Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.3 Billion |

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 2.88 Billion |

| Growth Rate (2026 - 2031) | 3.80% CAGR |

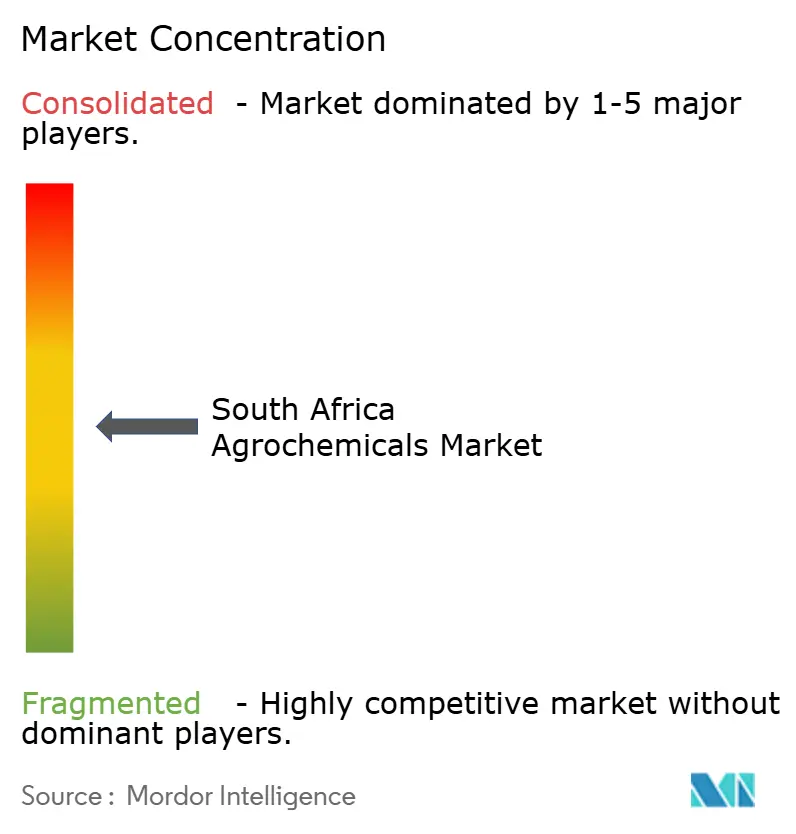

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Agrochemicals Market Analysis by Mordor Intelligence

The South Africa agrochemicals market size is expected to grow from USD 2.3 billion in 2025 to USD 2.39 billion in 2026 and is forecast to reach USD 2.88 billion by 2031 at 3.8% CAGR over 2026-2031. The market growth is driven by fertilizer subsidies, commercial farm modernization, and increased adoption of precision agriculture technologies, despite high raw material costs. The government's Agriculture and Agro-processing Master Plan encourages private investment in value-addition facilities and innovation centers.[3]Agroberichten Buitenland, “South Africa’s New Minister of Agriculture Commits to Building on Success,” agroberichtenbuitenland.nl Companies are establishing local blending and formulation facilities to strengthen supply chains and reduce exposure to currency fluctuations on imported inputs. Industry consolidation, such as Omnia's acquisition of Oro Agri, reflects a shift toward environmentally sustainable products, helping suppliers meet stricter residue regulations and export standards.

Key Report Takeaways

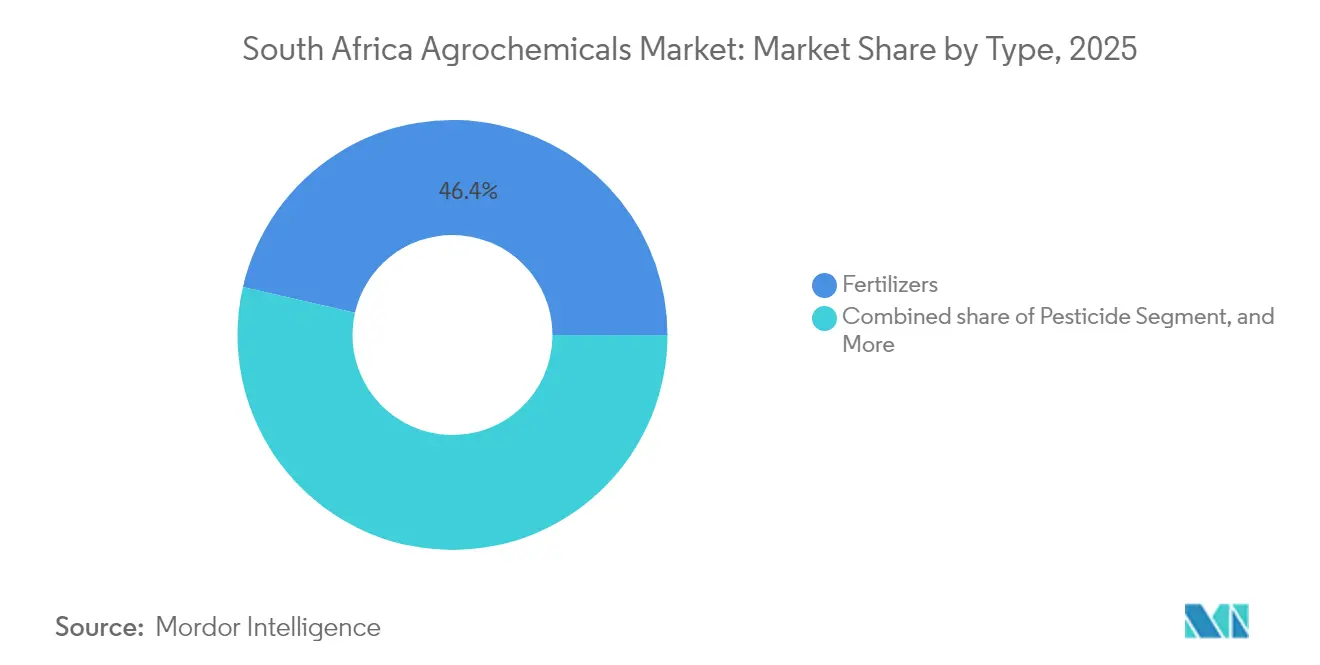

- By type, fertilizers led with 46.42% of South Africa agrochemicals market share in 2025, while adjuvants are rising the fastest at a 6.1% CAGR through 2031.

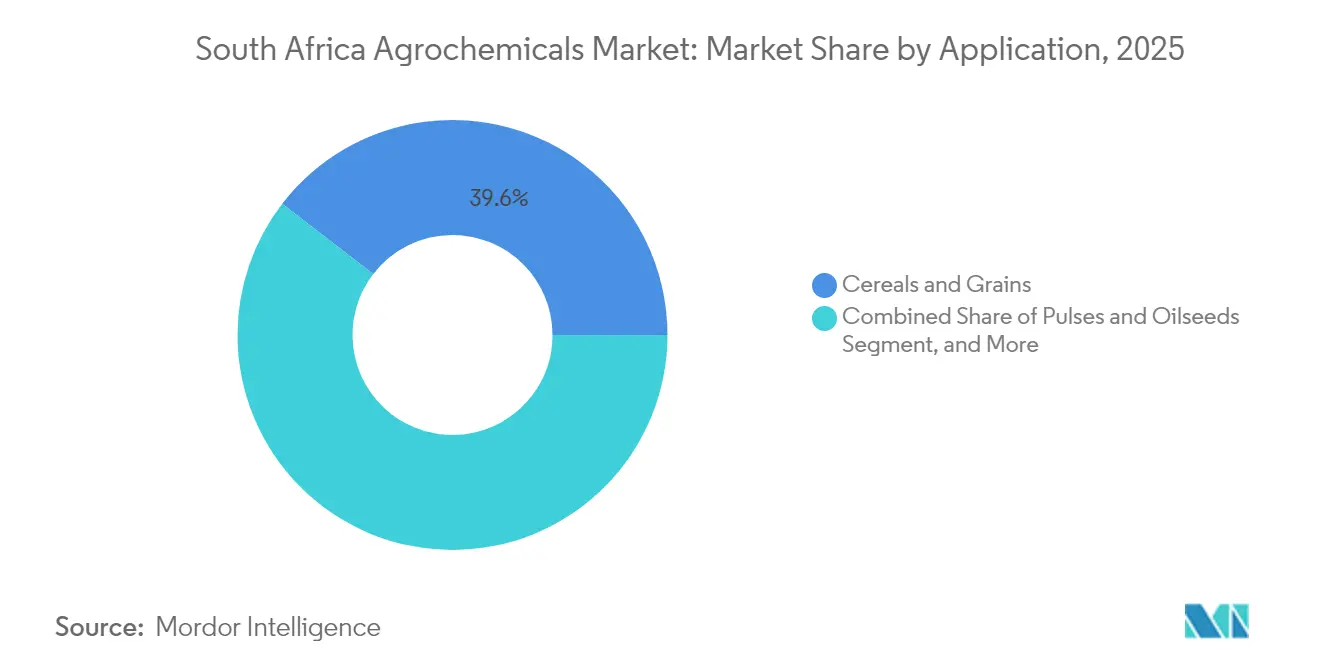

- By application, grains and cereals held 39.55% revenue share of the South Africa agrochemicals market size in 2025, and fruits and vegetables are projected to grow at a 5.45% CAGR to 2031.

- Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, and Omnia Group Limited collectively controlled nearly half of South Africa's agrochemicals market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Fertilizer Purchase Subsidies | +1.2% | National, focused on smallholder farmers | Medium term (2-4 years) |

| Expansion of Controlled Release Fertilizer Technologies | +0.8% | Western Cape, KwaZulu-Natal commercial farms | Long term (≥ 4 years) |

| Expansion of Commercial Farming Operations | +1.0% | Free State, Mpumalanga, Limpopo | Medium term (2-4 years) |

| Increasing Crop Disease Pressure from Climate Variability | +0.9% | National, Eastern Cape smallholders | Short term (≤ 2 years) |

| Rising Adoption of Drone Based Precision Spraying | +0.6% | Western Cape, Northern Cape commercial farms | Long term (≥ 4 years) |

| Rising Use of Plant-Growth Regulators to Maximize Fruit Set and Uniform Ripening | +0.4% | Western Cape fruit regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Fertilizer Purchase Subsidies

South Africa's fertilizer subsidy program supports small-scale growers by reducing input costs and maintaining consistent nutrient application.[1]South African Government, “Highlights of the State of the Nation Address 2022 – Agriculture,” gov.za Diesel refunds provide relief for commercial producers, though administrative requirements limit access for smaller farms. The government's outreach efforts aim to improve subsidy distribution equity across rural communities. Regulatory oversight under agricultural legislation maintains product quality and prevents counterfeit fertilizer circulation. While subsidy voucher conversion rates vary by province, these programs contribute to food security and rural livelihoods. Extension services remain essential for farmers to access and utilize these benefits.

Expansion of Controlled Release Fertilizer Technologies

Farmers are adopting controlled-release fertilizers to match nutrient availability with crop demand, reducing environmental impact and improving water efficiency. Distribution networks in major agricultural hubs facilitate access to these formulations, particularly in grain-producing regions. Trials in regenerative farming systems demonstrate improved yields with reduced synthetic inputs. Export-oriented fruit estates increasingly use these technologies to achieve uniform ripening and visual quality for international markets. Controlled-release products decrease fertilizer application frequency, reducing labor and fuel costs, while supporting climate-smart agriculture and soil conservation.

Expansion of Commercial Farming Operations

Mechanization and digital agriculture tools increase planted area and productivity across key provinces. Smallholders achieve labor efficiency gains, allowing more time for precision monitoring and crop management. Financial platforms offering integrated services, including climate analytics and input financing, help farmers manage drought and energy-related risks. Despite rising technology adoption, equipment costs, and skilled labor shortages persist, creating opportunities for leasing and training programs. Agribusiness-cooperative partnerships help reduce technology gaps, while rural infrastructure improvements support continued growth.

Increasing Crop Disease Pressure from Climate Variability

Climate variability increases pest and disease pressure across South African farms. Warmer conditions expand invasive species distribution, including aphids and fall armyworm, increasing pesticide use in maize cultivation. While warmer seasons can increase grain production, they elevate input costs, particularly for crop protection. Balanced nutrient management remains critical for yield stability under drought conditions. Smallholders face greater challenges due to limited access to crop insurance and monitoring services. Integrated pest management approaches help reduce chemical dependence, while research institutions and farmer networks distribute early warning data and adaptation strategies.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -1.1% | National, high import exposure provinces | Short term (≤ 2 years) |

| Stricter MRL Regulations on Synthetics | -0.7% | Export-oriented Western Cape fruit zone | Medium term (2-4 years) |

| Shift Toward Regenerative, Low Input Farming | -0.6% | Durban and Cape Town corridors | Short term (≤ 2 years) |

| Export Restrictions on Key Fertilizer Ingredients | -0.5% | Eastern Cape and KwaZulu-Natal smallholders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility

Fertilizer price volatility affects the agricultural sector by increasing working capital requirements and complicating input planning. Large-scale producers manage these challenges through early procurement and local blending initiatives. Small-scale farmers often respond by reducing application rates or using lower-quality inputs, which reduces crop yields and soil fertility. Global supply chain disruptions, geopolitical conflicts, and export restrictions intensify these challenges. Currency fluctuations and energy costs increase input price unpredictability, potentially leading to delayed planting decisions and reduced investment in productivity-enhancing technologies.

Stricter MRL Regulations on Synthetics

The implementation of stringent maximum residue level (MRL) regulations affects crop protection practices across the industry. Exporters and processors must modify their spray programs and product formulations to meet these enhanced standards, increasing operational costs. Product labeling and safety documentation requirements create operational challenges, particularly for small-scale distributors. The regulations require increased coordination between manufacturers, retailers, and compliance bodies. Non-compliance with new standards risks market access, especially for export-oriented producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fertilizers Lead Market Transformation

Fertilizers dominate the South Africa agrochemicals market share, commanding 46.42% of the total share in 2025, primarily due to intensive sugarcane cultivation. The segment's growth is supported by controlled-release formulations that improve nutrient efficiency in water-scarce conditions. Nitrogen pricing volatility influences grower decisions on application timing and rates, while government subsidies help small-scale farmers manage cost variations. The phosphatic fertilizer segment faces supply constraints due to export limitations, while potash remains stable but is subject to transportation risks. Fertilizer manufacturers are incorporating micronutrients into premium blends specifically designed for export-oriented horticultural crops.

Adjuvants are experiencing the fastest growth in the South Africa agrochemicals market, with a projected 6.1% CAGR through 2031. The integration of technology improves nutrient-use efficiency, supporting regenerative farming practices. Large commercial farms use digital soil monitoring systems and variable-rate spreaders to reduce application overlap and optimize input usage. Small-scale farmers access fertilizer spreading services through cooperatives, maintaining consistent fertilizer demand despite stabilizing application rates. Infrastructure investments in inland bulk terminals improve supply reliability and reduce transportation costs, particularly benefiting rural areas affected by currency fluctuations.

By Application: Grains Drive Volume, Fruits and Vegetables Accelerate Growth

Grains and cereals constitute the largest application segment, accounting for 39.55% of the South Africa agrochemicals market size in 2025. Maize production requires balanced fertilizer programs and strategic pesticide applications, with improved technology enabling precise application methods. The adoption of conservation tillage and cover crop systems maintains herbicide demand for managing crop residue while preserving soil quality.

The fruits and vegetables segment is growing at a 5.45% CAGR through 2031, supported by strong export prices that justify higher input investments. Western Cape fruit operations depend on plant-growth regulators and specific fungicide programs to meet international market requirements. Growth continues as vineyard and berry farm operations expand, while greenhouse cultivation systems increase local pesticide use intensity. Farmers maintain profitability through data-driven management practices and premium product positioning, despite increasing input expenses.

Geography Analysis

Western Cape, KwaZulu-Natal, and Free State anchor South Africa’s commercial agrochemical demand, each reflecting distinct cropping systems and input strategies. Western Cape leads the market with the largest share, driven by fruit orchards that rely heavily on high-spec inputs and plant-growth regulators. Export protocols shape precise spray schedules, and orchardists increasingly turn to specialty products to manage climatic challenges like insufficient winter chilling.

KwaZulu-Natal blends sugarcane estates with horticultural zones, resulting in strong fertilizer demand and rising adjuvant use, especially for aerial applications. The subtropical climate intensifies fungal disease pressure, prompting widespread use of systemic fungicides. Proximity to Durban’s port and rail infrastructure improves input access, though congestion risks encourage growers to maintain on-farm reserves for uninterrupted operations. Free State dominates maize and wheat production, focusing on bulk fertilizer shipments and herbicide programs that support conservation tillage. While adoption of advanced formulations is slower due to cost sensitivity, cooperative trials show potential for improved nutrient efficiency. Short growing seasons make timely delivery critical, and regional logistics continue to evolve to meet seasonal demand. Inland provinces like Limpopo and Gauteng add diversity, with irrigation-driven citrus and macadamia expansion and intensive peri-urban vegetable farming shaping localized input needs.

Competitive Landscape

The South Africa agrochemicals market remains moderately fragmented, with the five largest players holding nearly a half share in 2024. Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, and Omnia Group Limited collectively control this portion of the market. These companies maintain their positions through diversified portfolios, strategic acquisitions, and strong distribution networks. Their market presence is supported by technical expertise, brand recognition, and integration with commercial farming systems. Investment in local blending facilities and agronomic support strengthens their reach across estate-scale and smallholder operations.

Digital platforms are transforming supplier engagement by simplifying ordering processes and improving advisory services. Local specialists expand operations to provide rapid-response inputs and customized agronomic support. Data analytics and remote diagnostics optimize input usage and minimize waste. The integration of precision agriculture tools into crop management strategies improves operational efficiency and strengthens supplier relationships. These platforms also enable traceability and compliance monitoring, which are essential for export-oriented growers and high-value horticultural producers across key provinces.

Supply chain resilience has become a strategic priority, with companies investing in inland warehousing, on-site formulation, and port logistics to manage market volatility. The complex regulatory environment benefits well-capitalized companies that can effectively navigate compliance requirements. These factors create entry barriers for new players while strengthening established firms' positions. Companies adapt to changing climate conditions and infrastructure limitations by modifying delivery models and regional service offerings. Long-term success depends on operational agility, regulatory understanding, and consistent product availability throughout growing seasons.

South Africa Agrochemicals Industry Leaders

Bayer AG

Syngenta Group

Corteva Agriscience

BASF SE

Omnia Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: Bayer AG launched its new fungicide seed treatment, EverGol Energy, in South Africa, with availability set for farmers in 2024. This treatment targets both Fusarium spp. and Pythium spp. in maize and soybean crops.

- September 2023: Syngenta Group launched a plant growth regulator, "NoMow" for turf professionals in South Africa. The product is the trusted and economical plant growth regulator (PGR) that optimizes mowing effort and turf quality. NoMow can be safely used for up to 12 months of the year, as long as active turf growth occurs.

- July 2023: K+S Aktiengesellschaft acquired a 75% stake in the fertilizer division of Industrial Commodities Holdings (Pty) Ltd (ICH), a trading firm based in South Africa. Following the signing of the agreement, the newly acquired entity will function under the name Fertiva (Pty) Ltd. This strategic move aims to bolster and broaden K+S's distribution reach in South Africa.

South Africa Agrochemicals Market Report Scope

Agrochemicals are commercially produced chemicals or organic compounds used in farming for crop protection and nutrition. The South African agrochemicals market is segmented by type (fertilizers, pesticides, adjuvants, and plant growth regulators) and application (grains and cereals, oilseeds, fruits and vegetables, and other applications (plantation, turf, and ornamentals and grass)). The report offers market sizing in terms of values in USD.

By Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant-Growth Regulators |

By Application

| Grains and Cereals |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Plantation Crops |

| Turf, and Ornamentals |

| By Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant-Growth Regulators | ||

| By Application | Grains and Cereals | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Plantation Crops | ||

| Turf, and Ornamentals | ||

Key Questions Answered in the Report

How large is the South Africa agrochemicals market in 2026?

The market stands at USD 2.39 billion in 2026 and grows toward USD 2.88 billion by 2031 at a 3.8% CAGR.

Which segment accounts for the highest revenue?

Fertilizers lead with 46.42% of total sales to support intensive sugarcane and grain nutrition needs.

Which input type is growing the fastest?

Adjuvants record the fastest growth at a 6.1% CAGR due to precision spraying integration.

How concentrated is supplier competition?

The five largest manufacturers control 46% of sales, pointing to moderate fragmented and room for new entrants.

Page last updated on: