Healthcare Agentic AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

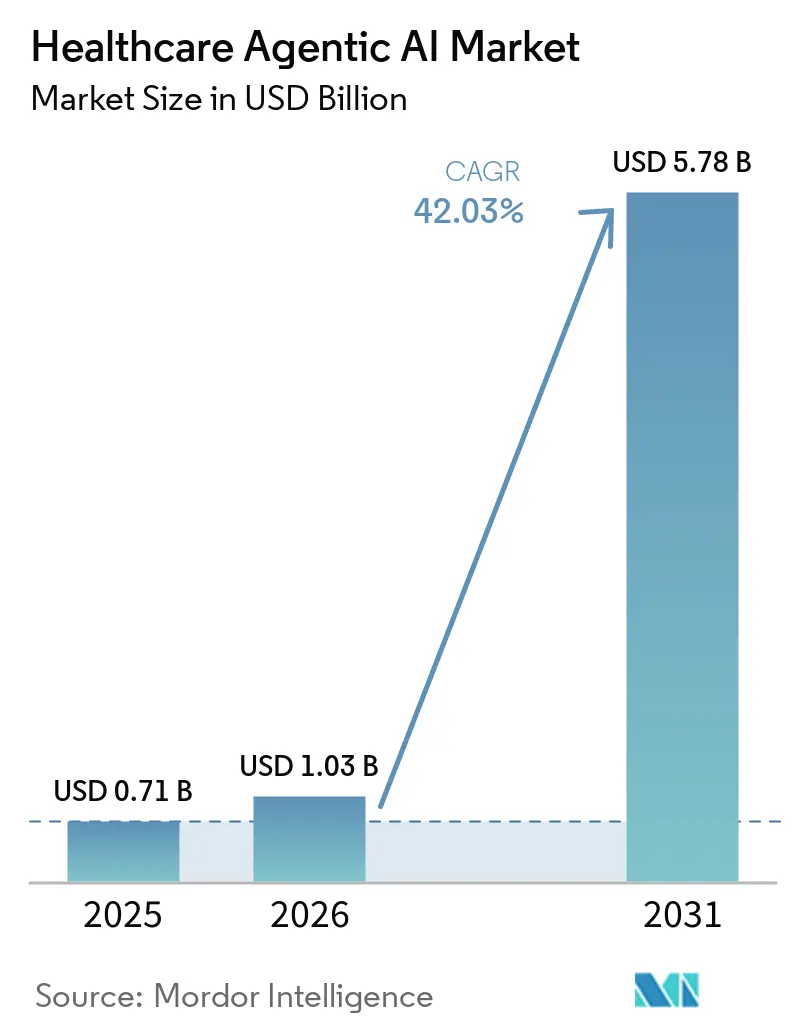

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 5.78 Billion |

| Growth Rate (2026 - 2031) | 42.03% CAGR |

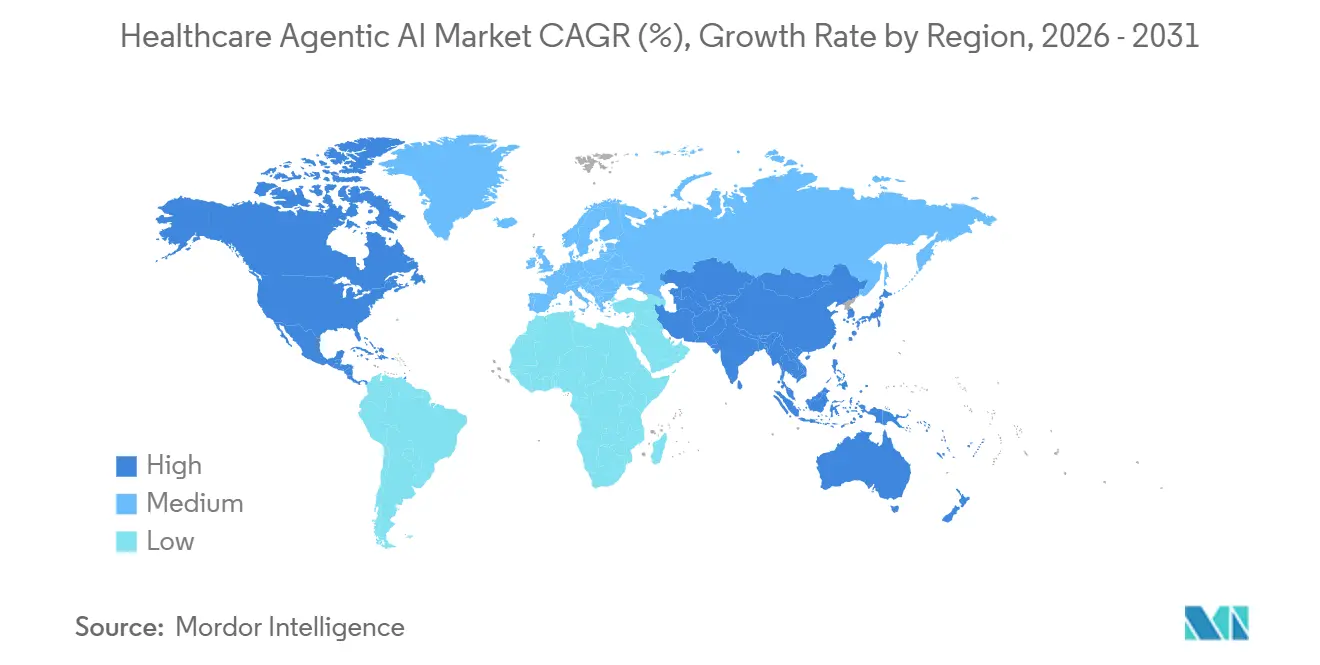

| Fastest Growing Market | Middle East |

| Largest Market | North America |

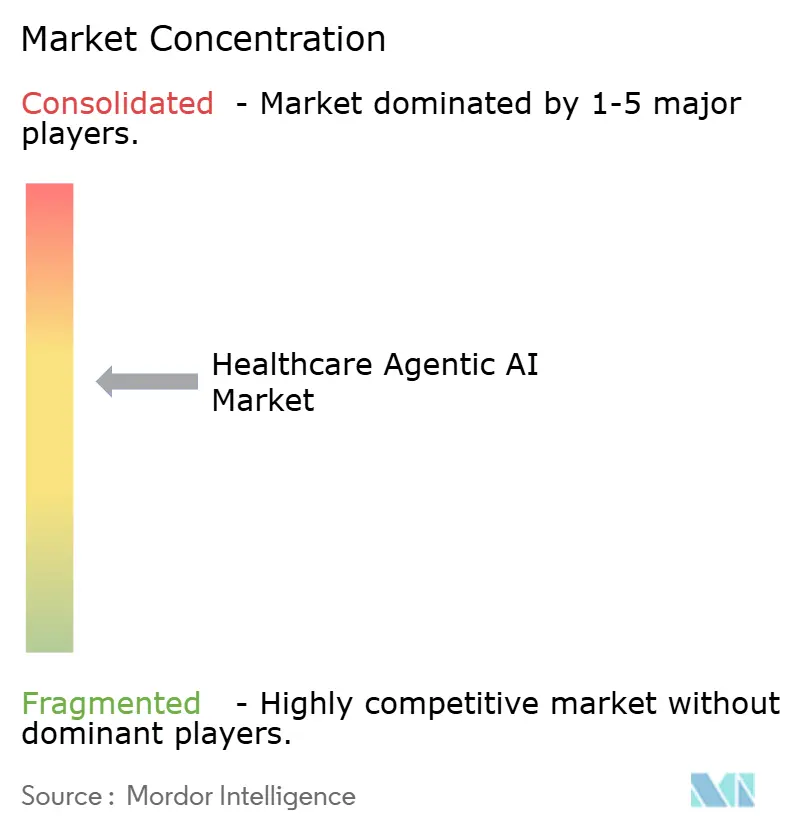

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Agentic AI Market Analysis by Mordor Intelligence

The healthcare agentic AI market size is expected to grow from USD 0.71 billion in 2025 to USD 1.03 billion in 2026 and is forecast to reach USD 5.78 billion by 2031 at 42.03% CAGR over 2026-2031. Growth is being driven by the move from pilot programs to routine deployment across documentation, prior authorization, diagnostic triage, and care coordination. Buyers are no longer treating these systems as point tools; many are now part of core operating workflows across provider and payer settings. Competition is also widening as large technology firms, EHR platform owners, and specialized healthcare AI vendors all try to secure a lasting place in clinical and administrative processes. Regulatory review is becoming stricter at the same time, pushing vendors to provide stronger evidence, clearer governance, and safer update pathways before adoption scales further. The strongest opportunity lies with organizations that combine longitudinal patient data, multimodal workflows, and compliant infrastructure to support lower-latency, more accountable deployment.

Key Report Takeaways

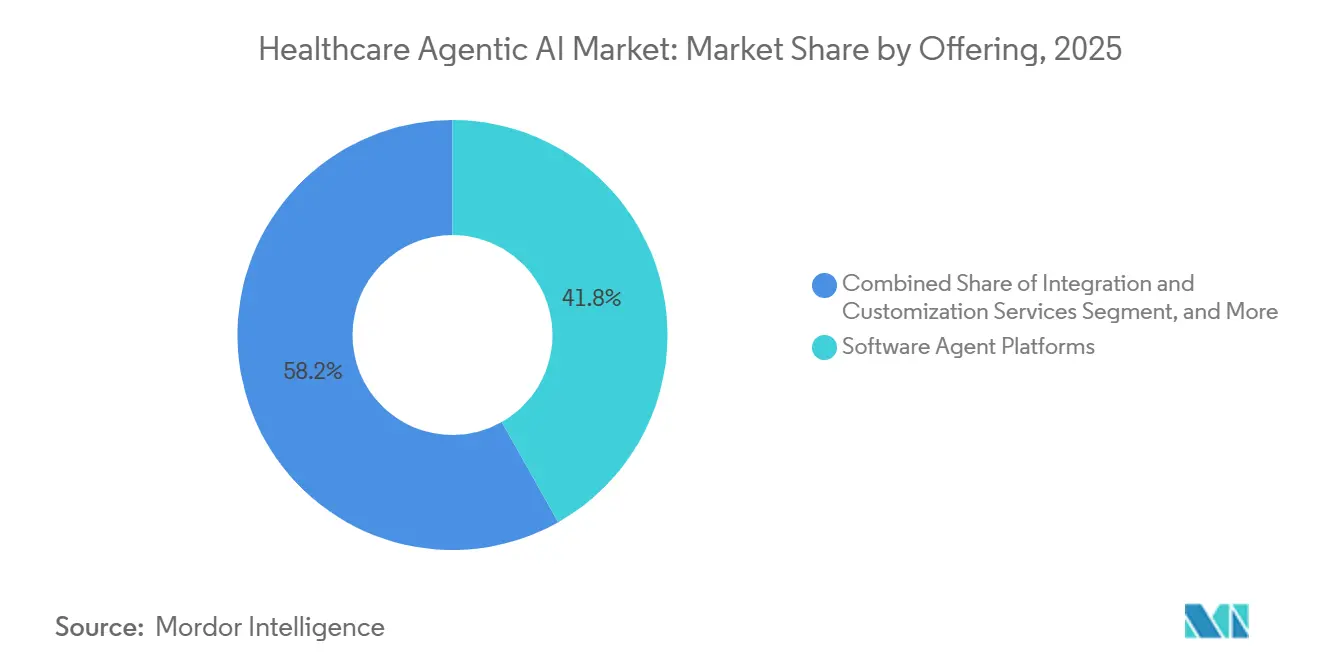

- By offering, software agent platforms led with a 41.82% revenue share of the healthcare agentic AI market in 2025, while edge devices and specialized hardware are projected to expand at a 42.63% CAGR through 2031.

- By deployment mode in the healthcare agentic artificial intelligence market, cloud-based architectures accounted for 52.38% of revenue of the healthcare agentic AI market in 2025, while hybrid edge-cloud configurations are forecast to grow at a 42.58% CAGR through 2031.

- By application, clinical decision support and diagnostics accounted for 29.63% of revenue of the healthcare agentic AI market in 2025, while remote monitoring and telehealth are projected to advance at 43.03% CAGR through 2031.

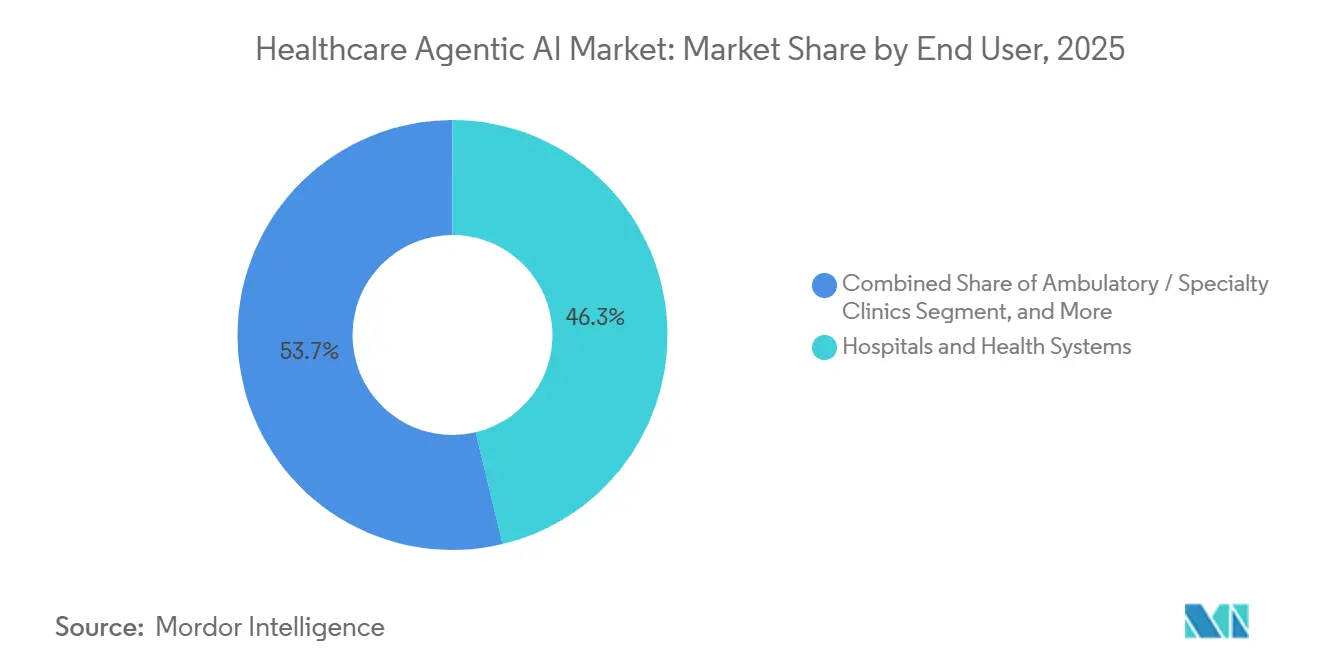

- By end user, hospitals and health systems accounted for 46.27% of the revenue of the healthcare agentic AI market in 2025, while the patients and direct-to-consumer segment is forecast to expand at a 42.78% CAGR through 2031.

- By 2025, large-language-model agents captured 38.91% of revenue of the healthcare agentic AI market, while multi-modal autonomous agents are projected to grow at a 42.81% CAGR through 2031.

- By geography, North America accounted for 44.74% of revenue of the healthcare agentic AI market in 2025, while the Middle East is forecast to expand at a 42.89% CAGR through 2031 for the healthcare agentic AI market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Agentic AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of LLM-Based Clinical ChatGPT Tools | +8.5% | Global, Led by North America and United Kingdom | Short term (≤ 2 years) |

| Increasing Shortage of Nursing Staff Driving Agent Assistants | +7.2% | Global, Highest Pressure in North America and Western Europe | Short term (≤ 2 years) |

| Payer Mandates for Prior Authorization Automation | +6.4% | North America, Primarily the United States, With Spillover Into Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Integration of Multi-Modal Sensing in Remote Monitoring Devices | +5.8% | Global, Strong in Asia-Pacific, With Spillover Into Middle East and Africa | Medium term (2-4 years) |

| Shift Toward Value-Based Care Incentivizing Automation | +4.6% | North America and Western Europe | Medium term (2-4 years) |

| Venture Capital Funding Surge in Healthcare Agentic Start-Ups | +3.5% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of LLM-Based Clinical ChatGPT Tools

In 2026, health systems began integrating LLM-based clinical tools into daily workflows instead of limiting them to pilot settings. OpenAI launched OpenAI for Healthcare in January 2026, partnering with 8 leading U.S. health institutions and using GPT-5.2 models developed with input from 260 physicians across 60 countries. The April 2026 release of ChatGPT for Clinicians expanded verified access for medical users and introduced a clinical benchmark through HealthBench Professional. Major vendors, such as Microsoft, are incorporating healthcare agent orchestration into their core product roadmaps. By late 2025, Microsoft introduced healthcare-specific AI models, a Healthcare Agent Orchestrator in Microsoft Foundry, and a healthcare AI marketplace. As verified AI tools gain acceptance, agentic AI in healthcare is transitioning from innovation budgets to operational spending.

Increasing Shortage of Nursing Staff Driving Agent Assistants

Workforce pressure is driving demand for virtual nursing and task-support agents. A study using U.S. labor data projects 194,500 annual registered nurse job openings through 2033, with non-metropolitan areas potentially facing an 11% shortage by 2038. Many automated tasks, such as patient summaries and outreach coordination, are tied to nurse workflows. Mayo Clinic demonstrated scalability by deploying its AI-powered Nurse Virtual Assistant to over 9,600 nurses in inpatient and emergency units by September 2025. This practical approach allows health systems to reclaim staff time without overhauling care models, keeping hospitals invested in agentic AI despite tight capital budgets.

Payer Mandates for Prior Authorization Automation

Prior authorization is a key policy-driven adoption area for healthcare agents. CMS's Interoperability and Prior Authorization Final Rule mandates that Medicare Advantage, Medicaid, and Marketplace plans resolve standard requests within 7 days and urgent requests within 72 hours by January 1, 2026.[1]Centers for Medicare and Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule CMS-0057-F,” CMS, cms.gov The rule also introduces the FHIR-based Prior Authorization API, effective January 1, 2027, encouraging 2026 deployments of agents to streamline documentation and requests. Providers benefit from early adoption, reducing administrative burdens before payer systems fully adapt. This ties agentic AI demand in healthcare to regulatory deadlines rather than optional digital transformation.

Integration of Multi-Modal Sensing in Remote Monitoring Devices

Remote monitoring is evolving as AI systems now integrate IoMT biosensors and clinical data in real time. A July 2025 study in Scientific Reports highlighted a transformer-based model achieving 98.6% accuracy on heart failure datasets by combining multiple data types. Google DeepMind further advanced this in April 2026 with AI co-clinician research, enabling live audio and video, as well as remote physical examination guidance. These advancements strengthen agentic AI's role in chronic disease management, post-acute care, and home-based care, emphasizing the importance of hybrid deployment for live inference near patients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and HIPAA Compliance Complexities | -4.2% | North America and Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Algorithmic Bias Risks Leading to Regulatory Scrutiny | -3.6% | Global | Medium term (2-4 years) |

| Lack of Standardized Interoperability Frameworks | -2.8% | Global, Most Acute in Asia-Pacific and Middle East and Africa | Medium term (2-4 years), Long term (≥ 4 years) |

| Limited Clinical Validation Evidence for Autonomous Agents | -2.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and HIPAA Compliance Complexities

Privacy requirements continue to hinder deployment despite rising demand. Agentic systems handling protected health information create multiple control points, increasing complexity, especially for multi-state health systems navigating HIPAA and state privacy laws.[2]Gabriela Rios, “Digital Diagnosis: Health Data Privacy in the U.S.,” Law and Biosciences Blog, law.stanford.edu The growth of national interoperability infrastructure further underscores the need for governance, as broader data exchange underscores the importance of secure access controls and auditability. Consequently, the agentic AI in the healthcare market favors vendors with clear data handling rules, secure integration, and robust oversight of third-party model layers.

Algorithmic Bias Risks Leading to Regulatory Scrutiny

Bias concerns are moving from academic debate to product review and updates. A 2026 study in Frontiers in Artificial Intelligence found that transparent models, such as logistic regression, can exhibit more severe bias than less interpretable ones, challenging the idea that explainability ensures fairness. The FDA's August 2025 guidance on AI-enabled device software requires manufacturers to monitor and mitigate bias in post-market updates. Systems trained on data from large academic centers may not represent all patient populations, necessitating broader validation and stronger monitoring. These requirements raise costs and review time in the agentic AI healthcare market, despite strong demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Lead While Hardware Expands at the Edge

Software agent platforms accounted for 41.82% of the healthcare agentic AI market share in 2025, driven by their integration into EHR-linked workflows, which increases switching costs. Microsoft and Oracle have advanced healthcare AI orchestration within their enterprise stacks, boosting recurring software revenue without requiring hardware replacement. Integration services remain vital as many provider networks operate mixed EHR and imaging systems.

Edge devices and specialized hardware are expected to grow fastest in the agentic AI healthcare market, with a 42.63% CAGR through 2031, driven by the need for local inference in imaging and monitoring where cloud latency affects clinical response. Philips and NVIDIA highlighted this trend in May 2025 by collaborating on an MRI model that leveraged NVIDIA infrastructure, including MAISI and VISTA-3D, for scan planning and automated detection.[3]Philips, “Philips Teams With NVIDIA to Drive AI in MRI,” Philips, philips.com This development establishes a distinct hardware layer between medical equipment and cloud software subscriptions.

By Deployment Mode: Cloud Leads While Hybrid Gains Ground

Cloud-based deployment accounted for 52.38% of the healthcare agentic artificial intelligence market in 2025. That lead reflects the fact that health systems can scale new AI functions faster when they do not need heavy upfront local infrastructure. Cloud-first deployment also aligns with the commercial strategy of major platform vendors, which aim to have AI services sit within existing enterprise relationships across data, productivity, and clinical systems. On-premise models still matter in markets and institutions where data sovereignty rules and internal governance standards remain stricter than what a cloud-only setup can easily satisfy.

Hybrid edge-cloud deployments are projected to grow at a 42.58% CAGR through 2031, balancing real-time local inference for triage and monitoring with centralized model updates. CHU de Montpellier’s 2026 Alliance Santé IA program, a EUR 14.9 million (USD 16.8 million) initiative, used sovereign local computing for AI deployment across 16,000 hospital professionals. National interoperability growth further supports hybrid models by enabling data coordination across sites without centralizing all inference, making hybrid architecture a key design shift in the agentic AI healthcare market.

By Application: Clinical Decision Support Leads While Remote Monitoring Speeds Up

Clinical decision support and diagnostics accounted for 29.63% of application revenue in 2025, driven by established workflows in radiology, oncology, stroke care, and emergency triage. Viz.ai highlighted this market scale, reporting its platform reached nearly 2,000 U.S. hospitals and covered over 230 million lives by the end of 2025. Administrative automation also grew, with Oracle stating in March 2026 that its Clinical AI Agent saved U.S. clinicians over 200,000 hours since launch.

Remote monitoring and telehealth are expected to grow fastest in the healthcare agentic AI healthcare market, with a 43.03% CAGR through 2031, fueled by demand for post-acute follow-up, chronic disease management, and patient engagement. Drug discovery and research, though smaller in scale, hold strategic importance. Tempus reported 2025 revenue of USD 1.3 billion, up 83.4% year-over-year, supported by AI partnerships with AstraZeneca, Merck, and Gilead. As sensor networks improve and care shifts outward, the agentic AI healthcare market is expanding beyond traditional hospital alerting tools.

By End-User: Hospitals Anchor Revenue While Consumer Demand Widens

Hospitals and health systems accounted for 46.27% of end-user revenue in 2025, driven by their control over large workflows, EHR integration, and enterprise-scale contracts. This benefits embedded ecosystem vendors, as buyers prefer tools compatible with existing systems. Oracle’s AI-driven EHR functions and clinical note generation highlight this trend. Smaller clinics remain relevant but require simpler, faster-to-deploy solutions with minimal IT support.

The direct-to-consumer segment is expected to grow at a 42.78% CAGR through 2031, driven by payer-funded and provider-sponsored digital engagement models. OpenAI expanded this market in 2026 with institution-facing healthcare products and clinician-access tools, normalizing agent use beyond back-office workflows. Additionally, tighter prior authorization timelines are pushing payers and providers toward automated interaction models, keeping hospitals dominant while broadening the agentic AI healthcare market.

By Technology: LLM Agents Lead While Multimodal Systems Broaden Care

Large-language-model agents accounted for 38.91% of 2025 technology revenue in the healthcare agentic artificial intelligence market, driven by the text-heavy nature of healthcare data and demand for documentation, communication, and administrative workflows. While rule-based and expert systems maintain a legacy presence, their growth has slowed as buyers prefer more flexible tools. Reinforcement-learning agents are more effective in operational areas like scheduling and bed management, where narrower action-reward structures are easier to optimize, giving text-driven systems an early lead.

Multi-modal autonomous agents are expected to grow at a 42.81% CAGR through 2031, combining imaging, EHR data, voice, and physiological signals in clinical processes. A 2026 Nature Communications study on DxDirector-7B showed the model outperformed larger systems in rare disease and complex cases by dynamically selecting diagnostic strategies and escalating higher-risk operations to physicians. Google DeepMind’s AI co-clinician work similarly integrates multimodal inputs with real-time consultation support, enhancing clinical utility by enabling escalation when necessary.

Geography Analysis

North America accounted for 44.74% of the agentic AI market share in healthcare in 2025, driven by widespread EHR adoption, robust cloud infrastructure, and a dynamic healthcare software ecosystem. Federal policies, such as CMS's tightened prior authorization timelines and expanded interoperability, further accelerated adoption. By early 2026, HHS reported TEFCA had facilitated nearly 500 million health record exchanges, strengthening data movement for agent workflows. The region’s primary challenge lies in addressing privacy, governance, and update control concerns as adoption scales.

Europe ranked second in 2025, following a compliance-driven approach emphasizing data governance, transparency, and sovereign deployment for high-risk clinical AI. The European Commission’s COMPASS-AI initiative, launched in October 2025, supports the safe adoption of technologies in areas such as oncology and remote care.[4]European Commission Representation in Germany, “Kommission Startet Leitinitiative Für Mehr Nutzung Von KI Im Gesundheitswesen,” European Commission, germany.representation.ec.europa.eu For instance, CHU de Montpellier is developing sovereign AI infrastructure, attracting interest from 15 additional hospital centers. Europe’s market is expected to prioritize local control and audit-compliant architectures over rapid cloud-only rollouts.

The Middle East is projected to grow at a 42.89% CAGR through 2031, the fastest regional growth rate, fueled by state-backed health transformation programs integrating AI-enabled care delivery. Asia-Pacific is also emerging as a key region, with China’s National Healthcare Security Administration launching the Personal Medical Insurance Cloud initiative in March 2026 to integrate data for 1.33 billion insured individuals. Workforce pressures, telehealth expansion, and large public digital programs are driving adoption in both regions.

Competitive Landscape

The healthcare agentic artificial intelligence market is moderately fragmented, with a concentrated platform layer and workflow-focused specialists. Major technology firms like Microsoft, Google, Amazon, and Oracle compete on model access, enterprise relationships, and integration depth. Microsoft emphasized healthcare-specific models in 2025, while Oracle advanced AI-driven EHR workflows and clinical note generation. Meanwhile, specialized vendors excel in narrower categories where outcome proof outweighs broad platform coverage, maintaining market fragmentation below the top tier.

Commercial success in this market hinges on proven operational or clinical impact. Oracle’s Clinical AI Agent saved over 200,000 clinician hours and reduced documentation time by 41% at AtlantiCare emergency departments, offering concrete workflow benefits. Tempus leveraged proprietary data assets, gaining revenue momentum and expanding collaborations with Merck and Gilead. Hippocratic AI launched Polaris 5.0 in 2026, a 5-trillion-parameter system validated by over 7,500 U.S.-licensed clinicians, emphasizing safety and data depth over raw model scale.

Opportunities remain in post-acute care coordination, cross-vendor governance, and multimodal telehealth support. Philips and NVIDIA advanced foundational MRI imaging models in 2025, while OpenAI expanded from healthcare APIs to clinician-facing tools in 2026. Consolidation is expected at the platform layer, but specialized vendors will thrive where local workflow fits, and evidence is critical. Buyers are likely to continue assembling mixed stacks, keeping fragmentation a key market characteristic despite the growing influence of large firms.

Healthcare Agentic AI Industry Leaders

Microsoft Corporation

Google, LLC

Amazon.com, Inc.

IBM Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tempus AI reported Q1 2026 revenue of USD 348.1 million, up 36.1% year-over-year, and announced a multi-year strategic collaboration with Merck to accelerate biomarker discovery using its multimodal Lens platform. The company also expanded its collaboration with Gilead for enterprise-wide access to Lens for oncology pipeline support.

- February 2026: Hippocratic AI launched Polaris 5.0 on April 30, 2026, a 5-trillion-parameter healthcare AI constellation built on 180 million patient interactions and validated by 7,500+ U.S.-licensed clinicians, achieving 99.1% HIPAA-compliant authentication accuracy and 99.75% clinical escalation safety across 7 body systems.

- April 2026: OpenAI launched ChatGPT for Clinicians on April 22, 2026, a free, verified-clinician AI tool powered by GPT-5.4 and tested on 6,924 clinical conversations with 99.6% safety ratings. It was simultaneously released alongside HealthBench Professional, an open benchmark for evaluating LLMs on real clinical tasks across consultation, documentation, and research.

- April 2026: Google DeepMind published its AI co-clinician research on April 30, 2026, demonstrating a dual-agent clinical architecture that performed comparably to or exceeded primary care physicians in 68 of 140 assessed consultation skill areas in randomized simulation studies, with active research collaborations across the U.S., India, Australia, New Zealand, Singapore, and the UAE.

Global Healthcare Agentic AI Market Report Scope

The Agentic AI in Healthcare Market refers to the global market for autonomous and semi-autonomous artificial intelligence systems designed to perform, optimize, and support healthcare-related tasks with minimal human intervention. These AI-powered agents leverage advanced technologies such as large language models (LLMs), multimodal AI, reinforcement learning, and rule-based intelligence to analyze medical data, automate workflows, assist clinical decision-making, enhance patient engagement, and improve operational efficiency across healthcare ecosystems.

The Agentic AI in Healthcare Market is Segmented by Offering (Platforms, Services, and Edge Devices), Deployment (Cloud, On-premise, and Hybrid), Application (Clinical Decision Support and Diagnostics, Patient Engagement and Virtual Nursing, Operational and Administrative Automation, Drug Discovery and Research, and Remote Monitoring and Tele-health), End-User (Hospitals and Health Systems, Ambulatory / Speciality Clinics, Payers and Insurance, Pharmaceutical and Biotech Companies, Patients), Technology (Large-Language-Model Agents, Multi-Modal Autonomous Agents, Reinforcemement-Larning Agents, and Rule-based / Expert Agents), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Agent Platforms |

| Integration and Customization Services |

| Edge Devices and Specialized Hardware |

| Cloud-based |

| On-premise |

| Hybrid |

| Clinical Decision Support and Diagnostics |

| Patient Engagement and Virtual Nursing |

| Operational and Administrative Automation |

| Drug Discovery and Research |

| Remote Monitoring and Tele-health |

| Hospitals and Health Systems |

| Ambulatory / Specialty Clinics |

| Payers and Insurance |

| Pharmaceutical and Biotech Companies |

| Patients (Direct-to-Consumer) |

| Large-Language-Model Agents |

| Multi-Modal Autonomous Agents |

| Reinforcement-Learning Agents |

| Rule-based / Expert Agents |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Offering | Software Agent Platforms | ||

| Integration and Customization Services | |||

| Edge Devices and Specialized Hardware | |||

| By Deployment Mode | Cloud-based | ||

| On-premise | |||

| Hybrid | |||

| By Application | Clinical Decision Support and Diagnostics | ||

| Patient Engagement and Virtual Nursing | |||

| Operational and Administrative Automation | |||

| Drug Discovery and Research | |||

| Remote Monitoring and Tele-health | |||

| By End-User | Hospitals and Health Systems | ||

| Ambulatory / Specialty Clinics | |||

| Payers and Insurance | |||

| Pharmaceutical and Biotech Companies | |||

| Patients (Direct-to-Consumer) | |||

| By Technology | Large-Language-Model Agents | ||

| Multi-Modal Autonomous Agents | |||

| Reinforcement-Learning Agents | |||

| Rule-based / Expert Agents | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the agentic AI in healthcare market?

The agentic AI in healthcare market stands at USD 1.03 billion in 2026 and is projected to reach USD 5.78 billion by 2031.

How fast is agentic AI in healthcare expected to grow through 2031?

The market is forecast to expand at a 42.63% CAGR from 2026 to 2031, which reflects rapid movement from pilot projects to scaled use across clinical and administrative workflows.

Which application area generates the most revenue today?

Clinical decision support and diagnostics leads application revenue with a 29.63% share in 2025, supported by adoption in radiology, oncology, and emergency triage.

Why are hybrid deployments becoming more important in healthcare AI?

Hybrid models are growing at 42.58% CAGR because providers want cloud scalability while keeping latency-sensitive inference and some sensitive data closer to the point of care.

Who are the main buyers of agentic AI tools in healthcare?

Hospitals and health systems remain the largest end-user group with 46.27% of 2025 revenue, but patient-facing and direct-to-consumer channels are growing quickly at 42.78% CAGR.

What is driving competition among vendors in this space?

Buyers are rewarding vendors that show measurable savings, stronger safety controls, and better workflow fit, which is why platform firms, EHR-linked vendors, and specialized clinical AI companies are all active.

Page last updated on: