Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

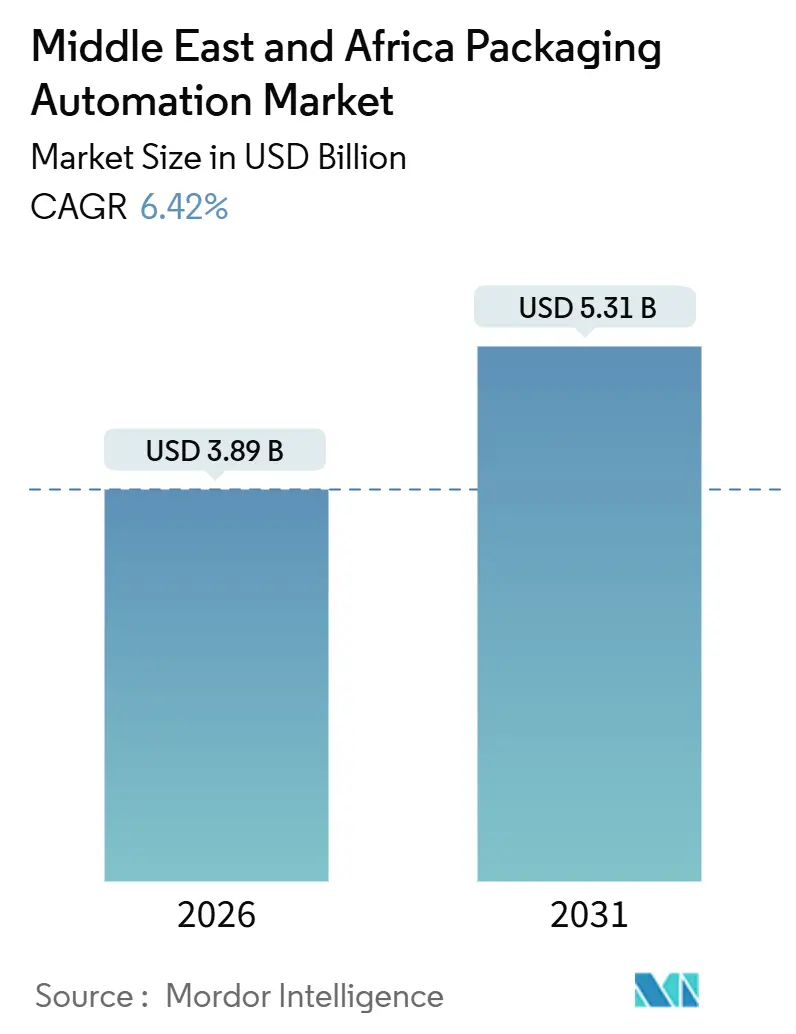

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Packaging Automation Market Analysis by Mordor Intelligence

The Middle East and Africa packaging automation market size reached USD 3.89 billion in 2026 and is projected to climb to USD 5.31 billion by 2031, reflecting a 6.42% CAGR over the forecast period. Rising labor costs in Gulf Cooperation Council economies and South Africa, as well as mandatory food-safety traceability laws, fast-scaling e-commerce fulfillment infrastructure, and sustained industrial investment under national diversification programs, are converging to sustain demand for high-speed, data-rich end-of-line solutions. Automated filling remains the largest installed base, but robotic palletising and case-packing lines are expanding fastest as omni-channel retailers compress delivery windows and manufacturers seek higher throughput with tighter quality control. Vendors able to combine hardware, digital-twin software, and multi-year service contracts under one roof are winning turnkey awards, pushing smaller suppliers toward specialist niches or regional integration partnerships. The Middle East and Africa packaging automation market continues to benefit from demographic growth, urbanization, and the steady rise in packaged food, beverage, and pharmaceutical consumption, despite power-quality gaps and capital-access constraints tempering short-term uptake in parts of Sub-Saharan Africa.

Key Report Takeaways

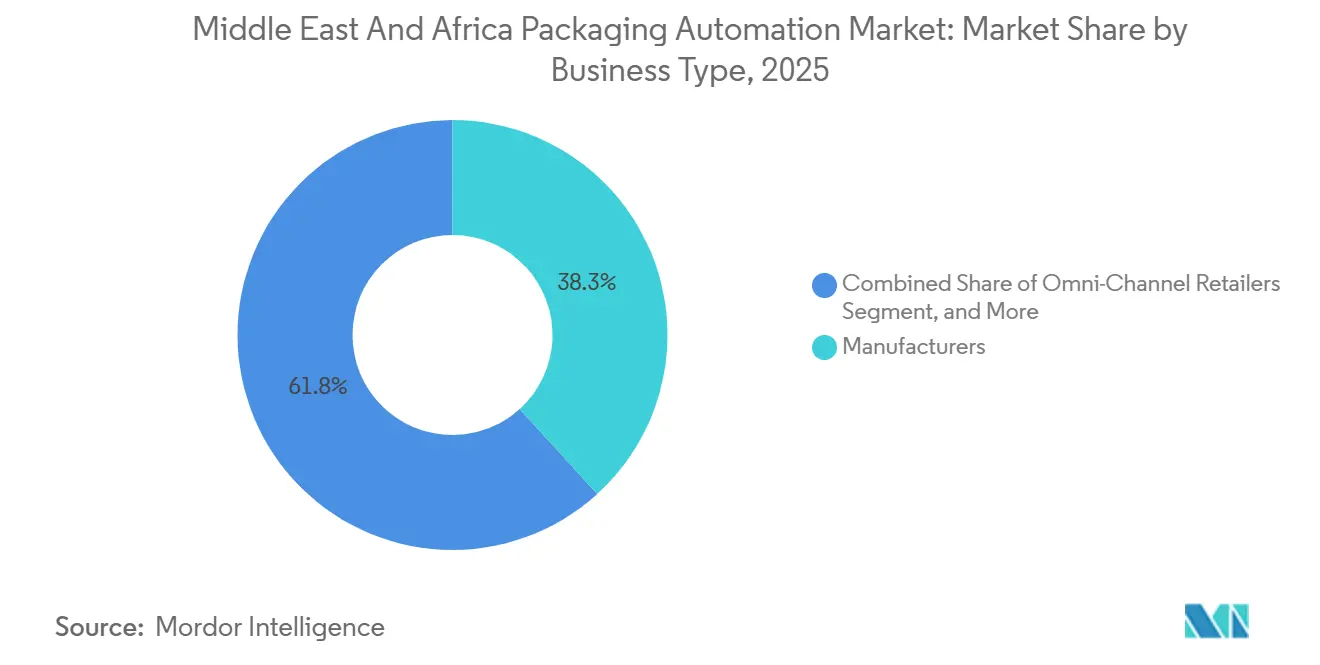

- By business type, manufacturers captured 38.25% of the Middle East and Africa packaging automation market share in 2025.

- By product type, the Middle East and Africa packaging automation market size for palletizing systems is projected to grow at an 8.57% CAGR between 2026 and 2031.

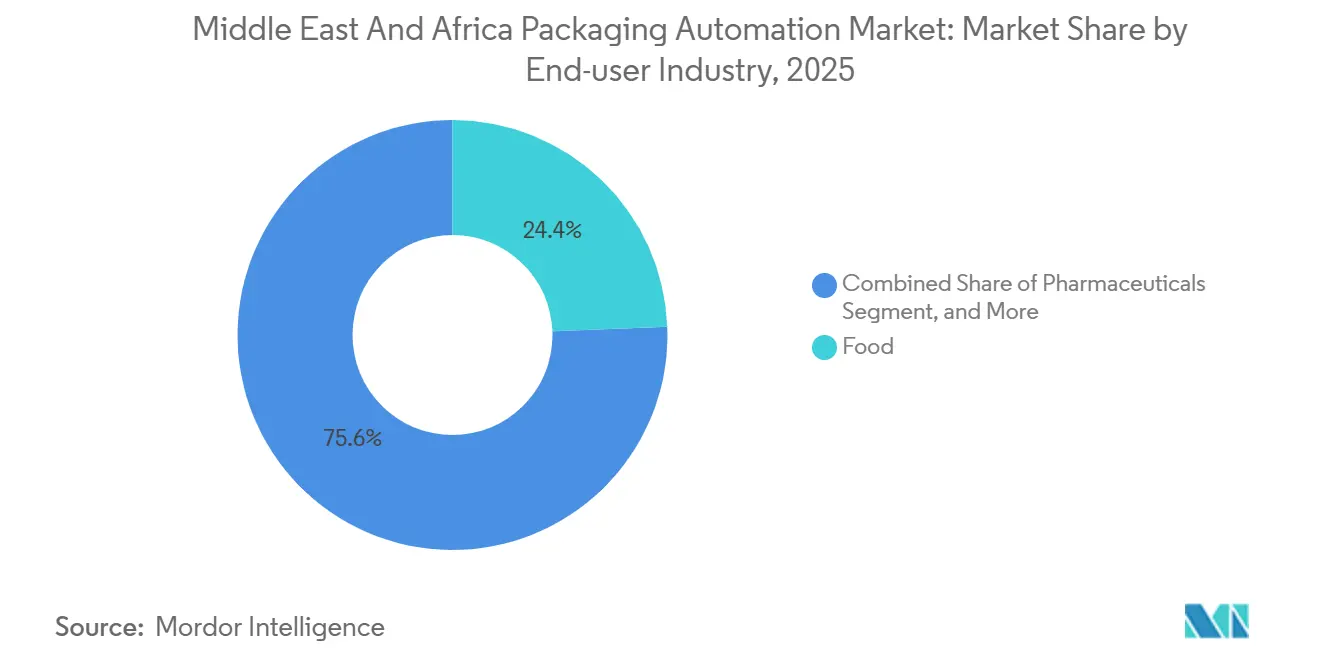

- By end-user industry, food processors captured 24.39% of the Middle East and Africa packaging automation market share in 2025.

- By country, the Middle East and Africa packaging automation market size for South Africa is projected to grow at an 8.19% CAGR between 2026 and 2031.

Middle East And Africa Packaging Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Labor-Cost Inflation Across GCC and South Africa | +1.2% | GCC core (UAE, Saudi Arabia, Qatar, Kuwait, Bahrain), South Africa | Medium term (2-4 years) |

| Mandatory Food-Safety Traceability Laws Driving Line Upgrades | +1.0% | Global, with early enforcement in GCC, Egypt, and South Africa | Short term (≤ 2 years) |

| E-Commerce Fulfilment Boom Demanding High-Speed End-of-Line Automation | +1.4% | GCC (UAE, Saudi Arabia), Egypt, South Africa | Short term (≤ 2 years) |

| Surging Investments in GCC Pharma Fill-Finish Facilities | +0.9% | GCC (UAE, Saudi Arabia, Qatar, Bahrain) | Medium term (2-4 years) |

| AI-Enabled Predictive-Maintenance Platforms Reducing Unplanned Downtime | +0.7% | Global, with early adoption in GCC and South Africa | Long term (≥ 4 years) |

| Water-Scarcity Push for Dry-Clean-In-Place (DCIP) Automated Systems | +0.6% | GCC, North Africa (Egypt, Algeria), select Sub-Saharan markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Labor-Cost Inflation Across GCC and South Africa

Labor-cost growth is shortening payback periods for robotic case packing and palletizing, making automation more attractive to mid-sized processors that previously relied on manual packaging. Wage pressure in South Africa and tighter expatriate-labor rules in the GCC have amplified the labor substitution effect. Apparel Group’s 300,000-unit-per-day automated fulfillment center in Dubai and Starlinks’ Riyadh hub, equipped with 254 autonomous mobile robots, illustrates the scale at which retailers are offsetting labor constraints with machine throughput. Lights-out warehousing is no longer a fringe concept; it is becoming the default for new fulfillment projects across major Gulf logistics parks. As wage escalation outpaces productivity, capital budgets continue to tilt toward high-speed, sensor-rich equipment that delivers predictable takt times and lower total cost per case.

E-Commerce Fulfillment Boom Demanding High-Speed End-of-Line Automation

Online retail has moved beyond urban millennials to capture a far wider consumer base, pushing fulfillment centers to process tens of thousands of small orders each day. Carrefour’s automation of grocery picking in the United Arab Emirates and Brands for Less' adopting of goods-to-person systems in Dubai confirm that next-day delivery commitments depend on automated bagging, labeling, and mixed-SKU palletising. Ship-from-store programs are proliferating, forcing retailers to install compact end-of-line systems in backrooms with tight footprints. Modular carton erectors, poly-baggers, and robotic palletisers configured for heterogenous SKU flows are now standard specification items in Gulf design-build tenders. As pure-play e-commerce and traditional retailers converge on an omni-channel model, regional demand for flexible secondary packaging automation is forecast to outpace the installation of new primary filling lines.

Mandatory Food-Safety Traceability Laws Driving Line Upgrades

Region-wide adoption of GS1 batch-level tracking standards requires producers to integrate serialization, vision inspection, and automated labeling into their existing packaging architectures. Pharmaceutical plants have led the charge as compliance with the EU Falsified Medicines Directive and the U.S. Drug Supply Chain Security Act becomes non-negotiable for export. Zetes and VISIOTT installations across Saudi Arabia and the United Arab Emirates provide real-time aggregation data at carton and pallet levels, closing gaps that previously exposed the supply chain to counterfeit risk.[1]“Zetes track-and-trace platform for GCC pharmaceuticals,” Zetes, zetes.com Food processors are now following suit, adding inline cameras, checkweighers, and barcode scanners tied to cloud quality-management software. These retrofits often trigger PLC upgrades and the installation of industrial Ethernet backbones, creating incremental demand for control vendors that can harmonize multi-vendor machines under a unified data model.

Surging Investments in GCC Pharma Fill-Finish Facilities

Gulf governments seeking autonomy in drug security are investing in aseptic filling and lyophilization plants. OZON Pharmaceuticals allocated AED 293 million (USD 79.3 million) to boost Dubai injectable capacity, while Acino’s Sharjah expansion underscores momentum behind regional fill-finish hubs. Integrated vial handling, precision dosing, tamper-evident capping, and automated visual inspection systems are procured as single-vendor blocks to satisfy stringent EU Good Manufacturing Practice and U.S. Food and Drug Administration standards. Demand extends into emerging African markets, as highlighted by Julphar’s Ethiopia plant, which is built to supply 25 million bottles annually. These facilities utilize flexible lines that can accommodate multiple container formats, minimize changeover downtime, and protect investment against shifting drug portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX and Long Payback Periods | -0.8% | Sub-Saharan Africa, select North African markets (Egypt, Algeria) | Short term (≤ 2 years) |

| Skilled Automation-Engineer Shortage in Sub-Saharan Africa | -0.6% | Sub-Saharan Africa (Nigeria, Kenya, Ethiopia, Angola) | Medium term (2-4 years) |

| Patchy Power-Quality Increasing Component Failure Rates | -0.5% | Sub-Saharan Africa, select North African grids | Medium term (2-4 years) |

| Restrictive Import Tariffs on Motion-Control Hardware in Egypt and Kenya | -0.4% | Egypt, Kenya, select East African markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Long Payback Periods

Turnkey filling-to-palletizing blocks can exceed USD 5 million, a threshold that stretches balance sheets for small Sub-Saharan food processors. Currency volatility risk weighs on lenders, leaving many firms to self-finance or defer projects. Greenfield budgets are further impacted by the switch to biodegradable films and recycled polyethylene terephthalate, which necessitate upgrades to heating, sealing, and inspection modules. Equipment makers are aware of market modular lines that allow for staged investment; however, adoption remains limited where after-sales support and spare parts logistics are underdeveloped. Without concessional loans or vendor financing, prospective buyers often postpone automation despite clear productivity gains.

Skilled Automation-Engineer Shortage in Sub-Saharan Africa

Packaging lines built around programmable logic controllers and six-axis robots require technicians proficient in advanced control platforms. Nigeria, Kenya, and Ethiopia report shortages of engineers certified in Siemens TIA Portal or Rockwell Studio 5000. Manufacturers, therefore, often fly in expatriate teams, which inflates commissioning costs and prolongs downtime during maintenance cycles. Siemens addressed the gap by opening an Industry 4.0 Innovation Center in Egypt that offers hands-on training and virtual prototyping modules. Schneider Electric’s partnership with the Abu Dhabi Investment Office pursues a similar workforce-uplift model; however, the scale of these programs lags behind market needs. Until a deeper talent pool emerges, some factories operate sophisticated equipment in manual or semi-automatic modes, eroding the return on capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Type: Omni-Channel Retailers Expand the Fastest

Manufacturers represented 38.25% of the 2025 revenue in the Middle East and Africa packaging automation market, reflecting their ownership of core production assets and a preference for in-house control over primary packaging quality. Omni-channel retailers, however, are projected to post an 8.17% CAGR through 2031 as integrated online-offline fulfillment models proliferate. Apparel Group’s Dubai micro-fulfillment center, utilizing cube storage, automated bagging, and smart labeling, demonstrates how retailers can retrofit compact, high-throughput lines to convert store backrooms into last-mile nodes. Manufacturers continue to invest in aseptic fillers, cappers, and labelers for dairy, beverage, and pharmaceutical operations; however, secondary-packaging outlays are shifting toward retailers and logistics providers that must palletize heterogeneous order profiles in real-time. As private-label production gains momentum, large retailers are blurring the divide between manufacturers and retailers, commissioning hybrid facilities that support both production and direct-to-consumer dispatch.

Flexibility sits at the core of emerging business-type requirements. B2C e-commerce specialists specify baggers that can switch between poly film widths without mechanical changeovers, while B2B platforms favor case packers that adjust on the fly to varied master-carton dimensions. Wholesale distributors, once hesitant, now deploy semi-automated stretch wrappers to stabilize mixed pallets for long-haul transport. Integration partners offering warehouse control software tied to enterprise resource planning systems are best placed to capture this business-type diversification, a dynamic set to reinforce the medium-term trajectory of the Middle East and Africa packaging automation market.

By Product Type: Palletising Systems Lead Growth Upside

Filling equipment captured 36.84% of 2025 spending in the Middle East and Africa packaging automation market, underpinned by high-speed beverage lines such as Krones’ 100,000-bottle-per-hour PET water installation for Mai Dubai. Palletising systems, however, are forecast to record an 8.57% CAGR between 2026 and 2031, reflecting warehouse throughput pressures and growing acceptance of collaborative robots that can handle mixed-SKU loads without mechanical tooling. The shift toward omni-channel fulfillment in metropolitan hubs places a premium on pallet integrity and sequencing, driving adoption of camera-guided pattern-building software and automatic stretch-film tension control. Suppliers can package palletiser cells with connected case conveyance, print-and-apply labeling, and end-of-line inspection stands to accelerate revenue capture.

Labeling and serialization continue to gain share as traceability mandates expand. Zetes installations deliver single-point aggregation data across multiple GCC pharmaceutical plants, and their middleware now syncs with vision systems to flag print degradation in real-time. Horizontal flow wrappers for bakery and confectionery products are transitioning from pneumatic to servo drives, enhancing speed and minimizing film waste. Bagging lines for rice, pulses, and pet food migrate to fully integrated form-fill-seal units with automatic weight correction. Whether upgrading an existing filler or specifying a new palletiser, buyers increasingly evaluate energy consumption, water usage, and predictive maintenance capability, supporting the long-term health of the Middle East and Africa packaging automation market.

By End-user Industry: Pharmaceuticals Outpace Food Processors

Food processors remained the largest buyer group in 2025 at 24.39%, reflecting the sector’s scale and its need to comply with Hazard Analysis and Critical Control Points documentation. Their projects often combine hygienic design, dry-clean-in-place modules, and continuous inspection to satisfy retail audit protocols. Pharmaceutical companies are projected to expand at an 8.79% CAGR through 2031, propelled by Gulf government investments in fill-finish plants that require aseptic environments, tiny dosing accuracy, and 100% visual inspection. OZON Pharmaceuticals, Acino, and Julphar projects demonstrate how injectable capacity is moving closer to regional patient populations, resulting in higher automation budgets per square meter of cleanroom area.

Beverage producers continue to push the speed frontier, drawing on integrated stretch-blow-mold, fill, and cap blocks that minimize footprint and cut changeover time. Cosmetics and personal-care brands adopt small-lot filling lines equipped with robots that automatically swap nozzles and grippers, catering to the high volume of promotional packs typical of the beauty market. Chemical and household product packagers prioritize explosion-proof drives and torque-monitored capping heads, striking a balance between safety compliance and high availability. Contract logistics providers serve multiple sectors, purchasing flexible secondary packaging cells that integrate with warehouse management systems to minimize downtime between client campaigns.

Geography Analysis

Saudi Arabia anchors regional revenue with 24.18% of 2025 sales, underpinned by Vision 2030 industrial programs that reward local manufacturing and import substitution. Krones’ multi-line supply to Alesayi Beverage, including PET, can, and glass formats, exemplifies the Kingdom’s preference for high-speed, integrated solutions. The United Arab Emirates follows closely, leveraging world-class logistics, export-friendly free zones, and flagship projects such as Pure Ice Cream’s AED 80 million (USD 21.8 million) automated plant, which aims to achieve an annual output of 50 million liters. South Africa is forecast to grow at 8.19% due to energy-efficient retrofits in the food and chemical industries, as well as the diversification of contract packaging services across Gauteng and KwaZulu-Natal.

Turkey’s role as a hub for machinery manufacturing extends across the region. Korteks’ digital yarn packaging upgrade achieved an ROI in under three years, showcasing the exportable benefits of Turkish automation expertise. Egypt hosts more than 17,000 food manufacturers and attracts continuous foreign direct investment, including Symrise’s 30,000-square-meter consolidated flavors facility designed to double volumes for African and Middle Eastern customers. Nigeria appeals to machinery vendors with the continent’s second-largest food and packaging technology spend in 2023 and recent rollouts of SACMI filling and capping lines in Lagos.

Algeria, Qatar, Kuwait, and Bahrain are pursuing food-security strategies that involve dairy mega-farms and cold-chain upgrades. GEA’s EUR 170 million (USD 192.1 million) contract to build the world’s largest integrated dairy facility in Algeria underscores the scale and complexity of such projects, which include advanced membrane filtration, spray drying, and fully automated powder packaging.[2]“GEA to build integrated Algerian dairy megaproject,” Presseportal, presseportal.de Kenya and Ethiopia remain early-stage adopters; however, donor-backed agro-processing parks and pharmaceutical start-ups, such as Julphar’s Ethiopia plant, signal a widening geographic footprint for the Middle East and Africa packaging automation market.

Competitive Landscape

Global original-equipment manufacturers dominate high-speed primary packaging, yet the overall market remains moderately fragmented. Tetra Pak, Krones, GEA, Siemens, and Schneider Electric command the lion’s share of turnkey bids because they combine hardware, process utilities, and digital-twin analytics in one commercial envelope. Tetra Pak’s three-year digitalization pact with Al Rabie integrates Internet of Things sensors, predictive maintenance, and water-reduction algorithms into a brownfield dairy plant, highlighting the value buyers place on full-life-cycle service.[3]“Tetra Pak inks three-year digitalization deal with Al Rabie,” Gulf Industry Online, gulfindustryonline.com Siemens and Schneider Electric monetize their installed power-distribution base by layering manufacturing execution systems and energy dashboards that optimize line efficiency and utility cost.

Turkish builders, including Atara, and regional integrators provide cost-effective solutions to small and mid-sized processors, particularly for secondary packaging. Their local presence and shorter lead times offset the technical edge enjoyed by multinational peers. The rise of vendor-agnostic machine control software and standardized industrial Ethernet protocols is lowering switching costs, intensifying price competition in the Middle East and Africa packaging automation market. Differentiation increasingly hinges on digital services, as vendors demonstrating quantifiable uptime gains through cloud-based condition monitoring are securing multi-line retrofits in Egypt and South Africa.

Mergers, distribution partnerships, and joint innovation centers will shape future consolidation. Larger OEMs are eyeing bolt-on acquisitions that extend their vertical reach into automation peripherals, such as autonomous mobile robots and machine-vision firms. Regional distributors focus on after-sales contracts to deepen recurring revenue and protect installed bases. Collectively, these strategies will nudge market concentration higher, although the top five players still account for well under 60% of total shipments, preserving room for specialist challengers.

Middle East And Africa Packaging Automation Industry Leaders

ABB Ltd.

Mitsubishi Electric Corporation

Rockwell Automation, Inc.

Schneider Electric SE

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Krones commissioned a high-speed PET water line and a canning line for Mai Dubai in the United Arab Emirates, integrating a Hydronomic water treatment system and digital line-management modules.

- July 2025: GEA Group secured a EUR 140-170 million contract with Baladna and the Algerian government to build the world’s largest integrated dairy farm and milk-powder facility in Adrar province, Algeria.

- May 2025: Schneider Electric and Abu Dhabi Investment Office formed a partnership to accelerate digitalization and workforce upskilling in Abu Dhabi’s industrial sector.

- May 2025: TECOM Group broke ground on Pure Ice Cream’s AED 80 million automated frozen-dessert plant at Dubai Industrial City, scheduled for completion in 2026.

Middle East And Africa Packaging Automation Market Report Scope

The Middle East and Africa packaging automation market refers to the regional industry segment focused on the development, supply, and integration of automated machinery and systems that streamline packaging processes. These solutions include robotic case packers, palletizers, automated filling and sealing machines, and integrated control systems designed to reduce manual intervention and enhance productivity.

The Middle East and Africa Packaging Automation Market Report is Segmented by Business Type (B2B E-Commerce Retailers, B2C E-Commerce Retailers, Omni-Channel Retailers, Wholesale Distributors, and Manufacturers), Product Type (Filling, Labelling, Horizontal/Vertical Pillow, Case Packaging, Bagging, Palletising, Capping, and Wrapping), End-user Industry (Food, Pharmaceuticals, Cosmetics, Household, Beverages, Chemicals, Logistics, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Business Type

| B2B E-Commerce Retailers |

| B2C E-Commerce Retailers |

| Omni-Channel Retailers |

| Wholesale Distributors |

| Manufacturers |

By End-user Industry

| Food |

| Pharmaceuticals |

| Cosmetics |

| Household |

| Beverages |

| Chemicals |

| Logistics |

| Other End-user Industries |

By Product Type

| Filling |

| Labelling |

| Horizontal / Vertical Pillow |

| Case Packaging |

| Bagging |

| Palletising |

| Capping |

| Wrapping |

By Region

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Business Type | B2B E-Commerce Retailers | |

| B2C E-Commerce Retailers | ||

| Omni-Channel Retailers | ||

| Wholesale Distributors | ||

| Manufacturers | ||

| By End-user Industry | Food | |

| Pharmaceuticals | ||

| Cosmetics | ||

| Household | ||

| Beverages | ||

| Chemicals | ||

| Logistics | ||

| Other End-user Industries | ||

| By Product Type | Filling | |

| Labelling | ||

| Horizontal / Vertical Pillow | ||

| Case Packaging | ||

| Bagging | ||

| Palletising | ||

| Capping | ||

| Wrapping | ||

| By Region | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Middle East and Africa packaging automation market?

The market is valued at USD 3.89 billion in 2026.

How fast is demand projected to grow?

Revenue is forecast to rise at a 6.42% CAGR from 2026 to 2031, reaching USD 5.31 billion.

Which business type will expand the quickest through 2031?

Omni-channel retailers are expected to post the fastest growth, at an 8.17% CAGR.

Why are palletising systems outpacing filling equipment in growth?

Warehouse throughput pressures and the need to build mixed-SKU pallets without mechanical changeovers drive an 8.57% CAGR for palletizers.

Which end-user segment shows the highest CAGR?

Pharmaceutical manufacturers lead with an anticipated 8.79% CAGR owing to heavy investment in fill-finish lines and serialization.

Which country represents the largest share of regional revenue?

Saudi Arabia holds 24.18% of 2025 sales and remains the single largest national market.

Page last updated on: