Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.7 Billion |

| Market Size (2026) | USD 12.21 Billion |

| Market Size (2031) | USD 15.08 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

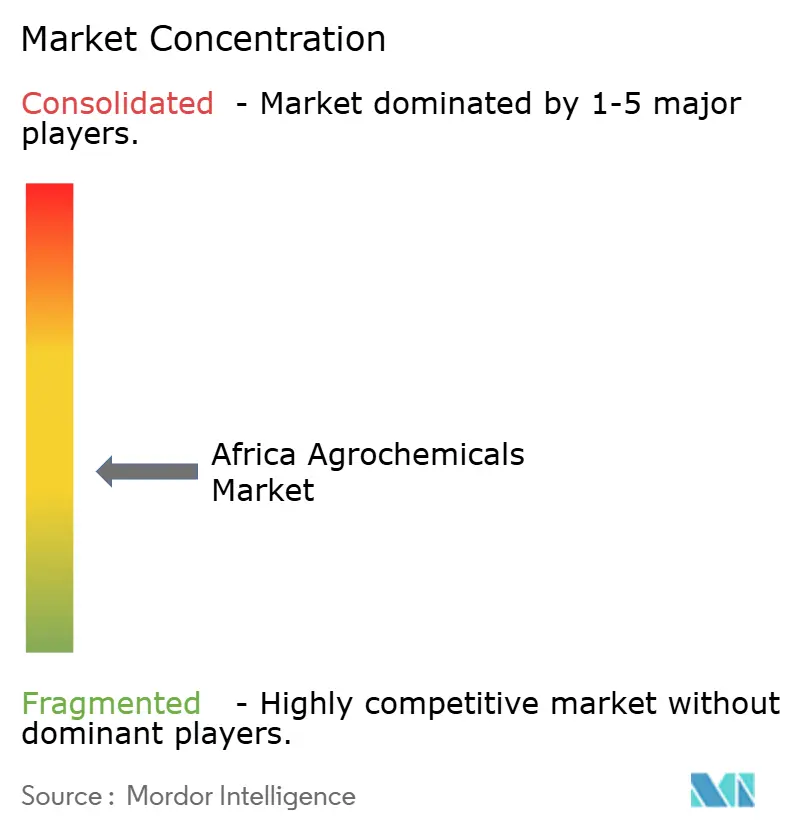

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Agrochemicals Market Analysis by Mordor Intelligence

The Africa agrochemicals market size is expected to grow from USD 11.7 billion in 2025 to USD 12.21 billion in 2026 and is forecast to reach USD 15.08 billion by 2031 at 4.32% CAGR over 2026-2031. Fertilizers held the largest share of the market in 2024, supported by widespread soil nutrient depletion across Africa. Plant growth regulators have emerged as the fastest-growing segment, as farmers increasingly adopt precision application methods[1]African Union Commission, “Statement at Africa Fertilizer and Soil Health Summit,” au.int. The market growth is supported by increasing pest challenges, growing food demand from population expansion, and government subsidy programs that improve access for smallholder farmers. High input costs and inconsistent regulations across regions limit efforts to close the agricultural yield gap. Market participants are establishing local manufacturing facilities, developing innovative distribution networks, and creating sustainable product lines with precision chemical solutions. Additionally, governments are expanding warehouse-receipt financing systems and mechanization support programs, which drive increased demand in the agrochemicals market.

Key Report Takeaways

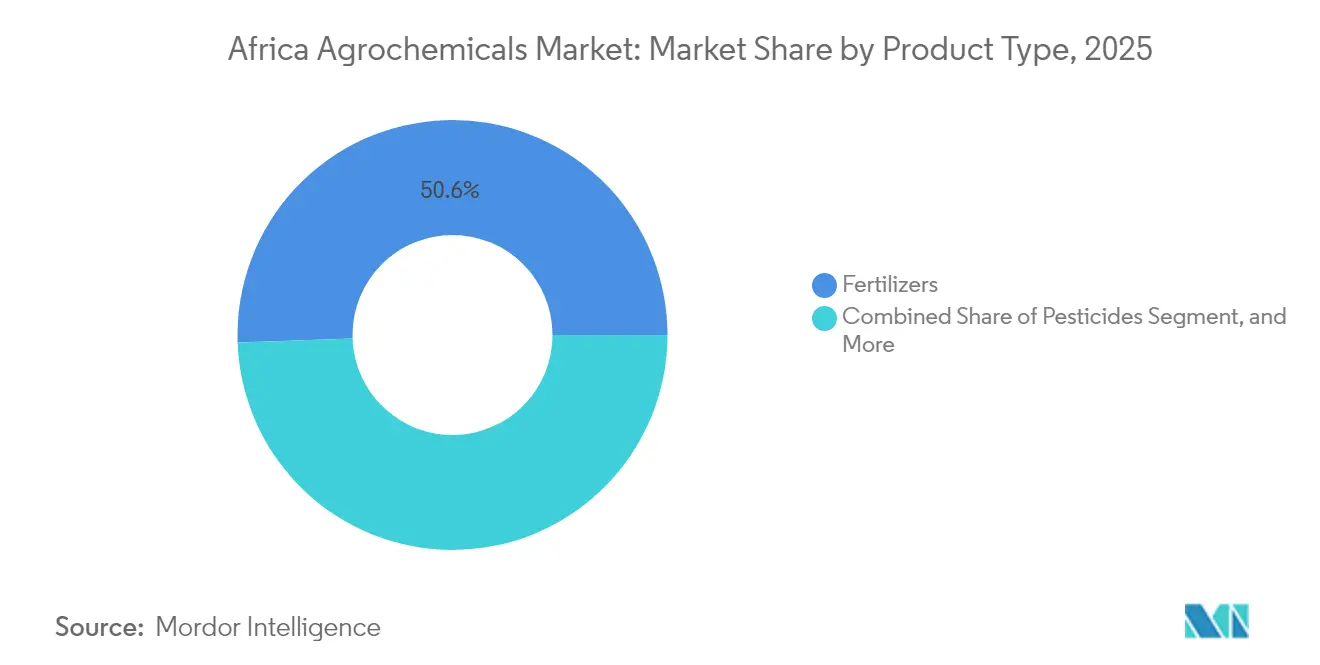

- By product type, fertilizers commanded 50.55% of the Africa agrochemicals market share in 2025, and plant growth regulators posted the highest 6.8% CAGR for 2026-2031.

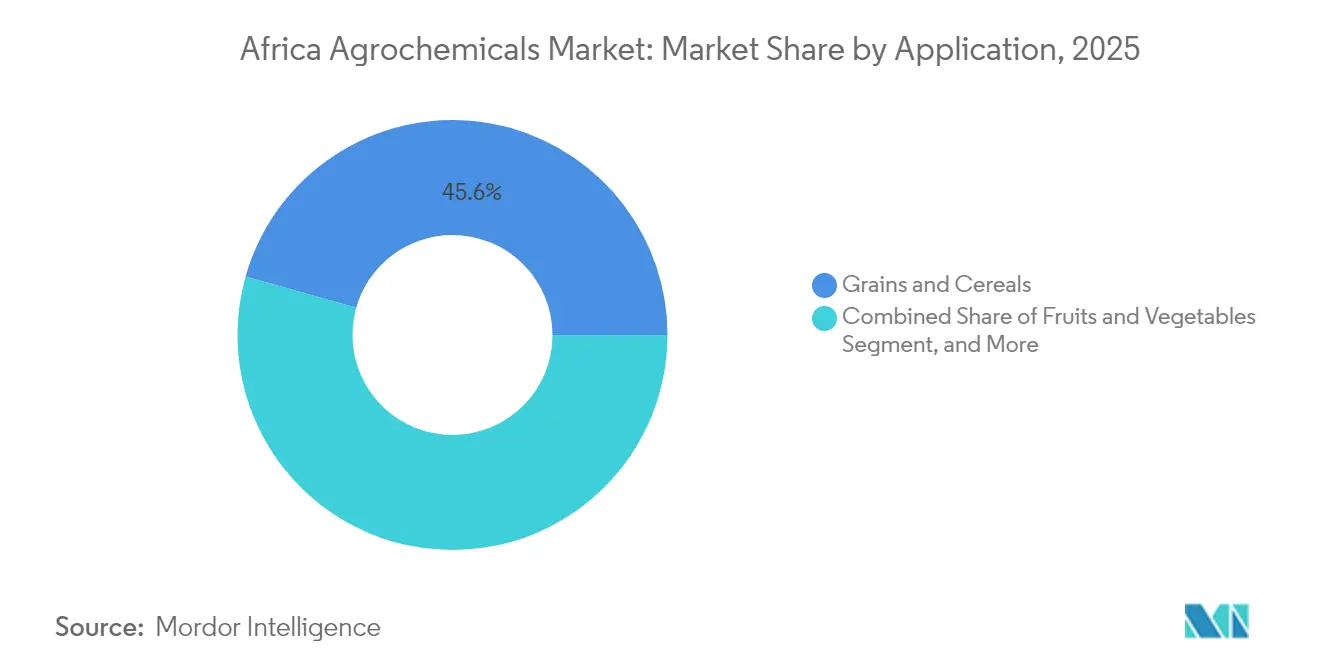

- By application, grains and cereals accounted for a 45.62% share of the Africa agrochemicals market size in 2025, and fruits and vegetables are advancing at a 5.69% CAGR for 2026-2031.

- By geography, South Africa led with an 17.72% revenue share in 2025, while Ethiopia is growing at a 6.49% CAGR to 2031.

- Major Players Bayer AG, BASF SE, Corteva Agriscience, UPL Limited, and Syngenta Group together held 44.2% of the market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate‐driven Rise in Pest and Disease Pressure | +1.2% | East and West Africa | Medium term (2-4 years) |

| Population Growth Accelerating Food-demand Gap | +0.9% | Nigeria, Ethiopia, and Tanzania | Long term (≥ 4 years) |

| Government Subsidy Programs for Fertilizer and Pesticide Adoption | +0.8% | Nigeria, Kenya, Ghana, and Morocco | Short term (≤ 2 years) |

| Mechanization and Precision-ag Adoption Boosting Agrochemical Efficiency | +0.6% | South Africa, Kenya, and Morocco | Medium term (2-4 years) |

| Expansion of Warehouse-receipt Financing Unlocking Working-capital for Inputs | +0.5% | Ghana, Kenya, and Tanzania | Medium term (2-4 years) |

| Emergence of Private-label Agro-retail Chains Improving Last-mile Distribution | +0.4% | Urban-adjacent zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate‐driven Rise in Pest and Disease Pressure

Variable weather patterns have increased the spread of invasive pests like fall armyworm across multiple African nations, significantly impacting maize yields. Striga weed infestations in cereal-growing regions continue to affect harvests, leading farmers to implement integrated chemical control programs. Kenya, Ghana, and Ethiopia have established emergency response protocols, while regional organizations coordinate pest surveillance networks. Agricultural companies have accelerated the development of precision insecticides targeting pest larvae, and digital monitoring platforms provide real-time alerts to farmers. These factors drive sustained growth in the Africa agrochemicals market. The market gains additional momentum through investments in seed treatment chemicals and farmer education programs. Public-private partnerships are improving farmer access to new crop protection solutions.

Population Growth Accelerating Food-demand Gap

Agricultural productivity remains limited as smallholder farmers use agrochemicals below recommended levels. Nigeria, Ethiopia, and Tanzania experience significant constraints due to urban migration, reducing the agricultural workforce. Government initiatives include investments in domestic fertilizer production and irrigation infrastructure to improve yields. Ethiopia's irrigation expansion program focuses on increasing lowland productivity and decreasing import dependence. Growing food demand continues to drive the African agrochemicals market for fertilizers, pesticides, and plant growth regulator products. The expansion of agricultural dealer networks and mobile advisory services helps improve farmers' access to inputs and knowledge. Farmers increasingly adopt climate-resilient agrochemical solutions to address changing weather conditions.

Government Subsidy Programs for Fertilizer and Pesticide Adoption

Nigeria's Growth Enhancement Support Scheme provided subsidized fertilizer to farmers, while Kenya's Africa Fertilizer Financing Mechanism increased fertilizer access across its farming population. Tanzania implemented a credit guarantee system that facilitated fertilizer trade and improved supply chain efficiency. The implementation of digital e-voucher systems and mobile wallets reduced distribution inefficiencies and shortened delivery times. The 2024 Africa Fertilizer and Soil Health Summit action plan strengthened these initiatives, driving demand in the Africa agrochemicals market. The improved transparency in distribution networks attracted private investment, while the harmonization of regional input standards facilitated cross-border trade.[2]African Development Bank, “Kenya Fertilizer Financing Mechanism,” afdb.org

Expansion of Warehouse-receipt Financing Unlocking Working-capital for Inputs

Ghana, Kenya, and Tanzania operate warehouse-receipt systems that enable farmers to use stored crops as collateral for loans, helping manage cash flow between harvest and planting seasons. Banks accept graded maize, sorghum, and rice as security, providing farmers with funds to purchase crop protection products. This system reduces rural interest rates, increases sales for agricultural agrochemicals retailers, and minimizes post-harvest losses, contributing to consistent growth in the African agrochemicals market.[3]World Bank Staff, “Can Warehouse Receipts Unlock Farmer Finance?” worldbank.org The warehouse-receipt systems enhance price transparency and promote formal market participation among small-scale farmers. Their growing adoption strengthens the connection between farmers, financial services, and agricultural agrochemicals supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Agrochemical Prices Unaffordable to Smallholders | -1.1% | Landlocked nations | Short term (≤ 2 years) |

| Fragmented and Stringent Regulatory Approval Timelines | -0.7% | Nigeria, South Africa, Kenya | Medium term (2-4 years) |

| Proliferation of Counterfeit Agrochemicals Eroding Farmer Trust | -0.6% | West and East Africa | Medium term (2-4 years) |

| Organic and Residue-free Export Crop Programs Curbing Synthetic Usage | -0.3% | Morocco, South Africa, Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Agrochemical Prices Unaffordable to Smallholders

Transport costs in landlocked countries account for up to 50% of final retail prices, while Ethiopia experienced significant increases in fertilizer prices in recent years. Kenya's proposed 16% VAT on agrochemicals through the 2025 Finance Bill may substantially increase production costs. Nigeria's record-high food inflation in mid-2024 forced households to spend most of their income on food, reducing funds available for farm investments. Farmers often turn to informal lenders charging high weekly interest rates, creating debt cycles that limit growth in the Africa agrochemicals market. The resulting affordability issues reduce the adoption of effective crop protection products, leading to suboptimal yields and continued food security challenges.

Fragmented and Stringent Regulatory Approval Timelines

Extended registration periods of over two years in South Africa and Nigeria, due to outdated pesticide laws and limited institutional capacity, delay the introduction of new agricultural chemicals. The underutilization of regional mutual-recognition frameworks stems from inconsistent data-review procedures among national authorities. These regulatory challenges increase compliance costs, encourage unauthorized imports, and restrict new product launches in the Africa agrochemicals market. The resulting limited competition delays the adoption of environmentally sustainable formulations. Enhanced regulatory efficiency could facilitate regional coordination and improve access to advanced agrochemical solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fertilizers Drive Market Foundation

Fertilizers held 50.55% of the Africa agrochemicals market share in 2025, addressing widespread soil nutrient deficiencies and supporting agricultural productivity across various agroecological zones. Nitrogen-based formulations remain essential for cereal production, while phosphatic and potassic fertilizers gain adoption through balanced nutrition programs. Digital subsidy e-vouchers and warehouse-receipt credit systems reduce financial barriers and enable timely fertilizer application.

Plant growth regulators demonstrate a 6.8% CAGR, driven by increased adoption of nutrients that improve stress tolerance, root development, and yield potential. Pesticides maintain significant volume across Africa, with herbicides dominating due to labor shortages and resistant weed populations. Insecticide demand increases in response to climate-related pest outbreaks, while fungicide use expands in horticultural regions. Adjuvants, though a smaller segment, grow in importance as precision spraying equipment requires advanced formulations for improved leaf coverage and simplified tank mixing.

By Application: Grains and Cereals Anchor Demand

Grains and cereals represented 45.62% of the Africa agrochemicals market size in 2025, reflecting their importance in food security and rural economies. Fertilizer and herbicide use concentrates in maize and sorghum production areas, supported by government mechanization programs and climate insurance schemes. Pulses and oilseeds integration into crop rotations provides farmers with income diversification while enhancing soil fertility through nitrogen fixation, supporting balanced fertilizer use.

The fruits and vegetables segment, growing at 5.69% CAGR, transforms peri-urban supply chains and increases demand for precision insecticides and specialty foliar nutrients. Export markets require compliance with residue-free standards, driving adoption of environmentally compatible agrochemicals. Premium pricing for quality produce encourages controlled-environment agriculture and drip-fertigation systems. Commercial crops, including sugarcane and cotton, maintain consistent pesticide demand through large-scale farming and organized procurement systems, highlighting agrochemicals' importance across different cultivation methods.

Geography Analysis

South Africa contributed 17.72% of Africa's agrochemicals market share in 2025, supported by advanced logistics networks, research extension services, and credit systems. Following drought-related declines in 2024, improved reservoir levels and stable power supply are enhancing horticultural prospects for 2025, driving increased fertilizer and pesticide demand. The potato sector demonstrates successful input optimization, achieving improvements in production and exports. However, outdated pesticide regulations delay new product registrations, though planned regulatory updates may accelerate innovation adoption.

Ethiopia exhibits the highest growth rate in Africa's agrochemicals market at 6.49% CAGR, supported by government initiatives for fertilizer independence through strategic partnerships and local ammonia production. The Grand Ethiopian Renaissance Dam's irrigation projects are expanding lowland agricultural capabilities. The agricultural sector's significance in Ethiopia's economy and employment drives sustained public investment in agrochemical accessibility. Improvements in infrastructure and multilateral funding support are reducing operational costs and expanding market coverage.

West and North African markets show varying performance based on natural resources and regulatory frameworks. Nigeria maintains its position as the continent's largest market, supported by private sector growth and industrial fertilizer production. Morocco utilizes its phosphate resources through environmental investment programs, supplying blended fertilizers to West African markets. Kenya, Tanzania, and Ghana are developing digital agricultural credit and warehouse systems to enhance agrochemical accessibility, while Egypt and Algeria are testing green ammonia production for sustainable fertilizers. DR Congo and Zambia show growth potential, dependent on infrastructure improvements and regulatory consistency.

Competitive Landscape

Market concentration is moderate, with the top five companies holding nearly half of the Africa agrochemicals market share, indicating growth for regional specialists and start-ups to innovate and scale. Bayer AG has strengthened its position as a market leader through strategic investments in agrochemical infrastructure, advancing the availability of innovative crop protection solutions across Africa. Syngenta Group applies AI-driven crop trait discovery through its partnership with InstaDeep’s AgroNT1 model, accelerating breeding cycles and aligning with climate resilience goals.

UPL Limited maintains a strong presence through its Natural Plant Protection line and regional partnerships that introduced new insecticide formulations in 2024. Corteva Agriscience and BASF SE continue to tailor growth regulator and herbicide solutions to African climatic conditions, while FMC leverages its proprietary diamide platform to address lepidopteran pest challenges in maize-growing regions. Local innovators like Apollo Agriculture in Kenya integrate fintech and agronomy to reach smallholders directly, capturing last-mile margins often missed by multinational firms.

Strategic investments increasingly emphasize precision and minimal/no-residue pesticides, carbon-efficient fertilizers, and digital advisory platforms. Cross-industry collaborations with telecom and fintech companies are improving farmer onboarding, payment collection, and agrochemical traceability. Insurance tie-ins are helping reduce default risk, making agrochemical financing more viable for lenders and suppliers. While global players continue to consolidate for market depth, antitrust oversight, and localization requirements are preserving competitive dynamics within the Africa agrochemicals market.

Africa Agrochemicals Industry Leaders

BASF SE

Syngenta Group

Bayer AG

Corteva Agriscience

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: KBR partnered with AMUFERT to construct a 2,300 metric tons/day ammonia plant in Soyo, Angola. The facility will utilize KBR's proprietary technology to enhance regional food security and support sustainable agriculture.

- March 2024: Indorama Corporation obtained a USD 75 million loan from the African Development Bank to expand its Nigerian fertilizer operations. The funds will support the construction of a third urea production line and a new port terminal, increasing both domestic supply and export capabilities.

- December 2023: Bayer AG launched EverGol Energy fungicide seed treatment in South Africa, specifically for maize and soybean crops affected by fungal diseases. This targeted solution enhances crop protection and boosts yield potential by effectively combating key fungal pathogens in maize and soybean.

Africa Agrochemicals Market Report Scope

Agrochemicals are pesticides, herbicides, or fertilizers used for the management of ecosystems in agricultural sectors. The African Agrochemicals Market is Segmented by Product Type (Fertilizer, Pesticides, Adjuvants, and Plant Growth Regulators), Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Commercial Crops), and Geography (Congo, Malawi, Mozambique, Zambia, and Rest of Africa). The report offers the market size and forecasts in terms of value in USD and volume in Metric Tons for all the above segments.

By Product Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Adjuvants | |

| Plant Growth Regulators |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops (Sugarcane, Cotton, and Others) |

By Geography

| Egypt |

| Morocco |

| Algeria |

| Kenya |

| Tanzania |

| Ethiopia |

| South Africa |

| Zambia |

| Zimbabwe |

| Nigeria |

| Ghana |

| DR Congo |

| Rest of Africa |

| By Product Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Commercial Crops (Sugarcane, Cotton, and Others) | ||

| By Geography | Egypt | |

| Morocco | ||

| Algeria | ||

| Kenya | ||

| Tanzania | ||

| Ethiopia | ||

| South Africa | ||

| Zambia | ||

| Zimbabwe | ||

| Nigeria | ||

| Ghana | ||

| DR Congo | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Africa agrochemicals market?

The market is valued at USD 12.21 billion in 2026.

How fast will the market grow through 2031?

It will expand at a 4.32% CAGR, reaching USD 15.08 billion.

Which product type currently dominates the market?

Fertilizers lead with a 50.55% share.

Which country is growing the fastest?

Ethiopia posts the highest 6.49% CAGR to 2031.

What key restraint limits adoption?

High input prices, especially in landlocked states, reduce smallholder uptake.

How concentrated is the competitive landscape?

The top five firms hold 44.2% share, indicating moderate concentration.

Page last updated on: