Africa Structured Cabling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

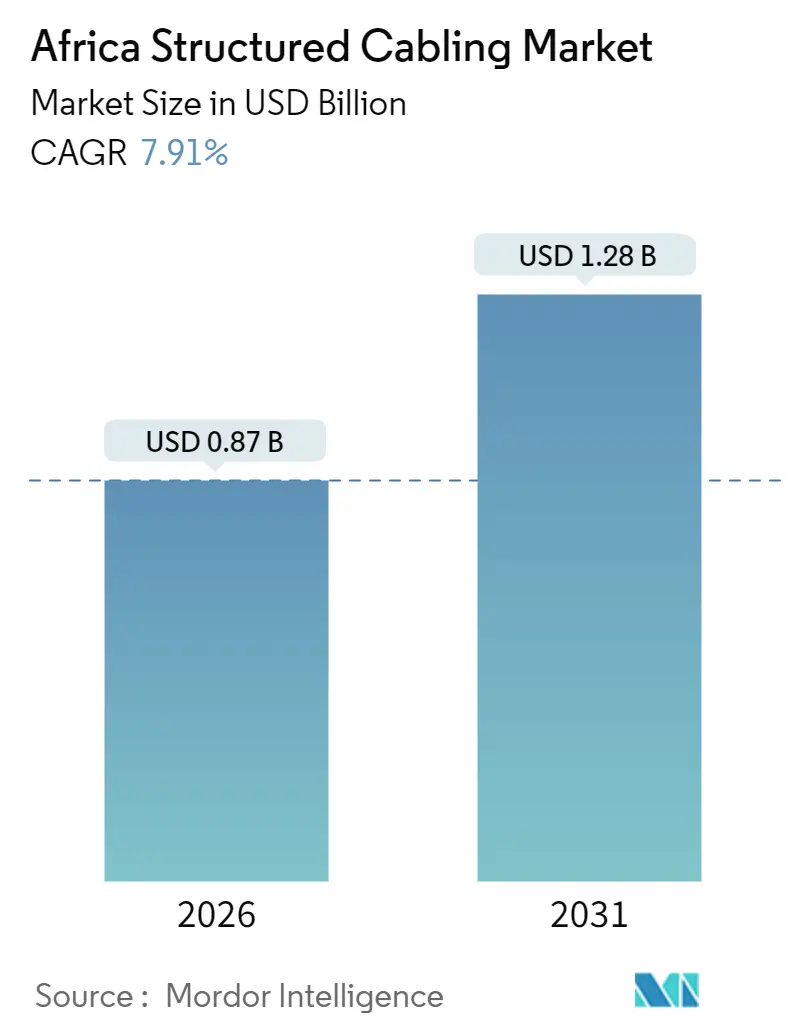

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 7.91% CAGR |

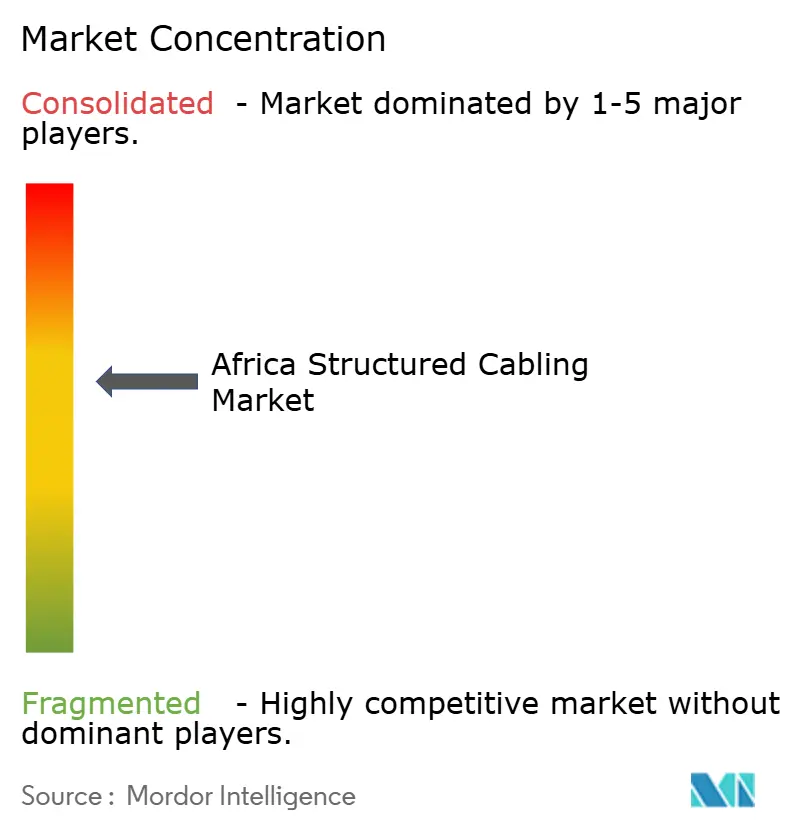

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Structured Cabling Market Analysis by Mordor Intelligence

The Africa structured cabling market size stood at USD 0.87 billion in 2026 and is projected to reach USD 1.28 billion by 2031, advancing at a CAGR of 7.91%. Growth rests on three pillars, namely hyperscale data center construction, metro-fiber densification by telecom operators, and government mandates that favour fixed-line connectivity. Multinational cloud providers, led by Microsoft and Equinix, are installing large African campuses that require thousands of high-density fiber links and Category 6A cross-connects. Currency volatility and import duties temper expansion, but have not derailed projects because prefabricated modular data centers trim on-site labour and speed payback periods. Vendors that combine copper, fiber, power, and cooling under one contract enjoy stickier relationships, while distributors with bonded warehouses mitigate customs delays and win mid-market orders. In short, the Africa structured cabling market benefits from strong secular tailwinds that outweigh near-term macro risks.

Key Report Takeaways

- By type, copper commanded 54.51% of Africa structured cabling market share in 2025. Fiber is expected to expand at an 8.56% CAGR through 2031, the fastest growth rate among all solutions.

- By cable category, Category 6 held 32.78% revenue share in 2025, while Category 6A is advancing at an 8.88% CAGR to 2031.

- By solution, component, hardware accounted for 61.66% of the Africa structured cabling market size in 2025. Services segment is rising at a 9.01% CAGR through 2031.

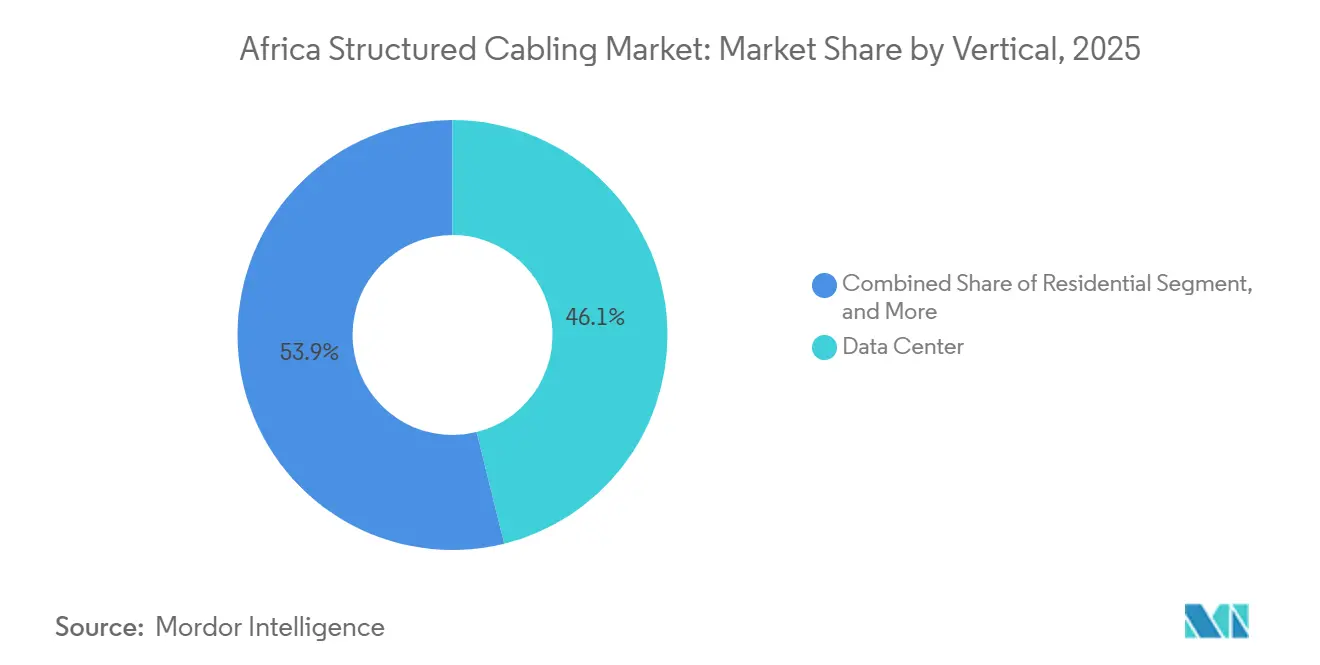

- By vertical, data centers captured 46.13% value in 2025 and are progressing at an 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Africa representing one of the more structurally developed among them. The global report on structured cabling market by Mordor Intelligence reflects how these regional layers combine into a single system.

Africa Structured Cabling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Technological Advancements Across Industries | +1.40% | Pan-African, concentrated in South Africa, Kenya, Nigeria, Egypt | Medium term (2-4 years) |

| Growing Expansion of Data Centers | +2.10% | South Africa, Kenya, Nigeria, Egypt, Morocco | Short term (≤ 2 years) |

| Government Digital Infrastructure Initiatives and Incentives | +1.60% | Kenya, Rwanda, Nigeria, Senegal, Ghana | Medium term (2-4 years) |

| Rapid Urban Fiber Backbone Rollouts by Telcos and ISPs | +1.30% | Nigeria, Kenya, South Africa, Tanzania, Uganda | Short term (≤ 2 years) |

| Adoption of Prefabricated Modular Data Centers Boosting Pre-terminated Cabling Demand | +0.90% | South Africa, Kenya, Nigeria | Short term (≤ 2 years) |

| Multilateral Development Bank Financing of Smart Industrial Parks Stimulating Cabling Procurement | +0.70% | Ethiopia, Côte d'Ivoire, Senegal, Rwanda | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Technological Advancements Across Industries

Enterprises adopting cloud-native architectures are replacing legacy Category 5e links with Category 6A or fiber because 10-gigabit throughput now underpins desktop virtualization, unified communications, and low-latency analytics. Financial institutions in Johannesburg and Lagos completed wholesale recabling in 2025 after latency spikes emerged during peak trading sessions, switching to OM4 multi-mode and single-mode trunks that keep insertion loss below 1.5 dB.[1]Siemon Case Studies, “MainOne West African Data Center Portfolio Deployment,” siemon.com Manufacturers rolling out industrial Ethernet over PROFINET or EtherCAT need sub-millisecond determinism that Category 6A delivers up to 100 meters and that fiber surpasses in electrically noisy plants. These upgrades reinforce sustained demand across the Africa structured cabling market.

Growing Expansion of Data Centers

Hyperscale and colocation builds are ramping faster than the pool of certified fiber splicers. Schneider Electric’s prefabricated modules for iXAfrica, commissioned in July 2024, cut site work by 35% and embedded structured cabling from the factory.[2]Schneider Electric Investor Presentation, “Africa Data Center Segment Growth,” se.com Airtel’s 75,000-kilometer Telesonic backbone and Google’s Umoja subsea cable both require dense cross-connect fields at landing stations, multiplying orders for fiber distribution frames. The pace of builds positions the Africa structured cabling market for multi-year double-digit expansion in data-center-heavy metros.

Government Digital Infrastructure Initiatives and Incentives

Kenya’s Digital Master Plan earmarked KES 15 billion (USD 115 million) for school and clinic fiber links that depend on indoor Category 6 cabling to reach classrooms and wards. Nigeria’s National Broadband Plan targets 70% penetration by end-2025, stimulating metro Ethernet rings that combine outdoor single-mode runs with indoor copper drops. World Bank IDEA financing of USD 2.48 billion between 2024 and 2028 unlocks cabling spend in secondary cities and funds installer certification, a structural boost for the Africa structured cabling industry.

Rapid Urban Fiber Backbone Rollouts by Telcos and ISPs

MTN’s USD 320 million East2West terrestrial route, SEACOM’s USD 563 million metro upgrades, and the 2Africa cable landings are converging on urban meet-me sites that each host hundreds of fiber jumpers and Category 6A patch fields. Because many links terminate inside converted warehouses with limited space, operators favour pre-terminated trunks that snap into high-density panels, reinforcing volume growth for the Africa structured cabling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Technical Skills and Complex Installation Process | -1.20% | Pan-African, acute in Francophone West Africa and East Africa | Medium term (2-4 years) |

| Rising Demand for Wireless Solutions | -0.80% | Urban centers in Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| High Upfront Capital Costs Amid Currency Volatility | -1.00% | Nigeria, Egypt, Ghana, Zambia | Short term (≤ 2 years) |

| Import Duties and Fragmented Regional Standards Increasing Supply-Chain Complexity | -0.70% | West Africa (ECOWAS), East Africa (EAC), Southern Africa (SADC) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Technical Skills and Complex Installation Process

Africa needs roughly 10,000 additional TIA- and ISO-certified technicians by 2031, yet only 500 graduated from Schneider Electric programs in 2024. Fiber terminations in dusty job sites frequently fail return-loss tests, prompting costly rework. Category 6A bundles demand alien-crosstalk mitigation through precise separation and grounding, which many general electricians cannot deliver. These gaps elongate project timelines and curb near-term throughput in the Africa structured cabling market.

High Upfront Capital Costs Amid Currency Volatility

The naira’s drop from 460 to 750 per USD between 2023 and 2024 lifted local-currency cable costs by nearly 65%, pushing small enterprises toward incremental Wi-Fi overlays rather than full rewires. Similar swings in the Egyptian pound constrain public budgets. Larger distributors hedge with forward contracts but pass premiums to customers, trimming some opportunity for the Africa structured cabling industry until exchange rates stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fiber Gains on Bandwidth Imperatives

Fiber and copper remain twin pillars of the Africa structured cabling market. Copper held 54.51% value in 2025 on the strength of retrofit LAN projects that reuse existing conduits, yet fiber is expanding at an 8.56% CAGR because hyperscale data centers require OM4 and OS2 links for 40, 100, and 400 gigabit fabrics. Combined, these dynamics place fiber at the forefront of future growth within the Africa structured cabling market.

Fiber’s climb rests on single-mode backbones that carry multiple 100-gigabit wavelengths without in-line amplification and multi-mode ribbons that slash switch port power. Corning’s manufacturing presence in Egypt shortens lead times, while Siemon’s VSFF connectors prepare African facilities for 800-gigabit rollouts, anchoring the long-term trajectory of the Africa structured cabling industry.

By Cable Category: Category 6A Bridges Legacy and Next-Gen

Category 6 accounted for 32.78% revenue in 2025, but Category 6A is racing ahead at an 8.88% CAGR, propelled by 10-gigabit server adoption and unified cabling mandates in new builds. In data centers, Vertiv’s OneCore modules ship with shielded Category 6A alongside fiber trunks, demonstrating design convergence that elevates Africa structured cabling market size for higher-grade copper.

Category 5e persists in low-budget residential installs, whereas Category 7 and Category 8 remain niche for EMI-heavy factories. Harmonized TIA-568.2-D enforcement in Kenya and South Africa accelerates the phasing out of sub-gigabit cabling, steering incremental investment toward Category 6A across the Africa structured cabling market.

By Solution Component: Services Surge on Skills Scarcity

Hardware drove 61.66% of 2025 value, yet services are climbing faster at 9.01% annually because certified labour is scarce. Buyers increasingly award turnkey contracts that cover design, pull, terminations, and warranty, inflating the services slice of Africa structured cabling market size.

Software remains small but gains traction as operators seek real-time port visibility. Schneider Electric packages DCIM dashboards with installation bundles, enhancing stickiness and widening its footprint in the Africa structured cabling industry.

By Vertical: Data Centers Dominate Demand and Growth

Data centers led with 46.13% share in 2025 and will continue to post the fastest 8.95% CAGR, ensuring the vertical remains the anchor of the Africa structured cabling market. Regulatory data-sovereignty rules plus Microsoft’s USD 1 billion Kenyan campus underscore hyperscalers’ commitment to African zones.

Enterprise LANs trail as the second-largest vertical, stimulated by office expansions and cloud migration. Commercial buildings adopt cabling for IP surveillance and BMS, while industrial automation favours shielded Category 6A or fiber to withstand EMI, jointly supporting healthy diversification across the Africa structured cabling market.

By Installation Environment: Indoor Dominates, Outdoor Gains on Fiber Rollouts

Indoor projects (data halls, risers, and residential units) remain the volume engine because they use plenum or riser-rated cable that meets strict flame and smoke codes. Outdoor installs, however, are accelerating as telcos deploy aerial or shallow-buried fiber backbones that feed 5G small cells and FTTH. MTN’s East2West route and Corning’s Ugandan aerial pilot highlight the expanding outdoor segment inside the Africa structured cabling industry.

Hybrid assemblies that transition from outdoor jackets to indoor tails in a continuous run simplify prefabricated modular data center hookups, knitting both environments into coherent growth for the Africa structured cabling market.

Geography Analysis

South Africa, Nigeria, Kenya, and Egypt together generated roughly two-thirds of 2025 demand, anchored by mature data center clusters and deeper installer talent pools. Equinix’s Johannesburg JN1 hub anchors South African deployments, while Microsoft’s geothermal campus cements Kenya as East Africa’s digital core. Nigeria wrestles with currency swings yet still fields large orders from Airtel’s Nxtra facility and metro Ethernet projects tied to the National Broadband Plan.

Egypt’s smart-city builds in New Cairo and the New Administrative Capital push single-mode fiber and Category 6A into governmental estates. Morocco and Ghana emerge next, fuelled by 2Africa landings and French-language enterprise relocations. Smaller economies, including Tanzania, Rwanda, and Côte d’Ivoire, benefit from World Bank IDEA grants that pay for standards harmonization and skills programs, gradually enlarging the addressable base of the Africa structured cabling market.

Regional blocs such as ECOWAS, EAC, and SADC aim to streamline customs and testing, but enforcement varies widely. Carrier-neutral landing stations for 2Africa and Umoja cables sprinkle demand across multiple coastlines, ensuring wider geographic dispersion of the Africa structured cabling industry.[3]2Africa Consortium Announcements, “2Africa Subsea Cable Operational Status,” 2africacable.com

Competitive Landscape

Global incumbents Corning, Nexans, Belden, Panduit, CommScope, Legrand, and Schneider Electric hold 50-55% of tier-one data center and telco projects, reflecting moderate concentration in the Africa structured cabling market. They leverage end-to-end portfolios and factory warranties that de-risk hyperscale builds. Schneider Electric grew double digits in 2024, with prefab modules bundling cabling, power, and cooling to lock in clients.

Regional distributors like Africa Digital Distributors and Liranz thrive on localized stock and credit terms, winning mid-market deals where availability trumps brand prestige. Scarcity of certified labour reshapes competition because vendors running training academies gain project preference, a trend evident in Schneider Electric’s 2024 upskilling program.

Innovation centers on high-density fiber connectors such as Siemon’s SN VSFF, introduced in January 2025 for 800-gigabit links, and Vertiv’s OneCore prefab racks that integrate Category 6A and fiber trunks in a single module. These differentiators sustain pricing power and uphold moderate competitive intensity across the Africa structured cabling market.

Africa Structured Cabling Industry Leaders

Africa Digital Distributors Limited

Corning Incorporated

Legrand Group

Schneider Electric SE

The Siemon Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vertiv unveiled OneCore integrated infrastructure that ships with Category 6A and fiber trunks, cutting design errors in African facilities.

- January 2025: The Siemon Company launched SN cord VSFF connectors for 800-gigabit and 1.6-terabit Ethernet, aligning with next-generation African data centers.

- October 2024: Equinix opened the JN1 data center in Johannesburg, a USD 160 million build featuring high-density fiber frames.

- July 2024: Schneider Electric installed NBOX1 hyperscale modules for iXAfrica in Kenya, bundling prefabricated cabling to trim site work by 35%.

Africa Structured Cabling Market Report Scope

The African structured cabling market study tracks the revenue gathered through the sale of cables (copper and fiber) and connectivity solutions (patch cords, jumpers, transceivers, fiber connectors, adaptors, panels, etc.) in the African region.

The Africa Structured Cabling Market Report is Segmented by Type (Copper Cable, Copper Connectivity, Fiber Cable Single-mode, Fiber Cable Multi-mode, Fiber Connectivity), Cable Category (Category 5e, 6, 6A, 7, 8, Single-mode Fiber, Multi-mode Fiber), Solution Component (Hardware, Software, Services), Vertical (Data Center, Enterprise LAN, Commercial Buildings, Industrial Automation, Telecom Operators, Residential, Government and Public Sector), Installation Environment (Indoor, Outdoor), and Geography. Market Forecasts are Provided in Terms of Value (USD).

| Copper | Copper Cable |

| Copper Connectivity | |

| Fiber | Fiber Cable, Single-mode |

| Fiber Cable, Multi-mode | |

| Fiber Connectivity |

| Category 5e |

| Category 6 |

| Category 6A |

| Category 7 |

| Category 8 |

| Single-mode Fiber |

| Multi-mode Fiber |

| Hardware |

| Software |

| Services |

| Data Center |

| Enterprise LAN |

| Commercial Buildings |

| Industrial Automation |

| Telecom Operators |

| Residential |

| Government and Public Sector |

| Indoor |

| Outdoor |

| By Type | Copper | Copper Cable |

| Copper Connectivity | ||

| Fiber | Fiber Cable, Single-mode | |

| Fiber Cable, Multi-mode | ||

| Fiber Connectivity | ||

| By Cable Category | Category 5e | |

| Category 6 | ||

| Category 6A | ||

| Category 7 | ||

| Category 8 | ||

| Single-mode Fiber | ||

| Multi-mode Fiber | ||

| By Solution Component | Hardware | |

| Software | ||

| Services | ||

| By Vertical | Data Center | |

| Enterprise LAN | ||

| Commercial Buildings | ||

| Industrial Automation | ||

| Telecom Operators | ||

| Residential | ||

| Government and Public Sector | ||

| By Installation Environment | Indoor | |

| Outdoor | ||

Key Questions Answered in the Report

How fast is structured cabling demand growing across Africa?

The Africa structured cabling market is advancing at a 7.91% CAGR through 2031, supported by hyperscale data centers and government fiber programs.

Which segment contributes the most revenue today?

Data centers led with 46.13% value in 2025 and remain the single largest contributor to spending.

Why is Category 6A adoption accelerating?

Category 6A supports 10-gigabit Ethernet over 100 meters with alien-crosstalk mitigation, aligning with server upgrades in new African data centers.

How does currency volatility affect cabling projects?

Depreciating local currencies inflate landed hardware costs, forcing smaller enterprises to delay full rewires or favor wireless overlays.

Which countries dominate current spending?

South Africa, Nigeria, Kenya, and Egypt together accounted for roughly two-thirds of 2025 demand.

Page last updated on: