Agentic AI Orchestration And Memory Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

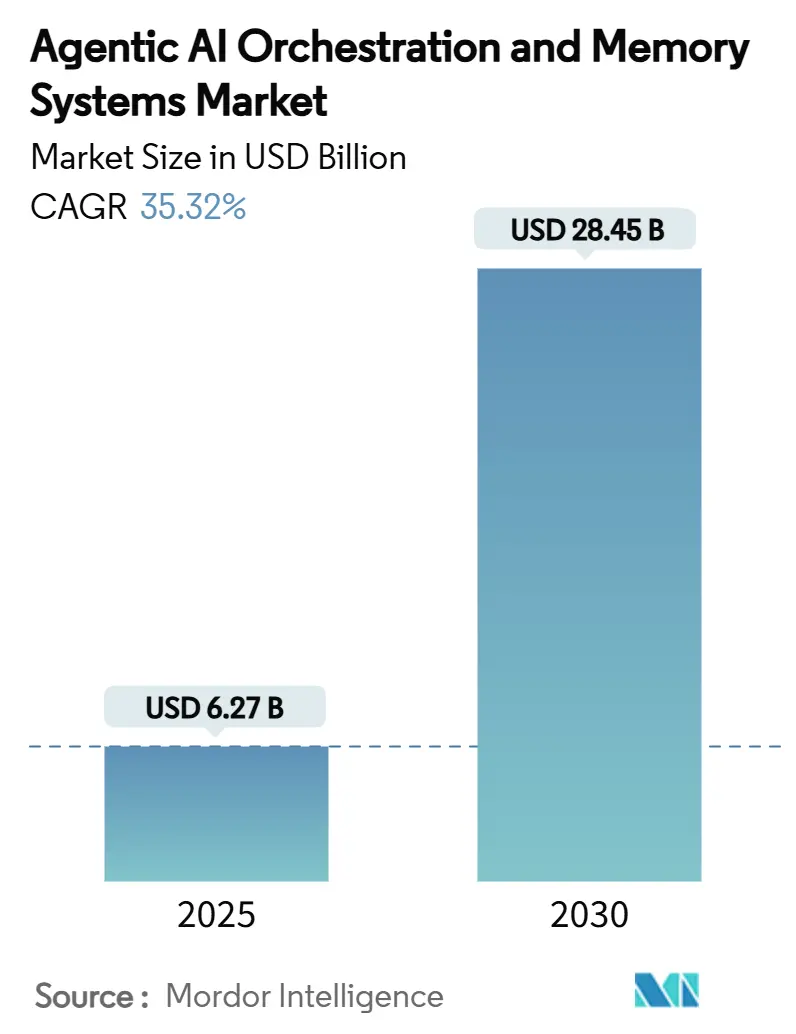

| Market Size (2025) | USD 6.27 Billion |

| Market Size (2030) | USD 28.45 Billion |

| Growth Rate (2025 - 2030) | 35.32% CAGR |

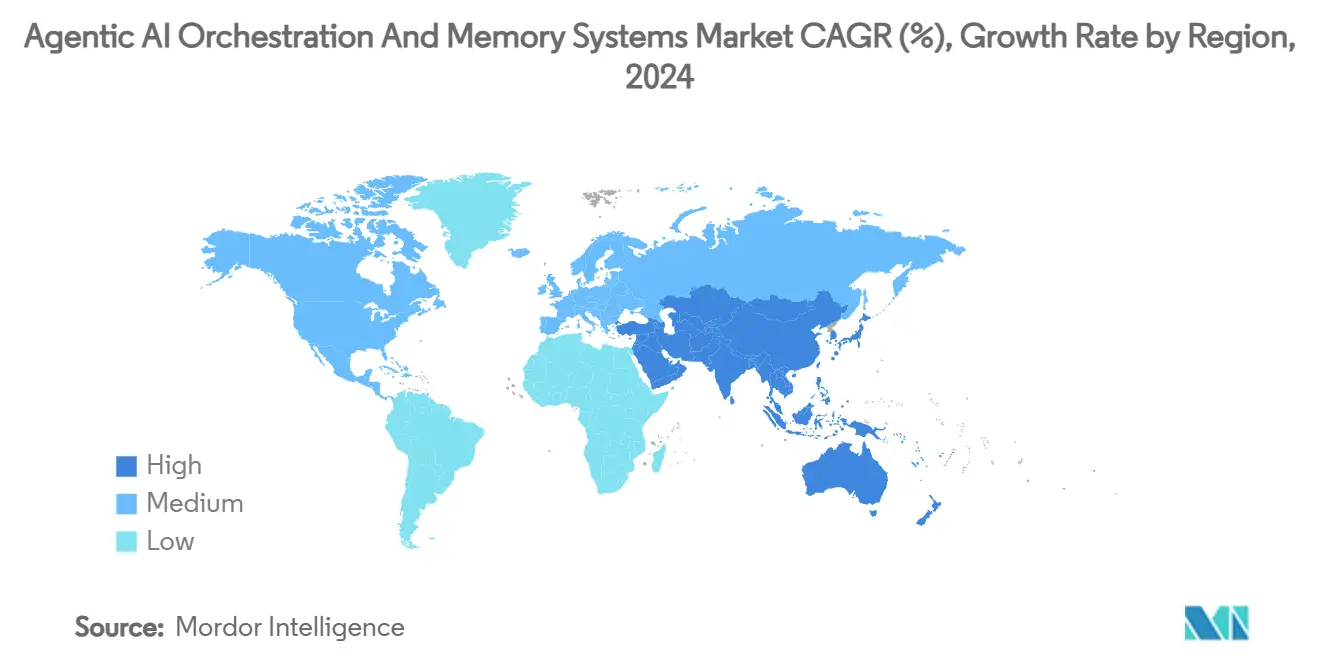

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

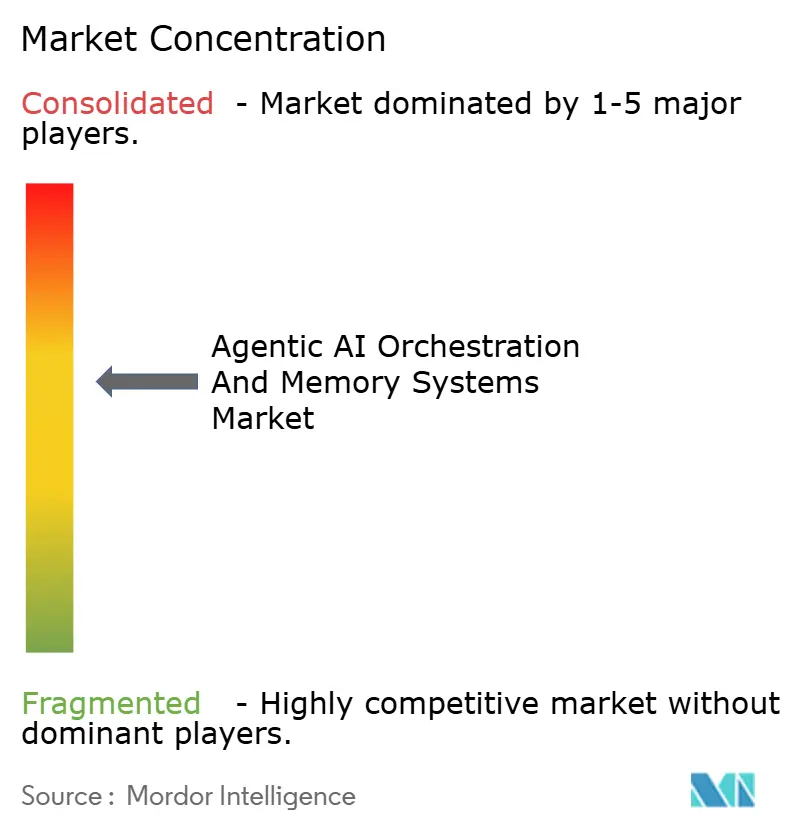

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Orchestration And Memory Systems Market Analysis by Mordor Intelligence

The Agentic AI Orchestration And Memory Systems Market size is estimated at USD 6.27 billion in 2025, and is expected to reach USD 28.45 billion by 2030, at a CAGR of 35.32% during the forecast period (2025-2030). The double-digit surge stems from enterprises shifting beyond pilots into production-grade, autonomous multi-agent workflows that cut manual touchpoints in core operations. Business value now pivots on orchestration layers that coordinate reasoning and action, while turnkey memory systems keep long-horizon context available to every agent. Vector databases integrated with orchestration APIs deliver this persistent memory, and cloud platforms embed the capability as a managed service, reducing build-and-run friction. Competitive intensity is rising as big-tech incumbents package reference architectures that remove architectural uncertainty, yet specialized start-ups defend share with deeper vector search, tighter observability, and domain-specific workflow logic. The agentic AI orchestration market also benefits from compliance mandates that require full audit trails for large-language-model (LLM) activity, making context retention a board-level priority[1]Microsoft Corporation, “Azure AI Agent Service,” MICROSOFT.COM.

Key Report Takeaways

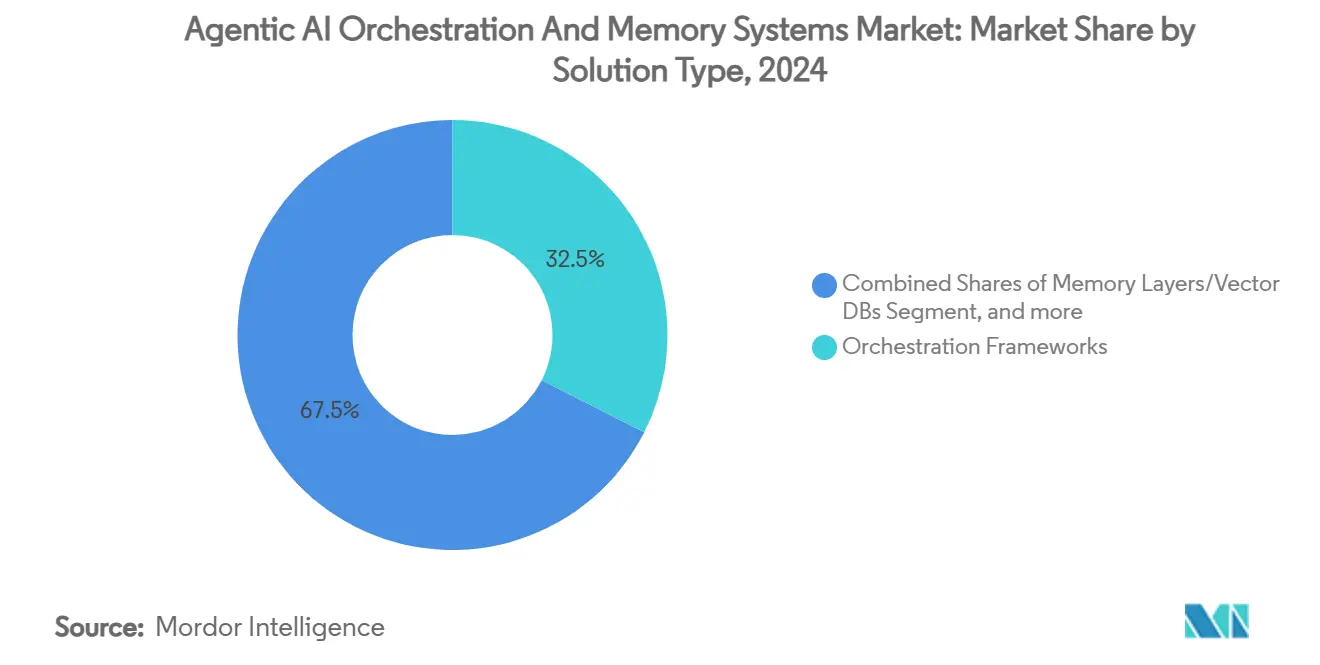

- By solution type, orchestration frameworks held 32.45% of agentic AI orchestration market share in 2024, while observability and testing tools are accelerating at a 37.45% CAGR through 2030.

- By deployment mode, cloud platforms commanded 67.84% share of the agentic AI orchestration market size in 2024 and are advancing at a 36.50% CAGR to 2030.

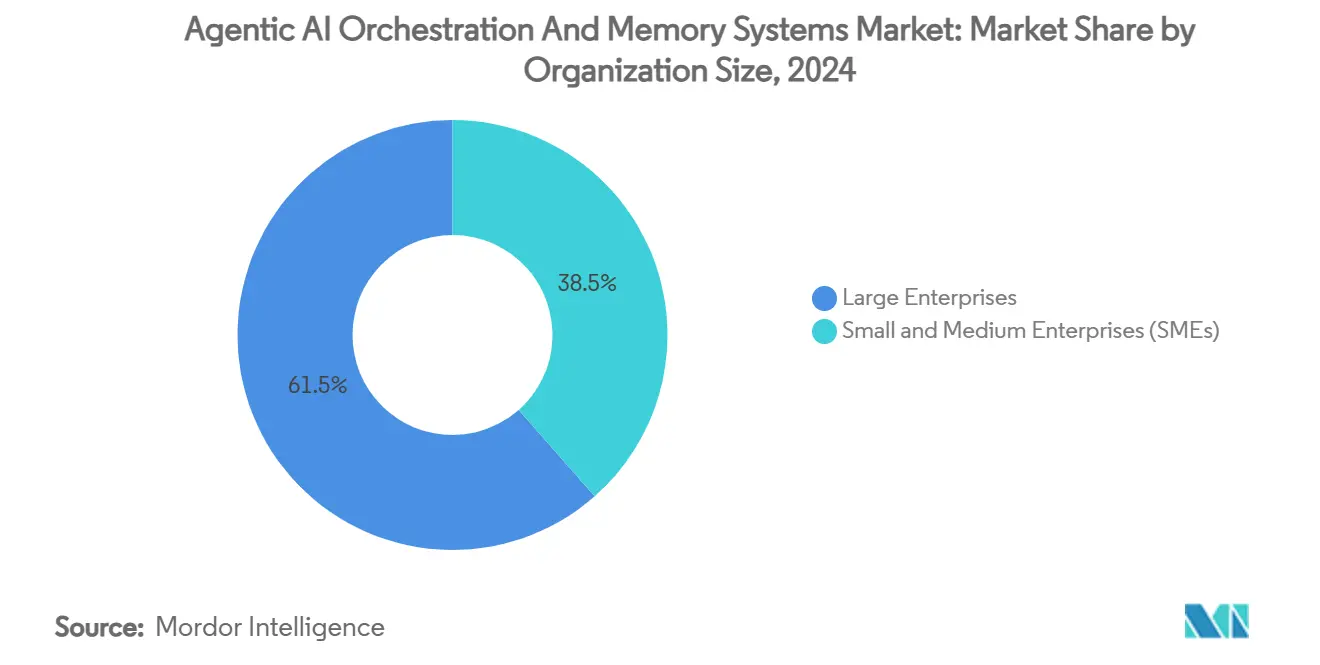

- By organization size, large enterprises led with 61.47% revenue share in 2024; small and medium enterprises are expanding at a 38.10% CAGR through 2030.

- By end-user industry, IT and telecom captured 23.40% share of the agentic AI orchestration market in 2024, while retail and e-commerce is projected to grow at 37.19% CAGR through 2030.

- By geography, North America accounted for 40.40% of 2024 revenue; Asia Pacific is registering the fastest 37.89% CAGR to 2030.

Global Agentic AI Orchestration And Memory Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native agent-ops stacks gaining CIO mindshare | +8.20% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Convergence of vector DBs & orchestration APIs into turnkey memory layers | +7.80% | Global | Short term (≤ 2 years) |

| Enterprise multi-agent pilots moving from POCs to production in 2025 | +6.50% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Big-tech vendor reference architectures lowering adoption risk | +5.90% | Global | Medium term (2-4 years) |

| Rising compliance mandates for LLM audit-trails driving persistent memory | +4.70% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Emergence of open protocols (A2A, MCP) enabling plug-and-play agent meshes | +3.10% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Agent-Ops Stacks Gaining CIO Mindshare

Chief information officers classify orchestration and memory systems as strategic infrastructure, replacing the perception of agentic AI as an experimental add-on. Spending moves to cloud-native agent-ops platforms because they dovetail with existing DevOps pipelines and security tooling. Microsoft’s Azure AI Agent Service embeds orchestration directly into virtual network boundaries, allowing enterprises to launch multi-agent flows without additional integration overhead. Early adopters report 30–40% operating expense savings once reasoning agents replace repetitive human tasks[2] Boston Consulting Group, “How AI Agents Are Opening the Golden Era of Customer Experience,” BCG.COM . The built-in governance modules satisfy regulatory checks for explainability, positioning cloud-native architectures as the default for new deployments through 2030. As big-ticket projects reach scale, CIOs benchmark vendor roadmaps on three metrics—latency under concurrency, automated rollout safety, and full lineage logging—converting these criteria into multi-year platform contracts.

Convergence of Vector DBs & Orchestration APIs into Turnkey Memory Layers

Stateless agent limitations are fading because vector store indexing and orchestration logic now interlock in a single managed layer. Mem0 AI pairs high-recall semantic search with workflow triggers, so every agent call retrieves, updates, and persists context in the same atomic transaction[3] Mem0 AI, “Memory Layer Platform,” MEM0.AI . Enterprises that install these turnkey memory layers note 40–60% higher task-completion accuracy than stateless baselines. The technical leap stems from late-binding of embeddings: memory writes only occur when relevance scores cross policy thresholds, controlling vector-store sprawl. With persistence solved, architects are redesigning end-to-end business processes—for example, order-to-cash flows now span multiple fiscal cycles without context loss, and agents reference months-old supplier negotiations during real-time pricing decisions. This structural capability is resetting expectations for what autonomous systems can cover inside corporate workflows.

Enterprise Multi-Agent Pilots Moving from POCs to Production in 2025

The proof-of-concept phase disappears for many Fortune 1000 firms in 2025. Wells Fargo pushed a customer-service agent mesh live across voice, chat, and email channels and published measurable cuts in average handle time alongside a lift in customer-satisfaction scores. Production readiness accelerated because observability stacks now capture every agent decision tree, letting compliance officers replay interactions on demand. Databricks survey data shows 60% of enterprises will migrate at least one pilot to production during 2025, a threefold jump from 2024. This pipeline of go-lives pushes vendors to guarantee four-nines availability for orchestration engines and to offer rollback strategies when emergent agent behavior deviates from policy. As production estates grow, buyers increasingly weigh vendors’ support SLAs and incident-response frameworks as heavily as their raw model-quality benchmarks.

Big-Tech Vendor Reference Architectures Lowering Adoption Risk

Microsoft, Google, and AWS weaponize their cloud footprints by shipping full-stack reference designs. Google’s Vertex AI Memory Bank stitches persistent vector memory into existing Identity and Access Management policies, accelerating security reviews. AWS Bedrock Agents pre-package token-level guardrails, enabling financial institutions to clear compliance hurdles in weeks instead of quarters. Enterprises adopting these templates report deployment cycles shrinking by 50–70%, prompting board-level green lights for wider roll-outs. Reference architectures codify best practices, so even firms with thin AI teams can stand up multi-agent applications that pass internal architecture review boards. These blueprints entrench big-tech providers at the orchestration core, but they also expand total addressable spend by reassuring risk-averse sectors such as healthcare and government.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immature observability & debugging toolchain for multi-agent workflows | -4.20% | Global | Short term (≤ 2 years) |

| High vector-store inference costs at scale for long-term context | -3.80% | Global | Medium term (2-4 years) |

| Fragmented standards creating interoperability overhead | -2.90% | Global | Long term (≥ 4 years) |

| Data-sovereignty concerns limiting cross-border memory replication | -2.10% | EU & APAC core, regulatory spillover globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Immature Observability & Debugging Toolchain for Multi-Agent Workflows

Enterprises face monitoring gaps because traditional Application Performance Management dashboards do not parse agent thought-traces or emergent collaboration patterns. Deepchecks lists only a handful of purpose-built LLM observability products, and feature parity with mature APM suites is still lacking[4] Deepchecks, “Top 5 LLM Observability Tools,” DEEPCHECKS.COM . Without full introspection, teams struggle to fine-tune reward functions or isolate race conditions when agents coordinate across microservices. XenonStack notes that 40–50% of stalled production roll-outs cite missing debugging telemetry as the root cause. This barrier disproportionately slows regulated industries that must evidence every algorithmic step. Vendors are racing to ship trace visualizers and anomaly detectors tailored to agent graphs, yet until coverage reaches parity with DevSecOps expectations, deployment risk continues to dampen near-term growth.

High Vector-Store Inference Costs at Scale for Long-Term Context

Maintaining million-document memory windows inside vector databases is compute-intensive, especially when embeddings reflow after fine-tuning. AI Multiple calculates that vector retrieval can represent 30–40% of live-agent operating costs in data-dense verticals[5] AI Multiple, “AI Agent Performance: Success Rates & ROI in 2025,” AIMULTIPLE.COM . Rapid Innovation reports similar cost ratios during supply-chain implementations where agents recall year-long shipment histories. The price curve rises non-linearly because similarity searches touch large index partitions as context expands. Smaller enterprises, therefore, cap vector depth, impairing agent reasoning quality. Vendors are experimenting with hybrid memory that off-loads cold vectors to object storage and re-hydrates them on demand, but commercial proofs remain limited. Until cost curves flatten, some CFOs will cap project scope, trimming the otherwise steep adoption trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Observability Tools Drive Enterprise Confidence

Observability and testing platforms recorded the fastest 37.45% CAGR through 2030 as enterprises learned that reliable production agents require deep instrumentation. The segment gained momentum once agent traces, token-level attribution, and policy-violation alerts became board-level audit requirements. In 2024, orchestration frameworks still owned the largest 32.45% share of the agentic AI orchestration market size, yet growth moderated as frameworks matured and new buyers prioritized monitoring add-ons. AgentOps and similar vendors monetized this gap with dashboards that replay every reasoning step and surface root-cause diagnostics[6] AgentOps, “AgentOps Platform,” AGENTOPS.AI . High uptake across financial services and healthcare verticals signals that observability is no longer optional.

Sophisticated memory layers that marry vector search with role-based access controls constituted the second-largest revenue slice. Workflow engines keep generating steady subscription renewals because they remain the backbone for task sequencing across agents. Context-management SDKs appeal to developer tooling teams that need abstractions for agent state handling and prompt versioning. The diversity of toolsets highlights that multi-agent orchestration is an ecosystem rather than a single product category, and buyers often bundle multiple components from different vendors to satisfy full life-cycle requirements.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployment captured 67.84% of the agentic AI orchestration market share in 2024 and is set to compound at 36.50% CAGR, far outpacing on-premises installations. Public-cloud providers abstract the operational complexity of sharding vector stores, autoscrolling context windows, and patching orchestration runtimes. Enterprises gravitate to managed endpoints that expose role-based governance while scaling horizontally on demand. Hybrid patterns still appear where data classified as highly confidential resides in private clusters, but orchestration and inference traffic stays in cloud VPCs. Nexos.ai’s gating layer that routes queries across 200 LLM endpoints exemplifies why firms prefer as-a-service gateways rather than self-managed clusters[7] Nexos.ai, “AI Gateway: Next-Level LLM Management for Enterprises,” NEXOS.AI .

On-premises builds continue in defense and certain EU public-sector contexts where data sovereignty rules preclude off-site storage. Even there, vendors ship turnkey appliances that mimic cloud orchestration stacks behind corporate firewalls. The continual hardening of sovereign cloud zones in Japan and India reduces hesitation among regulated industries, suggesting that cloud share will grow even in historically on-premises strongholds. Given these trends, investors expect cloud platform gross-profit pools to widen because margin-rich orchestration services upsell naturally into existing compute and storage spend.

By Organization Size: SMEs Drive Democratization

Small and medium enterprises grew at a head-turning 38.10% CAGR through 2030, yet large enterprises still command revenue dominance due to deal sizes that package hundreds of agent seats and terabyte-scale vector stores. The democratization arc runs on cost efficiency: SMEs can now launch entry-level orchestration projects for USD 20,000 to USD 60,000, a threshold reachable from operational budgets rather than multi-year CAPEX. Off-the-shelf templates for marketing automation or help-desk triage let smaller firms bypass data-science hires they cannot afford. OECD analysis indicates that skills gaps remain the top adoption roadblock, so vendors inject low-code orchestration studios and integrated prompt libraries to flatten learning curves.

Large enterprises retain leadership because they integrate agents across ERP, CRM, and supply-chain networks, creating high-ticket service engagements for systems integrators. They also negotiate volume discounts on vector storage and priority support. Yet as template libraries proliferate, SME growth will sustain volume metrics used by cloud vendors to justify continued R&D investments in orchestration features.

By End-User Industry: Retail Transformation Leads Growth

IT and telecom captured 23.40% of 2024 revenue because telcos needed autonomous network-monitoring agents, and IT outsourcers bundled orchestration into managed services. Retail and e-commerce, however, will drive the highest 37.19% CAGR as conversational shopping and dynamic pricing agents show immediate revenue lift. Fast Company documents double-digit conversion gains for brands deploying AI shopping concierges that remember prior browsing, negotiate discounts, and autofill checkout flows. BFSI uptake follows closely with fraud-detection agents that cross-reference contextual patterns at millisecond latency. Healthcare embraces orchestration for drug-trial data wrangling despite regulatory overhead, while manufacturing applies autonomous planning to predictive maintenance.

The agentic AI orchestration market size for retail personalization agents is projected to surpass USD 4 billion by 2030, reflecting how front-of-house revenue gains justify system rollout costs. Industrial adoption grows steadily as factories instrument robotics, yet overall share lags service industries where digital interactions dominate.

Geography Analysis

North America maintained 40.40% of 2024 revenue due to first-mover enterprise pilots and a regulatory patchwork that requires verifiable audit trails, pushing buyers toward mature U.S. orchestration stacks. Asia Pacific now posts the steepest 37.89% CAGR through 2030 because sovereign AI budgets in China, Japan, and India underwrite home-grown orchestrators optimized for local compliance rules. National subsidies lower procurement hurdles, and manufacturing heavyweights retrofit agent meshes into supply-chain control towers. Europe’s growth is steady but comparatively slower because GDPR and the forthcoming EU AI Act extend vendor due diligence cycles. Still, European-born platforms that bake in privacy-by-design earn traction among data-sensitive industries.

South America sees early adoption concentrated in Brazil’s digital-banking scene. The Middle East and Africa track oil-and-gas plus government digitalization agendas, though skills shortages temper velocity. Overall, APAC expansion reshapes vendor roadmaps: language support, regional compliance adapters, and onshore data-center footprints become table stakes for global suppliers.

Competitive Landscape

The competitive field displays moderate fragmentation. Microsoft, Google, and AWS bundle orchestration into cloud accounts, leveraging existing spend anchors to upsell advanced agent services. Azure delineates a shared-responsibility model that assigns data lineage to the customer while Microsoft manages orchestration runtime, pleasing risk teams who want clarity over breach liability. Google and AWS pursue parallel strategies with managed memory banks and guardrail policies. Their scale enables preferential GPU pricing and national-security approvals, helping them win heavily regulated accounts.

Specialists counter by deepening vertical capability. Pinecone focuses on ultra-low-latency vector search with enterprise access controls. LangChain offers an open-source framework that accelerates developer onboarding through composable prompt chains and supports self-hosting for firms wary of cloud lock-in. Mem0 AI captures datasets where context retention spans years, such as wealth-management client records. Start-ups like CrewAI Labs differentiate on iterative planning algorithms that optimize multi-agent collaboration inside complex workflows.

NVIDIA’s USD 700 million takeover of Run:ai underscores how orchestration is no longer a feature layer but a strategic control point for AI infrastructure[8] TechCrunch, “Nvidia Acquires AI Workload Management Startup Run:ai for USD 700 Million,” TECHCRUNCH.COM . Similarly, open-protocol initiatives (A2A, MCP) push vendors toward interoperability as enterprise architects rebel against closed ecosystems. The long-run competitive frontier therefore hinges on two questions: who guarantees lowest total latency from prompt to action, and who offers the most portable agent definition language that survives provider switches without re-engineering.

Agentic AI Orchestration And Memory Systems Industry Leaders

Pinecone Inc.

LangChain Technologies Ltd.

OpenAI LLC

UiPath Inc.

ServiceNow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nexos.ai raised USD 8 million to launch a gateway that routes traffic across 200 commercial LLMs and enforces unified security policies. The funding underscores venture conviction that multi-model orchestration reduces vendor lock-in and optimizes cost-per-token. The strategy centers on positioning Nexos.ai as a neutral broker layer that enterprises insert above proprietary endpoints.

- December 2024: NVIDIA finalized its USD 700 million purchase of Run:ai to embed GPU scheduling and AI workload management directly into orchestration pipelines. The move strengthens NVIDIA’s grip on the inference stack, giving customers one-click provisioning from GPU slice to multi-agent deployment, which may tilt share away from pure-software orchestrators that lack hardware optimization.

- November 2024: Microsoft’s general availability of Azure AI Agent Service delivered enterprise-grade orchestration plus template libraries for finance, healthcare, and retail. The rollout aims to collapse proof-of-concept timelines and cement Azure as the default launchpad for production agent estates that demand compliance guardrails.

- October 2024: Google introduced Vertex AI Memory Bank with cross-region replication and privacy controls. The launch attacks the persistent-context pain point and targets EU clients that require data residency assurances. Google’s bet is that built-in privacy certifications will unlock regulated verticals previously hesitant to store embeddings offshore.

- September 2024: LangChain Technologies secured USD 25 million Series A funding led by Sequoia Capital to harden its open-source framework for enterprise workloads. The cash fuels roadmap items such as native RBAC, prompt-version lineage, and premium support tiers, turning community traction into monetizable services while preserving openness.

Global Agentic AI Orchestration And Memory Systems Market Report Scope

| Orchestration Frameworks |

| Memory Layers / Vector DBs |

| Workflow Engines |

| Context-Management SDKs |

| Observability & Testing Tools |

| Cloud |

| On-Premises / Self-Hosted |

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| Others (Govt, Education, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | Orchestration Frameworks | ||

| Memory Layers / Vector DBs | |||

| Workflow Engines | |||

| Context-Management SDKs | |||

| Observability & Testing Tools | |||

| By Deployment Mode | Cloud | ||

| On-Premises / Self-Hosted | |||

| By Organization Size | Large Enterprises | ||

| Small & Medium Enterprises (SMEs) | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Others (Govt, Education, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the agentic AI orchestration market?

Persistent memory layers, cloud-native deployment, and ready-made reference architectures have lowered implementation risk and unlocked 35.32% CAGR growth through 2030.

How large will the agentic AI orchestration market be by 2030?

Forecasts place the agentic AI orchestration market size at USD 28.45 billion by 2030 on the back of sustained enterprise rollout momentum.

Which solution segment is expanding fastest?

Observability and testing tools are scaling at 37.45% CAGR because production systems need deep monitoring and debugging.

Why are SMEs adopting agentic AI now?

Cloud templates and low-code studios have cut entry costs to USD 20,000–60,000, helping SMEs overcome skills gaps and deploy multi-agent workflows.

Which region will contribute the most new revenue?

Asia Pacific leads with a 37.89% CAGR, supported by sovereign AI funding and heavy manufacturing automation initiatives.

Page last updated on: