Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.8 Billion |

| Market Size (2026) | USD 10.17 Billion |

| Market Size (2031) | USD 12.27 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

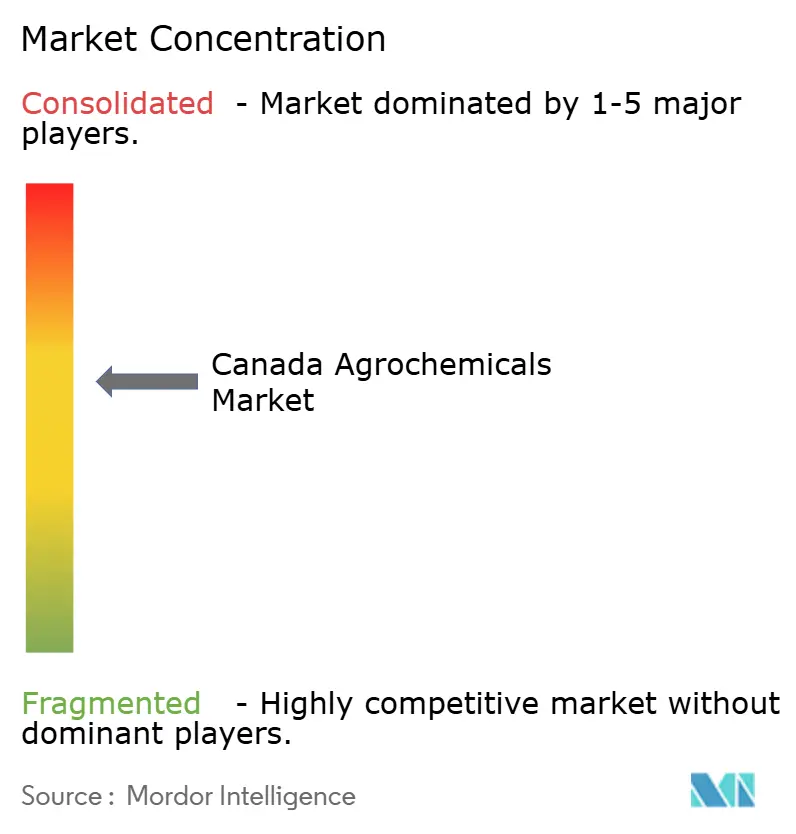

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Agrochemicals Market Analysis by Mordor Intelligence

The Canadian agrochemicals market size in 2026 is estimated at USD 10.17 billion, growing from 2025 value of USD 9.8 billion with 2031 projections showing USD 12.27 billion, growing at 3.81% CAGR over 2026-2031. Agricultural demand changes, regulatory updates, and improvements in input distribution infrastructure nationwide support market growth. In June 2025, the expansion of downstream processing facilities, such as Cargill's Regina facility and Richardson International's Yorkton plant, doubled canola crushing capacity, driving the demand for agricultural inputs to meet Asian export requirements. Federal emissions reduction targets, which mandate a 45-50% decrease in greenhouse gas emissions from 2005 levels by 2035, are influencing market dynamics. These targets are prompting fertilizer manufacturers to adopt low-carbon technologies while managing the limitations of rail and port infrastructure that impact potash exports. The competitive landscape is evolving as established companies integrate analytical services with chemical products, while regional players focus on local field trials to attract farmers.

Key Report Takeaways

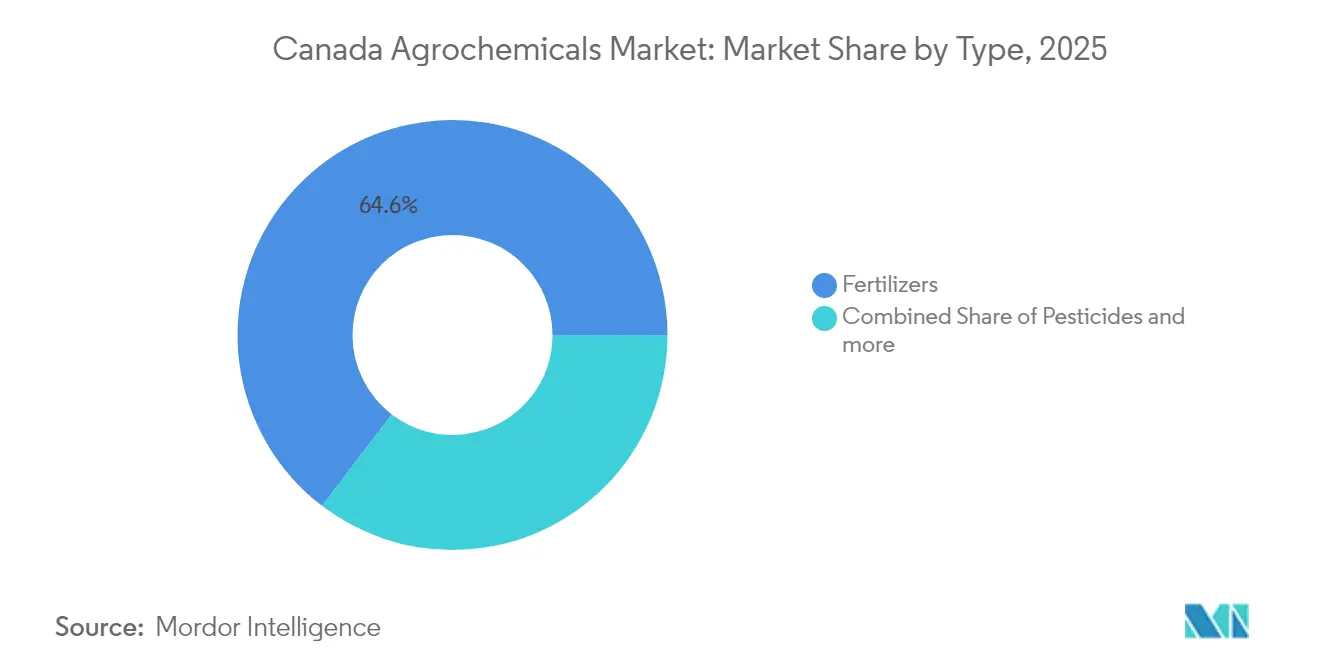

- By type, fertilizers commanded 64.62% of the Canada agrochemicals market share in 2025, whereas plant growth regulators are set to grow the fastest at a 6.54% CAGR through 2031.

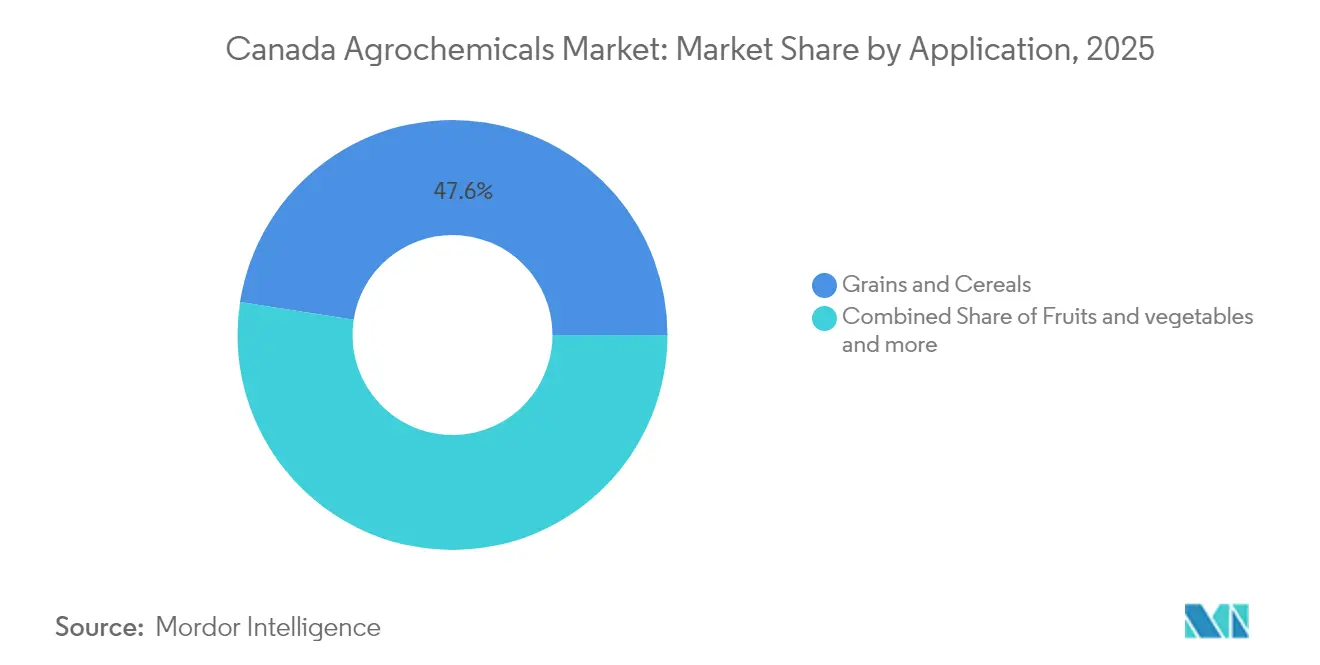

- By application, grains and cereals captured 47.55% of the Canada agrochemicals market size in 2025,fruits and vegetables are forecast to expand at a 5.51% CAGR to 2031.

- Nutrien, Bayer AG, Syngenta Group Group, BASF SE, and Corteva Agriscience together held 62.85% of total revenue in 2025, keeping the Canada agrochemicals market moderately concentrated.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing agricultural acreage shift toward oilseeds | +0.8% | Prairie Provinces | Medium term (2–4 years) |

| Expansion of the canola-crushing ecosystem | +0.6% | Saskatchewan and Alberta | Short term (≤2 years) |

| Rising food-export demand to Asia | +0.5% | National, strongest in Western Canada | Long term (≥4 years) |

| Wider adoption of precision-ag services | +0.4% | Ontario and the Prairies are expanding eastward | Medium term (2–4 years) |

| 4R nutrient-stewardship incentives by provincial governments | +0.3% | Alberta, Saskatchewan, and Ontario | Long term (≥4 years) |

| Climate-resilient crop genetics that require higher micronutrient inputs | +0.2% | Prairies and Ontario | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Agricultural Acreage shifts Toward Oilseeds

Farmers across the Prairie provinces are allocating more land to canola and soybean production, changing nutrient and herbicide usage patterns in Western Canada's agriculture sector. According to Statistics Canada, canola production reached 19.5 million metric tons in 2024, a 1.6% increase despite challenging growing conditions, while soybean production grew 2.4% to 7.1 million metric tons[1].Source: Statistics Canada, “Model-Based Principal Field Crop Estimates, July 2024,” statcan.gc.ca This shift in crop rotation increases the need for broadleaf weed control herbicides, particularly for managing kochia resistance, and creates demand for specialized micronutrient blends to maintain oil content and yield. The transition to oilseeds requires more precise nutrient application timing and placement compared to cereal crops, driving the adoption of precision application technologies. Health Canada's Pest Management Regulatory Agency supports this agricultural transition through streamlined registration processes for oilseed-specific formulations to ensure adequate input supply for expanded production.

Expansion Of The Canola-Crushing Ecosystem

Canada's canola processing infrastructure is expanding significantly, with five major facilities adding approximately 7 million metric tons of annual crushing capacity. This expansion is creating consistent local demand for agrochemical inputs and reshaping regional supply chains. Cargill's USD 350 million Regina facility, which is more than 50% complete and scheduled to begin operations in December 2025, will process 1 million metric tons annually [2]Source: Cargill, “Building the Future of Canola with Our Regina Canola Crush Facility,” cargillag.ca. In 2024, Richardson International doubled its Yorkton plant capacity to 2.5 million metric tons of seed annually, making it the world's largest canola crushing facility. This infrastructure development ensures stable domestic demand for canola production inputs, reducing export dependency and establishing more predictable pricing for herbicides, fungicides, and specialty fertilizers used in canola cultivation. The increased crushing capacity also increases demand for post-harvest storage and handling chemicals, as higher processing volumes require improved grain preservation technologies.

Rising Food-Export Demand to Asia

Canadian agricultural exports to Asia continue to grow, with canola shipments to China increasing by 80% in 2024-25 to 3.84 million metric tons. This growth is reshaping agricultural input demand as farmers adjust their production methods to meet export market requirements. According to Agriculture and Agri-Food Canada, total agricultural exports reached USD 67.2 billion (CAD 91.6 billion) in 2024, with Asia-Pacific markets representing 42% of total export value, an increase from 38% in 2020 . The expansion into diverse export markets has increased demand for specialized agricultural inputs, including fungicides for storage stability, nutrient formulations for protein optimization, and post-harvest treatments that comply with importing country residue standards. The 2024 Canada-Indonesia Comprehensive Economic Partnership Agreement creates additional market access opportunities, which may further expand production and increase input demand.

Wider Adoption Of Precision-Ag Services

Precision agriculture technology adoption is increasing across Canadian farms, with variable-rate application systems and AI-driven crop monitoring platforms improving input efficiency and specialty product consumption through targeted applications. Agriculture and Agri-Food Canada's Agricultural Clean Technology Program has allocated USD 238 million (CAD 325 million) to support the adoption of precision agriculture, with over 2,400 projects approved since the program began[3]Agriculture and Agri-Food Canada, “Agricultural Clean Technology Program,” agriculture.canada.ca. The technology shift has enabled more targeted applications of premium-priced specialty inputs while reducing overall chemical volumes, creating opportunities for manufacturers who develop precision-compatible formulations. Health Canada's regulatory framework supports precision agriculture by facilitating expedited reviews for products that demonstrate reduced environmental risks when used in conjunction with precision application technology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent federal pesticide-re-evaluation timelines | -0.7% | National, specialty-crop belt most exposed | Short term (≤2 years) |

| Accelerating consumer preference for organic produce | -0.5% | Ontario, Quebec and British Columbia | Medium term (2–4 years) |

| Fertilizer carbon-pricing and nitrous-oxide-reduction targets | -0.4% | National, focus on Prairies | Long term (≥4 years) |

| Rail and port bottlenecks for potash and bulk chemicals | -0.3% | Western export corridors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Federal Pesticide-Re-Evaluation Timelines

Health Canada's Pest Management Regulatory Agency has intensified pesticide re-evaluation processes, creating market uncertainty as active ingredients face extended review periods. These reviews can remove established products while delaying new registrations critical for resistance management strategies. The agency's REV2024-01 work plan for 2024-2029 outlines comprehensive re-evaluations that prioritize environmental sustainability and human health protection, potentially restricting access to conventional chemistry options [4]Source: Health Canada, “REV2024-01 Re-Evaluation Work Plan,” canada.ca. Statistics Canada data indicate pesticide active ingredient registrations declined 12% from 2020 to 2024, while re-evaluation completion times increased by an average of 8 months, demonstrating the regulatory constraints' measurable impact on market dynamics [5].Source: Statistics Canada, “Pesticide Sales, 2025,” statcan.gc.ca

Accelerating Consumer Preference For Organic Produce

Canadian retailers are implementing increasingly stringent pesticide residue thresholds in response to consumer demand for organic and reduced-chemical food products, constraining conventional agrochemical applications while creating premium market opportunities for specialty formulations. Statistics Canada reported organic farmland increased 3.8% to 1.36 million hectares in 2024, representing 2.9% of total agricultural land, with organic sales reaching USD 4.2 billion (CAD 5.7 billion) annually.The preference evolution also creates market segmentation opportunities, as premium pricing for organic and reduced-chemical products can offset volume declines in conventional segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialty Formulations Drive Premium Growth

Fertilizers hold a 64.62% market share in 2025, driven by precision nutrition and specialty formulation strategies. According to Statistics Canada, nitrogen fertilizer consumption reached 2.8 million metric tons in 2024, accounting for 58% of total fertilizer usage. Phosphate consumption was 1.1 million metric tons, while potash consumption reached 0.9 million metric tons. Pesticides constitute the second-largest category, with herbicide demand focused on broadleaf weed resistance management, particularly in canola systems where kochia and wild oat control necessitates multiple modes of action. Adjuvants show strong growth due to precision application technologies requiring enhanced active ingredient performance. Micronutrient blends are gaining importance as climate-resilient crop genetics show increased zinc and boron requirements.

Micronutrient fertilizers are growing at an 7.74% CAGR, emerging as the fastest-growing fertilizer subsegment. This growth stems from precision agriculture, enabling targeted application of zinc, boron, and manganese formulations to optimize crop quality and yield stability. The segment's evolution indicates that specialty formulations provide differentiation opportunities in commoditized chemical markets, though adoption varies by crop type and regional farming practices.

By Application: Specialty crops accelerate demand

Grains and cereals hold a 47.55% market share in 2025, as specialty crop expansion and precision horticulture adoption reshape input demand patterns across Canadian agriculture. This dominance reflects Canada's position as a major wheat and canola exporter, requiring intensive herbicide use for weed resistance management and fungicide applications for storage quality optimization. Statistics Canada reports that grain and oilseed production accounts for 78% of total pesticide applications in 2024, with herbicides comprising 65% of total active ingredient usage across these crops.

Pulses and oilseeds constitute the second-largest application segment, driven by crop rotation benefits and export market premiums that support higher per-acre input investments. Turf and ornamental grass applications, despite lower volumes, generate premium pricing through specialized formulations that meet urban and recreational environmental standards. The fruits and vegetables segment shows the highest growth rate at 5.51% CAGR through 2031. This growth is driven by greenhouse expansion and precision horticulture adoption, particularly in Ontario and British Columbia, where controlled environment agriculture enables intensive input applications with precise monitoring. The evolution of application segments reflects agricultural diversification as farmers transition to higher-value crops that support premium input investments while meeting market quality requirements.

Geography Analysis

Western Canada accounts for approximately two-thirds of agrochemical expenditure. Saskatchewan's contribution stems from 18 million metric tons of planned potash production by 2025 and extensive canola acreage requiring multiple herbicide applications. Alberta shows increased adoption of split-application nitrogen practices and maintains the country's largest area under 4R certification. Manitoba benefits from diverse crop rotations and strategic warehouse locations that facilitate the delivery of spring inputs.

Ontario's greenhouse complexes near the United States border require high-purity foliar nutrients and specialized plant growth regulators. The province leads in variable-rate technology implementation, with 42% of farmers utilizing zone maps. Quebec's strict drift buffer regulations and language-specific labeling requirements extend product launch timelines but create opportunities for specialty formulations that address environmental concerns.

British Columbia's year-round climate-controlled environment supports the growth of produce exports, while Atlantic potato production relies on soil fumigants and nematicides. The Prince Rupert corridor expansion aims to double container capacity, though rail congestion affects potash and bulk glyphosate shipments to Asia-Pacific markets. These regional variations influence inventory management strategies for wholesalers in the Canadian agrochemicals market.

Competitive Landscape

The Canadian agrochemicals market maintains a moderate concentration, with five major players, including Nutrien Ltd, Bayer AG, Syngenta Group, BASF SE, and Corteva Agriscience are dominating through their extensive R&D capabilities and nationwide retail networks. These companies focus their investments on research and development to expand product portfolios, particularly in sustainable and bio-based solutions. They compete through product innovation, regularly introducing new formulations for specific crops and pest management needs. The industry has seen an increase in strategic partnerships, particularly in distribution and technology development. Companies have expanded into digital agriculture, offering integrated solutions that combine traditional products with precision farming tools and data-driven advisory services. To improve supply chain control and market responsiveness, significant investments have been made in local manufacturing and formulation facilities.

Companies differentiate themselves through the deployment of technology, investing in precision agriculture platforms, specialty chemical integration, and digital distribution channels. Regulatory compliance capabilities provide competitive advantages, particularly for companies that successfully navigate Health Canada's pesticide re-evaluation processes while maintaining product registrations that address farmer resistance management needs.

The market structure remains moderate concentration, with multinational corporations maintaining market power through established brands and distribution networks. These global entities use their international research capabilities and technological expertise to maintain market advantages. Local players operate primarily in niche segments or serve as distributors for global manufacturers. High entry barriers, including strict regulatory requirements and substantial R&D investment needs, strengthen the position of established companies.

The market has experienced strategic mergers and acquisitions focused on portfolio expansion and market consolidation. These transactions target complementary product lines, regional presence enhancement, and access to new technologies, particularly in biological products. Companies pursue vertical integration to control value chain components from manufacturing to distribution, while developing specialized capabilities in precision agriculture and digital farming solutions.

Canada Agrochemicals Industry Leaders

Nutrien Ltd

Bayer AG

BASF SE

Syngenta Group

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Syngenta Group has launched CAZADO, the first dual-mode wild oat herbicide for Canadian wheat growers, combining pinoxaden and thiencarbazone-methyl to combat herbicide-resistant wild oats. After seven years of development, CAZADO is now available, with national and international expansion planned.

- January 2025: Genesis Fertilizers partnered with Stamicarbon to build a low-carbon nitrogen complex in Saskatchewan using NX STAMI urea technology, slated for 2029 start-up.

- November 2023: Syngenta Group launched Cruiser Maxx Vibrance Potato, a fungicide and insecticide seed treatment containing fludioxonil, thiamethoxam, difenoconazole, and sedaxane, to combat a broad spectrum of yield-inhibiting pests.

- September 2023: Sollio Agriculture, the Agri-business Division of Sollio Cooperative Group, inaugurated CRF Agritech, a new controlled-release fertilizer production plant in St. Thomas, Ontario. The 25,800-square-foot facility required an investment of over USD 18.5 million.

Canada Agrochemicals Market Report Scope

Agrochemicals are chemical products comprised of fertilizers, plant-protection chemicals or pesticides, and plant-growth hormones used in agriculture. Canada Agrochemicals Market is Segmented by Product Type (Fertilizer, Pesticides, Adjuvants, and Plant Growth Regulators) and Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Turfs and Ornamental Grass). The report offers market size and forecasts in terms of Value (USD) and Volume (Metric Tons).

By Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Micronutrient Blends | |

| Other Fertilizers | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Plant Growth Regulators | |

| Adjuvants |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Turf and Ornamental Grass |

| By Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Micronutrient Blends | ||

| Other Fertilizers | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Plant Growth Regulators | ||

| Adjuvants | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Turf and Ornamental Grass | ||

Key Questions Answered in the Report

What is the current value of the Canada agrochemicals market?

The market was valued at USD 10.17 billion in 2026 and is forecast to hit USD 12.27 billion by 2031.

Which segment is growing fastest in Canada's agrochemical mix?

Plant growth regulators are projected to grow at a 6.54% CAGR through 2031, the highest among all product types.

How dominant are fertilizers in Canadian input spending?

Fertilizers captured 64.62% of 2025 revenue and remain the backbone of crop input budgets.

What is the biggest regulatory headwind for agrochemical suppliers?

Health Canada intensified re-evaluation schedule creates uncertainty and potential delisting risk for several legacy actives.

Page last updated on: