Agentic AI In The Supply Chain And Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

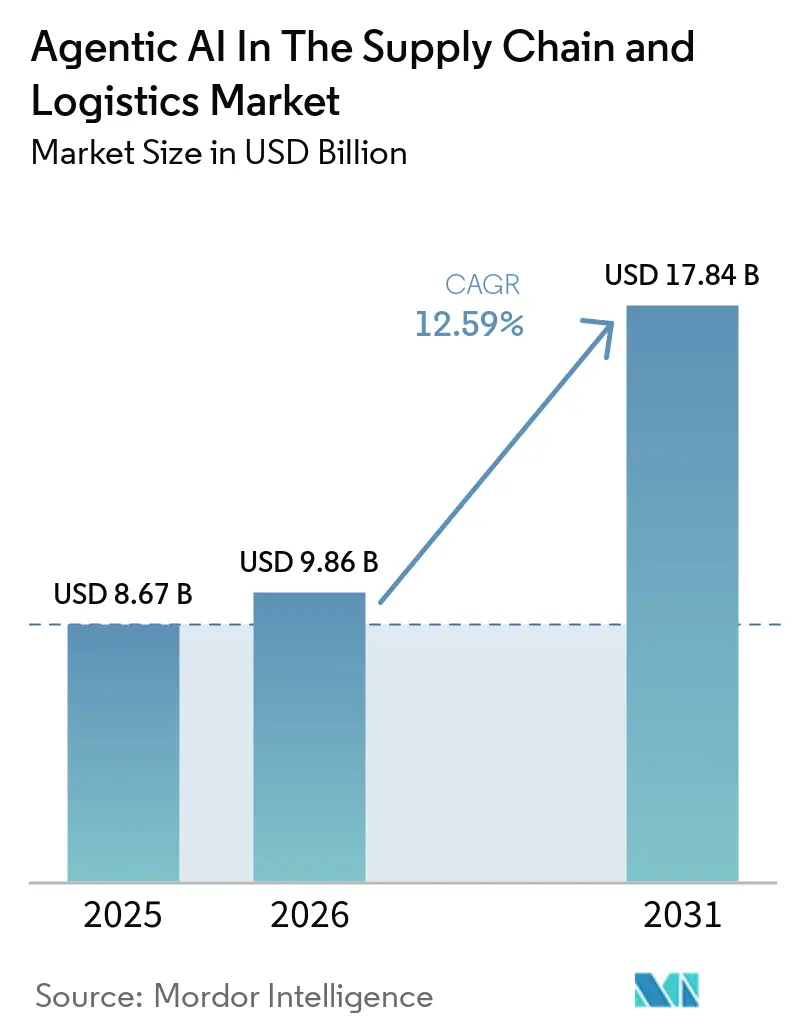

| Market Size (2026) | USD 9.86 Billion |

| Market Size (2031) | USD 17.84 Billion |

| Growth Rate (2026 - 2031) | 12.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In The Supply Chain And Logistics Market Analysis by Mordor Intelligence

The agentic AI market in the supply chain and logistics market is expected to grow from USD 9.86 billion in 2026 to USD 17.84 billion by 2031, expanding at a CAGR of 12.59% over the same period. Enterprises are moving past rule-based automation toward autonomous multi-agent systems that make real-time decisions across procurement, warehousing, transportation, and last-mile delivery. Software platforms delivered more than half of 2025 revenue, yet falling sensor and compute prices are lifting demand for AI-enabled hardware and converged edge-robotics solutions. Early adopters report double-digit productivity gains, attracting fresh investment even as regulatory compliance costs climb. Competitive intensity is rising because cloud hyperscalers embed agentic functions directly into supply-chain suites, while specialist vendors supply composable agent modules that integrate via open APIs.

Key Report Takeaways

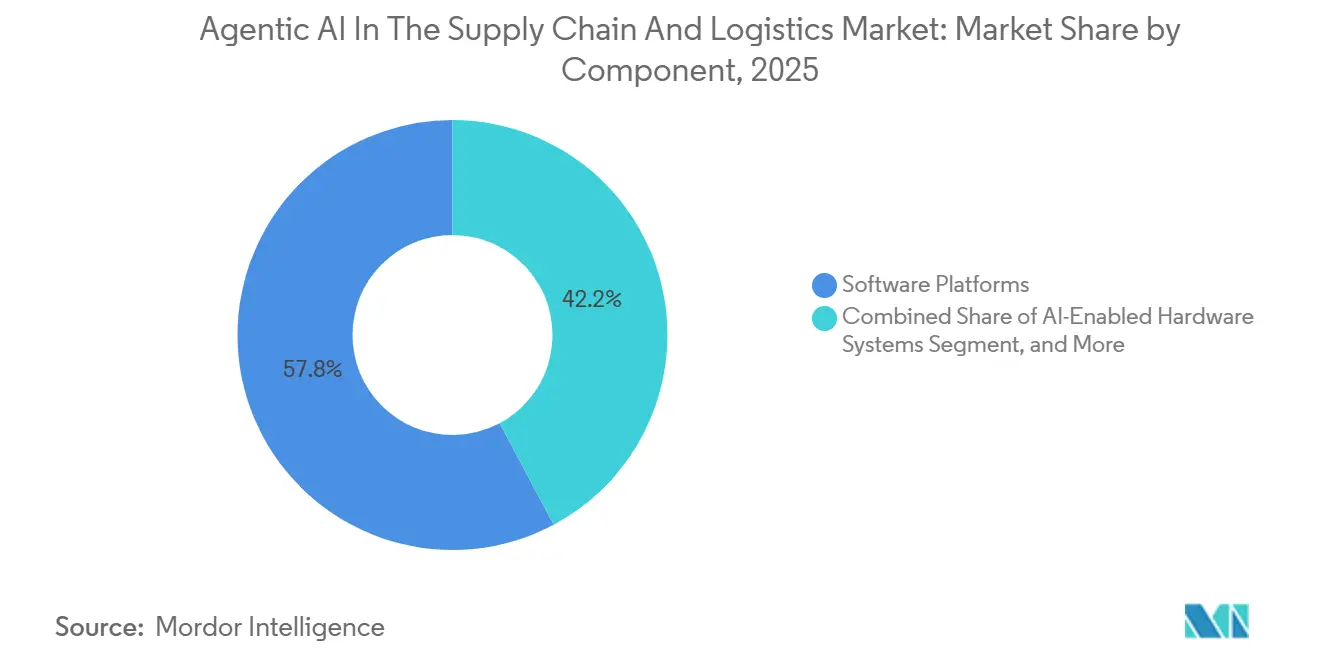

- By component, software platforms captured 57.81% of 2025 revenue, while AI-enabled hardware is projected to post the strongest 13.19% CAGR through 2031.

- By application, demand forecasting and planning led with 35.83% of 2025 sales; last-mile delivery orchestration is forecast to advance at the fastest 13.79% CAGR over 2026-2031.

- By deployment model, cloud-based solutions accounted for 62.89% of 2025 spend, whereas hybrid architectures are set to register a 13.08% CAGR as firms balance latency with data-sovereignty mandates.

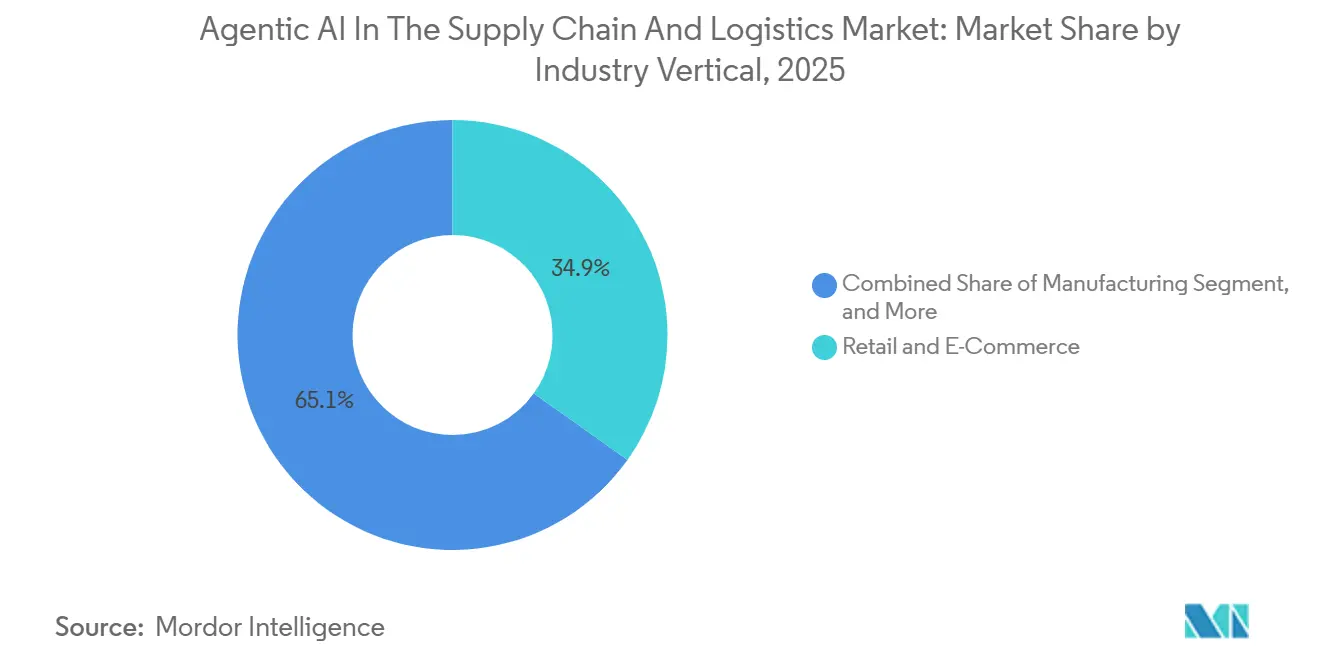

- By industry vertical, retail and e-commerce delivered 34.88% of 2025 demand, while healthcare and pharmaceuticals are on track for the highest 13.67% CAGR through 2031.

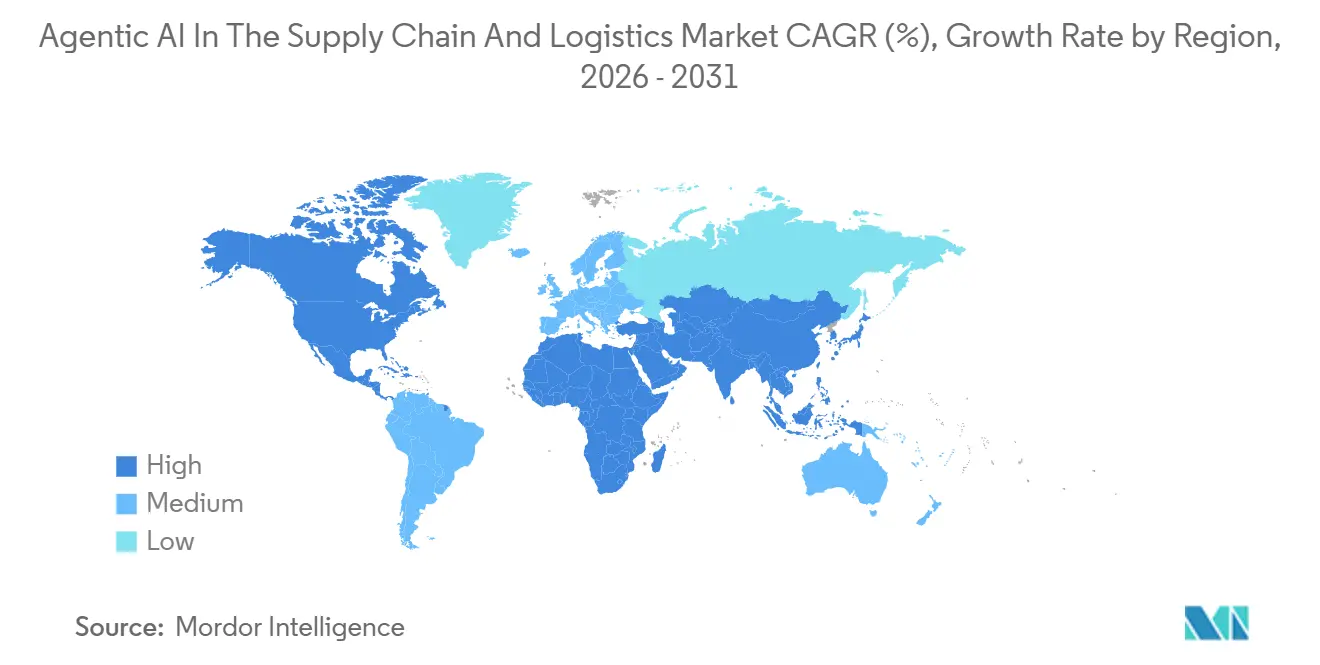

- By geography, North America accounted for 41.83% of 2025 revenue, yet Asia-Pacific is expected to log the fastest 13.59% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In The Supply Chain And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud-Native SCM Platforms With Embedded AI Agents | +3.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Labor Shortages Accelerating Warehouse Automation Investments | +2.8% | North America, Western Europe, Japan, Australia | Short term (≤ 2 years) |

| Declining Sensor and Compute Costs Enabling Affordable AI-Enabled Hardware | +2.1% | Global, with rapid uptake in Asia-Pacific and South America | Medium term (2-4 years) |

| Surging Demand for Explainable Agent Governance Frameworks Post EU AI Act | +1.6% | Europe, spillover to North America and Asia-Pacific | Long term (≥ 4 years) |

| Rising Usage of Real-Time Emissions Data for Carbon-Aware Routing Incentives | +1.4% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Emergence of Autonomous Multi-Agent Benchmark Datasets Standardizing Procurement KPIs | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Native SCM Platforms With Embedded AI Agents

Cloud hyperscalers now ship multi-agent tools as part of their supply-chain suites, removing integration friction and cutting decision latency from hours to seconds. Amazon Web Services introduced Connect Decisions in May 2025, while Oracle and SAP followed with embedded agents for demand sensing, freight booking, and customs documentation. Mid-market enterprises lacking in-house AI talent can activate these capabilities through subscription tiers, though platform lock-in risk increases once decision histories accumulate inside proprietary clouds.

Labor Shortages Accelerating Warehouse Automation Investments

Low unemployment and high worker turnover push logistics operators to deploy autonomous mobile robots and humanoid systems controlled by multi-agent frameworks. UPS directed USD 120 million toward AI-driven unloading equipment in 2025, and GXO Logistics reported 22% productivity gains after rolling out Dexterity and Agility Robotics pilots across several sites. Real estate design norms are shifting toward robot-friendly layouts, marginalizing legacy facilities that cannot accommodate automated workflows.

Declining Sensor and Compute Costs Enabling Affordable AI-Enabled Hardware

NVIDIA’s Jetson Orin Nano, priced at USD 249, delivers 40 TOPS of performance, making it a cost-effective solution for edge AI applications. Similarly, Qualcomm’s Cloud AI 100 Ultra is specifically designed to cater to edge inference needs in industries such as fleet management and warehouse operations. These advancements in hardware economics enable regional carriers to implement technologies such as vision-guided picking systems and autonomous route optimization without incurring recurring cloud service charges. As a result, the competitive advantage in these sectors is shifting away from mere access to computational power and is now increasingly dependent on the quality of data and the efficiency of multi-agent coordination algorithms.

Surging Demand for Explainable Agent Governance Frameworks Post EU AI Act

The EU AI Act classifies supply-chain agents that influence worker scheduling or carrier selection as limited-risk, but it mandates audit logs and human override. SAP, Microsoft, and IBM launched governance modules that translate agent reasoning into plain language and flag anomalous decisions in 2025-2026.[1]European Commission, “EU AI Act,” ec.europa.eu Symbolic and hybrid neuro-symbolic models thus gain favor over opaque deep-learning approaches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Analysis |

|---|---|---|---|

| High Integration Costs With Legacy ERP and TMS Systems | -1.8% | Global, acute in North America and Europe with mature IT estates | Short term (≤ 2 years) |

| Data Privacy and Sovereignty Regulations Increasing Compliance Burdens | -1.4% | Europe, China, India, with spillover to multinational operators | Medium term (2-4 years) |

| Scarcity of Domain-Specific Simulation Sandboxes Limiting RL Agent Training | -0.9% | Global, most acute in emerging markets lacking digital-twin infrastructure | Long term (≥ 4 years) |

| Enterprise Change-Management Fatigue From Multi-Agent Workflow Overhauls | -0.7% | Global, particularly in industries with unionized workforces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Costs With Legacy ERP and TMS Systems

Most mid-market operators continue to rely on monolithic databases that use batch updates, which limits their ability to adopt advanced technologies such as event-driven streams for multi-agent AI systems. Transitioning to such systems involves high costs, ranging from USD 5 million to USD 20 million per distribution network, and the implementation process can take up to 3 years. Additionally, each agent platform employs its own proprietary ontologies, necessitating the development of custom middleware solutions. This requirement further complicates the adoption process and exacerbates the productivity disparities between large enterprises, which have the resources to manage such transitions effectively, and smaller enterprises, which often struggle to keep pace.

Data Privacy and Sovereignty Regulations Increasing Compliance Burdens

China’s Personal Information Protection Law and India’s Digital Personal Data Protection Act mandate that personal data be stored and processed locally within their respective jurisdictions. This requirement forces logistics networks to implement region-specific agent instances that synchronize operations across fragmented silos while adhering to local regulations.[2]Ministry of Electronics and Information Technology India, “Digital Personal Data Protection Act,” meity.gov.in Furthermore, the EU AI Act introduces additional documentation requirements, significantly increasing compliance costs for businesses. These heightened regulatory demands are particularly challenging for smaller providers, often driving them to establish regional sub-networks with restricted cross-border coordination to manage costs and ensure compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Upswings Amid Platform Dominance

AI-driven software captured 57.81% of the total 2025 revenue in the agentic AI market for supply chain and logistics. The agentic AI in the supply chain and logistics market size for hardware is on course to grow faster at 13.19% as edge inference converges with robotics. Falling chip prices and pre-integrated perception stacks shorten payback periods, bringing autonomous forklifts and vision-guided picking within reach of regional carriers. Services revenue scales as integrators retrofit legacy systems, tune vertical agents, and train supervisors. Software suites continue to benefit from consumption pricing and pre-existing cloud relationships, so they remain the entry point for most newcomers.

Enterprises adopt hardware once they trust the orchestration logic resident in their platforms. Jetson-powered robots and Gaudi-based conveyors are bundled with reference agents that slot into leading cloud SCM suites, shrinking integration effort. Hyperscalers thus monetize both subscription software and certified device ecosystems, while robotics vendors differentiate on specialized gripper design, sensor fusion, and safety certifications.

By Application: Last-Mile Orchestration Accelerates

Demand forecasting led 2025 allocation at 35.83% because most retailers and manufacturers already collect the data needed for time-series and causal models. Last-mile orchestration, however, will log the fastest 13.79% CAGR as dense cities, same-day expectations, and labor shortages collide. FedEx pilots achieve 15% reductions in delivery costs when RFID and route-planning agents coordinate vehicles and sidewalk robots. Warehouse optimization remains a core area, as annual U.S. warehouse turnover exceeded 43% and 400,000 vacancies in 2025.

Procurement agents gain traction as benchmark datasets standardize supplier performance, while carbon-aware fleet routing embeds real-time emissions data to satisfy sustainability mandates. Reverse logistics and cross-docking remain niche but rise gradually with e-commerce returns and circular-economy rules. Each sub-segment taps different data modalities, yet all require multi-agent coordination to eliminate manual bottlenecks.

By Industry Vertical: Healthcare Cold Chains Gain Momentum

Retail and e-commerce accounted for 34.88% of 2025 spending, but healthcare and pharmaceuticals are set to expand by 13.67% through 2031 as serialization and cold-chain traceability rules take effect. Cardinal Health invested USD 1.5 billion to modernize its distribution by implementing multi-agent temperature monitoring and autonomous inventory control. Food and beverage operators deploy similar orchestration for chilled products, and automotive manufacturers digitize just-in-time networks for greater resilience.

The agentic AI in the supply chain and logistics industry increasingly supports domain-specific templates to shorten configuration times. Healthcare agents embed regulatory workflows for the U.S. Food Safety Modernization Act Section 204, while automotive suites model multi-tier supplier lead times and risk scores. These vertical layers promote higher average selling prices yet require deep process expertise from vendors and integrators.

By Deployment Model: Hybrid Balances Latency and Regulation

Cloud-hosted solutions accounted for 62.89% of 2025 deployments inside the agentic AI in supply chain and logistics market. Edge-heavy hybrid architectures, however, will notch a 13.08% CAGR as operators push latency-sensitive agents, such as task assignment and collision avoidance, to local servers while retaining cloud training loops. China’s localization mandates and similar rules in India drive multinationals toward region-specific hybrid clusters.

Hybrid arrangements reduce the 50-200 millisecond cloud round-trip, improving robot throughput and worker collaboration. GXO Logistics observed 22% productivity lifts after running vision inference on-prem and syncing anonymized metrics to the cloud for retraining. On-premise pure plays remain confined to defense contractors and tightly regulated markets because they require in-house AI talent and larger capital budgets.

Geography Analysis

North America accounted for 41.83% of 2025 revenue, thanks to mature cloud infrastructure and early adoption by Amazon, UPS, and FedEx. Public-sector incentives for domestic semiconductor fabrication also support the expansion of the edge hardware ecosystem. Europe grows more slowly because the EU AI Act adds documentation overhead, though carbon-aware routing subsidies partially offset compliance costs.

Asia-Pacific is forecast to post the fastest 13.59% CAGR through 2031 as China, India, and Japan channel more than USD 50 billion in sovereign AI funding into domestic hardware and large language models. China’s State Council earmarked supply-chain applications, prompting provincial grants for smart ports and bonded-zone logistics. India’s startup scene brings agentic procurement tools to small manufacturers, and Japan’s aging workforce propels robot adoption in distribution centers.

South America advances as Brazilian e-commerce surpasses half the population, spurring demand for autonomous delivery in São Paulo and Rio de Janeiro. Argentina pursues AI-guided freight matching despite macro volatility, while limited broadband in parts of the region slows cloud uptake. The Middle East and Africa remain early-stage, yet the United Arab Emirates and Saudi Arabia fold agentic AI into national logistics corridors aligned with diversification strategies.[3]Saudi Vision 2030, “Logistics Investments,” vision2030.gov.sa

Competitive Landscape

The agentic AI market in supply chain and logistics is moderately fragmented. Cloud hyperscalers, Amazon Web Services, Microsoft Azure, and Google Cloud, bundle embedded agents with consumption billing, locking clients into end-to-end ecosystems. Enterprise software incumbents, such as SAP, Oracle, and Blue Yonder, augment ERP and WMS suites with orchestration layers to defend installed bases. Robotics specialists, including Locus Robotics and Dexterity, differentiate on teleoperation fallback, safety certifications, and rapid-deployment kits.[4]Locus Robotics, “2 Billion Picks Milestone,” locusrobotics.com

White space opens in cold-chain orchestration, reverse logistics, and cross-border compliance, where failure costs are high and regulations are complex. Semiconductor vendors partner with software firms to accelerate inference and reduce power consumption, turning chips into essential components of solution stacks. The battleground shifts from isolated capabilities to data pipeline control, ecosystem breadth, and total cost of ownership.

Startups offering API-first, composable agents are increasingly attracting enterprises cautious about vendor lock-in. These startups provide flexible solutions that allow businesses to integrate and customize their systems without being tied to a single provider. However, despite the appeal of such flexibility, switching costs continue to rise as historical decision logs and operational data become deeply embedded within a specific cloud infrastructure. This creates a significant barrier to change, making it challenging for enterprises to transition to alternative platforms. To address this complexity, specialist integrators have identified an opportunity to bridge the gap by offering turn-key solutions for converting legacy facilities into modern, adaptable systems. These integrators capitalize on the intricate nature of such transitions, further reinforcing a multi-tier competitive hierarchy within the market.

Agentic AI In The Supply Chain And Logistics Industry Leaders

Blue Yonder, Inc.

Microsoft Corporation

SAP SE

Kinaxis Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP released its Logistics Management module to general availability, adding Joule conversational agents for freight booking and customs documentation, and positioning itself as a single-platform option for global operators.

- January 2026: GXO Logistics rolled out Dexterity and Agility Robotics systems across 15 more sites, with early data showing 22% productivity gains and 18% fewer injuries.

- December 2025: Blue Yonder completed the Luminate platform upgrade, enabling autonomous demand forecasting and supplier collaboration for 3,000 customers.

- October 2025: FedEx began deploying last-mile agentic AI and RFID integration to cut per-package delivery costs by 15%.

Global Agentic AI In The Supply Chain And Logistics Market Report Scope

The Agentic AI in Supply Chain and Logistics Market refers to the global industry focused on developing, deploying, and commercializing autonomous and semi-autonomous artificial intelligence systems to optimize, automate, and coordinate supply chain and logistics operations. Agentic AI systems utilize advanced technologies such as machine learning, generative AI, reinforcement learning, large language models (LLMs), computer vision, predictive analytics, and multi-agent orchestration frameworks to independently execute or assist with operational tasks, real-time decision-making, workflow coordination, and process optimization across complex supply chain networks.

The Agentic AI in Supply Chain and Logistics Market Report is Segmented by Component (Software Platforms, AI-Enabled Hardware Systems, and Services), Application (Demand Forecasting and Planning, Warehouse and Fulfillment Optimization, Transportation Routing and Fleet Management, Procurement and Sourcing Automation, Last-Mile Delivery Orchestration, and Other Applications), Industry Vertical (Retail and E-Commerce, Manufacturing, Food and Beverage, Healthcare and Pharmaceuticals, Automotive, and Other Industry Verticals), Deployment Model (Cloud-Based, On-Premise, and Hybrid), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Platforms |

| AI-Enabled Hardware Systems |

| Services (Integration and Consulting) |

| Demand Forecasting and Planning |

| Warehouse and Fulfillment Optimization |

| Transportation Routing and Fleet Management |

| Procurement and Sourcing Automation |

| Last-Mile Delivery Orchestration |

| Other Applications |

| Retail and E-Commerce |

| Manufacturing |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Automotive |

| Other Industry Verticals |

| Cloud-Based |

| On-Premise |

| Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software Platforms | ||

| AI-Enabled Hardware Systems | |||

| Services (Integration and Consulting) | |||

| By Application | Demand Forecasting and Planning | ||

| Warehouse and Fulfillment Optimization | |||

| Transportation Routing and Fleet Management | |||

| Procurement and Sourcing Automation | |||

| Last-Mile Delivery Orchestration | |||

| Other Applications | |||

| By Industry Vertical | Retail and E-Commerce | ||

| Manufacturing | |||

| Food and Beverage | |||

| Healthcare and Pharmaceuticals | |||

| Automotive | |||

| Other Industry Verticals | |||

| By Deployment Model | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current agentic AI in supply chain and logistics market size?

The market was valued at USD 9.86 billion in 2026 and is projected to reach USD 17.84 billion by 2031, according to Mordor Intelligence.

Which component leads spending on agentic AI solutions across supply chains?

Software platforms led with 57.81% of 2025 revenue, reflecting enterprise preference for cloud-native orchestration suites.

How fast will last-mile orchestration grow inside this space?

Last-mile delivery orchestration is expected to expand at a 13.79% CAGR between 2026 and 2031 as urban density and same-day expectations rise.

Why are hybrid architectures gaining favor over pure cloud deployments?

Hybrid setups lower inference latency for warehouse and vehicle agents while satisfying data-sovereignty rules in China, India, and Europe.

Which industry vertical is forecast to grow the fastest?

Healthcare and pharmaceuticals are set to register a 13.67% CAGR through 2031 due to stringent cold-chain and serialization requirements.

What is a key restraint that could slow adoption of agentic AI?

High integration costs with legacy ERP and TMS systems remain a major hurdle, especially for mid-market operators with aging IT estates.

Page last updated on: