Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 710.50 Million |

| Market Size (2026) | USD 742.83 Million |

| Market Size (2031) | USD 928.07 Million |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Agrochemicals Market Analysis by Mordor Intelligence

The Malaysia agrochemicals market size is expected to grow from USD 710.50 million in 2025 to USD 742.83 million in 2026 and is forecast to reach USD 928.07 million by 2031 at 4.55% CAGR over 2026-2031. Continuing mechanization across 5.74 million hectares of oil palm and 1.07 million hectares of rubber estates sustains year-round chemical demand, while accelerated paddy and horticulture programs amplify seasonal peaks. Rising adoption of precision spraying drones, labor-saving slow-release fertilizers, and innovative pest control solutions broadens supplier opportunities. Budget 2025 raised federal food-security spending to RM4.188 billion (USD 1.01 billion), channeling grants toward smallholder replanting and fertilizer subsidies that directly underpin input purchases. At the same time, tighter residue limits under the Malaysian Sustainable Palm Oil (MSPO) scheme encourage migration toward registered, higher-quality formulations.

Key Report Takeaways

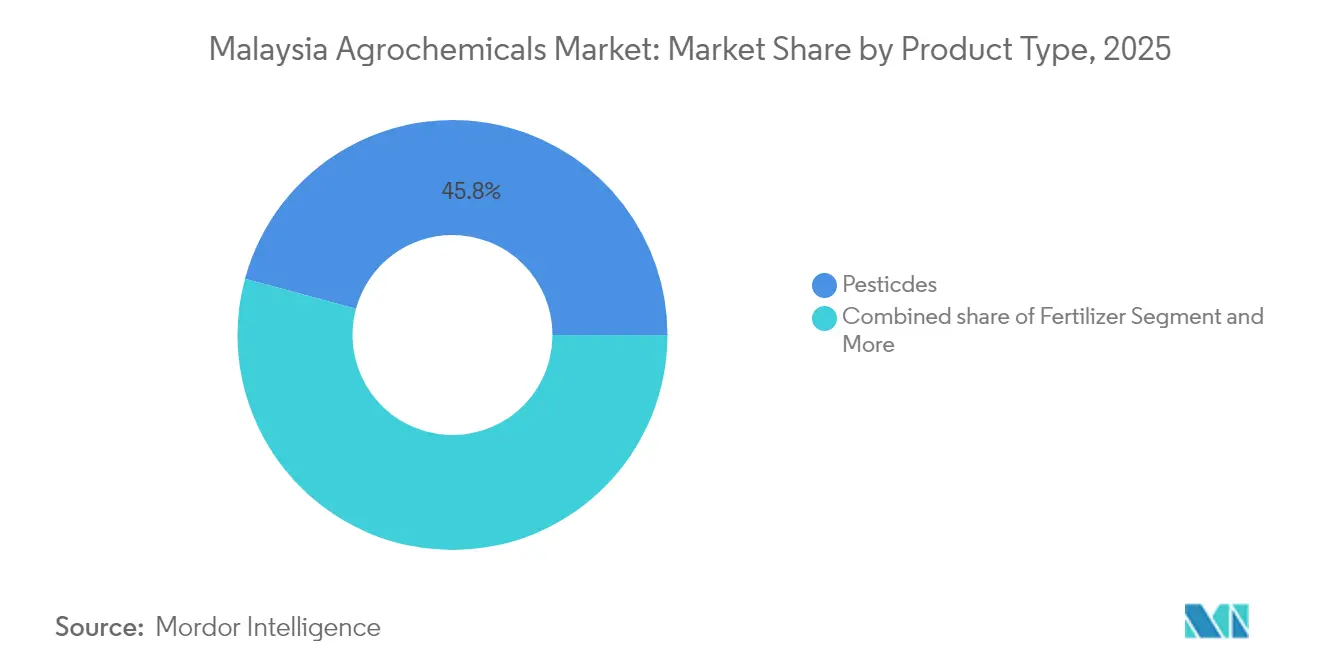

- By product type, pesticides led with 45.78% of Malaysia agrochemicals market share in 2025, while plant growth regulators are projected to expand at a 9.41% CAGR through 2031.

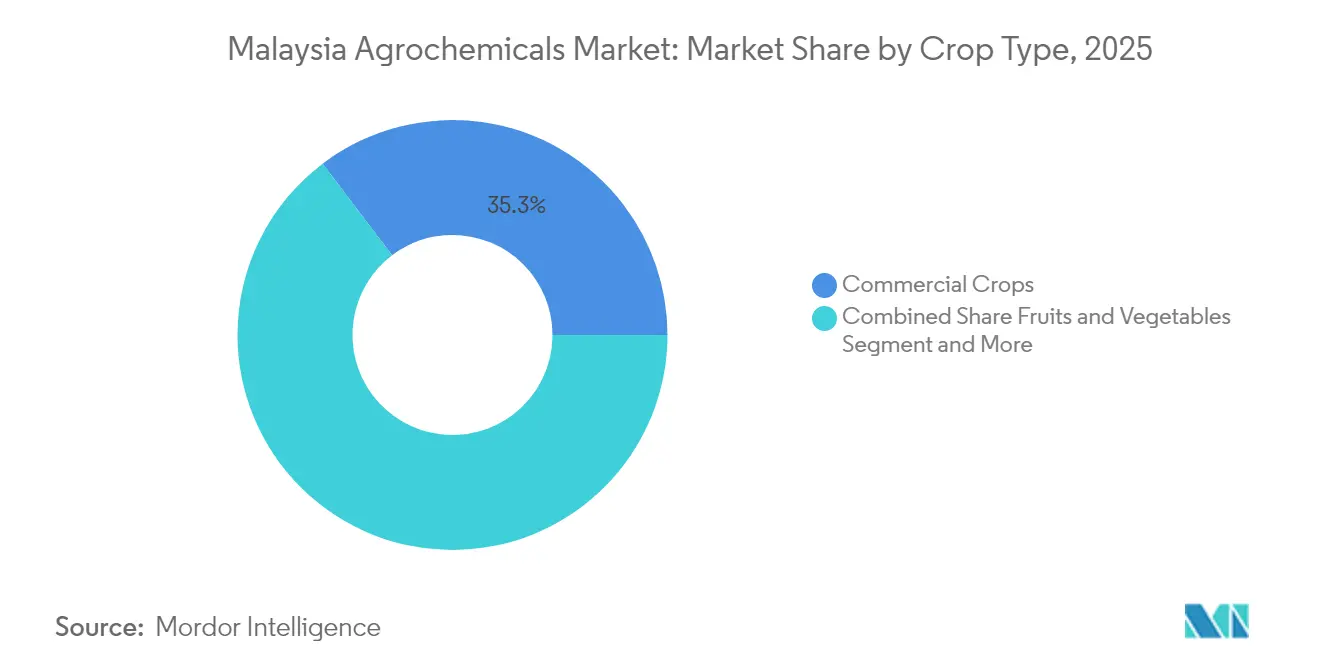

- By crop type, commercial crops accounted for a 35.32% share of Malaysia agrochemicals market size in 2025, while fruits and vegetables are advancing at a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of pests and diseases | 1.2% | National, with higher intensity in Peninsular Malaysia plantation belts | Medium term (2-4 years) |

| Rising food demand and need for higher crop productivity | 1.5% | National, concentrated in granary areas of Kedah, Perlis, and Perak | Long term (≥ 4 years) |

| Government subsidies and fertilizer tax incentives | 0.8% | National, with targeted focus on smallholder areas | Short term (≤ 2 years) |

| Expansion of oil palm and rubber plantations | 1.0% | Sabah, Sarawak, and southern Peninsular Malaysia | Long term (≥ 4 years) |

| Adoption of precision-farming services | 0.6% | Early adoption in Johor, Selangor, and Perak commercial farms | Medium term (2-4 years) |

| Growth of agri-fintech-enabled smallholder credit | 0.4% | Rural areas across all states, particularly Felda settlements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising food demand and need for higher crop productivity

Malaysia’s rice self-sufficiency rate stalled between 60% and 70%, prompting the National Agrofood Policy 2021-2030 to raise average paddy yields from 3.75 metric tons per hectare to 5.0 metric tons per hectare.[1]Source: Ministry of Plantation and Commodities, “Laman Web Rasmi KPK – Home,” kpk.gov.my The five-season paddy initiative in Kelantan, Pahang, and Terengganu magnifies fertilizer and pesticide cycles, especially urea, compound NPK, and synthetic pyrethroids. Intensification extends to protected horticulture, where fertigation and sticky-trap monitoring are displacing broad-spectrum sprays. Credit lines from the FarmByte-Agrobank platform cover input purchases and link growers to bundled crop-advice apps, fostering adoption of registered products. Rising urban incomes support premium produce, encouraging residue-free inputs with export compliance certification.

Government subsidies and fertilizer tax incentives

Budget 2025 earmarked RM300 million (USD 72 million) for new agricultural projects and RM2.6 billion (USD 624 million) for palm oil sector support.[2]Source: Ministry of Finance, “Government Implements Targeted Diesel Subsidy,” mof.gov.my Under the targeted diesel subsidy, logistics operators hauling agrochemicals pay RM2.15 per liter (USD 0.52), trimming distribution costs by 35%. Replanting grants of RM100 million (USD 24 million) to the Federal Land Development Authority (FELDA) cover seedling and pesticide expenses during the immature phases. The Sales and Service Tax exemption on imported fertilizers lower landed costs for compound NPKs by 3-5 %, improving affordability for smallholders adhering to Good Agricultural Practices (GAP) certification.

Expansion of oil palm and rubber plantations

National oil palm area reached 5.74 million ha in 2025, supporting continual herbicide and foliar nutrient programs. Mechanization grants encourage drone spraying that cuts labor needs while improving deposition uniformity by 18%. In 2024, SD Guthrie’s five-year RM2.5 billion (USD 600 million) automation plan targets a 70% uptake of variable-rate application rigs across 600,000 ha. Rubber rehabilitation covering 56,000 ha integrates pheromone traps with carbaryl sprays against leaf-eating caterpillars, reducing defoliation episodes. MSPO certification requires integrated pest management audits, driving estates to rotate chemical modes of action and include entomopathogenic fungi.

Adoption of precision-farming services

Digital farming tools are boosting Malaysia’s agrochemicals market. The Malaysia Digital Economy Corporation’s Digital Agtech program equipped 25,000 growers with sensors and satellite imagery, cutting fertilizer use by 30% in tomato farms while keeping yields stable. In oil palm, remote sensing for Ganoderma supports targeted fungicide use, creating steady demand. Geo-referenced scouting apps, linked with Syngenta’s Cropwise, send spray alerts to 180,000 smallholders, directly shaping pesticide purchases. These platforms also feed into agri-fintech credit scoring, where loans often require buying approved inputs, formalizing sales, and favoring branded products. As adoption spreads, precision-farming services will remain a key driver of agrochemical demand in Malaysia

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental regulations and residue limits | -0.7% | National, with stricter enforcement in export-oriented regions | Short term (≤ 2 years) |

| Adoption of gene-edited pest-resistant crop varieties | -0.3% | Research centers and progressive farms in Peninsular Malaysia | Long term (≥ 4 years) |

| Proliferation of counterfeit agrochemicals | -0.5% | Border states and rural distribution networks | Medium term (2-4 years) |

| Plantation labor shortages curbing application rates | -0.9% | Sabah, Sarawak, and Johor plantation estates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plantation labor shortages curbing application rates

The majority of plantation field workers, comprising 80%, are migrants, and visa delays have left 42,000 positions unfilled in 2024, which has postponed fertilizer applications by up to three weeks. Estates adopt controlled-release urea, extending nutrient availability to 90 days and reducing pass counts. Robotics projects aim to raise per-worker coverage from 10 ha to 17 ha in palm oil, trimming herbicide labor hours by 40%. Companies also push backpack-mounted electrostatic sprayers that shorten spray time per row. While automation offsets shortages, CapEx outlays curb uptake among smaller estates, provoking industry calls for accelerated depreciation incentives.

Proliferation of counterfeit agrochemicals

The Transnational Alliance to Combat Illicit Trade estimated illegal pesticides represent 10-25% of the regional supply, with e-commerce platforms acting as conduits. Malaysia’s Pesticides Board now requires QR-coded labels linked to registration databases, aiding enforcement at farm-gate inspections. Customs units in Kedah and Kelantan intensified border checks, seizing 4.1 metric tons of unregistered herbicides in 2024. Crop residue violations in mandarin oranges triggered Health Ministry advisories, leading supermarket chains to audit supplier spray logs. Industry associations are piloting blockchain traceability that logs batch numbers from importer to retailer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pesticides Remain Core While Plant Growth Regulators Accelerate

Pesticides captured 45.78% of Malaysia agrochemicals market share in 2025, reflecting endemic tropical pest pressure on perennial estates. The herbicide subset continues to dominate, driven by glyphosate and metsulfuron use in immature palm circles where labor scarcity elevates chemical weed control. Insecticide demand spikes during Metisa plana outbreaks. Aerial Bacillus thuringiensis drone sprays reduced larval incidence by 72% in 2024 trials. Fungicide volumes rise alongside Ganoderma-related yield losses, with systemic triazoles favored for trunk injections due to extended residual activity. Adjuvant uptake grows in tandem with variable-rate technology that relies on uniform droplet spectra to ensure canopy penetration. Plant growth regulators largely include ethephon and cytokinin blends, posting a 9.41% CAGR, benefiting from longan and durian flowering manipulation and tissue culture propagation in oil palm nurseries.

Fertilizers represent the largest volume segment, with nitrogenous formulations dominating paddy applications while potassic blends gain traction in plantation sectors seeking enhanced fruit quality and disease resistance. Precision soil testing in Johor identifies micro-nutrient deficiencies, spurring specialty blends with boron and magnesium additives. Controlled-release formulations reach 18% penetration in estate nutrition programs, lowering leaching losses and aligning with MSPO environmental metrics. Specialty foliar fertilizers for high-value fruits register double-digit growth as export buyers tighten quality specifications.

By Crop Type: Commerical Crops Dominance Challenged by High-Value Horticulture

Commercial crops accounted for 35.32% of Malaysia agrochemicals market share in 2025, as oil palm estates spray herbicides and broadcast fertilizers throughout the year to sustain fresh-fruit bunch yields in a crop that supplies 44% of global palm oil. Rubber plantations follow in value, yet replanting programs under the Rubber Industry Smallholders Development Authority combine selective fungicides with larvicides to curb leaf diseases on aging stands. Grains and cereals mainly paddy across 688,000 hectares tap intensive NPK formulas and split applications that underpin the five-season planting drive aimed at moving yields from 3.75 metric tons/ha to 5.0 metric tons/ha. In this segment, controlled-release urea and drone broadcasting lower labor requirements and improve uptake efficiency.

Fruits and vegetables post the fastest 9.18% CAGR through 2031, as premium prices justify chemical inputs that run 15-20% of production costs, driving use of low-residue insecticides and fertigation-grade nutrients. Emerging oilseeds and pulses receive policy support for import substitution, prompting trial plots that mix conventional herbicides with rhizobial seed coatings. Turf and ornamental grass demand expands in tandem with golf course construction and urban landscaping projects that favor selective pre-emergent herbicides and iron chelate foliar feeds. Smaller commercial crops such as sugarcane and cocoa command niche premiums, allowing estates to pilot precision nutrient mapping, align with Malaysian Sustainable Palm Oil environmental standards. Collectively, these dynamics diversify Malaysia agrochemicals market size growth drivers beyond its traditional plantation backbone.

Geography Analysis

Peninsular Malaysia generated a significant amount of Malaysia agrochemicals market size in 2025, reflecting intensive input use on mature palm, rubber, and paddy farms clustered along the central and southern corridor. Johor leads state demand due to concentrated estates operated by IOI Corporation and SD Guthrie, combined with proximity to the Port of Tanjung Pelepas, which streamlines imports. Selangor functions as the principal distribution hub, with multinational formulators locating warehousing near Port Klang to serve domestic and re-export flows.

Sabah and Sarawak regions are underpinned by ongoing new-planting programs and federal replanting incentives worth RM2.4 billion (USD 576 million) for FELDA and FELCRA settlers. Hilly terrains favor aerial drone spraying that increases chemical penetration on terraced slopes. The Sarawak state government promotes rubber rehabilitation mixed with inter-cropped banana, raising compound fertilizer use. Local agrochemical blenders in Bintulu capture downstream value by toll-manufacturing herbicides for national brands.

Smaller states such as Perlis and Melaka, urban farming expansion, and greenhouse vegetable projects supported by the Malaysia Digital Economy Corporation, inject incremental growth. Border states Kedah and Kelantan face counterfeit influx risks, triggering intensified customs collaboration and retailer education campaigns that encourage barcode scanning at the point of sale. Across all regions, adoption of MSPO-aligned integrated pest management compresses blanket spraying in favor of threshold-based applications, a trend projected to temper overall volume growth yet raise average unit value.

Regulatory Landscape

Malaysia regulates pesticides under the Pesticides Act 1974, administered by the Pesticides Board under the Department of Agriculture (DOA). Product approvals follow the Pesticides (Registration) Rules 2005, with registration dossiers covering efficacy, toxicology, and formulation, and the DOA maintaining a public register of approved products that governs what can be legally imported, distributed, and used on farms.

The control framework is periodically updated through schedule amendments, including the Pesticides (Amendment of First Schedule) Order 2024 (effective 31 May 2024), which added new controlled pesticide entities, including ethephon. On fertilizers, the Ministry of Agriculture and Food Security (KPKM) stated in June 2026 that it is drafting a Fertiliser Bill focused on quality standards and supply chain stability, while continuing targeted assistance and subsidies to manage farmer exposure to input-price volatility.

Competitive Landscape

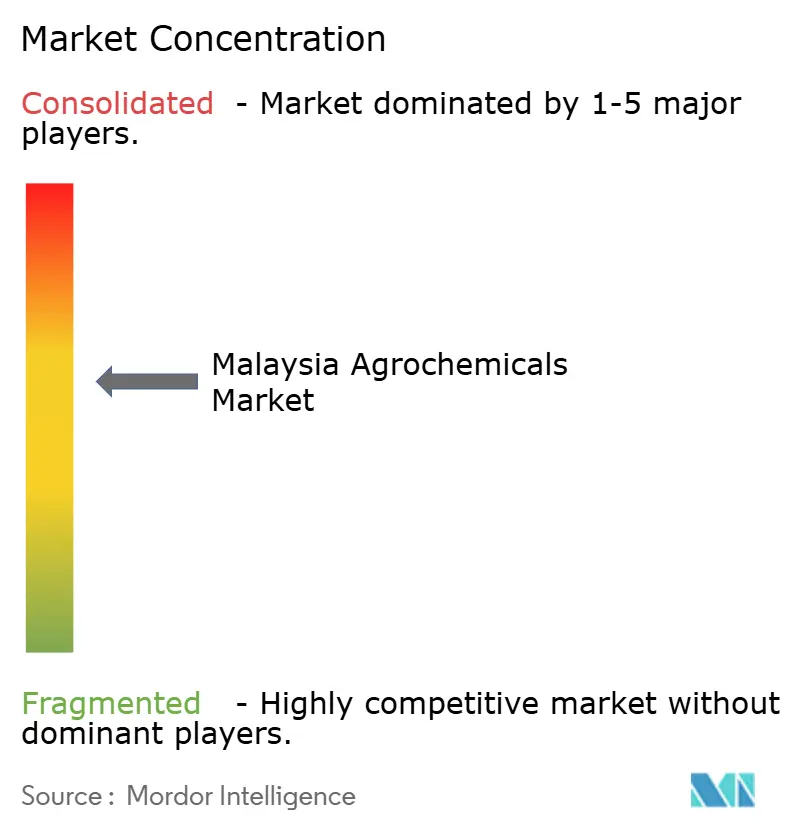

The top-five players held around 60% Malaysia agrochemicals market share in 2025, indicating moderate concentration that still permits mid-tier participation. Global majors leverage proprietary active ingredients and digital platforms. Syngenta’s Cropwise AI tailors threshold alerts, locking customers into its chemistry bundle. Bayer partners with MIMOS Berhad to co-develop data-driven crop-diagnosis models, while BASF SE pilots biodegradable polymer-coated fertilizers in paddy.

Local champion Hextar Group of Companies pursues backward integration, expanding its Pasir Gudang plant to produce 6,000 metric tons per year of dimethyl disulfide, a key pesticide intermediate. Ancom Nylex Berhad strengthened active-ingredient synthesis capability through HELM AG’s USD 23.1 million equity placement, ensuring secure offtake into Southeast Asia distribution channels. Joint ventures between formulators and drone service providers proliferate, bundling product sales with per-hectare application fees that transfer risk away from growers.

Competitive strategy now hinges on stewardship and traceability. Companies sponsor MSPO compliance workshops and QR-based verification to differentiate themselves from counterfeit products. Smallholders gravitate to distributors offering seasonal credit and technical advice, sustaining multilayered channels where wholesalers, sub-dealers, and village-level retailers coexist. The Chemical Industry Roadmap 2030 (CIR2030) of Malaysia aims to increase the industry's GDP contribution from 3.4% to 4.5% by 2030, generating an additional value of RM40 billion (USD 8.5 billion). The roadmap focuses on three primary areas, sustainability, specialty chemicals, and industrial integration. The implementation strategy encompasses 22 strategic focus areas supported by 10 key enablers.

Malaysia Agrochemicals Industry Leaders

Bayer AG

Syngenta Group

BASF SE

Hextar Group of Companies

Ancom Nylex Berhad

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digital advisory and precision-application programs create a gap for suppliers that can pair registered products with data-driven recommendations and traceability. In March 2026, the nationwide rollout of Rakan Tani (an AI-enabled tool for padi farmers) underscored government-backed demand for pest-risk monitoring and fertilizer application guidance, which supports differentiated offerings such as variable-rate compatible formulations, adjuvants, and decision-support services that fit into farm workflows.

Quality and compliance measures also support higher-assurance inputs and domestic upgrading in fertilizer technologies. The 31 May 2024 update to controlled pesticide substances under the Pesticides (Amendment of First Schedule) Order 2024 reinforces the need for compliant, properly registered pesticide portfolios, while the June 2026 disclosure that a Fertiliser Bill is being drafted signals tighter quality oversight and supply-chain governance. With subsidy mechanisms for seeds, fertilizers, and pesticides continuing, suppliers with strong stewardship, QR-enabled anti-counterfeit labeling, and locally anchored controlled-release or specialty nutrient production can compete on reliability and compliance as well as price.

Recent Industry Developments

- June 2026: Malaysia's Ministry of Agriculture and Food Security expanded padi-sector fertilizer and pesticide incentives from RM160 to RM300 per hectare per planting season after reporting input-price increases between January and May 2026. The move protected near-term purchasing power for smallholders and kept formal channels relevant as volatility and counterfeit risks rise.

- July 2025: Bangladesh signed a government-to-government agreement with Malaysia's FELCRA Niaga Sdn Bhd to import premium-grade fertilizers. The arrangement added a cross-border demand outlet and supported collaboration themes such as joint ventures and technical exchange, reinforcing Malaysia's role in regional fertilizer trade flows.

- September 2024: HELM AG entered a strategic partnership with Ancom Nylex Berhad by becoming a major shareholder. The deal strengthened Ancom Nylex's active-ingredient and crop protection development platform and broadened its route-to-market across Southeast Asia through a larger global partner.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of agrochemicals sold for agricultural use in Malaysia, including fertilizers, pesticides, adjuvants, and plant growth regulators, based on manufacturer and channel revenues recognized in the country.

Scope exclusions: We exclude farm tools and equipment, seeds, irrigation hardware, and agricultural services that sit outside chemical input sales.

Segmentation Overview

- By Product Type

- Fertilizers

- Nitrogenous

- Phosphatic

- Potassic

- Other Fertilizers

- Pesticides

- Herbicides

- Insecticides

- Fungicides

- Other pesticides

- Adjuvants

- Plant Growth Regulators

- Fertilizers

- By Crop Type

- Grains and Cereals

- Oilseeds and Pulses

- Fruits and Vegetables

- Commercial Crops

- Turf and Ornamental Grass

- Other Crops

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to anchor demand drivers to Malaysia crop patterns. We reviewed public statistics that show planted area and output by crop, then tested whether the implied agrochemical intensity (per hectare and per crop) looked realistic.

The supply side was checked through regulator and association materials to understand product availability and how products reach farms. We then tied those signals back to company disclosures such as annual reports, investor presentations, and press releases. Public and paid desk sources referenced during the study included Malaysia government agriculture releases and trade statistics, FAOSTAT, World Bank indicators, UN Comtrade, and open agronomy and residue related journal literature, plus paid subscriptions for company financials and intelligence, news and financials, patent lookups, and shipment level import export checks when local production versus imports needed clarification.

These desk sources are illustrative only, since many other public and paid references were used for data collection, validation, and follow up clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating how demand is formed in Malaysia across plantations and mixed crop farms, and how channel pricing moves through distributors and dealers. We spoke with senior and mid level stakeholders across manufacturers, formulators, importers, distributors, large growers, and agronomy advisors, then used those inputs to close gaps in application rates, seasonality, and price realization assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 19% | |

| Mid tier: 46% | Functional/Unit leaders: 39% | |

| Smaller Players: 22% | Managers: 42% |

Market-Sizing & Forecasting

Our sizing starts from a top-down demand pool build using Malaysia crop area and production patterns, followed by typical application intensity by crop and product class (for example, fertilizer nutrient mixes and pesticide treatment frequency). Once that demand picture is built, it is converted into value using observed price bands by formulation type and pack size. We then adjust for channel margins and the share of imported versus locally formulated volumes.

To keep the model grounded, results are corroborated with selective bottom-up approximations such as rolling up a sample of supplier and distributor revenues, then stress testing the implied market size against import trends and planting season timing. Key inputs used in the model include oil palm and rubber planted area, crop mix shifts, pest and disease pressure signals, fertilizer nutrient demand indicators, average product prices in local currency with conversion timing, and regulatory registration pace that impacts product availability. For forecasting, scenario analysis was applied to reflect different outcomes for commodity linked planting decisions, weather disruptions, and input cost swings, and then the final path was aligned to consensus expectations shared by primary research respondents.

Data Validation & Update Cycle

Outputs are checked through multiple validation steps so obvious overstatements and missed categories get caught early. We compare the modeled totals against independent signals such as trade flows for key active ingredients and formulations, changes in planted area, and reported pricing direction from channels, then investigate any variance that looks out of line.

Before sign-off, assumptions are re-reviewed by another analyst and follow up calls are triggered when a major mismatch shows up by product group or crop coverage. Reports are refreshed annually, and interim updates are made when material events occur such as policy changes, sharp currency moves, or supply disruptions. Right before delivery, a final pass is done to confirm the latest public updates have been reflected in the numbers and narrative.

Mordor Intelligence's Agrochemicals Market Malaysia Market Size Versus Other Published Estimates

Published market values for Malaysia agrochemicals can differ even when the topic name looks the same, because the study boundary is not always identical and the timing of the base year also shifts. Differences usually come from what is counted inside agrochemicals, how price realization is treated across channels, and whether plantation heavy demand patterns are fully reflected.

Import checks for active ingredients and finished formulations, together with planted area and crop output signals, are the evidence used to keep Mordor Intelligence's 2025 estimate aligned to the Malaysia demand pool rather than to broad regional averages. Some published figures lean more on a single base year snapshot without adjusting for channel margin structure, currency conversion timing, or the split between crop-based and non-crop-based applications, which can move the total up or down.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.71 B (2025) | |

| Trade Publisher A | USD 0.68 B (2024) | Uses a 2024 base and may not fully normalize pricing and currency timing into the estimation year, which can understate value when price realization shifts through the channel. |

| Industry Research Firm B | USD 0.70 B (2025) | Broader inclusion of adjacent input items and wider distribution channel definitions can slightly lift totals, especially when minor categories and dealer markups are treated differently. |

The spread is narrow, but it still points to practical drivers, which are base year choice, what sits inside the agrochemicals boundary, and how channel pricing is converted into market value. By tying the size to observable crop and trade signals and then validating assumptions through field feedback, the estimate stays repeatable and easy to audit when clients want to trace the number back to clear steps.

Key Questions Answered in the Report

What is the projected value of the Malaysia agrochemicals market in 2031?

The market is forecast to reach USD 928.07 million by 2031, growing at a 4.55% CAGR.

Which product segment leads Malaysia agrochemical consumption?

Pesticides lead with 45.78% share, driven by continuous weed and pest control on perennial estates.

Why are plant growth regulators growing faster than other product types?

Adoption in fruit-flower induction and oil-palm tissue culture drives a 9.41% CAGR for plant growth regulators.

How are government subsidies influencing input purchases?

Budget 2025 allocations and diesel subsidies lower production costs, encouraging formal input sourcing and supporting market growth.

Page last updated on: