Agentic AI In Transportation And Smart Mobility Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

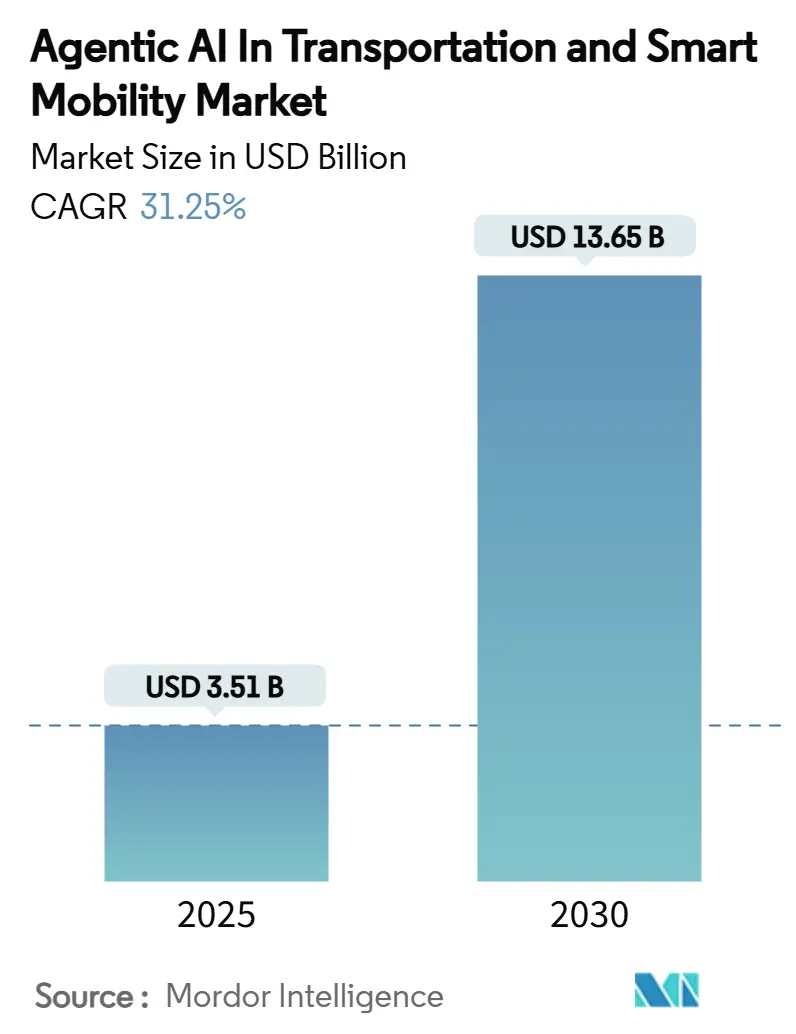

| Market Size (2025) | USD 3.51 Billion |

| Market Size (2030) | USD 13.65 Billion |

| Growth Rate (2025 - 2030) | 31.25% CAGR |

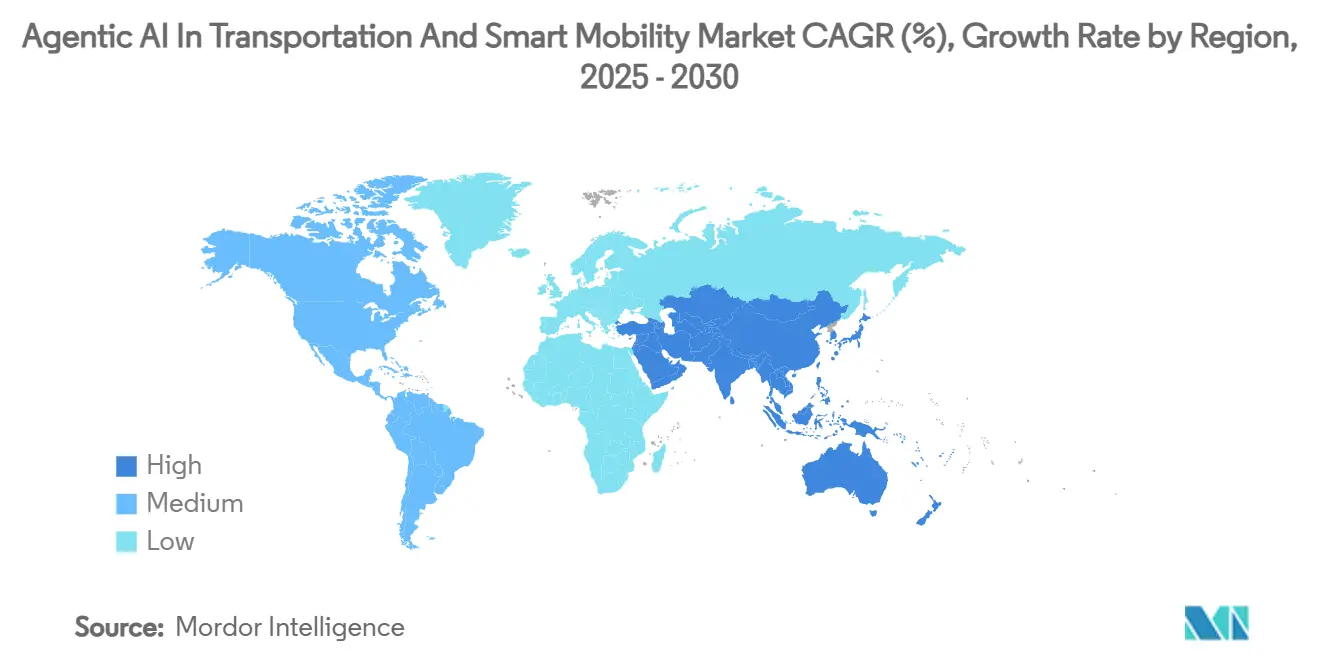

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Transportation And Smart Mobility Market Analysis by Mordor Intelligence

The Agentic AI in transportation and smart mobility market size reached USD 3.51 billion in 2025 and is projected to soar to USD 13.65 billion by 2030, reflecting a robust 31.25% CAGR. Growth is underpinned by a systemic pivot from rule-based automation toward self-learning, decision-autonomous platforms that recalibrate vehicle behavior in real time. Regulatory sandboxes in key automotive hubs, falling onboard compute costs and an aggressive public-private push for vehicle-to-everything (V2X) connectivity are driving faster commercialization cycles. Meanwhile, operators are reallocating capital away from hardware toward data and software layers that deliver lifetime upgradability, thereby compressing total cost of ownership. Competitive positioning is evolving around ecosystem partnerships in which traditional OEMs contribute scale and compliance know-how while AI specialists supply edge-to-cloud learning algorithms that capture cross-fleet network effects. As a result, the Agentic AI in transportation and smart mobility market now represents a critical battleground for both incumbent automakers and digital entrants vying for platform control.

Key Report Takeaways

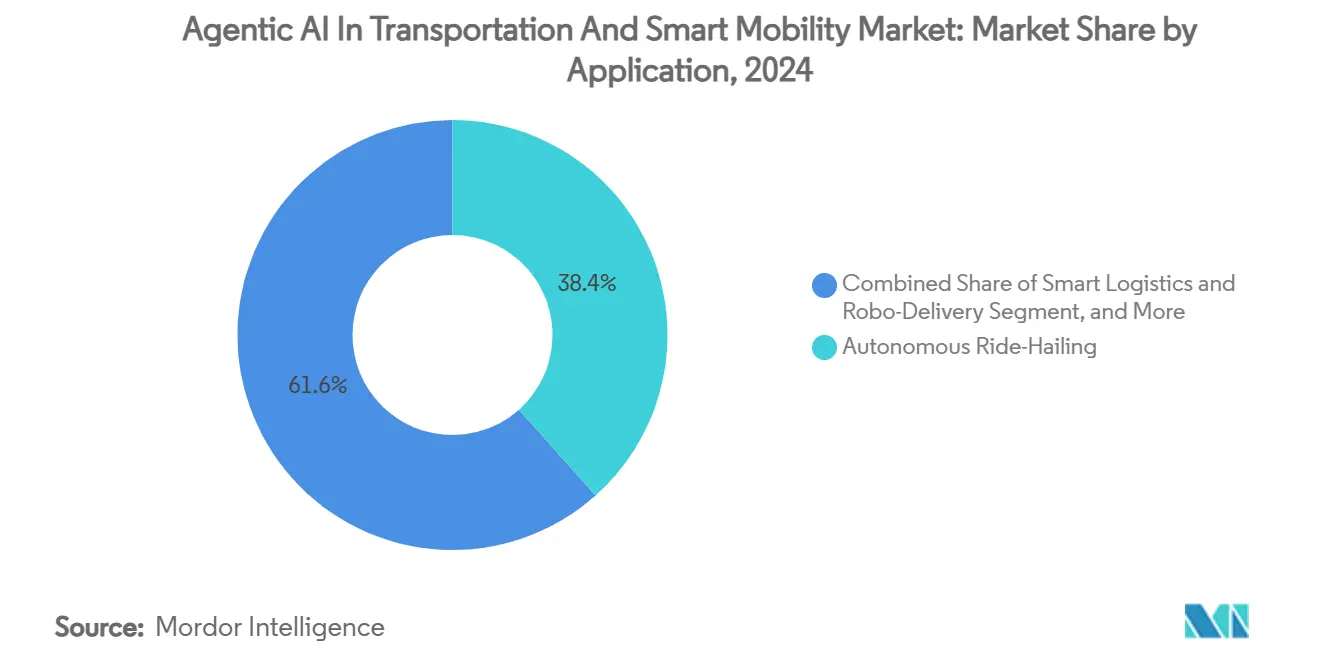

- By application, Autonomous Ride-Hailing held 38.41% of the Agentic AI in transportation and smart mobility market share in 2024, whereas Emergency & Roadside Assistance is advancing at a 35.23% CAGR to 2030.

- By offering, the Software Stack segment commanded 42.15% of the Agentic AI in transportation and smart mobility market size in 2024, while Data & Simulation Services are expanding at a 38.65% CAGR between 2025-2030.

- By deployment mode, Edge/On-Vehicle architectures retained 43.62% share of the Agentic AI in transportation and smart mobility market size in 2024 and Hybrid Edge-Cloud solutions are forecast to accelerate at 36.23% CAGR through 2030.

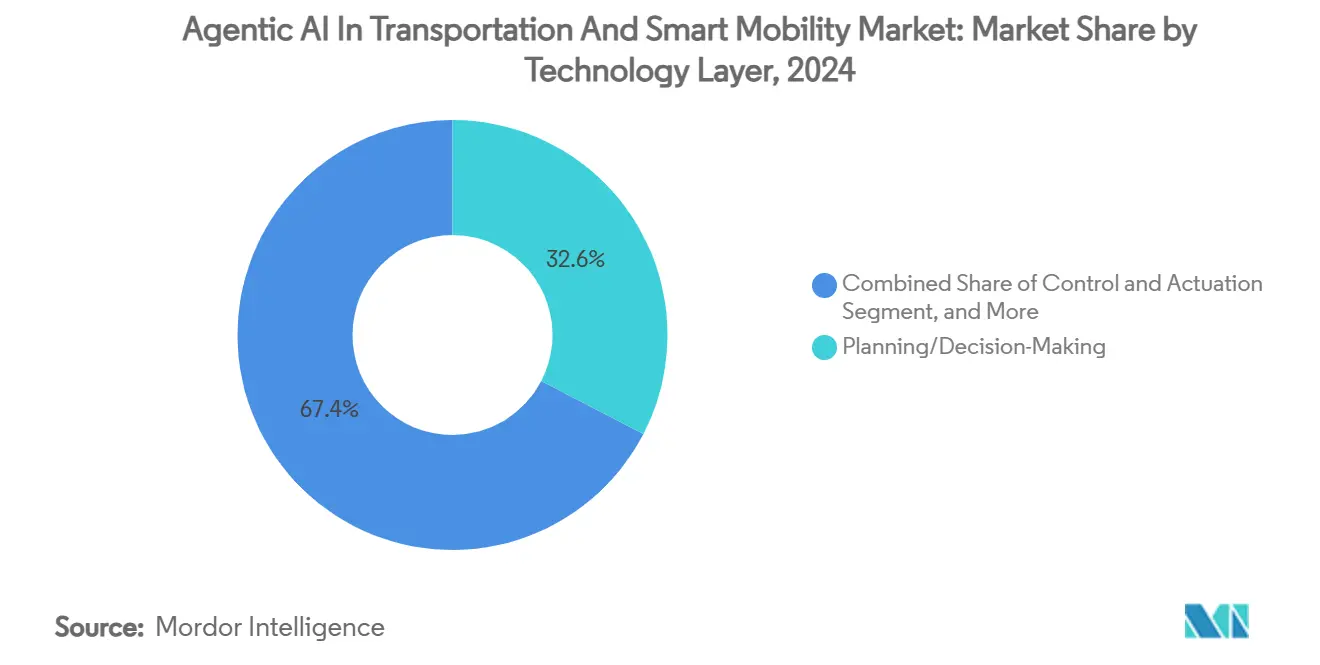

- By technology layer, Planning/Decision-Making platforms led with 32.61% revenue share in 2024; Edge-to-Cloud Learning is projected to grow at a 38.95% CAGR across the period.

- By transportation mode, Passenger Cars accounted for 42.59% of the Agentic AI in transportation and smart mobility market share in 2024, while Air Mobility eVTOL/UAM solutions are set to climb at a 39.06% CAGR to 2030.

- By geography, North America accounted for 38.53% of the Agentic AI in transportation and smart mobility market share in 2024, while Asia-Pacific are set to climb at a 34.26% CAGR to 2030.

Global Agentic AI In Transportation And Smart Mobility Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM push for L4/L5 automated platforms | +8.2% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Regulatory incentives for V2X-enabled safety | +6.8% | North America & EU primary, APAC emerging | Short term (≤ 2 years) |

| Rising urban congestion costs | +5.4% | Global urban centers, highest impact in APAC megacities | Long term (≥ 4 years) |

| Rapid drop in onboard AI compute $/TOPS | +7.1% | Global, with fastest adoption in cost-sensitive APAC markets | Short term (≤ 2 years) |

| Fleet-wide self-optimising agentic algorithms | +4.9% | North America & EU commercial fleets, expanding to APAC | Medium term (2-4 years) |

| Carbon-credit monetisation via agentic eco-routing | +3.8% | EU regulatory framework, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Push for L4/L5 Automated Platforms

Automakers have earmarked multi-billion-dollar war chests to accelerate Level 4 and Level 5 programs. Hyundai Motor Group alone committed USD 21 billion for 2025-2028, allocating USD 6 billion to autonomous driving and robotics partnerships that fuse edge inference with centralized training.[1]Hyundai Motor Group, “Hyundai Motor Group Commits to U.S. Growth with USD 21 Billion Investment,” hyundaimotorgroup.com Toyota’s USD 13 billion plan signals that competitive advantage is migrating from mechanical engineering prowess to learning-centric software differentiation. The capital outlay is simultaneously de-risking adoption for Tier-1 suppliers and startups that can plug-in modular planning stacks. Consequently, the Agentic AI in transportation and smart mobility market is becoming integral to long-term brand equity as vehicles transition into continuously improving software platforms.

Regulatory Incentives for V2X-Enabled Safety

Mandates for V2X equipment and AI auditability are altering purchase criteria for fleet operators. The U.S. Department of Transportation now ties autonomous testing permits to evidence of explainable decision frameworks.[2]U.S. Department of Transportation, “Connected Vehicle Infrastructure Investment,” transportation.gov Parallel provisions under the EU AI Act assign liability according to algorithmic transparency, nudging adopters toward agentic systems able to document learning provenance. Early compliance winners gain preferential access to controlled test corridors, enhancing data flywheels that further widen capability gaps. Japan’s green-light for driverless operations on 25 roads by March 2025 entrenches the practice of proving learn-and-adapt logic in real traffic, catalysing demand across the Agentic AI in transportation and smart mobility market.

Rising Urban Congestion Costs

City governments face rising congestion-driven productivity losses-USD 87 billion annually in the United States alone—and are shifting procurement toward AI-adaptive traffic control. Google’s Green Light deployment in 70 cities trimmed signal delays by up to 20% while cutting fuel burn 15%, validating tangible return on investment for agentic traffic orchestration.[3]Google, “Green Light Traffic Optimization Project,” google.com Municipalities therefore view such systems as a direct lever to reclaim GDP drag and meet climate goals. The feedback loop between enhanced emergency response times and public acceptance is further emboldening investments, reinforcing the long-run demand trajectory for the Agentic AI in transportation and smart mobility market.

Rapid Drop in Onboard AI Compute USD/TOPS

Automotive-qualified silicon costs plummeted from USD 2,000 per TOPS in 2023 to under USD 800 in 2024 as specialized architectures like NVIDIA Thor delivered 2,000+ TOPS within a 1,000-watt envelope. Similar cost curves from Horizon Robotics are widening accessibility across mid-tier vehicle classes. Once compute outlays fall beneath those of sensor redundancy, managerial economics favor intelligence over hardware excess, accelerating install rates throughout the Agentic AI in transportation and smart mobility market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse edge-cloud 5G coverage outside Tier-1 cities | -4.2% | Global, most severe in rural North America & developing APAC regions | Medium term (2-4 years) |

| High ASP for automotive-grade AI SoCs | -3.8% | Cost-sensitive markets in APAC & Latin America | Short term (≤ 2 years) |

| Cyber-physical liability gaps for autonomous agents | -5.1% | Global regulatory uncertainty, most acute in North America & EU | Long term (≥ 4 years) |

| Public skepticism toward self-learning AV logic | -4.6% | Western markets with high AV awareness, particularly North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Edge-Cloud 5G Coverage Outside Tier-1 Cities

Connectivity shortfalls force vehicles to default to local inference, throttling the real-time collaboration needed for swarm learning. Operators consequently deploy dual-mode stacks that raise bill-of-materials and complicate operational policies when fleets roam between coverage zones. Competitive advantage therefore concentrates in urban cores, limiting scale efficiencies for nationwide services and tempering growth expectations within the Agentic AI in transportation and smart mobility market.

Public Skepticism Toward Self-Learning AV Logic

Surveys reveal 61% of U.S. adults fear self-driving technology, with just 13% extending trust to learning-based platforms. Liability studies show the public assigns more blame to autonomous service providers than to human drivers in identical crash scenarios. To bridge the trust gap, industry coalitions such as PAVE are staging live demonstrations, yet adoption curves remain sensitive to high-visibility incidents. Reputation risk therefore imposes conservative rollout cadences, dampening near-term volume expectations despite technological readiness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Emergency Services Drive Innovation

Emergency & Roadside Assistance is forecast to surge at 35.23% CAGR, even as Ride-Hailing retained the largest 38.41% revenue share of the Agentic AI in transportation and smart mobility market in 2024. Deployment in 911 dispatch centers has cut average response times 25-40%, a performance delta that municipalities willingly underwrite through premium service contracts. Ride-Hailing pioneers meanwhile exploit cross-fleet learning to minimise pick-up latency, but profit pools are increasingly contested by logistics operators repurposing agentic routing engines.

The Agentic AI in transportation and smart mobility market is also seeing Smart Logistics and Robo-Delivery platforms unlock 30% energy savings by adjusting routes in line with live demand clusters. Public Transit Optimisation tools allocate bus capacity dynamically, reducing idle miles while boosting passenger satisfaction. Advanced Traffic Management integrates with these services to deliver city-scale coordination, creating data network effects where algorithmic insights from ride-sharing feed emergency services and vice versa. Stakeholders consequently prioritise openness standards to preserve interoperability across growing application constellations.

By Offering: Data Services Accelerate Growth

Software Stack solutions captured 42.15% of 2024 revenue, yet Data & Simulation Services are expanding 38.65% annually as safety regulators insist on millions of virtual test miles before public deployment. Operators favour simulation-native validation flows that reduce expensive on-road trials and shorten certification lead times. Consulting services are gaining momentum as legacy fleets struggle with retro-fit complexity and compliance uncertainty.

Hardware remains essential for sensor fusion latency but faces commoditisation pressure. Hence, value creation is migrating toward lifelong learning loops that update vehicle behaviour post-sale. This shift unlocks recurring revenue models that appeal to capital-market investors chasing software-like margins, ensuring sustained momentum for the Agentic AI in transportation and smart mobility market.

By Deployment Mode: Hybrid Architectures Gain Momentum

Edge/On-Vehicle processing still accounts for 43.62% of the Agentic AI in transportation and smart mobility market size, primarily to guarantee sub-10 millisecond latency for collision avoidance. However, Hybrid Edge-Cloud approaches are scaling 36.23% annually as operators offload non-critical computation to cloud GPUs, lowering vehicle unit cost while preserving safety envelopes.

Cloud-Only models are reserved for depot-based use cases such as autonomous yard tractors where deterministic connectivity is assured. Infrastructure-Centric schemes flourish in closed campuses like ports, where a single control tower orchestrates fleets to achieve near-zero downtime. This architectural pluralism enables providers to tailor cost-performance profiles to operational contexts, further broadening addressable demand.

By Technology Layer: Learning Systems Lead Growth

Planning/Decision-Making software contributed 32.61% of 2024 revenue and remains indispensable; however, Edge-to-Cloud Learning modules are set to grow 38.95% as fleets recognise that resilient performance stems from perpetual adaptation rather than one-off feature releases. Perception stacks have reached component maturity, spawning open-standard interfaces that lower switching costs.

Control and Actuation software is integrating driver preference models patented by Ford, enabling vehicles to personalise dynamics without compromising regulatory compliance. The aggregation of these layers into unified DevOps pipelines ensures over-the-air updates propagate seamlessly, which in turn elevates customer lifetime value within the Agentic AI in transportation and smart mobility market.

By Transportation Mode: Air Mobility Emerges

Passenger Cars maintained 42.59% revenue share, yet Air Mobility eVTOL/UAM platforms are registering a 39.06% CAGR as urban air corridors become operational. eVTOL developers such as Supernal rely on agentic flight-path optimisers that judiciously manage battery state, weather volatility and three-dimensional traffic.

Commercial Road Freight fleets embed eco-routing agents that balance load weight, delivery windows and refuelling stops, trimming diesel consumption 8-12% across pilot programs. Micro-Mobility operators focus on fleet-wide charge orchestration, while rail incumbents deploy predictive maintenance agents to avoid unplanned stoppages. Cross-modal reuse of learning models accelerates innovation cycles, securing expansion capacity for the Agentic AI in transportation and smart mobility market across diverse transport verticals.

Geography Analysis

North America accounted for 38.53% of global revenue in 2024, a position reinforced by USD 1.2 billion in federal grants for connected infrastructure and a permissive state-level testing regime. U.S. venture investors injected over USD 1 billion into agentic innovators such as Wayve, signalling confidence in software-centric platforms. Canadian smart-city pilots, notably Toronto’s Quayside redevelopment, provide live laboratories where mobility, energy and public safety data converge to refine cross-domain agents.

Asia-Pacific is the fastest-growing region with a 34.26% CAGR. China’s Apollo program reached 10-city commercial scale, while South Korea earmarked KRW 1.1 trillion (USD 825 million) to leapfrog toward Level 4 capabilities. Japan’s designation of driverless corridors funnels real-world data into edge-cloud learning pools, reinforcing first-mover advantages and attracting semiconductor investment that underpins cost leadership. Local manufacturers of AI accelerators further democratise adoption, deepening the Agentic AI in transportation and smart mobility market’s reach.

Europe maintains resilient expansion under the EU AI Act’s structured liability provisions that reward explainable AI. German premium OEMs co-develop decision stacks with chipmakers to meet stringent TÜV safety thresholds, while Nordic countries experiment with carbon-credit marketplaces that monetise eco-routing outputs. Pan-regional focus on privacy mandates encryption-by-design data transfer, compelling vendors to refine federated learning schemes and strengthening buyer confidence in agentic offerings.

Competitive Landscape

The Agentic AI in transportation and smart mobility market demonstrates moderate concentration as ecosystem alliances replace fully vertical models. Hyundai’s USD 6 billion collaboration with Boston Dynamics and NVIDIA anchors a strategy of combining robotic platforms with high-throughput inference engines. Similar tie-ups between General Motors and Cruise or Ford and Argo AI reflect a shared logic: speed to market trumps proprietary isolation when regulatory clocks are ticking.

Emerging pure-play disruptors leverage end-to-end neural architectures to sidestep handcrafted rules, enabling rapid geographic redeployment. Wayve’s fund-raise earmarks resources for cloud-based simulation and edge-deployed learning loops that require minimal HD mapping, shrinking rollout overhead. Patent data indicates Tesla is entrenching defensibility around over-the-air adaptation layers, potentially opening licensing revenue as industry peers seek shortcut access.

White-space opportunities abound in high-stakes niches such as emergency response, port logistics and urban air mobility. Incumbent Tier-1 suppliers possess limited domain expertise here, allowing startups to lock in early adopters through performance guarantees. As simulation libraries scale, data-network effects will likely concentrate algorithmic performance leadership in a handful of platform providers, reshaping bargaining power across the Agentic AI in transportation and smart mobility market.

Agentic AI In Transportation And Smart Mobility Industry Leaders

Waymo LLC

Tesla, Inc.

Mobileye Global Inc.

Cruise LLC

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Motor Group confirmed a USD 21 billion U.S. expansion that allocates USD 6 billion for autonomous and robotics R&D aimed at shortening L4 validation cycles. Strategically, the move localises production near premium customer clusters while securing political goodwill for large-scale pilot deployments.

- February 2025: Motional completed a driver’s-license-style safety test for its IONIQ 5 robotaxi, aligning AV validation with established consumer mental models to enhance public acceptance and streamline regulator approvals.

- January 2025: Japanese regulators approved driverless operations on 25 routes, offering a sandbox for OEMs to refine edge-cloud learning flows under live conditions and advance toward nationwide deployment horizons.

- December 2024: Google expanded its Green Light traffic management to 70 global cities, locking-in municipalities via measurable congestion and emission reductions that create switching-cost barriers for competing solutions.

Global Agentic AI In Transportation And Smart Mobility Market Report Scope

| Autonomous Ride-Hailing |

| Smart Logistics and Robo-Delivery |

| Public Transit Optimisation |

| Advanced Traffic Management |

| Emergency and Roadside Assistance |

| Software Stack |

| AI Compute Hardware |

| Data and Simulation Services |

| Integration and Consulting |

| Edge/On-Vehicle |

| Cloud-Based |

| Hybrid Edge-Cloud |

| Infrastructure-Centric (Roadside/Control-Center) |

| Perception and Sensor Fusion |

| Planning/Decision-Making |

| Control and Actuation |

| Edge-to-Cloud Learning |

| Passenger Cars |

| Commercial Road Freight |

| Micro-Mobility |

| Rail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Application | Autonomous Ride-Hailing | |

| Smart Logistics and Robo-Delivery | ||

| Public Transit Optimisation | ||

| Advanced Traffic Management | ||

| Emergency and Roadside Assistance | ||

| By Offering | Software Stack | |

| AI Compute Hardware | ||

| Data and Simulation Services | ||

| Integration and Consulting | ||

| By Deployment Mode | Edge/On-Vehicle | |

| Cloud-Based | ||

| Hybrid Edge-Cloud | ||

| Infrastructure-Centric (Roadside/Control-Center) | ||

| By Technology Layer | Perception and Sensor Fusion | |

| Planning/Decision-Making | ||

| Control and Actuation | ||

| Edge-to-Cloud Learning | ||

| By Transportation Mode | Passenger Cars | |

| Commercial Road Freight | ||

| Micro-Mobility | ||

| Rail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected CAGR for the Agentic AI in transportation and smart mobility market through 2030?

The market is forecast to grow at a 31.25% CAGR between 2025 and 2030.

Which application currently dominates revenue?

Autonomous Ride-Hailing captured 38.41% of 2024 revenue.

Why are Data & Simulation Services growing faster than hardware sales?

Regulators require extensive virtual testing, and operators prefer flexible software subscriptions to hardware upgrades.

What geographic region is expanding the quickest?

Asia-Pacific is advancing at a 34.26% CAGR due to aggressive public funding and manufacturing cost advantages.

How are OEMs addressing public skepticism about self-learning AVs?

Strategies include transparent safety demonstrations, driver’s-license-style tests and partnerships with education coalitions such as PAVE.

What deployment architecture best balances latency and scalability?

Hybrid Edge-Cloud models run safety-critical tasks onboard and offload optimization to cloud resources, achieving both responsiveness and cost efficiency.

Page last updated on: