Agrochemical Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.56 Billion |

| Market Size (2031) | USD 4.83 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Agrochemical Additives Market Analysis by Mordor Intelligence

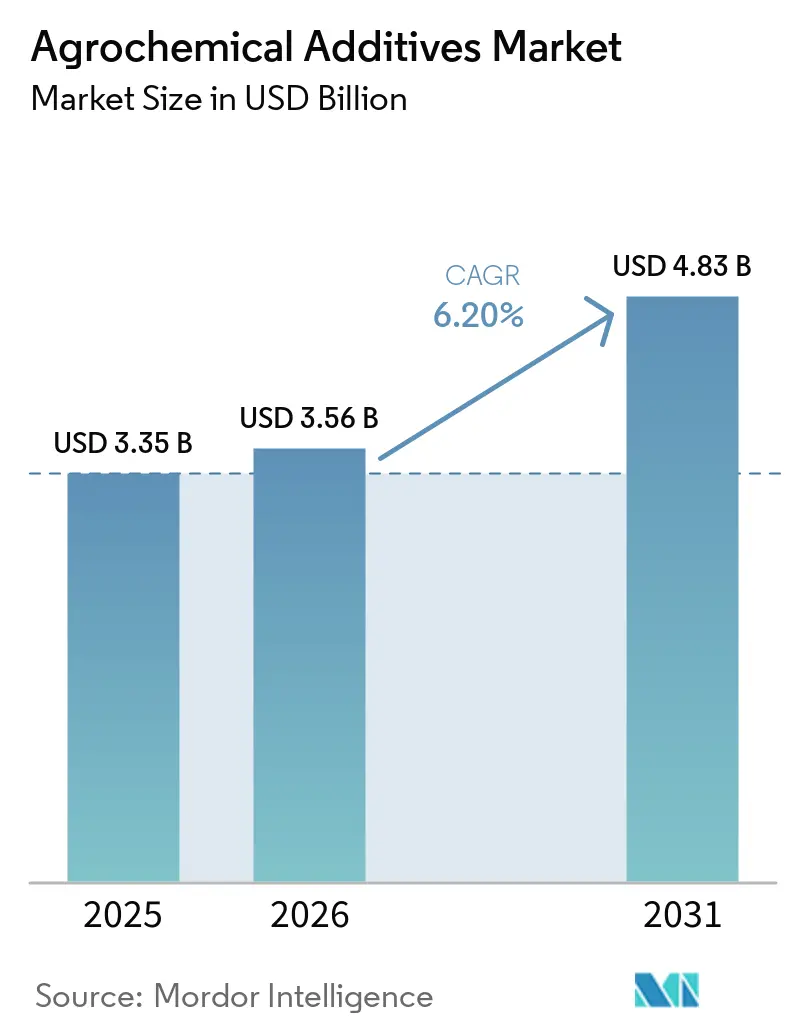

The agrochemical additives market size is projected to grow from USD 3.35 billion in 2025 to USD 3.56 billion in 2026 and is projected to reach USD 4.83 billion by 2031, registering a CAGR of 6.2% during 2026-2031. Current innovations focus on drone-compatible, low-viscosity liquid adjuvants designed to prevent nozzle clogs and reduce spray volumes. Stricter spray-drift regulations in key export markets are driving demand for polymer drift-control agents, which increase the median droplet size, meeting the United States Environmental Protection Agency's drift-reduction standards. Additionally, carbon-credit programs offering growers incentives for using nitrification inhibitors are lowering adoption costs and integrating additives into fertilizer applications. However, suppliers are facing challenges from feedstock price volatility. For instance, ethylene oxide prices surged due to outages at two global production facilities, squeezing margins for surfactant manufacturers reliant on spot contracts.

Key Report Takeaways

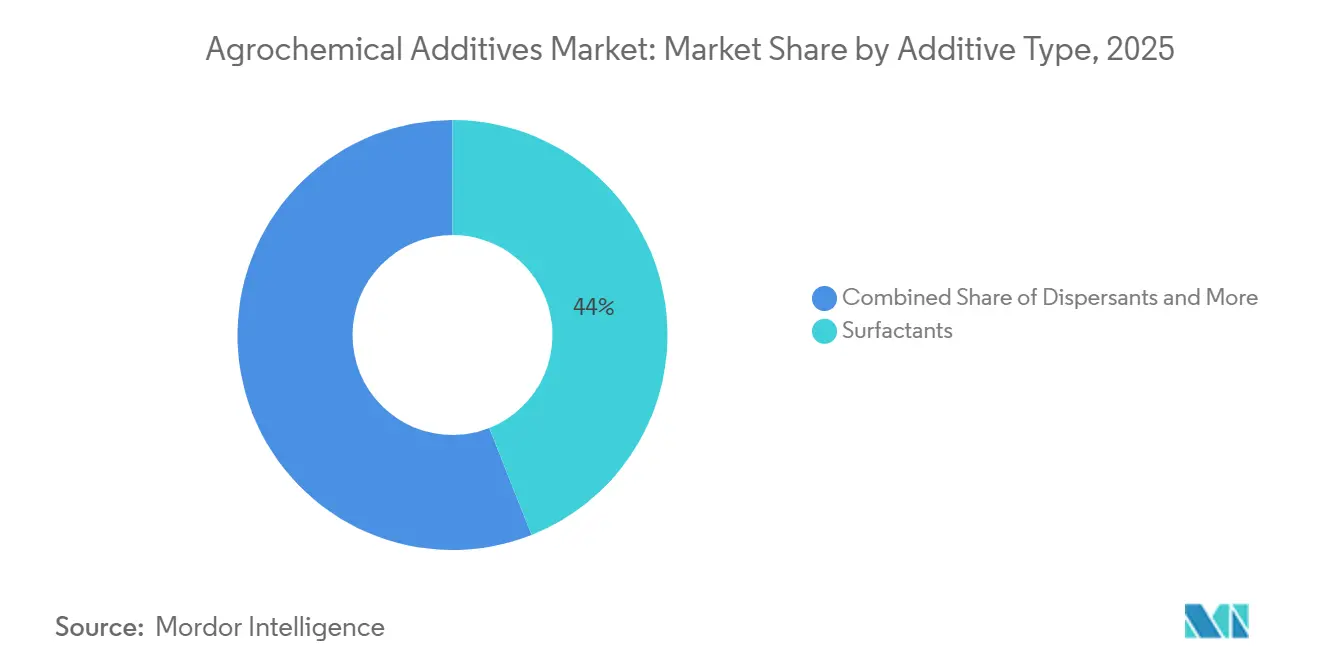

By additive type, the agrochemical additives market share for the surfactants segment held the largest 44% in 2025, while the agrochemical additives market size for the drift control agents segment is projected to grow at the fastest 9.5% CAGR from 2026 to 2031.

By form, liquid formulation accounted for the largest 61% share of the agrochemical additives market in 2025, and the liquid segment is projected to expand at the fastest 6.8% CAGR from 2026 to 2031.

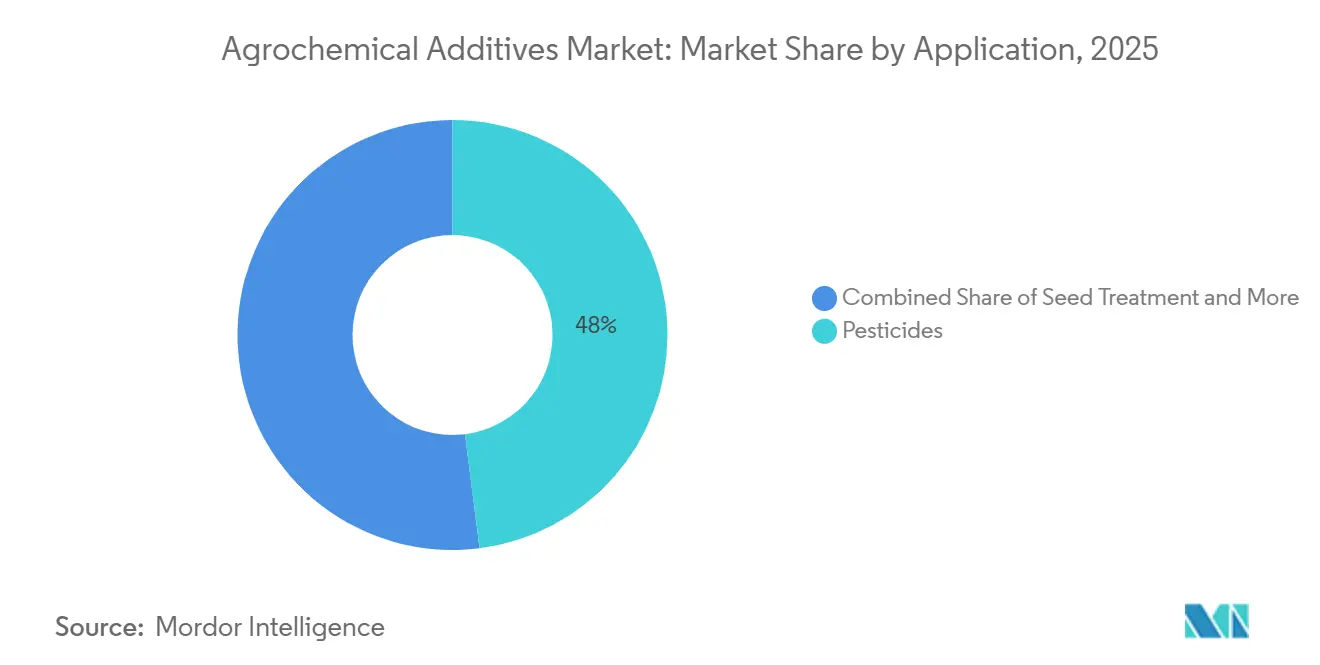

By application, pesticides accounted for the largest 48% share of the agrochemical additives market in 2025, while the seed treatment market is projected to grow at the fastest 8.7% CAGR from 2026 to 2031.

By crop type, cereals and grains captured the largest 37% share of the agrochemical additives market in 2025, whereas the fruits and vegetables segment is projected to grow at the fastest 7.5% CAGR from 2026 to 2031.

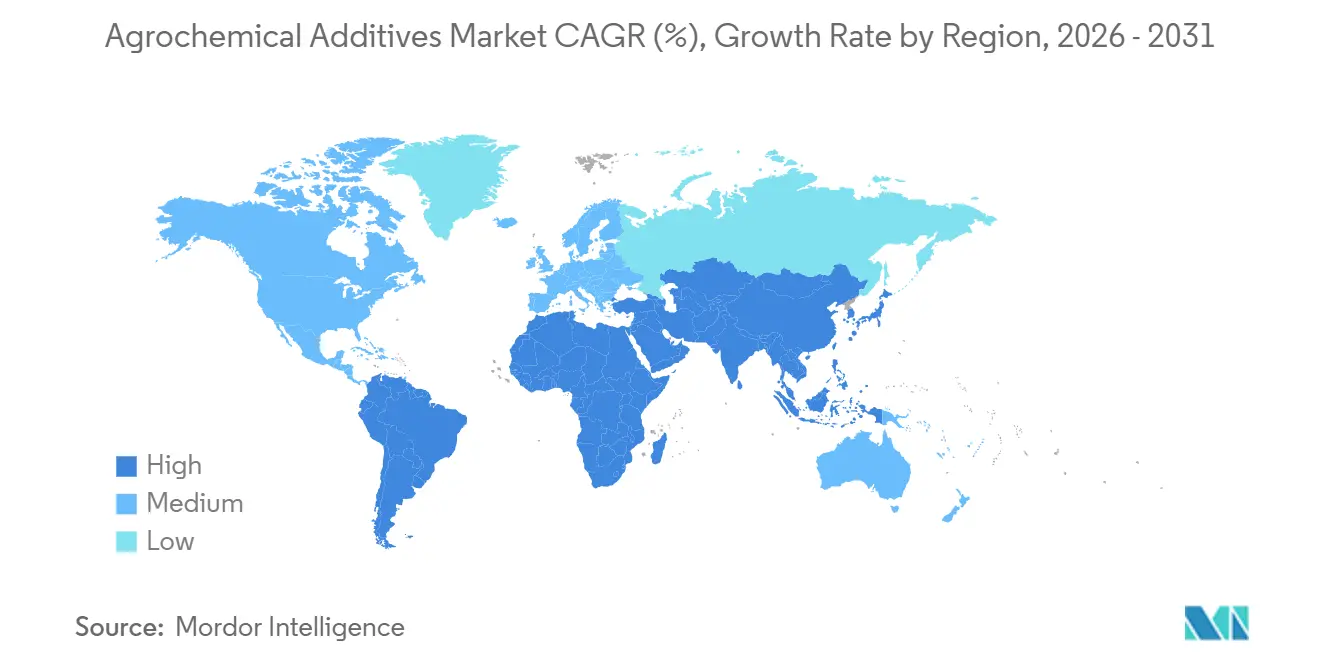

By geography, Asia-Pacific commanded the largest 34% revenue share in 2025, while the Africa market is forecasted to grow at the fastest 7.8% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agrochemical Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for higher crop yield intensification | +1.2% | Global with peak intensity in Asia-Pacific and South America | Medium term (2–4 years) |

| Rapid uptake of precision spraying and nano-formulations | +1.0% | North America and Europe, spillover to Brazil and Australia | Short term (≤ 2 years) |

| Government subsidy shift toward adjuvant-optimized formulations | +0.9% | Asia-Pacific, Africa, and South America | Medium term (2–4 years) |

| Expansion of glyphosate-tolerant crops needing adjuvant compatibility | +0.8% | South America and North America | Long term (≥ 4 years) |

| Rising drone-based foliar application requiring low-viscosity additives | +0.7% | China, Japan, Australia, and emerging in Africa | Short term (≤ 2 years) |

| Carbon-credit monetization for fertilizer reduction via additives | +0.6% | North America and Europe, pilots in South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Higher Crop Yield Intensification

The increasing demand for higher crop yield intensification is highlighted by data from the Food and Agriculture Organization (FAO), which reports that global cereal production rose from 2,849 million metric tons in 2024 to 2,911 million metric tons in 2025, representing a 2.1% year-on-year increase[1]Source: Food and Agriculture Organization, "Food Outlook Report, 2025", openknowledge.fao.org. This growth is primarily attributed to improved yields rather than the expansion of cultivated land, reflecting a focus on efficiency-driven farming practices. These productivity improvements rely on precision agriculture and optimized input usage, where agrochemical additives play a critical role in enhancing pesticide effectiveness, nutrient absorption, and spray efficiency. This trend is contributing to rising demand in the agrochemical additives market.

Rapid Uptake of Precision Spraying and Nano-Formulations

Precision spraying technologies are experiencing significant adoption due to their capability to improve application accuracy and operational efficiency. Researchers from the Indian Institute of Information Technology, Allahabad, reported that UAV-based spraying systems achieved up to 95% spray coverage efficiency while reducing drift by nearly 80% as of 2025, emphasizing the advantages of targeted application methods. This level of performance necessitates formulations with optimized viscosity, stability, and spray characteristics, thereby increasing the demand for advanced additives and nano-formulations. Additionally, the expanding use of drone-based spraying is driving the need for precision-grade formulation technologies that are compatible with modern agricultural equipment.

Government Subsidy Shift Toward Adjuvant-Optimized Formulations

Government policies are increasingly promoting the use of optimized formulations through subsidies, tax benefits, and regulatory incentives, emphasizing the importance of performance-enhancing inputs in modern agriculture. In 2025, the Government of Kenya introduced a 16% value-added tax on agrochemicals while exempting certified adjuvants, thereby enhancing the price competitiveness of compliant additive products. Financial support programs and regulatory frameworks are increasingly tied to the use of registered and environmentally compliant solutions, indirectly encouraging the adoption of compatible additives in spray applications. Simultaneously, stricter environmental regulations and residue limits are driving demand for formulations that enhance efficiency and minimize chemical losses, accelerating the global adoption of advanced agrochemical additive solutions.

Expansion of Glyphosate-Tolerant Crops Needing Adjuvant Compatibility

According to the United States Department of Agriculture (USDA), herbicide-tolerant soybeans dominated the United States soybean landscape, claiming 96% of the acreage in both 2024 and 2025[2]Source: United States Department of Agriculture, "Adoption of Genetically Engineered Crops in the United States – Recent Trends, 2025", ers.usda.gov. This overwhelming adoption underscores the heavy reliance on glyphosate and stacked herbicide programs to tackle resistant weeds. Consequently, there's a growing trend of mixing tank applications with multiple actives, including dicamba and 2,4-D. These combinations necessitate the use of compatible additives to manage pH levels, curb volatility, and boost spray efficacy. Such developments highlight the significance of formulation strategies centered on compatibility, granting suppliers with validated additive systems a notable edge in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory scrutiny on ethoxylated nonylphenols | -0.8% | Europe and North America, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Volatility in ethylene oxide and alcohol-ethoxylate feedstock costs | -0.7% | Global, with acute effect in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Farmer reluctance toward premium bio-based adjuvants | -0.5% | Global, strongest in South America and Africa | Medium term (2–4 years) |

| Ag-chem distributor consolidation squeezing additive margins | -0.4% | North America and Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Scrutiny on Ethoxylated Nonylphenols

Regulatory bodies are tightening their grip on ethoxylated nonylphenols, given their prevalent environmental footprint and the health hazards they pose. In a 2025 investigation, Toxics Link uncovered nonylphenol ethoxylates in 15 of the 40 products tested. Concentrations peaked at 957 mg/kg in products and reached 70 µg/L in river water, underscoring the severity of contamination. Such revelations amplify worries about endocrine disruption and the compounds' longevity in the environment, leading to heightened regulatory vigilance. Consequently, manufacturers are pivoting towards safer product formulations. This shift increases compliance costs, lengthens approval timelines, and restrains market growth.

Volatility in Ethylene Oxide and Alcohol-Ethoxylate Feedstock Costs

Feedstock cost volatility continues to impact profitability across the agrochemical additives value chain. Ethylene oxide and alcohol ethoxylates are closely tied to petrochemical supply dynamics, making them sensitive to production disruptions and energy price fluctuations. This instability reduces margin predictability and complicates procurement strategies for manufacturers. Companies are increasingly adopting flexible pricing mechanisms to manage cost fluctuations, but this often strains distributor relationships and encourages substitution toward lower-cost alternatives. As a result, uncertain input costs limit investment confidence and slow capacity expansion across the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Surfactants Dominate, Drift Control Accelerates

The surfactants segment held the largest 44% share of the agrochemical additives market in 2025, maintaining its dominance due to its critical role in enhancing spray coverage and ensuring formulation stability in pesticide applications. Their widespread use in emulsifiable concentrates and suspension systems supports consistent demand in major agricultural regions. With a regulatory focus on spray efficiency and environmental safety, the importance of drift-control agents has increased. The growing adoption of precision spraying technologies has further boosted the demand for functional additives that improve droplet control, emphasizing the role of performance-oriented chemistries in modern formulation strategies.

The drift control agents segment is projected to grow at the fastest CAGR of 9.5% during 2026-2031, driven by stricter regulatory requirements to minimize spray drift and enhance application accuracy. The rapid adoption of advanced spraying technologies, including drones and precision tools, is fueling demand for viscosity-modifying polymers. These polymers not only ensure effectiveness but also meet stringent environmental standards. Furthermore, sustainability trends are fostering innovation in biodegradable and eco-friendly additives. This shift toward specialized, regulation-compliant solutions is transforming the competitive landscape, favoring high-performance additive systems.

By Form: Liquids Lead and Witness Fastest Growth in Seed Treatment Applications

Liquid formulations accounted for the largest 61% of the agrochemical additives market share in 2025, driven by their rapid dispersion, ease of handling, and compatibility with modern spraying systems. These formulations are the preferred choice in large-scale agricultural operations due to their seamless integration with high-capacity sprayers and precision technologies. Their dominance is further supported by increasing mechanization and the adoption of foliar application methods, where uniform mixing and consistent delivery are essential for optimizing performance in pesticide and nutrient applications.

Liquid formulations are anticipated to maintain the fastest growth trajectory, registering a CAGR of 6.8% during the forecast period 2026-2031, fueled by advancements in precision agriculture and drone-based spraying systems. Meanwhile, solid formulations are gaining popularity in seed treatment and regions sensitive to logistics due to their stability and reduced transportation challenges. Environmental factors, such as packaging reduction and improved shelf life, are also contributing to the gradual adoption of solid formats. However, liquids are projected to maintain their leading position owing to their operational efficiency and compatibility with evolving agricultural technologies.

By Application: Pesticides Prevail, Seed Treatment Gains Momentum

Pesticides accounted for the largest 48% of the agrochemical additives market in 2025, driven by their essential role in crop protection and yield enhancement. The increasing complexity of pest management strategies, including the use of combined herbicide and fungicide applications, is boosting demand for additives that improve efficacy and stability. Farmers are increasingly relying on advanced formulations to achieve better coverage, minimize volatilization, and optimize performance under diverse field conditions. This continued dependence on crop protection solutions remains a key factor sustaining demand in this application segment.

Seed treatment is anticipated to grow at the fastest CAGR of 8.7% from 2026 to 2031, driven by advancements in coating technologies and targeted input delivery systems. The adoption of film-forming polymers and encapsulation techniques is enhancing seed protection while reducing chemical usage. These innovations are gaining popularity as farmers prioritize cost-effective and sustainable solutions that support improved germination and early plant development. With input optimization becoming increasingly important, seed-based applications are emerging as a significant growth area within agricultural input systems.

By Crop Type: Cereals Lead, High-Value Horticulture Accelerates

Cereals and grains accounted for the largest 37% of the agrochemical additives market in 2025, driven by their extensive global cultivation and consistent demand for agricultural inputs. The large-scale production of staple crops such as wheat, rice, and corn necessitates efficient crop protection and nutrient management solutions. Additives are critical in enhancing spray performance and optimizing input utilization, thereby supporting productivity in high-acreage farming systems. This broad application base ensures steady demand from cereal-focused agricultural economies.

Fruits and vegetables are projected to grow at the fastest CAGR of 7.5% from 2026 to 2031, fueled by rising demand for high-value crops and stricter quality standards. Growers are increasingly adopting advanced formulations that improve spray retention and minimize the need for reapplication. The higher profit margins in horticulture facilitate the adoption of premium solutions, such as rainfastness and anti-transpirant additives. This trend toward value-driven agriculture is fostering innovation and the adoption of specialized input solutions within this segment.

Geography Analysis

Asia-Pacific held the largest 34% agrochemical additives market share in 2025, supported by rapid agricultural modernization and the widespread adoption of precision technologies. Countries such as China and India are advancing mechanized farming and promoting efficient input utilization through policy support and technology integration. The region's extensive cultivation base and growing emphasis on productivity enhancement are sustaining demand for performance-focused solutions. Additionally, the expansion of local manufacturing and government-supported initiatives is bolstering regional supply chains and facilitating the adoption of advanced agricultural practices.

Africa market size is projected to grow at the fastest 7.8% CAGR from 2026 to 2031, driven by increasing investments in agricultural productivity and improved access to farming inputs. Financial inclusion programs and subsidy-linked initiatives are enhancing the adoption of modern farming inputs among smallholder communities. Furthermore, rising awareness of efficient input usage and crop protection is driving demand. Meanwhile, South America continues to exhibit strong growth potential, supported by large-scale commercial farming and the growing adoption of advanced crop management techniques.

North America holds a prominent position due to its high level of technological adoption and well-structured agricultural systems. According to the United States Department of Agriculture (USDA), the total cropland used for crops in the United States was 328 million acres in 2024, highlighting the scale of intensive farming and consistent input utilization[3]Source: United States Department of Agriculture (USDA), "Economic Research Service – Chart of Note: Cropland for crops in 2024, 2025", ers.usda.gov . This extensive cultivation base drives steady demand for crop protection solutions reliant on performance-enhancing formulations. Europe remains a regulated but innovation-focused market, while the Middle East exhibits gradual growth, supported by water-efficiency initiatives and controlled-environment agriculture.

Competitive Landscape

The market is moderately consolidated, with the top five players including BASF SE, Evonik Industries AG, Croda International Plc, Dow Inc., and Syensqo SA. Portfolio strategies are now divided into two main approaches. Large incumbents are increasing alkoxylation and dispersant capacity while sourcing certified low-carbon ethylene oxide to meet government tender requirements that prioritize verified greenhouse gas reductions. Meanwhile, specialty suppliers are focusing on high-margin niches, including drone-compatible drift agents and biodegradable seed-coating polymers that comply with European Union eco-label regulations.

The market is projected to witness rising competitive intensity driven by pricing pressures and distribution consolidation, resulting in varied growth paths for different players. Large distributors are increasing their bargaining power, leading to price negotiations and margin reductions for mid-sized suppliers. The expansion of private-label products is further heightening competition, shifting demand toward cost-efficient manufacturers capable of fulfilling bulk supply needs. In response, companies are prioritizing operational efficiency, forming strategic partnerships, and offering value-added products to remain competitive in a price-sensitive and volume-driven market.

Competition is increasingly influenced by sustainability and innovation standards. According to the United States Environmental Protection Agency, stricter regulations on chemical inputs are encouraging a shift toward safer and environmentally compliant formulations. Companies investing in biodegradable chemistries, low-emission feedstocks, and advanced formulation technologies are gaining an advantage in procurement programs. Simultaneously, capacity expansions and research investments are enabling suppliers to meet evolving regulatory requirements while addressing performance demands, making innovation and environmental compliance critical for long-term competitive positioning.

Agrochemical Additives Industry Leaders

-

BASF SE

-

Evonik Industries AG

-

Croda International Plc

-

Dow Inc.

-

Syensqo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BASF SE has commissioned a new Controlled Free Radical Polymerization (CFRP) dispersant production line in China to enhance its agrochemical additives portfolio. This expansion addresses the growing demand for advanced dispersants that enhance formulation stability and performance in agrochemical applications.

- August 2025: BASF SE has expanded its VALERAS platform with the introduction of Tinuvin NOR, an advanced hindered amine light stabilizer (HALS) solution for agricultural films. This product is designed to enhance resistance to agrochemicals, UV radiation, heat stress, and adverse weather conditions.

- June 2025: Stepan Company increased its alpha-olefin sulfonate production capacity by 25% at its manufacturing facilities in the United States, enhancing the supply of surfactant chemistries commonly used in agricultural formulations and crop protection products.

Global Agrochemical Additives Market Report Scope

Agrochemical additives are functional components incorporated into pesticides, fertilizers, and other crop inputs to enhance their performance, stability, and application efficiency. These additives improve characteristics such as spreading, adhesion, penetration, and compatibility, enabling farmers to achieve more effective crop protection and nutrient utilization. The agrochemical additives market report is segmented by additive type (surfactants, dispersants, emulsifiers, antifoaming agents, drift control agents, and other additives), by form (liquid and solid), by application (pesticides, fertilizers, seed treatment, and soil conditioners), by crop type (cereals and grains, fruits and vegetables, oilseeds and pulses, and other crops), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Surfactants |

| Dispersants |

| Emulsifiers |

| Antifoaming Agents |

| Drift Control Agents |

| Others |

| Liquid |

| Solid |

| Pesticides |

| Fertilizers |

| Seed Treatment |

| Soil Conditioners |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Additive Type | Surfactants | |

| Dispersants | ||

| Emulsifiers | ||

| Antifoaming Agents | ||

| Drift Control Agents | ||

| Others | ||

| By Form | Liquid | |

| Solid | ||

| By Application | Pesticides | |

| Fertilizers | ||

| Seed Treatment | ||

| Soil Conditioners | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the estimated value of the agrochemical additives market in 2026?

The agrochemical additives market size is estimated at USD 3.56 billion in 2026 and is projected to reach USD 4.83 billion by 2031, growing at a CAGR of 6.2% during 2026-2031.

Which additive type holds the largest share?

Surfactants led with the largest 44.0% of agrochemical additives market share in 2025.

Which segment is growing fastest?

Drift control agents are forecast to expand at the fastest 9.5% CAGR from 2026 to 2031.

Which region will see the highest growth?

Africa is poised to grow at the fastest 7.8% CAGR from 2026 to 2031.

Page last updated on: