Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

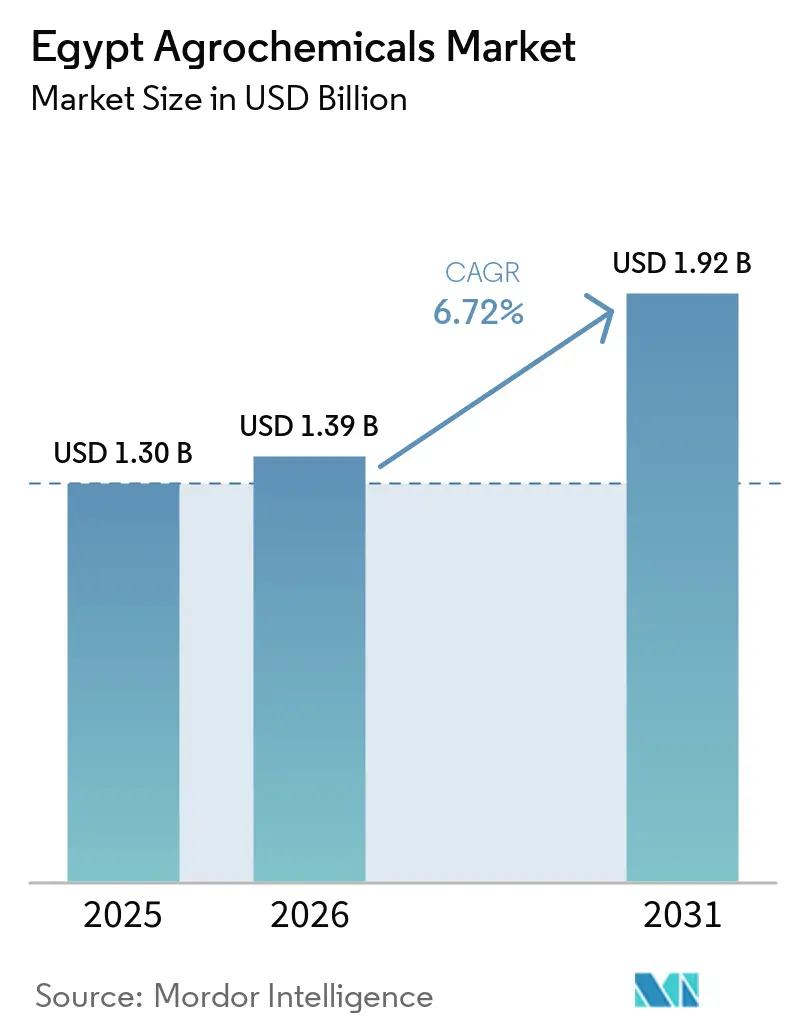

| Base Year Market Size (2025) | USD 1.30 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Agrochemicals Market Analysis by Mordor Intelligence

Egypt agrochemicals market size was valued at USD 1.30 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.92 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). Rising population, limited arable land, and the government’s large-scale reclamation schemes are the prime factors boosting demand for fertilizers, pesticides, and specialty adjuvants across the Egyptian agrochemicals market. Input intensity is climbing fastest in newly irrigated desert corridors where drip systems and saline water require tailored formulations. Concurrently, export incentives for citrus, grapes, and greenhouse vegetables increase the need for compliant pest-control chemistry that meets strict European residue tolerances. The growing deployment of satellite-enabled decision-support tools, together with the rapid adoption of fertigation, is enabling more precise nutrient and crop-protection applications, supporting the Egypt agrochemicals market’s shift toward higher-value specialty inputs.

Key Report Takeaways

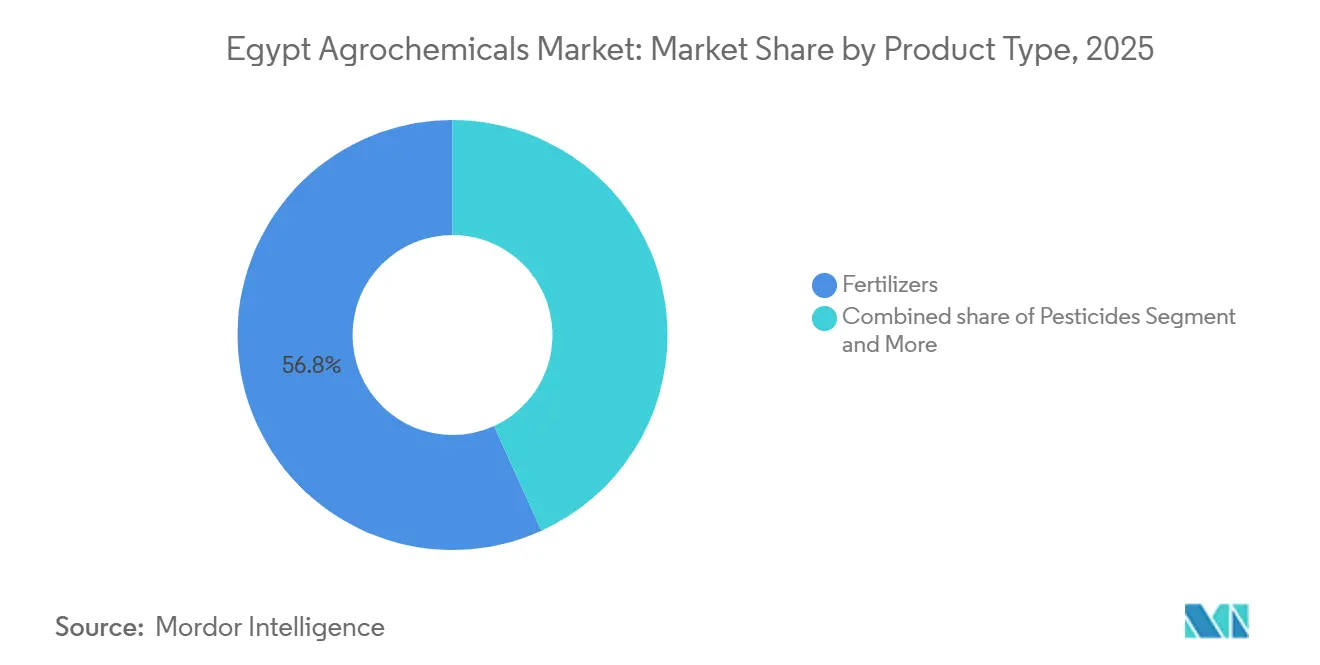

- By product type, fertilizers were the largest segment, holding 56.8% of the Egypt agrochemicals market share in 2025, and adjuvants are the fastest-growing segment, forecast to expand at a 7.8% CAGR through 2031.

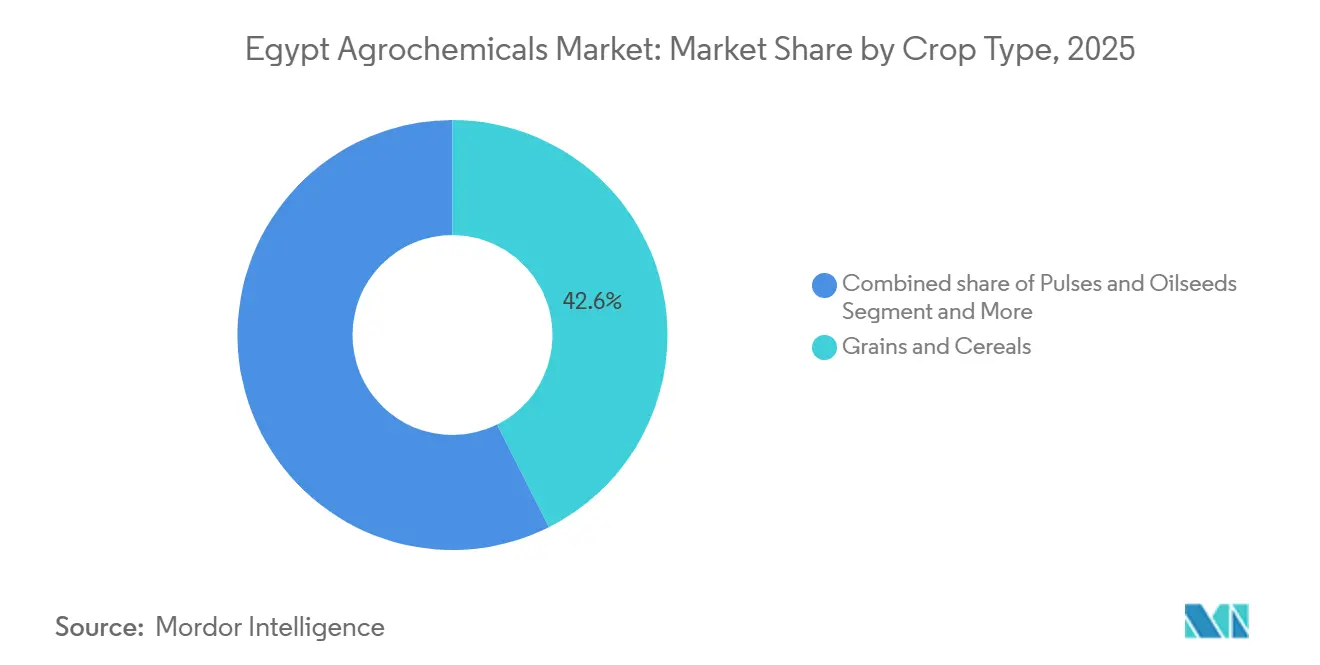

- By crop type, grains and cereals were the largest segment, accounting for 42.6% of the Egypt agrochemicals market size in 2025. Fruits and vegetables are the fastest-growing segment, projected to grow at a 6.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decreasing arable land is intensifying input demand | +1.2% | National with acute pressure in the Nile Delta and Valley | Long term (≥ 4 years) |

| Desert-reclamation megaprojects expanding treated hectares | +1.8% | Western Desert Corridors, Upper Egypt, Sinai, Suez, and Canal | Medium term (2-4 years) |

| Rapid fertigation and liquid-fertilizer adoption | +1.1% | National early gains in Western Desert Corridors and Greater Cairo | Medium term (2-4 years) |

| Government export-rebate program for high-value crops | +0.9% | National concentrated in the Nile Delta and coastal zones | Short term (≤ 2 years) |

| Pivot to climate-smart drip-ready nutrient blends | +0.7% | Western Desert Corridors and Upper Egypt | Long term (≥ 4 years) |

| Satellite-enabled pest-pressure alerts | +0.5% | National pilots in the Nile Delta and the Western Desert | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Decreasing Arable Land Intensifying Input Demand

According to the World Bank, Egypt’s per capita availability of agricultural land has steadily declined over the past two decades. In 2022, agricultural land availability was 3.4 hectares per capita, and it further decreased to 3.3 hectares in 2023, underscoring the need for productivity-driven input demand[1]Source: World Bank, “Agricultural Land (Hectares Per Capita) – Egypt,” World Bank Data, data.worldbank.org. This structural pressure has directly increased the demand for yield-enhancing agrochemicals, including specialty fertilizers, micronutrients, and crop protection products. Farmers are addressing land scarcity by increasing input intensity. Fertilizer application rates in Egypt remain above the African average, reflecting this intensification. Given that Egypt’s cultivable land accounts for only a small proportion of its total land area, farmers are compelled to maximize yields per feddan by increasing the use of agrochemicals. This necessity drives up nitrogen application rates, particularly for winter cereals, and increases the demand for foliar micronutrients to address nutrient deficiencies in soils depleted by continuous cropping.

Rapid Fertigation and Liquid-Fertilizer Adoption

Egypt's increasing use of drip irrigation systems in reclaimed desert areas has driven the adoption of fertigation practices. Liquid fertilizers designed for compatibility with irrigation systems are gaining market share, particularly in horticulture and export-oriented crops. Fertigation, which involves injecting soluble nutrients through drip lines, is becoming more popular due to its ability to reduce labor, minimize nutrient runoff, and enable real-time nutrient adjustments based on crop phenology. Liquid NPK formulations and water-soluble powders, which are compatible with inline dosing systems, command a significant price premium over granular alternatives. Despite this, their adoption is growing among commercial vegetable growers in the Western Desert, who focus on export windows for crops such as bell peppers and cherry tomatoes, thereby driving market growth.

Government Export-Rebate Program for High-Value Crops

Egypt is increasing its agricultural exports, focusing on citrus, grapes, and vegetables. Export-oriented production necessitates stricter pest management practices and the use of high-quality crop protection inputs to comply with international standards. These export crops demand higher-value agrochemical inputs, and residue-compliant pesticides, thereby contributing to market value growth. The government is supporting export-driven agriculture through financial incentives and improved logistics. The Investment and Foreign Trade Minister, along with Finance Minister Ahmed Kouchouk, has outlined the details of Egypt’s new export subsidy rebate program for the fiscal year 2025/2026. This policy encourages growers to implement integrated pest management protocols that combine biological controls, pheromone traps, and selective insecticides, thereby increasing per-hectare crop protection spending for export-focused farms.

Pivot to Climate-Smart Drip-Ready Nutrient Blends

Reclaimed desert soils often exhibit high electrical conductivity, typically exceeding 4 deciSiemens per meter. This limits root absorption of conventional fertilizers, necessitating the use of low-salt formulations designed for saline irrigation water. These specialty blends are priced significantly higher than standard NPK fertilizers. Their adoption is increasing among corporate farms in the Western Desert Corridors. These farms operate under strict water budgets and aim to prevent yield losses caused by micronutrient deficiencies. Climate variability, water scarcity, and increasing salinity are driving the adoption of climate-smart agricultural inputs, such as controlled-release fertilizers and salinity-tolerant nutrient blends. Egypt’s Ministry of Agriculture supports climate adaptation strategies as part of the national climate plans. Under Egypt’s National Climate Change Strategy 2050, agriculture is identified as a priority sector for enhancing climate resilience, which is boosting demand for specialty agrochemical formulations designed for stress mitigation and water-efficient systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter European Union residue-tolerance limits on exports | -0.8% | National acute in Delta citrus and vegetables | Short term (≤ 2 years) |

| Natural-gas-linked ammonia price volatility | -1.1% | National stronger in nitrogen-heavy cereals | Medium term (2-4 years) |

| Counterfeit pesticide trade via informal channels | -0.6% | National prevalent in Upper Egypt and rural Delta | Medium term (2-4 years) |

| Rising soil-salinity-induced micronutrient lock-out | -0.5% | Western Desert Corridors, Sinai, Upper Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Europe Union Residue-Tolerance Limits on Exports

The European Union is Egypt's primary export destination for citrus and vegetables. Stricter Maximum Residue Limits (MRLs) under the Europe Union Rapid Alert System for Food and Feed (RASFF) have increased compliance costs for Egyptian exporters. Rejected consignments result in financial losses and compel exporters to use higher-cost, premium pesticides. This situation reduces affordability for smaller growers and puts pressure on profit margins. In 2025, Egypt recorded 131 interceptions, including 83 for fruits and vegetables and 26 for citrus. In 2024, a record 180 interceptions were reported, with 86 for fruits and vegetables and 34 for citrus. Over a five-year period, Egypt registered 672 detections. According to the Valencian Association of Farmers (AVA-ASAJA), Egyptian oranges intercepted in Italy contained 0.21 mg/kg of chlorpropham, a herbicide and growth regulator banned in the Europe Union since 2019, exceeding the allowed maximum residue limit (MRL) by up to 21 times, thereby impacting the market[2]Source: Valencian Association of Farmers, “Excessive Chlorpropham Detected in Egyptian Oranges Imported Into Italy,” AVA-ASAJA, ava-asaja.org.

Natural-Gas-Linked Ammonia Price Volatility

Egypt's nitrogen fertilizer production is heavily reliant on natural gas. Price reforms and global gas market volatility directly impact ammonia production costs. Domestic subsidy reforms have led to increased cost pass-through to fertilizer producers. This volatility disrupts stable pricing, affecting farmers' affordability and altering agrochemical consumption patterns. Ammonia spot prices in the Mediterranean basin rose in 2025, driven by fluctuations in European demand and supply disruptions in the Black Sea region. These factors contribute to urea price volatility, which reduces farmers' purchasing power, particularly when subsidy support is insufficient. Smallholders cultivating less than 3 feddans, who constitute a significant portion of Egypt's Agriculture population, often delay nitrogen applications during price surges to avoid incurring debt.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Adjuvants Lead Specialty Surge

Fertilizers were the largest segment, holding 56.8% of the Egypt agrochemicals market share in 2025, reflecting Egypt's status as a net grain producer reliant on nitrogen-intensive wheat and rice rotations. In the fertilizer segment, nitrogenous products dominate, with urea serving as the primary nitrogen source for cereal crops. Phosphatic and potassic fertilizers are primarily used in niche applications, such as vegetable and fruit production. In 2024, the Misr Fertilizers Production Company in Egypt allocated USD 890 million to a green ammonia production facility in Damietta, Egypt. In these systems, improved rainfastness reduces the need for reapplications, resulting in lower herbicide costs per hectare[3]Source: Misr Fertilizers Production Company, “MOPCO Allocates USD 890 Million for Damietta Green Ammonia Facility,” MOPCO Press Release, mopco-eg.com.

Adjuvants are the fastest growing segment, projected to expand at a CAGR of 7.8% through 2031, the highest in the Egypt agrochemicals market. Demand is rising as Egyptian growers focus on improving spray efficiency, reducing input wastage, and optimizing pesticide performance under arid and water-stressed conditions. Increasing awareness of cost-effective crop protection practices and the need to comply with tightening residue regulations are further supporting adoption

By Crop Type: Cereals Lead, Horticulture Grows Fastest

Grains and cereals were largest segment, accounted for 42.6% of the Egypt agrochemicals market size in 2025, owing to intensive wheat and rice rotations subsidized by state procurement. Rice cultivation, despite restrictions aimed at conserving water, continues to cover 1.1 million feddans in the Nile Delta. Herbicides such as penoxsulam are commonly used to manage barnyard grass and aquatic weeds. Cereals are susceptible to pest infestations and require effective crop protection to sustain high yields. Adjuvants play a crucial role in improving the effectiveness of herbicides and pesticides applied to these crops. This is especially significant as cereals constitute a substantial portion of the total agricultural land in Egypt.

Fruits and vegetables are the fastest-growing segment, projected to grow at a 6.7% CAGR through 2031, powered by European and Gulf demand. Greenhouse vegetable production, primarily located in Greater Cairo and coastal regions, utilizes drip fertigation and climate-control systems to enable year-round cultivation. This results in agrochemical expenditures per hectare that are 2 to 3 times higher than those of open-field systems. Turf and ornamental plants, catering to golf courses, public parks, and landscaping projects associated with new urban developments, represent a niche market. They demonstrate consistent demand for specialty herbicides and growth regulators to maintain their aesthetic quality.

Geography Analysis

Greenhouse clusters in Greater Cairo implement weekly fertigation using water-soluble NPK fertilizers and micronutrients. The controlled environment within these greenhouses necessitates more frequent pesticide applications. Meanwhile, projects in the Western Desert and Toshka regions use low-salt fertilizers tailored for alkaline soils, underscoring the need for desert-corridor distribution hubs to meet logistical demands.

The Nile Delta and Valley continue to account for over two-thirds of total agricultural input sales. The growth corridors in the Western Desert are experiencing double-digit annual expansion, setting a new pace for market development. Soil-salinity mapping indicates that 87.5% of irrigation-water samples in the northeastern Delta fall into categories that severely limit agricultural productivity. This has increased demand for inputs such as gypsum, elemental sulfur, and chelated micronutrients. In Upper Egypt, the Luxor-Aswan belt is gaining importance as large-scale irrigation systems reach newly cultivated areas, supported by public-private investments in pump stations and subsurface drip irrigation infrastructure.

Groundwater quality is a critical factor influencing input strategies. In the Nile Valley, concerns over aquifer depletion are driving demand for water-holding soil polymers. Variations in soil salinity, water quality, and cropping systems across regions are fragmenting the market. This fragmentation is prompting suppliers to adapt their product portfolios and distribution strategies to meet specific local agronomic conditions, rather than relying on uniform formulations.

Competitive Landscape

The Egypt agrochemicals market is moderately fragmented, with the top five suppliers, including BASF SE, Bayer CropScience Ltd., UPL Limited, Corteva Agriscience, and Syngenta Group Co., Ltd. are accounting for a significant portion of the market share. Multinationals differentiate via digital agronomy portfolio, while domestic producers leverage subsidized gas allocations and geographic proximity.

Technology adoption is becoming a competitive differentiator, with companies deploying agronomist networks, mobile apps, and soil-testing services to build grower loyalty beyond product efficacy. Field studies indicate a 75% probability of uptake for subsurface drip under high water-cost scenarios, driving bundled sales of pressure-compensated emitters and fertigated nutrient blends. As retailers integrate satellite diagnostics and mobile e-commerce, last-mile reach into Upper Egypt and New Valley zones is improving, narrowing the service gap for smallholders.

Opportunities are emerging in adjuvants and micronutrient chelates of a potential addressable market but growth. Smaller contenders such as Evergrow Fertilizers and Indofil Industries are gaining share by offering water-soluble NPK blends and drip-compatible formulations at prices high multinational equivalents, appealing to cost-conscious greenhouse operators and export-oriented vegetable growers. On the crop-protection front, regulatory tightening encourages portfolio shifts toward low-residue actives suppliers with advanced R&D pipelines stand to gain share as Europe Union standards tighten.

Egypt Agrochemicals Industry Leaders

BASF SE

Bayer CropScience Ltd.

UPL Limited

Corteva Agriscience

Syngenta Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Syngenta and Al Dahra implemented Cropwise Operations across 220,000 acres in Egypt, Romania, Serbia, and Morocco, incorporating real-time agronomic analytics. This initiative is projected to contribute significantly to the development of the Egypt agrochemicals market by enhancing farming practices and optimizing crop yields.

- March 2025: Egypt’s Agriculture Ministry signed a soil-fertilizer plant deal with Saudi Green Company for Agricultural Development in Nubaria.

- July 2024: The Misr Fertilizers Production Company (MOPCO) partnered with Scatec, a Norwegian Company, to build a green ammonia production plant that produces 150 thousand metric tons in Damietta, Egypt. The Egyptian government supported the project and invested USD 10 million.

Egypt Agrochemicals Market Report Scope

Agrochemicals are chemical products used in agriculture to enhance crop productivity and protect plants from pests, diseases, and weeds. They include fertilizers, pesticides such as insecticides, herbicides, and fungicides, plant growth regulators, and soil conditioners that help improve yield quality and farm efficiency.

The report on the Egypt agrochemicals market analyzes the industry across key product categories such as fertilizers, pesticides, adjuvants, and plant growth regulators. It further evaluates demand across major crop segments, including grains and cereals, pulses and oilseeds, fruits and vegetables, and turf and ornamentals. Market estimates and forecasts are presented in value terms expressed in USD.

By Product Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

By Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Turf and Ornamentals |

| By Product Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Crop Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

Key Questions Answered in the Report

What is the forecast value of the Egypt agrochemicals market by 2031?

The Egypt agrochemicals market is estimated to grow from USD 1.39 billion in 2026 to USD 1.39 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031).

Which product category dominates spending today?

Fertilizers account for 56.8% of the market share in 2025, led by nitrogenous formulations applied to wheat and rice.

Which segment is growing the fastest?

Adjuvants are projected to post a 7.8% CAGR through 2031 as growers use surfactants and drift-control agents to improve active-ingredient performance.

Why are Western Desert Corridors important for suppliers?

Desert-reclamation megaprojects such as the New Delta will add millions of irrigated feddans, creating new demand for saline-tolerant fertilizers and precision herbicides.

Page last updated on: