Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.3 Billion |

| Market Size (2026) | USD 4.54 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Agrochemicals Market Analysis by Mordor Intelligence

The Indonesia agrochemicals market size is expected to grow from USD 4.3 billion in 2025 to USD 4.54 billion in 2026 and is forecast to reach USD 5.95 billion by 2031 at 5.55% CAGR over 2026-2031. The market expansion is supported by government fertilizer subsidies, the development of climate-adaptive synthetic products, agricultural mechanization, and increasing horticultural exports. However, market growth faces challenges from counterfeit products, increasing adoption of organic farming practices, and growing herbicide resistance. PT Pupuk Indonesia, the state-owned enterprise, holds a significant market share through its subsidy distribution network. This market dominance has led multinational companies to focus on premium, technology-enhanced synthetic products to maintain profit margins. While Java continues to be the primary consumption center, the development of new production facilities in Papua, Kalimantan, and Sumatra is reducing logistics costs and enabling region-specific product formulations. The implementation of digital voucher systems, artificial intelligence-based crop advisory services, and mechanized paddy field transformation is increasing the per-hectare usage of agricultural inputs, strengthening Indonesia's synthetic agrochemicals market fundamentals.[1]Muhammad Harianto and Resinta Sulistiyandari, “Indonesia boosts fertilizer subsidy by Rp28 trillion,” ANTARA News, en.antaranews.com

Key Report Takeaways

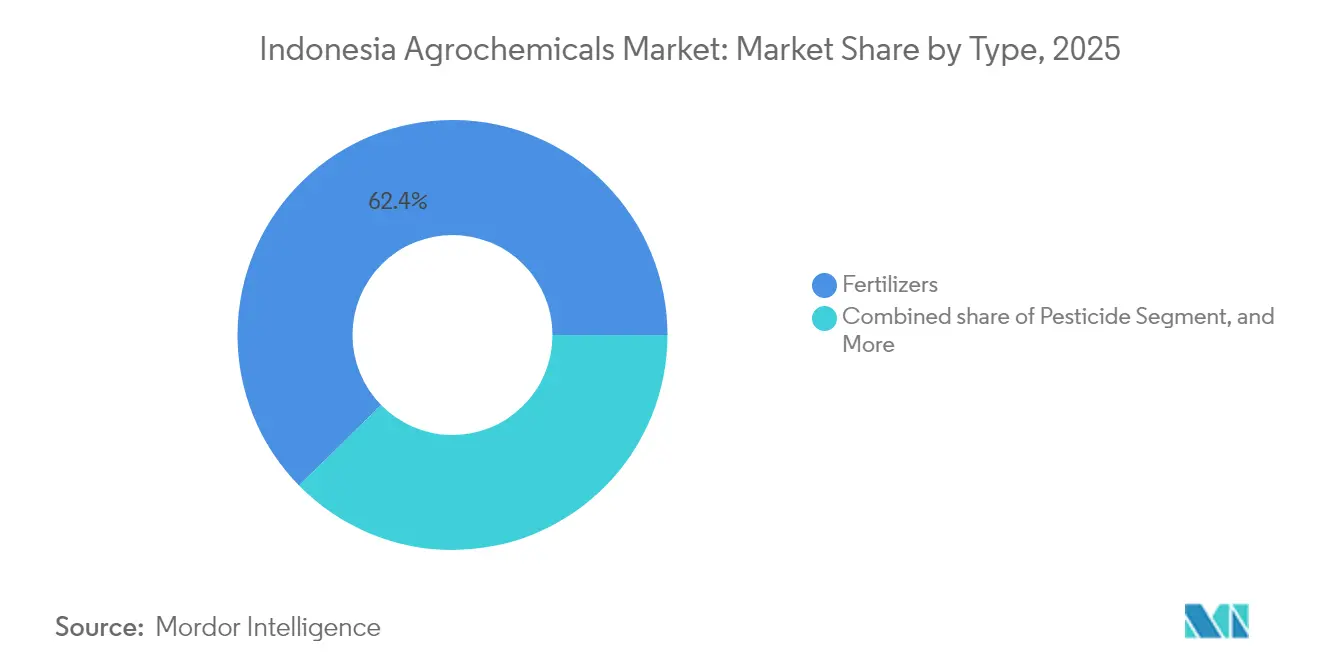

- By type, fertilizers led with 62.35% revenue share in 2025, and plant growth regulators are advancing at an 8.05% CAGR through 2031.

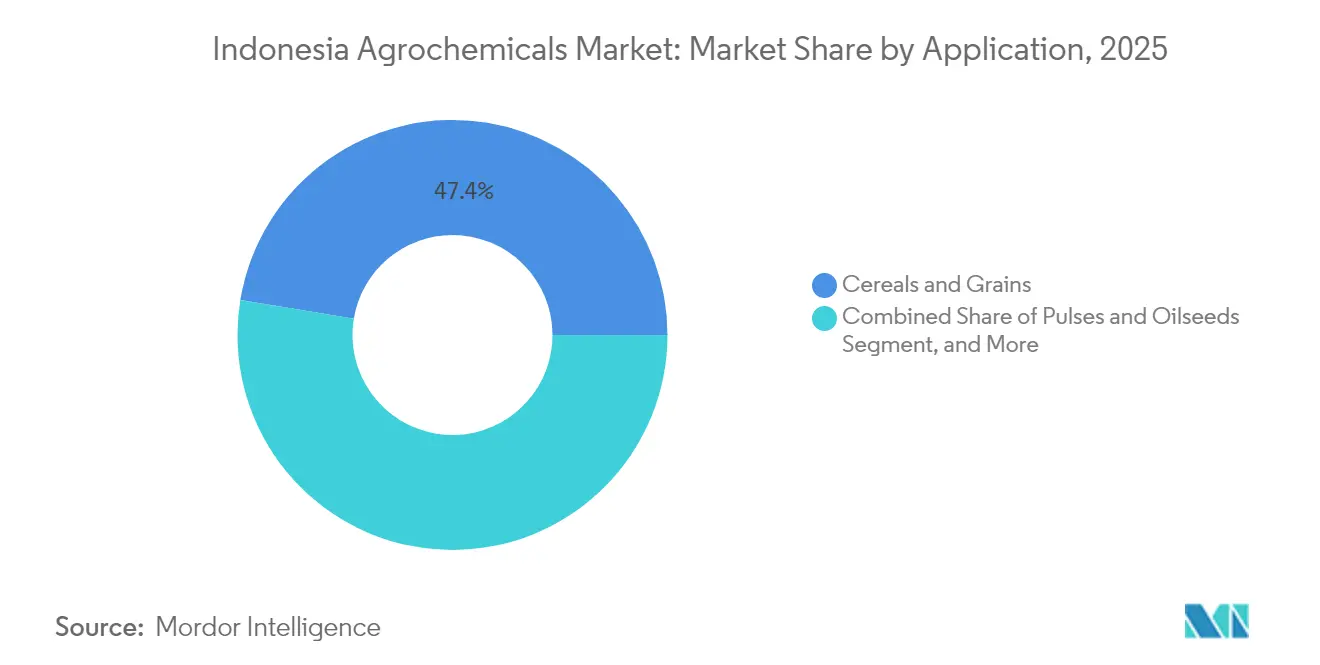

- By application, cereals and grains accounted for 47.40% of the Indonesia agrochemicals market share in 2025, while fruits and vegetables are projected to climb at a 6.72% CAGR through 2031.

- Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, and PT. Pupuk Indonesia together controlled more than half of the Indonesia agrochemicals market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Fertilizer Subsidies and E-voucher Distribution | +1.8% | National, concentrated in Java, Sumatra, and Sulawesi | Short term (≤ 2 years) |

| Expansion of Domestic Fertilizer Capacity | +1.2% | National, with major facilities in East Java, and East Kalimantan | Medium term (2-4 years) |

| Accelerating Mechanized Paddy Conversion Drives | +0.9% | Java, Sumatra, and South Sulawesi rice production centers | Medium term (2-4 years) |

| Chemical Use Surge in Horticulture Export Targets | +0.7% | Java, North Sumatra, and West Java export corridors | Long term (≥ 4 years) |

| AI-enabled Crop Advisory Apps Boosting Agrochemicals Intensity | +0.5% | Java, expanding to Sumatra and Sulawesi | Long term (≥ 4 years) |

| Palm-oil By-product Plant Growth Regulators Gaining Regulatory Fast-track | +0.3% | Sumatra, Kalimantan, and Riau palm oil regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Fertilizer Subsidies and E-voucher Distribution

Indonesia's fertilizer subsidy program has created a dual-tier market where subsidized nutrient blends compete with premium formulations. The digital delivery through mobile platforms improves targeting and transparency, allowing suppliers to match products with regional cropping requirements. This system maintains steady demand for basic fertilizers and increases farmer loyalty to domestic producers, while encouraging international companies to develop differentiated blends and enhanced coatings. East Java receives the largest share of subsidies, with distribution networks centered around major urban areas. As the subsidy focuses on staple crops like rice, suppliers of specialty inputs must modify their approaches to serve horticultural zones outside the subsidy coverage. The program maintains price stability and highlights the importance of government collaboration in the agrochemical industry.

Expansion of Domestic Fertilizer Capacity

Indonesia's significant investment in fertilizer production infrastructure includes new facilities and upgrades across various regions. This expansion aims to decrease import dependence and enhance supply chain performance, particularly to remote islands with historical logistics challenges. The higher production volume increases competition in standard fertilizer grades, encouraging manufacturers to focus on value-added formulations for better profit margins. The expansion increases demand for upstream chemical components, creating opportunities for international specialty chemical suppliers. The additional capacity will influence market dynamics by reducing production costs and promoting market segmentation into premium categories.

Accelerating Mechanized Paddy Conversion Drives

Agricultural machinery adoption in rice cultivation areas is changing input application patterns. Mechanized equipment enables accurate and well-timed fertilizer and pesticide application, improving yields and increasing chemical usage per hectare. Government financing programs help smallholder farmers access these technologies, particularly in the main food-producing regions. Mechanization integrates with digital farming tools that guide application timing, encouraging farmers to use diverse agrochemical products. With increasing labor scarcity and costs, mechanization continues to drive demand for equipment-compatible formulations and specialized additives.

Chemical Use Surge in Horticulture Export Targets

Indonesia's increased emphasis on tropical fruit production aims to establish regional export leadership. This development requires high-quality agrochemical inputs to meet export market requirements. Farmers are adopting advanced fungicides and pest control products with reduced pre-harvest intervals to meet residue limits. Areas with expanding fruit and vegetable production show increased demand for micronutrients and specific disease control products.[2]Kementerian Sekretariat Negara, “Tahun 2025, Indonesia Bisa Jadi Produsen Buah Tropika Terbesar di Asia,” setneg.go.id Government-provided technical training supports the implementation of intensive chemical programs, including water-soluble fertilizers for precision irrigation systems. The expansion of orchards and greenhouse operations is diversifying the agrochemical market beyond traditional field crops.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and Illegal Pesticide Inflow | -0.8% | National and concentrated in border regions and major ports | Short term (≤ 2 years) |

| Growing Smallholder Shift to Organic Certifications | -0.6% | Java, Yogyakarta, and Central Java organic farming zones | Medium term (2-4 years) |

| Herbicide-resistant Weed Outbreaks | -0.4% | Sumatra, Kalimantan palm oil and rice regions | Medium term (2-4 years) |

| El-Niño Induced Fertilizer Price Shocks | -0.7% | National and severe impact in Eastern Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Illegal Pesticide Inflow

The Indonesian agricultural sector faces significant challenges from unauthorized agrochemical products entering the market. These illicit pesticides, which often mimic established brands, negatively impact farmer trust and disrupt authorized distribution networks. Companies have increased their investments in protective measures, including tamper-evident packaging and digital tracking systems, to maintain brand authenticity. The country's maritime borders remain susceptible to illegal imports due to logistical complexities and enforcement limitations. While industry participants and regulatory authorities work together to strengthen controls and enforcement measures, market disruptions continue. Companies are implementing preventive strategies, including retail outlet inspections and farmer awareness programs, to maintain market confidence and protect sales.

Growing Smallholder Shift to Organic Certifications

Small-scale farmers increasingly adopt low-input farming methods that prioritize environmental sustainability and financial stability. These agricultural practices generate lower yields per hectare but maintain economic viability through reduced synthetic input requirements and enhanced environmental stress tolerance. The adoption rate increases through community networks, particularly in areas where farmers seek protection against input price fluctuations. Traditional agrochemical suppliers face potential sales volume reductions unless they adapt their product portfolios to meet these changing farmer requirements. Organic certification attracts premium pricing from urban retailers and export buyers, encouraging gradual acreage conversion. The ongoing transition to diverse input strategies may transform market demand patterns, requiring suppliers to develop integrated solutions and complementary products that support these emerging agricultural practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fertilizers Anchor Market Amid Specialty Growth

Fertilizers contributed 62.35% of Indonesia's agrochemicals market size in 2025. Government subsidies maintain consistent demand, while market commoditization has prompted manufacturers to develop coated, slow-release, and micronutrient-enriched products for improved margins. The expansion of domestic production capacity has led traditional fertilizer manufacturers to partner with specialty chemical companies to access new technologies. Pesticides remain the second-largest segment, with resistance management driving diversification in active ingredients and stewardship programs. Fungicides and adjuvants show steady growth, particularly in high-frequency application areas where performance and compatibility are essential.

Plant growth regulators, despite their small market share, demonstrate the highest growth rate at 8.05% CAGR, supported by precision farming practices and controlled cultivation methods that require hormonal products for harvest uniformity. Multinational companies now combine regulators and adjuvants with pesticide products to provide comprehensive crop management solutions. Extended registration periods create barriers to entry, benefiting established companies but limiting the introduction of new formulations. Market success requires strong regulatory compliance and adaptable research capabilities to address evolving agricultural needs.

By Application: Cereals Dominance Challenged by Export Crops

Cereals and grains represented 47.40% of the Indonesia agrochemical market share in 2025, supported by rice self-sufficiency initiatives and increased corn cultivation, which maintains high demand for nitrogen fertilizers and herbicides. Growth in this segment is stabilizing as subsidy levels plateau. The fruits and vegetables segment is expanding at 6.72% CAGR, driven by export opportunities and increased urban demand for consistent produce supply. Plantation crops, particularly palm oil, maintain a stable demand for fungicides and herbicides suited for long-term cultivation.

Indonesia's regions display distinct agrochemical usage patterns. Java's intensive shallot and pepper intercropping requires substantial pesticide use, North Sumatra's citrus production needs balanced micronutrient applications, and Riau's palm oil estates require targeted weed management for resistance control. Export-oriented producers increasingly adopt low-residue products and traceable input systems to meet international requirements, leading suppliers to provide documentation and compliance support. These regional and crop-specific requirements create distinct market opportunities within Indonesia's agrochemical sector

Geography Analysis

Java dominates value capture, accounting for more than half of Indonesia's agrochemicals market transactions. Dense cropping patterns, efficient logistics, and well-established advisory networks drive this. East Java reinforces its primacy through substantial fertilizer distribution, while Central and West Java mirror this intensity. The widespread adoption of AI-driven advisory tools among rice farmers in these regions has led to increasingly sophisticated input strategies. However, land scarcity and growing environmental scrutiny are prompting a gradual shift toward low-chemical models in select districts.

Sumatra represents the market's fastest-growing region. The diversification of palm-oil estates into corn, rice, and tropical fruits increases crop protection product demand. North Sumatra's export infrastructure supports high-value horticulture, increasing fungicide consumption. Riau and South Sumatra focus on mature plantation rejuvenation through integrated weed management, while Lampung's smallholder practices moderate synthetic input demand.

Kalimantan and Sulawesi present growth opportunities despite infrastructure limitations. South Kalimantan's agroindustry initiatives attract distributors offering adaptable logistics solutions. Central Kalimantan's food-estate developments increase per-acre agrochemical expenditure through mechanization and irrigation improvements. South Sulawesi shows increased demand for new active ingredients and stewardship programs due to resistance management needs. While expansion into these outer islands requires sustained investment and region-specific approaches, they offer early-entry advantages as Java's market reaches saturation.

Competitive Landscape

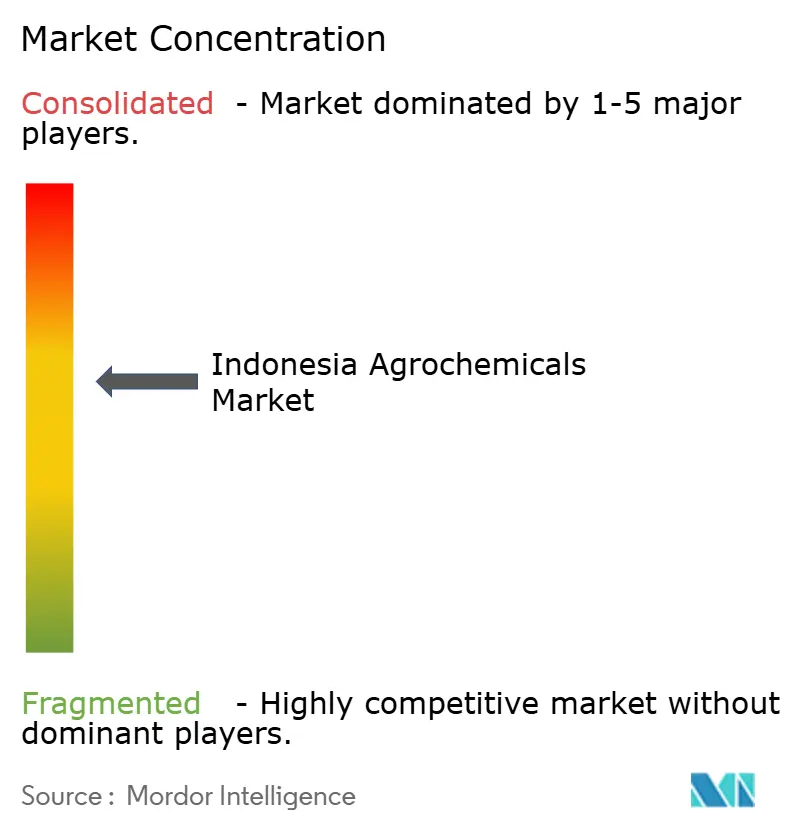

The Indonesia agrochemicals market shows moderate consolidation, with Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, and PT. Pupuk Indonesia holds more than half of the Indonesia agrochemical market share in 2024. The market structure combines state-backed control in commodity fertilizers and multinational presence in innovation-focused segments. PT Pupuk Indonesia maintains its position through subsidy distribution management, warehouse infrastructure, and integrated logistics across staple crop regions. Global companies focus on digital agronomy platforms, resistance-management solutions, and specialized crop protection programs to address farmer requirements.

Multinational companies are strengthening their market presence by integrating advisory services and combining agricultural inputs through local retail networks. This approach improves engagement with small-scale farmers and increases the adoption of comprehensive solutions. International companies are acquiring strategic assets to enhance distribution capabilities, combining global brands with local production facilities and improving access to micronutrient and specialty products. The combination of global expertise and local market understanding has become essential for market growth and customer retention.

Sustainability initiatives are becoming a key competitive advantage. Domestic manufacturers are investing in low-carbon production through green ammonia and hybrid manufacturing processes, meeting environmental standards and attracting environmentally conscious investors. Global companies are collaborating with drone operators for precision application services, while local firms are developing alternative raw materials for specialized market segments. While regulatory approvals remain time-intensive, they benefit established companies with strong compliance systems. Market success requires the integration of technology, commitment to sustainability practices, and implementation of farmer-focused service approaches that extend beyond traditional product sales.

Indonesia Agrochemicals Industry Leaders

Bayer AG

Syngenta Group

Corteva Agriscience

BASF SE

PT. Pupuk Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: PT. Pupuk Indonesia partnered with Brunei Fertilizer Industries to jointly produce urea and ammonia, focusing on enhancing regional food security and collaboration within the Association of Southeast Asian Nations (ASEAN) for fertilizer development.

- October 2023: Xingfa Group acquired a 70% stake in Indonesian pesticide manufacturer AMCO (PT. Adil Makmur Fajar Company). This acquisition represents Xingfa Group's initial overseas production investment and extends its paraquat and glyphosate distribution in Southeast Asia.

- January 2023: FMC Corporation launched Quintect 105SC in Indonesia, a systemic fungicide containing pikarbutrazol. The product targets leaf and stem blight in potato crops to enhance harvest yields.

Indonesia Agrochemicals Market Report Scope

Agrochemicals are commercially manufactured chemicals that enhance crop performance and prevent crop destruction by pests, diseases, and weeds, thereby improving crop yield and quality. The Indonesia Agrochemicals Market is segmented by Type (Fertilizers, Pesticides, Adjuvants, and Plant Growth Regulators) and Application (Cereals, Oilseed, Fruits and Vegetables, and Other Crops). The report offers market sizing and forecasts regarding value (USD) for all the above segments.

By Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

By Application

| Cereals and Grains |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops |

| By Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Application | Cereals and Grains | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Commercial Crops | ||

Key Questions Answered in the Report

What is the current value of the Indonesia agrochemicals market?

The market is valued at USD 4.54 billion in 2026 and is projected to reach USD 5.95 billion by 2031.

Which segment leads by type in Indonesia?

Fertilizers dominate with 62.35% revenue share in 2025, supported by large-scale government subsidies.

Which crop application segment is growing fastest?

Fruits and vegetables are expanding at a 6.72% CAGR through 2031 as Indonesia pushes tropical fruit exports.

Which region outside Java offers the strongest growth potential?

Sumatra, driven by palm-oil diversification and export horticulture, provides the most attractive expansion opportunities for suppliers.

Page last updated on: