Agent-as-a-Service (AaaS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

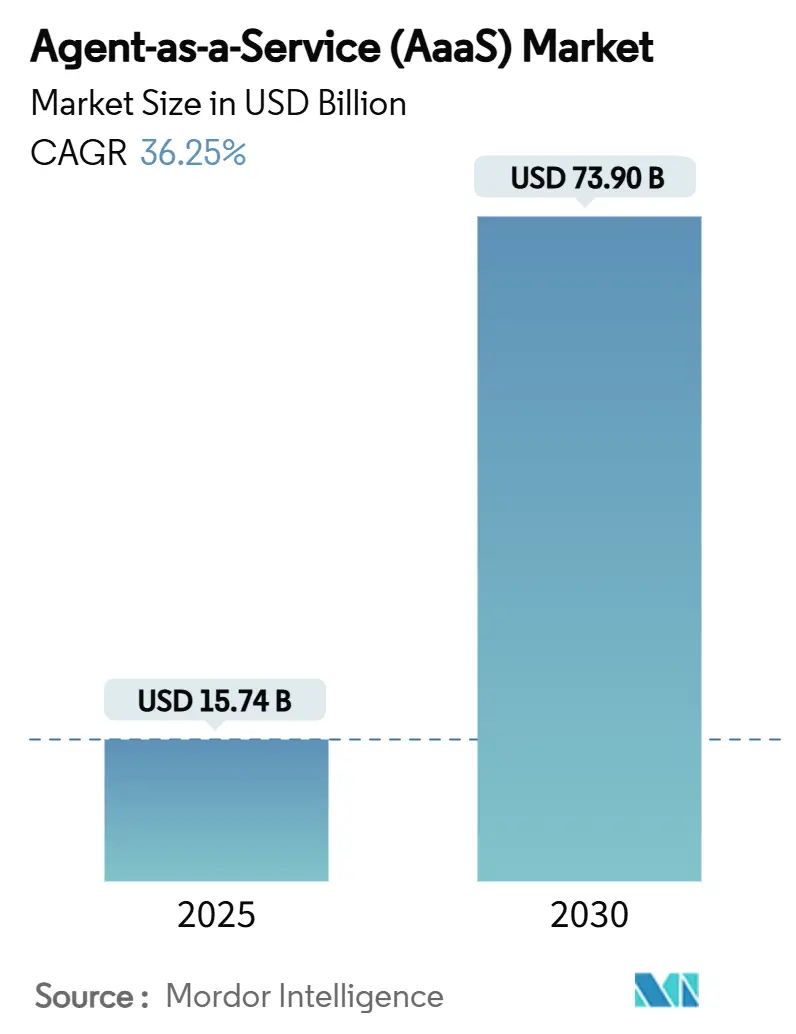

| Market Size (2025) | USD 15.74 Billion |

| Market Size (2030) | USD 73.90 Billion |

| Growth Rate (2025 - 2030) | 36.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agent-as-a-Service (AaaS) Market Analysis by Mordor Intelligence

The Agent-as-a-Service Market size is estimated at USD 15.74 billion in 2025, and is expected to reach USD 73.90 billion by 2030, at a CAGR of 36.25% during the forecast period (2025-2030). Generative AI models are witnessing cost compression, API-first cloud architectures are gaining traction, and enterprise automation budgets are expanding – these are the key drivers fueling the surge in adoption. Autonomous agents have now infiltrated areas like customer engagement, risk management, and IT operations, enabling enterprises to boost productivity and reduce technology costs. Hyperscale cloud providers and dedicated automation vendors are setting platform standards, and capital markets are favoring consolidation efforts that integrate workflow, orchestration, and compliance features. Geographically, North America is capitalizing on supportive policy initiatives, while Asia-Pacific is sprinting ahead, driven by a surge in demand for manufacturing and retail automation.

Key Report Takeaways

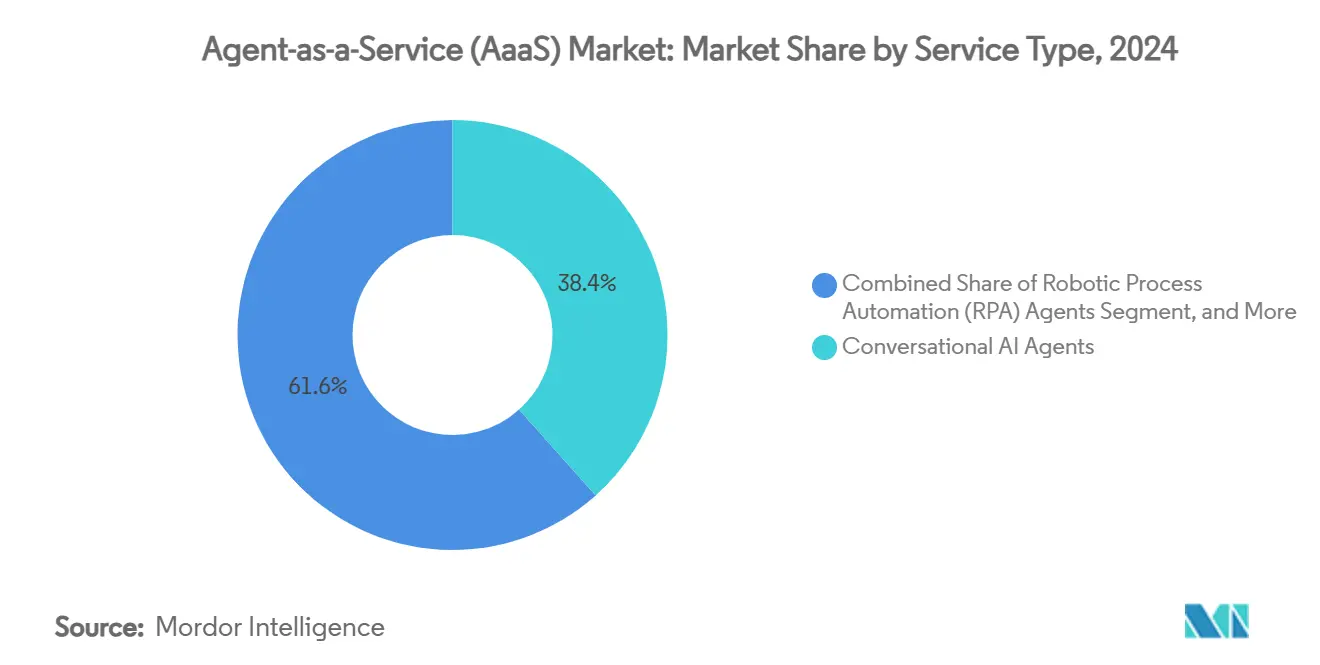

- By service type, Conversational AI held 38.40% of 2024 revenue, while Cyber-Security agents are forecast to grow at 37.50% CAGR to 2030.

- By deployment model, cloud solutions accounted for 68.38% of 2024 spending, whereas hybrid architectures are set to expand at 38.41% CAGR through 2030.

- By organisation size, large enterprises commanded 59.50% share of the Agent-as-a-Service market size in 2024, but SMEs are projected to post 38.40% CAGR between 2025-2030.

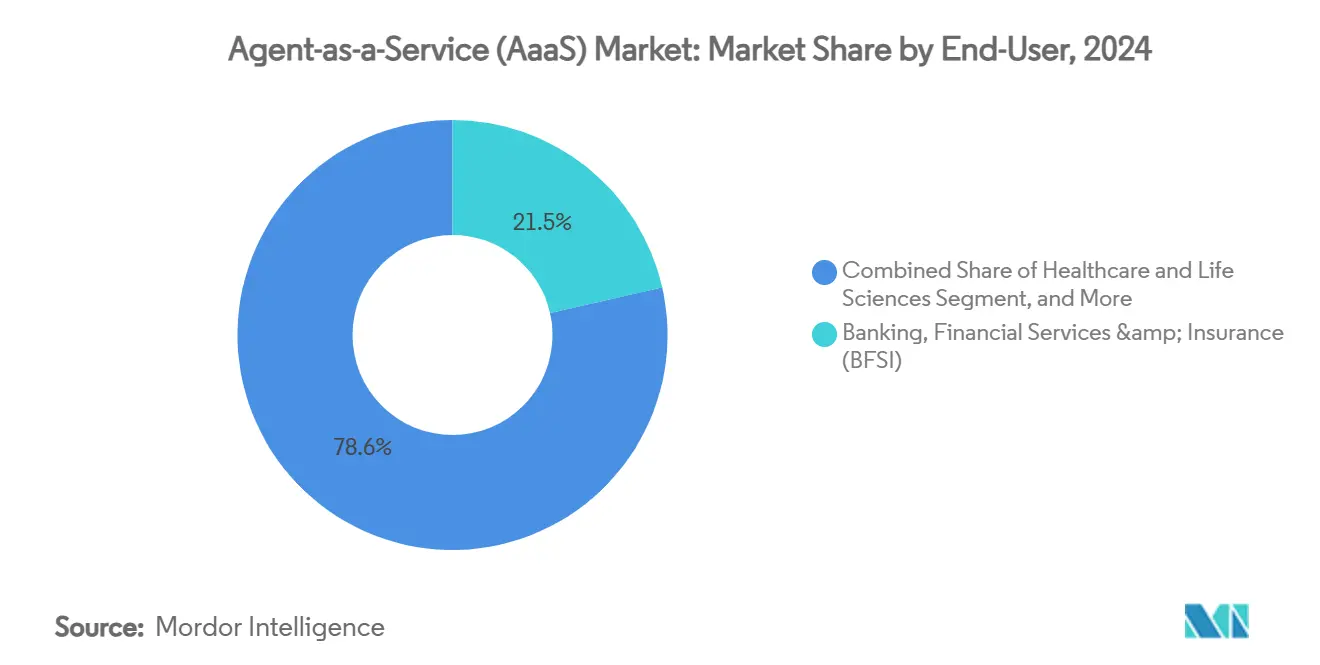

- By end-use industry, the BFSI segment led with 21.45% of 2024 revenue; retail & e-commerce will accelerate at 37.90% CAGR to 2030.

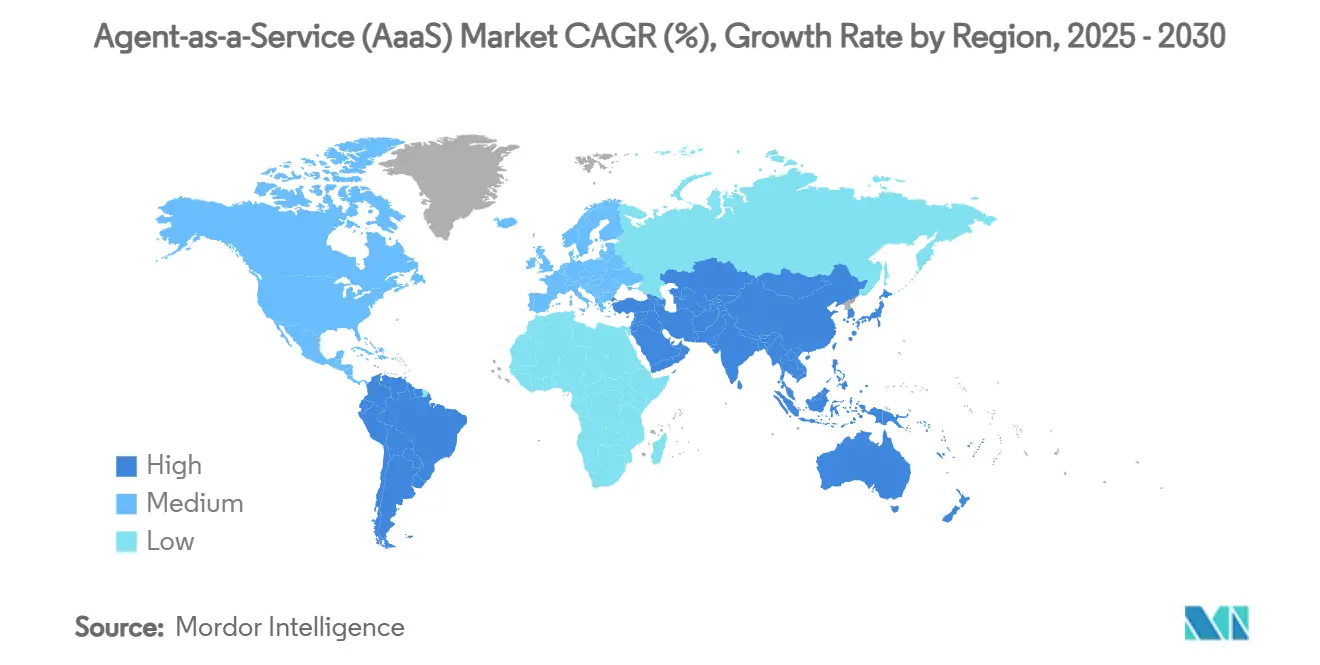

- By geography, North America held 42.78% market share, while Asia-Pacific is poised for 38.70% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agent-as-a-Service (AaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI cost reductions for agent deployment | +8.2% | Global, early uptake in North America & EU | Short term (≤ 2 years) |

| Proliferation of API-first cloud platforms | +6.8% | Core in North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rapid contact-center cloud migration | +5.4% | Global, fastest in APAC | Medium term (2-4 years) |

| Hyper-automation programs in BFSI | +7.1% | Finance hubs in North America & EU, spreading worldwide | Long term (≥ 4 years) |

| Vertical-specific small-language-model agents | +4.9% | APAC manufacturing belts, then global | Long term (≥ 4 years) |

| Algorithmic liability regulations in EU and US | +3.8% | EU & US, global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generative-AI Cost Reductions for Agent Deployment

Investment in optimized AI infrastructure lowered inference costs, allowing mid-market firms to add autonomous agents without on-premises hardware commitments. Microsoft’s USD 80 billion multi-cloud expansion targets training-cost cuts of 40%, enabling enterprises to redirect budgets toward new agent use cases [1]Source: Ferguson, Mackenzie, “Microsoft and OpenAI Pave New Paths in AI with Multi-Cloud Move,” OpenTools, opentools.ai. Corporate pilots report 30-40% savings in customer service and double-digit efficiency gains in warehouse analytics after integrating low-cost conversational and predictive agents. The lower price of model access narrows competitive gaps between large incumbents and resource-constrained challengers, intensifying market penetration of subscription-based agent services. Vendor roadmaps now bundle fine-tuned small-language-models with orchestration consoles, packaging compute savings directly into commercial offerings. This dynamic expands the Agent-as-a-Service market by opening untapped SME cohorts previously priced out of enterprise AI tooling.

Proliferation of API-First Cloud Platforms

Standardised APIs unlock rapid connectivity between agents and legacy applications, collapsing deployment cycles from months to weeks. Salesforce’s AgentExchange already lists more than 200 partner integrations, demonstrating how a unified schema simplifies cross-vendor workflows [2]Source: Salesforce, “Salesforce Launches AgentExchange,” salesforce.com. The resulting data liquidity lets agents pull transactional, CRM, and ERP feeds in real time, fostering multi-agent collaboration on complex tasks. Deloitte’s roll-out of 100 pre-built agents using Agent-to-Agent protocols illustrates growing demand for interoperable frameworks that reduce vendor lock-in [3]Source: UiPath Inc., “UiPath Launches First Enterprise-Grade Platform for Agentic Automation,” uipath.com. As APIs mature, platform providers gain a durable moat through network effects, accelerating uptake across mainstream enterprise segments.

Rapid Contact-Center Cloud Migration

Enterprises shifting contact-center workloads to the cloud gain elastic compute that scales automated agents on demand. JPMorgan Chase reports a multibillion-dollar value pool from AI assistants applied to live support and fraud workflows [4]Source: Son, Hugh, “Goldman Sachs Rolls Out an AI Assistant,” CNBC, cnbc.com. Cloud platforms integrate sentiment analysis and contextual routing, letting agents handle routine inquiries while human staff resolve exceptions. Partnerships such as UiPath and Amelia embed conversational AI in IT service desks, supplying 24/7 support within existing automation pipelines. The virtuous loop of lower call times, higher customer satisfaction, and realtime analytics underpins continued investment in the Agent-as-a-Service market.

Hyper-Automation Programs in BFSI

Financial institutions broaden robotic process initiatives into agentic decision-making for fraud detection, compliance monitoring, and risk scoring. Goldman Sachs deployed an internal AI assistant to 10,000 employees and plans full coverage for knowledge workers in 2025. Regulators welcome auditable agent workflows that provide consistent rule interpretation, encouraging wider uptake of AaaS platforms. Analyses from Citi GPS foresee banking profit pools expanding by USD 170 billion as autonomous agents streamline back-office operations. BFSI demand guarantees premium pricing for secure, compliance-ready agent offerings and subsidises product innovation that later diffuses into other sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy-first legislation limiting data capture | -4.2% | EU GDPR zones, spreading to US states | Medium term (2-4 years) |

| Talent scarcity in prompt & flow engineering | -3.8% | Global, acute in North America & EU | Short term (≤ 2 years) |

| GPU supply-chain volatility | -2.9% | Worldwide, concentrated in APAC production hubs | Short term (≤ 2 years) |

| “Agentic hallucination” risk in regulated sectors | -3.1% | Global, stricter in EU & US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy-First Legislation Limiting Data Capture

The EU AI Act effective August 2024 restricts data categories that agents may process, penalising non-compliance with fines up to EUR 35 million or 7% of global turnover. Enterprises must document data-handling practices at model and workflow level, raising integration overheads for AaaS vendors. US states are enacting parallel rules, creating a complex compliance mosaic that fragments data pipelines. Providers responding with privacy-preserving retrieval, federated learning, and synthetic data generation can protect revenue, yet smaller vendors face rising legal costs that may slow market entry.

Talent Scarcity in Prompt and Flow Engineering

Specialised design of agent prompts and multi-step workflows demands scarce skill sets. Global surveys place total compensation for senior AI engineers at USD 900,000-4.2 million, placing them beyond reach of numerous mid-market firms. European leaders report 75% difficulty filling AI openings, lengthening deployment timelines. Vendors respond with low-code orchestration studios and template libraries, but staffing constraints still temper near-term expansion of the Agent-as-a-Service market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Conversational Agents Dominate as Security Workflows Surge

The segment for conversational agents captured a 38.40% 2024 revenue share, reflecting enterprise familiarity with chat interfaces and direct ROI from automated customer support. Cyber-Security agents, however, are projected for 37.50% CAGR through 2030, propelled by escalating threat volumes and the need for real-time remediation. Within this segment, the Agent-as-a-Service market size for security workflows is forecast to expand quickly as SOC teams combine detection agents with response playbooks that integrate orchestration layers. Decision-intelligence agents gain purchase in risk analytics and supply-chain optimisation, while specialised healthcare and industrial agents extend addressable use cases. Vendors bundling multi-agent suites with a single governance console lower integration friction and amplify cross-sell opportunities.

Although conversational deployments begin as discrete chatbots, enterprises increasingly converge them with process agents to achieve end-to-end task execution. This integration elevates the Agent-as-a-Service market share of multi-agent solutions, creating platform stickiness. Security agents benefit from the same orchestration trend, plugging seamlessly into broader automation fabrics that include identity verification and incident triage. Service portfolios now often package at least one conversational, one workflow, and one security agent, reinforcing the segment’s synergy effect across verticals.

By Deployment: Cloud Retains Scale Advantage While Hybrid Models Accelerate

Cloud implementations represented 68.38% of 2024 spend because managed infrastructure eliminates capital outlays and offers global reach. The Agent-as-a-Service market size for hybrid deployments is forecast to expand at 38.41% CAGR as policy frameworks and cost-control strategies push enterprises to process sensitive data locally while offloading model training to hyperscale GPUs. The emergence of cloud-edge orchestration stacks allows agents to operate near data sources, improving latency and compliance adherence.

Hybrid momentum redistributes the Agent-as-a-Service market share of compute across colocation sites, private clouds, and edge devices, spurring ecosystem demand for deployment-agnostic tooling. Vendors respond by adding on-premises gateways, encrypted parameter streaming, and portable inference runtimes. Longer term, federated deployment will underpin new service models in healthcare, public sector, and industrial IoT where data sovereignty and deterministic response times trump cloud ubiquity.

By End-Use Industry: BFSI Remains Anchor Customer, Retail Gains Pace

BFSI held 21.45% of 2024 revenue, leveraging agents for anti-fraud, underwriting, and customer onboarding. The vertical’s investment capacity and stringent audit obligations drive demand for robust governance and explainability modules, setting a functional benchmark across industries. Retail and e-commerce is positioned for 37.90% CAGR through 2030 as merchants deploy personalisation, inventory, and fulfilment agents to meet real-time consumer expectations. The Agent-as-a-Service market share for healthcare, manufacturing, and government segments also rises steadily on the back of diagnostic aid, predictive maintenance, and citizen-service automation respectively. Cross-industry learnings shorten deployment cycles, with vendors packaging sector-specific ontologies and compliance presets to accelerate time-to-value.

By Organisation Size: Enterprises Lead, SMEs Drive Volume Growth

Large organisations accounted for 59.50% of 2024 revenue because they possess the budgets and in-house talent to orchestrate complex agent ecosystems at scale. However, falling model-as-a-service pricing and low-code design tools position SMEs as the fastest-growing cohort, with 38.40% CAGR forecast through 2030. This democratisation widens the Agent-as-a-Service market size among firms previously restricted to basic automation, unlocking green-field opportunities for subscription providers.

Enterprises continue to set functional blueprints, piloting multi-agent governance protocols later adopted by mid-market adopters. Platform vendors increasingly tier feature sets, offering compliance, role-based access, and audit trails for enterprises while delivering template-based agents for SMEs. The dual-track strategy enlarges the total Agent-as-a-Service market without cannibalising high-margin enterprise offerings.

Geography Analysis

North America retained a commanding 42.78% share in 2024 thanks to policy support and a dense ecosystem of cloud hyperscalers, venture capital, and research universities [5]Source: The White House, “Removing Barriers to American Leadership in Artificial Intelligence,” whitehouse.gov. Federal initiatives like Executive Order 14179 promote open innovation, while capital markets fund consolidation moves exemplified by ServiceNow’s USD 2.85 billion Moveworks acquisition. The resulting flywheel of enterprise demand and vendor capacity reinforces regional leadership, and the Agent-as-a-Service market size in North America benefits from early standard-setting around data governance and interoperability.

Asia-Pacific represents the fastest-growing region, forecast at 38.70% CAGR through 2030. Manufacturing and retail conglomerates in China, South Korea, and Japan embrace agentic automation to counter labour-cost inflation and sustain just-in-time production cycles. Government-backed digitisation programmes in ASEAN economies further widen the client base. Local tech giants such as Tencent and Baidu embed agents throughout marketing and analytics suites, providing reference implementations that accelerate adoption across SMEs. Despite distinct data-localisation rules, the region’s appetite for lightweight, vertical agents positions APAC as a prime terrain for hybrid cloud and edge deployments.

Europe records moderate growth as firms adapt to the EU AI Act’s prescriptive rules. While compliance raises integration costs, it also delivers long-term legal certainty that favours providers with built-in governance capabilities. Public-private research partnerships in Germany and the Nordics foster advances in explainable AI and privacy-enhancing computation. Across South America, Middle East, and Africa, digital-transformation programmes and maturing cloud infrastructure produce a rising tide of pilot projects—particularly in energy, mining, and public-sector service delivery—laying foundations for wider Agent-as-a-Service market adoption post-2027.

Competitive Landscape

The competitive field is moderately fragmented, with leading cloud providers leveraging infrastructure scale to integrate orchestration, monitoring, and billing into turnkey agent platforms. Amazon Web Services, Google Cloud, Microsoft, and IBM channel existing customer bases to upsell agent capabilities tightly coupled with their AI model services. ServiceNow’s USD 2.85 billion purchase of Moveworks demonstrates the race to add domain-rich conversational IP that complements workflow automation.

Specialised vendors such as UiPath, Salesforce, and OpenAI differentiate through vertical templates, low-code studios, and advanced language models. Salesforce’s AgentExchange and Workday’s AI Agent Partner Network illustrate platform bets on third-party ecosystems that drive stickiness and accelerate content diversity. Edge computing specialists stake claims in privacy-sensitive sectors by deploying compact agents on-device, reducing latency and compliance hurdles. Competitive intensity is expected to grow as incumbents bundle agent services with existing SaaS contracts, while newcomers chase niche white-space in regulated verticals and emerging markets.

Strategic moves in 2025 include platform unification, cross-cloud interoperability, and AI control towers that centralise policy enforcement. Vendors with multi-tenant governance layers attract enterprise clients seeking a single pane of glass for model registries, provenance tracking, and performance metrics. As consolidation proceeds, the top five players are estimated to hold roughly 45-50% combined Agent-as-a-Service market share by 2027, indicating ample room for specialist differentiation.

Agent-as-a-Service (AaaS) Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

International Business Machines Corporation

Salesforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: OpenAI valuation rose to USD 300 billion amid agent adoption boom.

- June 2025: Workday launched AI Agent Partner Network to integrate digital agents with workforce platforms.

- May 2025: UiPath released Medical Record Summarization agent with Google Cloud, halving authorisation turnaround time.

- May 2025: ServiceNow unveiled AI Control Tower, unifying model and workflow oversight.

Global Agent-as-a-Service (AaaS) Market Report Scope

| Conversational AI Agents |

| Robotic Process Automation (RPA) Agents |

| Decision-Intelligence Agents |

| Cyber-Security Agents |

| Other Specialized Agents |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| IT and Telecommunications |

| Manufacturing |

| Government and Public Sector |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Conversational AI Agents | ||

| Robotic Process Automation (RPA) Agents | |||

| Decision-Intelligence Agents | |||

| Cyber-Security Agents | |||

| Other Specialized Agents | |||

| By Deployment | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Organisation Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-Use Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| IT and Telecommunications | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Agent-as-a-Service market?

The market reached USD 15.74 billion in 2025 and is forecast to grow rapidly at a 36.25% CAGR.

Which service category leads spending today?

Conversational agents dominate, accounting for 38.40% of 2024 revenue.

Why are hybrid deployments increasing so quickly?

Enterprises mix cloud scalability with on-premises data control, driving a 38.41% CAGR for hybrid models through 2030.

Which industry invests most in Agent-as-a-Service solutions?

Banking, financial services, and insurance held 21.45% of 2024 market revenue, focusing on fraud, compliance, and onboarding workflows.

Which region will post the fastest growth to 2030?

Asia-Pacific is projected for 38.70% CAGR, driven by manufacturing automation and large-scale digital initiatives.

Page last updated on: