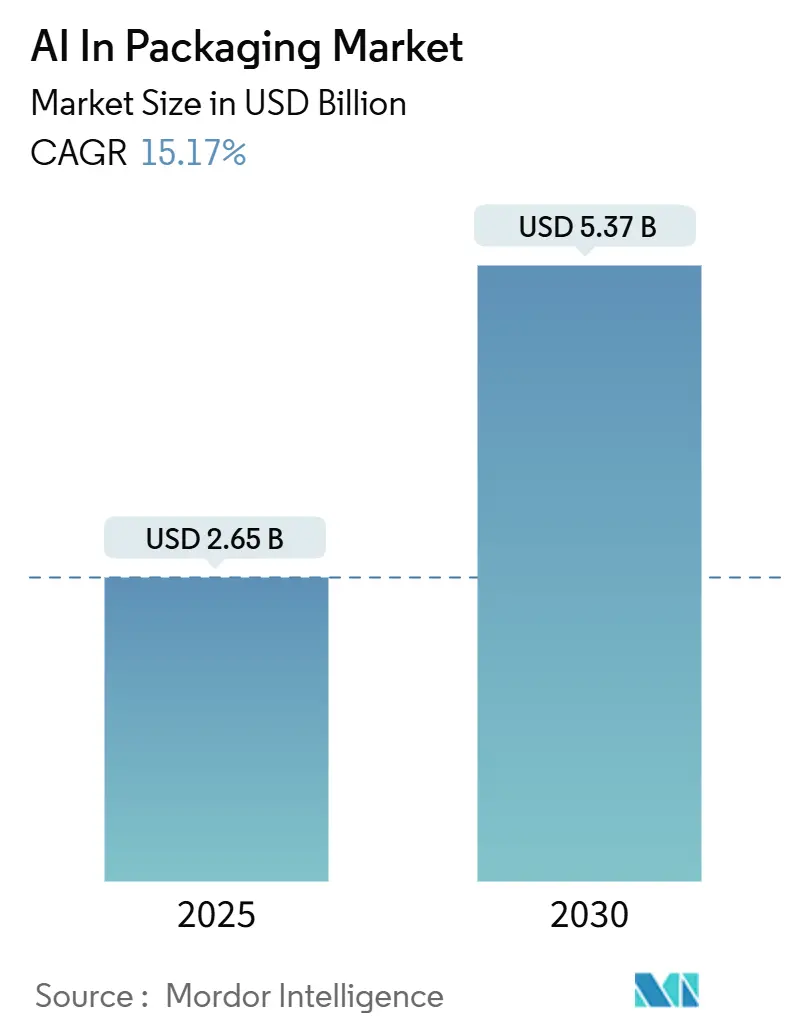

| Market Size (2025) | USD 2.65 Billion |

| Market Size (2030) | USD 5.37 Billion |

| Growth Rate (2025 - 2030) | 15.17% CAGR |

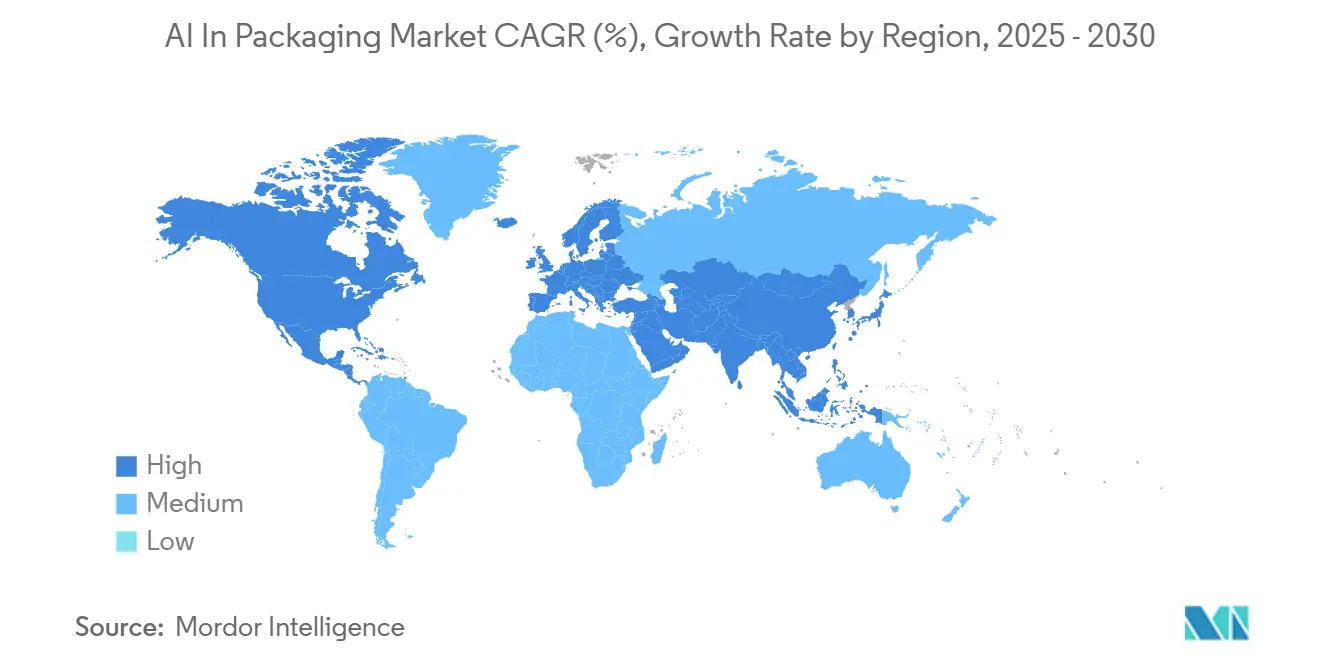

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

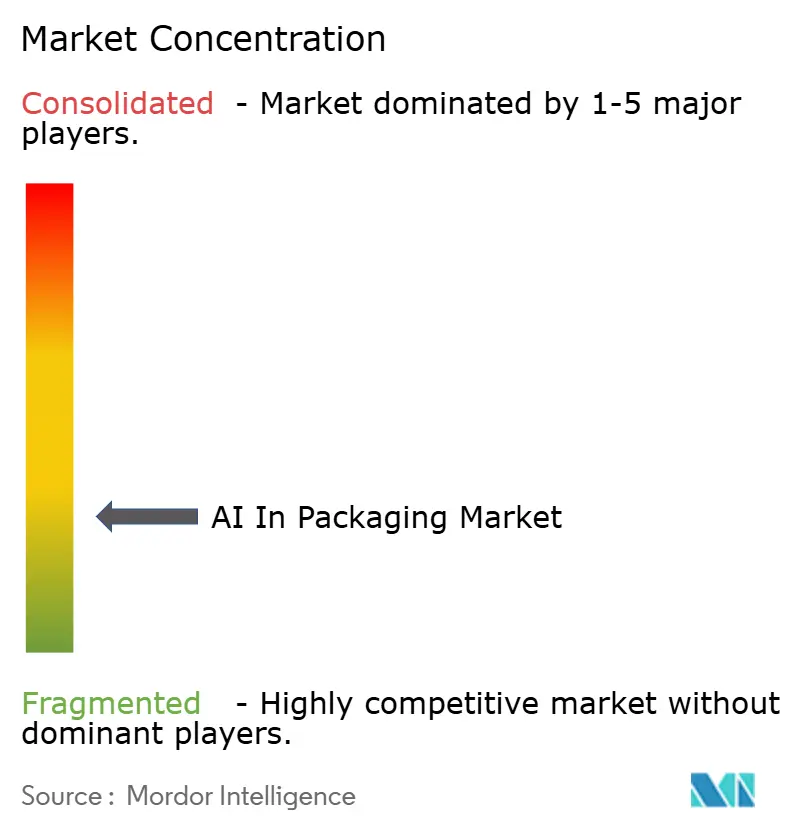

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Packaging Market Analysis by Mordor Intelligence

The AI In Packaging Market size is estimated at USD 2.65 billion in 2025, and is expected to reach USD 5.37 billion by 2030, at a CAGR of 15.17% during the forecast period (2025-2030). This momentum positions the AI in packaging market size as one of the most rapidly scaling technology segments inside the broader smart manufacturing space. Accelerators include continuous labor shortages on plant floors, a sharp uptick in e-commerce order complexity, and stringent global regulations that require traceability at the individual‐unit level. Machine learning‐driven vision systems now conduct quality checks that once required multiple human inspectors, while generative models compress packaging design timelines from months to weeks. Brands also view AI as a pathway to harsher sustainability goals because predictive analytics can slash waste and improve recyclability by selecting optimal materials. Edge computing architectures, often coupled with private 5G, enable real-time AI execution on the line, giving manufacturers the speed and data sovereignty they require without a round trip to the public cloud.

Key Report Takeaways

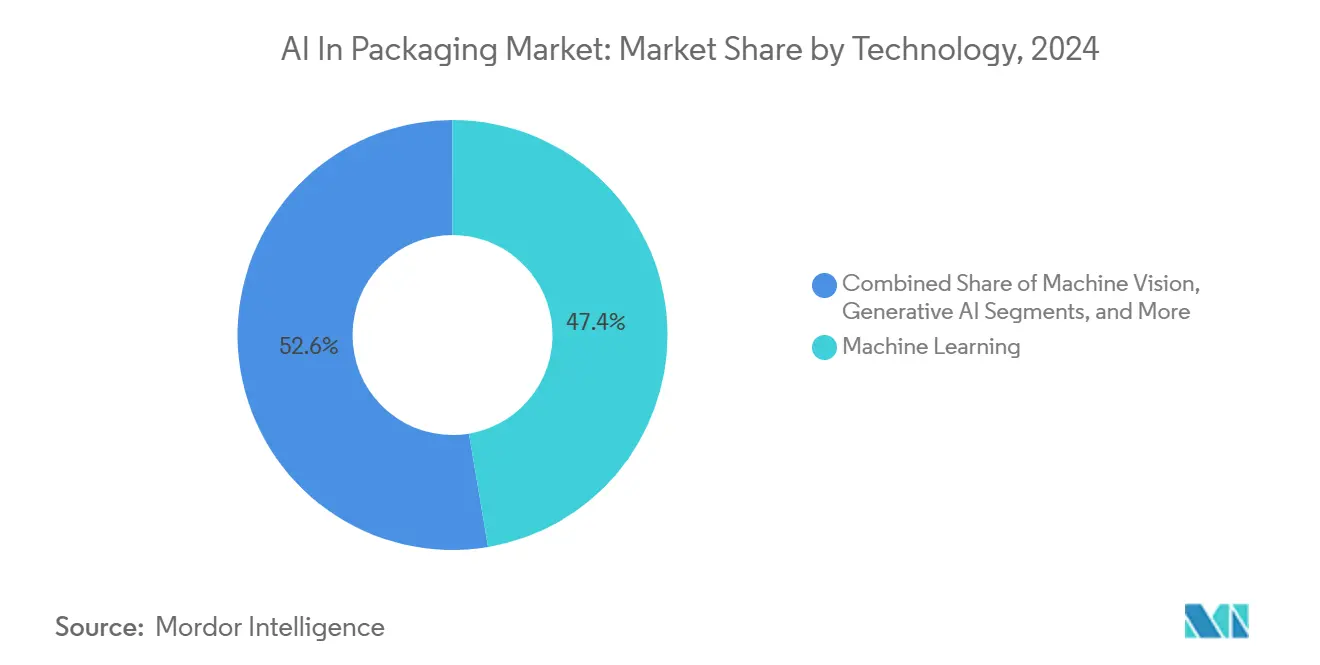

- By technology, machine learning held 47.36% of the AI in packaging market share in 2024, while generative AI is projected to expand at a 27.54% CAGR through 2030.

- By application, design and customization contributed 33.12% of the AI in packaging market size in 2024; recycling and sustainability enablement is forecast to accelerate at a 24.32% CAGR to 2030.

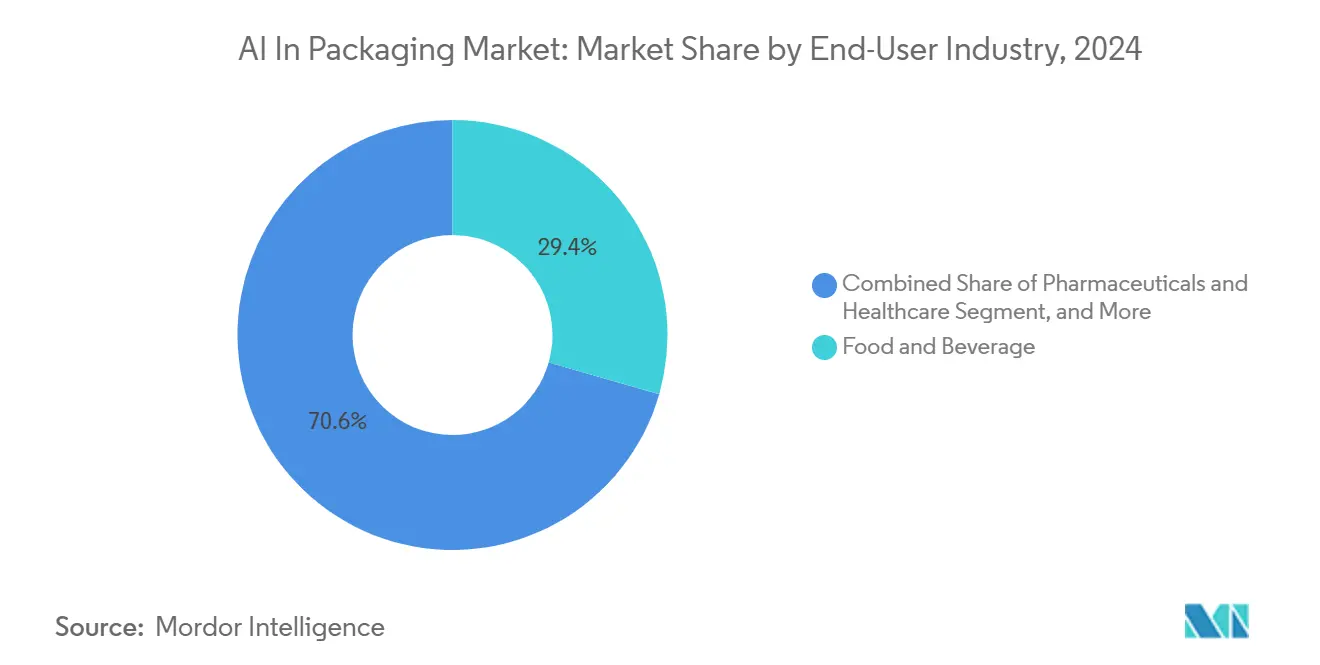

- By end-user industry, food and beverage led with 29.45% revenue share in 2024, whereas e-commerce and logistics is advancing at a 21.18% CAGR through 2030.

- By deployment mode, on-premise edge solutions commanded 93.56% of the 2024 AI in packaging market share, but hybrid deployments are growing at 20.07% CAGR to 2030.

- By geography, North America captured 36.78% share in 2024, while Asia-Pacific is set to grow fastest at an 18.45% CAGR to 2030.

Global AI In Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-shortage-driven automation demand | +3.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Escalating e-commerce throughput and accuracy needs | +2.8% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Regulatory push for unit-level traceability | +2.1% | Europe and North America expanding to Asia-Pacific | Long term (≥ 4 years) |

| Edge-AI and private-wireless convergence on shop floor | +1.9% | Manufacturing hubs worldwide | Medium term (2-4 years) |

| Breakthrough AI-enzyme recycling lowers rPET cost | +1.7% | Europe leading, global expansion | Long term (≥ 4 years) |

| Generative-AI-led lightweight sustainable design | +1.5% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor-Shortage-Driven Automation Demand

Manufacturing operators across the United States reported more than 800,000 open manufacturing roles in 2024, and packaging lines are among the hardest positions to fill because tasks are repetitive, physically taxing, and require round-the-clock staffing. [1]“Job Openings and Labor Turnover Summary,” U.S. Bureau of Labor Statistics, bls.gov Producers now deploy collaborative robots guided by computer vision to manage variable product forms, freeing human workers for higher-value activities. Reported productivity gains range from 25% to 40% once AI systems assume repeatable inspection and material-handling duties, and average investment payback has compressed to under two years due to surging wage inflation. The combination of vision recognition, gripper sophistication, and real-time path planning allows robots to handle delicate items without reprogramming for every SKU, a task once deemed impractical for automation. These capabilities let midsize manufacturers access the same efficiencies that only large multinationals could once afford. Wider adoption should continue as national policies tie grant funding to productivity improvements in advanced manufacturing.

Escalating E-commerce Throughput and Accuracy Needs

Amazon alone processed more than 5 billion parcels in 2024, with machine learning orchestrating 87% of sortation and routing events to achieve same-day delivery targets.[2]“Amazon Fulfillment Innovation,” Amazon, aboutamazon.com On a packaging line, predictive algorithms choose the most space-efficient box on the fly, factoring merchandise dimensions, shipping zone, and projected handling risk, which reduces material usage by roughly 15% while holding error rates below 1%. Natural language models integrated with warehouse systems let operators request replenishment verbally, shrinking decision latency and raising order pick speeds. When demand spikes, advanced analytics forecast material consumption so corrugated supplies arrive on dock hours before bottlenecks form, preventing downtime. For high-velocity retail calendars such as Singles Day and Cyber Monday, automated pack stations scale headcount virtually by adding AI-directed mobile robots instead of temporary staff, keeping throughput consistent regardless of labor availability.

Regulatory Push for Unit-Level Traceability

Drug Supply Chain Security Act deadlines require every pharmaceutical package sold in the United States to carry a unique serialization code that is auditable across the supply network, translating to billions of scans per year.[3]“Drug Supply Chain Security Act Law,” U.S. Food and Drug Administration, fda.gov AI-enhanced camera systems inspect codes at line speed while machine learning models cross-verify data against enterprise resource planning records. Package-level insight improves recall precision, often enabling surgical removals that limit financial losses and protect brand reputation. Food safety authorities are adopting similar traceability frameworks as sensors inside cartons collect temperature, humidity, and shock data, sending analytics to cloud dashboards that isolate compromised lots within minutes, not days. Such visibility underpins stricter consumer protection statutes taking effect across the European Union in 2026, pushing manufacturers to embed AI tools today to avoid steep non-compliance fines later. Investment thresholds are trending downward thanks to modular vision hardware and subscription software models, which helps extend adoption to small regional processors.

Edge-AI and Private-Wireless Convergence on Shop Floor

Seventy-three percent of industrial firms surveyed by major automation providers place on-premise AI capabilities above cloud-first solutions because sub-100 millisecond latency is critical for defect rejection and motion control tasks. Modern industrial PCs outfitted with AI acceleration chips run inferencing algorithms right beside conveyors, returning pass-fail decisions in microseconds. Private 5G networks blanket the factory with deterministic connectivity, so video streams never buffer and command packets never drop. Combining these infrastructures also eliminates data-sovereignty headaches since analytics stay behind corporate firewalls. For predictive maintenance, sensor feeds are processed locally to learn vibration baselines on motors and gearboxes, which allows downtime to be scheduled before catastrophic failure. As chip vendors embed machine learning co-processors directly into smart cameras and servo drives, entry costs continue to fall, broadening access to edge intelligence for even single-line facilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and uncertain ROI for SMEs | -2.3% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Global shortage of AI-skilled packaging engineers | -1.8% | Global, severe in North America and Europe | Medium term (2-4 years) |

| IP and data-governance risks in AI-generated designs | -1.4% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Frequent model-retraining for new mono-materials | -1.1% | Global, advanced manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Uncertain ROI for SMEs

Comprehensive AI retrofits for a single packaging line can exceed USD 500,000, a figure that strains small and medium-sized converters. Integration outlays often double initial hardware spend because legacy PLCs, conveyors, and motion controllers demand custom interfaces. For many SMEs, recruiting systems integrators and training operators represent hidden expenses that drag payback beyond typical two-year investment horizons. Technology obsolescence worry compounds the hesitation: vision sensors bought today risk lagging behind next-generation neural cameras within three years. Financial institutions have begun to offer equipment-as-a-service models, yet loan underwriters still classify AI hardware as high risk, requiring higher collateral than traditional machinery. Consequently, growth in under-50-employee converters is slower than in enterprise plants despite equivalent labor pressures.

Global Shortage of AI-Skilled Packaging Engineers

University programs rarely blend mechatronics, materials science, and machine learning, leaving manufacturers to rebuild curricula internally. Even experienced packaging engineers need between 12 and 18 months of immersive training to become competent in algorithm tuning and data pipeline maintenance.[4]Eliza Strickland, “AI Skills Gap,” IEEE Spectrum, spectrum.ieee.org Compensation gaps further complicate recruitment as pure-tech sectors pay premiums that typical packaging firms cannot match. The result is tight competition for a small talent pool and soaring wages that eat into the savings AI solutions would otherwise provide. In response, some industry consortia are pooling resources to create shared centers of excellence, where mid-tier converters can access experts on a project basis, but global demand for those experts still outstrips supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Machine Learning Anchors Immediate Value

Machine learning contributed 47.36% of 2024 revenues, ensuring the AI in packaging market retained a foundation of proven defect detection and predictive maintenance use cases. Generative models are the fastest-moving layer, registering a 27.54% CAGR through 2030, because they automate parametric design to deliver lighter, more sustainable formats without compromising protective strength. Early adopters link computer vision feeds to reinforcement learning agents that adjust line speeds and reject thresholds autonomously, raising first-pass yield. Integration among machine learning modules, generative design engines, and robotics control logic is tightening as vendors converge around standardized industrial protocols. The compound effect is a virtuous cycle where vision data informs design optimization, which then feeds back into robotic handling parameters.

Robotics AI control systems are gaining prominence in pharma and beverage bottling lines that run 24 hours daily, employing adaptive grasping algorithms to switch SKUs on the fly. Natural language interfaces are surfacing for maintenance tasks, allowing technicians to query downtime diagnostics conversationally rather than sift through log files. While still niche, chatbots cut troubleshooting times by giving frontline workers real-time suggestions derived from historical incident libraries. Adoption of these ancillary technologies amplifies the installed base of core machine learning engines, reinforcing the AI in packaging market as an ecosystem rather than a bundle of point solutions.

By Application: Design Innovation Sparks Sustainability Transformation

Design and customization held 33.12% share in 2024, underscoring brand demand for rapid iteration and limited-edition packaging drops. Algorithms now evaluate structural strength, print registration, and stacking efficiency concurrently, which compresses physical prototyping cycles from six iterations to two. Recycling and sustainability enablement is expanding at 24.32% CAGR, aligning with mandates that impose minimum recycled content and penalize excessive material usage. Predictive analytics models quantify trade-offs between weight reduction and protective performance so engineers can validate eco-friendly choices before committing to tooling. Quality inspection remains a critical gateway application because defect detection delivers instant waste reduction and customer satisfaction payoffs, making it a low-risk entry point.

Smart packaging is entering mainstream programs where RFID, NFC, or QR codes transmit condition data. Machine learning dashboards analyze inbound signals to flag temperature excursions or shocks, thereby protecting high-value perishables. Predictive maintenance engines complement those capabilities by analyzing servo torque and conveyor vibration, trimming unplanned downtime by up to 40% in high-speed canning lines. Supply chain optimization algorithms round out the application mix by forecasting material inventory, preventing both line stoppages and obsolete stock write-offs. Together, these workflows push the AI in packaging market toward a circular manufacturing future where every gram of fiber or resin is tracked, minimized, and recovered.

By End-User Industry: Food Dominance Faces E-commerce Momentum

Food and beverage accounted for 29.45% of 2024 spending because regulatory regimes governing contamination prevention and allergen labeling leave little room for error. Vision-guided robotics inspect fill levels and cap integrity faster than human line staff, and digital twins simulate line changes before actual production, accelerating launches of new flavors. E-commerce and logistics applications are the fastest climbers at 21.18% CAGR, driven by small-parcel shipping that demands form factors optimized for both dimensional weight pricing and consumer unboxing experience. AI helps fulfillment centers pick just-right box sizes, cutting void fill usage and last-mile damage claims.

Pharmaceutical companies rank high in AI penetration given serialization mandates and the life-and-death stakes of dosage accuracy. Consumer electronics brands use generative design to create molded fiber inserts that protect fragile components without polystyrene. Automotive suppliers, facing costly warranty claims for scratched parts, apply predictive analytics to predict shock exposure during transport and specify reinforcements only where statistically necessary. Cosmetics entrench AI for aesthetic design, applying computer-vision sentiment analysis to gauge color combinations likely to resonate on social platforms.

By Deployment Mode: Edge Reliability Meets Hybrid Flexibility

On-premise edge solutions made up 93.56% of 2024 spend because milliseconds matter; a single missed reject at 600 ppm line speeds can trigger entire batch recalls. Local execution also satisfies data-sovereignty mandates in pharmaceuticals and defense packaging. That said, enterprises are layering cloud-based analytics atop local inference, yielding a hybrid model that grows 20.07% CAGR. Cloud instances train large models overnight using aggregated datasets from many plants, then push distilled parameters back to line-side hardware. This partitioning delivers both scale and reliability, propelling the AI in packaging market toward harmonized architectures that share domain knowledge across global networks without compromising uptime.

Private cloud setups appeal to multinationals with dozens of plants, providing centralized governance over algorithm versions and audit trails. Cost barriers fall as AI accelerator prices decline, letting even single-line SMEs host inference engines locally. As silicon roadmaps promise double-digit performance gains annually, the compute budget per node continues to drop, further democratizing access.

Geography Analysis

North America commanded 36.78% of 2024 revenue thanks to early Industry 4.0 pilots, robust venture funding for automation startups, and sizable regulatory investments in food and drug safety. Regional beverage giants have standardized on AI-directed vision inspection, cutting spoilage and recall exposure. Many facilities brought cloud training clusters in-house to mitigate concerns about third-party data access, and tax incentives encouraged capital spending on advanced machinery. Despite this head start, the AI in packaging market grows at single-digit rates locally compared with double-digit upswings overseas.

Asia-Pacific generates the most aggressive growth curve at 18.45% CAGR. Governments in China, South Korea, and Singapore co-finance industrial AI deployments, and massive consumer goods exporters adopt edge-based quality inspection to maintain competitiveness. Regional electronics giants push suppliers to embed traceability tags linked to real-time analytics for defect root-cause analysis, spurring adoption even among small subcontractors. Local OEMs now offer bundled AI modules with new filling or forming equipment, cutting integration effort and lowering entry thresholds. Consequently, Asia-Pacific may eclipse North America in total investment before the decade closes.

Europe remains the sustainability trendsetter, with circular economy regulations nudging converters toward AI models that minimize resin usage and validate recycled content levels. Custom duty exemptions for recyclable formats incentivize firms to upgrade inspection lines. In parallel, Middle East and Africa markets are emerging via economic diversification programs that build greenfield factories from scratch, integrating AI at day one. South American adoption is steadier but benefits from export demand to North American retailers, who mandate serialized, machine-verified packaging before accepting shipments.

Competitive Landscape

The competitive arena features legacy automation majors like Cognex, Keyence, Omron, SICK AG, ABB, and FANUC, each layering machine learning onto established sensor and robotics portfolios. Vision specialists integrate deep learning into edge cameras that recognize defects invisible to conventional rule-based systems, halving false reject rates. Robotics leaders acquire AI navigation startups to embed simultaneous localization and mapping inside collaborative arms, enabling packaging tasks on variable conveyor layouts. Meanwhile, software-first entrants leverage open-standard OPC UA and MQTT interfaces to connect disparate legacy assets without costly hardware swaps.

Consolidation is rising as equipment OEMs buy niche AI firms to present full-stack platforms to buyers overwhelmed by heterogeneous toolchains. Packaging‐specific startups differentiate via pre-trained models tuned to corrugate, bottle, or blister formats, which shorten time-to-value. Value shifts from hardware margins toward annual software subscriptions that offer continuous algorithm updates. Vendors able to supply predictive maintenance, vision inspection, and generative design under a single license increasingly win multi-line tenders because procurement teams favor integrated support contracts. Open ecosystems still thrive for custom use cases, but most end-users gravitate toward turnkey bundles that guarantee performance and compliance.

Security and governance now influence deal decisions. Companies with strong data-protection frameworks, including encrypted edge storage and on-device model execution, command premium pricing. Regional partners also matter as buyers seek local language service teams and spare-parts depots. Given the talent shortage, service models that embed remote AI engineers inside subscription packages gain favor, allowing plants to outsource algorithm tuning without hiring scarce specialists. Overall, supplier strategies converge on solution breadth, ecosystem openness, and lifecycle services to cement recurring revenue streams, cementing moderate market concentration within the decade.

AI In Packaging Industry Leaders

Cognex Corporation

Omron Corporation

Antares Vision S.p.A.

Mettler-Toledo International Inc.

SICK AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cognex Corporation began volume shipments of its In-Sight D900 deep-learning vision suite to European beverage bottlers seeking sub-second cap integrity inspection.

- October 2024: Cognex Corporation launched its AI-powered In-Sight D900 vision system specifically for packaging applications, reducing false rejects by 50% compared with rule-based alternatives.

- September 2024: Siemens Digital Industries Software committed USD 150 million to AI-driven packaging optimization software that links to Opcenter manufacturing execution.

- August 2024: SICK AG partnered with Microsoft Azure to co-develop cloud-connected smart sensors that blend edge AI with cloud analytics for predictive maintenance.

- July 2024: ABB Ltd. acquired Sevensense Robotics for USD 85 million to upgrade mobile robots with advanced navigation for complex packaging assignments.

Global AI In Packaging Market Report Scope

The AI in Packaging Market Report is Segmented by Technology (Machine Vision, Machine Learning and Analytics, Generative AI, Natural-Language and Chatbots, Robotics AI Control Systems, Other Technologies), Application (Quality Inspection and Defect Detection, Packaging Design and Customization, Smart/Intelligent Packaging and Tracking, Predictive Maintenance and Asset Optimization, Supply-Chain and Inventory Optimization, Recycling and Sustainability Enablement, Other Applications), End-user Industry (Food and Beverage, Pharmaceuticals and Healthcare, Consumer Electronics, Cosmetics and Personal Care, Industrial and Automotive, E-commerce and Logistics, Other End-user Industries), Deployment Mode (On-premise Edge, Cloud-based, Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD), Based on Availability.

| Machine Vision |

| Machine Learning and Analytics |

| Generative AI |

| Natural-Language and Chatbots |

| Robotics AI Control Systems |

| Other Technologies |

| Quality Inspection and Defect Detection |

| Packaging Design and Customization |

| Smart / Intelligent Packaging and Tracking |

| Predictive Maintenance and Asset Optimization |

| Supply-Chain and Inventory Optimization |

| Recycling and Sustainability Enablement |

| Other Applications |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Consumer Electronics |

| Cosmetics and Personal Care |

| Industrial and Automotive |

| E-commerce and Logistics |

| Other End-user Industries |

| On-premise Edge |

| Cloud-based |

| Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Machine Vision | ||

| Machine Learning and Analytics | |||

| Generative AI | |||

| Natural-Language and Chatbots | |||

| Robotics AI Control Systems | |||

| Other Technologies | |||

| By Application | Quality Inspection and Defect Detection | ||

| Packaging Design and Customization | |||

| Smart / Intelligent Packaging and Tracking | |||

| Predictive Maintenance and Asset Optimization | |||

| Supply-Chain and Inventory Optimization | |||

| Recycling and Sustainability Enablement | |||

| Other Applications | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals and Healthcare | |||

| Consumer Electronics | |||

| Cosmetics and Personal Care | |||

| Industrial and Automotive | |||

| E-commerce and Logistics | |||

| Other End-user Industries | |||

| By Deployment Mode | On-premise Edge | ||

| Cloud-based | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue value is forecast for the AI in packaging market by 2030?

The sector is projected to reach USD 5.37 billion by 2030, sustained by a 15.17% CAGR over the forecast period.

Which technology currently delivers the highest revenue inside packaging lines?

Machine learning accounts for 47.36% of 2024 revenues, largely due to its proven quality inspection and predictive maintenance performance.

Why are hybrid deployment models gaining interest?

Manufacturers realize they can keep millisecond-level edge responsiveness for production tasks while leveraging cloud resources for model training, resulting in a 20.07% CAGR for hybrid setups.

Which region shows the quickest expansion?

Asia-Pacific is advancing at an 18.45% CAGR as state incentives and large exporter requirements drive rapid AI uptake across packaging plants.

How does AI help meet sustainability goals?

Generative design algorithms cut material mass, predictive analytics optimize recycled content ratios, and vision systems slash in-process waste, collectively reducing environmental impact while enhancing cost efficiency.

Page last updated on: