Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

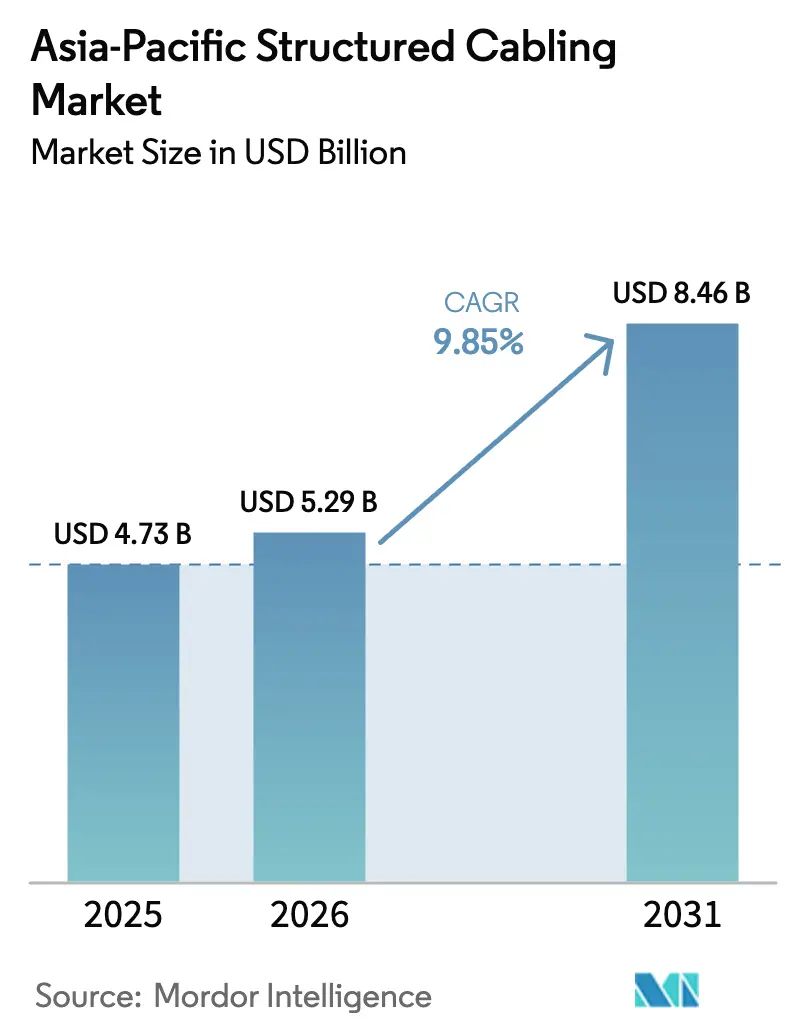

| Base Year Market Size (2025) | USD 4.73 Billion |

| Market Size (2026) | USD 5.29 Billion |

| Market Size (2031) | USD 8.46 Billion |

| Growth Rate (2026 - 2031) | 9.85% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Structured Cabling Market Analysis by Mordor Intelligence

The Asia-Pacific Structured Cabling Market size is expected to grow from USD 4.73 billion in 2025 to USD 5.29 billion in 2026 and is forecast to reach USD 8.46 billion by 2031 at 9.85% CAGR over 2026-2031. This growth reflects surging hyperscale construction, sovereign AI compute clusters, and large-scale fiber-to-the-home rollouts that together amplify demand for high-density copper and optical connectivity. Hardware still drives the bulk of revenue, yet services are expanding faster as enterprises retrofit legacy local-area networks to support multi-gigabit PoE switches and Wi-Fi 6E access points. Fiber optic solutions dominate new builds because single-mode trunks and 400G-plus optics reduce latency inside AI clusters, while Cat 6 copper is winning horizontal runs where 10GBASE-T headroom is vital. Competitive pressure remains intense as global manufacturers battle regional specialists that promise shorter lead times and local-content compliance, although raw-material volatility and stricter standards compliance add cost friction across the value chain.

Key Report Takeaways

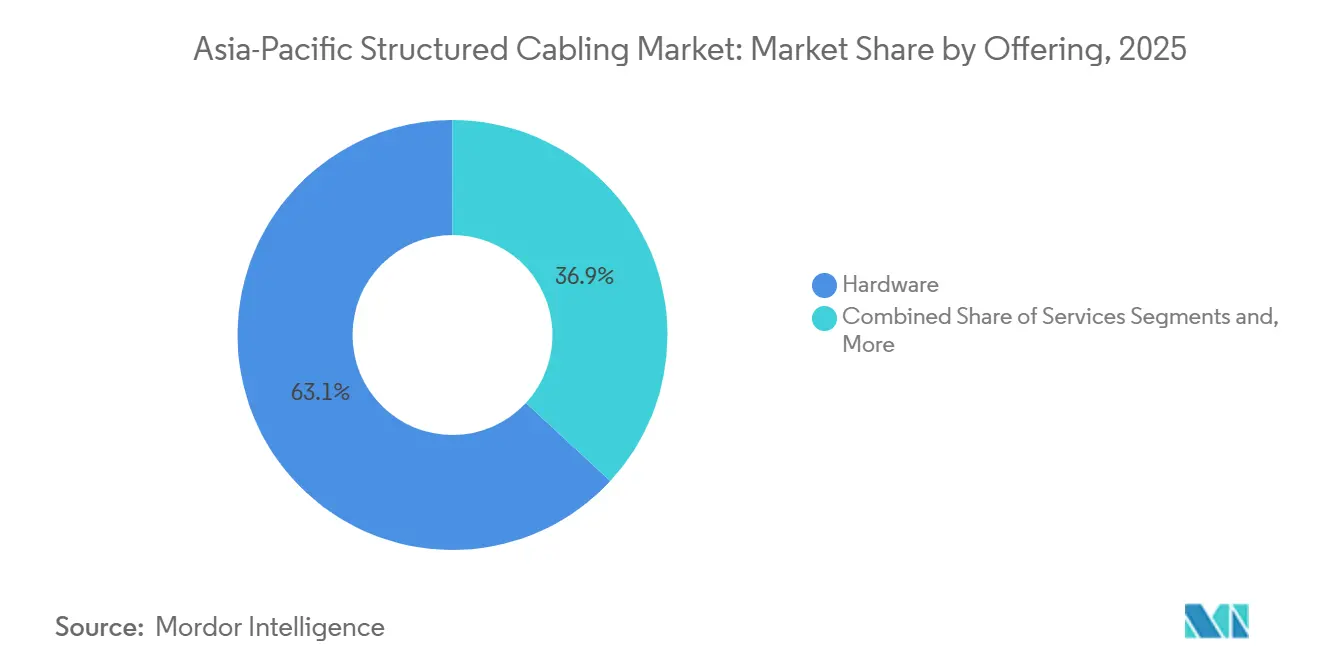

- By offering, hardware led with 63.12% revenue share in 2025 while services are advancing at a 10.22% CAGR through 2031.

- By cable type, fiber optic solutions captured 56.41% of 2025 revenue and are forecast to expand at a 10.97% CAGR to 2031.

- By cable category standard, Cat 5e retained 51.8% share in 2025 whereas Cat 6 is progressing at a 10.56% CAGR through 2031.

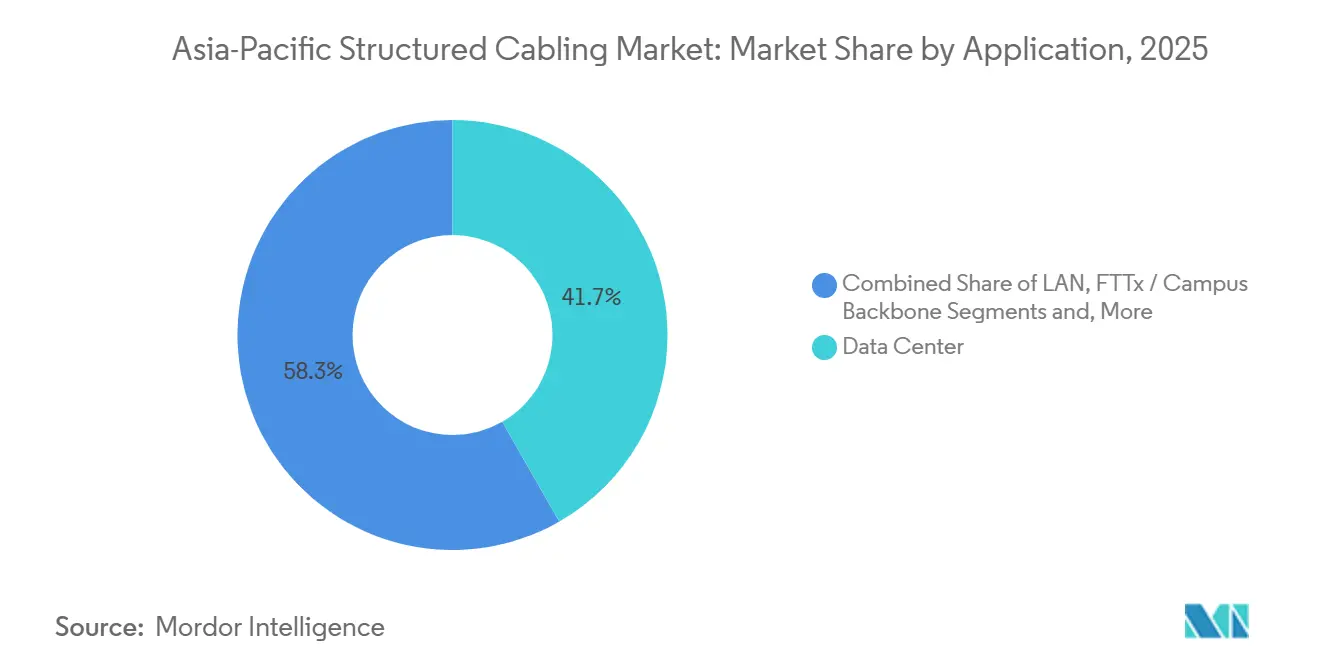

- By application, data centers held 41.73% of 2025 revenue; FTTx and campus backbones are growing at a 10.32% CAGR to 2031.

- By end-user industry, cloud and colocation operators commanded 35.21% spending in 2025 and post the fastest 11.22% CAGR through 2031.

- By geography, China accounted for 29.67% of 2025 value while India is set to outpace all markets with a 10.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Structured Cabling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating hyperscale and edge data-center build-outs | +2.8% | China, India, Singapore, Australia, Japan, South Korea | Medium term (2-4 years) |

| Surge in PoE and remote powering requirements | +1.6% | India, ASEAN, Australia, China | Short term (≤ 2 years) |

| Increasing retrofits for smart buildings and campuses | +1.4% | China, Japan, South Korea, Singapore, Australia | Medium term (2-4 years) |

| Government fiber-to-the-home initiatives | +2.2% | India, Indonesia, Thailand, Vietnam, Philippines | Long term (≥ 4 years) |

| Low-latency demand for AI and ML cluster interconnects | +1.9% | China, India, Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Convergence of OT and IT cabling in Industry 4.0 factories | +1.5% | China, Japan, South Korea, India, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Hyperscale And Edge Data-Center Build-Outs

Investments from hyperscale providers exceed USD 50 billion across Southeast Asia, India, and Australia, with AWS, Google, Microsoft, Alibaba Cloud, and Oracle each commissioning multigigawatt campuses that rely on 144- or 288-fiber MPO trunks and Cat 6 top-of-rack links. Rising construction in secondary cities such as Hyderabad, Chengdu, and Ho Chi Minh City shortens latency for streaming and gaming applications and enlarges the addressable footprint for vendors. Edge facilities under 5 MW use pre-terminated solutions to cut installation time by up to 40%, leading integrators to favor factory-assembled cassettes over field terminations. Because labor costs in Singapore and Sydney rose 3.8% in 2025, contractors actively seek designs that trim onsite hours without sacrificing performance.[1]Cushman and Wakefield, “Asia Pacific Data Center Construction Cost Report,” cushmanwakefield.com Component suppliers that bundle cabling, racks, and cable management gain share by mitigating project risk for hyperscale tenants that demand reliable completion schedules.

Government Fiber-To-The-Home Initiatives

India’s BharatNet installed 692,676 km of optical fiber and connected 214,323 gram panchayats by December 2025 under a INR 220 billion (USD 2.6 billion) allocation. Thailand, Indonesia, and Vietnam follow similar blueprints that pair universal service funds with domestic-content rules, steering contracts toward local manufacturers that meet delivery windows in cyclone-prone regions. These mandates elevate single-mode fiber demand, spur fusion splicer sales, and push rural operators to adopt hardened closures that withstand monsoon flooding. Because sovereign broadband plans stretch to 2030 and beyond, structured cabling vendors lock in decade-long revenue visibility and hedge against cyclical data-center spending. The initiatives also foster public-private partnerships that bundle dark-fiber leases with smart-city use cases, accelerating campus backbone upgrades in provincial towns.

Surge In PoE And Remote Powering Requirements

Ratification of IEEE 802.3bt enables 90-watt PoE, catalyzing adoption of LED lighting, Wi-Fi 6E access points, and PTZ cameras that each draw 25-30 watts.[2]IEEE Standards Association, “IEEE 802.3bt Power over Ethernet Standard,” ieee.org Enterprises in Singapore, Tokyo, and Bengaluru are ripping out Cat 5e and installing Cat 6 to cap voltage drop across 100 m horizontal runs, thereby consolidating power and data over a single cable. Smart-building retrofits now bundle PoE lighting with environmental sensors to realize 40% energy savings, pushing integrators to preconfigure switch stacks for converged management planes. IDC surveys show 80% of Asia-Pacific IT leaders see 6 GHz Wi-Fi as transformational for wired infrastructure, nudging refresh cycles forward by two years. These upgrades, while modest in material volume, create lucrative service engagements because contractors must validate thermals, grounding, and load balancing across newly electrified cable bundles.

Low-Latency Demand For AI And ML Cluster Interconnects

NVIDIA’s GB200 NVL72 rack draws 132 kW and depends on 400G InfiniBand or Ethernet to complete training jobs within acceptable SLAs.[3]NVIDIA Corporation, “GB200 NVL72 AI Infrastructure Specifications,” nvidia.com SoftBank, Oracle, and KT Corporation collectively earmarked more than USD 18 billion for AI facilities that will enter service between 2026 and 2028, each requiring hundreds of 288-fiber MPO cassettes per hall. Pre-terminated single-mode trunks slash installation errors and enable spine-leaf topologies that achieve sub-microsecond latency, a must for LLM training. Liquid-cooled racks force designers to reroute cable trays above coolant loops, and vendors that offer integrated pathways gain a premium. Because AI nodes cluster in seismic zones such as Japan and Taiwan, consultants now specify seismic-rated ladder racks and flexible fiber raceways to comply with local building codes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of enterprise WLAN and 5G FWA solutions | -1.2% | India, ASEAN, Australia, China | Short term (≤ 2 years) |

| Complex standards compliance and testing costs | -0.9% | Asia-Pacific (all markets) | Medium term (2-4 years) |

| Supply-chain volatility in copper and optical fiber | -1.1% | China, India, ASEAN, Australia | Short term (≤ 2 years) |

| Deferral of on-premises data-center builds amid cloud migration | -1.0% | Asia-Pacific developed and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of Enterprise WLAN And 5G FWA Solutions

Wi-Fi Alliance has certified more than 2,500 Wi-Fi 6E devices, and field trials show average throughputs above 1.7 Gbps, prompting many office planners to adopt a wireless-first strategy that trims the need for new horizontal cable drops. Telcos in India, Indonesia, and the Philippines now market 100-300 Mbps 5G fixed wireless packages, with Reliance Jio alone activating 115,000 FWA terminals during 2025, thereby bypassing last-mile copper or fiber in cost-sensitive locations. Cisco benchmarks indicate that Wi-Fi 6E access points draw roughly 28 watts, requiring 90-watt PoE switch ports but still fewer cable runs per floor, which compresses demand for Cat 6 in small and midsize offices. Systems integrators report that renovation projects now devote only 25% of cabling budgets to copper endpoints compared with 45% in 2022, redirecting spend toward aggregation links and network services. While data-center and hyperscale environments remain insulated because high-density racks depend on fiber trunks, reduced office installations constitute a meaningful headwind for structured-cabling vendors in Australia, Thailand, and urban India.

Supply-Chain Volatility In Copper And Optical Fiber

Copper spot prices on the London Metal Exchange peaked near USD 10,719 per tonne in October 2025, while a projected 900,000-tonne shortfall in 2026 has prompted buyers to secure long-term contracts or shift to aluminum-clad copper for non-critical runs. Fiber manufacturers face less raw-material risk, yet draw-tower capacity constraints surfaced during 2024 when hyperscalers synchronized expansion schedules. Vendors with vertically integrated smelters or in-house draw towers weather these shocks better, but installers still grapple with 8-12-week lead times on niche SKUs, stretching project timelines and pressuring margins. Contractors pass cost increases through to clients, yet hyperscale tenants cap allowable price escalation, intensifying competition and eroding profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Hardware On Retrofit Complexity

The Asia-Pacific structured cabling market size for hardware reached USD 3.34 billion in 2025, equal to 63.12% of total spend, thanks to copper pairs, fiber trunks, modular panels, and cable management systems that dominate greenfield budgets. Design and installation services, however, are growing at a 10.22% CAGR because enterprises must upgrade legacy cabling to support 90-watt PoE, 10GBASE-T throughput, and Wi-Fi 6E backhaul. This service boom benefits contractors certified under BICSI Installer 2, whose credentials shorten procurement cycles for hyperscale tenants. Vendors bundle as-built documentation and thermal simulation into maintenance contracts that now stretch seven years, reflecting higher rack densities and the scarcity of skilled technicians in Indonesia and India.

Software remains a sliver of revenue but is ascending as hyperscalers automate cable inventories to lower mean-time-to-repair by up to 40%. Platforms that ingest test results directly from Fluke or Viavi certifiers produce ISO-compliant handover packs in minutes, trimming administrative labor. Hybrid build-operate agreements are emerging, where integrators assume responsibility for uptime over a five-year horizon, thus embedding recurring revenue during the post-installation phase. The Asia-Pacific structured cabling market creates room for value-added resellers that overlay digital twin capabilities onto cabling blueprints, enabling predictive maintenance on PoE switch ports and fiber-channel utilization.

By Cable Type: Fiber Dominates On AI And Backbone Demand

Fiber captured 56.41% of 2025 value and is expanding at a 10.97% CAGR because spine-leaf architectures inside AI clusters demand 400G-plus optics and single-mode trunks that sustain link budgets beyond 300 meters. OM4 and OM5 multimode still serve short-reach links inside server rows, yet hyperscalers increasingly leapfrog to single-mode to standardize spares. Copper retains relevance in horizontal runs and industrial plants where Cat 6 shielded cable tolerates electromagnetic interference. Rising copper prices and mining concentration in Chile, Peru, and the Democratic Republic of the Congo amplify price swings, making aluminum-clad copper attractive for budget-constrained LANs.

Connector technology evolves in tandem: LC duplex still dominates data-center patching, but 16-fiber MPO and emerging SN interfaces shrink port counts on 800G switches, driving density gains. Pre-terminated assemblies reduce installer labor by 25-35%, a key selling point amid chronic talent shortages in Southeast Asia. Because fiber boasts lower raw-material volatility than copper, telcos with long planning horizons prefer single-mode to hedge cost risk, reinforcing the Asia-Pacific structured cabling market share advantage for optical connectivity.

By Cable Category Standard: Cat 6 Persists in Legacy Builds While Cat 5e Retains Lead

Cat 5e lingers mainly in cost-sensitive retrofits, accounting for 51.8% of 2025 revenue. Low-rise residential buildings and temporary facilities such as construction site offices. Contractors continue to stock Cat 5e because its smaller diameter simplifies pulls through congested conduits, and its material cost can be 18-22% lower per meter than Cat 6. However, rising demand for 30-watt PoE endpoints exposes Cat 5e’s higher DC resistance, prompting facility managers to schedule gradual upgrades when budgets allow. Some provincial administrations in Indonesia and Vietnam still approve Cat 5e for subsidized broadband hubs, creating isolated pockets of volume that keep the category alive. Even in these scenarios, tender documents increasingly bundle fiber backbones, signaling that Cat 5e’s role will narrow to short horizontal drops as the Asia-Pacific structured cabling market size shifts decisively toward higher-grade copper.

Cat 6 is underscoring its position as the mainstream choice for new horizontal runs across offices, campuses, and small data rooms.[4]Telecommunications Industry Association, “ANSI/TIA-568.0-E Standard Update,” tiaonline.org Enterprises value its proven support for 1 Gbps throughput over 100 m channels, lower insertion loss than Cat 5e, and straightforward termination that keeps labor costs predictable. Regional building codes in Singapore, Hong Kong, and Sydney now specify Cat 6 or higher for new construction, effectively locking the category into most greenfield projects. As Wi-Fi 6 access points saturate floors, owners deploy Cat 6 to maintain Gigabit uplinks without overpaying for higher-category jackets, helping the Asia-Pacific structured cabling market share for Cat 6 stay dominant through 2028. Integrators also favor Cat 6 for industrial control rooms where shielded variants mitigate electromagnetic interference, extending adoption beyond commercial real estate.

By Application: FTTx And Campus Backbone Surge On Government Mandates

Data centers generated 41.73% of 2025 revenue, reflecting the fiber-heavy architectures required for AI accelerators, but FTTx and campus backbones are climbing at a 10.32% CAGR under national broadband missions. BharatNet alone aims to connect 270,000 villages by 2030, guaranteeing multi-year demand for single-mode fiber, hardened splice closures, and pole hardware. Smart-city pilots in China’s tier-3 municipalities deploy fiber rings that link traffic cameras, environmental monitors, and 5G macro sites, further expanding addressable volumes.

LAN spend remains roughly flat as wireless substitution tempers new outlet counts; however, each Wi-Fi 6E access point uplink now requires 10GBASE-T and 90-watt PoE, doubling per-port cabling cost relative to Cat 5e installations pre-2020. Industrial automation networks in China, Japan, and South Korea specify shielded Cat 6 or fiber with ruggedized jackets to combat oil, vibration, and electromagnetic noise, commanding 10-15% price premiums. As factories chase Industry 4.0 digitization, the Asia-Pacific structured cabling market gains a stable secondary demand stream that is less correlated with hyperscale capital cycles.

By End-User Industry: Enterprise Offices Split Between Cat 5e Cost Control and Cat 6 Performance

Cloud and colocation operators spend predominantly on fiber inside white space but still specify Cat 6 for administrative floors and BMS consoles because it balances Gigabit headroom with manageable bend radius. Financial institutions retrofit branches to Cat 6 as they roll out high-resolution conferencing booths and digital-signage walls that exceed Cat 5e’s 100 MHz envelope. Retail chains remain loyal to Cat 5e at new storefronts across Indonesia and the Philippines, finding it adequate for inventory scanners and payment terminals while freeing budget for Wi-Fi mesh systems.

Healthcare campuses in Japan and Australia standardize on Cat 6 for nurse-call stations and real-time location-tracking tags, citing lower latency and straightforward migration paths to 2.5 Gbps. Manufacturers show a similar split; automotive plants in China select shielded Cat 6 to mitigate welding-arc interference, whereas textile mills in Vietnam employ Cat 5e for non-critical monitoring lines. Education networks reveal the starkest duality: urban universities migrate to all-fiber backbones with Cat 6 classrooms to support VR labs, while rural schools funded by provincial grants still pull Cat 5e to keep per-seat costs down. As a result, demand skews toward Cat 6 in high-density, high-power use cases, yet Cat 5e persists wherever cost and ease of installation outrank performance headroom.

Geography Analysis

China held 29.67% of the Asia-Pacific structured cabling market in 2025, anchored by Alibaba Cloud’s USD 52.4 billion multiyear infrastructure plan and continuous fiber build-outs in tier-3 cities. Domestic cable makers benefit from proximity to the world’s largest refined copper supply and frequently undercut imported products, although export controls on critical minerals encourage hyperscalers to dual-source components. Made in China 2025 accelerates industrial automation spending, driving ruggedized cabling demand inside automotive and electronics plants across Guangdong, Jiangsu, and Zhejiang provinces.

India is poised for the fastest 10.74% CAGR through 2031, fueled by BharatNet’s village-level fiber, USD 6 billion from Google Cloud, USD 30 billion from Reliance, and USD 1 billion from TCS HyperVault. Scarcity of powered sites in Mumbai and Hyderabad lifts land conversion costs and favors brownfield conversions that require complex retrofit cabling. Metro fiber rings upgrade to 200G coherent optics for 5G backhaul, while BFSI and government offices standardize on Cat 6 to power IoT-enabled service counters and electronic-identification kiosks.

Japan, South Korea, and Australia form a mature triad where AI-specific facilities dominate incremental growth. SoftBank’s USD 9 billion AI center in Mihara, Oracle’s USD 8 billion Tokyo program, and KT Corporation’s USD 1.02 billion Gimcheon site drive demand for 400G optics and seismic-rated cable management. Singapore, Indonesia, Thailand, Malaysia, and Vietnam continue to attract hyperscale capital, yet land scarcity in Singapore caps capacity and shifts investments toward Batam, Johor, and Bangkok suburbs. Australia’s National Broadband Network upgrade to fiber for 10 million premises by end-2025 couples with hybrid work adoption, sustaining enterprise LAN refreshes to Cat 6 and fiber spines. Collectively, these dynamics preserve a diverse opportunity landscape across developed and emerging economies, reinforcing the strategic importance of supply-chain localization for participants in the Asia-Pacific structured cabling market.

Competitive Landscape

The Asia-Pacific structured cabling market remains moderately fragmented; the top five suppliers together control roughly 45% share, leaving ample space for regional challengers. Prysmian, Nexans, Corning, Furukawa, and Sumitomo dominate premium data-center and FTTH segments by leveraging global manufacturing footprints and extensive standards compliance. LS Cable and System, Hengtong, and Sterlite rise quickly in government projects where local-content requirements or aggressive pricing decide tenders. Hyperscale tenants are consolidating vendor rosters to minimize SKU counts and enforce uniform quality metrics, yet smaller colocation operators diversify suppliers to hedge lead-time risk caused by copper price volatility.

Product innovation centers on pre-terminated fiber assemblies, high-density 16-fiber MPO cassettes, and Cat 6 shielded patch-cord ranges that withstand 90-watt PoE temperatures. Panduit, Legrand, and Belden embed automated documentation software that ingests certification results and populates digital twins, giving facility managers real-time visibility of physical layer assets. Manufacturers with in-house compound extrusion smoothly adopted the stricter flame-retardancy criteria outlined in UL plenum tests, whereas smaller firms struggle with higher scrap rates. Standards revisions, notably ANSI/TIA-568.0-E and ISO/IEC 11801, lift pass-fail thresholds, effectively raising the bar for newcomers and consolidating share within incumbents that fund continuous R&D.

Regional specialists exploit faster service response times and tailored SKUs, such as typhoon-rated aerial fiber for the Philippines or termite-resistant cables for Northern Australia, extracting 10-30% price premiums. However, chronic shortages of BICSI-certified technicians limit deployment velocity in high-growth territories like Vietnam and Malaysia, giving integrated cabling and services providers an edge. Currency swings and freight bottlenecks favor suppliers with distributed warehousing, a compelling proposition as hyperscalers demand just-in-time delivery to meet tight commissioning schedules. Overall, technology differentiation, standards agility, and service depth will decide long-term winners in the Asia-Pacific structured cabling market.

Asia-Pacific Structured Cabling Industry Leaders

Belden Inc.

CommScope Holding Company Inc.

Corning Incorporated

Prysmian Group SpA

Nexans SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: KT Corporation started construction on its USD 1.02 billion AI data center in Gimcheon, South Korea, featuring liquid-cooled racks and 400G fiber interconnects.

- December 2025: India’s BharatNet completed 692,676 km of optical fiber, linking 214,323 gram panchayats under an INR 220 billion (USD 2.6 billion) allocation.

- November 2025: AWS unveiled a USD 5 billion plan to expand its Bangkok region with new availability zones relying on high-density fiber trunks.

- October 2025: Oracle committed USD 6.5 billion to Thailand for cloud and AI centers deploying 400G optics and liquid-cooling systems.

Asia-Pacific Structured Cabling Market Report Scope

The Asia-Pacific Structured Cabling Market Report is Segmented by Offering (Hardware, Services, Software), Cable Type (Copper, Fiber), Cable Category Standard (Cat 5e, and Cat 6), Application (LAN, Data Center, FTTx/Campus Backbone, Industrial Automation Networks), End-User Industry (IT and Telecom, Cloud and Colocation, BFSI, Healthcare, Government, Manufacturing, Education), and Geography (China, India, Japan, South Korea, ASEAN, Australia, New Zealand). Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Hardware | Cabling (Copper, Fiber) |

| Connectivity (Connectors, Patch-Panels, Jacks, Cords) | |

| Racks, Cabinets and Cable Management | |

| Services | Design and Consulting |

| Installation and Integration | |

| Maintenance and Support | |

| Software |

By Cable Type

| Copper | Copper Cable |

| Copper Connectivity | |

| Fiber | Single-Mode Cable |

| Multi-Mode Cable | |

| Fiber Connectivity |

By Cable Category Standard

| Cat 5e |

| Cat 6 |

By Application

| LAN |

| Data Center |

| FTTx / Campus Backbone |

| Industrial Automation Networks |

By End-User Industry

| IT and Telecom Service Providers |

| Cloud and Colocation Data Centers |

| BFSI and Enterprise Offices |

| Healthcare Facilities |

| Government and Defense |

| Manufacturing and Industrial |

| Education |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific |

| By Offering | Hardware | Cabling (Copper, Fiber) |

| Connectivity (Connectors, Patch-Panels, Jacks, Cords) | ||

| Racks, Cabinets and Cable Management | ||

| Services | Design and Consulting | |

| Installation and Integration | ||

| Maintenance and Support | ||

| Software | ||

| By Cable Type | Copper | Copper Cable |

| Copper Connectivity | ||

| Fiber | Single-Mode Cable | |

| Multi-Mode Cable | ||

| Fiber Connectivity | ||

| By Cable Category Standard | Cat 5e | |

| Cat 6 | ||

| By Application | LAN | |

| Data Center | ||

| FTTx / Campus Backbone | ||

| Industrial Automation Networks | ||

| By End-User Industry | IT and Telecom Service Providers | |

| Cloud and Colocation Data Centers | ||

| BFSI and Enterprise Offices | ||

| Healthcare Facilities | ||

| Government and Defense | ||

| Manufacturing and Industrial | ||

| Education | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How fast is the Asia-Pacific structured cabling market growing through 2031?

It is expected to rise from USD 5.29 billion in 2026 to USD 8.46 billion by 2031, reflecting a 9.85% CAGR.

Which segment adds revenue fastest within the Asia-Pacific structured cabling market?

Services exhibit the highest growth, expanding at a 10.22% CAGR because enterprises retrofit networks for 90-watt PoE and 10GBASE-T.

Why is fiber capturing the largest Asia-Pacific structured cabling market share?

AI data centers and national broadband projects rely on single-mode trunks and 400G optics that demand fiber’s reach and bandwidth.

What drives Cat 6 adoption across new commercial buildings?

Tenants require 10 Gbps throughput and 90-watt PoE support for Wi-Fi 6E access points, LED lighting, and smart-building sensors.

Which geography posts the quickest expansion in structured cabling demand?

India leads with a projected 10.74% CAGR, underpinned by BharatNet village fiber, hyperscale build-outs, and metro backhaul upgrades.

How is the copper supply deficit affecting project budgets?

Spot-price volatility and a forecast 900,000-tonne shortfall for 2026 push contractors to lock long-term contracts or shift to aluminum-clad alternatives.

Page last updated on: